Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

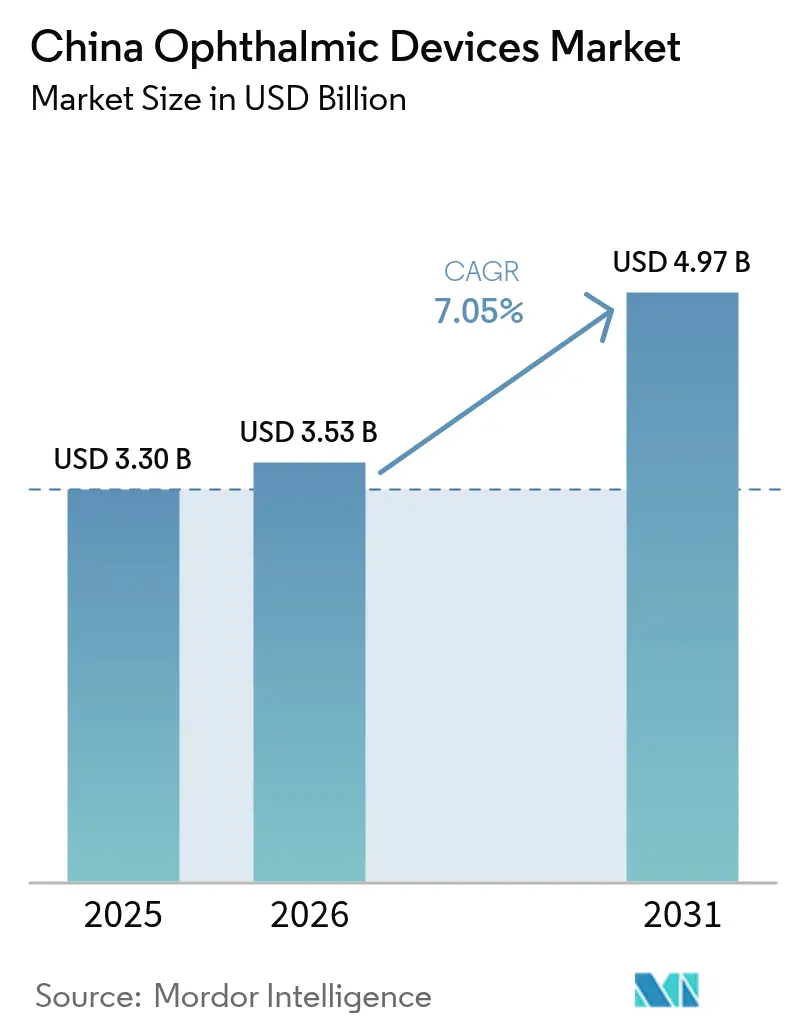

| Base Year Market Size (2025) | USD 3.30 Billion |

| Market Size (2026) | USD 3.53 Billion |

| Market Size (2031) | USD 4.97 Billion |

| Growth Rate (2026 - 2031) | 7.05% CAGR |

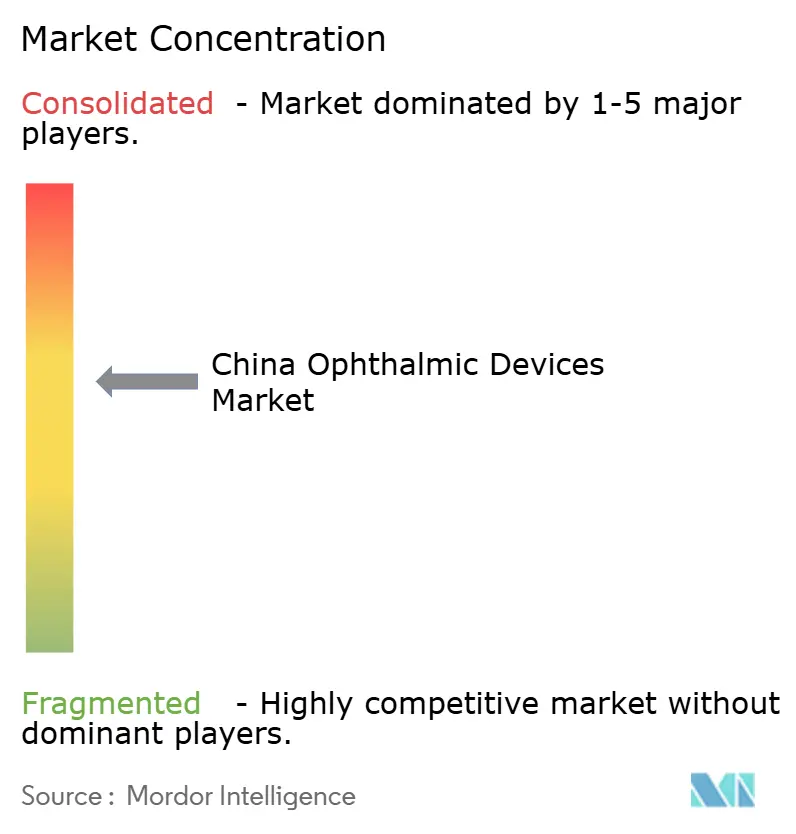

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Ophthalmic Devices Market Analysis by Mordor Intelligence

China ophthalmic devices market size in 2026 is estimated at USD 3.53 billion, growing from 2025 value of USD 3.30 billion with 2031 projections showing USD 4.97 billion, growing at 7.05% CAGR over 2026-2031. Demographic ageing, a steep rise in juvenile myopia and a national cataract-reimbursement program are enlarging procedure volumes, while government-run bulk-buy auctions propel domestically engineered imaging, surgical and vision-care products into mainstream procurement. Hospitals facing tariff-inflated import prices now trial Chinese premium lasers that meet global accuracy thresholds, accelerating import substitution and diversifying supply. In parallel, private eye-care chains are equipping Tier-II and Tier-III cities with turnkey diagnostic suites, widening geographic coverage and reinforcing the China ophthalmic devices market’s momentum through the decade.

Key Report Takeaways

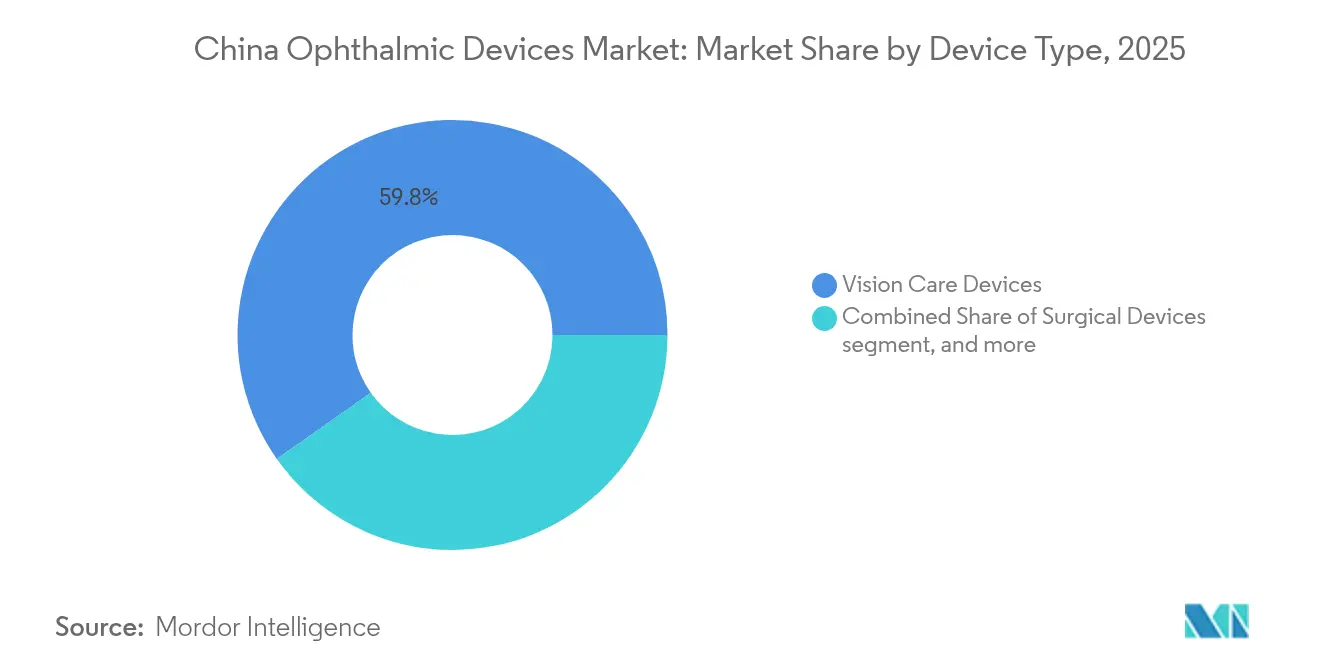

- By device type, vision care held 59.78% of the China ophthalmic devices market share in 2025; diagnostic and monitoring devices are projected to grow at a 9.68% CAGR to 2031.

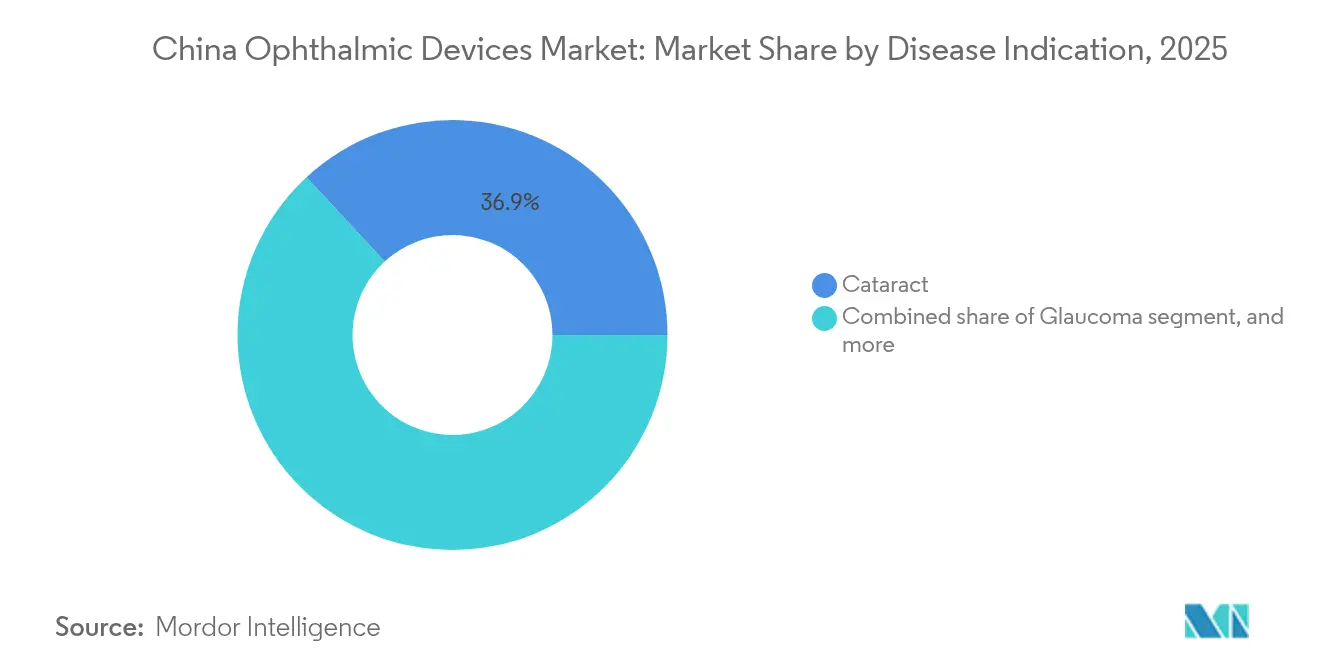

- By disease indication, cataract accounted for a 36.88% share of the China ophthalmic devices market size in 2025, while diabetic retinopathy is set to expand at a 10.56% CAGR through 2031.

- By end-user, hospitals dominated with 43.62% revenue in 2025, whereas ambulatory surgery centers are expected to post a 7.21% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Ophthalmic Devices Market Trends and Insights

Driver Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid urban myopia surge among Chinese youth | +1.4% | Tier-I & Tier-II cities | Medium term (2-4 years) |

| Government-led cataract surgery reimbursement expansion | +1.2% | Nationwide | Long term (≥ 4 years) |

| Growing private eye-care chain investments in Tier-II & III cities | +0.9% | Tier-II & Tier-III cities | Medium term (2-4 years) |

| Aging-related cataract & glaucoma incidence spike in coastal provinces | +0.8% | Coastal provinces | Long term (≥ 4 years) |

| AI-enabled screening kiosks adoption by community hospitals | +0.7% | County-level & community hospitals | Short term (≤ 2 years) |

| NMPA fast-track approvals for innovative ophthalmic implants | +0.5% | Nationwide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Urban Myopia Surge Transforms Device Demand

Escalating juvenile myopia has reoriented family spending from basic spectacles toward premium screening and treatment, lifting high-margin segments inside the China Ophthalmic Devices market. National-Medical-Products-Administration-cleared phakic intraocular lenses now extend surgical correction to teenagers, evidencing a leap from adult-only procedures[1]National Medical Products Administration, “Device Registration Approval List,” nmpa.gov.cn. Community clinics deploy AI fundus cameras with >95% diagnostic accuracy, accelerating early detection and feeding referrals into surgical hubs. Parents increasingly choose daily disposable lenses promising axial-elongation control, boosting retailer revenue and sustaining demand for axial-length biometers that track therapy outcomes. Shorter innovation cycles in diagnostic software drive system upgrades ahead of hardware depreciation, reinforcing repeat-purchase behaviour.

Government-Led Cataract Surgery Reimbursement Expansion

National reimbursement doubled cataract surgeries in five years, elevating use of viscoelastics, phaco handpieces and intraocular lenses. Budget certainty prompts hospitals to replace aging consoles with femtosecond platforms that lower complication rates, confident that higher capital outlays are offset by guaranteed case volumes[2]National Health Security Administration, “Annual Reimbursement Catalogue Update,” nhsa.gov.cn. Bulk-buy tenders favour domestic consumables meeting price ceilings, anchoring a long-run revenue engine for the China Ophthalmic Devices market. Suppliers bundling capsulotomy add-ons and single-use packs gain advantage by compressing turnover times and operating-room staffing.

Private Eye-Care Chain Investments in Tier-II & III Cities

Chain operators employ a “1 + 8 + N” hub-and-spoke expansion, whereby each flagship tertiary hospital anchors multiple satellite clinics, each requiring autorefractors, slit-lamps and fundus suites. Foreign-funded hospitals entering pilot zones raise base diagnostic specifications, forcing vendors to include maintenance, training and inventory pooling in bids. Nationwide contracts reward suppliers with dense service footprints, enhancing the China Ophthalmic Devices market’s scale outside metropolitan cores.

Ageing-Related Cataract & Glaucoma Incidence Spike

Coastal provinces show the fastest growth in populations aged ≥55, lifting cataract and glaucoma caseloads. Hospitals compressed inpatient stays via day-surgery pathways, selecting compact phaco consoles and portable microscopes that fit small theatres. Glaucoma specialists adopt minimally invasive canaloplasty tools that shorten case time, supporting higher daily throughput. Community centers prioritise optic-nerve OCT in suburban screening camps, spreading advanced imaging across lower-tier facilities.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of fellowship-trained ophthalmic surgeons in inland China | –0.7% | Inland provinces | Short term (≤ 2 years) |

| High import tariffs on premium surgical lasers | –0.5% | Nationwide | Medium term (2-4 years) |

| Price-sensitive public hospital procurement auctions | –0.6% | Nationwide | Short term (≤ 2 years) |

| Counterfeit diagnostic hand-helds in informal distribution channels | –0.4% | Rural areas & informal marketplaces | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shortage of Fellowship-Trained Ophthalmic Surgeons

Surgeon-to-population ratios lag national targets in inland counties, capping surgical throughput despite equipment availability. Provincial grants subsidise AI-triage kiosks that refer only confirmed cases to city hospitals, easing workload but constraining adoption of complex vitreoretinal platforms. Training partnerships mandate donation of simulation systems, boosting capital equipment sales in teaching centres yet not fully eliminating the manpower bottleneck that tempers China Ophthalmic Devices market growth.

High Import Tariffs on Premium Surgical Lasers

Successive tariff rounds inflate landed costs on imported femtosecond and excimer lasers, narrowing their cost-benefit margin in public tenders. Domestic OEMs unveil 1 000 Hz ablation systems meeting global benchmarks, capturing pilots and extending supply contracts once clinical outcomes hold steady[3]Source: Ministry of Commerce, “Tariff Adjustment Notice 2024,” mofcom.gov.cn. Some multinationals re-assemble units in bonded zones to mitigate duties, but transition delays widen the substitution window for local competitors.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Domestic Diagnostics Disrupt Import Dominance

Diagnostic & Monitoring devices represented 23.62% of the 2025 China Ophthalmic Devices market size and are expected to compound at 9.68%CAGR to 2031. Local suppliers now install more than half of OCT workstations in county hospitals, buoyed by AI modules that allow technicians to deliver referral-ready reports without specialist oversight. Faster software release cycles persuade facilities to refresh equipment ahead of depreciation schedules, lifting replacement revenue. Vision Care remains the largest slice at 59.78%, driven by daily disposable silicone-hydrogel lenses that benefit from e-commerce penetration. Surgical devices contribute 16.60% and gain from bulk tender guarantees that underpin cataract lens offtake, while ambulatory centres purchase phaco consoles with integrated capsulotomy to minimize theatre time.

By Disease Indication: Myopia Management Drives Innovation

Myopia solutions constitute 32.58% of the 2025 China Ophthalmic Devices market size and carry a 8.74%CAGR forecast through 2031, propelled by ortho-k lenses, atropine therapy and axial-length tracking tools bundled into integrated practice platforms. Cataract remains dominant at 36.88% and grows at 6.85%CAGR on the back of reimbursement and extended life expectancy. Diabetic-retinopathy devices, though smaller, post an 10.56%CAGR as hand-held fundus cameras linked to cloud AI enable rural screening and trigger follow-up laser interventions.

By End-User: Ambulatory Centres Reshape Care Delivery

Ambulatory Surgery Centres (ASCs) accounted for 28.74% China ophthalmic devices market share in 2025 and are forecast to deliver an 7.21%CAGR through 2031 as regulators mandate that day-surgery constitute 60% of elective ophthalmic procedures. Rising throughput pushes operators to favour compact phaco consoles, refractive-laser suites and vitrectomy units that maintain sterility in small, high-turnover theatres. Suppliers strengthen bids by offering leasing, pay-per-use and managed-service contracts that align equipment costs with procedure revenue, a model that lowers entry barriers for independent chains eager to expand into Tier-III cities.

Hospitals retained 43.62% of China ophthalmic devices market size in 2025, largely because complex vitreoretinal and corneal graft cases still centralise around tertiary centres able to invest in intraoperative OCT, 3-D heads-up microscopes and hybrid laminar-flow theatres. Management teams expand simulation labs to accelerate resident training and shorten credentialing timelines, thereby boosting demand for trainer-configured microscopes and practice phaco units. Specialty ophthalmic clinics hold the remaining share and scale through franchise templates that pre-specify autorefractors, slit-lamps and visual-field analysers, giving manufacturers predictable refresh cycles tied to centrally negotiated replacement windows.

Geography Analysis

Eastern coastal provinces contributed more than half of the China ophthalmic devices market size in 2025 and continue to set the technology agenda with early uptake of femtosecond cataract platforms and multifocal intraocular lenses, reflecting patient readiness to self-fund premium outcomes. Urban hospitals integrate AI screening into electronic medical record ecosystems and link imaging archives to provincial cloud platforms, accelerating replacement of legacy fundus cameras with smart systems that meet cybersecurity standards. In parallel, 5 G roll-outs enable real-time surgical mentoring, reinforcing the referral magnetism of coastal centres and sustaining incremental equipment demand.

Tier-II and Tier-III cities exhibit the fastest 8.73%CAGR through 2031, propelled by municipal subsidies that underwrite private-chain clinic construction. Local authorities exchange rent concessions for commitments to train community optometrists, sparking cluster orders for turnkey diagnostic packages of autorefractors, slit-lamps, tonometers and portable OCT workstations. Equipment makers win contracts by bundling cloud telemetry, remote troubleshooting and shared-inventory depots that minimise downtime in geographies with fragmented service coverage. These measures close the technology gap between metropolitan and mid-sized cities, deepening the China Ophthalmic Devices market.

Rural counties still lag specialist coverage but progress through mobile outreach programs that deploy vans equipped with dust-proof, battery-backed fundus cameras, slit-lamps and autorefraction kiosks. Provincial tele-medicine grants link these units to tertiary reading centres, creating a pipeline of surgically eligible patients routed toward county hubs. Over time, rising referral volumes justify investments in compact phaco consoles, single-use surgical packs and pre-loaded intraocular lenses optimized for resource-constrained settings. The bottom-up expansion narrows urban–rural care gaps and seeds long-run growth for the China Ophthalmic Devices market.

Competitive Landscape

Competitive balance in the China ophthalmic devices market has shifted toward domestic innovators after 121 high-end devices received National Medical Products Administration clearance over the last 24 months, ensuring home-grown options in segments once dominated by imports. Policy guarantees that at least one domestic brand receives a tender slot in every bulk-procurement round deliver baseline volumes that de-risk R&D spending and motivate venture investors to keep funding iterative upgrades.

Global incumbents retain strongholds in premium refractive lasers and advanced vitreoretinal platforms, yet tariff escalations continue to compress imported average selling prices. Carl Zeiss Meditec answered by acquiring Dutch Ophthalmic Research Center to bolster its surgical-device mix and by localising cloud-based software upgrades that add intraoperative imaging functions without hardware swaps. Alcon partnered with Shanghai-based service providers to reduce spare-part lead times, a move aimed at protecting hospital renewals even as bulk-buy committees scrutinise total lifecycle cost.

Emerging Chinese companies specialise in unmet niches such as phakic intraocular lenses for high myopia and AI triage platforms for diabetic retinopathy. Eyebright Medical’s Loong Crystal PR lens received Class III approval and is now marketed across major refractive centres. Nova Eye Medical’s iTrack Advance canaloplasty system posted USD 360,000 China sales within one quarter and expanded its Shanghai training hub to support surgeon onboarding. Domestic OEMs also unveil 1,000 Hz femtosecond prototypes, leveraging local supply chains to accelerate iteration cycles and erode the remaining import premium in laser refractive surgery.

China Ophthalmic Devices Industry Leaders

Alcon Inc.

Johnson & Johnson Vision Care Inc.

Carl Zeiss Meditec AG

Bausch + Lomb Corp.

Topcon Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Pharmcube reported that 121 high-end ophthalmic devices have obtained NMPA approval, signalling that domestic OCT and biometry systems now outsell imports in public hospitals.

- April 2025: The Vision Council met White House officials to discuss tariff-driven cost increases on Class I medical devices imported from China, prompting exporters to diversify destination markets.

- March 2025: A new 20% duty on Chinese optical materials raised effective tariffs on some eyeglass cases to 65%, encouraging manufacturers to redirect capacity toward Southeast Asia and Latin America.

- February 2025: China’s State Council issued the 2025 Opinions to streamline review timelines for innovative medical devices, shortening pathways for AI-enabled diagnostics.

- January 2025: Eyebright Medical secured NMPA Class III certification for its Loong Crystal PR phakic lens, clearing the path to nationwide launch.

China Ophthalmic Devices Market Report Scope

As per the scope of the report, ophthalmology is a branch of medical sciences that deals with the structure, function, and various diseases related to the eye. Ophthalmic devices are medical equipment designed for diagnosis, surgery, and vision correction purposes. Devices (Glaucoma Devices, Intraocular Lenses, Lasers, and Other Surgical Devices), Diagnostic and Monitoring Devices (Autorefractors and Keratometers, Ophthalmic Ultrasound Imaging Systems, Ophthalmoscopes, Optical Coherence Tomography Scanners, and Other Diagnostic and Monitoring Devices) make up the Chinese Ophthalmic Devices Market. The report offers the value (in USD million) for the above segments.

By Device Type

| Diagnostic & Monitoring Devices | OCT Scanners |

| Fundus & Retinal Cameras | |

| Autorefractors & Keratometers | |

| Corneal Topography Systems | |

| Ultrasound Imaging Systems | |

| Perimeters & Tonometers | |

| Other Diagnostic & Monitoring Devices | |

| Surgical Devices | Cataract Surgical Devices |

| Vitreoretinal Surgical Devices | |

| Refreactive Surgical Devices | |

| Glaucoma Surgical Devices | |

| Other Surgical Devices | |

| Vision Care Devices | Spectacles Frames & Lenses |

| Contact Lenses |

By Disease Indication

| Cataract |

| Glaucoma |

| Diabetic Retinopathy |

| Other Disease Indications |

By End-user

| Hospitals |

| Specialty Ophthalmic Clinics |

| Ambulatory Surgery Centers (ASCs) |

| Other End-users |

| By Device Type | Diagnostic & Monitoring Devices | OCT Scanners |

| Fundus & Retinal Cameras | ||

| Autorefractors & Keratometers | ||

| Corneal Topography Systems | ||

| Ultrasound Imaging Systems | ||

| Perimeters & Tonometers | ||

| Other Diagnostic & Monitoring Devices | ||

| Surgical Devices | Cataract Surgical Devices | |

| Vitreoretinal Surgical Devices | ||

| Refreactive Surgical Devices | ||

| Glaucoma Surgical Devices | ||

| Other Surgical Devices | ||

| Vision Care Devices | Spectacles Frames & Lenses | |

| Contact Lenses | ||

| By Disease Indication | Cataract | |

| Glaucoma | ||

| Diabetic Retinopathy | ||

| Other Disease Indications | ||

| By End-user | Hospitals | |

| Specialty Ophthalmic Clinics | ||

| Ambulatory Surgery Centers (ASCs) | ||

| Other End-users | ||

Key Questions Answered in the Report

What is the current size of the China ophthalmic devices market?

The China ophthalmic devices market size is USD 3.53 billion in 2026 and is forecast to reach USD 4.97 billion by 2031.

Which device category leads revenue in China’s ophthalmic sector?

Vision-care products hold the largest 59.78% share of 2025 revenue, reflecting strong demand for disposable contact lenses and lens-care solutions.

Which segment is growing the fastest through 2031?

Diagnostic and monitoring devices are projected to register the highest 9.68%CAGR by 2031, propelled by AI-enabled imaging upgrades.

How are ambulatory surgery centres influencing equipment demand?

Policy shifts that mandate 60% day-surgery rates drive ASCs to adopt compact phaco consoles and pay-per-use financing, supporting a 7.21%CAGR for this end-user group.

What is the chief regulatory trend shaping market competition?

Bulk-procurement rules that reserve at least one tender slot for a domestic brand are increasing local manufacturers’ market access and hastening import substitution.

Page last updated on: