Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

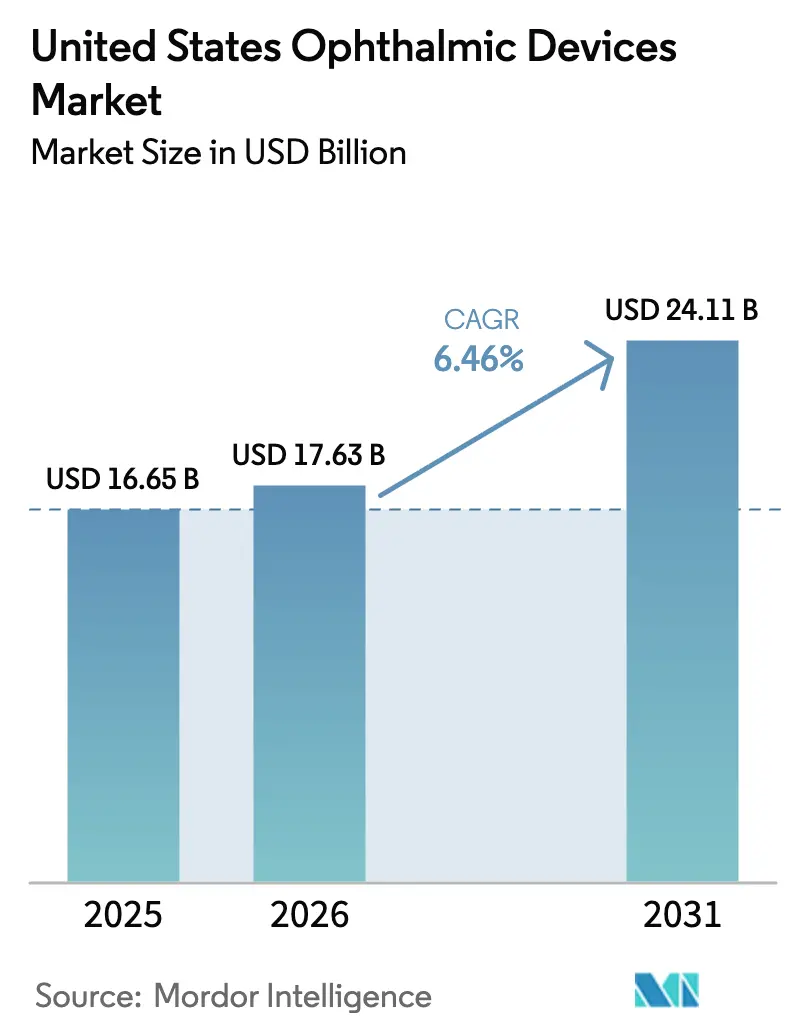

| Base Year Market Size (2025) | USD 16.65 Billion |

| Market Size (2026) | USD 17.63 Billion |

| Market Size (2031) | USD 24.11 Billion |

| Growth Rate (2026 - 2031) | 6.46% CAGR |

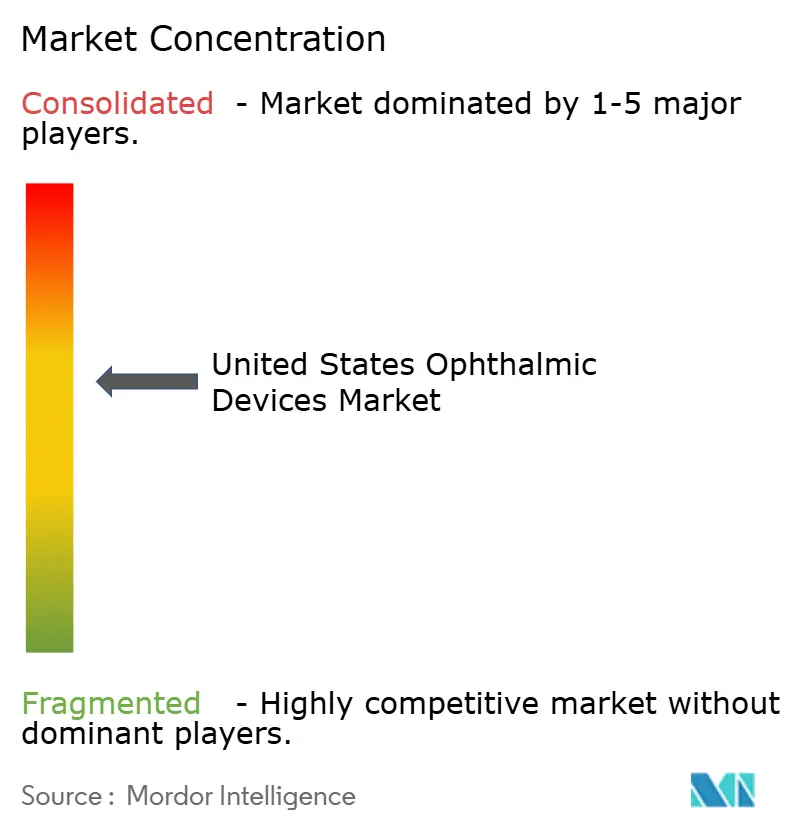

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Ophthalmic Devices Market Analysis by Mordor Intelligence

The United States Ophthalmic Devices Market size is projected to be USD 16.65 billion in 2025, USD 17.63 billion in 2026, and reach USD 24.11 billion by 2031, growing at a CAGR of 6.46% from 2026 to 2031.

A sharp rise in cataract volumes among seniors, an expanding diabetic and glaucoma population, and the rapid adoption of autonomous artificial-intelligence screening tools are reinforcing sustained demand. Device makers are pivoting toward ambulatory surgery centers (ASCs), which now handle most routine cataract and minimally invasive glaucoma surgery (MIGS) cases, and are unbundling service contracts to appeal to cost-conscious buyers. Premium intraocular lenses (IOLs) priced beyond USD 2,500 per eye continue to gain acceptance as patients seek spectacle independence. At the same time, daily-disposable contact lenses are displacing monthly formats, helping high-volume manufacturers leverage automated production. Regulatory momentum has accelerated for AI-driven diagnostics, while tariff pressure on steel and titanium surgical instruments is nudging vendors to diversify supply chains and safeguard margins.

Key Report Takeaways

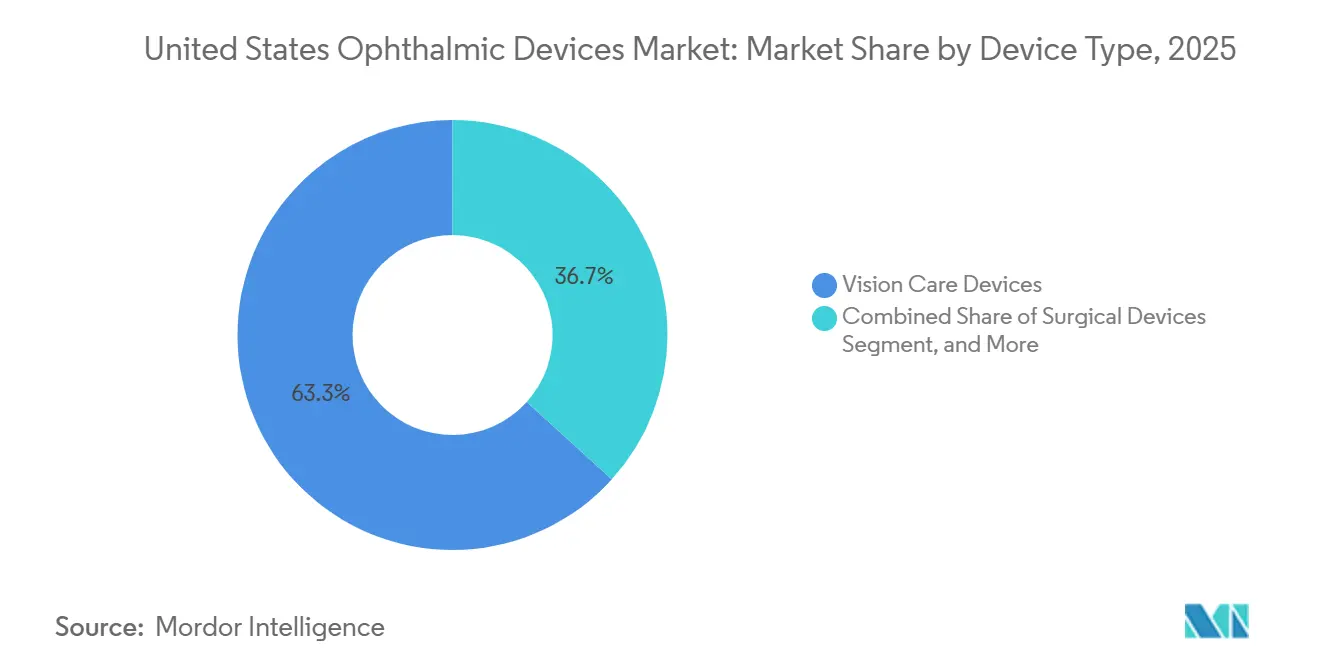

- By device type, vision care devices led with 63.27% revenue share in 2025; diagnostic and monitoring platforms are projected to post the fastest 7.32% CAGR through 2031.

- By disease indication, cataract procedures accounted for 39.33% share of the United States ophthalmic devices market size in 2025, whereas diabetic retinopathy diagnostics are advancing at a 6.69% CAGR through 2031.

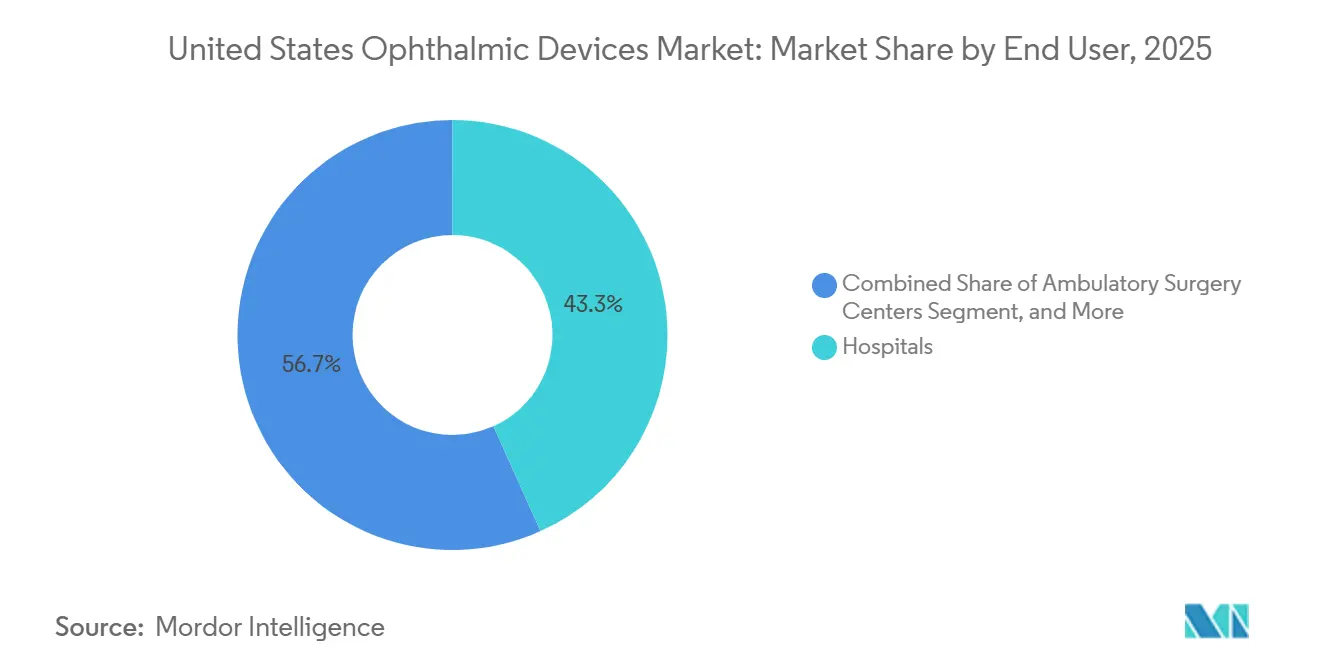

- By end-user, hospitals held 43.28% of the United States ophthalmic devices market share in 2025, while ASCs are expanding at a robust 9.01% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Ophthalmic Devices Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging Population & Cataract Prevalence Surge | +1.2% | National, with concentration in Sun Belt states (Florida, Arizona, Texas) | Long term (≥ 4 years) |

| Rising Diabetes & Glaucoma Comorbidity Burden | +0.9% | National, with higher prevalence in Southern and Appalachian regions | Medium term (2-4 years) |

| Shift of Cataract & MIGS Procedures to ASCs | +1.5% | National, led by metropolitan areas with ASC density | Medium term (2-4 years) |

| Surge in Premium IOL & Daily-Disposable Contact Lens Uptake | +0.8% | National, skewed toward urban and suburban affluent demographics | Short term (≤ 2 years) |

| AI-Integrated OCT & Fundus Imaging Adoption | +1.1% | National, with early adoption in integrated health systems and retail clinics | Medium term (2-4 years) |

| Sustainability Push for Single-Use Surgical Packs | +0.3% | National, driven by hospital sustainability mandates and GPO procurement policies | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Aging Population & Cataract Prevalence Surge

The U.S. Census Bureau expects the 65-plus cohort to reach 73 million by 2030, up from 58 million in 2022.[1]National Eye Institute, “Diabetic Retinopathy Statistics,” nei.nih.gov Cataract formation accelerates after age 60, and the National Eye Institute projects 50 million Americans could have cataracts by 2050. Medicare covers standard monofocal cataract extraction, ensuring broad access, while premium IOL penetration rose to 35% of procedures in 2024, according to JAMA Ophthalmology. Sun Belt states attract retiring patients and record-high volumes, prompting vendors to open regional service hubs to minimize downtime.

Rising Diabetes & Glaucoma Comorbidity Burden

The CDC counted 38.4 million Americans with diabetes in 2024, and roughly a quarter will develop diabetic retinopathy within 15 years of diagnosis.[2]American Academy of Ophthalmology, “Capital Expenditure Guide for Diagnostic Suites,” aao.org Glaucoma Research Foundation data indicate 3.3 million Americans aged 40 and older have glaucoma, expected to reach 4.3 million by 2030. Diabetic patients face a 40% higher risk of open-angle glaucoma, prompting demand for integrated platforms that identify both conditions in one visit. Autonomous AI systems such as IDx-DR extend screening into primary-care offices, easing rural capacity gaps.

Shift of Cataract & MIGS Procedures to ASCs

Medicare’s 2025 Physician Fee Schedule raised ASC payments for cataract extraction by 2.8% versus a 1.9% hospital outpatient increase. Lower overhead spurs surgeons to migrate cases to ASCs, where overhead costs are 30-40% lower than in hospitals. ASCs now complete 68% of U.S. cataract surgeries, up from 62% in 2020. Bundling MIGS with cataract extraction elevates procedural efficiency, yet intense ASC price negotiations are compressing phacoemulsification and handpiece margins.

Surge in Premium IOL & Daily-Disposable Contact Lens Uptake

Toric, multifocal, and extended-depth-of-focus IOLs continue to outpace monofocal lens growth as patients value spectacle freedom. Alcon’s PanOptix Toric and Johnson & Johnson Vision’s TECNIS Synergy series exemplify the technology leap. A 2024 American Society of Cataract and Refractive Surgery survey found that 42% of patients opted for premium lenses when benefits were clearly explained.[3] Daily-disposable contact lenses, led by CooperVision’s MyDay brand, cater to infection-conscious presbyopes and fuel double-digit revenue expansion.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Cost of Femtosecond & OCT Platforms | -0.7% | National, with greater impact on independent practices and rural ASCs | Medium term (2-4 years) |

| Reimbursement Uncertainty for Emerging MIGS & AI Diagnostics | -0.5% | National, with regional variation in private payer coverage policies | Short term (≤ 2 years) |

| Growing ASC Price Pressure on Instrument Vendors | -0.4% | National, concentrated in high-ASC-density metropolitan markets | Medium term (2-4 years) |

| Tariff-Driven Raw-Material Inflation for Steel/Titanium Tools | -0.3% | National, affecting all device categories with metal components | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capital Cost of Femtosecond & OCT Platforms

Acquiring a femtosecond laser requires USD 500,000-750,000, with annual service fees of USD 50,000-100,000. Independent practices rarely reach the 300-case threshold needed to justify these expenses. Advanced multimodal OCT units cost more than USD 150,000, prompting rural clinics to defer upgrades. Leasing and click-fee programs shift risk to vendors, tightening their profit margins.

Reimbursement Uncertainty for Emerging MIGS & AI Diagnostics

Glaukos’ iDose TR lacks a dedicated CPT code, forcing providers to bill using unlisted codes and resulting in payment delays. While Medicare covers CPT 92229 for autonomous diabetic retinopathy screening, regional reimbursement variations often fail to offset software licensing costs. Mixed private-payer determinations further stall adoption.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Vision Care Dominates, Diagnostics Accelerate

Vision care devices accounted for 63.27% of revenue in 2025, underpinned by the vast base of spectacle and contact lens users. Diagnostic and monitoring equipment is on track for a 7.32% CAGR through 2031 as AI platforms migrate into primary care settings. Spectacle lenses, especially EssilorLuxottica’s Stellest for myopia control, continue to drive high unit demand. Daily-disposable contact lenses continue to outpace monthly formats, driven by convenience and perceived hygiene. Surgical devices remain vital for cataract, vitreoretinal, refractive, and glaucoma care. Premium IOLs bundled with advanced phacoemulsification consoles deepen vendor-ASC relationships, while MIGS and sustained-release glaucoma implants open new therapy classes.

A broad installed base of phaco consoles means replacement cycles create stable revenue, but the commoditization of consumables tightens margins. Diagnostic players are differentiating through cloud connectivity and AI-based analytics. The CIRRUS 6000 OCT illustrates this shift, automatically segmenting retinal layers to flag early change and reducing technician variability. Fundus cameras coupled with EyeArt AI extend reliable screening to retail and federally qualified clinics. Collectively, these trends reinforce growth in the United States ophthalmic devices market even as vision-care dominance persists.

By Disease Indication: Cataract Still Leads but Diabetic-Retinopathy Solutions Outpace

Cataract remained the largest indication, generating 39.33% of 2025 revenue. Medicare reimbursement secures procedure volumes, and rising IOL adoption drives average selling prices higher. Diabetic retinopathy diagnostics, however, are the fastest-growing segment at a 6.69% CAGR to 2031, thanks to AI tools that allow non-specialists to screen in primary-care settings. Glaucoma solutions benefit from the aging demographics and the overlap with diabetes, reinforcing demand for perimeters, tonometers, and OCT-based progression monitoring.

Other conditions, including age-related macular degeneration and dry eye, add incremental growth. Home OCT technology shifts wet-AMD monitoring from clinic to home, reducing patient travel and improving adherence. Thermal pulsation devices for dry-eye treatment create cash-pay streams for specialty clinics even though upfront procedure costs exceed USD 1,000. Overall, diversified disease needs ensure resilient expansion of the United States ophthalmic devices market.

By End User: Hospitals Retain Influence While ASCs Speed Ahead

Hospitals accounted for 43.28% of 2025 sales but are ceding routine cases to ASCs, which are projected to grow at a strong 9.01% CAGR through 2031. Narrowing Medicare payment gaps makes ASC economics attractive, and lower overhead enables competitive private-payer contracts. High-volume metro markets such as Dallas, Phoenix, and Orlando illustrate this shift. Specialty ophthalmic clinics focus on premium services like LASIK and advanced IOL implantation and often rely on cash-pay models. Retail chains and federally qualified health centers leverage autonomous AI cameras to embed diabetic retinopathy screening into routine exams, widening access for underserved populations.

Geography Analysis

Sun Belt states drive cataract growth as retirees flock to warmer climates. Florida alone accounts for roughly 12% of national cataract procedures, and high ASC density in Miami, Tampa, and Orlando enables competitive bidding on capital equipment. Texas mirrors this pattern across Dallas-Fort Worth, Houston, and Austin. California’s large diabetic cohort creates sustained demand for diagnostic imaging, particularly in federally qualified health centers serving low-income patients. The prevalence of diabetic retinopathy in these regions supports the expansion of AI-enabled fundus-camera fleets.

The Midwest and Appalachia face limited ophthalmologist availability, prompting primary care facilities to install AI fundus camera systems such as IDx-DR and EyeArt AI. Veterans Health Administration facilities in Montana, Wyoming, and the Dakotas use teleophthalmology programs that pair home OCT devices with centralized reading centers, reducing travel burdens for elderly veterans.

Urban hubs, including New York, Chicago, and Boston, are home to specialty refractive and premium-IOL centers that serve cash-pay segments. These clinics invest in high-specification femtosecond lasers and digital microscopes to differentiate patient experience. Tariff-driven supply-chain adjustments are influencing procurement across all regions, with distributors securing alternative sources in Mexico and Vietnam to maintain instrument availability and cost stability.

Competitive Landscape

Market leadership remains moderately concentrated. Alcon embeds premium PanOptix Toric and Vivity IOLs within its Centurion ecosystem, locking ASCs in with service bundles. Bausch + Lomb targets cost-sensitive buyers with enVista Toric IOLs and the Stellaris Elite phaco platform. Carl Zeiss Meditec leads premium diagnostics through CIRRUS 6000 OCT and IOLMaster 700 biometry, both featuring AI analytics that reduce reliance on expert technicians.

Glaukos pioneers hybrid device-drug models such as the iDose TR implant that delivers sustained travoprost and potentially curtails daily drop dependence. Disruptors like Notal Vision and Eyenuk are expanding the home monitoring and autonomous screening niches. Vendors race to add cloud connectivity, predictive analytics, and remote interpretation capabilities to differentiate their offerings. Section 510(k) clearances remain the norm, yet breakthrough designations for innovations such as Home OCT accelerate approval cycles. Consolidated service networks become a competitive lever as high-volume ASCs demand near-zero equipment downtime.

United States Ophthalmic Devices Industry Leaders

Alcon Inc.

Bausch + Lomb Corp.

Ziemer Ophthalmic Systems AG

Carl Zeiss Meditec AG

Johnson & Johnson Vision Care Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: New World Medical secured FDA 510(k) clearance for the VIA360 surgical system.

- January 2025: Carl Zeiss Meditec received FDA approval for the MEL 90 excimer laser, completing its corneal-refractive workflow.

- October 2024: ZEISS introduced VisioGen patient-communication software and the MICOR 700 handheld lens-removal device.

- September 2024: Johnson & Johnson launched TECNIS Odyssey IOL across the United States.

United States Ophthalmic Devices Market Report Scope

As per the scope of the report, ophthalmic devices are medical equipment designed for diagnosis, surgical, and vision correction purposes.

The United States Ophthalmic Devices Market is Segmented by Devices (Surgical Devices (Glaucoma Drainage Devices, Glaucoma Stents and Implants, Intraocular Lenses, Lasers, and Other Surgical Devices), Diagnostic and Monitoring Devices (Autorefractors and Keratometers, Corneal Topography Systems, Ophthalmic Ultrasound Imaging Systems, Ophthalmoscopes, Optical Coherence Tomography Scanners, Other Diagnostic, and Monitoring Devices) and Vision Correction Devices (Spectacles, Contact Lenses)). The report offers the value (in USD million) for the above segments.

By Device Type

| Diagnostic & Monitoring Devices | OCT Scanners |

| Fundus & Retinal Cameras | |

| Autorefractors & Keratometers | |

| Corneal Topography Systems | |

| Ultrasound Imaging Systems | |

| Perimeters & Tonometers | |

| Other Diagnostic & Monitoring Devices | |

| Surgical Devices | Cataract Surgical Devices |

| Vitreoretinal Surgical Devices | |

| Refreactive Surgical Devices | |

| Glaucoma Surgical Devices | |

| Other Surgical Devices | |

| Vision Care Devices | Spectacles Frames & Lenses |

| Contact Lenses |

By Disease Indication

| Cataract |

| Glaucoma |

| Diabetic Retinopathy |

| Other Disease Indications |

By End-user

| Hospitals |

| Specialty Ophthalmic Clinics |

| Ambulatory Surgery Centers (ASCs) |

| Other End-users |

| By Device Type | Diagnostic & Monitoring Devices | OCT Scanners |

| Fundus & Retinal Cameras | ||

| Autorefractors & Keratometers | ||

| Corneal Topography Systems | ||

| Ultrasound Imaging Systems | ||

| Perimeters & Tonometers | ||

| Other Diagnostic & Monitoring Devices | ||

| Surgical Devices | Cataract Surgical Devices | |

| Vitreoretinal Surgical Devices | ||

| Refreactive Surgical Devices | ||

| Glaucoma Surgical Devices | ||

| Other Surgical Devices | ||

| Vision Care Devices | Spectacles Frames & Lenses | |

| Contact Lenses | ||

| By Disease Indication | Cataract | |

| Glaucoma | ||

| Diabetic Retinopathy | ||

| Other Disease Indications | ||

| By End-user | Hospitals | |

| Specialty Ophthalmic Clinics | ||

| Ambulatory Surgery Centers (ASCs) | ||

| Other End-users | ||

Key Questions Answered in the Report

What is the current value of the United States ophthalmic devices market?

The United States ophthalmic devices market size stands at USD 16.65 billion in 2025 and is projected to reach USD 22.7 billion by 2030.

Which device category holds the largest share of revenue?

Surgical systems lead with 42.11% of United States ophthalmic devices market share in 2024, driven by cataract and glaucoma procedures.

How fast are ambulatory surgical centers expanding their device purchases?

Ambulatory surgical centers show a 5.23% CAGR through 2030 as outpatient models gain reimbursement support.

Which emerging technology is reshaping diagnostics?

AI-enhanced OCT and fundus-imaging platforms that predict visual acuity and automate referral decisions are revolutionizing clinic workflows.

How is the regulatory environment affecting laser-device innovation?

Extended FDA approval timelines add cost and slow product refresh, slightly tempering growth in refractive-laser sales.

Page last updated on: