Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 2.53 Billion |

| Market Size (2026) | USD 2.71 Billion |

| Market Size (2030) | USD 3.95 Billion |

| Growth Rate (2026 - 2031) | 7.81% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

France Ophthalmic Devices Market Analysis by Mordor Intelligence

The France Ophthalmic Devices Market size is projected to expand from USD 2.53 billion in 2025 and USD 2.71 billion in 2026 to USD 3.95 billion by 2030, registering a CAGR of 7.81% between 2026 to 2030.

A swelling population aged 65 years and above, which will account for 26% of citizens by 2030, is pushing cataract procedures beyond 850,000 per year, while premium intraocular lenses (IOLs) priced three to five times those of monofocal options are raising average selling prices. Government policy also fuels demand: the Health Innovation 2030 program earmarked EUR 670 million (USD 730 million) for digital health, of which EUR 9.8 million (USD 10.7 million) is allocated to medical imaging, accelerating the adoption of optical coherence tomography (OCT) and ultrawidefield retinal cameras. At the same time, ambulatory surgical centers (ASCs) capture routine cataract and glaucoma cases through reimbursement parity, enabling a shift to fast-turnover day surgery that compresses capital budgets and directs purchasing toward compact phacoemulsification and MIGS implants. Vendor strategy is evolving accordingly: EssilorLuxottica’s recent roll-up of Heidelberg Engineering and Cellview Imaging positions the group to bundle diagnostics with its 2,000-plus retail outlets, while Alcon leverages its installed base of Centurion, LenSx, and ORA systems to lock in higher-margin implantables revenue.

Key Report Takeaways

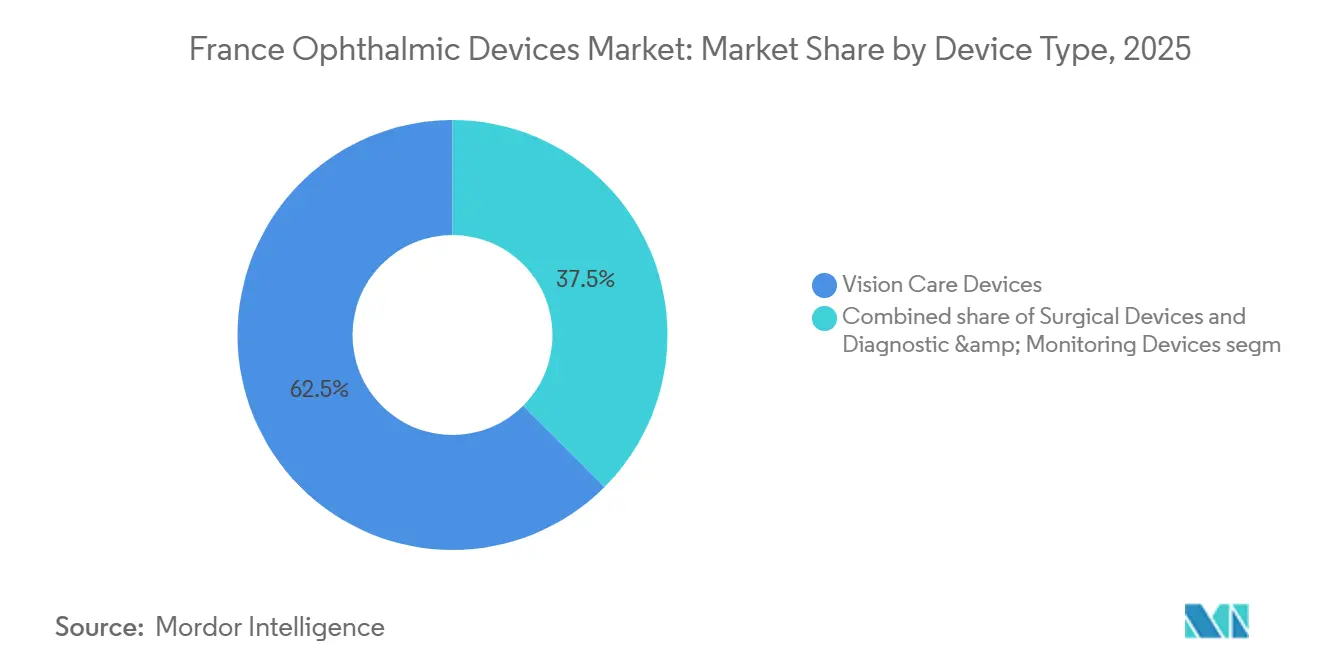

- By device type, vision care devices led with 62.49% revenue share in 2025, whereas diagnostic & monitoring devices are projected to expand at an 8.17% CAGR through 2031.

- By disease indication, cataract procedures captured 38.85% of the France ophthalmic devices market share in 2025, while diabetic retinopathy solutions are forecast to grow at a 9.63% CAGR to 2031.

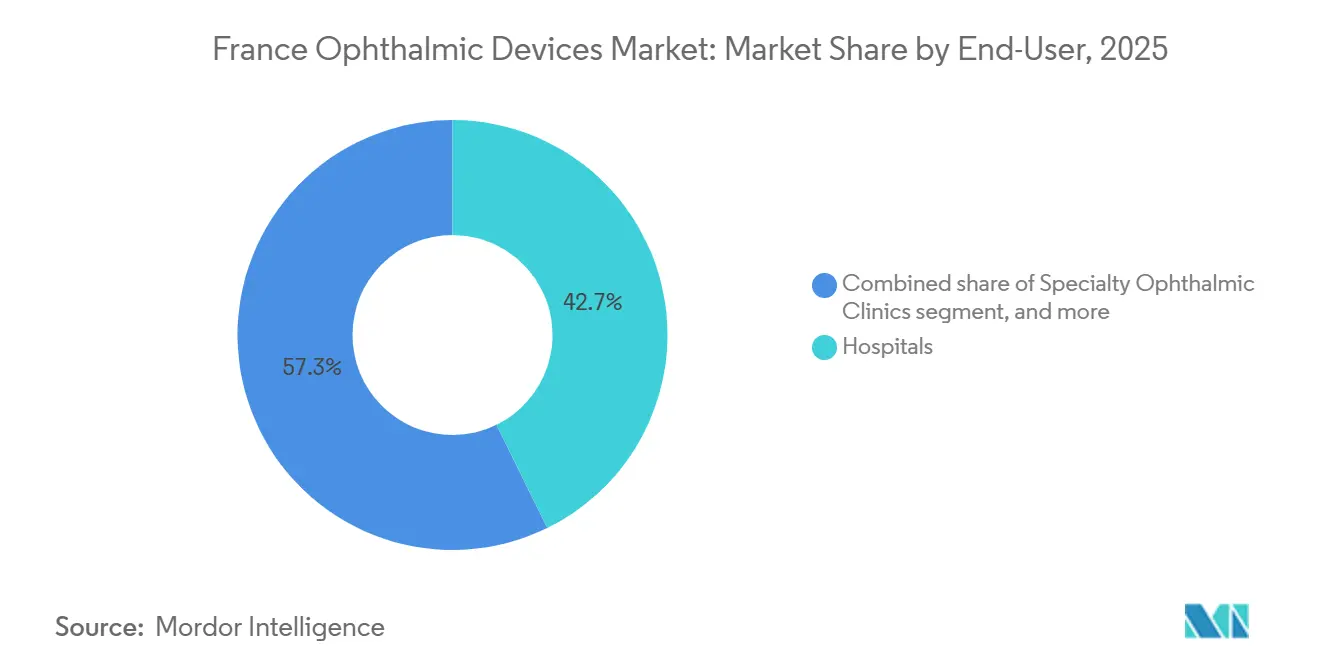

- By end user, hospitals retained a 42.75% share in 2025; ASCs recorded the fastest growth at a 10.25% CAGR over 2026-2031 as cataract and glaucoma surgeries migrate to day-care settings.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

France Ophthalmic Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging Population & Rising Cataract Prevalence | +1.8% | National, concentrated in Île-de-France, Provence-Alpes-Côte d'Azur, Auvergne-Rhône-Alpes | Long term (≥ 4 years) |

| Technological Advances in Diagnostic Imaging | +1.5% | National, early adoption in university hospital centers (CHU) in Paris, Lyon, Marseille, Toulouse | Medium term (2-4 years) |

| Expansion of Premium IOL Reimbursement Pathways | +1.2% | National, with pilot programs in Île-de-France and Occitanie | Medium term (2-4 years) |

| Emergence of Tele-Ophthalmology Hubs Linked to Regional Hospitals | +0.9% | Rural departments (Normandy, Burgundy, Nouvelle-Aquitaine, Grand Est) | Short term (≤ 2 years) |

| Government-Backed Health Innovation 2030 Funds for Med-Tech Manufacturing | +0.8% | National, with R&D clusters in Île-de-France (Créteil, Wissous), Occitanie (Toulouse) | Long term (≥ 4 years) |

| Rising Diabetes & Glaucoma Comorbidity Burden | +1.3% | National, higher prevalence in overseas territories (Réunion, Guadeloupe, Martinique) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Aging Population & Rising Cataract Prevalence

Citizens aged 75 years and older will swell by 40% between 2025 and 2035, ensuring a sustained upswing in lens-extraction demand that already exceeds 850,000 procedures annually.[1]M. Vidal-Sanz et al., “EviRed Multicenter OCTA Study,” PubMed, pubmed.ncbi.nlm.nih.gov Multifocal and extended-depth-of-focus lenses now account for 25% of private-clinic implants, tripling unit values compared with monofocal alternatives. Regional hot spots align with high-volume laser platforms, and Alcon’s international implantables revenue rose 9% currency in 2024 on the back of French premium-IOL adoption.

Technological Advances in Diagnostic Imaging

Swept-source OCT and OCT angiography achieve axial resolution below 5 µm, pushing early detection of macular edema, optic-nerve fiber loss, and micro-aneurysms past the limits of color fundus photography. The 5,000-patient EviRed study showed OCTA sensitivity above 92% for proliferative diabetic retinopathy, compared with 78% for fundus imaging. CNAM reimbursement codes granted in 2024 catalyzed private-clinic uptake, and EssilorLuxottica deepened the modality with its February 2025 acquisition of Cellview Imaging.

Expansion of Premium IOL Reimbursement Pathways

Following the 100 % Santé eyewear reform, regional agencies piloted 50% coverage for toric and multifocal IOLs in 2024, lifting premium penetration from 22% to 31% within a year. Scaling the pilots nationally awaits Haute Autorité de Santé appraisal, but early momentum already feeds Alcon’s 6% surgical revenue growth.

Emergence of Tele-Ophthalmology Hubs

OPHDIAT’s hub in Paris processes 15,000 retinopathy screens per year with 98% sensitivity, demonstrating that non-mydriatic cameras in pharmacies and GP offices can help offset specialist shortages.[2]OPHDIAT, “Tele-Ophthalmology Network,” ophdiat.org Tilak Healthcare’s OdySight app and M2care’s EUR 26 million tele-consultation deployment extend the model into home monitoring, with ISO 13485-certified devices fulfilling ANSM oversight.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Cost of Advanced Surgical Platforms | -0.7% | National, most acute in smaller ASCs and specialty clinics outside metro areas | Medium term (2-4 years) |

| Stringent EU MDR & ANSM Approval Timelines | -0.6% | Pan-European, with ANSM adding national-layer oversight in France | Long term (≥ 4 years) |

| Shortage of Ophthalmic Surgeons Outside Metro Regions | -0.5% | Rural departments (Normandy, Burgundy, Nouvelle-Aquitaine, Grand Est, Centre-Val de Loire) | Long term (≥ 4 years) |

| Growing ASC Price Pressure on Instrument Vendors | -0.4% | National, concentrated in private ASC networks negotiating bundled contracts | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capital Cost of Advanced Surgical Platforms

Femtosecond lasers priced at USD 400,000–600,000 plus USD 40,000-60,000 annual service fees deter clinics performing fewer than 1,000 cataract cases a year. Pay-per-procedure leasing shifts margin pressure to manufacturers and slows next-generation R&D despite vendor initiatives that cut per-case fees to EUR 150-200.

Stringent EU MDR & ANSM Approval Timelines

Under MDR, Class IIb and III ophthalmic devices face 12-18 month certification cycles, 20-30% higher pre-market costs, and ANSM post-market audits that narrow commercial windows, pushing small innovators to delay launches or exit product lines.[3]Agence Nationale de Sécurité du Médicament et des Produits de Santé (ANSM), “EU MDR Implementation,” ansm.sante.fr

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Diagnostic Upswing Against Vision-Care Dominance

Vision Care Devices accounted for 62.49% of the France ophthalmic devices market in 2025, underpinned by EssilorLuxottica’s 35-plant, 583-lab network which yielded roughly 550 million prescription lenses per year. The Diagnostic & Monitoring sub-category is forecast to outpace at an 8.17% CAGR, as OCT scanners, AI-ready fundus cameras, and remote-reading software equip community practices and tele-screening hubs. Heidelberg Engineering’s OCT line, now 80%-owned by EssilorLuxottica, anchors the surge. Surgical

Product-level differentiation hinges on bundled ecosystems: diagnostics feed surgical conversion, and vision-care chains cross-sell contact lenses and myopia-control spectacles. This closed-loop positioning allows vertical giants to defend margins, whereas standalone imaging firms pursue OEM alliances. Competitive spillover already sees vision-care cash-flows underwriting R&D for swept-source imaging, sustaining technology refreshes every 2-4 years.

By Disease Indication: Screening Turns Diabetic Retinopathy Into Fastest Riser

Cataract retained a 38.85% share in 2025 thanks to high procedure volumes and premium IOL upsell, but solutions for diabetic retinal diseases are projected to expand at a 9.63% CAGR through 2031. The France ophthalmic devices market for diabetic retinopathy hardware and software is accelerating as AI triage tools like OphtAI and IDx-DR secure CE marks and reimbursement codes. Tele-screening ecosystems cut wait times in rural pharmacies from 9 months to same-day referrals, increasing early-stage detection and funneling patients into OCT and laser-treatment workflows. Glaucoma commands around 20% share and benefits from the expanding MIGS toolkit, although procedure uptake remains slower than U.S. benchmarks despite favorable EUR 1,154 per QALY economics for iStent inject.

By End-User: ASC Shift Reshapes Purchasing

Hospitals captured 42.75% of the France ophthalmic devices market share in 2025, anchoring complex vitreoretinal and corneal work. Yet ASCs illustrate double-digit expansion, 10.25% CAGR, because bundled payments reward high-throughput cataract and glaucoma cases. Device makers increasingly consign inventory and offer outcomes-based contracts, compressing gross margins while protecting volume. The remaining demand arises from optical retail and tele-screening nodes, where diagnostic devices integrate into primary-care workstreams.

Geography Analysis

Île-de-France, Auvergne-Rhône-Alpes, and Provence-Alpes-Côte d’Azur had similar population density, higher disposable income, and the presence of university hospital centers that trial next-generation hardware. Ophthalmologist density peaks at 8 per 100,000 in Paris versus 3 per 100,000 in Normandy and Burgundy, spurring tele-ophthalmology rollouts such as OPHDIAT’s 15,000-exam annual network. Overseas territories show elevated diabetes prevalence, boosting demand for retina-imaging equipment but hampered by logistics and specialist shortages.

Policy instruments concentrate investment in urban R&D corridors. EssilorLuxottica’s Labex facility in Wissous adds automated surfacing lines and ISO 13485-compliant QC labs to support regional supply. France 2030 grants also fund PREMYOM, a consortium tackling pediatric myopia with Stellest and SightGlass DOT lenses. Meanwhile, Île-de-France and Occitanie pilots covering half of premium-IOL co-pays show that even limited reimbursement can shift implant mix by nine percentage points in a year.

Competitive intensity differs by region. Multinationals dominate surgical and diagnostic installs in metro hospitals, while French startups exploit telemedicine niches in sparsely populated departments. MDR compliance favors players with dedicated regulatory teams, further adding to incumbents' moat.

Competitive Landscape

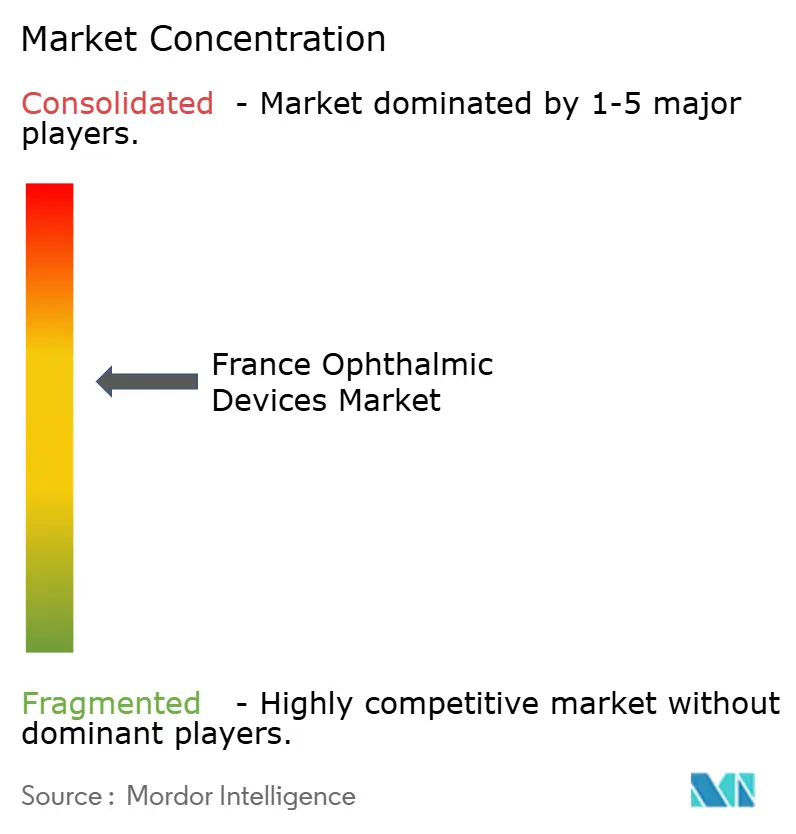

The top five suppliers, EssilorLuxottica, Alcon, Carl Zeiss Meditec, Bausch + Lomb, and Johnson & Johnson Vision, command an estimated significant 2025 revenue, giving the French ophthalmic devices market a moderate-to-high concentration profile. EssilorLuxottica’s lens plants, 583 labs, and more than 1,000 retail stores across EMEA generate an integrated loop that smaller vendors struggle to match. Its acquisitions of Heidelberg Engineering and Cellview Imaging elevate diagnostic presence, while the Espansione deal adds dry-eye therapy to the portfolio.

White space persists in rural tele-screening and MIGS penetration. Evolucare’s OphtAI secured the CE mark in 2024 for automated diabetic-retinopathy grading, while Tilak Healthcare’s OdySight raised EUR 10 million to deliver home-monitoring, underscoring venture appetite for niche disruption. Yet scaling such models requires MDR-ready quality systems and notified-body access, hurdles that entrenched groups navigate more readily.

France Ophthalmic Devices Industry Leaders

EssilorLuxottica SA

Alcon Inc.

Carl Zeiss Meditec AG

Johnson & Johnson Vision Care

Topcon Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: EssilorLuxottica inaugurated a new excellence laboratory in Paris, positioning the site as a hub for smart-lens prototyping and clinical collaboration. The facility underlines national efforts to anchor high-value manufacturing in France.

- January 2024: The MEDITWIN consortium launched with governmental backing, aiming to build virtual twins that personalize ophthalmic treatment pathways and integrate seamlessly with imaging devices.

- August 2024: Haute Autorité de Santé issued a favorable reimbursement decision for EYLEA (aflibercept) in neovascular age-related macular degeneration, reinforcing policy support for evidence-backed innovations.

- May 2024: The Choose France Summit announced health-care investment pledges of EUR 15 billion (USD 16.3 billion), signaling sustained capital inflows to medical technology projects.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study counts every revenue dollar generated inside France from any medical device whose primary purpose is to test, treat, or correct human vision, including diagnostic imaging systems, surgical hardware, and vision-care products such as contact lenses and spectacles.

Scope exclusions include over-the-counter eye drops, pharmaceutical implants, and service fees that are not sized in this model.

Segmentation Overview

- By Device Type

- Diagnostic & Monitoring Devices

- OCT Scanners

- Fundus & Retinal Cameras

- Autorefractors & Keratometers

- Corneal Topography Systems

- Ultrasound Imaging Systems

- Perimeters & Tonometers

- Other Diagnostic & Monitoring Devices

- Surgical Devices

- Cataract Surgical Devices

- Vitreoretinal Surgical Devices

- Refreactive Surgical Devices

- Glaucoma Surgical Devices

- Other Surgical Devices

- Vision Care Devices

- Spectacles Frames & Lenses

- Contact Lenses

- Diagnostic & Monitoring Devices

- By Disease Indication

- Cataract

- Glaucoma

- Diabetic Retinopathy

- Other Disease Indications

- By End-user

- Hospitals

- Specialty Ophthalmic Clinics

- Ambulatory Surgery Centers (ASCs)

- Other End-users

Detailed Research Methodology and Data Validation

Desk Research

We began with public macro and trade data from Sante Publique France, Eurostat health accounts, and UN Comtrade, which outline procedure volumes, import values, and population health risks. Policy notes from Haute Autorite de Sante and the French Ophthalmology Society clarified reimbursement pathways and device adoption rules. Company 10-Ks and investor decks helped us capture selling price shifts, while reputable news archives in Dow Jones Factiva and equipment shipment snapshots in D&B Hoovers supplied early demand signals. The sources listed here illustrate, not exhaust, the references mined by our analysts.

Primary Research

Interviews with hospital purchasing heads, community optometrists, and device distributors across Ile-de-France, Auvergne-Rhone-Alpes, and Provence-Alpes-Cote d'Azur let us validate hospital cap-ex intentions, average selling prices, and product mix shifts that secondary data cannot fully reveal. Inputs from regulatory consultants clarified pending MDR compliance costs.

Market-Sizing & Forecasting

Mordor analysts first built a top-down demand pool using surgical procedure counts, outpatient exam visits, and per-capita spectacle replacement cycles, which are then balanced with selective bottom-up cross-checks such as sampled ASP multiplied by unit shipments reported by key distributors. Critical variables include cataract surgery volume growth, diabetic-retinopathy screening penetration, premium intraocular-lens uptake, euro-to-dollar exchange trends, and public hospital budget ceilings. A multivariate regression links these drivers to historical revenue to forecast 2025-2030, while scenario analysis adjusts for reimbursement reform. Any gaps in distributor rolls are bridged using regional import trends and validated with expert sentiment.

Data Validation & Update Cycle

Outputs run through variance screens against independent procedure tallies and customs data. Senior reviewers question anomalies, and findings loop back to experts where needed before sign-off. We refresh each model annually and trigger interim updates when material events, such as tariff shifts or a blockbuster product recall, occur.

Why Our France Ophthalmic Devices Baseline Stands Firm

Published figures often diverge because firms pick different device lists, price assumptions, and refresh rhythms.

Key gap drivers here include some publishers excluding spectacles, others inflating values by layering service fees, a few converting euros at outdated rates, and several using aggressive premium-lens penetration curves that our hospital checks do not yet confirm.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.35 B (2024) | Mordor Intelligence | - |

| USD 0.65 B (2024) | Global Consultancy A | Omits vision-care products and applies 3-country average pricing |

| USD 1.35 B (2024) | Industry Portal B | Bundles drugs and devices, then splits by fixed 60-40 ratio |

| USD 1.40 B (2023) | Regional Consultancy C | Uses 2023 base, rolls forward at flat 5.8 percent without recent procedure rebound |

The comparison shows why buyers should rely on Mordor's disciplined scope selection, mixed-method model, and yearly refresh, which together give a balanced, transparent baseline that decision makers in France's eye-care ecosystem can trust.

Key Questions Answered in the Report

How fast is the France ophthalmic devices market expected to grow through 2031?

The market is projected to expand from USD 2.71 billion in 2026 to USD 3.95 billion by 2031 at a 7.81% CAGR.

Which product category leads revenue today?

Vision Care Devices command 62.49% of 2025 revenue, driven by EssilorLuxottica’s vast lens and retail network.

What segment is forecast to grow the quickest?

Diagnostic & Monitoring Devices, including OCT and AI-enabled fundus cameras, are set to rise at an 8.17% CAGR through 2031.

Why are ambulatory surgery centers important for suppliers?

ASCs are projected to post a 10.25% CAGR because reimbursement parity pushes cataract and glaucoma cases out of hospitals, reshaping purchasing toward compact, cost-efficient platforms.

Page last updated on: