Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 97.27 Billion |

| Market Size (2031) | USD 127.55 Billion |

| Growth Rate (2026 - 2031) | 5.57% CAGR |

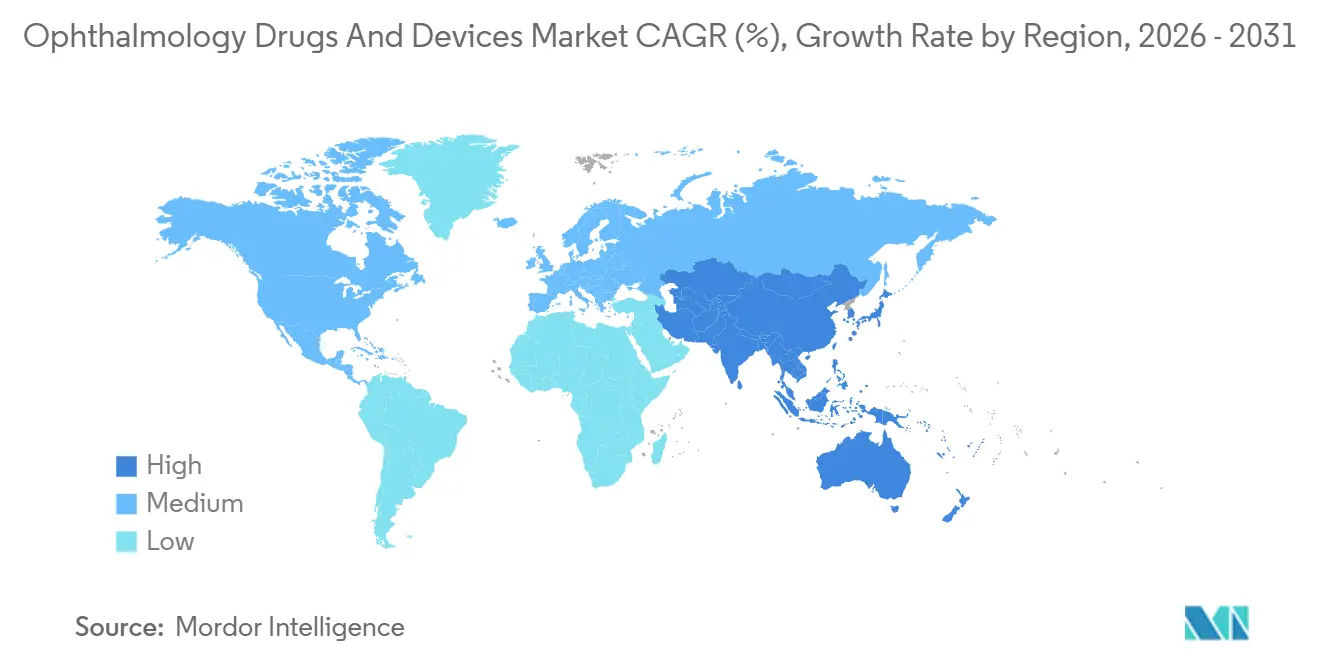

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ophthalmology Drugs And Devices Market Analysis by Mordor Intelligence

The Ophthalmology Drugs And Devices Market size is estimated at USD 97.27 billion in 2026, and is expected to reach USD 127.55 billion by 2031, at a CAGR of 5.57% during the forecast period (2026-2031).

Steady incidence growth in diabetic retinopathy, myopia and age-related disorders, coupled with surgical miniaturization and drug-delivery innovation, anchors demand expansion. Hospitals are shifting cataract and glaucoma cases to ambulatory surgical centers that operate with lower overhead, while long-acting anti-vascular-endothelial-growth-factor (anti-VEGF) agents halve injection visits, easing clinic congestion. Biosimilar entry is squeezing branded margins yet broadening access in price-sensitive markets. At the same time, swept-source optical-coherence-tomography (OCT) and femtosecond platforms raise imaging speed and surgical efficiency, driving a recurring consumables model. Artificial-intelligence (AI) algorithms moving into retail pharmacies and primary-care clinics are expanding the diagnostic funnel and pushing complex cases toward specialists for high-value procedures.

Key Report Takeaways

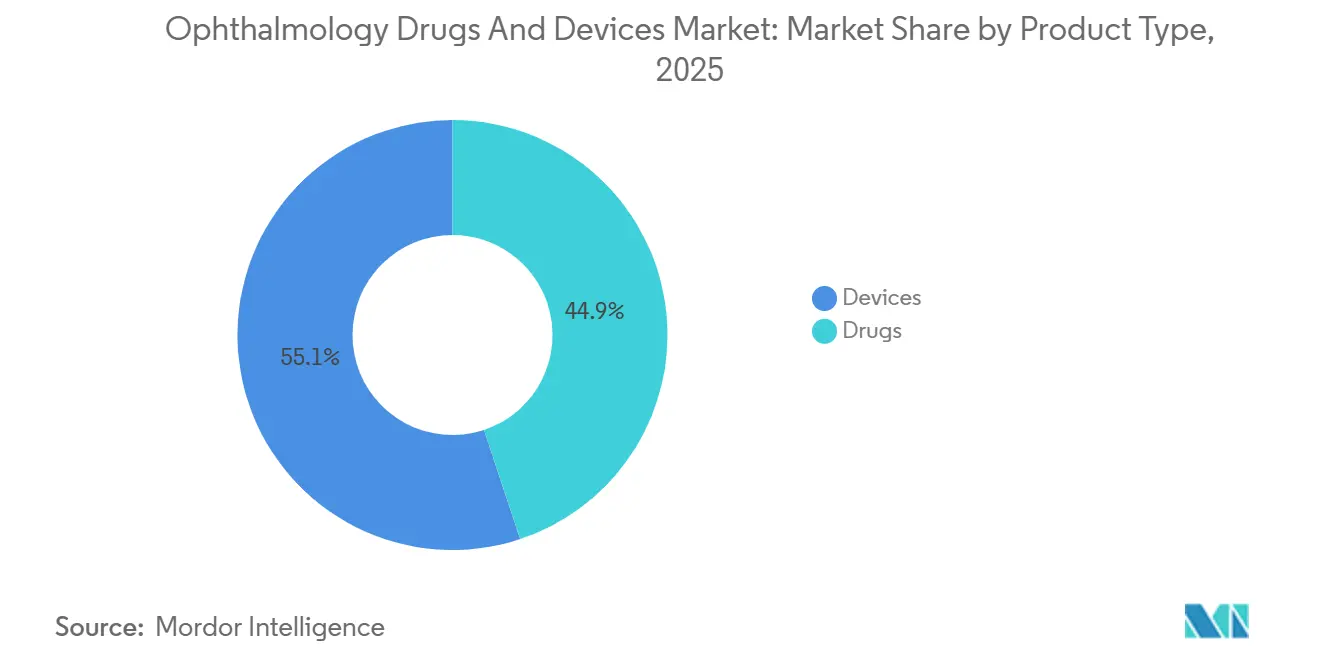

- By product type, devices led with 55.12% ophthalmology drugs and devices market share in 2025. Drugs are projected to grow at an 8.25% CAGR through 2031.

- By disease, glaucoma captured 40.53% of revenue in 2025. Diabetic retinopathy is forecast to expand at an 8.85% CAGR through 2031.

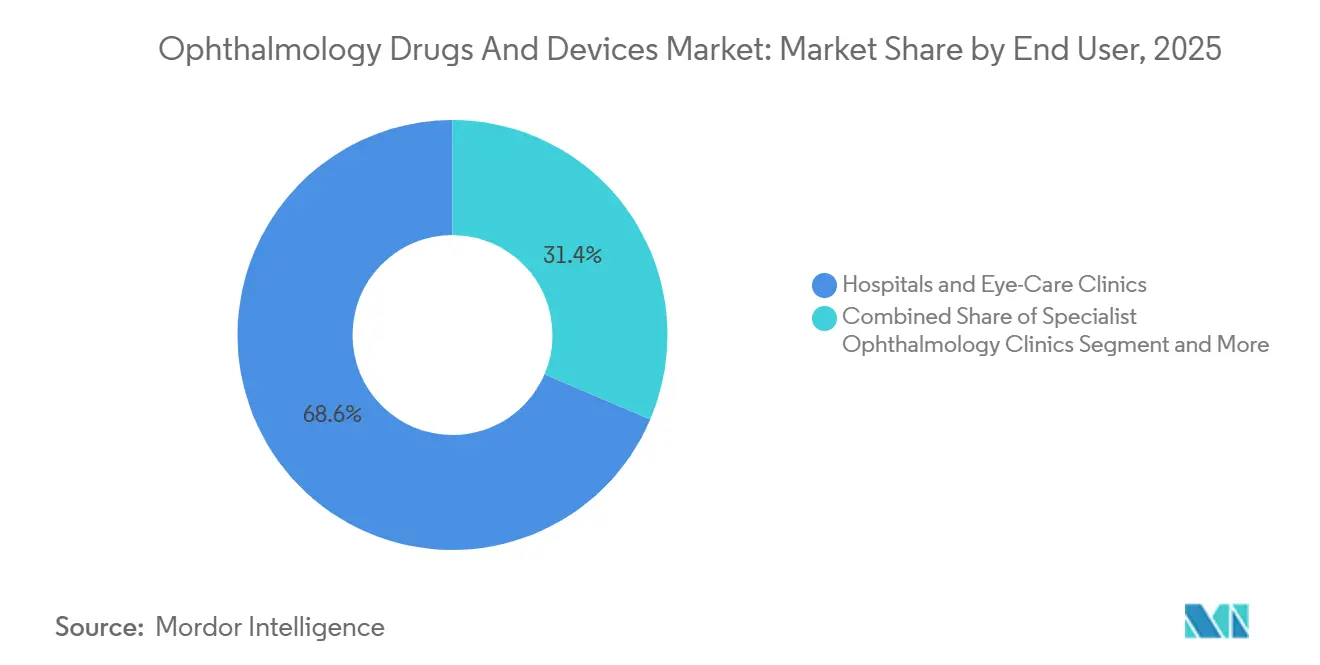

- By end user, hospitals and eye-care clinics accounted for 68.63% of spending in 2025. Specialist ophthalmology clinics are poised to grow at an 8.72% CAGR to 2031.

- By geography, North America retained 42.13% of value in 2025, while Asia-Pacific is projected to rise at a 9.51% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Ophthalmology Drugs And Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging population and rising eye-disease prevalence | +1.2% | Global, peak in Japan, Germany, Italy, South Korea | Long term (≥ 4 years) |

| Rapid adoption of minimally-invasive and femtosecond-laser surgeries | +0.9% | North America, Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Long-acting anti-VEGF biologics and sustained-delivery implants | +1.5% | North America, Western Europe, spreading globally | Medium term (2-4 years) |

| ASC shift unlocking device-kit demand | +0.7% | United States, early uptake in Canada, Australia | Short term (≤ 2 years) |

| AI-enabled point-of-care diagnostics | +0.6% | North America, EU, urban China, India | Medium term (2-4 years) |

| Diabetes and progressive myopia raising retinal and refractive procedures | +1.3% | Asia-Pacific core, spillover to Middle East, Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Aging Population And Rising Eye-Disease Prevalence

Populations are aging faster than ophthalmology workforces can expand. Japan recorded 29% of residents over 65 in 2024, the EU’s median age crossed 44, and South Korea logged a 23% jump in glaucoma diagnoses between 2020 and 2024. Longer lifespans translate into multi-year treatment cycles for wet age-related macular degeneration (AMD) and chronic glaucoma, locking in predictable biologic revenue but stretching specialist capacity. Health systems encourage home monitoring and tele-ophthalmology to offset clinician shortages. Payers, facing lifetime therapy costs, now authorize premium drugs only after real-world evidence of functional vision gains, not anatomic changes alone.

Rapid Adoption Of Minimally-Invasive And Femtosecond-Laser Surgeries

Ambulatory surgical centers (ASCs) in the United States completed over half of outpatient ophthalmic procedures in 2024, boosted by a 2.9% payment rise for 2025[1]Centers for Medicare & Medicaid Services, “CY 2025 ASC Payment System,” cms.gov. LENSAR’s ALLY adaptive femtosecond laser introduced real-time OCT guidance, lowering phaco energy and complication rates. Glaukos’ iStent infinite, launched in 2024, lowered intraocular pressure without bleb formation, accelerating micro-invasive glaucoma surgery uptake. Hospitals lag in capital purchases because Medicare pays identical facility fees regardless of technology. Consequently, ASCs bundle premium laser packages and capture co-payments, feeding a virtuous cycle of equipment turnover and consumables growth.

Long-Acting Anti-VEGF Biologics And Sustained-Delivery Implants

Regeneron’s EYLEA HD (aflibercept 8 mg) entered the U.S. market in 2024 with 16-week dosing, cutting intravitreal visits by half. Interchangeable biosimilars Yesafili and Opuviz launched at 15%-20% lower prices, prompting step-therapy protocols that steer first-line patients to cheaper alternatives. The market is splitting: high-volume, low-margin biosimilars versus low-volume, high-margin extended-interval agents. Port-delivery implants such as Genentech’s Susvimo now treat diabetic macular edema and diabetic retinopathy, but regional regulators differ; the European Medicines Agency withheld approval for Syfovre in 2024 over long-term safety questions.

ASC Shift Unlocking Device Kit Demand

ASCs favor disposable phaco handpieces, intraocular-lens injectors, and viscoelastics that remove re-processing costs. Alcon reported USD 1.1 billion in surgical revenue for Q3 2024, with consumables growing faster than consoles, confirming a razor-and-blade strategy. CMS trimmed Omidria reimbursement to USD 425.89 per dose for 2025, encouraging volume discounts or compounded substitutes. Consolidation looms: multi-site ASC chains secure better device pricing, which could reduce the pool of independent purchasers and sharpen bargaining power against manufacturers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital cost of advanced platforms | -0.8% | Global, acute in emerging markets | Short term (≤ 2 years) |

| Stringent FDA and EMA post-market evidence mandates | -0.6% | North America, Europe | Medium term (2-4 years) |

| Carbon-footprint scrutiny of single-use consumables | -0.3% | Europe, select U.S. systems | Long term (≥ 4 years) |

| API-trade tariff shocks disrupting generic supply | -0.4% | Global, strong in cost-sensitive regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capital Cost Of Advanced Platforms

Swept-source OCT and femtosecond lasers list above USD 150,000, restricting adoption to high-volume centers. Zeiss’s CIRRUS 6000 debuted at USD 180,000, delivering 100,000 A-scans per second, yet many rural hospitals operate on annual equipment budgets below USD 50,000. Topcon now offers pay-per-scan leasing at USD 25, shifting financial risk to practices that must maintain minimum throughput. In emerging markets, refurbished equipment remains the norm, limiting early disease detection and reinforcing inequality.

Stringent FDA & EMA Post-Market Evidence Mandates

Draft FDA guidance in 2024 requires up to 24-month registries with functional endpoints, adding USD 5-10 million per product. The EMA’s 2024 Syfovre refusal after U.S. approval highlights divergent evidence thresholds. Smaller biotechs often lack funds for long surveillance, pushing them toward early licensing or acquisition by large pharmaceutical companies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Devices Anchor Revenue, Drugs Accelerate Growth

Devices held 55.12% of the ophthalmology drugs and devices market in 2025, reflecting an installed base that drives consumables pull-through. Premium intraocular lenses (IOLs) captured 35% of cataract units in developed regions, with Alcon’s PanOptix and Vivity generating USD 450 million combined revenue in 2024[2]Alcon, “Investor Relations Q3 2024 Earnings,” alcon.com. Diagnostic platforms are migrating from spectral-domain to swept-source OCT; Heidelberg’s SPECTRALIS OCT2 integrates angiography and autofluorescence, cutting multimodal imaging time.

Drugs advance at an 8.25% CAGR through 2031, propelled by anti-VEGF biologics and dry-eye innovations. Retinal therapeutics contributed 48% of pharmaceutical revenue in 2024, yet biosimilars trimmed wholesale prices. Dry-eye prescriptions topped USD 2.1 billion in 2024, but patent expiries invite generic erosion. Fixed-dose glaucoma combinations reduce drop burden and improve adherence, consolidating prescription share.

By Disease: Glaucoma Leads, Diabetic Retinopathy Surges

Glaucoma generated 40.53% of revenue in 2025, supported by lifelong medication and growing MIGS acceptance. Glaukos sold 12,000 iStent infinite units in Q3-2024, up 45% year over year. PreserFlo MicroShunt likewise gains traction for refractory cases.

Diabetic retinopathy posts the fastest growth at 8.85% CAGR through 2031, reflecting the CDC projection of 14.7 million U.S. cases by 2050. Anti-VEGF agents such as EYLEA HD serve both AMD and diabetic phenotypes, aiding cost amortization. Cataract surgery still leads on procedure volume but faces ASP pressure from low-cost Asian lenses. Myopia management is emerging as a preventive segment with annuity-style revenue from pediatric interventions.

By End User: Hospitals Dominate, Specialist Clinics Gain Share

Hospitals and general eye-care clinics absorbed 68.63% of 2025 spending, underpinned by referral patterns for complex retinal and corneal surgeries. Yet specialist ophthalmology clinics grow at 8.72% CAGR to 2031, buoyed by higher injection throughput and streamlined capital amortization. ASCs now deliver more than half of U.S. outpatient eye procedures, leveraging 2.9% higher CMS payments for 2025 to invest in premium technology.

Retail and online pharmacies lost 12% ophthalmic prescription volume in 2024 as payers directed patients to specialty channels with adherence oversight. Tele-ophthalmology and optical-chain OCT screening continue to widen first-line detection.

Geography Analysis

North America represented 42.13% of the ophthalmology drugs and devices market in 2025. Medicare Advantage penetration and earlier uptake of premium IOLs underpin value. CMS fixed Omidria payment at USD 425.89 per dose for 2025, pushing ASCs to seek discounts. The FDA cleared EYLEA HD and expanded Susvimo labeling, supporting long-interval therapy adoption.

Europe held 28% of revenue in 2025 but faces stringent cost-effectiveness hurdles. The EMA’s Syfovre non-approval signals higher evidence bars. Germany and the United Kingdom dominate spending, while Central-Eastern states benefit from EU infrastructure funds. The EU Medical Device Regulation forces environmental disclosures, tilting demand toward reusable or low-carbon options. Roche secured a CE mark for Contivue in 2025, yet uptake depends on surgical capacity and infection-control data.

Asia-Pacific advances at a 9.51% CAGR to 2031, led by Japan’s super-aged demographic, China’s school vision mandates, and India’s high-volume cataract networks. Japan’s PMDA approved anti-VEGF biosimilars in 2024, expanding access. South Korea fast-tracked Zeiss’s VisuMax 800 for SMILE, displacing LASIK. China’s urban youth myopia crisis drives orthokeratology and atropine adoption. India pilots fundus-image tele-networks to bridge ophthalmologist shortfalls. Australia accelerates device import through TGA alignment with CE marks, and its Pharmaceutical Benefits Scheme reimburses biosimilar aflibercept at 40% lower patient cost.

The Middle East and Africa plus South America remain nascent. Saudi Arabia and the UAE import premium IOLs under Vision 2030, while Brazil cleared 450,000 cataract cases in 2024 yet faces a million-plus backlog[3]Agência Nacional de Vigilância Sanitária Brazil, “ANVISA Approvals,” anvisa.gov.br. Argentina’s peso depreciation hampers imports, extending device lifecycles beyond optimal usability.

Competitive Landscape

Market concentration is moderate. Alcon, Bausch + Lomb, Zeiss, and other market players captured a significant percentage of the ophthalmology drugs and devices market revenue in 2025. Alcon’s consumables strategy lifted surgical sales 6% year over year. Regeneron’s share slipped to 38% in 2025 as Yesafili and Opuviz biosimilars gained traction. Novartis leverages licensing to sustain Lucentis royalties while investing in gene therapy. Zeiss differentiates through AI-integrated imaging, cutting reading time by 70% and enhancing same-day treatment decisions.

Emerging disruptors include Apellis, which seized 12% of the nascent geographic-atrophy space within 18 months, and Glaukos, whose MIGS line erodes traditional filtration surgery volumes. Gene therapy momentum continues after the March 2025 approval of ENCELTO for macular telangiectasia, indicating payer readiness to fund single-administration cures at USD 850,000 per eye. Device makers respond by bundling AI analytics and maintenance into service contracts, locking clinics into ecosystem platforms.

Ophthalmology Drugs And Devices Industry Leaders

Alcon Inc.

Allergan (AbbVie)

Bausch + Lomb Corp.

Johnson & Johnson Vision Care Inc.

Carl Zeiss Meditec AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Regeneron won FDA approval for EYLEA HD to treat macular edema following retinal vein occlusion with dosing every eight weeks after loading.

- July 2025: Alcon announced plans to acquire LumiThera and its photobiomodulation device for early to intermediate dry AMD. The PBM system demonstrated statistically meaningful vision improvement over baseline in clinical studies.

Global Ophthalmology Drugs And Devices Market Report Scope

As per the scope of the report, ophthalmology drugs and devices are specialized products used to diagnose, treat, and manage eye conditions. Drugs include eye drops, ointments, and systemic medications for issues like infections, glaucoma, and allergies. Devices encompass instruments and equipment such as laser systems, contact lenses, and surgical tools that aid in eye diagnosis, monitoring.

The segmentation for the ophthalmology drugs and devices market is categorized by product type, disease, end user, and geography. By product type, the market includes devices and drugs. Devices are further segmented into surgical devices, which include intraocular lenses, ophthalmic lasers, and others, and diagnostic devices, which include optical coherence tomography, fundus imaging, biometers and ultrasound A/B, slit-lamps and digital microscopes, and corneal topographers and aberrometers. Drugs are segmented into anti-glaucoma agents, retinal-disorder drugs, dry-eye therapeutics, allergy and inflammation drugs, anti-infectives, and other drugs. By disease, the market is segmented into glaucoma, cataract, age-related macular degeneration, diabetic retinopathy, inflammatory and ocular-surface diseases, refractive errors, and other disorders. By end user, the market includes hospitals and eye-care clinics, ambulatory surgical centers (ASC), specialist ophthalmology clinics, retail and online pharmacies, and others. By geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East, and Africa, and South America. The market forecasts are provided in terms of value (USD).

By Product Type

| Devices | Surgical Devices | Intraocular Lenses |

| Ophthalmic Lasers | ||

| Others | ||

| Diagnostic Devices | Optical Coherence Tomography | |

| Fundus Imaging | ||

| Biometers & Ultrasound-A/B | ||

| Slit-lamps & Digital Microscopes | ||

| Corneal Topographers & Aberrometers | ||

| Biometers & Ultrasound-A/B | ||

| Drugs | Anti-Glaucoma Agents | |

| Retinal-Disorder Drugs | ||

| Dry-Eye Therapeutics | ||

| Allergy / Inflammation Drugs | ||

| Anti-infectives | ||

| Other Drugs | ||

By Disease

| Glaucoma |

| Cataract |

| Age-Related Macular Degeneration |

| Diabetic Retinopathy |

| Inflammatory & Ocular-Surface Diseases |

| Refractive Errors |

| Other Disorders |

By End User

| Hospitals & Eye-Care Clinics |

| Ambulatory Surgical Centers (ASC) |

| Specialist Ophthalmology Clinics |

| Retail & Online Pharmacies |

| Others |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Devices | Surgical Devices | Intraocular Lenses |

| Ophthalmic Lasers | |||

| Others | |||

| Diagnostic Devices | Optical Coherence Tomography | ||

| Fundus Imaging | |||

| Biometers & Ultrasound-A/B | |||

| Slit-lamps & Digital Microscopes | |||

| Corneal Topographers & Aberrometers | |||

| Biometers & Ultrasound-A/B | |||

| Drugs | Anti-Glaucoma Agents | ||

| Retinal-Disorder Drugs | |||

| Dry-Eye Therapeutics | |||

| Allergy / Inflammation Drugs | |||

| Anti-infectives | |||

| Other Drugs | |||

| By Disease | Glaucoma | ||

| Cataract | |||

| Age-Related Macular Degeneration | |||

| Diabetic Retinopathy | |||

| Inflammatory & Ocular-Surface Diseases | |||

| Refractive Errors | |||

| Other Disorders | |||

| By End User | Hospitals & Eye-Care Clinics | ||

| Ambulatory Surgical Centers (ASC) | |||

| Specialist Ophthalmology Clinics | |||

| Retail & Online Pharmacies | |||

| Others | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| Australia | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | GCC | ||

| South Africa | |||

| Rest of Middle East and Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

How large is the ophthalmology drugs and devices market in 2026?

The market stands at USD 97.27 billion in 2026 and is projected to reach USD 127.55 billion by 2031.

Which segment shows the fastest growth to 2031?

Diabetic retinopathy leads with an 8.85% CAGR, reflecting rising diabetes prevalence and tighter screening protocols.

Why are long-acting anti-VEGF agents important?

They cut injection visits from monthly to quarterly or longer, easing clinic load and improving patient adherence.

What drives Asia-Pacific's outsize growth rate?

An aging Japanese population, China's myopia control mandates and India's high-volume cataract programs push a 9.51% CAGR.

How are biosimilars affecting market dynamics?

Interchangeable aflibercept biosimilars entered at 15%-20% discounts, reducing branded share but widening access in cost-sensitive regions.

Page last updated on: