Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

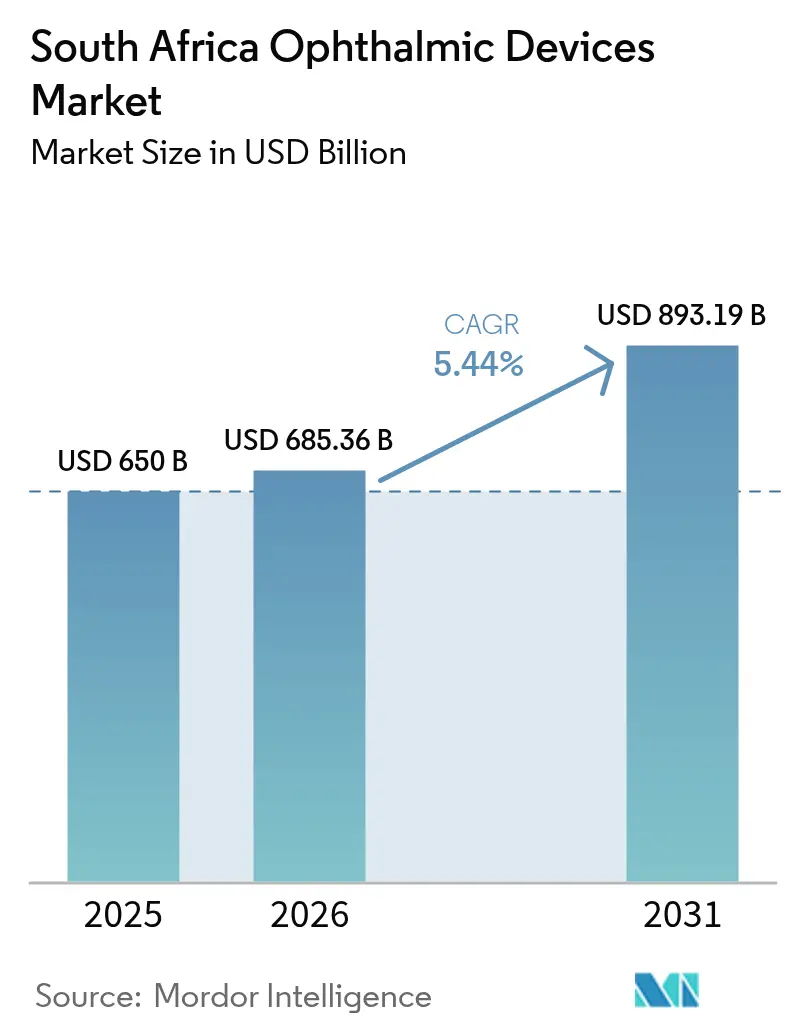

| Base Year Market Size (2025) | USD 650 Billion |

| Market Size (2026) | USD 685.36 Billion |

| Market Size (2031) | USD 893.19 Billion |

| Growth Rate (2026 - 2031) | 5.44% CAGR |

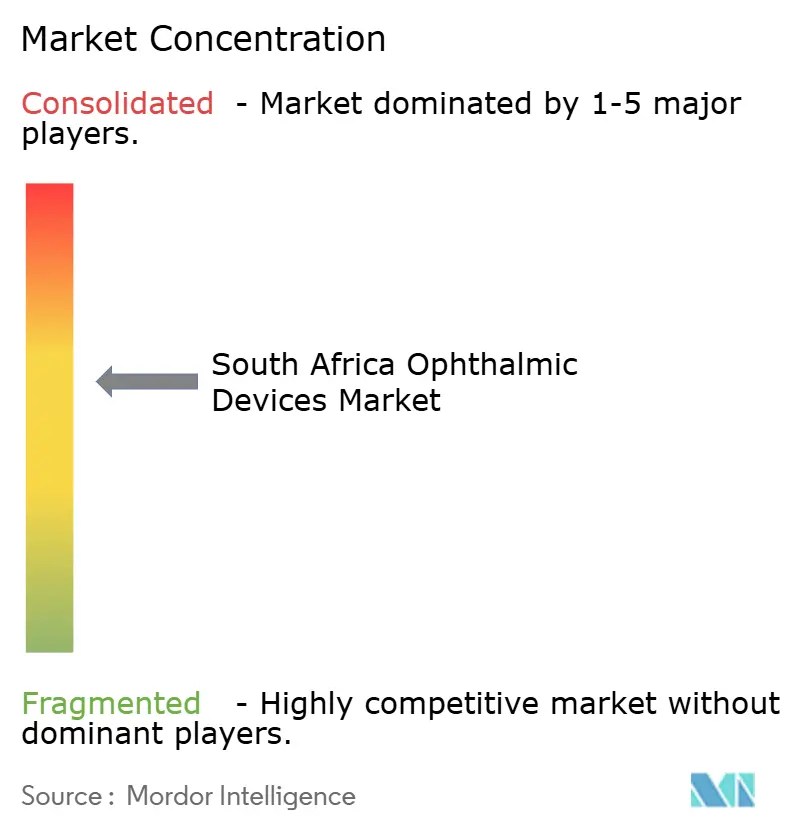

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Africa Ophthalmic Devices Market Analysis by Mordor Intelligence

The South Africa ophthalmic devices market size is expected to grow from USD 650 million in 2025 to USD 685.36 million in 2026 and is forecast to reach USD 893.19 million by 2031 at 5.44% CAGR over 2026-2031. Demand is expanding as rising cataract surgery volumes, growing diabetic retinopathy screening programs, and wider medical-scheme reimbursement converge with technology upgrades in both public and private settings. Multinational manufacturers have responded by establishing local assembly hubs to offset rand volatility, while public-sector tenders increasingly specify whole-of-life service contracts that bundle devices with training and maintenance. Early adoption of AI-assisted diagnostics in urban hospitals is demonstrating workflow gains that, in turn, spur purchases of high-resolution OCT and fundus imaging systems. Simultaneously, the proliferation of optical retail chains in townships is broadening the entry-level pool of patients who later transition to surgical care.

Key Report Takeaways

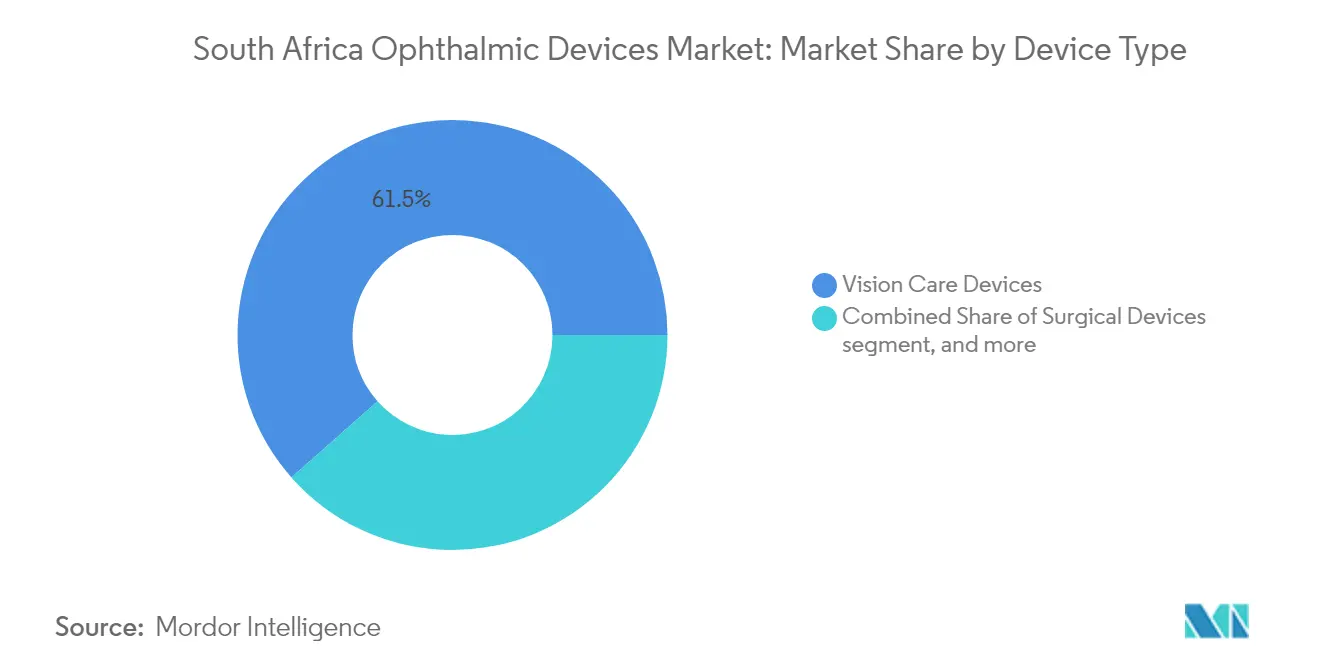

- By device type, vision care products held 61.52% of the South Africa ophthalmic devices market share in 2025, while diagnostic and monitoring devices are forecast to expand at a 7.54% CAGR to 2031.

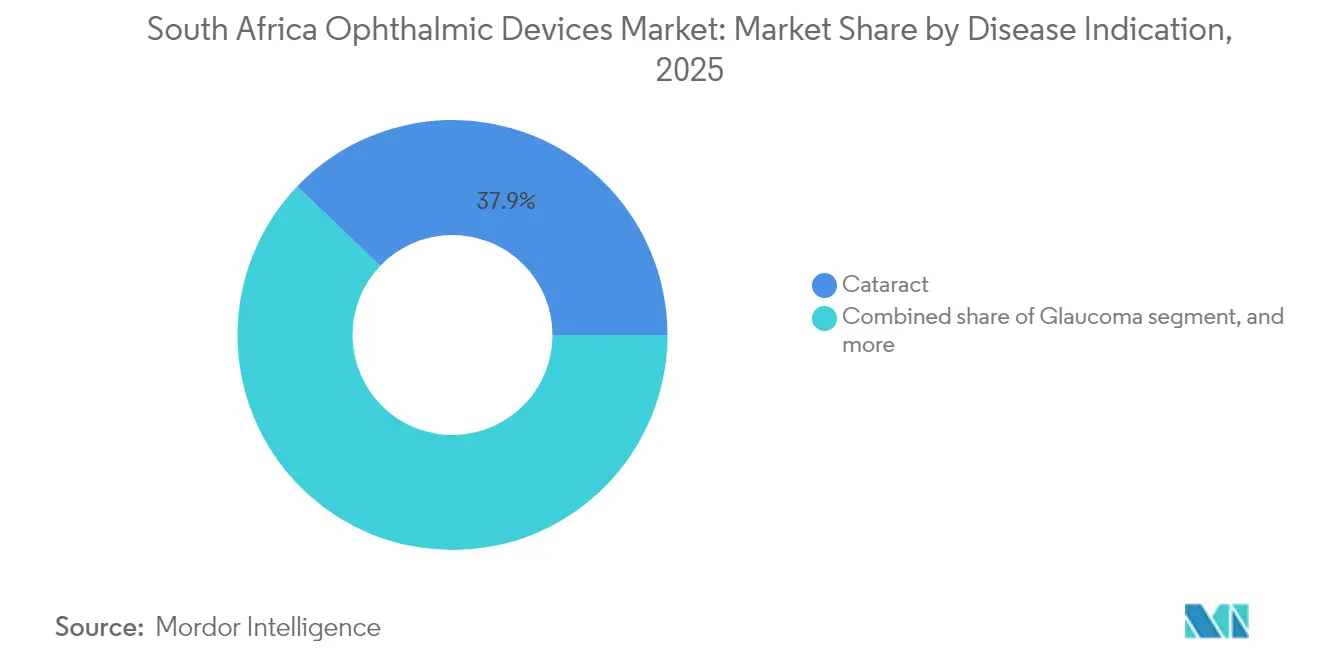

- By disease indication, cataract products dominated with 37.86% share of the South Africa ophthalmic devices market size in 2025; diabetic-retinopathy devices are poised to grow at a 6.78% CAGR through 2031.

- By end-user, hospitals accounted for 42.09% revenue share of the South Africa ophthalmic devices market in 2025; ambulatory surgery centers (ASCs) record the highest projected CAGR at 6.62% over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South Africa Ophthalmic Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising incidence of diabetic retinopathy amid South Africa’s growing diabetes prevalence | +0.40 | Limpopo and major urban provinces | Long term (≥ 4 years) |

| Government Vision 2030 Eye-Health Programme boosts surgical volume in public sector | +0.30 | National public hospitals | Medium term (2-4 years) |

| Rapid adoption of femto cataract and SMILE lasers in private hospitals | +0.35 | Gauteng & Western Cape | Short term (≤ 2 years) |

| Expansion of medical-scheme coverage for intraocular lenses & premium diagnostics | +0.25 | Major urban centers | Medium term (2-4 years) |

| Growth of vision-care retail chains in urban townships increasing device demand | +0.15 | Johannesburg, Cape Town, Durban townships | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Escalating Diabetic Retinopathy Prevalence

South Africa’s 35.3% diabetic-retinopathy prevalence among diabetes patients in Limpopo is driving unprecedented orders for high-resolution OCT scanners and mydriatic fundus cameras, with total demand forecast to rise 40% by 2027. Hospitals are increasingly adopting teleophthalmology models in which technicians capture retinal images in rural clinics and ophthalmologists interpret them remotely, cutting referral delays by up to 60%. Equipment vendors now structure contracts as service-based subscriptions that spread costs across multiyear screening quotas, reducing upfront capital outlays. The resulting procurement flexibility is accelerating uptake among provincial health departments that previously delayed purchases over budget-cycle constraints. Suppliers that integrate AI grading algorithms into imaging platforms report 25% faster reading times, freeing scarce ophthalmologists for surgical duties.

Government Vision 2030 Eye-Health Programme

The Vision 2030 Eye-Health Programme targets a 30% increase in effective cataract-surgery coverage (eCSC) and has already lifted public-hospital cataract volumes 15% year-on-year in 2024[1]World Health Organization, “World Report on Vision,” who.int. Tender documents increasingly bundle phaco machines, microscopes, and consumables with surgeon-training modules, ensuring continuous device utilization after installation. Manufacturers offering modular surgical kits suited to district-hospital theatres are winning bids in Limpopo and Eastern Cape, where less than 47% of facilities previously had adequate eye-care infrastructure. As the programme expands, suppliers anticipate multiyear delivery pipelines for intraocular lenses, phacoemulsification handpieces, and low-cost slit lamps that can withstand intermittent power.

Rapid Uptake of Femto Cataract and SMILE Lasers

Private hospitals in Gauteng and Western Cape installed 35% more femtosecond laser platforms in 2024, propelling the segment toward double-digit growth[2]European Society of Cataract and Refractive Surgeons, “Adoption Trends in FLACS,” escrs.org. Pay-per-procedure financing is proving pivotal for independent clinics that previously could not justify USD 1 million capital purchases. Patient demand is buoyed by reduced surgical energy and faster visual recovery, leading insurers to classify FLACS as a reimbursable upgrade rather than a purely elective procedure. Clinics that market combined femto cataract and SMILE refractive packages report 18% higher conversion rates among myopic patients aged 25-40, broadening the surgical funnel for premium intraocular lenses.

Expansion of Medical-Scheme Coverage

Eye-care benefits accounted for 3.1% of total scheme payouts in 2024, and new 2025 gap-cover products now reimburse premium multifocal IOLs up to ZAR 213,000 per annum. Closed schemes, which spend more per beneficiary than open schemes, negotiate volume-based discounts that shorten payback periods on diagnostic devices for network hospitals. Device manufacturers now tailor segmented product lines—economy, standard, and premium—to match the tiered benefits structure. As copayments for ophthalmology fall below optometry services, more patients bypass routine spectacles and elect for definitive surgical correction, expanding the total addressable base for surgical platforms and consumables.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited ophthalmologist density outside Gauteng & Western Cape restricts device uptake | −0.80 | Rural provinces | Long term (≥ 4 years) |

| High import duties and rand volatility inflating capital-equipment costs | −0.70 | National | Short term (≤ 2 years) |

| Delayed reimbursement approvals for new ophthalmic technologies by Council for Medical Schemes | −0.50 | Private-sector providers | Medium term (2-4 years) |

| Counterfeit low-cost lenses in informal markets undermining premium brand sales | −0.20 | Informal urban markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Limited Ophthalmologist Density Outside Gauteng & Western Cape

More than 90% of optometrists serve fewer than 16% of the population, and 85% of ophthalmologists practice in the private sector, leaving vast rural districts without specialist coverage[3]Department of Health, “Vision 2030 Eye-Health Implementation Framework,” health.gov.za. This imbalance lowers device-penetration potential by up to 80% in provinces such as Northern Cape and North West. To bridge the gap, manufacturers are developing automated autorefractors and simplified slit-lamp cameras that nurses can operate after short courses, yet uptake remains constrained by limited maintenance capacity. The hub-and-spoke teleophthalmology model alleviates workflow bottlenecks but depends on reliable broadband, which only reaches 42% of rural clinics. Consequently, suppliers must bundle solar power kits and remote diagnostics to keep devices operational.

High Import Duties and Rand Volatility

Over 70% of ophthalmic devices are imported, and the rand’s swings have widened price quotations by as much as 15% within a single tender cycle. Smaller practices defer upgrades when exchange-rate spikes lift loan repayments, prolonging replacement cycles. Multinationals such as Alcon have responded by assembling intraocular lens packs locally, trimming landed costs by 12% and cushioning public-sector budgets. Regional component sourcing is also gaining traction; one leading microscope maker expects to shift 30% of its precision-metal parts to a Durban supplier by 2027. These localization moves gradually dampen price volatility but require technology-transfer agreements and regulatory approvals that lengthen time-to-market for new models.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Vision Care Leads, Diagnostics Accelerate

The vision-care category generated 61.52% of the South Africa ophthalmic devices market in 2025, reflecting the country’s high burden of uncorrected refractive errors and the role of spectacles as the most accessible entry point to eye health. Steady retail-chain expansion into townships is broadening consumer reach, while online lens-replacement platforms lift repeat-purchase frequency. Premium daily-wear contact lenses now account for 17% of retail turnover, signaling an upgrade cycle that boosts unit margins.

The diagnostic-and-monitoring segment, forecast to compound at 7.54% through 2031, is the fastest-growing contributor to the South Africa ophthalmic devices market. OCT scanners already represent more than 24% of diagnostic sales, buoyed by diabetic-retinopathy screening mandates. Suppliers increasingly bundle AI detection software that classifies pathology with 97.3% accuracy, enabling non-ophthalmologists to triage cases quickly. Over the forecast window, a more connected public-sector procurement model will force vendors to ensure compatibility with national health-information exchanges, cementing software as a decisive tender criterion.

Surgical devices comprise a smaller but rapidly evolving slice of the South Africa ophthalmic devices market. Femto-laser platforms, MIGS implants, and hand-held phaco tips collectively anchor a high-value niche fueled by Vision 2030 cataract targets and private-sector demand for premium vision-correction options. The OMNI Surgical System, for instance, offers combined canaloplasty and trabeculotomy in a single device, reducing postoperative medication reliance and shortening national hospitalization stays. Device makers that supply both conventional and micro-invasive solutions occupy a strategic position as surgeons transition to next-generation techniques.

By Disease Indication: Cataract Dominance, Diabetic Retinopathy Momentum

Cataract products commanded 37.86% of the South Africa ophthalmic devices market share in 2025, driven by robust surgical protocols and growing government emphasis on clearing backlogs. Public-sector tender volumes surged following the 15% increase in cataract surgeries in 2024, prompting phaco-probe manufacturers to scale regional inventory hubs to prevent stock-outs.

Devices targeting diabetic retinopathy register the fastest forecast expansion at a 6.78% CAGR, powered by epidemiological pressure from rising diabetes prevalence and the national commitment to tele-enabled retinal screening. Fundus cameras designed for battery operation now penetrate mobile clinics that serve mining communities, while cloud-hosted AI graders cut reporting turnaround to under 24 hours.

The glaucoma device segment, including MIGS implants and long-acting drug-delivery stents, retains meaningful scale because chronic intraocular-pressure management demands lifelong follow-up. New micro-shunt designs that integrate with electronic health-record systems illustrate how surgical hardware and data capture are converging into a holistic disease-management proposition. Broader adoption hinges on training; workshops led by visiting glaucoma surgeons from Gauteng have doubled MIGS procedural volumes in Eastern Cape since 2023.

By End-User: Hospitals Continue to Lead, ASCs Gain Speed

Hospitals accounted for 42.09% of South Africa ophthalmic devices market revenue in 2025, thanks to comprehensive service portfolios and established referral chains who.int. Public facilities, energized by Vision 2030 funding, are refreshing aging microscopes and slit lamps after more than a decade of deferred maintenance. Private hospitals differentiate on premium technology, advertising Zeiss-based 3-D heads-up visualization and LenSx-enabled cataract suites to attract insured patients.

Ambulatory surgery centers, projected to grow at 6.62% CAGR, offer lower overheads and rapid case throughput, making them attractive partners for pay-per-click femto-laser vendors. Moreover, several ophthalmologist cooperatives have converted vacant retail space into procedure-ready outposts that perform up to 25 cataract cases daily. This model trims facility fees up to 30% below hospital tariffs, allowing schemes to authorize surgeries that would otherwise exceed benefit limits.

Specialty ophthalmic clinics in urban nodes remain innovation testbeds, often piloting AI-enabled keratometry and wavefront-guided LASIK platforms before wider diffusion. Their active social-media outreach builds consumer awareness that ultimately feeds both ASC and hospital pipelines, reinforcing the integrated-care loop that public planners envision for national eye health.

Geography Analysis

Gauteng and Western Cape provinces contributed roughly 64.58% of South Africa ophthalmic devices market revenue in 2025, an outsized share relative to their 30% population weight. This concentration reflects higher disposable incomes, dense medical-scheme penetration, and the clustering of more than 70% of active ophthalmologists in Johannesburg, Pretoria, and Cape Town. Device vendors frequently pilot new technologies in these hubs before scaling to secondary cities because proven utilization statistics streamline reimbursement negotiations.

KwaZulu-Natal and Eastern Cape are emerging focal points as provincial health departments direct Vision 2030 funds to neglected districts. Eastern Cape adults aged 35 + exhibit visual-impairment prevalence of 51% and blindness of 6.6%, chiefly from uncorrected refractive error (38%) and cataract (20%). Targeted mobile-surgery caravans, equipped with compact phaco machines and solar-charged microscopes, now host weekly outreach camps that collectively perform 1,200 cataract extractions per quarter—unlocking incremental consumables demand.

Limpopo, Northern Cape, and North West provinces illustrate the gap-closing potential—and challenges—of public investment. Fewer than 47% of Limpopo facilities possessed adequate eye-care resources in late-2024, prompting an equipment-procurement drive that prioritizes rugged slit lamps, autorefractors, and paediatric vision-screening kits. However, supply-chain hurdles—long road distances, limited cold-chain capacity for certain imaging sensors, and intermittent electricity—require vendors to redesign packaging and include off-grid power solutions. Manufacturers that address these logistical realities are gaining early-mover advantage as provincial tenders increasingly weigh lifecycle support over sticker price.

Urban townships adjoining Johannesburg, Cape Town, and Durban represent the fastest-growing vision-care retail segment. Chains that blend optometry, basic ophthalmic diagnostics, and micro-loan financing enable first-time spectacle wearers to upgrade to contact lenses within a single credit cycle. These outlets also feed referral pipelines to nearby ASCs for laser-vision-correction consultations, subtly shifting surgical volumes away from big hospitals. Teleophthalmology rollouts are further equalizing specialist access: township clinics equipped with cloud-connected fundus cameras now forward images to academic hospitals, reducing unnecessary travel and concentrating surgical referrals on cases that truly need tertiary care.

Competitive Landscape

The South Africa ophthalmic devices market remains moderately fragmented, yet the premium tier shows rising concentration around a handful of global players. Alcon, Johnson & Johnson Vision Care, and Carl Zeiss Meditec together controlled 47% of premium intraocular lens revenue in 2024, a lead they reinforce through surgeon-education programs and multimodal service bundles. Local subsidiaries invest in technical-support teams that provide same-day loaner equipment during repairs, a critical differentiator in high-volume cataract centers where downtime erodes profitability.

Regional challengers focus on cost-optimized diagnostic devices and generic consumables. A Durban-based manufacturer recently introduced a single-use phaco tip priced 22% below imported equivalents, capturing share in cash-paying segments. Although counterfeit lenses circulate in informal markets, their impact skews toward low-income spectacles rather than surgical categories; nonetheless, premium brands enforce hologram authentication and QR-code verification to preserve consumer trust.

Strategic partnerships are proliferating as manufacturers seek reimbursement traction. One leading OCT vendor secured a framework agreement with a closed medical scheme covering 280,000 lives to install devices at 14 network hospitals, funded through a per-screen fee payable from savings on late-stage retinopathy complications. Simultaneously, data-analytics alliances position device makers as population-health collaborators: Zeiss integrates anonymized imaging datasets with an academic-AI lab in Pretoria to refine glaucoma-progression algorithms, strengthening its claim in future tenders that emphasize data-science capabilities.

Despite rand volatility, multinationals view localized production as a hedge; Alcon’s assembly line for Clareon IOLs in Cape Town slashed lead times to two weeks and cut landed costs 12%, prompting Johnson & Johnson to scout Bloemfontein for a potential contact-lens blister-pack plant. Such moves signal a strategic shift from pure import dependency toward hybrid supply chains that cushion currency swings while supporting regional export ambitions into Botswana, Namibia, and Zimbabwe.

South Africa Ophthalmic Devices Industry Leaders

Alcon Inc.

Carl Zeiss Meditec AG

Johnson & Johnson Vision Care Inc.

Bausch + Lomb (Bausch Health)

Hoya Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Oculate became exclusive distributor for Sterimedix in South Africa, widening surgeon access to single-use ophthalmic cannulas and handpieces.

- April 2025: Alcon commenced local assembly of Clareon monofocal and toric IOL packs at its Cape Town facility, reducing delivery lead times for Vision 2030 tenders.

- February 2025: Zeiss Meditec and the University of Pretoria launched a glaucoma-progression AI initiative using anonymized national OCT datasets.

- December 2024: Johnson & Johnson Vision Care signed a framework agreement with Mediclinic Southern Africa to deploy TECNIS Synergy multifocal IOLs across 22 hospitals.

South Africa Ophthalmic Devices Market Report Scope

As per the scope of the report, ophthalmology is a branch of medical science that deals with structure, function, and various diseases related to the eye. Ophthalmic devices are medical equipment designed for diagnosis, surgical, and vision correction purposes. The South Africa Ophthalmic Devices Market is segmented by Devices (Surgical Devices, and Diagnostic and Monitoring Devices). The report offers the value (in USD million) for the above segments.

By Device Type

| Diagnostic & Monitoring Devices | OCT Scanners |

| Fundus & Retinal Cameras | |

| Autorefractors & Keratometers | |

| Corneal Topography Systems | |

| Ultrasound Imaging Systems | |

| Perimeters & Tonometers | |

| Other Diagnostic & Monitoring Devices | |

| Surgical Devices | Cataract Surgical Devices |

| Vitreoretinal Surgical Devices | |

| Refreactive Surgical Devices | |

| Glaucoma Surgical Devices | |

| Other Surgical Devices | |

| Vision Care Devices | Spectacles Frames & Lenses |

| Contact Lenses |

By Disease Indication

| Cataract |

| Glaucoma |

| Diabetic Retinopathy |

| Other Disease Indications |

By End-user

| Hospitals |

| Specialty Ophthalmic Clinics |

| Ambulatory Surgery Centers (ASCs) |

| Other End-users |

| By Device Type | Diagnostic & Monitoring Devices | OCT Scanners |

| Fundus & Retinal Cameras | ||

| Autorefractors & Keratometers | ||

| Corneal Topography Systems | ||

| Ultrasound Imaging Systems | ||

| Perimeters & Tonometers | ||

| Other Diagnostic & Monitoring Devices | ||

| Surgical Devices | Cataract Surgical Devices | |

| Vitreoretinal Surgical Devices | ||

| Refreactive Surgical Devices | ||

| Glaucoma Surgical Devices | ||

| Other Surgical Devices | ||

| Vision Care Devices | Spectacles Frames & Lenses | |

| Contact Lenses | ||

| By Disease Indication | Cataract | |

| Glaucoma | ||

| Diabetic Retinopathy | ||

| Other Disease Indications | ||

| By End-user | Hospitals | |

| Specialty Ophthalmic Clinics | ||

| Ambulatory Surgery Centers (ASCs) | ||

| Other End-users | ||

Key Questions Answered in the Report

What is the current value of the South Africa ophthalmic devices market?

The South Africa ophthalmic devices market is valued at USD 685.36 million in 2026 and is expected to reach USD 893.19 million by 2031.

Which segment is growing fastest in the South Africa ophthalmic devices market?

Diagnostic and monitoring devices are growing fastest, with a projected 7.54% CAGR over 2026-2031.

How is the Vision 2030 Eye-Health Programme influencing device demand?

The programme targets a 30% rise in effective cataract-surgery coverage, driving higher procurement of surgical devices and intraocular lenses.

Why are ambulatory surgery centers gaining momentum?

ASCs offer cost-efficient, high-volume procedures and are projected to grow at 6.62% CAGR over 2026-2031, supported by pay-per-procedure financing for femto-laser platforms.

What challenges limit wider adoption of ophthalmic devices in rural South Africa?

Key constraints include an 80% lower specialist coverage in rural areas and price volatility from import duties and currency fluctuations.

Page last updated on: