Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

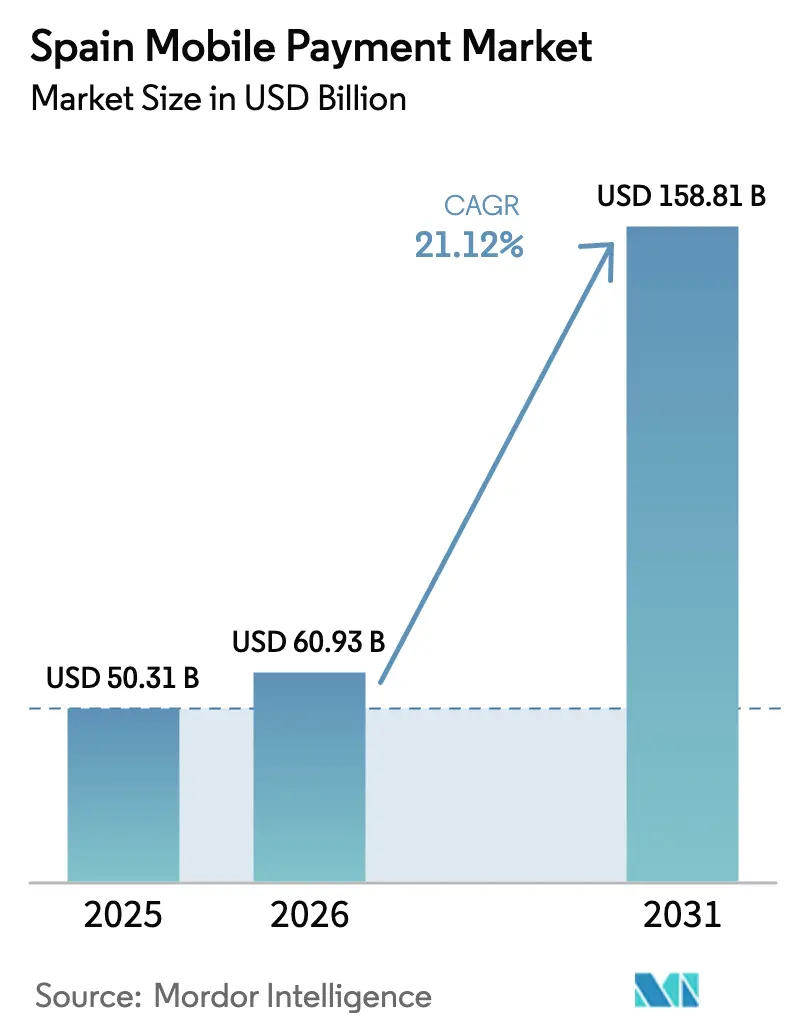

| Base Year Market Size (2025) | USD 50.31 Billion |

| Market Size (2026) | USD 60.93 Billion |

| Market Size (2031) | USD 158.81 Billion |

| Growth Rate (2026 - 2031) | 21.12% CAGR |

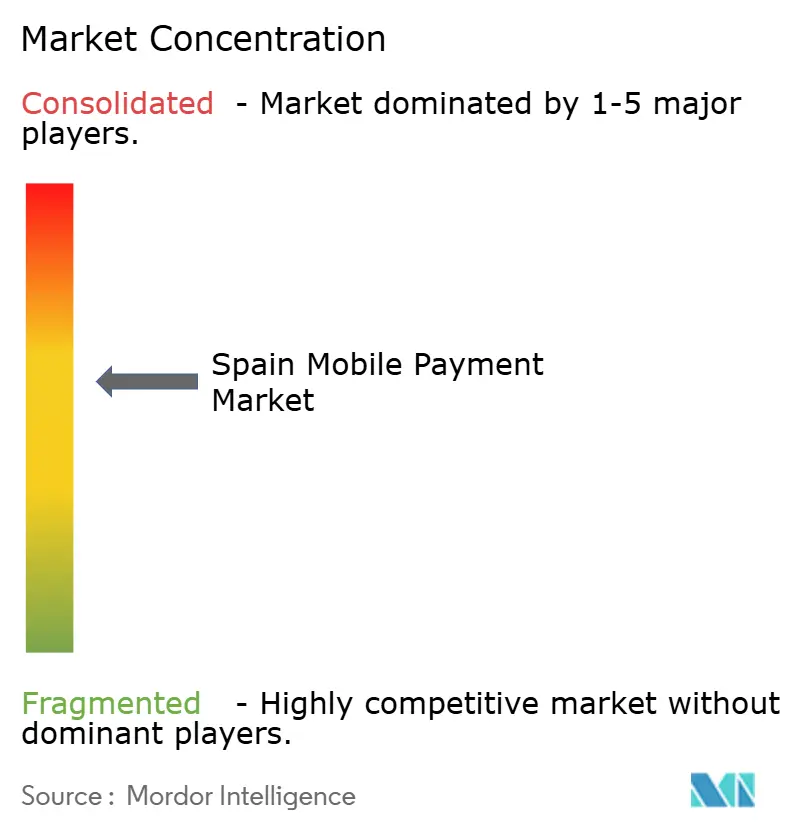

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Spain Mobile Payment Market Analysis by Mordor Intelligence

The Spain mobile payment market size is expected to grow from USD 50.31 billion in 2025 to USD 60.93 billion in 2026 and is forecast to reach USD 158.81 billion by 2031 at 21.12% CAGR over 2026-2031. The sharp growth rests on three pillars: a 43% instant-payment penetration rate that far outstrips the EU average, Iberpay’s rails that settled EUR 2.8 trillion (USD 3.08 trillion) in 2024, and Bizum’s 1.093 billion transactions that underline consumer trust in real-time account-to-account (A2A) transfers.[1]Iberpay, “Informe Anual 2024,” iberpay.com Policy tailwinds add momentum—EU instant-payment mandates now cap settlement at 10 seconds, and the European Central Bank’s (ECB) digital-euro sandbox is enrolling Spanish banks for pilot use cases. At the same time, 92.3% 5G coverage and 95.2% fiber connectivity give the ecosystem the network reliability it needs for dense transaction volumes.[2]International Trade Administration, “Spain – Digital Economy,” trade.gov Cybersecurity investments by large incumbents are mitigating fraud-loss concerns, while near-field-communication (NFC) innovation—ranging from Tap-to-Pay smartphones to wearable rings—continues to widen consumer appeal.

Key Report Takeaways

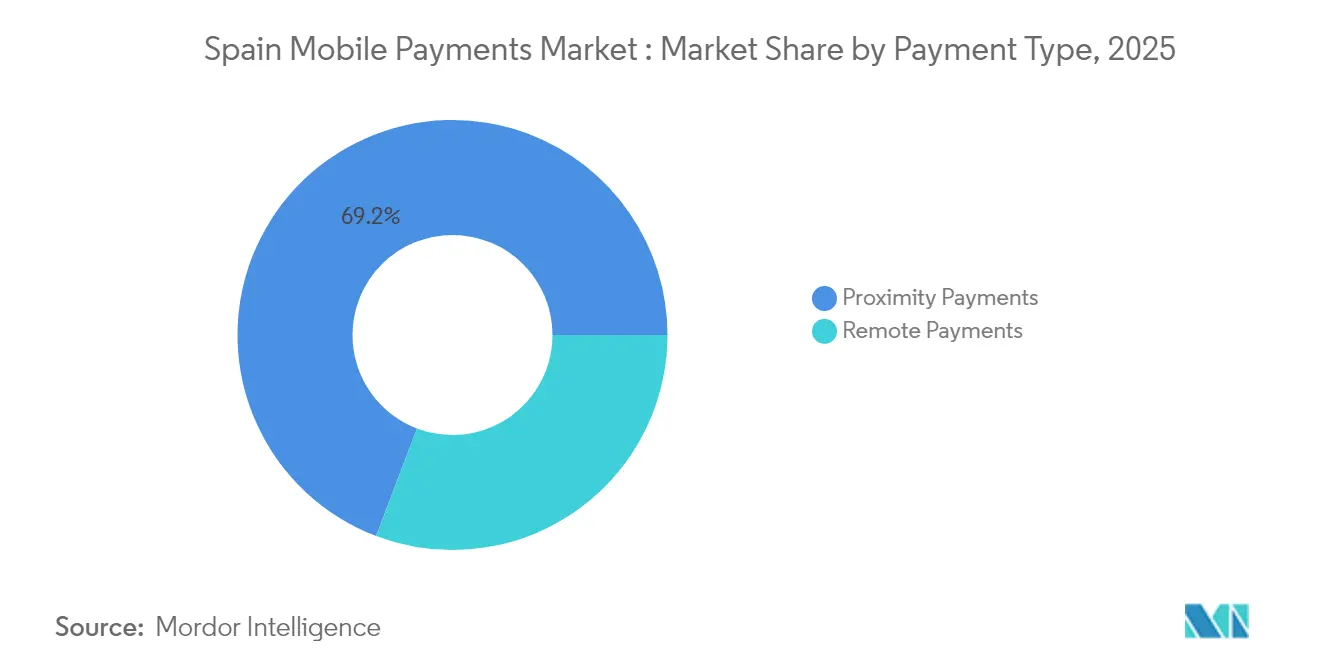

- By payment type, proximity payments led with 69.22% revenue share in 2025, whereas remote payments are forecast to expand at a 22.96% CAGR through 2031.

- By transaction type, in-store point-of-sale captured 45.34% of the Spain mobile payment market share in 2025; person-to-merchant (P2M) checkout solutions are set to rise at a 23.85% CAGR.

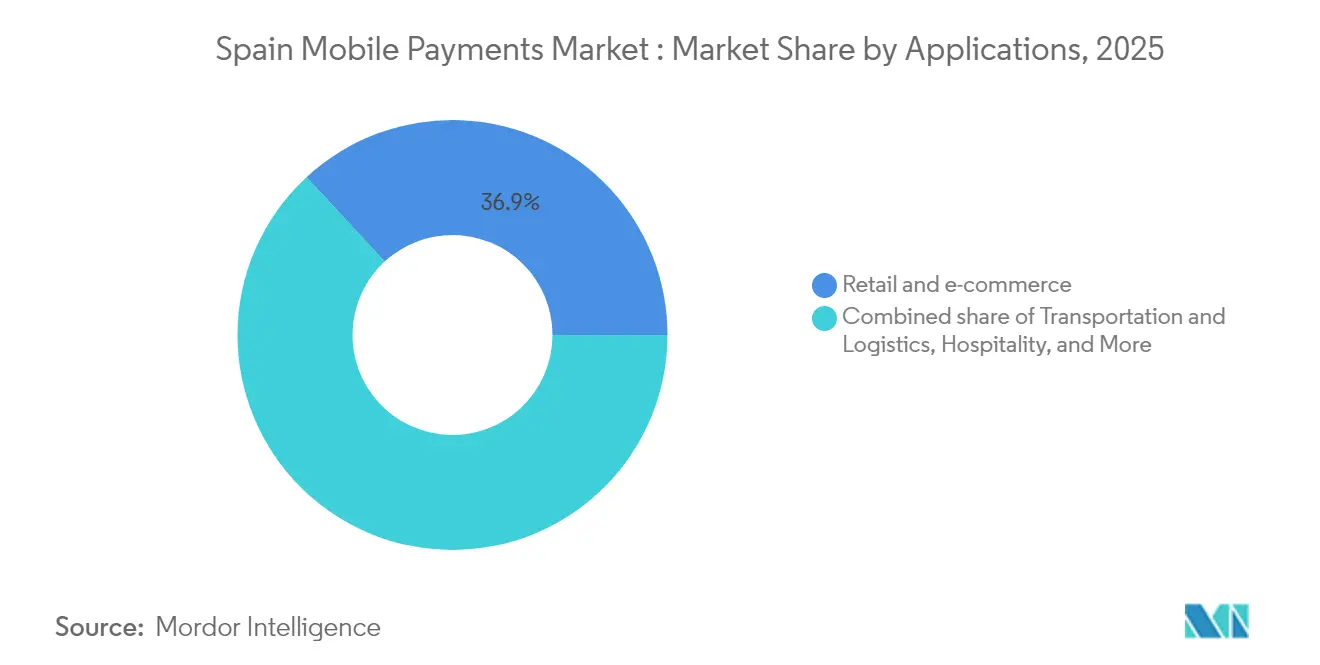

- By application, retail and e-commerce accounted for 36.88% of the Spain mobile payment market size in 2025; the government and public-sector segment is advancing at a 25.02% CAGR.

- By end-user, personal usage remained dominant at 65.12%, while the business segment is projected to log a 22.14% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Spain Mobile Payment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising smartphone & 4G/5G penetration | +4.2% | National, with urban concentration in Madrid, Barcelona, Valencia | Short term (≤ 2 years) |

| Bizum & open-banking rails scaling instant A2A payments | +6.8% | National, with spillover to Portugal, Italy, Andorra | Medium term (2-4 years) |

| Shift to contact-free payments drives the market | +3.9% | National, accelerated in hospitality and retail sectors | Short term (≤ 2 years) |

| Digital-Euro pilots to fast-track wallet interoperability | +2.1% | EU-wide, with Spain as early adopter market | Long term (≥ 4 years) |

| Mandatory-cash-acceptance law spurring POS upgrades | +1.8% | National, concentrated in retail and hospitality | Medium term (2-4 years) |

| Iberpay cross-border instant rails opening B2C payout use-cases | +2.9% | Cross-border focus: Spain-Portugal-Italy corridor | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising smartphone & 4G/5G penetration

Spain has achieved 92.3% 5G coverage and 95.2% fiber-to-the-premises reach, creating low-latency conditions that favor on-device authentication and sub-second settlement. Government funding via the España Digital 2026 plan directs 26% of NextGenerationEU capital toward connectivity, ensuring rural provinces close the digital gap. Consumer response is immediate: mobile-payment usage jumped to 50% of Spaniards in 2023 from 29.7% in 2022, a shift echoed in rising NFC-ring pilots that anonymize credentials at the point of tap. Network robustness also supports the Digital Beta Wallet, a state-backed app that layers age-verification on top of payment credentials, foreshadowing integrated identity-plus-payment wallets.[3]Government of Spain, “Digital Beta Wallet,” digital.gob.es

Bizum & open-banking rails scaling instant A2A payments

Bizum demonstrates how a bank-consortium model can out-innovate fintech disruptors. Its 17% annual volume jump in 2024 brought total operations to 1.093 billion, while online purchases soared to EUR 3.107 billion (USD 3.42 billion).[4]Bizum, “Bizum alcanza los 1.100 millones de operaciones en 2024,” elespanol.com PSD2 open-banking APIs let third-party providers plug directly into 186 domestic and foreign institutions, trimming card-network fees and enabling immediate settlement. The 2025 EuroPA launch extends Bizum to Portugal, Italy, and Andorra, giving merchants a cross-border customer base of 50 million without additional integration. Merchant uptake shows 56% growth to 82,000 retail points, cementing Bizum as Spain’s de-facto A2A standard.

Shift to contact-free payments drives the market

Hospitality venues report that 66% of patrons now prefer mobile settlement, and 82% of tourists demand contactless options during peak season. Bars and nightlife spending climbed at a 15.6% CAGR in 2024, a trend fueled by Tap-to-Pay rollouts that remove the need for PIN pads. The Madrid Virtual Transport Card processed 588,500 trips in pilot phase, validating consumer readiness for hardware-less NFC services. QR and Pay-by-Link workflows offer a bridge between physical and online retail, while AI-vision checkout kiosks reduce transaction time and labor cost in supermarkets.

Digital-euro pilots to fast-track wallet interoperability

The ECB’s 70-participant innovation platform is stress-testing programmable money features—conditional disbursement, offline transfer, and privacy tiers—with Spanish banks in the first cohort. Academic modeling suggests 32.29% of Spanish depositors could shift up to 5.57% of household balances into digital euros, altering bank funding mixes but opening new transaction rails. Because the CBDC is by design mobile-first, existing wallet providers must upgrade to pan-EU interoperability standards sooner, catalyzing back-end harmonization. Spain’s instant-payment proficiency offers a blueprint for the ECB on fraud mitigation and real-time reconciliation, accelerating continental rollout.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fraud & data-security concerns | -2.8% | National, with higher impact in urban areas | Short term (≤ 2 years) |

| Legacy card-fee economics slowing merchant adoption | -1.9% | National, concentrated in SME segment | Medium term (2-4 years) |

| Ageing cash-oriented population & legal right-to-cash | -1.4% | Rural areas and elderly demographics | Long term (≥ 4 years) |

| Single aggregator (Redsys) bottlenecks open-API quality | -1.1% | National payment processing infrastructure | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fraud & data-security concerns

Spain logged over 96,000 cybersecurity incidents in 2024, a 15% rise that hit financial services disproportionately. High-profile leaks such as the Air Europa breach keep risk perception elevated. The ECB’s fraud-prevention taskforce now recommends real-time data-sharing and biometric authentication, compelling providers to add cost-intensive defenses. SMEs are especially exposed; 22,000 cyber incidents in 2023 hit freelancers and micro-firms, with one-third related to online fraud. This threat matrix slows onboarding for merchants that lack the budget for multilayer defense.

Legacy card-fee economics slowing merchant adoption

Spain’s anti-fraud law caps professional cash payments at EUR 1,000 (USD 1142.04), nudging merchants toward electronic acceptance, yet interchange fees remain stubbornly high for small retailers. Redsys processes the lion’s share of card traffic, and its single-hub status means API enhancements move at a pace set by one vendor, creating a bottleneck. Consumer research shows 67% of Spaniards rank security above speed, so merchants must fund premium fraud filters to win trust—another cost hurdle. Although the EU’s instant-payment regulation bans extra fees for 10-second transfers, its staging timeline allows entrenched fee structures to persist for several quarters, delaying ROI on mobile-payment upgrades.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Payment Type: Proximity Growth Faces Remote Surge

Proximity transactions held 69.22% of the Spain mobile payment market in 2025, an edge built on ubiquitous NFC-capable terminals and consumer familiarity at grocery checkouts. Remote payments, however, are accelerating at a 22.96% CAGR, buoyed by Bizum’s online-checkout plugin, which doubled e-commerce volumes to EUR 3.107 billion (USD 3.42 billion) in 2024. Madrid’s Virtual Transport Card illustrates how proximity modes keep innovating, recording 588,500 test rides without physical passes.

Remote-payment momentum stems from cross-border interoperability: Bizum’s EuroPA link will let 50 million users send instant transfers beyond Spain. Parallel innovations in Pay-by-Link and QR codes blur the boundary between remote and in-person transactions, enabling merchants to reconcile both flows in one ledger. While proximity volumes dominate, remote payments rewrite the unit-economics calculus by slashing interchange, putting card networks under margin pressure. This dual-track dynamic ensures both modes expand but at varied trajectories, shaping gateway and processor roadmaps through 2031.

By Transaction Type: POS Resilience Meets P2M Innovation

In-store POS still commands 45.34% of the Spain mobile payment market in 2025, thanks to retailer investment in contactless terminals and integrated loyalty apps. Person-to-merchant (P2M) checkouts, however, top the growth chart at a 23.85% CAGR. Bizum’s merchant base rose 56% to 82,000 locations, demonstrating that A2A rails can undercut card fees for micro-ticket sales. Peer-to-peer flows remain a stable pillar: Bizum captured 95% of domestic P2P volume with 1.093 billion transfers in 2024.

AI-vision checkout and Tap-to-Phone services are reshaping queue management by converting consumer handsets into POS devices, a boon for pop-up retail. Cross-border P2M capabilities from the EuroPA launch unlock Italian and Portuguese shoppers for Spanish e-tailers at domestic fee rates, redefining addressable revenue pools. Meanwhile, POS-network providers must invest in real-time fraud scoring to keep pace with instant-settlement expectations, prompting consolidation among independent service operators.

By Application: Retail Leadership Meets Government Acceleration

Retail and e-commerce represented 36.88% of the Spain mobile payment market size in 2025, translating into superior checkout-conversion rates and basket-value lifts for omni-channel merchants. Government and public-sector wallets are on a steeper 25.02% CAGR slope, propelled by EUR 1.6 billion (USD 1.76 billion) in subsidies earmarked for digital ticketing in 2025. Madrid’s account-based ticketing system—and its upcoming expansion to iOS and monthly passes—validates the scale potential of civic applications.

Hospitality ranks next in wallet adoption as tourists demand touch-free interactions; nightly bar spend rose at 15.6% CAGR, a cash-replacement storyline embraced by city tourism boards. Health-care and education remain nascent but will benefit from the Digital-Spain 2026 blueprint, which funds biometric ID integration for hospital check-ins and school meal plans. The Digital Beta Wallet’s age-verification feature showcases cross-domain utility, weaving payments and digital identity into a single UX.

By End-User: Personal Dominance Anchors Business Upside

Personal accounts contributed 65.12% of the Spain mobile payment market in 2025, underpinned by epayment literacy and 72% European wallet penetration. Business end-users, however, post a 22.14% CAGR, accelerated by regulatory ceilings on cash transactions and the tax office’s e-invoice mandate for SMEs. The BBVA-Sabadell merger adds EUR 5 billion (USD 5.5 billion) in annual lending headroom that can be channeled into working-capital lines tied to integrated payment suites.

SMEs flock to Pay-by-Link and Tap-to-Pay because they eliminate hardware capex and shorten settlement cycles vis-à-vis card rails. Bizum enabled 1 million charitable donations worth EUR 49.2 million in 2024, illustrating product versatility beyond P2P. As digital-euro integration looms, corporates are requesting wallet solutions that can toggle between commercial bank money and CBDC, spurring treasury-software updates.

Geography Analysis

Spain outperforms the broader EU on real-time adoption, processing 43% of all domestic transactions as instant settlements in 2025. Iberpay links 99% of the country’s financial institutions and cleared 3.185 billion payments last year, cementing a national backbone for user-friendly A2A experiences. Urban centers multiply the effect: Madrid’s Virtual Transport Card pilot recorded 588,500 trips, while Barcelona and Valencia gear up for similar NFC wallets, signaling network effects across large metro areas.

Regional disparities persist. Rural provinces, home to an ageing demographic, still rely heavily on cash despite the EUR 1,000 threshold on professional cash usage. Digital-Spain 2026 dedicates fiber and 5G subsidies to these zones, aiming to push coverage beyond today’s 92.3% level. Island territories such as the Balearics are early testers of QR-code fare collection for ferries, illustrating how tourism corridors experiment with lightweight solutions.

Cross-border momentum elevates Spain to gateway status for southern Europe. Bizum’s 2025 extension to Portugal, Italy, and Andorra enables the first multi-country instant-payment corridor at scale. Spanish banks are pilot nodes in the ECB’s digital-euro sandbox, adding to the country’s reputational edge in payments R&D. This geographic synergy pulls inbound fintech investment and positions Spanish processors to license out their fraud-analytics IP across the eurozone

Competitive Landscape

Traditional banks anchor the ecosystem by controlling core settlement rails, yet fintech challengers spur rapid product cycles. The Spain mobile payment market therefore displays a “co-opetition” model: Bizum’s banking consortium shares APIs across rival institutions, generating network effects that single-player apps struggle to match. Strategic emphasis has shifted to embedded payments—CaixaBank’s 70.5% digital-client ratio enables in-app micro-loans that settle via mobile wallets in seconds.

The approved BBVA-Sabadell merger changes the leaderboard by creating Spain’s second-largest lender, consolidating product budgets for AI-fraud suites and multi-rail wallets. CaixaBank and Santander counterbalance through partnerships: Santander’s stablecoin pilot under MiCA aims to offer corporate treasurers on-chain settlement, while CaixaBank co-develops Request-to-Pay flows with BBVA for B2B invoices.

Technology suppliers occupy a crucial tier. Redsys remains the dominant processor, but open-banking aggregators such as PPRO and Paycomet differentiate via merchant-specific analytics. Patent filings—2,111 in 2023—show a tilt toward automated tolling and IoT micro-payments, reinforcing Spain’s reputation for applied payments engineering. As regulatory compliance costs rise—MiCA for crypto and instant-payment mandates for banks—scale economics increasingly favor incumbents, implying further consolidation in processing and gateway niches.

Spain Mobile Payment Industry Leaders

PayPal Holdings, Inc.

Apple Inc.

Google LLC

CaixaBank S.A.

Banco Bilbao Vizcaya Argentaria S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: EU Instant Payments Regulation entered force, mandating fee-free 10-second transfers, thereby raising baseline expectations for Spanish bank apps.

- May 2025: The ECB’s innovation platform admitted 70 market actors—including Spanish banks—to prototype digital-euro functionalities such as conditional payments.

- April 2025: The CNMC cleared BBVA’s takeover of Banco Sabadell, creating a EUR 5 billion (USD 5.5 billion) annual lending boost while obliging the merged bank to preserve SME service levels.

- April 2025: Bizum launched cross-border transfers to Portugal, Italy, and Andorra under the EuroPA umbrella, linking 50 million users across 186 institutions and giving merchants cost-neutral access to foreign customers.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines Spain's mobile payment market as the total annual value of transactions that consumers or businesses authorize through a smartphone, smartwatch, or tablet via bank apps, native wallets, QR, or NFC, whether the payment is completed in-store, online, or peer-to-peer.

Scope exclusion: Card transactions begun on a mobile device but finalized on a fixed-line POS without mobile credentials are not counted.

Segmentation Overview

- By Payment Type

- Proximity Payments

- Remote Payments

- By Transaction Type

- Peer-to-Peer (P2P)

- In-store Point-of-Sale (POS)

- Person-to-Merchant (P2M/Checkout)

- Other Transaction Types

- By Application

- Retail and eCommerce

- Transportation and Logistics

- Hospitality and Food-Service

- Government and Public Sector

- Other Applications (Education, Healthcare)

- By End-user

- Personal

- Business

Detailed Research Methodology and Data Validation

Primary Research

We interview issuing banks, acquirers, telecom operators, and omni-channel retailers across Madrid, Barcelona, Valencia, and Bilbao to verify user penetration, average ticket sizes, and merchant acceptance rates. Targeted surveys with fintech founders clarify pricing spreads and promotional burn.

Desk Research

Mordor analysts first harvest foundational indicators from Banco de España payment statistics, Eurostat's Digital Economy Survey, ECB SEPA-Instant files, AEB trade briefs, CNMC e-commerce reports, and shipment-level smartphone import logs. Company 10-Ks, investor decks, and press releases add adoption ratios, while Dow Jones Factiva and D&B Hoovers enrich firm-level revenues. These sources are illustrative rather than exhaustive, with many other datasets consulted for validation.

Market-Sizing & Forecasting

A top-down build starts with total electronic payments from Banco de España, from which we isolate mobile's share using penetration rates confirmed in interviews. Selective bottom-up checks, Bizum volumes, wallet user counts, and sampled average spend calibrate totals. Key variables include smartphone penetration, contactless POS density, Bizum active users, e-commerce turnover, and mean ticket value. Forecasts to 2030 employ multivariate regression on these drivers, with scenario bands for regulatory or macro shocks.

Data Validation & Update Cycle

Outputs clear automated variance screens, senior analyst peer review, and a pre-publish refresh. We revisit the model quarterly for material events; otherwise, the full update is annual.

Why Mordor's Spain Mobile Payment Baseline Commands Reliability

Published estimates often diverge because firms mix scopes, currencies, and refresh cadences. Primary gaps stem from treatment of P2P transfers, refund netting, and exchange-rate choices.

Mordor converts euro totals at the average ECB 2025 rate and removes double-count reversals, steps many publishers skip.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 50.31 B (2025) | Mordor Intelligence | - |

| USD 42.89 B (2024) | Regional Consultancy A | Excludes in-app P2P; fixed 2023 FX |

| USD 1.00 B (2023) | Industry Association B | Tracks merchant fees only |

| USD 500 B (2022) | Trade Journal C | Applies global wallet ratio to Spain |

The comparison shows that Mordor's disciplined scope selection, driver-based model, and frequent refresh deliver a balanced, transparent baseline that decision-makers can trust and replicate.

Key Questions Answered in the Report

What is the current Spain mobile payment market value?

The market stands at USD 60.93 billion in 2026 and is forecast to reach USD 158.81 billion by 2031 at a 21.12% CAGR.

How fast are remote payments growing versus proximity payments?

Remote payments are projected to expand at a 22.96% CAGR, whereas proximity payments remain the volume leader with 69.22% share.

Which segment holds the largest Spain mobile payment market size?

Retail and e-commerce lead with 36.88% share, reflecting strong card-to-wallet migration and omnichannel adoption.

What is driving government adoption of mobile payments?

EUR 1.6 billion (USD 1.76 billion) in transport subsidies and the Digital Beta Wallet initiative are fueling 25.02% CAGR growth in public-sector applications.

How will the digital euro affect local providers?

Spanish banks in the ECB sandbox get early exposure to wallet interoperability standards, but they must adapt to potential deposit flight into CBDC holdings.

What are the top cybersecurity challenges?

A 15% year-on-year rise in cyber incidents—96,000 cases in 2024—reinforces the need for biometric authentication and AI-driven fraud analytics across all payment apps.

Page last updated on: