Cell Dissociation Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 0.7 Billion |

| Market Size (2031) | USD 1.41 Billion |

| Growth Rate (2026 - 2031) | 14.96% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

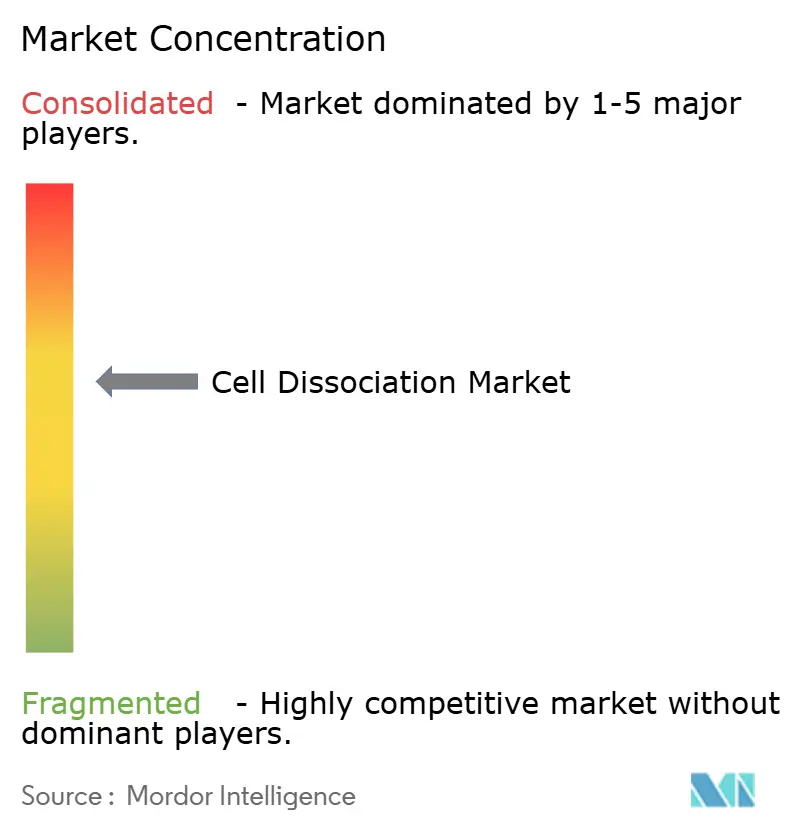

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cell Dissociation Market Analysis by Mordor Intelligence

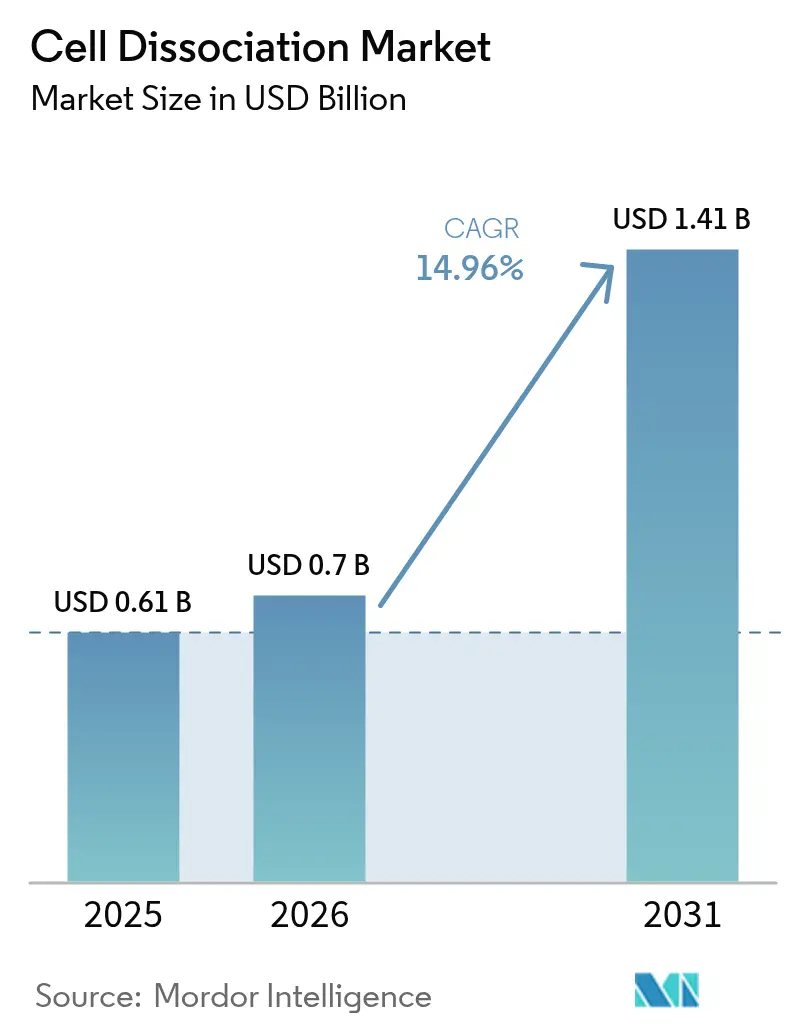

The cell dissociation market size was valued at USD 0.61 billion in 2025 and estimated to grow from USD 0.7 billion in 2026 to reach USD 1.41 billion by 2031, at a CAGR of 14.96% during the forecast period (2026-2031). The market’s ascent is tied to its enabling role in cell and gene therapy production, single-cell omics, and personalized-medicine pipelines. Regulatory approvals for advanced therapies, automation breakthroughs, and large-scale public biotechnology funding collectively accelerate adoption. Pharmaceutical and biotechnology firms remain the primary purchasers, yet contract research organizations (CROs) capture rising share as sponsors outsource complex tasks. North America keeps the lead owing to established infrastructure, while Asia-Pacific posts the fastest growth backed by multibillion-dollar national programs in China, Japan, and India.

Key Report Takeaways

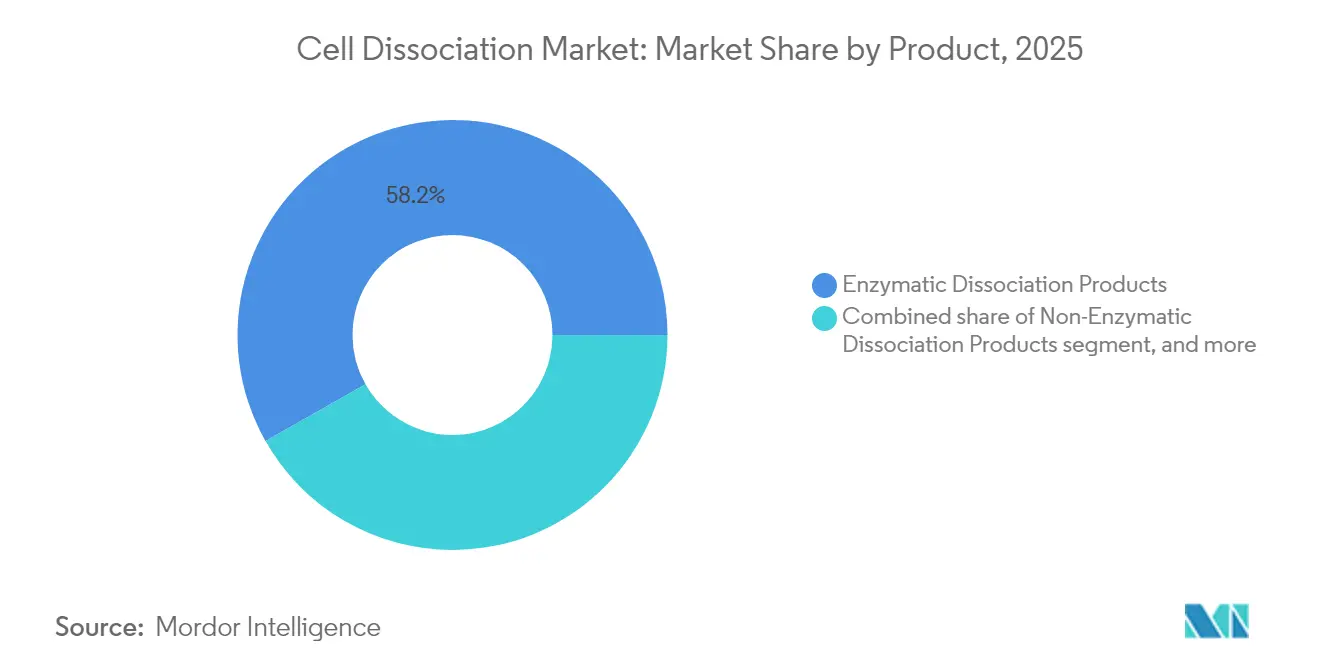

- By product category, enzymatic reagents led with 58.21% of cell dissociation market share in 2025, whereas non-enzymatic products are projected to expand at 17.08% CAGR through 2031.

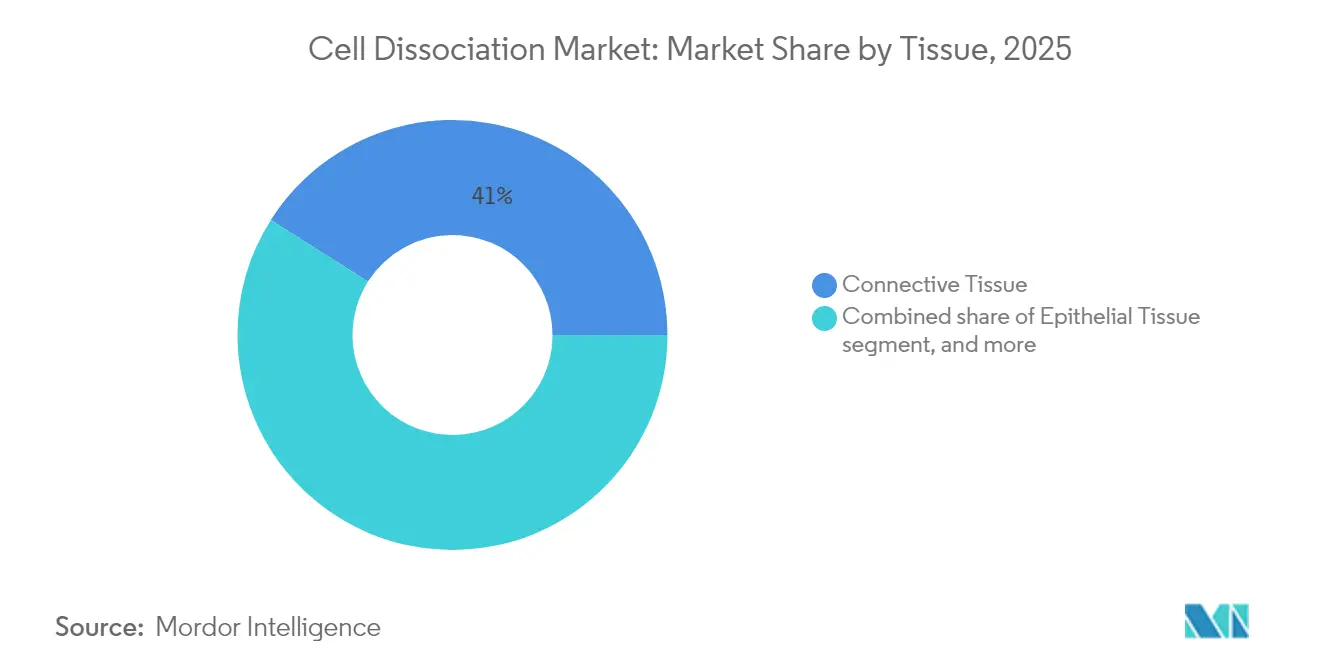

- By tissue type, connective tissue commanded 41.02% of cell dissociation market size in 2025; tumor and organoid applications advance at 17.32% CAGR to 2031.

- By end-user, pharmaceutical and biotechnology companies held 46.18% of cell dissociation market size in 2025, while CROs register the highest 17.85% CAGR through 2031.

- By geography, North America accounted for 38.32% of cell dissociation market share in 2025, whereas Asia-Pacific is forecast to post a 16.21% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cell Dissociation Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of cell and gene therapy pipelines | +3.2% | North America & Europe | Medium term (2-4 years) |

| Rising adoption of single-cell omics technologies | +2.8% | North America & Asia-Pacific | Short term (≤2 years) |

| Surge in biomanufacturing for personalized medicine | +2.1% | North America & EU | Long term (≥4 years) |

| Growing investments in regenerative medicine research | +1.9% | Global with APAC acceleration | Medium term (2-4 years) |

| Increasing demand for high-throughput automation | +1.7% | North America & EU | Short term (≤2 years) |

| Government initiatives to strengthen biotechnology infrastructure | +1.5% | Asia-Pacific & Middle East-Africa | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Expansion of Cell and Gene Therapy Pipelines

Seven cell and gene therapies secured FDA approval in 2024, and the agency expects 10-20 clearances annually through 2025[1]International Society for Cell & Gene Therapy, “Cell and Gene Therapy Approvals 2024,” isctglobal.org. Each product requires sophisticated cell-isolation protocols, elevating demand for automated dissociation platforms that can cut lot-release costs by 50%. Solid-tumor and autoimmune programs diversify tissue inputs, intensifying reagent-quality and scalability requirements. Allogeneic formats further raise batch volumes per donor, underscoring the need for standardized, GMP-grade workflow.

Rising Adoption of Single-Cell Omics Technologies

Microfluidic chips now process upward of 100,000 cells per run, a step-change from prior capacities. To preserve RNA integrity, new FixNCut protocols enable reversible tissue fixation before dissociation, easing sample transport without data loss. Oncology applications dominate demand as heterogeneity studies rely on high-viability single-cell suspensions. AI-augmented pipelines intensify the push for standardized protocols that minimize variability.

Surge in Biomanufacturing for Personalized Medicine

Patient-derived organoids reach a 62% establishment success rate and predict effective therapies in 91% of pancreatic-cancer cases. Hospitals pursuing point-of-care manufacturing seek compact, closed-system dissociators fit for Grade C cleanrooms. FDA guidance on animal-derived materials heightens scrutiny of reagent provenance, steering buyers toward well-documented suppliers.

Increasing Demand for High-Throughput Automation

Surface-acoustic-wave devices yield label-free, high-compatibility micromixing that preserves fragile cells. Sartorius’ CellCelector Flex integrates imaging and gentle dissociation to accelerate clone selection for GMP lines. BD and Biosero have robot-ready flow cytometers that streamline screening workflows.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of advanced dissociation technologies | -2.1% | Global, stronger in emerging markets | Medium term (2-4 years) |

| Variability and standardization challenges | -1.8% | Global, impacts scalable manufacturing | Short term (≤2 years) |

| Stringent regulatory and validation requirements | -1.6% | North America, EU & high-regulation markets | Medium term (2-4 years) |

| Limited availability of GMP-grade enzymes | -1.5% | Global, acute in Asia-Pacific & Latin America | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

High Cost of Advanced Dissociation Technologies

Closed, fully automated suites frequently exceed USD 1 million, limiting adoption among smaller labs. The global pancreatic-enzyme shortage further inflates raw-material costs and delivery times. China’s CAR-T landscape shows how high production costs can shift most payments out-of-pocket.

Variability and Standardization Challenges

Donor-derived variability complicates automation, demanding custom protocols that resist harmonization. The European Pharmacopoeia Commission’s new monograph sets stricter QC for cell-based products, yet cross-application compliance remains complex. Transitioning manual steps to robots requires extensive bridging studies that slow time-to-market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Non-Enzymatic Solutions Drive Innovation

Enzymatic reagents retained 58.21% share in 2025, with bacterial collagenase from Clostridium histolyticum prized for specificity. Trypsin dominates routine passaging, while dispase and elastase service niche applications. Non-enzymatic formulations post the fastest 17.08% CAGR as single-cell workflows shy away from protease exposure. ATCC’s chelator-based solution and recombinant TrypLE exemplify this regulatory-friendly shift. Automated tissue dissociators now come bundled with reagent cartridges to minimize operator variability.

By Tissue: Tumor Applications Lead Growth

Connective tissue captured 41.02% of market share in 2025 thanks to well-standardized collagenase protocols across liver and lung studies. Tumor and organoid samples log the highest 17.32% CAGR, with electric-field-assisted workflows achieving 95% tissue dissociation in under five minutes while maintaining viability. Mouse mammary tumor methods now reach 90% viable cell recovery for single-cell transcriptomic analysis.

By End-User: CROs Experience Rapid Expansion

Pharmaceutical and biotech firms retained 46.18% market share in 2025 but CROs rise fastest at 17.85% CAGR thanks to capacity constraints at large sponsors. Contract manufacturing held 67.13% of the USD 9.95 billion 2023 cell-and-gene-therapy production market, highlighting outsourcing momentum. Charles River’s acquisition of Cognate BioServices typifies vertical integration of development and GMP supply.

Geography Analysis

North America held 38.32% of market share in 2025, buoyed by FDA fast-track pathways for advanced therapies. New York’s USD 430 million BioGenesis Park adds 1,530 jobs and new GMP suites. Canada’s USD 22.5 million investment in STEMCELL Technologies ensures domestic reagent capacity. Sartorius and Siemens collaborate on digital-twin automation that trims lot-release time.

Asia-Pacific advances at 16.21% CAGR, led by China’s USD 4.17 billion biopark program. Japan’s Startup Development Five-Year Plan and aging-society needs push biotech growth toward ¥15 trillion by 2030. India’s BioE3 policy aims to position local CDMOs as global suppliers in anticipation of supply-chain diversification from U.S. Biosecure Act compliance.

Europe benefits from the EU biotechnology strategy targeting greater participation in the EUR 720 billion global market. EMA guidelines for cell-based products and new European Pharmacopoeia QC chapters provide regulatory clarity. Lonza’s Dutch plant produces CASGEVY for Vertex, underscoring Europe’s relevance as a high-volume contract-manufacturing hub.

Regulatory Landscape

Cell dissociation reagents and instruments used in regulated cell and gene therapy workflows are largely positioned as ancillary or processing materials within the Chemistry, Manufacturing, and Controls (CMC) framework, rather than as standalone therapeutic products. Sponsors are typically required to describe and justify mechanical or enzymatic dissociation steps in their CMC packages, including controls for residuals and impacts on critical quality attributes. This drives demand for traceable, well-characterized materials (for example, recombinant or animal-origin-free enzymes) and standardized documentation such as certificate of analysis, origin statements, stability data, and impurities profiling.

Across major markets, regulators converge on GMP-aligned quality systems and risk management for biologically sourced materials, including viral safety considerations and TSE/BSE-related controls where applicable. In Europe, EudraLex Volume 4 GMP specific to ATMPs, along with EMA guidance for gene therapy and investigational ATMPs, influences how dissociation reagents are qualified and how process changes are validated. That, in turn, reinforces the need for consistent batch-to-batch performance and structured change-control. Suppliers often align with recognized excipient-quality frameworks such as IPEC GMP and EXCiPACT to support customer qualification and auditing requirements in clinical and commercial manufacturing environments.

Competitive Landscape

Thermo Fisher Scientific dominates through broad reagent lines and plans USD 40-50 billion in acquisitions targeting complementary technologies. BD will spin off its Biosciences and Diagnostics arm into a USD 3.4 billion life-science tools specialist to sharpen focus on growth areas. Sartorius’ CellCelector Flex and Siemens’ digital-twin automation deliver end-to-end solutions that minimize labor and increase consistency. Miltenyi Biotec leverages MACS technology to enable point-of-care manufacturing at hospital sites. Enzyme suppliers lock in long-term contracts to hedge against shortages, while microfluidic start-ups launch chip-based dissociators aimed at single-cell labs.

Cell Dissociation Industry Leaders

Thermo Fisher Scientific, Inc.

Becton, Dickinson And Company

Merck KGaA

Miltenyi Biotec

STEMCELL Technologies

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Automation and standardization in front-end tissue processing remain a clear whitespace area as single-cell omics and translational programs push labs to produce reproducible, high-viability single-cell suspensions across variable tissues. A specific signal is STEMCELL Technologies' commercial launch of the STEMprep Tissue Dissociator System in June 2025, which points to ongoing demand for benchtop automation that reduces operator variability and supports higher throughput in cancer and immunology research.

Process and reagent selection increasingly affects regulatory readiness, opening room for GMP-grade, well-documented dissociation enzymes and closed, workflow-integrated consumables that simplify qualification for cell therapy programs where dissociation steps must be described in CMC. Non-contact and gentler dissociation approaches also offer a technical pathway for rare-cell and tumor applications, supported by published demonstrations such as Hypersonic Levitation and Spinning (HLS) reporting 92.3% cell viability in renal cancer tissue. In parallel, formalized standards for single-cell workflows are moving forward, including ISO/CD 25383 reaching Committee Draft stage in October 2025, which supports demand for harmonized sample-prep protocols and traceable reagents to reduce cross-site variability.

Recent Industry Developments

- May 2026: Thermo Fisher Scientific unveiled an integrated platform to advance scalable cell therapy manufacturing, including the Gibco CTS DynaXS Single Use Bioreactor for cGMP-ready cell expansion. This reinforces ongoing demand for standardized upstream cell-processing workflows in which dissociation and expansion steps perform consistently at scale.

- October 2025: BD and Opentrons announced a multi-year collaboration to integrate robotics with BD single-cell multiomics workflows. The collaboration supports more automated, repeatable sample preparation and handling, which raises expectations for dissociation reagents and accessories compatible with robotic and high-throughput lab operations.

- December 2024: Thermo Fisher Scientific launched CTS Detachable Dynabeads CD4 and CTS Detachable Dynabeads CD8 to support cell therapy development and production. By expanding upstream cell-processing options for clinically oriented workflows, the launch supports broader adoption of end-to-end, qualification-friendly consumables adjacent to tissue processing and dissociation steps.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the cell dissociation market covers purchased products and tools used to detach adherent cells or break tissue into viable single cell suspensions for downstream lab and bioprocess workflows. Revenue is counted at the supplier selling price and reflects routine procurement by research and biomanufacturing users.

Scope exclusions: Excludes basal culture media sold separately, general lab plastics, and single-cell analysis hardware that sits downstream of the dissociation step.

Segmentation Overview

- By Product

- Enzymatic Dissociation Products

- Collagenase

- Trypsin

- Papain

- Dispase

- Elastase & Hyaluronidase

- Non-Enzymatic Dissociation Products

- Chelating Agents

- Recombinant Enzyme-Free Solutions (Accutase, TrypLE)

- Mechanical Dissociation Kits & Filters

- Instruments & Accessories

- Automated Tissue Dissociators

- Microfluidic Dissociation Devices

- Cell Strainers & Filtration Units

- Consumable Accessories (Tubes, Rotors)

- Enzymatic Dissociation Products

- By Tissue

- Connective Tissue

- Epithelial Tissue

- Muscular Tissue

- Nervous Tissue

- Tumor & Organoid Samples

- By End-User

- Pharmaceutical & Biotechnology Companies

- Research & Academic Institutes

- Contract Research Organizations

- Hospitals & Diagnostic Laboratories

- Other End-Users

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work was used to set the market boundaries, map demand pools, and build the first round of assumptions before the numbers were stress tested. We relied on public and official sources such as the NIH and other government grant databases, the US FDA database for cell therapy and biologics filings, the World Health Organization health statistics, and OECD science and innovation indicators. To keep the demand story grounded, we also referred to peer reviewed articles describing tissue dissociation protocols and adoption in single cell workflows, along with association and university core facility pages that describe typical lab practices.

On the supply side, company annual reports, investor decks, product catalogs, and regulatory and quality disclosures were reviewed to understand pricing bands and product mix at a high level. Select paid subscriptions were used only for company financials, patent searches, and tracking major contracts and tenders linked to lab automation purchases. This desk list is illustrative, and other public sources were used for cross checks and clarification during the research process.

Primary Interviews and Surveys

Primary work focused on validating what gets purchased, how frequently it gets replenished, and where price realization differs by region and end user. We spoke with a mix of reagent suppliers, instrument-focused teams, distributors, and lab managers across Americas, EMEA, and APAC so assumptions from desk research could be corrected and then triangulated with real buying behavior.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 38% | CXOs: 15% | APAC: 40% |

| Mid tier: 44% | Functional/Unit leaders: 38% | EMEA: 36% |

| Smaller Players: 18% | Managers: 47% | Americas: 24% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where research activity and bioprocess scale signals are converted into a dissociation demand pool, then filtered by typical usage rates and average selling prices. The model leans on variables such as funded life science project volumes, the number of active cell and gene therapy pipelines, growth in single cell experiment throughput, typical dissociation reagent consumption per run, and the installed base trend for tissue dissociation instruments. When public data is reported in different units, conversions are kept simple and cross checked with interview feedback so the math stays reproducible.

To avoid over-reliance on any one indicator, totals are corroborated with selective bottom-up approximations, including sampled supplier portfolio checks (volume times price bands) and channel-level feedback on replenishment cycles. When product mix data is missing, gaps are handled by using conservative mix splits supported by expert inputs, then stress tested against import-export signals and patent activity direction where relevant. Forecasts are developed using scenario analysis around research funding momentum and therapy commercialization pace, and then refined with an ARIMA-based time series check so the final curve remains realistic for a procurement-led market.

Data Validation & Update Cycle

Before finalizing the numbers, outputs are compared against independent signals such as regional research spend direction, publication and protocol adoption trends, and instrument shipment commentary from public disclosures. Variance checks are run by region and product type so any sharp jumps can be traced back to a specific input change, then reviewed in a second analyst pass. If a large mismatch shows up, interviews are revisited and assumptions are adjusted only after supporting evidence is clear.

Reports are refreshed annually, and interim updates are triggered when material events occur, such as major regulatory moves, a step change in funding, or pricing shifts tied to supply constraints. Right before delivery, the model is rechecked with the latest public releases so clients receive an up-to-date view.

Mordor Intelligence's Cell Dissociation Market Size Measured Against Other Published Estimates

Published market sizes for cell dissociation often vary, and the spread is usually not random. Differences tend to come from what gets counted as dissociation spend, which year is treated as the anchor, and how quickly pricing and adoption assumptions are refreshed.

Single-cell sequencing and analysis instruments are a frequent add-on in some estimates, and that expands totals beyond the dissociation step. Even so, those platforms are outside Mordor Intelligence's scope for this market. Other gaps come from whether in-house prepared buffers are treated as market revenue, how instrument sales are split between dedicated dissociation systems and broader lab automation, and whether currency conversion uses an annual average rate or a point-in-time rate for the base year.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 0.70 B (2026) | |

| Global Consultancy A | USD 0.42 B (2023) | Uses an earlier base year and appears to blend instruments, reagents, and accessories without clearly separating dedicated dissociation tools from adjacent lab workflow spending, which can shift the starting value and growth curve. |

| Trade Journal B | USD 0.50 B (2024) | Employs a narrower forecast window and product framing that can over-weight catalog list pricing and broad product buckets, with limited visibility on regional price realization and replenishment frequency. |

The table shows that the biggest drivers are definition and timing rather than math differences. By keeping the counted spend tied to identifiable dissociation products and then checking the result against multiple demand signals, the final estimate stays easier to trace, replicate, and update when new market information emerges.

Key Questions Answered in the Report

How large is the cell dissociation market in 2026 and what is its growth outlook?

The cell dissociation market is valued at USD 0.7 billion in 2026 and is projected to reach USD 1.41 billion by 2031, advancing at a 14.96% CAGR during the forecast period (2026-2031).

Which product category leads the cell dissociation market?

Enzymatic reagents lead, accounting for 58.21% of cell dissociation market share in 2025, largely due to their well-established efficacy in a wide range of tissues.

What is driving the rapid growth of non-enzymatic dissociation solutions?

Non-enzymatic products grow at a 17.08% CAGR because single-cell omics and immunophenotyping workflows demand gentler methods that preserve surface markers and gene-expression fidelity.

Why are CROs emerging as the fastest-growing end-user segment?

CROs post an 17.85% CAGR as pharmaceutical companies outsource complex cell-therapy process development and manufacturing to specialized partners with dedicated capacity.

Which region shows the highest growth, and why?

Asia-Pacific demonstrates the fastest 16.21% CAGR through 2031, supported by multi-billion-dollar government investments, expanding clinical trial pipelines, and cost-advantaged manufacturing infrastructure.

What are the main restraints that could slow market expansion?

High capital costs for advanced automation and the challenge of standardizing protocols across variable tissue sources can shave up to 2.1% and 1.8% off the forecast CAGR, respectively.

Page last updated on: