Heart Attack Diagnostics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

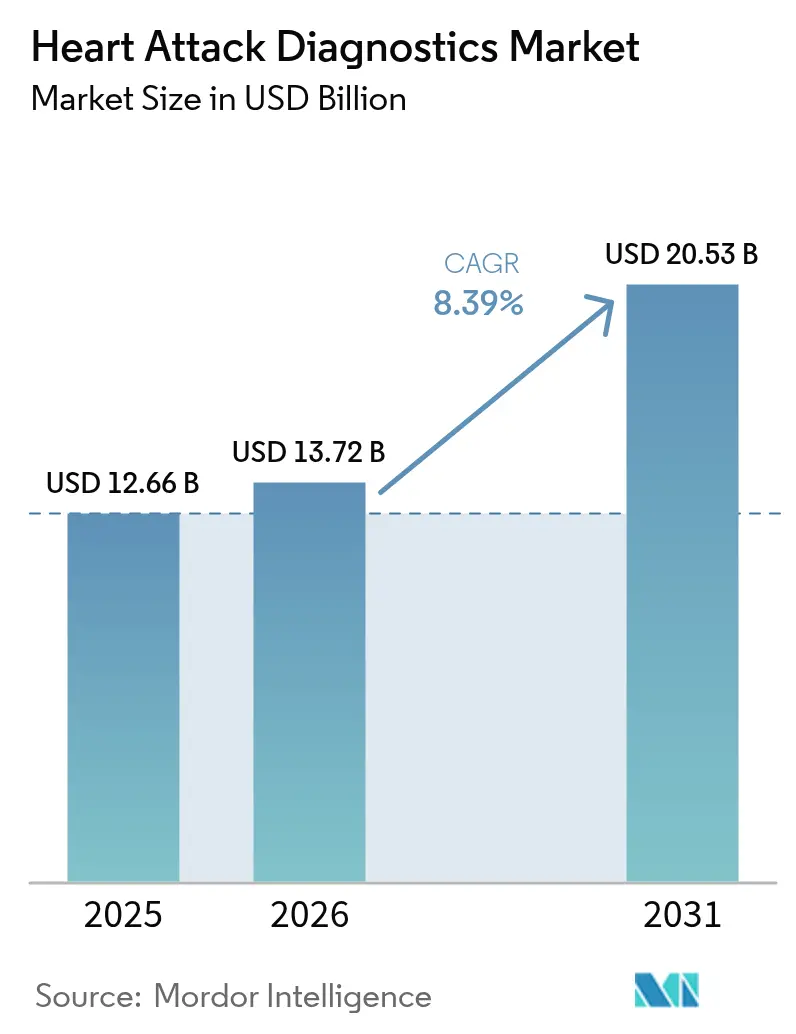

| Market Size (2026) | USD 13.72 Billion |

| Market Size (2031) | USD 20.53 Billion |

| Growth Rate (2026 - 2031) | 8.39% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Heart Attack Diagnostics Market Analysis by Mordor Intelligence

The heart attack diagnostics market size was valued at USD 12.66 billion in 2025 and estimated to grow from USD 13.72 billion in 2026 to reach USD 20.53 billion by 2031, at a CAGR of 8.39% during the forecast period (2026-2031). Continuing growth is fueled by the rising proportion of people aged 65 years and older, accelerated innovation in high-sensitivity cardiac biomarkers, and the shift toward predictive cardiology that links early detection with lower downstream treatment costs. Rapid-turnaround blood assays, AI-enabled electrocardiogram (ECG) analytics, and imaging platforms that can visualize even subclinical myocardial injury now converge in emergency departments, specialty clinics, and increasingly in patients’ homes. Hospitals remain the single largest channel for diagnostic spending, yet remote-monitoring programs are expanding fastest because health systems seek to decompress overcrowded emergency settings while still capturing revenue through reimbursable tele-cardiology services. Intensifying regulatory focus on test accuracy and device interoperability is itself a growth catalyst: firms with deep compliance expertise can move products through global approval pipelines faster, generating earlier cash flows and reinforcing brand credibility. Finally, competitive pressure is rising as integrated platform suppliers face niche entrants that deliver single-use, disposable, or cloud-native solutions that bypass legacy hardware.

Key Report Takeaways

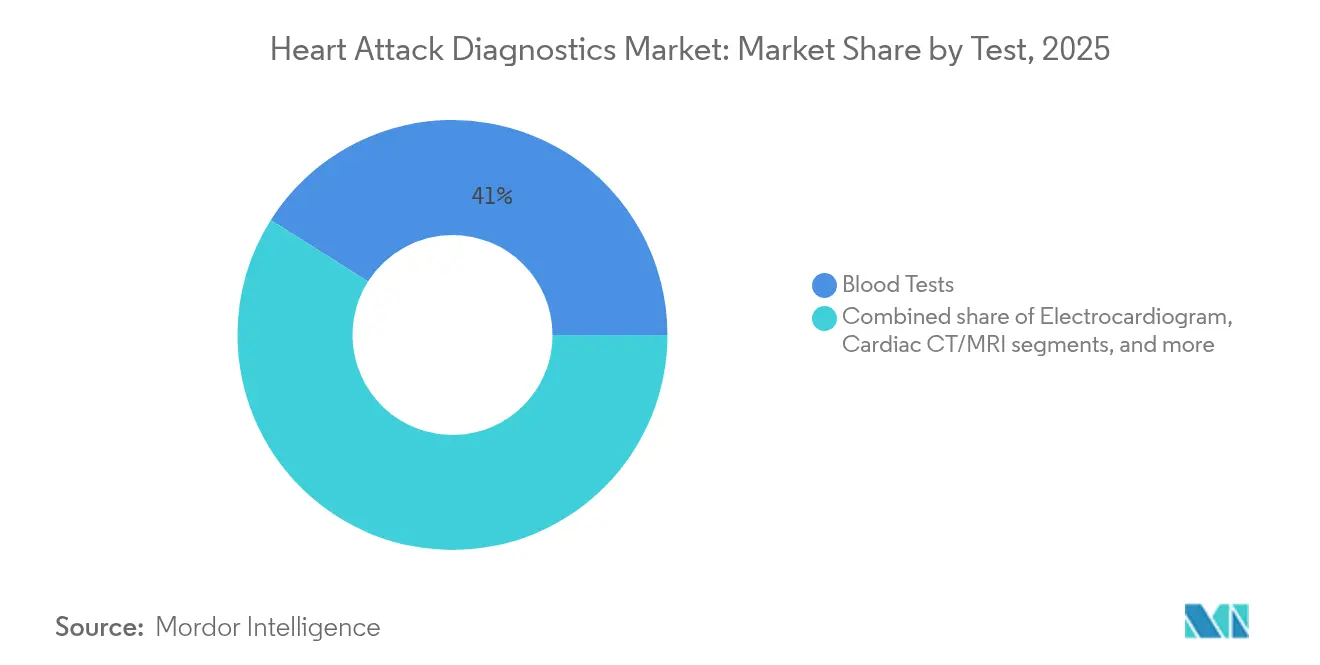

- By test, blood tests led with a 41.02% share of the heart attack diagnostics market in 2025, while wearable and AI-driven ECG systems are projected to grow at a 12.74% CAGR to 2031.

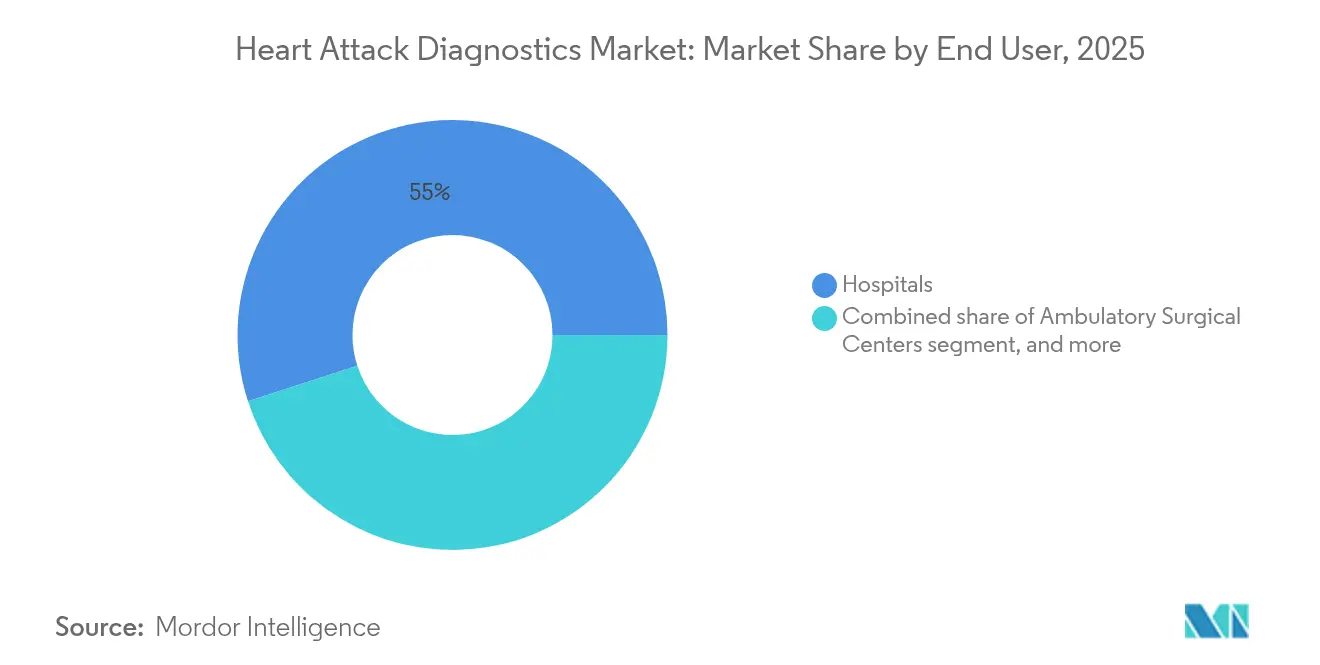

- By end user, hospitals accounted for 54.98% of the heart attack diagnostics market share in 2025; home-based and tele-cardiology settings record the highest projected CAGR at 16.35% through 2031.

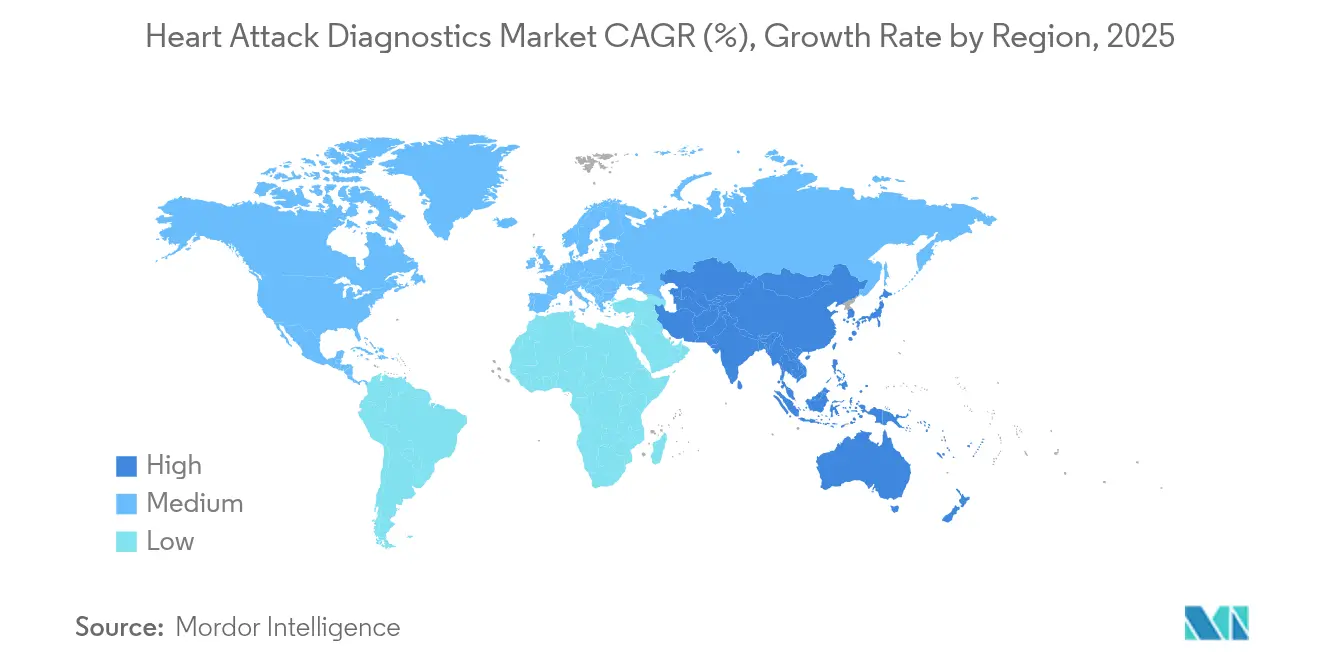

- By geography, North America contributed 35.02% of global revenue in 2025, whereas Asia-Pacific is forecast to expand at a 10.41% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Heart Attack Diagnostics Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Global Burden of Cardiovascular Disease & Aging Population | +2.1% | North America & Europe highest | Long term (≥ 4 years) |

| Rising Demand For Rapid, Accurate Diagnosis In Emergency & Critical-Care Settings | +1.8% | Urban hospitals worldwide | Medium term (2-4 years) |

| Continuous Innovation In Cardiac Biomarkers, Imaging & Analytics Technologies | +1.6% | North America & Europe leading | Medium term (2-4 years) |

| Expansion Of Decentralized / Point-Of-Care Testing Infrastructure Worldwide | +1.4% | Asia-Pacific core; spill-over to MEA & Latin America | Long term (≥ 4 years) |

| Favourable Government Initiatives And Reimbursement For Early MI Detection | +0.9% | North America & Europe | Short term (≤ 2 years) |

| Increasing Healthcare Expenditure And Adoption Across Emerging Markets | +0.7% | Asia-Pacific, MEA, Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Global Burden of Cardiovascular Disease & Aging Population

The demographic wave is reshaping the heart attack diagnostics market. As average life expectancy rises, comorbidities such as diabetes, renal disease, and hypertension converge to create atypical symptom profiles that blunt the specificity of historical diagnostic algorithms. The European Society of Cardiology predicts atrial fibrillation prevalence will double by 2050, widening the pool of patients who require chronic rhythm monitoring to avoid sudden myocardial events[1]European Society of Cardiology, “ESC Guidelines on Acute Coronary Syndromes,” escardio.org. Consequently, payers now view investment in high-sensitivity assays and remote rhythm monitors as a cost-containment measure rather than a discretionary expense. Device makers are responding by embedding cloud-based analytics that stratify risk in near-real time, supporting clinical decisions long before patients reach critical-care beds.

Rising Demand for Rapid, Accurate Diagnosis in Emergency & Critical-Care Settings

Every minute lost while confirming myocardial infarction raises mortality risk. Emergency-department physicians must therefore rely on diagnostics that deliver lab-grade accuracy within a sub-10-minute window. Clinical registries show that patients lacking regular cardiology follow-up experience 24% higher in-hospital mortality, underscoring the stakes of frontline triage. Point-of-care analyzers and handheld ECG readers now incorporate AI algorithms that replicate specialist interpretation, closing skills gaps in understaffed facilities. These capabilities are especially impactful in rural hospitals, where cardiologists are scarce and air-transfer delays can exceed therapeutic time windows.

Continuous Innovation in Cardiac Biomarkers, Imaging & Analytics Technologies

The market is shifting from single-parameter testing toward multi-analyte panels that reveal nuanced biochemical patterns. High-sensitivity troponin can detect injury at picogram levels, but distinguishing acute events from chronic micro-necrosis demands additional markers such as copeptin, galectin-3, or metabolomic signatures. Imaging keeps pace: cadmium-zinc-telluride (CZT) single-photon emission computed tomography (SPECT) cameras deliver higher sensitivity than legacy systems while reducing radiation dose, according to peer-reviewed trials in the Journal of Nuclear Medicine[2]Journal of Nuclear Medicine, “CZT Cameras Improve Myocardial Perfusion Imaging,” snmjournals.org. Layered on top, machine-learning platforms sift through time-series data to flag patterns invisible to clinicians, pushing diagnostics toward predictive care models rather than confirmatory snapshots.

Expansion of Decentralized / Point-of-Care Testing Infrastructure Worldwide

National health plans in rapidly urbanizing economies view decentralized diagnostics as a means to extend cardiovascular care without constructing costly tertiary-care hospitals. Portable troponin analyzers, smartphone-based ECG patches, and modular imaging vans bring core services into primary-care clinics and even community pharmacies. The U.S. Food and Drug Administration signaled growing regulatory flexibility by exploring reclassification of certain diagnostic devices to accelerate review cycles[3]Regulatory Affairs Professionals Society, “MDUFA VI Framework Discussions,” raps.org. Although initial capital outlays remain substantial, decentralized programs reduce readmissions and increase screening volumes, allowing providers to amortize equipment costs over a broader revenue base.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital and operating costs of advanced diagnostic systems & consumables | –1.2% | Emerging markets hardest hit | Medium term (2-4 years) |

| Stringent regulatory approval pathways and compliance requirements | –0.8% | North America & Europe | Long term (≥ 4 years) |

| Shortage of skilled healthcare professionals trained in cardiac diagnostics | –1.0% | Global, most acute in rural and low-income settings | Medium term (2-4 years) |

| Limited accessibility and reimbursement in low-resource settings | –0.9% | Sub-Saharan Africa, parts of South & Southeast Asia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital and Operating Costs of Advanced Diagnostic Systems & Consumables

Sticker prices for high-throughput chemistry analyzers or CZT-SPECT cameras can exceed USD 2 million, but the larger burden lies in recurring reagent kits, annual service contracts, and staff training. Smaller community hospitals rarely process enough specimens to recoup those costs within typical budgeting cycles. Pediatric transplant units, however, demonstrate that once-perfusion blood tests can reduce post-operative monitoring expenses tenfold without compromising safety. This example illustrates that targeted innovation can overcome cost barriers, yet scaling such solutions across broader populations remains challenging.

Stringent Regulatory Approval Pathways and Compliance Requirements

Predictive biomarkers, unlike well-established troponin assays, face lengthy validation phases that involve multi-site trials and complex statistical endpoints. Upcoming changes to the U.S. Medical Device User Fee Amendments (MDUFA VI) will determine whether application review timelines compress or extend, directly affecting launch schedules for next-generation point-of-care platforms. While rigorous oversight protects patients, it also creates a moat for incumbents who possess in-house regulatory teams, sophisticated quality-management systems, and capital reserves that can absorb the cost of prolonged development.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Test: Blood Dominates, Wearable ECG Sets the Pace

Blood assays secured 41.02% of the heart attack diagnostics market in 2025, a position underpinned by high-sensitivity cardiac troponin I/T kits that generate definitive yes-or-no answers within the first hour of suspected infarction. That scale translates into a tangible heart attack diagnostics market size advantage, yielding USD 5.19 billion in revenues and affirming the segment as a cash-flow engine for reagent suppliers. Parallel tests such as CK-MB and myoglobin remain clinically relevant for rule-in or rule-out scenarios when baseline troponin is elevated due to chronic disease. Yet the demand profile is changing. Wearable ECG platforms are advancing at a 12.74% CAGR and are projected to overtake angiogram referrals for first-line rhythm analysis by the late-2020s. Cloud-based dashboards push continuous data streams to cardiology hubs, triggering alerts when algorithms detect ST-segment deviation or paroxysmal atrial fibrillation, a precursor to embolic myocardial events.

This growth gap underscores how the heart attack diagnostics market is migrating from episodic biomarker snapshots toward holistic, real-time physiologic surveillance. Integrated solutions combine fingerstick troponin kits, smart-patch ECG sensors, and AI-curated symptom trackers within a single subscription model. The approach appeals to health insurers because early rhythm detection can avert ambulance transfers and catheter lab admissions, both high-cost events. Imaging still holds strategic relevancy. CT coronary angiography and cardiac MRI quantify plaque burden, left-ventricular ejection fraction, and microvascular perfusion, supporting prognosis and therapy selection. Vendors capable of harmonizing biochemical, electrical, and structural data within interoperable dashboards are likely to command premium margins and lock-in users through ecosystem effects.

By End User: Hospitals Hold Court, Home-Based Care Accelerates

Hospitals captured 54.98% of 2025 global spending, reflecting embedded procurement pipelines, access to interventional teams, and the ability to run multi-modality protocols on-site. Bedside troponin testing combines with radiology and cardiology consults under one roof, reinforcing hospital dominance across diagnostic revenues. Nonetheless, the weight of chronic disease management is straining inpatient capacity. Large health systems are piloting home-hospital programs that deploy virtual command centers, courier-delivered biomarker kits, and AI-triaged ECG sensors. These models drive the fastest growth, at a 16.35% CAGR, and are expected to boost the heart attack diagnostics market size for the home-care segment to USD 2.71 billion by 2031.

Adoption is propelled by reimbursement reforms that compensate tele-cardiology consultations at parity with in-person visits, plus evidence that remote titration of cardiac drugs improves adherence. Nature Communications recently showed that machine-learning analysis of wearable ECGs cut unplanned readmissions by 28% in moderate-risk patients nature.com. Diagnostic imaging and pathology centers remain relevant but face commoditization pressures as hospital networks insource CT scanners and as miniaturized ultrasound probes move into primary-care offices. Ambulatory surgery centers specialize in elective coronary revascularizations and thus procure adjunctive diagnostics selectively, focusing spending on portable devices that support same-day discharge.

Geography Analysis

North America led global revenue with a 35.02% share in 2025, fueled by mature payer systems that reimburse novel biomarkers and digital ECG analytics without lengthy coverage lags. The United States has embedded troponin turnaround-time targets into quality metrics tied to hospital payment, ensuring that devices capable of sub-10-minute results secure favorable placement. Canada’s single-payer structure stresses outcomes-based procurement, promoting multi-platform solutions that reduce total admissions rather than stand-alone tests. Clinical practice guidelines issued by the American Heart Association and the European Society of Cardiology are widely adopted, smoothing cross-border clinical pathways.

Europe contributes a substantial volume of procedures through universal coverage and rigorous evidence-based approval processes. Germany’s Netzwerk Herzzentren has standardized biomarker protocols, while the United Kingdom’s National Health Service is trialing AI-enabled ECG triage in community clinics. Adoption across Italy, France, and Spain accelerates where domestic producers partner with public hospitals to localize production of consumables, thereby sidestepping supply-chain constraints. Regulatory convergence under the European Medical Device Regulation continues to raise compliance costs but also harmonizes market access across member states.

Asia-Pacific is the fastest-growing territory, expanding at a 10.41% CAGR from 2026 to 2031. China’s Healthy China 2030 blueprint earmarks cardiovascular illness as a national priority, pushing public hospitals to deploy high-sensitivity troponin and low-radiation CT angiography in prefecture-level cities. Japan’s super-aging demographic accelerates demand for ambulatory cardiac monitors that can upload data to cloud repositories compliant with stringent privacy laws. India’s Ayushman Bharat scheme widens insurance coverage, encouraging public-private partnerships to distribute point-of-care troponin kits into district hospitals. Collectively, these initiatives enlarge the heart attack diagnostics market, but vendors must tailor price points and service models to heterogeneous payer structures.

Across the Middle East & Africa, Gulf Cooperation Council states invest in Western-standard tertiary centers that install state-of-the-art biomarker analyzers. In contrast, sub-Saharan health ministries favor portable diagnostics that function in low-infrastructure settings. South American nations grapple with currency volatility; however, Brazil’s Unified Health System funds nationwide chest-pain units equipped with handheld ECG devices. These dynamics illustrate that while North America sets revenue benchmarks, long-term volume growth increasingly hinges on strategies tuned to emerging-market needs.

Regulatory Landscape

Regulation for heart attack diagnostics covers in vitro diagnostics, cardiac monitoring hardware, and software-as-a-medical-device, with the United States largely relying on FDA classification and the 510(k) pathway for many cardiac diagnostic devices (for example, under 21 CFR Part 870). A key quality-system milestone is the FDA Quality Management System Regulation (QMSR), effective February 2, 2026, which incorporates ISO 13485:2016 concepts into 21 CFR Part 820 and raises the bar for design controls, supplier management, and post-market processes across biomarker assays and ECG platforms.

In Europe, market access is shaped by EU MDR 2017/745 and the capacity and timelines of notified bodies. The adoption of Commission Implementing Regulation (EU) 2026/977 on May 4, 2026 addresses parts of the conformity-assessment workflow by standardizing elements of notified body requirements and timelines, while MDR certifications and clearances (for example, Acarix's CADScor System achieving EU MDR certification, and Hemolens Cardiolens Viewer completing MDR conformity assessment) show ongoing vendor investment in compliance to support EU commercialization. These changes increase the importance of evidence generation, cybersecurity, and interoperability documentation for AI-enabled ECG interpretation and connected diagnostic ecosystems used in emergency departments and decentralized settings.

Competitive Landscape

The heart attack diagnostics market shows moderate consolidation. The top five firms—Abbott Laboratories, F. Hoffmann-La Roche, Siemens Healthineers, Beckman Coulter, and Philips—collectively control an estimated 65% of global revenues. Their advantage lies in end-to-end portfolios covering reagents, analyzers, ECG equipment, and software analytics that integrate within single vendor contracts. Abbott’s MultiPoint Pacing technology produced an 87% responder rate in recent clinical audits, illustrating how device-algorithm symbiosis enhances patient benefit while protecting premium pricing. Siemens Healthineers packages high-sensitivity troponin with CT angiography platforms, leveraging synergies in capital equipment sales and recurrent consumable demand.

Mid-tier players concentrate on specialized niches. QuidelOrtho is scaling single-cartridge troponin tests that function in ambulance settings, and AliveCor pushes smartphone-based ECGs that interoperate with telehealth portals. Venture-backed start-ups attack AI interpretation, promising cardiologist-level accuracy through cloud APIs that can embed in any ECG device. Success in this layer depends on regulatory clearances and data-security credentials that satisfy hospital audits.

Partnership networks are widening. Diagnostic firms license proprietary biomarkers discovered in university labs, trade imaging algorithms for distribution rights, or co-develop embedded chips with semiconductor giants to drive down unit costs. Acquisitions spike whenever a start-up secures a groundbreaking algorithm or crosses pivotal regulatory milestones. Given this dynamic, market leaders must continue to refresh product pipelines or risk ceding share to agile entrants that capitalize on unmet workflow pain points.

Heart Attack Diagnostics Industry Leaders

F Hoffmann-La Roche Ltd

Abbott Laboratories

Siemens Healthineers

GE HealthCare

Beckman Coulter (Danaher)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A near-term opportunity is the continued shift of acute chest-pain evaluation toward faster rule-in/rule-out workflows that reduce emergency department congestion. That dynamic supports demand for high-sensitivity biomarker assays and rapid platforms that can be deployed beyond central laboratories. The 2026 regulatory cadence also points to continued product refresh activity in cardiac markers, with clearances cited for BNP/NT-proBNP and inflammation-linked cardiac risk markers (for example, Beckman Coulter Access BNP II and Axis-Shields Alere NT-proBNP for Alinity i). These procurement cycles can drive upgrades to immunoassay menus used for acute cardiac decisioning.

Decentralized diagnostics also creates placement opportunities in home-based and tele-cardiology settings, where the market context points to the fastest growth in care delivery models and a rising role for wearable and AI-driven ECG systems. Real-world commercialization actions in 2026, such as AliveCor's European launch of a handheld 12-lead ECG platform, and clinical evaluation programs such as HeartBeams ALIGN-ACS pilot enrolling chest pain patients, indicate movement toward portable ECG acquisition and algorithm-assisted interpretation outside traditional cath-lab driven pathways. As these ecosystems mature, integration with reimbursable remote-monitoring programs and interoperable cloud analytics remains a differentiator for suppliers seeking share gains without relying only on large capital imaging placements.

Recent Industry Developments

- April 2026: AliveCor launched the AI-powered Kardia 12L handheld 12-lead ECG system across European markets including France, Germany, Italy, Spain, and the UK following CE Mark. The launch expands access to higher-fidelity ECG acquisition in more decentralized settings, supporting tele-cardiology workflows where rapid electrical assessment can complement biomarker testing and imaging triage.

- September 2025: Roche published results from its TSIX study program for the Elecsys Troponin T hs Gen 6 test, highlighting performance for identifying acute myocardial infarction and supporting rule-out decisions. The update reinforces competitive intensity around high-sensitivity troponin generations, where assay performance and workflow impact are central to hospital standardization decisions.

- March 2024: Powerful Medical received FDA Breakthrough Device Designation for its PMcardio STEMI AI ECG model for detecting ST-elevation myocardial infarction. The designation elevates momentum for AI-enabled ECG interpretation tools and signals a faster dialogue with regulators for software that can shorten time-to-diagnosis in acute cardiac pathways.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenues earned from diagnostic tests and procedures used to detect and confirm an acute heart attack, across care settings where patients are assessed and managed.

Scope exclusions: general wellness wearables that only track heart rate or rhythm without diagnostic clearance are excluded.

Segmentation Overview

- By Test

- Electrocardiogram (12-lead, 3-lead, Wearable)

- Blood Tests

- Cardiac Troponin I/T

- CK-MB & Myoglobin

- BNP & NT-proBNP

- Angiogram (Invasive & CT Coronary)

- Cardiac CT/MRI

- Other Tests

- By End User

- Hospitals

- Ambulatory Surgical Centers

- Diagnostic Imaging & Pathology Centers

- Home-based & Tele-cardiology Settings

- Other End Users

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with aligning the disease context and the testing pathway. Heart attack workups commonly combine ECG, cardiac biomarker blood tests, and confirmatory imaging when needed, so we reviewed open and credible references such as CDC and WHO cardiovascular statistics, NIH and NLM literature sources, FDA public databases for diagnostic clearances, and AHA guidance documents. The goal was to understand test usage triggers and how practice is shifting toward faster rule out.

We then mapped likely volumes and pricing logic using sources such as hospital and lab publications, peer reviewed papers on high sensitivity troponin adoption and sampling intervals, and importer exporter trade statistics where relevant for device categories. Company filings and investor presentations were also used to sense check product revenue mix, and a paid subscription for company financials, patents, and shipment level trade intelligence was selectively referenced to cross verify trends. The sources listed above are illustrative only, and many other public and paid references were used to collect, validate, and clarify data points.

Primary Interviews and Surveys

Primary inputs were gathered through expert interviews and structured surveys with clinicians involved in chest pain workups, lab and imaging decision makers, and distribution or service side stakeholders who see test throughput trends. We used these discussions to confirm adoption of high sensitivity troponin workflows, typical repeat test frequency in emergency care, procedure mix between invasive and CT coronary angiography, and the practical split between hospital and outpatient diagnostics across regions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 25% | CXOs: 17% | APAC: 49% |

| Mid tier: 58% | Functional/Unit leaders: 40% | EMEA: 32% |

| Smaller Players: 17% | Managers: 43% | Americas: 19% |

Market-Sizing & Forecasting

Sizing begins with a top-down build that reconstructs the demand pool from acute chest pain presentations and suspected acute coronary syndrome pathways, then filters it through testing rates by modality. We check the results with selective bottom-up approximations, such as sampled average selling price times estimated test volumes for troponin and other biomarker assays, plus category level roll ups for ECG and imaging procedure revenues, before reconciling totals.

Key inputs used in the model include troponin testing penetration and repeat sampling cadence, the mix shift toward high sensitivity assays, emergency department throughput and chest pain protocol timing, imaging utilization rates for cardiac CT and MRI in acute settings, and angiography procedure mix between invasive and CT coronary approaches. For pricing, we applied market relevant ASP or reimbursement proxies by test class and geography, then normalized currency assumptions to a consistent year to avoid artificial jumps.

Forecasts rely mainly on scenario analysis supported by expert consensus on adoption speed. In practice, guideline changes and lab workflow updates can move volumes faster than population growth alone. Where bottom-up signals were missing for smaller geographies, we used peer country ratios based on care access, testing infrastructure, and acute cardiovascular burden, then rechecked against regional totals.

Data Validation & Update Cycle

Validation is handled through multiple cross checks. Model outputs are compared against independent signals such as procedure and test utilization ranges in clinical literature, regulatory clearance activity, and company reported category performance. Outliers are reviewed, assumptions are re tested, and respondents are re contacted when variance cannot be explained by a known shift such as a high sensitivity rollout or a reimbursement update.

Before sign off, the workbook and narrative go through stepwise analyst reviews, and key calculations are audited for unit consistency and regional add ups. Reports are refreshed annually, and interim updates are made when material events occur, with a final fresh pass completed before delivery so clients receive the latest updated view.

Mordor Intelligence's Heart Attack Diagnostics Market Size Compared Against Other Published Estimates

It is common to see different market sizes for heart attack diagnostics. Publishers do not always count the same testing steps, and some approaches combine device sales with procedure revenues in different ways. In our model, the scope is centered on tests used to diagnose and confirm acute events, then linked to observable usage patterns and pricing logic.

Wellness wearables that only track generic heart rate sit outside Mordor Intelligence's scope, and that single inclusion difference can shift totals when consumer monitoring is treated as diagnostic demand. Other discrepancies come from how fast high sensitivity troponin conversion is assumed, whether repeat sampling is counted consistently, and whether imaging and angiography are treated as acute confirmation only or blended with broader cardiac screening volumes.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 13.72 B (2026) | |

| Industry Publisher A | USD 9.80 B (2026) | Uses a narrower definition that leans toward in-vitro testing revenues, which can undercount procedure based confirmation steps such as angiography and cardiac CT/MRI in acute workups. |

| Research Outlet B | USD 7.50 B (2023) | Anchors on an earlier base year and applies a slower adoption curve for high sensitivity biomarker workflows, and it also appears to treat some imaging and ECG revenues as part of broader cardiac monitoring rather than acute diagnosis. |

The spread across sources is largely explained by what gets counted as diagnostic demand, plus timing and pricing assumptions that change volumes quickly in emergency care. By keeping the scope aligned to acute testing pathways and then checking the totals against practical usage indicators, we produce a market value that stays traceable to clear variables and repeatable steps.

Key Questions Answered in the Report

What is the current value of the heart attack diagnostics market?

The market is worth USD 13.72 billion in 2026 and is forecast to grow at an 8.39% CAGR to USD 20.53 billion by 2031.

Which test type holds the largest heart attack diagnostics market share?

Blood assays, led by high-sensitivity troponin, accounted for 41.02% of global revenue in 2025.

Why are wearable ECG devices expanding faster than laboratory tests?

Wearables combine continuous rhythm monitoring with AI interpretation, enabling earlier detection of anomalies and supporting remote-care models that lower hospital admissions.

Which region is growing fastest?

Asia-Pacific is projected to expand at a 10.41% CAGR because of healthcare modernization, rising cardiovascular disease prevalence, and supportive government funding.

How do regulatory changes influence market dynamics?

Streamlined review pathways under deliberation in the United States and Europe could shorten time-to-market for innovative devices, benefiting manufacturers able to navigate new compliance requirements efficiently.

Page last updated on: