Netherlands Freight Brokerage Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

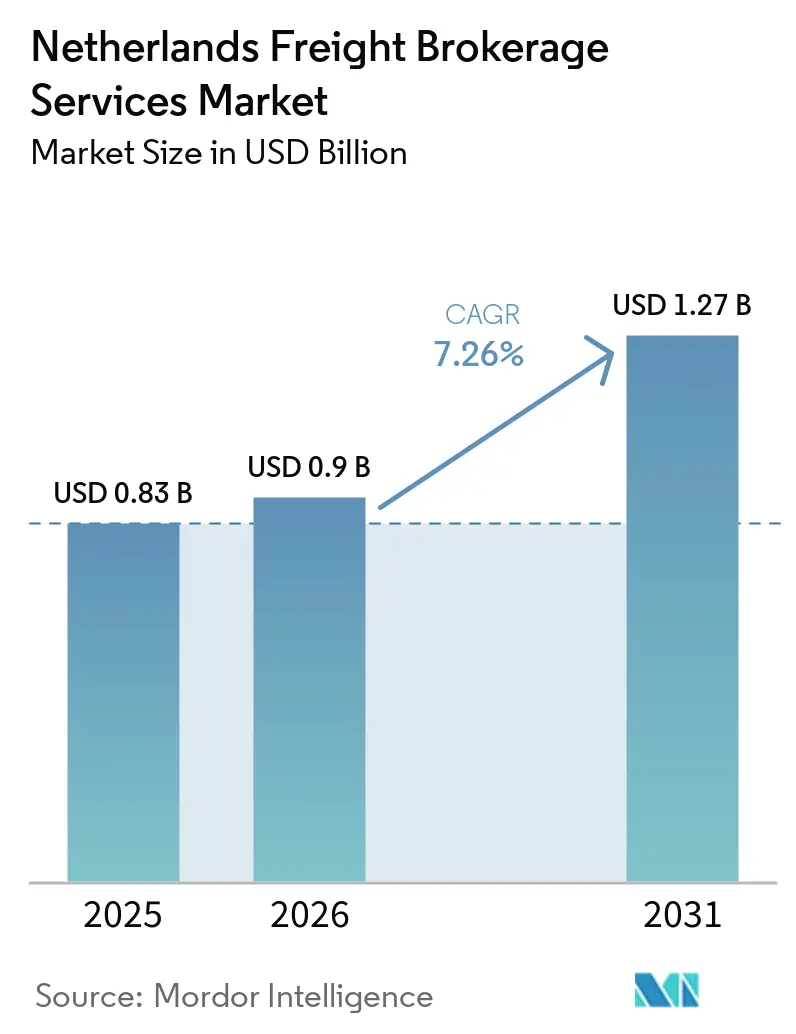

| Base Year Market Size (2025) | USD 0.83 Billion |

| Market Size (2026) | USD 0.9 Billion |

| Market Size (2031) | USD 1.27 Billion |

| Growth Rate (2026 - 2031) | 7.26% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Netherlands Freight Brokerage Services Market Analysis by Mordor Intelligence

The Netherlands freight brokerage services market was valued at USD 0.83 billion in 2025, is estimated at USD 0.90 billion in 2026, and is projected to reach USD 1.27 billion by 2031, growing at a CAGR of 7.26% over 2026–2031. Three structural shifts underpin this trajectory: Dutch brands are pivoting to direct-to-consumer (D2C) fulfillment models, the Maasvlakte II and ECT Delta deep-sea container berths added 3.5 million TEU of capacity, and quick-commerce grocery operators now demand sub-60-minute urban delivery. Platform adoption of AI-driven dynamic lane pricing further boosts yield, while the EU’s ICS2 pre-lodgement system has cut average customs clearance times by 40%, allowing faster cross-border flows. Simultaneously, the government’s EUR 35 million hydrogen corridor program is nurturing a zero-emission long-haul ecosystem that appeals to shippers with strict environmental targets. Collectively, these factors ensure that the Netherlands freight brokerage services market remains a pivotal logistics node for European supply chains.

Key Report Takeaways

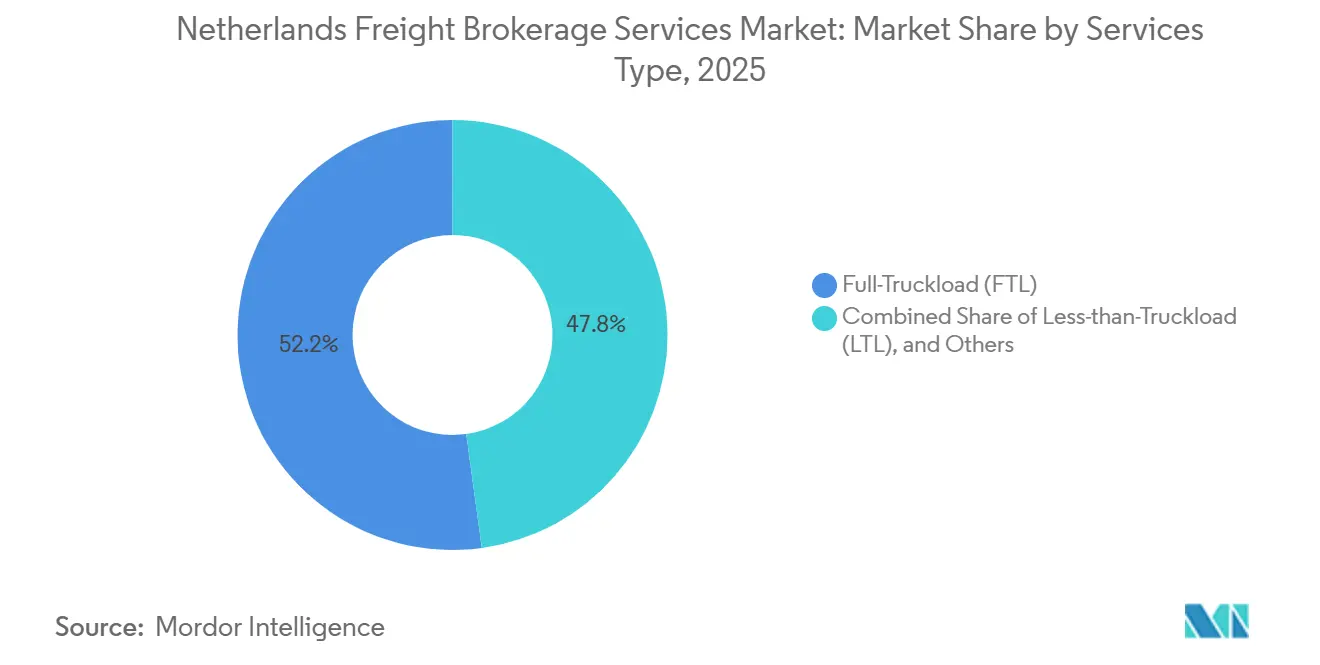

- By service category, full-truckload held 52.18% of the Netherlands freight brokerage services market share in 2025, while less-than-truckload is advancing at a 9.03% CAGR through 2031.

- By equipment type, dry van configurations commanded 44.36% of the Netherlands freight brokerage services market size in 2025 and refrigerated van demand is rising at a 9.87% CAGR.

- By haul length, regional routes controlled 50.83% of the Netherlands freight brokerage services market share in 2025, whereas local trips below 100 miles are projected to grow at 11.57% CAGR.

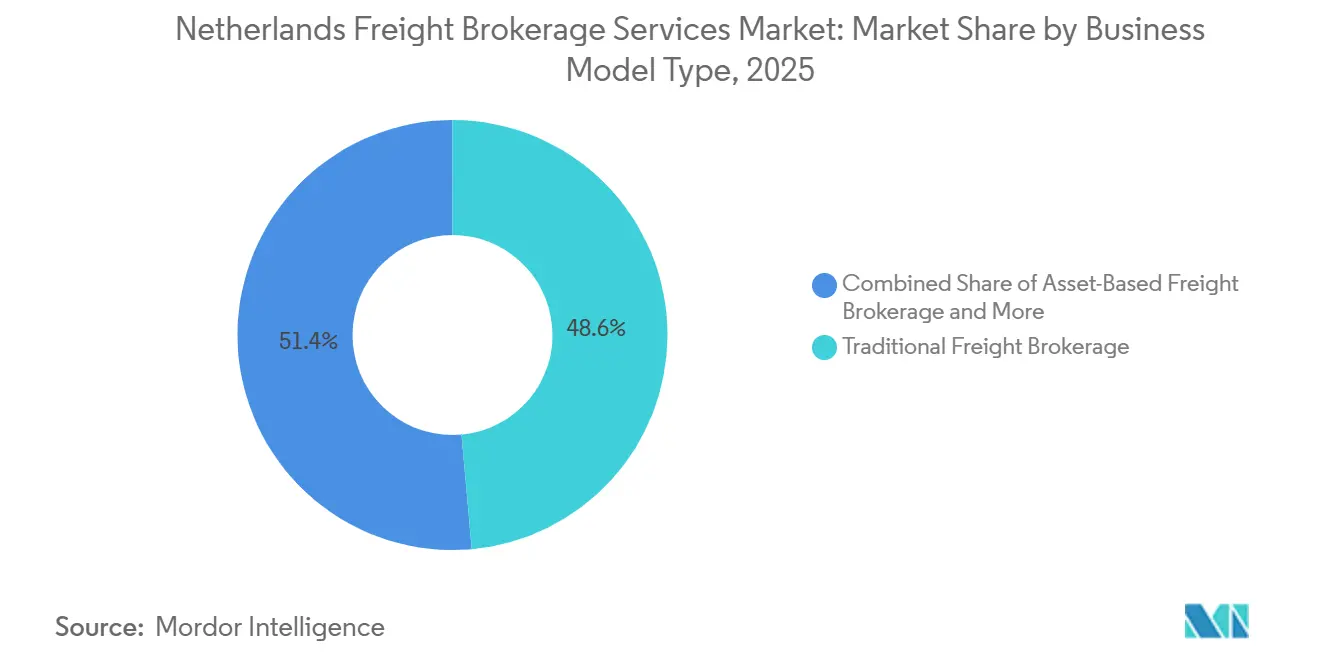

- By business model, traditional brokerage accounted for 48.58% of the Netherlands freight brokerage services market size in 2025, but digital brokerage models are scaling at a 19.39% CAGR.

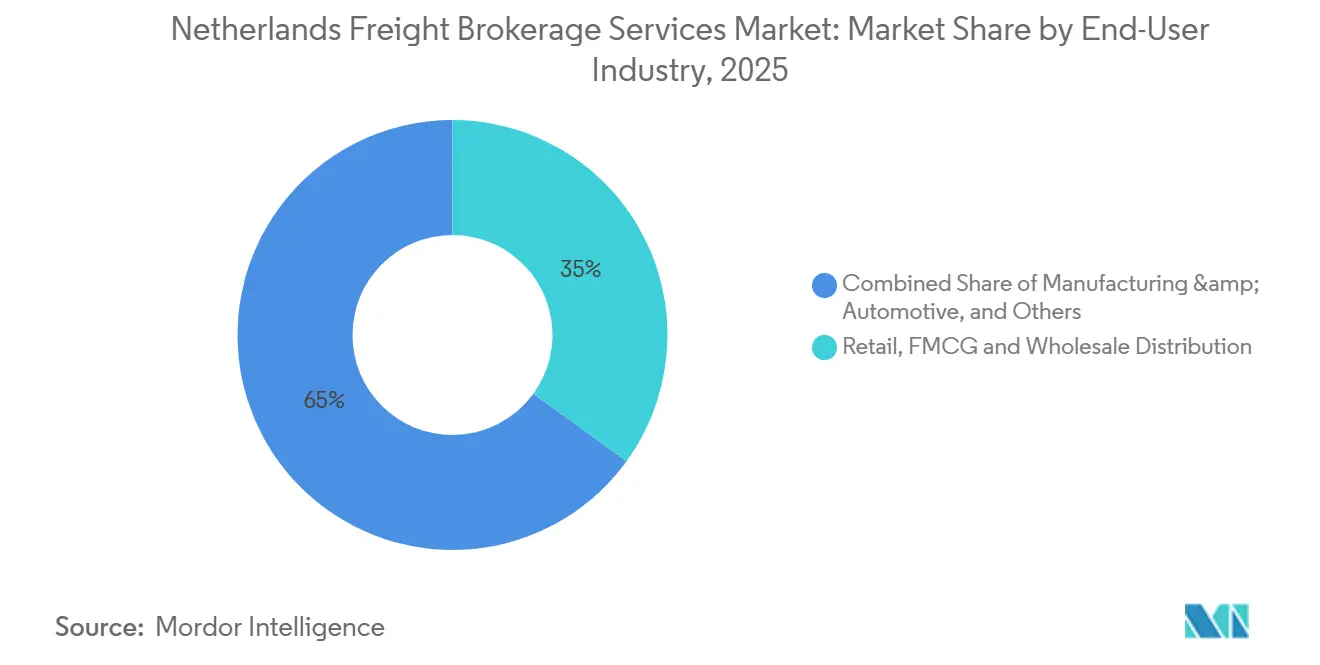

- By end-user industry, Retail / FMCG / Wholesale led with 34.98% share in 2025; E-commerce and 3PL fulfillment is the fastest-growing segment at 16.32% CAGR to 2031.

- By customer size, Large enterprises controlled 52.09% of the Netherlands freight brokerage services market share in 2025, while Small businesses are increasing platform use at 12.85% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

National developments in Netherlands connect differently with activity unfolding across other parts of the world. In the global freight brokerage services market coverage, Mordor Intelligence integrates these into a single analytical framework.

Netherlands Freight Brokerage Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Direct-to-Consumer (D2C) Shipping Surge Among Dutch Manufacturers and Brands | +1.5% | Netherlands national, with cross-border spillover to Germany and Belgium | Short term (≤ 2 years) |

| Capacity Expansion of Rotterdam Deep-Sea Terminals (Maasvlakte II, ECT Delta) Unlocking Additional Container Volumes | +1.3% | Netherlands gateway ports, affecting pan-European hinterland distribution | Medium term (2-4 years) |

| Explosive Growth of Quick-Commerce Grocery Platforms Driving Time-Definite Parcel Freight | +1.2% | Netherlands urban centers, expanding to secondary cities | Short term (≤ 2 years) |

| EU ICS2 Pre-Lodgement Regime Accelerating Customs Clearance and Boosting Brokerage Throughput | +0.9% | EU-wide, concentrated at Netherlands border crossings | Medium term (2-4 years) |

| Rapid Adoption of AI-Driven Dynamic Lane-Pricing by Digital Freight Platforms | +0.8% | Netherlands national, with regional platform integration | Short term (≤ 2 years) |

| Government-Backed Hydrogen Truck Corridors (Rotterdam–Antwerp–Ruhr) Catalysing Green Long-Haul Demand | +0.6% | Netherlands-Belgium-Germany corridor, expanding to broader EU network | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Direct-to-Consumer Shipping Surge Among Dutch Manufacturers and Brands

Manufacturers such as Tony’s Chocolonely and Rituals shifted 28-35% of 2025 sales to D2C channels, replacing pallet-level wholesale orders with small, high-frequency consignments that require agile brokerage coordination. Smaller shipment sizes have lifted reverse-logistics volumes, with apparel return rates near 22%, forcing brokers to optimize bidirectional flows. API connections to Shopify and WooCommerce now automate booking and tracking, improving customer experience and lowering manual processing costs. Brokers offering multi-carrier coverage across 27 EU states benefit most because D2C brands demand consistent delivery promises in every destination. The Netherlands freight brokerage services market therefore gains incremental volume and margin from D2C growth[1]“Import Control System 2 Roll-out,” Directorate-General Taxation & Customs, ec.europa.eu.

Capacity Expansion of Rotterdam Deep-Sea Terminals Unlocking Additional Container Volumes

APM Terminals Maasvlakte II and ECT Delta reached full utilization in 2025, bringing total port capacity to 4.5 million TEU per facility and cutting vessel dwell times through 35 crane moves per hour. Higher throughput translates to inland surges that require sophisticated brokerage scheduling. Dedicated rail and barge links now enable brokers to pre-book block-trains toward Germany’s Ruhr Valley, smoothing weekly demand peaks. Ultra Large Container Vessels offload concentrated cargo volumes, and brokers that secure rail slots avoid truck congestion at peak gate windows. Intermodal commitments thus become a strategic differentiator within the Netherlands freight brokerage services market.

Explosive Growth of Quick-Commerce Grocery Platforms Driving Time-Definite Parcel Freight

Getir, Gorillas and Flink operated 127 Dutch dark stores by December 2025, each replenished 8-12 times daily to maintain ultra-fast order fulfillment. The model generates dense, recurring freight lanes ideal for brokers that can guarantee hourly delivery into micro-fulfillment hubs. Fresh and chilled items account for up to 50% of volumes, prompting IoT-enabled temperature monitoring to validate cold-chain integrity. Replenishment cadence produces reliable backhauls, letting brokers engineer round-trip density that raises load factors. As new cities add dark stores, the Netherlands freight brokerage services market captures incremental refrigerated demand and premium pricing power[2]“Hydrogen Corridor Funding,” Ministry of Infrastructure & Water Management, government.nl .

EU ICS2 Pre-Lodgment Regime Accelerating Customs Clearance and Boosting Throughput

ICS2 went live for express cargo in March 2024 and reduced average Dutch border clearance from 4.2 hours to 2.5 hours for compliant entries. Physical inspection rates for low-risk goods fell 30-40%, freeing capacity and enabling brokers to promise tighter lead times on cross-border lanes. Yet incomplete filings trigger 12-24 hour delays, so brokers invested in data-validation software and shipper onboarding programs. Early mastery of ICS2 differentiates digital platforms that can guarantee compliance for every shipment type. Faster clearance sustains the Netherlands freight brokerage services market advantage as Europe’s preferred gateway.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 2026 Nationwide Road-Pricing ("Betalen naar Gebruik") Increasing Cost Per Kilometre for Hauliers and Brokers | -1.2% | Netherlands national, affecting all road freight movements | Short term (≤ 2 years) |

| Acute Shortage and Rising Rents of Cross-Dock and Warehouse Space in the Randstad Logistics Triangle | -0.9% | Netherlands Randstad region, with spillover to secondary markets | Medium term (2-4 years) |

| Escalating Cyber-Insurance Premiums Following 2025 Ransomware Attacks on Dutch TMS Providers | -0.7% | Netherlands national, with broader EU digital platform implications | Short term (≤ 2 years) |

| EU DAC7 Platform-Reporting Rules Imposing New Compliance and Data-Governance Costs on Digital Brokers | -0.5% | EU-wide, concentrated among digital freight platforms | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

2026 Nationwide Road-Pricing Increasing Cost Per Kilometer

Distance-based charges averaging EUR 0.067 per km will raise Dutch haulier cost bases 8-11%, compressing brokerage margins unless surcharges are passed through. Variable tolls by weight and emission class complicate LTL network design and incentivize cross-border carriers that transit without domestic pickups. Brokers are integrating road-pricing APIs into routing engines to minimize chargeable distance while maintaining on-time performance. Contract renegotiations increasingly adopt automatic road-pricing adjusters similar to fuel clauses, protecting broker profitability within the Netherlands freight brokerage services market.

Acute Shortage and Rising Rents of Cross-Dock and Warehouse Space

Randstad vacancy dropped below 2.5% in Q4 2025 and prime rents jumped 23% to EUR 95-110 per m² per year, straining LTL consolidation economics. Environmental zoning slows new construction, extending build timelines beyond 18 months. Larger brokers are vertically integrating real estate to secure scarce hubs, shifting the historical asset-light model. Some mid-sized players pre-lease space in planned parks to lock-in capacity. Without mitigation, elevated rents could temper the Netherlands freight brokerage services market expansion[3]“Betalen naar Gebruik Road-Pricing Act,” Ministry of Infrastructure & Water Management, government.nl .

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: LTL Gains Ground Through Consolidation Economics

Less-than-Truckload posted a 9.03% CAGR and is narrowing the volume gap with Full-Truckload, which still held 52.18% of the Netherlands freight brokerage services market share in 2025. Rising e-commerce parcel counts and quick-commerce replenishment create shipment fragmentation that favors LTL aggregation hubs. The Netherlands freight brokerage services market size for LTL is projected to reach USD 0.46 billion by 2031 as brokers automate cross-dock sequencing and deploy AI route builders to blend up to 60 consignments per tour[4]“Container Volume Expansion,” Port of Rotterdam Authority, portofrotterdam.com.

Traditional Full-Truckload business remains indispensable for bulk industrial cargo that requires dedicated trailers and fixed schedules. Yet shippers increasingly mix modes, pushing brokers to offer dynamic load-splitting where FTL moves between regional DCs feed LTL urban distribution. Digital brokers lead in small-parcel density optimization, accelerating competitive pressure on manual phone-based intermediaries.

By Equipment Type: Refrigerated Demand Surges with Cold-Chain Complexity

Refrigerated vans are advancing at 9.87% CAGR, fueled by pharmaceutical logistics and fresh-food e-commerce, while Dry vans retained 44.36% of the Netherlands freight brokerage services market size in 2025. The EU F-Gas phase-down encourages carriers to retrofit with natural refrigerants, raising capex yet enabling brokers to charge 25-35% rate premiums for compliant capacity.

Cold-chain lanes require end-to-end temperature telemetry, and brokers now integrate IoT probes that stream data into shipper portals. Flatbed and tanker niches remain stable, serving construction materials and petrochemicals routed through Rotterdam’s refinery cluster. Electrified urban vans cater to zero-emission zones, though payload limits confine them to sub-150 km circuits, prompting hybrid diesel-electric routing strategies.

By Haul Length: Local Segments Accelerate with Urban Density

Regional hauls captured 50.83% of the Netherlands freight brokerage services market share in 2025, but Local trips under 100 miles are growing fastest at 11.57% CAGR as city logistics intensify. Micro-fulfillment centers inside Amsterdam and Rotterdam now require twice-daily replenishment, transforming brokers into orchestration hubs for last-mile fleet partners.

Long-haul volumes toward Central and Eastern Europe shift gradually to rail-intermodal services for cost efficiency, so brokers bundle trucking with terminal drayage and customs filing. Local-regional hybrids emerge, where consolidated loads break in satellite hubs before zero-emission vans complete final delivery, improving sustainability metrics for the Netherlands freight brokerage services market.

By Business Model: Digital Platforms Reshape Competitive Dynamics

Traditional brokerage retained 48.58% of market share in 2025, yet digital platforms are racing ahead at a 19.39% CAGR to capture standardized lanes with instant pricing. Automated matching compresses booking cycles from hours to seconds, lowering administrative overhead and attracting SMEs that crave self-service dashboards.

Complex hazmat, oversized cargo, and multi-modal routings still benefit from relationship-driven experts who navigate permits and escorts. Consequently, hybrid brokers invest in API layers that expose legacy capacity to digital storefronts, blending high-touch expertise with high-tech execution and reinforcing the Netherlands freight brokerage services market versatility.

By End-User Industry: E-Commerce Outpaces Traditional Retail

Retail / FMCG / Wholesale held 34.98% market share of 2025 value, but E-commerce and 3PL fulfillment is growing 16.32% annually as consumer online spending surges. High return rates and seasonal peaks favor brokers capable of rapid carrier scaling and reverse-logistics orchestration.

Manufacturing and Automotive provide steady baseline tonnage yet face Europe-wide production headwinds. Healthcare and Pharmaceuticals require GDP-validated cold-chain, generating high-margin lanes. Construction material flows ride public infrastructure investment, while petrochemical moves depend on Rotterdam’s refinery cycles, ensuring a diversified revenue base across the Netherlands freight brokerage services market.

By Customer Size: Platform Accessibility Democratizes SME Access

Large enterprises controlled 52.09% market share of 2025 billings, but Small businesses are adopting digital platforms at 12.85% CAGR because minimum-volume barriers have vanished. Quicargo and Forto offer instant quotes and no annual contracts, empowering startups to ship ad hoc pallets with tracking parity to global brands.

Mid-market shippers toggle between contract and spot sourcing, using dashboards that compare brokered rates with in-house fleet cost benchmarks. Tiered service menus let customers mix self-booking for simple lanes with managed solutions for sensitive cargo, broadening total addressable demand for the Netherlands freight brokerage services market.

Geography Analysis

Rotterdam’s deep-sea expansions added 3.5 million TEU and anchor the Netherlands freight brokerage services market as Europe’s primary ocean gateway. The Schengen open-border regime and ICS2-enabled digital customs clearance reduce friction on pan-EU corridors, channeling sizeable inbound Asian cargo through Dutch ports into Germany’s manufacturing belt.

Within the country, the Randstad triangle dominates distribution; however, warehouse scarcity there is rerouting cross-dock investments to Venlo and Tilburg. Zero-emission zones scheduled for January 2026 compel fleet upgrades, and brokers are segmenting lanes into diesel long-haul plus electric last-mile combinations to remain compliant in Amsterdam, Rotterdam, and Utrecht. Hydrogen refueling along the Rotterdam-Antwerp-Ruhr spine further strengthens the Netherlands freight brokerage services market green credentials by enabling 400-500 km zero-emission hauls.

Economic integration with Germany and Belgium underpins bilateral flows, yet the forthcoming road-pricing scheme will alter route economics and may divert some transit traffic toward Antwerp. National broadband logistics infrastructure, including the Basis Data-Infrastructuur network, underwrites high-quality data exchange among carriers, terminals, and customs, reinforcing the market’s reputation for end-to-end visibility and operational predictability.

Mordor Intelligence's coverage of the freight brokerage services market extends across other regions including Europe and North America, while country-specific intelligence is also available for Russia, Germany, Canada, South Africa, South Korea, Mexico, and Spain, each offering a view on the jurisdiction-level dynamics as applicable.

Competitive Landscape

The Netherlands freight brokerage services market shows moderate concentration, with digital-driven consolidation accelerating. Sennder’s February 2025 purchase of C.H. Robinson’s European surface arm instantly scaled its Dutch footprint, while DSV’s USD 15.85 billion takeover of DB Schenker in April 2025 created the world’s largest logistics provider with dominant multimodal assets across Dutch gateways. Traditional houses leverage legacy carrier alliances for complex cargo, but AI-enabled upstarts undercut on standardized lanes.

Technology is the chief battleground. Leading brokers deploy predictive ETAs, blockchain documents, and carbon dashboards to secure enterprise contracts subject to ESG audits. Cyber-security emerged as a strategic differentiator after 2025 ransomware outages raised insurance thresholds; brokers proving robust defenses win procurement points. Green capacity sourcing is another wedge, as hydrogen-truck partnerships allow premium offerings to sustainability-focused shippers.

Niche specialists target high-compliance verticals. Pharmaceutical forwarders tout GDP-certified networks, while heavy-lift experts handle onshore wind components traversing the A15 corridor. Meanwhile, platform-agnostic agents continue to provide last-mile cultural fluency and tariff knowledge in peripheral Dutch provinces, ensuring service coverage breadth across the Netherlands freight brokerage services market.

Netherlands Freight Brokerage Services Industry Leaders

C.H. Robinson

DHL Group

Uber Freight

Sennder

DSV A/S

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Bleckmann launched “Bscale” in the Netherlands and the United Kingdom, offering modular, pay-as-you-grow warehousing and fulfillment with automation and same-day delivery without long-term lease commitments.

- May 2025: Rhenus Group officially inaugurated its cutting-edge logistics hub in Venlo. The 71,980 m² "Gateway to Europe" facility integrates warehousing, cross-docking, and regional distribution, offering storage for up to 28,000 pallets with advanced infrastructure.

- February 2025: Sennder completed the acquisition of C.H. Robinson’s European Surface Transportation operations, scaling its digital freight platform throughout the Netherlands gateway.

- January 2025: Kuehne+Nagel inaugurated a 75,000 m² automated Tilburg DC featuring autonomous robots and AI inventory control to support Benelux e-commerce.

Netherlands Freight Brokerage Services Market Report Scope

| Full-Truckload (FTL) |

| Less-than-Truckload (LTL) |

| Others |

| Dry Van |

| Refrigerated Van |

| Flatbed / Step-Deck |

| Tanker (Bulk Liquid and Chemical) |

| Others |

| Long-Haul (More than 500 miles) |

| Regional (100-500 miles) |

| Local (Less than 100 miles) |

| Traditional Freight Brokerage |

| Asset-Based Freight Brokerage |

| Agent Model Freight Brokerage |

| Digital Freight Brokerage |

| Manufacturing and Automotive |

| Construction and Infrastructure Projects |

| Oil, Gas, Mining and Chemicals |

| Agriculture and Food / Beverage |

| Retail, FMCG and Wholesale Distribution |

| Healthcare and Pharmaceuticals |

| E-commerce and 3PL Fulfilment |

| Other End-User Industry |

| Large Enterprise Shippers (More than USD 100 M) |

| Mid-Market Shippers (USD 10-100 M) |

| Small Businesses (Less than USD 10 M) |

| By Service | Full-Truckload (FTL) |

| Less-than-Truckload (LTL) | |

| Others | |

| By Equipment / Trailer Type | Dry Van |

| Refrigerated Van | |

| Flatbed / Step-Deck | |

| Tanker (Bulk Liquid and Chemical) | |

| Others | |

| By Haul Length | Long-Haul (More than 500 miles) |

| Regional (100-500 miles) | |

| Local (Less than 100 miles) | |

| By Business Model | Traditional Freight Brokerage |

| Asset-Based Freight Brokerage | |

| Agent Model Freight Brokerage | |

| Digital Freight Brokerage | |

| By End-User Industry | Manufacturing and Automotive |

| Construction and Infrastructure Projects | |

| Oil, Gas, Mining and Chemicals | |

| Agriculture and Food / Beverage | |

| Retail, FMCG and Wholesale Distribution | |

| Healthcare and Pharmaceuticals | |

| E-commerce and 3PL Fulfilment | |

| Other End-User Industry | |

| By Customer Size | Large Enterprise Shippers (More than USD 100 M) |

| Mid-Market Shippers (USD 10-100 M) | |

| Small Businesses (Less than USD 10 M) |

Key Questions Answered in the Report

What is the projected value of the Netherlands freight brokerage services market in 2031?

It is forecast to reach USD 1.27 billion by 2031, expanding at a 7.26% CAGR.

Which service type is growing fastest in the country?

Less-than-Truckload is advancing at a 9.03% CAGR thanks to e-commerce fragmentation.

How will the 2026 road-pricing scheme affect freight costs?

Distance-based tolls averaging EUR 0.067 per km are expected to raise haulier costs 8-11%.

Why are digital brokerage platforms gaining share?

AI-driven pricing, instant capacity matching, and self-service portals shorten booking cycles and lower admin costs.

What sustainability initiatives influence Dutch brokerage demand?

Government-funded hydrogen refueling along the Rotterdam-Antwerp-Ruhr corridor is supporting zero-emission long-haul trucking.

Which equipment type shows the strongest growth outlook?

Refrigerated vans, driven by pharma and fresh-food volumes, are growing at 9.87% annually.

Page last updated on: