Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

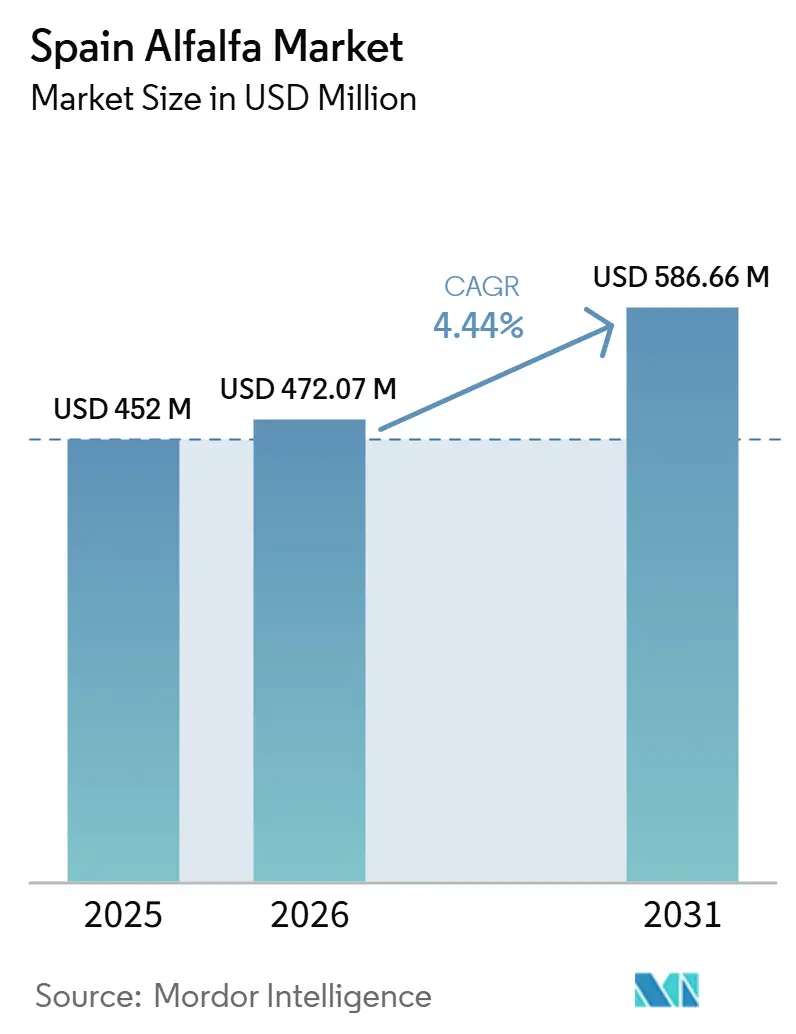

| Base Year Market Size (2025) | USD 452 Million |

| Market Size (2026) | USD 472.07 Million |

| Market Size (2031) | USD 586.66 Million |

| Growth Rate (2026 - 2031) | 4.44% CAGR |

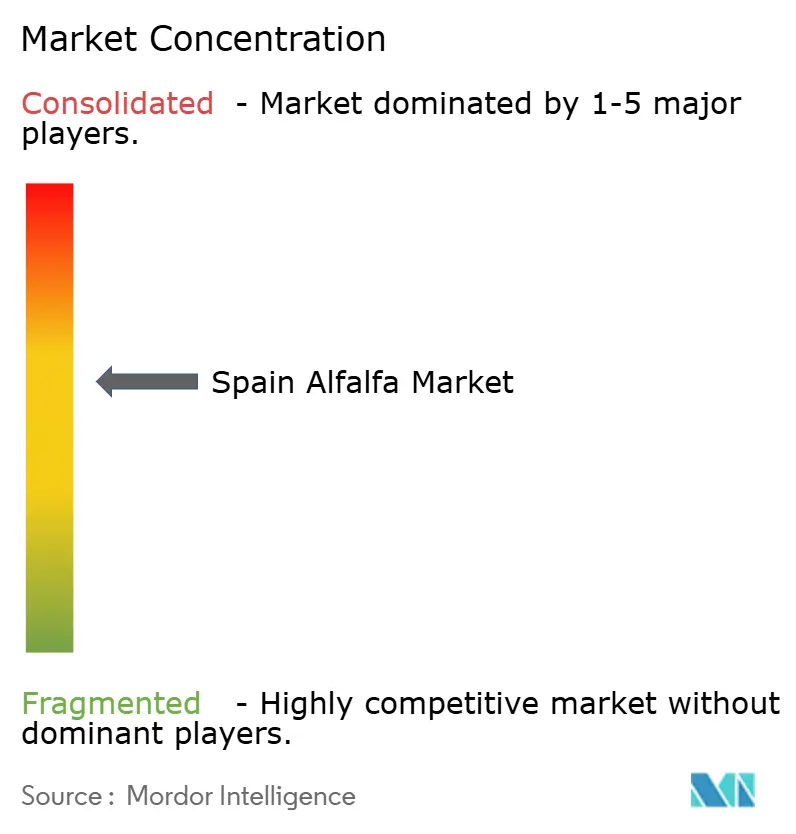

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Spain Alfalfa Market Analysis by Mordor Intelligence

The Spain Alfalfa Market size is expected to increase from USD 452 million in 2025 to USD 472.07 million in 2026 and reach USD 586.66 million by 2031, growing at a CAGR of 4.44% over 2026-2031. Spain's position as the world's largest exporter of dehydrated alfalfa is the primary factor supporting this growth, as export demand continues to shape planting, processing, and pricing decisions across the country. The Ebro Valley and the Monegros basin in Aragón account for most of Spain's dehydrated fodder output, and the region's four to five cuts per season keep dehydration plants active through the core summer months. Export demand also broadened in 2025, with stronger shipments to the Gulf, gains in South Korea, and increased buying from Morocco, which reduced dependence on a single export corridor. Additionally, premium pellets and traceable high-protein formats are opening higher-value channels for specialty animal nutrition, while irrigation upgrades, certification requirements, and water planning are reshaping how capacity is added in the market. As a result, while yields remain important, competitive advantage is now equally tied to export access, process control, and the ability to supply audited formats with reliable logistics.

Key Report Takeaways

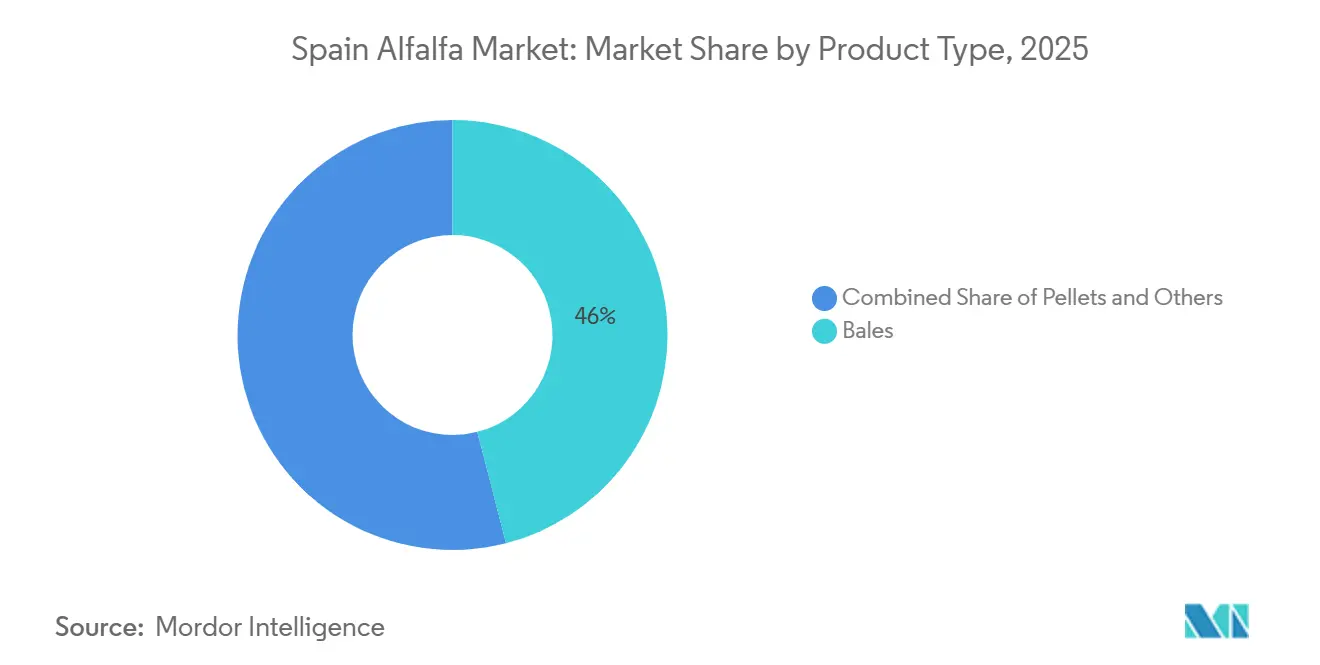

- By product type, bales is the largest segment and held 46.0% of the market share in 2025, while pellets is the fastest growing segment and is anticipated to expand at a 6.7% CAGR between 2026 and 2031.

- By application, dairy cattle feed is the largest segment and held 62.0% of the market size in 2025, while poultry feed is the fastest growing segment and is anticipated to expand at a 7.3% CAGR between 2026 and 2031.

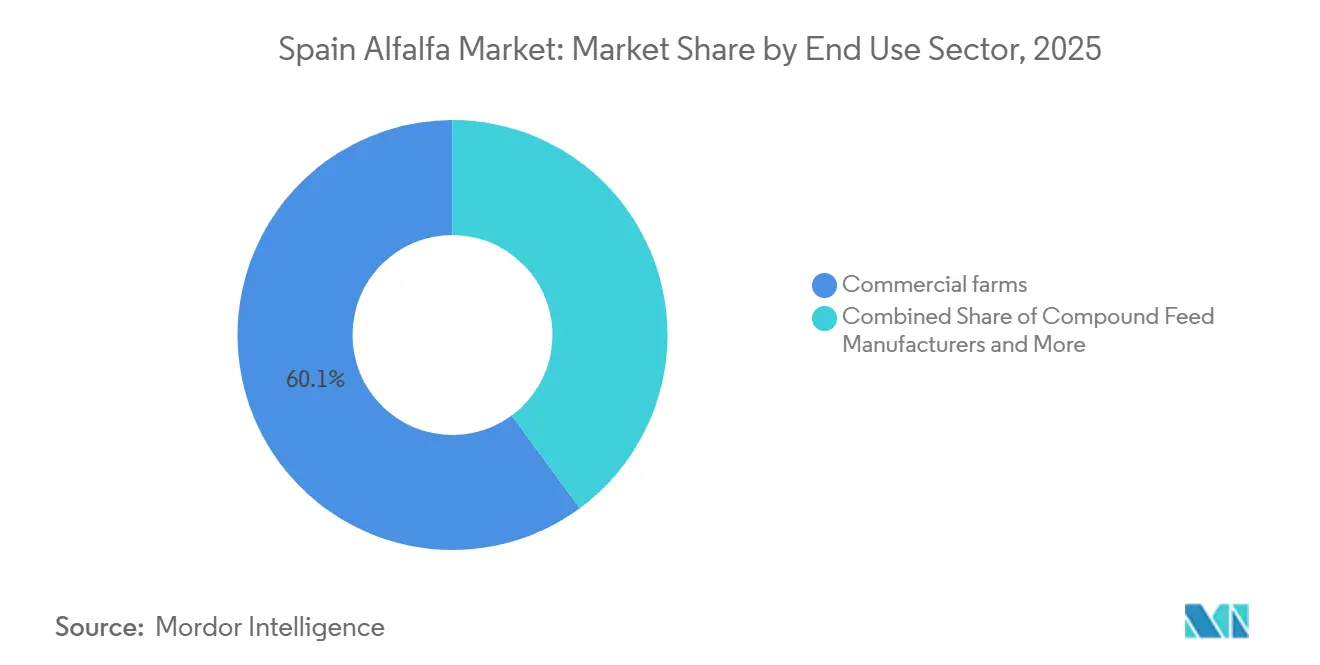

- By end use sector, commercial farms is the largest segment and held 60.1% of the market share in 2025, while pet food and specialty nutrition is the fastest growing segment and is anticipated to expand at a 9.0% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Spain Alfalfa Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aragón and catalonia dehydration corridor expansion | +1.2% | Spain, strongest in Aragón, Catalonia, and Navarra | Medium term (2-4 years) |

| Export demand from gulf feed and equine buyers | +1.1% | Spain, Saudi Arabia, UAE, Jordan, South Korea, Morocco | Short term (≤ 2 years) |

| CAP incentives for rotational forage crops | +0.8% | Spain and European Union-27, strongest in Spain | Long term (≥ 4 years) |

| Irrigated production advantage in the ebro valley | +0.9% | Spain, strongest in the Ebro Valley, Aragón, and Catalonia | Medium term (2-4 years) |

| Industrial dehydration and processing network | +0.7% | Spain with spillover into Gulf and Asian export routes | Medium term (2-4 years) |

| Shift toward traceable high-protein forage formats | +0.5% | Global, with early adoption in Spain and Gulf import markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Aragón and Catalonia Dehydration Corridor Expansion

The processing density in the Aragón and Catalonia corridor gives the Spain alfalfa market an advantage that other European suppliers struggle to match at industrial scale. The Los Monegros X and XI modernization project covers 6,800 hectares and is anticipated to be completed in 2026, with EUR 55 million (USD 59.4 million) in investment supporting pressure-fed irrigation networks to replace older systems. This transition reduces water use per hectare, improves field consistency, and shortens the time between cutting and plant intake, enabling processors to manage moisture more precisely before drying. It also supports private expansion decisions in the Spain alfalfa market, as processing plants add capacity more confidently when the surrounding raw material base becomes more reliable.

Export Demand from Gulf Feed and Equine Buyers

Export demand from Saudi Arabia and the UAE continues to anchor the Spain alfalfa market, with those two destinations together accounting for more than 280,000 metric tons in the 2024/25 campaign, representing approximately 40% of total export volume[1]Source: COAG Castilla y León “ALFALFA: From the lands of the Ebro and the Douro to the camel races of Dubai: the war in the Gulf puts the most exotic business in the Spanish countryside in check,” coag-cyl.org. These buyers are significant not only because of their volume but also because they source steady quantities of dehydrated forage for organized dairy, equine, and camel feeding systems that require consistent product quality and reliable shipping, with Spain being one of the key suppliers. South Korea strengthened external demand in 2024-25, with procurement rising 548.4%, indicating that Spanish processed formats retain room to penetrate East Asian feed channels. Morocco also increased purchases by 387.2% in the same campaign, reflecting how drought-related feed gaps in nearby markets can generate a secondary source of demand when conditions tighten elsewhere. This broader buyer mix makes the Spain alfalfa market more resilient than when the Gulf corridor dominated nearly all export planning, even though Gulf-bound trade still sets the basic tone for processor utilization and inventory strategy. The strong rebound in 2025 export volumes confirms that external demand remains the clearest near-term support for market growth.

CAP Incentives for Rotational Forage Crops

Policy support under Spain's Common Agricultural Policy (CAP) 2023–2027 Strategic Plan is helping stabilize the planted base in the Spain alfalfa market, particularly where growers compare rotation economics against cereals. The European Commission approved an amendment to the plan in August 2025, simplifying eco-scheme procedures and extending flexibility for forage rotation support. The amendment also specifies a 2025 payment level of EUR 69.32 per hectare (USD 74.9) for relevant multi-year forage rotations, which improves the relative return of alfalfa even when commodity conditions soften. Alfalfa's nitrogen-fixing role also reduces fertilizer requirements in subsequent cereal crops, adding rotation value beyond the price of the forage harvest itself. Research on soil conservation policy in Spain indicates that CAP-linked soil requirements are becoming more important for access to basic support, further reinforcing rotation continuity. This helps the Spain alfalfa market maintain a more stable production floor than a purely price-driven crop would typically sustain.

Irrigated Production Advantage in the Ebro Valley

The Ebro Valley remains the primary production hub of the Spain alfalfa market, as irrigation covers most of the cultivated area used for dehydrated fodder. The United States Department of Agriculture (USDA) reported that around 75% of Spain's dehydrated fodder land is irrigated, supporting a four to five cut cycle that rain-fed competitors in Central and Eastern Europe cannot consistently match [2].Source: United States Department of Agriculture “Spanish Fodder Production and Exports Set to Recover in New Marketing Year,” apps.fas.usda.govModernized drip systems are improving water productivity, meaning the same water allocation can support a larger effective production area than older flood irrigation methods allowed. This efficiency keeps the northeastern production base highly productive, rather than distributing output across regions with weaker water security. Southern regions retain growth potential, but drought pressure has made their contribution less reliable than the Ebro axis. As a result, the Spain alfalfa market is likely to remain concentrated in fewer but more efficient irrigated zones over the forecast period.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Water allocation pressure in irrigated growing zones | -1.0% | Spain, strongest in Aragón, Catalonia, and the Ebro Basin | Long term (≥ 4 years) |

| Heavy export dependence on a narrow buyer base | -0.9% | Spain, strongest across Gulf and China-facing trade flows | Short term (≤ 2 years) |

| Fuel cost sensitivity in dehydration plants | -0.8% | Spain nationally, with spillover from wider European Union energy conditions | Medium term (2-4 years) |

| Competition from alternative feed and forage sources | -0.6% | Global, especially European Union, Asia-Pacific, and North American dairy and livestock markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Water Allocation Pressure in Irrigated Growing Zones

Water policy remains the most significant structural risk to the Spain alfalfa market, as the most productive areas also depend heavily on irrigation. The Confederación Hidrográfica del Ebro (CHE) originally proposed cutting Ebro basin irrigation allocations by 12% to 15% for the 2028 to 2033 period, which raised concerns about raw material availability in the main production corridor. Aragón's regional government filed objections, and irrigator groups argued that lower allocations would weaken double-cropping economics and reduce the value of recent modernization works. The CHE signaled in November 2025 that it was reconsidering the proposal, but the issue remains relevant to medium-term planning. Drought conditions have already demonstrated how quickly supply risk can shift from policy debate to physical constraint, as seen in the 50% cut in irrigated crop area at the Ebro Delta during the Catalonia drought in 2024. The 14% decline reported for Aragón's 2026 campaign confirms that weather and water volatility are active operating issues for the Spain alfalfa market, not distant concerns.

Competition From Alternative Feed and Forage Sources

Alfalfa competes with corn silage, soybean meal, and fermented forage blends in dairy and beef cattle feed, with substitution largely driven by relative protein costs and supply availability. When soybean meal prices fall, cost-sensitive dairy buyers can reduce alfalfa inclusion in feed formulations, lowering demand for Spanish processors. Romanian and United States producers are also expanding dehydrated alfalfa capacity, increasing competition for Gulf and Asian buyers that Spain had previously supplied more consistently. AEFA director Luis Machín stated in 2025 that Spain's export target of more than 1 million metric tons per year now faces structural pressure from these competing origins. In poultry and small ruminant feed, locally produced fresh forage and manufactured pellet blends can also replace imported Spanish product due to lower freight costs in domestic markets. This substitution pressure is most pronounced in the commodity bale segment, where buyers can switch suppliers easily on price, while premium traceable and certified formats remain a more defensible position for Spanish producers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Bales Anchor Export Volumes While Pellets Redefine Growth

Bales held the largest share of 46.0% of the Spain alfalfa market in 2025, remaining the dominant format by value and the primary product form driving Spain's export activity. Their dominance reflects continued reliance by Gulf and Korean buyers on bale shipments for dairy, equine, and feed operations that require stable moisture and high protein retention. Cubes play a smaller but functional role in markets where storage space is limited, particularly in North Africa and parts of East Asia that require denser packaged forage. Compressed bales serve a distinct premium niche, as Gulf equine buyers prefer high-density formats that are easier to store and handle through port logistics. These product distinctions indicate that the Spain alfalfa market supplies a range of processed formats designed around different shipping, storage, and end-animal requirements, rather than a single standard feed item. This product mix also allows processors to spread risk across buyers with different handling systems and nutrition goals.

The Spain alfalfa market size for pellets is projected to grow the fastest at a 6.7% CAGR between 2026 and 2031. Pellet demand is rising across two fronts simultaneously, with large-volume fibrous pellets moving into livestock feed channels and smaller premium pellets moving into specialty nutrition applications. This shift is significant because pellet growth is no longer tied solely to commodity livestock rations, allowing processors to target higher-value channels with stricter specifications. In the market, this change favors operators that can control particle size, microbial quality, and batch traceability without disrupting throughput. Asociación Española de Fabricantes de Alfalfa Deshidratada's (AEFA) 2026 promotion efforts in Vietnam and China reflect the market's attempt to broaden processed-format demand beyond the Gulf corridor. These efforts support the broader Spain alfalfa market by opening underpenetrated Asian channels for products that ship and store efficiently. Over time, pellets are likely to matter less for volume alone and more for their contribution to average realized value across the product mix. This makes pellets central to growth quality, even though bales continue to dominate current revenue.

By Application: Dairy Cattle Feed Provides a Base, Poultry Opens a Fast Lane

Dairy cattle feed held the largest share of 62.0% in the Spain alfalfa market by application in 2025. This position reflects consistent demand from Spain's domestic dairy regions, as well as export-linked supply relationships with organized dairy operators outside the country. Contracted supply routes between processors in Aragón and Navarra and dairy areas such as Galicia, Cantabria, and Castile y León provide logistical continuity that does not shift quickly from one season to the next. This stability gives the Spain alfalfa market a reliable outlet even when export timing becomes uneven. Equine and camel segments are smaller in tonnage but command higher prices, as buyers require certified, dust-free, and consistent material. The application mix therefore gives Spain both a stable bulk base and a profitable high-specification niche. This balance reduces the risk of any single end-animal category dominating processor economics and helps explain why product quality is a key consideration in a market that is still often described in simple forage terms.

The Spain alfalfa market for poultry feed is projected to grow the fastest at a 7.3% CAGR between 2026 and 2031. This growth reflects changing feed formulation practices that use alfalfa-derived xanthophylls in place of synthetic colorants for egg-yolk and broiler-skin performance. Small ruminant feed remains a steady domestic outlet, as sheep and goat systems value the same combination of protein and fiber that supports dairy and breeding animals. The market therefore serves a wider application base than export volume alone might suggest. Poultry is becoming an increasingly important application not because it will overtake dairy in the near term, but because it strengthens the value of processed output. The application profile is widening in a way that supports both resilience and margin, a pattern that should keep dairy as the anchor while allowing poultry and specialty uses to drive faster growth.

By End Use Sector: Commercial Farms as the Central Pivot, Specialty Nutrition as the Outlier

Commercial farms held the largest share of 60.1% in the Spain alfalfa market in 2025. Their role is structural, as these farms typically purchase at scale, contract across multiple product formats, and provide the base demand that dehydration plants rely on for utilization planning. This makes commercial farms the operational center of the Spain alfalfa market, even as export destinations receive more public attention than domestic procurement structures. Compound feed manufacturers represent a second major outlet, incorporating alfalfa meal and pellets into blended rations for commercial livestock systems that do not source all ingredients directly. Their consolidation strengthens the position of large processors, as buyers prefer suppliers capable of delivering consistent batches at industrial scale. Household and hobby animal owners form a much smaller segment, but they purchase in small packs and typically pay significantly higher unit prices than bulk export customers, making them commercially relevant despite their limited tonnage. End-use concentration therefore favors processors with broad product portfolios and steady supply commitments.

Pet food and specialty nutrition is projected to record the fastest growth at a 9.0% CAGR between 2026 and 2031. This channel is attractive because dehydrated alfalfa pellets meeting specialty specifications command a 15% to 20% price premium over standard livestock pellets. The domestic companion animal feed channel is also expanding, giving processors a local outlet for premium-format pellets alongside export demand. Within the Spain alfalfa market, this is one of the clearest indicators that value is shifting downstream toward functional ingredients rather than remaining concentrated in bulk dehydrated forage. Processors that already operate certified production systems are better positioned to capture this shift, as the channel presents higher barriers to entry than mainstream livestock feed. The segment will remain smaller than commercial farms in absolute revenue during the forecast period, but its growth rate makes it strategically important. It also provides the market with a domestic premium path that is less exposed to shipping disruptions than export-heavy segments, which matters in a market where logistics shocks can still alter sales timing quickly. Specialty nutrition therefore remains an outlier segment, but one that is becoming increasingly influential.

Geography Analysis

Aragón and Lleida in Catalonia contributed around 80% of Spain's dehydrated alfalfa output, making the Spain alfalfa market geographically concentrated in a narrow but highly efficient production corridor. Irrigation across most of the cultivated area supports the four to five cut cycle that gives this corridor its output and protein advantage. The Los Monegros modernization project is improving water delivery, extending the effective irrigated area, and helping the Spain alfalfa market defend its most productive base. Navarra remains smaller in absolute output, but its use of precision irrigation and carbon-linked pilot practices gives it a profile that appeals to buyers focused on traceability and sustainability.

Castile y León and Castile-La Mancha together contribute around 20% of national dehydrated output, making them important supporting regions rather than the primary production center [3]Source: United States Department of Agriculture “Spanish Fodder Production and Exports Set to Recover in New Marketing Year,” apps.fas.usda.gov. According to the USDA, approximately 70% of Castile y León's alfalfa area is rain-fed, creating a different risk profile compared to the irrigation-led northeast. In the 2024-25 season, production in Navarra grew by 27%, Catalonia by 25%, and Castile-La Mancha by 23%, indicating that secondary regions responded actively to stronger pricing and rotation incentives. Andalusia benefits from a long frost-free period and favorable shipping proximity to North African routes, but weaker reservoir conditions limit its output. As a result, the Spain alfalfa market continues to rely more on the irrigated northeast than on broader national production.

Saudi Arabia and the UAE together accounted for a significant share of Spain's export volumes. China took 84,088 metric tons and South Korea took 61,905 metric tons in the same campaign, with growth of 60.9% and 548.4% respectively, indicating that East Asia is becoming a more relevant demand layer. The Strait of Hormuz disruption in early 2026 highlighted how sensitive Spanish production economics remain to Gulf shipping routes. According to AEFA, Morocco's 387.2% surge and stronger push into Asian markets indicate that export diversification is progressing, though a few high-impact corridors continue to dominate the export landscape.

Competitive Landscape

The top five producers in the Spain alfalfa market held a major share of combined revenue in 2025. This level of concentration creates a clear leading tier in the market, while still leaving meaningful room for mid-sized operators across producing regions. Al Dahra Agriculture LLC's Spanish platform is notable for integrating farm ownership, dehydration, and direct export logistics within a single operating model. Its Al Dahra Fagavi unit operates six facilities across Lleida and Aragón, providing coverage across the country's most productive belt. In the Spain alfalfa market, this type of vertical integration reduces decision cycles between cutting schedules, plant throughput, and shipment planning.

Processing scale is only one dimension of competition. Proximity to ports such as Barcelona, Cartagena, and Almería also shapes delivered economics in export trade. The Ebro axis holds an advantage in this regard, as product can move from Zaragoza to Barcelona for container loading within 24 hours. This logistical advantage supports higher asset utilization and allows larger firms to respond more quickly to sudden shifts in export demand. Several leading operators are also installing biomass boilers fueled by almond shells and olive pits, with these retrofits capable of reducing fossil gas consumption by as much as 60%. As a result, the Spain alfalfa market is increasingly divided between plants that can invest in process efficiency and those that remain exposed to tighter margin pressure.

A further competitive opportunity exists in premium nutrition formats, where higher-specification pellets command better pricing than standard livestock material. Producers that can operate certified lines, document traceability, and maintain consistent quality are better positioned to capture this demand than firms focused solely on bulk dehydration. Several operators in Castile y León and Navarra are also testing contract-farming structures that combine agronomic support with minimum-price assurances, helping to secure supply ahead of new capacity additions. Competitive advantage in the Spain alfalfa market is therefore shifting toward audited supply, reliable logistics, and value-added processing rather than volume alone.

Spain Alfalfa Industry Leaders

Alfalfa Monegros S.L.

Grupo Osés Agroalimentaria S.L. (NAFOSA)

Alfeed (EXPORTACION ALFALFA FEED SL.)

Al Dahra ACX Global Inc.

AE Group, S.L.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: The European Commission approved an amendment to Spain's CAP 2023–2027 Strategic Plan, introducing simplified eco-scheme application processes and extended flexibility for forage crop rotation payments under the EAGF. The amendment is anticipated to sustain farmer uptake of multi-year alfalfa rotation programs through 2027.

- May 2025: Irrigation modernization works at the Los Monegros X and XI canal sectors, covering 6,800 hectares and benefiting 524 farmers across Lalueza, Capdesaso, Albalatillo, and Sariñena, advanced toward mid-2026 completion with total investment of EUR 55 million (USD 59.4 million) funded through Spain's Recovery Plan. Conversion from flood and diesel-pump systems to natural-pressure networks will reduce water consumption per hectare while expanding effective irrigated area for alfalfa cultivation.

- November 2025: The CHE indicated it was reconsidering its proposed 12% to 15% reduction in Ebro basin irrigation allocations for the 2028–2033 plan following formal objections from the Aragón regional government and Ferebro. The revision entered a new technical review cycle.

Spain Alfalfa Market Report Scope

Alfalfa is obtained from the alfalfa plant, also known as lucerne and Medicago sativa. It is cultivated as an important forage crop and is widely used in animal nutrition because of its high protein content and forage value.

The Spain Alfalfa Market is Segmented by Product Type (Bales, Pellets, Cubes, and Compressed Bales), by Application (Dairy Cattle Feed, Beef Cattle Feed, Poultry Feed, Equine Feed, Small Ruminant Feed, Camelids and Other Livestock Feed), by End Use Sector (Commercial Farms, Compound Feed Manufacturers, Household and Hobby Animal Owners, and Pet Food and Specialty Nutrition). The Market Size and Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

By Product Type

| Bales |

| Pellets |

| Cubes |

| Compressed Bales |

By Application

| Dairy Cattle Feed |

| Beef Cattle Feed |

| Poultry Feed |

| Equine Feed |

| Small Ruminant Feed |

| Camelids and Other Livestock Feed |

By End Use Sector

| Commercial Farms |

| Compound Feed Manufacturers |

| Household and Hobby Animal Owners |

| Pet Food and Specialty Nutrition |

| By Product Type | Bales |

| Pellets | |

| Cubes | |

| Compressed Bales | |

| By Application | Dairy Cattle Feed |

| Beef Cattle Feed | |

| Poultry Feed | |

| Equine Feed | |

| Small Ruminant Feed | |

| Camelids and Other Livestock Feed | |

| By End Use Sector | Commercial Farms |

| Compound Feed Manufacturers | |

| Household and Hobby Animal Owners | |

| Pet Food and Specialty Nutrition |

Key Questions Answered in the Report

What is the 2031 value forecast for Spain alfalfa?

The Spain alfalfa market is forecasted to reach USD 586.66 million by 2031, up from USD 472.07 million in 2026, at a 5.2% CAGR between 2026 and 2031.

Which product format leads revenue in Spain alfalfa?

Bales led product revenue with a 46.0% share in 2025, reflecting their continued role as the main export format for large overseas buyers.

Which application is growing the fastest in Spanish alfalfa demand?

Poultry feed is projected to grow the fastest, with a 7.3% CAGR between 2026 and 2031, as feed formulations increasingly use alfalfa-derived functional inputs.

What is the main risk facing Spanish dehydrated alfalfa exporters?

The main risk is export concentration, since Saudi Arabia and the UAE still account for aa major export volume and route disruptions can quickly interrupt shipments.

Page last updated on: