Market Overview

| Study Period | 2021 - 2031 |

|---|---|

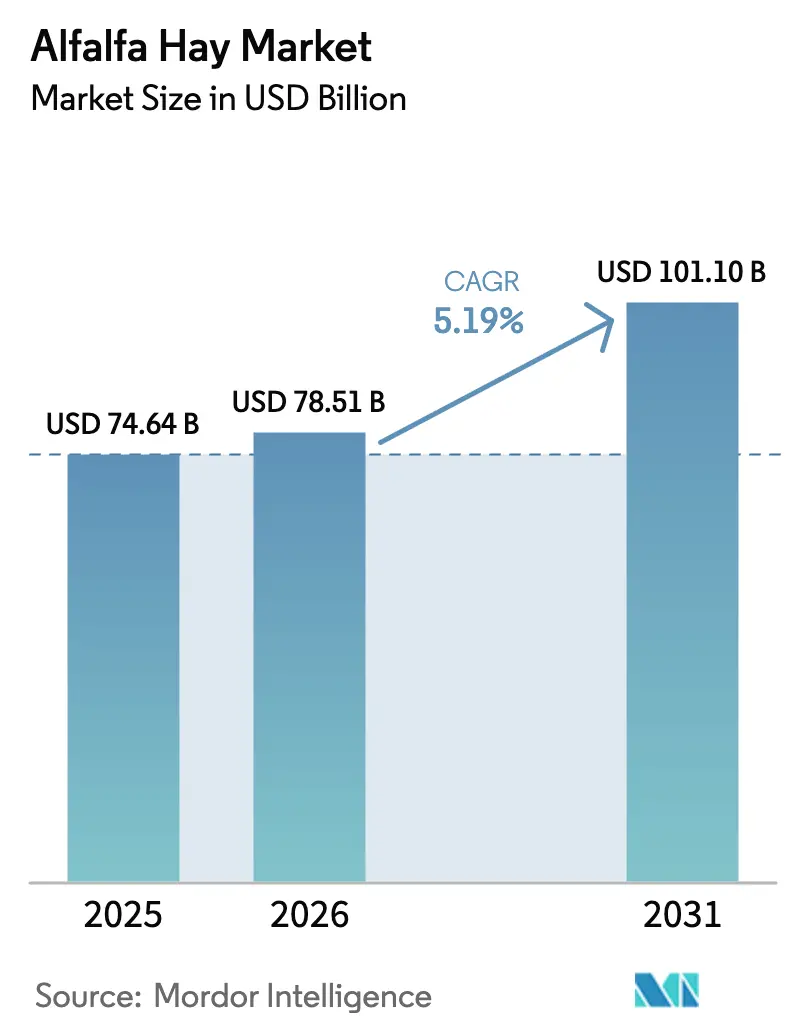

| Market Size (2026) | USD 78.51 Billion |

| Market Size (2031) | USD 101.10 Billion |

| Growth Rate (2026 - 2031) | 5.19% CAGR |

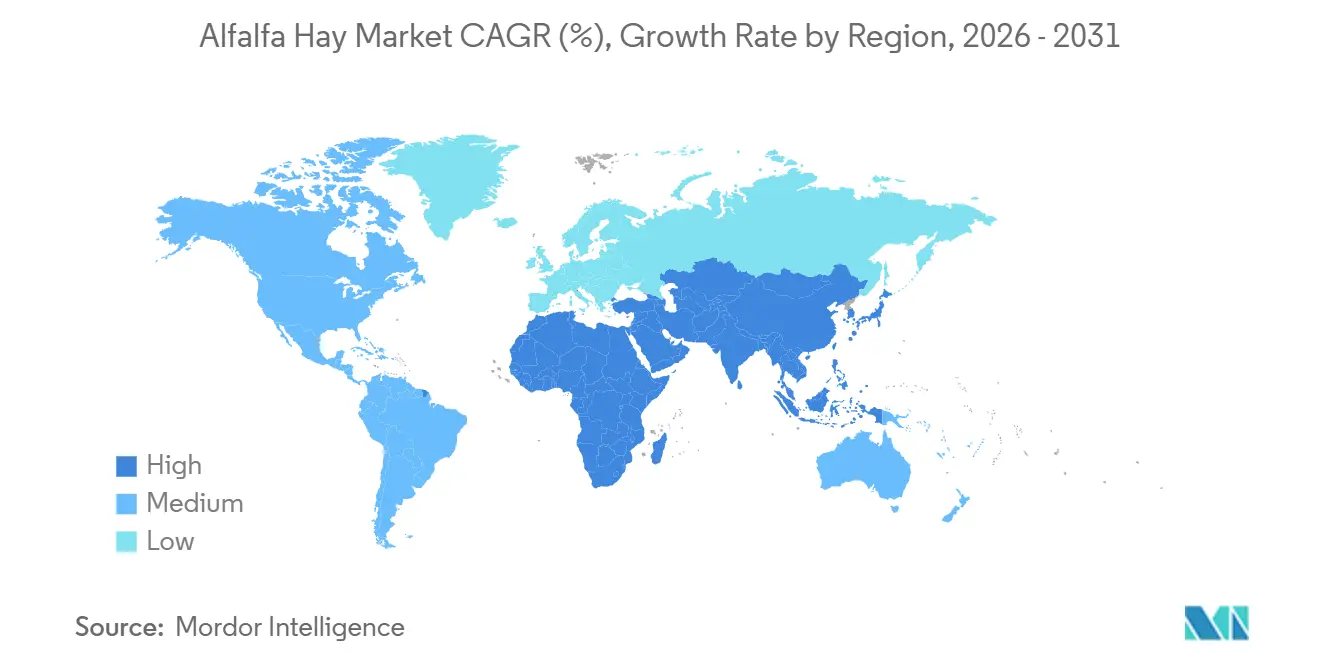

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Alfalfa Hay Market Analysis by Mordor Intelligence

The alfalfa hay market size was valued at USD 74.64 billion in 2025 and estimated to grow from USD 78.51 billion in 2026 to reach USD 101.1 billion by 2031, at a CAGR of 5.19% during the forecast period (2026-2031). Growth is driven by dairy intensification across the Asia-Pacific, food security mandates in the Middle East, and technological advancements that enhance processing efficiency while reducing spoilage. North America remains the largest producing hub, and acreage is shifting as the Colorado River cuts tighten water availability, prompting growers to shift toward higher-value grades and pelletized formats. Import demand is accelerating in Saudi Arabia and the United Arab Emirates, where strict water limits constrain domestic cultivation. At the same time, e-commerce is unlocking new pockets of premium demand from pet and equine owners who prize dust-free nutrition and traceable sourcing.

Key Report Takeaways

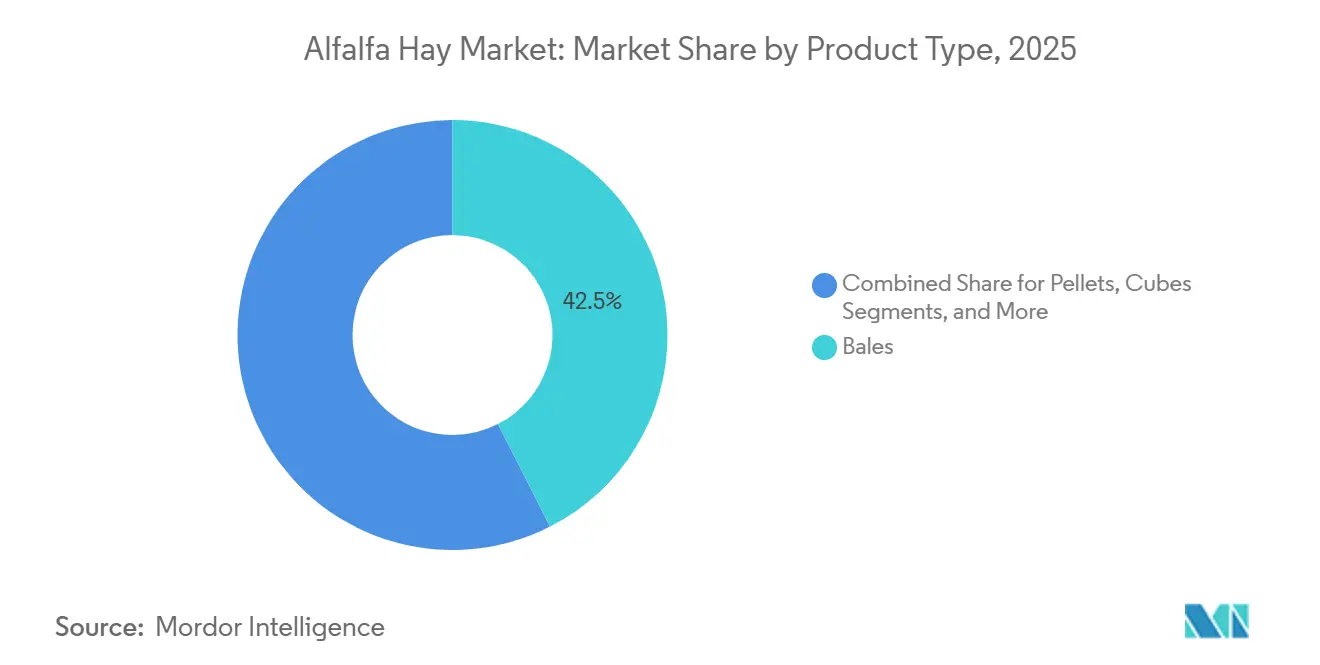

- By product type, bales led with a 42.5% alfalfa hay market size in 2025, while dehydrated pellets are projected to advance at an 8.4% CAGR through 2031.

- By grade, premium (RFV 170-185) captured 33.0% of the alfalfa hay market size in 2025, and Supreme (RFV More Than 185) is projected to grow at a 6.9% CAGR through 2031.

- By processing technology, field-dried conventional methods accounted for 41.2% of the 2025 value, and solar-assisted dehydration is projected to grow at a rate of 9.7% through 2031.

- By distribution channel, export trading houses led with a 37.3% revenue share in 2025, while e-commerce platforms are projected to grow at an 8.8% CAGR through 2031.

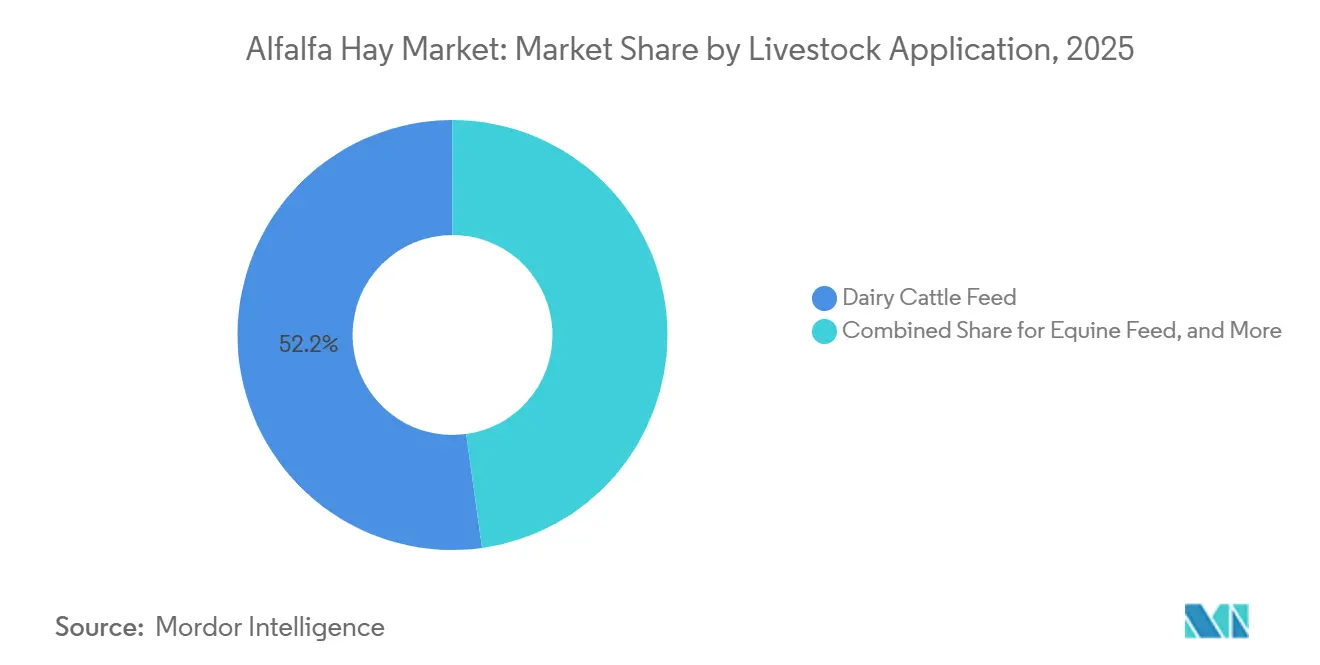

- By livestock application, dairy cattle feed accounted for 52.2% of the value in 2025, while the equine segment is growing at an 8.5% CAGR through 2031.

- By end-use sector, commercial farms held 60.1% of the market in 2025, while the pet-food and specialty segment is growing at a 9.0% CAGR through 2031.

- By geography, North America led with a 36.2% revenue share in 2025, while the Asia-Pacific region is projected to grow at a 6.8% CAGR through 2031.

- AL Dahra ACX Global Inc., Standlee Premium Products, LLC, Riverina Stockfeeds, Green Prairie International Inc, and Border Valley Trading were among the leading companies in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Alfalfa Hay Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Dairy and Animal-Protein Demand Surge | +1.2% | Global, with a concentration in Asia-Pacific and the Middle East | Long term (≥ 4 years) |

| Government-Backed Forage Import Quotas Expand | +0.9% | Middle East core, Asia-Pacific secondary | Medium term (2-4 years) |

| Superior Protein and Fiber Profile vs Other Forage | +0.8% | Global | Long term (≥ 4 years) |

| Carbon-Credit Monetization of Regenerative Rotations | +0.4% | North America and Europe, with early adoption in select South American markets | Medium term (2-4 years) |

| IoT-Enabled In-field Drying Tech Cuts Post-Harvest Loss | +0.5% | North America and Asia-Pacific, with spill-over to the Middle East import specifications | Short term (≤ 2 years) |

| Premium Pet and Equine Nutrition Channels Accelerate | +0.6% | Global, led by North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Dairy and Animal-Protein Demand Surge

China's dairy herd reached 6.2 million heads in 2024, supporting 41.97 million metric tons of milk output, a 2.1% increase over the prior year. Meanwhile, per-capita consumption climbed to 43 kilograms annually as urbanization and cold-chain expansion penetrated tier-two and tier-three cities [1]Source: National Bureau of Statistics of China, “National Dairy Data,” stats.gov.cn. High-yielding Holstein operations require 18 to 22 kilograms of dry-matter forage per cow per day, and alfalfa's 18% to 22% crude-protein content makes it the benchmark roughage for balancing concentrate-heavy rations that target 10,000 to 12,000 liters of annual milk production. Middle Eastern governments are locking in multi-year import agreements as Saudi Arabia's Ministry of Environment, Water, and Agriculture confirmed the phase-out of domestic alfalfa cultivation by the 2027-2028 marketing year to conserve groundwater, redirecting demand to suppliers in the United States, Spain, and Argentina.

Government-Backed Forage Import Quotas Expand

The United Arab Emirates' National Food Security Strategy 2051 designated forage as a critical commodity, prompting state-backed entities such as AL Dahra to secure long-term acreage contracts in California's Imperial Valley and Washington's Columbia Basin, ensuring supply continuity despite domestic water constraints. Saudi Arabia extended tariff exemptions on alfalfa imports through 2026 and allocated USD 1.2 billion in subsidies for cold-storage infrastructure at Jeddah and Dammam ports, thereby reducing spoilage rates and enabling year-round inventory buffers for the kingdom's 400,000-head dairy herd. China's General Administration of Customs granted phytosanitary clearance to additional United States export facilities in 2024, increasing the approved supplier count from 87 to 104 and signaling Beijing's intention to diversify away from Australian and Canadian sources that had faced periodic trade friction.

Superior Protein and Fiber Profile vs Other Forage

Alfalfa delivers 18% to 22% crude protein and 30% to 35% neutral detergent fiber, outperforming grass hay at 8% to 12% protein and 55% to 60% fiber, which positions it as the preferred forage for high-production dairy rations targeting 35 to 40 liters of milk per cow per day. The crop's deep taproot accesses subsoil moisture and nutrients unavailable to annual grasses, yielding 8 to 12 metric tons per acre under irrigation compared to 3 to 5 metric tons for timothy or orchardgrass, and its nitrogen-fixing symbiosis with Rhizobium bacteria deposits 150 to 200 pounds of nitrogen per acre annually, reducing input costs for subsequent rotations of corn or wheat. Beef feedlots blend alfalfa at 5% to 10% of dry-matter intake to buffer rumen pH and prevent acidosis in high-grain finishing diets, supporting average daily gains of 3.5 to 4.0 pounds and improving carcass marbling scores.

Carbon-Credit Monetization of Regenerative Rotations

Alfalfa's perennial root system sequesters 0.5 to 1.2 metric tons of carbon per acre annually in the top 30 centimeters of soil, and low-till or no-till establishment practices preserve the soil structure and microbial communities that enhance organic matter accumulation. Indigo Ag's carbon-credit program enrolled over 500,000 acres of alfalfa rotations in Montana, Wyoming, and South Dakota by 2025, paying growers USD 15 to USD 20 per metric ton of verified carbon sequestration, which translates to USD 7.50 to USD 24 per acre in supplemental revenue.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Water-Footprint and Drought Policy Pressure | -0.7% | North America (United States West), Southern Europe, spill-over to Australia | Medium term (2-4 years) |

| Ocean-Freight and Container-Rate Volatility | -0.5% | Global trade lanes, particularly the trans-Pacific and Middle East routes | Short term (≤ 2 years) |

| Rise of Hydroponic Fodder and Alternative Roughage | -0.3% | Middle East, North America high-tech dairy operations | Long term (≥ 4 years) |

| Phytosanitary Barriers in Export Lanes | -0.4% | United States-China, United States-Korea, Australia-China trade corridors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Water-Footprint and Drought Policy Pressure

Arizona's groundwater-management framework restricted new irrigation permits in the Phoenix and Tucson Active Management Areas in 2024, and the state's share of Colorado River water dropped by 1.04 million acre-feet under the 2023 Drought Contingency Plan, forcing alfalfa acreage to contract by an estimated 85,000 acres, or 12%, between 2023 and 2025 [2]Source: Arizona Department of Water Resources, “Groundwater Management Updates,” azwater.gov. California's Sustainable Groundwater Management Act mandated basin-level pumping reductions by 2040, and interim allocations in the San Joaquin Valley resulted in a 20% to 30% cut in irrigation deliveries in critically overdrafted sub-basins, prompting growers to fallow marginal fields or shift to lower-water-use crops, such as pistachios and almonds.

Ocean-Freight and Container-Rate Volatility

Trans-Pacific container rates from the United States West Coast to China fluctuated between USD 2,800 and USD 4,200 per forty-foot equivalent unit during 2024 and 2025, driven by port congestion, chassis shortages, and labor negotiations at Los Angeles and Long Beach terminals. Alfalfa's low value-to-weight ratio, typically ranging from USD 250 to USD 350 per metric ton for export-grade material, results in freight costs accounting for 30% to 45% of the delivered price in the Asia-Pacific region. Increases in freight rates reduce importer margins or necessitate retail price hikes, which can suppress demand.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Bales Retain Leadership While Pellets Accelerate

Bales account for 42.5% of the alfalfa hay market size in 2025, supported by established handling systems and widespread adoption among livestock operators. Mechanized dairy farms prefer large square bales, while round bales provide weather protection for extensive beef operations. This format diversity ensures consistent demand across different regions. Dehydrated pellets, representing a smaller market share, are experiencing an 8.4% CAGR through 2031, driven by automated feeding systems and increased container-load density that reduces ocean transportation costs. Pellets also provide consistent quality, simplifying formulation processes for compound feed mills serving the dairy and equine markets.

Mobile pellet line investments generate premiums of USD 30-40 per metric ton above bale prices, compensating for increased energy consumption. Cubes and compressed bales cater to the equine and small-ruminant segments, where users prioritize convenience over cost. Field dryers that reduce moisture content to below 12% within 1.5 hours minimize weather-related risks during harvest periods. These technological advancements strengthen the alfalfa hay market and accelerate the transition to processed formats.

By Grade/Quality: Supreme Grade Captures Value

Premium (RFV 170-185) captured 33.0% of the alfalfa hay market share in 2025, serving the core dairy and beef feedlot segments that balance nutrition and cost. Premium grade (RFV 170-185) maintains its dominant position among commercial dairy farms by providing an optimal balance between cost and milk production targets. Good grade serves primarily beef cattle operations that focus on cost-effective digestible protein content. Fair and Utility grades are showing a declining market presence as buyers implement stricter mycotoxin and contaminant limits. The United States Department of Agriculture (USDA's) hay-grading standards, codified in the Agricultural Marketing Service's handbook, provide voluntary quality benchmarks, export markets increasingly reference private specifications, such as the Japanese Standard for Imported Hay, which imposes stricter thresholds for ash, acid-detergent fiber, and visual color scores[3]Source: USDA Agricultural Marketing Service, “Hay Grading Standards,” ams.usda.gov.

Supreme (RFV More Than 185) is projected to grow at a 6.9% CAGR through 2031. Supreme hay, harvested at early-bloom or pre-bloom stages with leaf-to-stem ratios exceeding 60:40, fetched USD 380 to USD 450 per metric ton at United States West Coast ports in 2025, a 25% to 35% premium over premium grades, and Japanese importers specified moisture below 12%, foreign-material content under 1%, and stem length under 1.5 inches to minimize feed refusals and maximize butterfat yields. Quality assessments revealed the presence of mycotoxins in all tested Chinese samples, prompting premium buyers to shift toward North American suppliers. Producers who implement precise harvest timing, efficient field drying methods, and advanced storage monitoring systems can secure price premiums of USD 50-60 per metric ton, demonstrating the market's value differentiation based on quality standards.

By Processing Technology: Solar-Assisted Systems Gain Traction

Field-dried conventional methods accounted for 41.2% of the 2025 value, primarily due to their low capital requirements. Solar-assisted dehydration is projected to grow at a 9.7% CAGR through 2031, as producers seek to reduce weather dependency and minimize environmental impact. Research by the United States National Institute of Food and Agriculture demonstrates the economic viability of small and medium-sized farms in regions with solar insolation exceeding 4.5 kWh/m²/day. Forced-air mobile dryers offer operational flexibility in humid areas, while rotary drum facilities produce export-quality hay with precise moisture and color control.

The integration of solar pre-heating with rotary stabilization reduces fuel consumption by 25% compared to traditional methods. These operational efficiencies, combined with potential carbon credit benefits, support capital investment and are projected to increase the market share of processed alfalfa hay during the forecast period.

By Distribution Channel: Export Trading Houses Dominates

Export trading houses accounted for a 37.3% revenue share in 2025, benefiting from established buyer relationships and robust port logistics infrastructure. E-commerce platforms are projected to grow at an 8.8% CAGR through 2031, as mobile connectivity expands among producers and small retailers. In the Philippines, pilot programs demonstrated a 12% improvement in farm-gate prices when digital bidding replaced traditional intermediaries. Direct farm-gate transactions maintain strong loyalty in local markets, while feed integrators purchase bulk quantities to maintain formulation consistency across multiple animal feed lines.

E-commerce platforms enable subscription models that lock in recurring revenue, and SmallPetSelect reported 40% of its 2025 alfalfa sales came from auto-ship customers who receive monthly deliveries of 10-pound or 25-pound bags, smoothing seasonal demand volatility and providing growers with forward visibility. Quality verification remains the primary challenge for online transactions. Blockchain-based traceability systems and third-party inspection services are being developed to verify RFV levels and contaminant thresholds before shipment. Companies implementing these verification tools expand their revenue sources and increase their potential customer base in the alfalfa hay market.

By Livestock Application: Dairy Cattle Dominates but Equine Segment Rises

Dairy operations occupied 52.2% of the alfalfa hay market size in 2025, driven by the growing livestock population. High-yielding dairy operations require 18 to 22 kilograms of dry-matter forage per cow per day to balance concentrate-heavy rations and support rumen health. Research indicates that 1 kg of high-lysine alfalfa can increase milk yield by 0.44 kg compared to isocaloric grass hay rations. Beef cattle operations utilize good-grade alfalfa in finishing diets, although consumption is influenced by price. In poultry feed, alfalfa meal is primarily used as a source of xanthophyll pigments for egg yolk coloration. Camelids and small ruminants benefit from alfalfa's digestible fiber content.

The equine segment demonstrates the highest growth rate at 8.5% CAGR through 2031, driven by sport-horse owners' requirements for dust-free pellets and cubes. In the United States, the horse population is about 7.2 million, with premium positioning in performance, show, and breeding segments, where owners pay USD 25 to USD 40 per 50 pound bag for dust-free cubes and pellets that support bone density and coat quality. These buyers typically pay premiums of over USD 60 per metric ton above dairy-grade alfalfa, encouraging dedicated production. The diverse application portfolio creates stable demand across the alfalfa hay market, minimizing dependence on individual livestock sectors.

By End-Use Sector: Commercial Farms and Specialty Nutrition Lead Growth

Commercial farms accounted for 60.1% of consumption in 2025, encompassing dairy operations with 100 to 5,000 head, beef feedlots with 1,000 to 50,000 head capacity, and diversified livestock enterprises that purchase hay in truckload or railcar quantities, prioritizing cost per unit of protein and fiber over brand or packaging. They leverage economies of scale and organized procurement systems. Dairy processors establish forward contracts with growers to secure pricing and ensure consistent protein levels. Compound-feed manufacturers process alfalfa into extruded feed blends for various animal species, adding value to the supply chain.

The pet food and specialty nutrition segments demonstrate the highest growth rate, at 9.0% CAGR through 2031, driven by increasing pet humanization trends. Pet food and specialty nutrition channels are growing at an annual rate of 9.0% as small-animal owners shift to cubed and pelleted formats sold through online platforms. Companies implement strict quality standards for mycotoxins, heavy metals, and pesticides, requiring suppliers to establish on-farm testing systems to ensure compliance with these standards. While household and hobby-animal owners represent a fragmented market segment, their shift toward e-commerce purchases in 20-40 kg packages expands retail distribution for alfalfa hay.

Geography Analysis

North America accounted for 36.2% of 2025 revenue, supported by mechanized operations, quality grading systems, and access to Pacific export terminals. The United States' hay production increased by 3.3% to 122.5 million metric tons in 2024, though water policy changes in Arizona and California pose risks to production areas. Increasing dairy herd productivity, advancements in water-efficient irrigation systems, and improved container port turnaround times along the United States' West Coast are contributing to demand-supply imbalances, supporting higher prices for premium forage. Factors such as higher protein inclusion rates in dairy feed, the growing preference for organic and non-genetically modified (GMO) forage, and the release of additional acreage from the Conservation Reserve Program (CRP) are driving volume growth.

Asia-Pacific is anticipated to grow at a 6.8% CAGR through 2031. The modernization of dairy operations in India and the Southeast Asia-Pacific region drives feed demand, while China maintains its position as one of the largest importer despite adjustments in volume. While China aims to expand domestic production, near-term import requirements persist due to herd growth. Australia's hay supply constraints following the suspension of the Nammuldi project highlight climate-related vulnerabilities.

Europe maintains a stable demand with an emphasis on sustainability and traceability, where producers with carbon certifications gain market advantages. South America is developing as a competitive exporter, particularly in Chile and Argentina, benefiting from suitable climate conditions and improved port facilities. Middle Eastern markets continue to depend on imports due to water limitations, with Saudi Arabia becoming the second-largest importer in 2024, surpassing Japan. Africa shows initial growth potential as commercial dairy operations expand in Kenya and Nigeria, indicating future opportunities in the alfalfa hay market.

Competitive Landscape

The alfalfa hay market remains fragmented, with the top AL Dahra ACX Global Inc., Standlee Premium Products, LLC, Riverina Stockfeeds, Green Prairie International Inc., and Border Valley Trading, holding significant market shares in 2025. Larger operators benefit from economies of scale, allowing them to invest in solar dehydration, bale compression, and blockchain traceability systems. The market is experiencing vertical integration as compound feed producers acquire farmland to secure protein inputs, while farm equipment manufacturers collaborate with cooperatives to develop precision harvesting systems.

The market shows increased innovation through patent activity, particularly in on-the-go drying systems that achieve energy consumption of 1,100-1,200 BTU per pound of water removed. Companies implementing sustainability practices gain competitive advantages through carbon credit monetization, helping maintain profitability despite reduced commodity margins. Hydroponic-fodder production offers a year-round supply with 90% reduced water consumption, though high capital requirements currently limit its application to equine and pet-food segments.

Regional consolidation patterns vary significantly. North American operations trend toward larger consolidated farm blocks, while the Asia-Pacific region maintains a diverse base of smallholder suppliers serving domestic dairy operations. The formation of freight-forwarding alliances and shared dehydration facilities continues to influence market competition by optimizing logistics operations.

Alfalfa Hay Industry Leaders

Al Dahra ACX Global Inc.

Standlee Premium Products, LLC

Green Prairie International Inc

Border Valley Trading

Riverina Stockfeeds

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: DLF's North American business segment announced the establishment of specialized Product Knowledge Centers in Philomath, Oregon, and Port Hope, Ontario. These centers will display the complete DLF portfolio, including alfalfa and the latest developments in seed modification technologies.

- January 2025: Norden Manufacturing launched the Norden AlfaTed, a new reel-style tedder designed to help farmers maintain the quality of harvested alfalfa before baling. Compared to traditional rotating tedders, the AlfaTed offers a reliable and gentle solution with increased working speeds.

- April 2024: Mayak, a Siberian agricultural company, announced plans to invest USD 60 million in constructing an alfalfa feed mill, with a primary focus on exports to China. The project includes USD 28 million allocated for land reclamation and advanced irrigation systems to enhance alfalfa cultivation in Siberia.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study views the alfalfa hay market as the total value generated when freshly harvested alfalfa is dried and subsequently traded worldwide as loose or compressed bales, cubes, dehydrated pellets, and mixed forage blends that retain the botanical identity of Medicago sativa. The valuation covers farm-gate, processing, and first-level distribution transactions that ultimately serve dairy cattle, beef cattle, equine, poultry, and specialty pet segments.

Scope exclusion: Fermented silage, alfalfa seed, and pasture grazing services sit outside the numbers presented here.

Segmentation Overview

- By Product Type

- Bales

- Round Bales

- Square Bales

- Pellets

- Cubes

- Dehydrated Pellets

- Compressed Bales

- Bales

- By Grade/Quality

- Supreme (RFV More Than 185)

- Premium (RFV 170-185)

- Good (RFV 150-169)

- Fair (RFV 130-149)

- Utility (RFV Less Than 130)

- By Processing Technology

- Field-Dried Conventional

- Forced-Air Mobile Dryer

- Rotary Drum Dehydration

- Solar-Assisted Dehydration

- By Distribution Channel

- Direct Farm Gate

- Export Trading Houses

- Feed Integrators and Mills

- E-commerce/Online Platforms

- By Livestock Application

- Dairy Cattle Feed

- Beef Cattle Feed

- Poultry Feed

- Equine Feed

- Small Ruminant Feed

- Camelids and Other

- By End-Use Sector

- Commercial Farms

- Compound Feed Manufacturers

- Household/Hobby Animal Owners

- Pet-food and Specialty Nutrition

- By Geography

- North America

- United States

- Canada

- Mexico

- Rest of North America

- Europe

- Germany

- United Kingdom

- France

- Spain

- Italy

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- New Zealand

- South Korea

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Chile

- Rest of South America

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Kenya

- Rest of Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Structured interviews and web surveys were completed with feed formulators, dairy nutritionists, hay exporters, and large-scale hay growers across North America, Europe, the Gulf, and East Asia. Discussions validated the inclusion of dehydrated pellets in the trade pool, clarified grade-wise average selling prices, and flagged regional trip points such as export quality regulations in China.

Desk Research

Mordor analysts compile production statistics and trade matrices from tier-1 public sources such as FAOSTAT, USDA-NASS, UN Comtrade, Eurostat, and national customs dashboards. Season-average alfalfa hay prices are traced through the World Bank commodity database, state extension services, and selected auction market bulletins. Company filings, listed-farmer co-op reports, and reputed farm journals add operating cost and demand context. Paywalled datasets (D&B Hoovers and Dow Jones Factiva) enrich supplier revenue splits and shipment news. This list is illustrative; many additional outlets inform our desk work.

Market-Sizing & Forecasting

A top-down reconstruction starts with country-level production, import, and ending-stock series, which are then valued with grade-weighted average selling prices. Results are cross-checked through selective bottom-up roll-ups of processor throughput and sampled bale-volume × ASP calculations. Key variables feeding the model include dairy cow population growth, export parity pricing, hay yield per hectare, moisture-adjusted shrink losses, and pelletization capacity utilization. Multivariate regression with lagged livestock inventory and milk price indices produces the forecast trajectory, while scenario analysis adjusts for drought probability bands. Data gaps in minor economies are bridged using three-year moving averages anchored to regional trade ratios.

Data Validation & Update Cycle

Model outputs pass anomaly checks against independent feed cost indices and quarterly export receipts. Any variance beyond preset bands triggers re-contact with earlier respondents before final sign-off. Reports refresh each year, and interim updates follow material policy or weather shocks; a last-mile analyst review ensures clients receive the newest view.

Why Our Alfalfa Hay Baseline Commands Reliability

Published figures often diverge because firms draw lines at different product forms, apply unlike price anchors, or lock exchange rates to a single base year.

Key gap drivers include the exclusion of pellet and cube trade, reliance on farmgate-only valuation, or bundling seed revenues. Mordor's disciplined scope, annual refresh cadence, and dual-route (top-down and bottom-up) triangulation keep our baseline steady yet transparent.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 101.2 B (2025) | Mordor Intelligence | - |

| USD 24.1 B (2024) | Global Consultancy A | Omits pellets & cubes, values only top 35 exporting nations |

| USD 29.3 B (2025) | Research Publisher B | Uses constant 2018 FX rates and farm-gate prices, drops dehydrated product |

| USD 88.1 B (2024) | Online Portal C | Bundles hay with alfalfa seed and pasture land value |

The comparison shows how scope, pricing basis, and refresh cadence reshape totals. By grounding every line item in traceable production, trade, and price data, Mordor Intelligence offers decision-makers a balanced, defensible starting point for strategic choices.

Key Questions Answered in the Report

What is the current value of the alfalfa hay market?

The alfalfa hay market size reached USD 78.51 billion in 2026.

How fast is demand growing in the Asia-Pacific?

Driven by domestic water bans, Asia-Pacific demand is advancing at a 6.8% CAGR through 2031.

Which product format is expanding the quickest?

Dehydrated pellets lead growth with an 8.4% CAGR through 2031 because they maximize logistics efficiency and deliver shelf-stable nutrition.

Why are supreme-grade bales priced higher than premium grades?

Supreme hay above 185 RFV commands premiums of up to 35% since its higher protein and lower fiber meet strict Japanese and Korean dairy standards.

Page last updated on: