Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

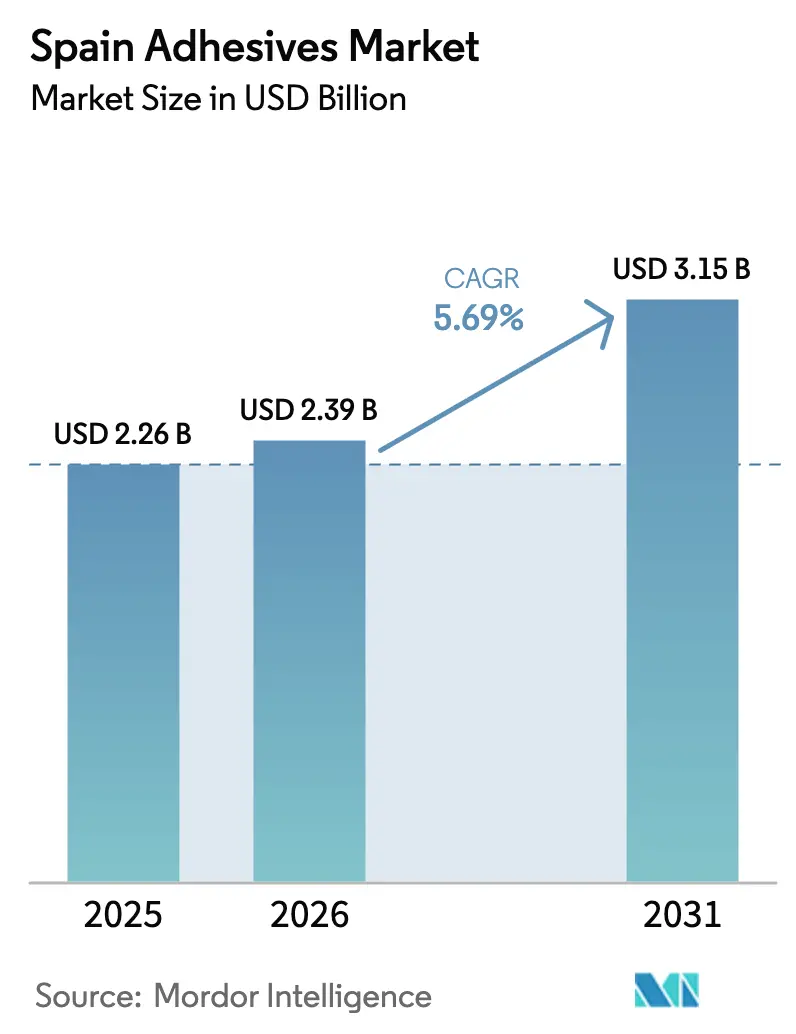

| Base Year Market Size (2025) | USD 2.26 Billion |

| Market Size (2026) | USD 2.39 Billion |

| Market Size (2031) | USD 3.15 Billion |

| Growth Rate (2026 - 2031) | 5.69% CAGR |

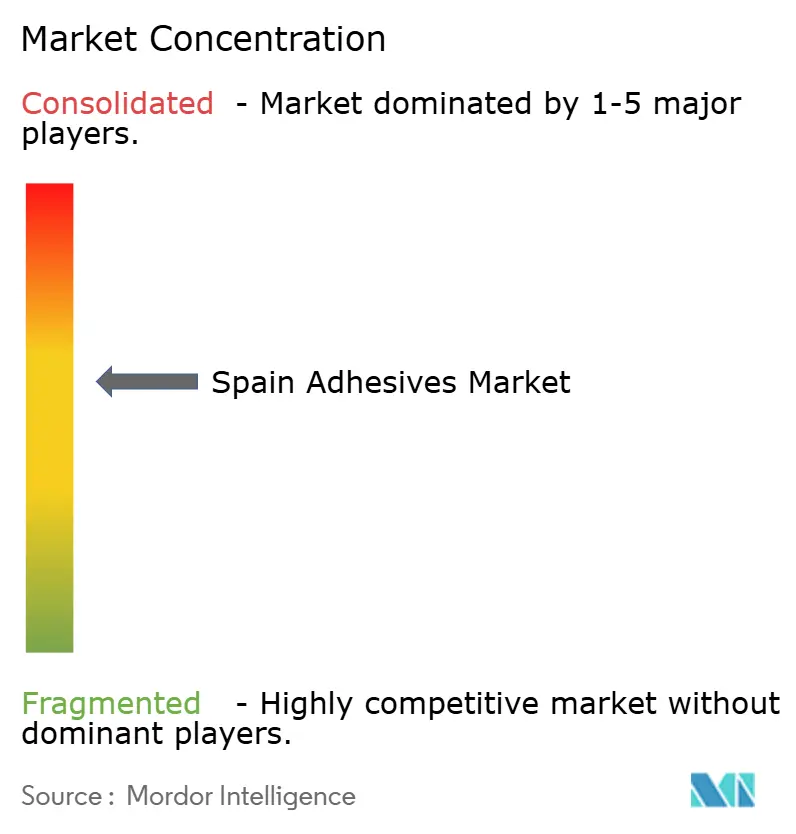

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Spain Adhesives Market Analysis by Mordor Intelligence

The Spain Adhesives Market size was valued at USD 2.26 billion in 2025 and is estimated to grow from USD 2.39 billion in 2026 to reach USD 3.15 billion by 2031, at a CAGR of 5.69% during the forecast period (2026-2031). Spain’s construction retrofits, fast-growing EV battery plants, and sweeping EU VOC caps are steering demand toward water-borne emulsions, reactive hybrids, and next-generation hot melts. Builders specifying thicker insulation and airtight membranes need breathable yet durable bonding agents, lifting consumption of polyurethane foams and MS-polymer sealants relative to solvent systems. Automotive manufacturers are shifting to structural and thermal adhesives for cell-to-pack architecture, while packaging converters automate linerless labels that rely on low-temperature hot melts. Multinational suppliers dominate, but regional specialists defend share by customizing formulations for Spain’s diverse climate zones and tight repair-and-maintenance cycles. Feedstock volatility, labor shortages in structural bonding, and the emergence of plasma bonding in footwear temper the long-term outlook, yet the overall Spain adhesives market retains healthy momentum toward mid-decade.

Key Report Takeaways

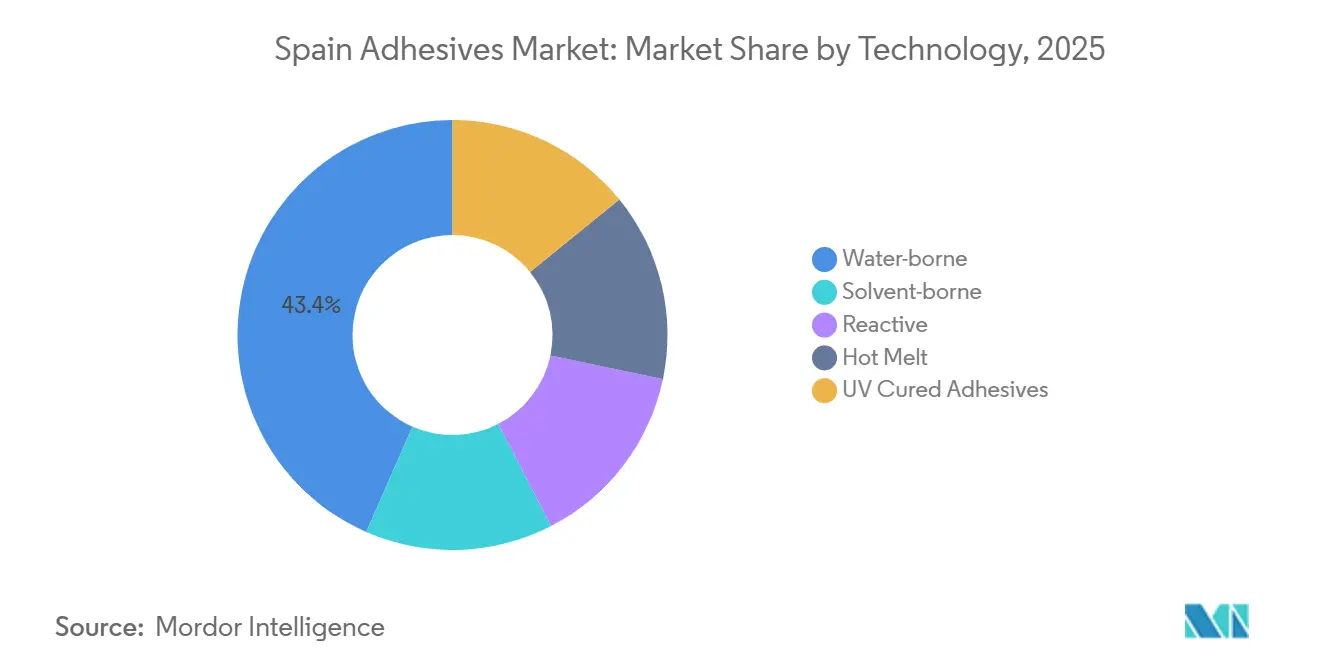

- By technology, water-borne adhesives held 43.44% of the Spain adhesives market share in 2025, while hot melts are forecast to expand at a 6.26% CAGR through 2031.

- By resin, acrylic systems commanded 27.67% of the Spain adhesives market size in 2025, and VAE/EVA resins are projected to grow at a 6.45% CAGR between 2026-2031.

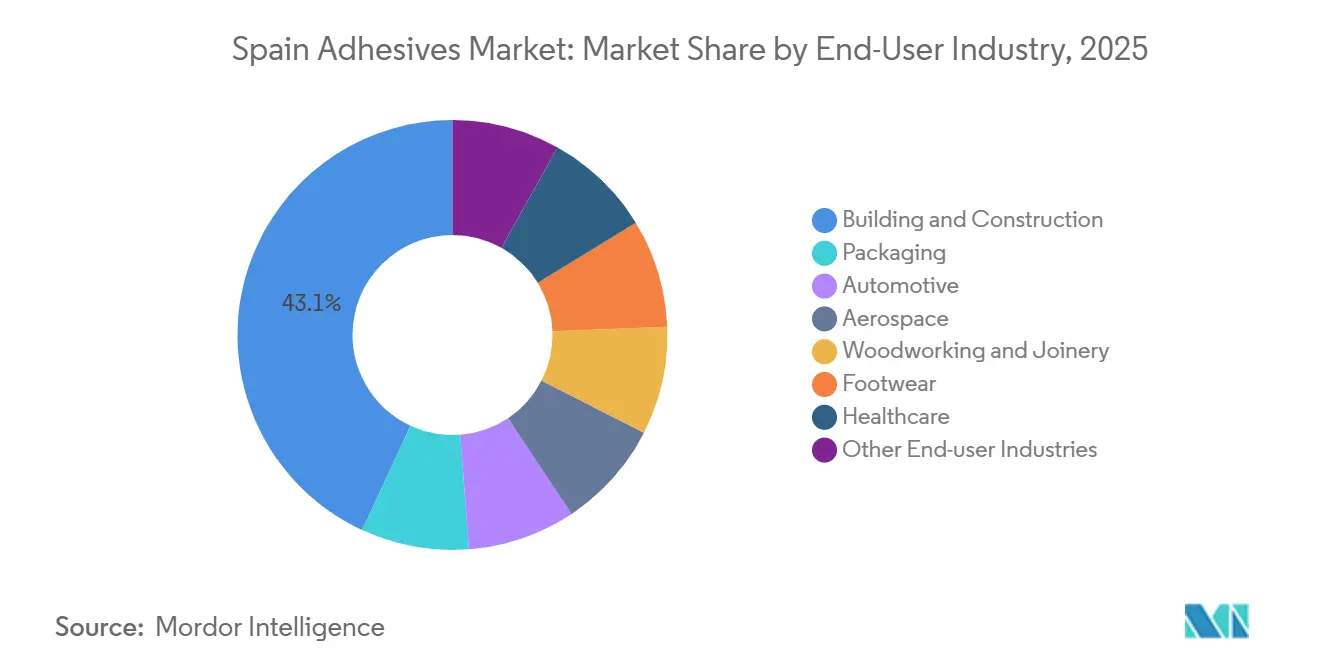

- By end-user industry, building and construction captured 43.11% of revenue in 2025; automotive is advancing at a 6.31% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Spain Adhesives Market Trends and Insights

Driver Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising residential renovation and green-build mandates | +1.2% | National, strongest in Madrid, Barcelona, Valencia metropolitan areas | Medium term (2-4 years) |

| Automotive lightweighting and EV shift | +1.4% | National, concentrated in Martorell, Pamplona, Sagunto/Valencia battery corridor | Medium term (2-4 years) |

| EU push toward low-VOC, water-borne chemistries | +0.9% | National, aligned with EU-wide enforcement | Short term (≤ 2 years) |

| Wind-turbine blade manufacturing clusters in Aragón and Navarre | +0.6% | Regional, Aragón and Navarre with spillover to recycling infrastructure | Long term (≥ 4 years) |

| Gigafactory subsidies driving battery-assembly adhesive demand | +1.1% | Regional, Valencia/Sagunto and Zaragoza (Stellantis/CATL planned 50 GWh) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Residential Renovation and Green-Build Mandates

Spain’s PNRE 2026 roadmap obliges residential buildings to trim primary energy use 16% below 2020 levels by 2030, triggering an upswing in internal insulation bonded with vapor-open MS-polymer and dispersion adhesives[1]Ministerio de Vivienda y Agenda Urbana, “PNRE 2026,” vivienda.gob.es. Heritage properties that cannot receive external insulation now favor capillary-active systems, widening the addressable base for breathable adhesive chemistries. Digital Product Passports, phased in from 2026, demand batch-level traceability and LCA data, rewarding suppliers with ISO 14025 EPD credentials. Insurers are discouraging combustible spray foams after façade fire incidents, further tilting preference toward mineral-wool panels fixed with low-VOC water-borne adhesives. Together, these forces underpin steady growth for the Spain adhesives market in residential retrofits.

Automotive Lightweighting and EV Shift

PowerCo’s 40 GWh gigafactory in Sagunto will start output in 2026 and feed unified prismatic cells to SEAT Martorell’s cell-to-pack lines, where structural adhesives, thermal interface materials, and potting compounds replace 100 fasteners per pack[2]Volkswagen Group, “PowerCo Battery Strategy,” volkswagen-group.com. Adhesive formulations must combine low outgassing, high thermal conductivity, and robotic dispensability under clean-room protocols. Henkel’s AI-assisted battery labs shorten debonding-solution development for end-of-life recovery, aligning with Spain’s circular-economy policies. The Stellantis/CATL plan for a 50 GWh LFP plant in Zaragoza adds a second demand node, concentrating Spain adhesives market opportunities along the Valencia–Zaragoza corridor.

EU Push Toward Low-VOC, Water-Borne Chemistries

EU revisions effective mid-2026 slash permissible VOC emissions for multiple adhesive categories and compel end-of-life disclosure. Spain’s Royal Decree 117/2003 already limits large-scale solvent use, but the new caps accelerate reformulation, particularly in packaging and D-I-Y channels. The formaldehyde restriction (EU 2023/1464) forces a pivot from urea-formaldehyde and phenolic systems toward EPI and formaldehyde-free alternatives, benefiting water-borne VAE, PVA, and styrene-acrylic emulsions. Installers need retraining because cure windows and tooling differ from legacy contact adhesives, yet early movers consolidate share within the Spain adhesives market.

Wind-Turbine Blade Clusters in Aragón and Navarre

Iberdrola’s EnergyLOOP blade-recycling facility in Navarre began operations in 2025, processing 10,000 t/year of retired composite blades. Policy signals hint at future recycled-content mandates in repowering projects, impelling adhesive suppliers to design resins compatible with reclaimed fibers. Blade manufacturers in Aragón require bonding agents that allow disassembly or thermal recovery, opening niches for recyclable epoxy or thermoplastic-compatible systems. These dynamics add a long-tail growth lever for the Spain adhesives market beyond 2030.

Restraint Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile petrochemical feedstock prices | -0.8% | National, with exposure to Brent crude and naphtha spot markets | Short term (≤ 2 years) |

| Stringent VOC limits for solvent-borne systems | -0.5% | National, aligned with EU enforcement timelines | Short term (≤ 2 years) |

| Shortage of skilled applicators for structural bonding | -0.4% | National, acute in aerospace (Seville, Getafe) and wind-blade clusters (Aragón, Navarre) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Petrochemical Feedstock Prices

Acrylates, styrene, EVA, and polyurethane polyols track Brent crude, which climbed in the low single digits during 2025 and faces upside risk in 2026. Spain imports most intermediates, exposing formulators to EUR/USD swings and Mediterranean refinery outages. Smaller firms such as QS Adhesives lack hedging muscle and must pass costs to footwear and furniture OEMs that already battle Asian competition. Bio-based mass-balance inputs cushion exposure but carry 10-20% premiums, squeezing margins across the Spain adhesives market.

Stringent VOC Limits for Solvent-Borne Systems

The mid-2026 EU update tightens VOC ceilings and mandates EPD-style labeling, forcing high-solvent SKUs off shelves. Spain’s paint decree overlays additional labeling duties, and ePRTR data confirm a steady decline in dichloromethane emissions. Installers face a learning curve with water-borne systems, creating interim productivity dips. Early adopters such as Henkel and Quilosa tout ready-stock low-VOC lines, but laggards risk retail delistings, trimming near-term volumes in the Spain adhesives market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Water-Borne Dominance Meets Hot-Melt Acceleration

Water-borne systems accounted for 43.44% of the Spain adhesives market in 2025 as EU VOC rules favored emulsions in construction and packaging. Hot melts are projected to register a 6.26% CAGR to 2031, reflecting linerless label automation and footwear’s pivot from solvent contact cements. Henkel’s EUR 20 million Bopfingen upgrade adds capacity for sustainable polyolefin hot melts, and Ravenwood’s Com500 coaters rely exclusively on dedicated hot-melt PSAs. The Spain adhesives market size for hot melts could exceed USD 920 million by 2031 if adoption rates match current purchase commitments.

Solvent-borne share keeps eroding under Royal Decree 117/2003 caps, while reactive adhesives - epoxy, polyurethane, cyanoacrylate - retain high-value niches in aerospace and EV batteries. Henkel’s new Montornès hub supplies structural epoxies to Airbus, and dual-cure UV/hot-melt systems gain traction in interior automotive trim. UV-cure volumes remain small but double-digit growth is visible in electronics assembly lines in Catalonia. Collectively, technology shifts reinforce the Spain adhesives market as a testbed for greener chemistries.

By Resin: VAE/EVA Gains While Acrylic Holds Construction

Acrylics held a 27.67% stake in 2025, largely from tile adhesives, EIFS, and flooring underlays. Yet VAE/EVA emulsions are forecast to outpace at 6.45% CAGR thanks to flexible-packaging laminations migrating to APEO-free grades. Arkema’s purchase of Dow’s USD 250 million laminate portfolio brought five plants and new research and development to Iberia, quickening chemistry transfer into Spanish converters. The Spain adhesives market share for VAE/EVA could crest 18% by 2031 if proposed PPWR recyclability scores enter force unaltered.

Polyurethane reigns in foams, parquet, and battery modules; Henkel’s electric-boiler retrofit at Montornès advances carbon-light PU output. Epoxies remain irreplaceable for aerospace and wind blades but face bisphenol scrutiny. Cyanoacrylates continue as high-margin D-I-Y staples under AC Marca’s CEYS label, while silicone sealants sustain sanitary and façade joints. Resin-level diversification lets suppliers hedge regulation risk inside the Spain adhesives market.

By End-User Industry: Automotive Outpaces Construction

The building and construction industry kept 43.11% of volume in 2025, but EV platform rollouts will lift automotive demand at a 6.31% CAGR to 2031. Battery cell-to-pack lines in Martorell apply more than 5 kg of adhesive per vehicle for structural bonding, gap filling, and thermal management. Packaging stays resilient as e-commerce and linerless shipments climb, while aerospace adhesives spike with Airbus C295 output at Seville. Woodworking gains from mass-timber components requiring formaldehyde-free glues, and healthcare laminates enter portfolios via Arkema’s flexible-packaging deal, enhancing the Spain adhesives market size across diversified verticals.

Footwear factories in Elche pilot plasma bonding to eliminate sole adhesives, potentially sidelining contact cements by decade’s end. Yet hot-melt sticks already replaced VOC-rich neoprenes in many children’s shoe lines. Electronics, textiles, and DIY remain niche but profitable appendages. End-use pluralism cushions cyclical dips and supports long-run expansion of the Spain adhesives market.

Geography Analysis

Regional demand shows marked splits tied to industrial clusters. Catalonia concentrates aerospace and medical-device assembly, driving sales of epoxy, polyurethane, and UV-cure grades. Valencia’s Sagunto corridor anchors EV battery adhesives, supported by PowerCo’s 40 GWh plant and SEAT logistics networks. Aragón and Navarre dominate wind-blade manufacturing and recycling, anchoring long-cycle epoxy consumption. Madrid and Barcelona metropolitan areas spearhead retrofit activity under PNRE 2026, raising water-borne dispersion uptake for insulation and façade work. Andalusia, with heritage constraints, leans on breathable MS-polymer and lime-compatible systems.

Northern ports at Bilbao and Santander handle bulk imports of polyols, EVA, and isocyanates, shaping logistics footprints for multinational warehouses. Canary and Balearic Islands exhibit steady but small volumes for tourism-linked construction adhesives. Overall, localized climatic needs and industrial policies nurture a mosaic of sub-markets, each reinforcing nationwide momentum of the Spain adhesives market.

Competitive Landscape

The Spain adhesives market is moderately consolidated. Henkel’s EUR 35 million Montornès aerospace hub, AI modeling labs, and zero-gas production lines exemplify forward integration into low-carbon, high-margin sectors. Sika’s plant consolidation after the MBCC buy streamlines powder adhesives and reserves Alcobendas for future liquid lines. Arkema’s Dow laminate takeover grants Bostik an instant footprint in medical and food packaging.

Domestic champion AC Marca leverages its CEYS brand and ferretería network for fast-moving consumer adhesives, while Selena-Quilosa differentiates through biodegradable product introductions. Regional specialists like QS Adhesives and Kefrén win footwear and furniture contracts via rapid customization and local service. Disruptive fronts include plasma bonding, recyclability-ready epoxies, and mass-balance bio-acrylate sourcing, all of which could scramble rankings yet widen the Spain adhesives market size.

Spain Adhesives Industry Leaders

Henkel AG & Co. KGaA

H.B. Fuller Company

Sika AG

Arkema

Dow

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Henkel inaugurated a EUR 35 million aerospace adhesive hub at Montornès del Vallès.

- December 2024: Arkema closed its USD 150 million acquisition of Dow’s flexible-packaging laminating adhesives arm.

Spain Adhesives Market Report Scope

Adhesives are materials designed to bond surfaces together effectively, ensuring durability and resistance to separation. Various industries, including building and construction, packaging, automotive, aerospace, woodworking and joinery, footwear, healthcare, and other end-user sectors, rely on specific types of adhesives tailored to their composition and functional requirements.

The Spain adhesives market is segmented by technology, resin, and end-user industry. By technology, the market is segmented into water-borne, solvent-borne, reactive, hot melt, and UV cured adhesives. By resin, the market is segmented into polyurethane, epoxy, acrylic, cyanoacrylate, VAE/EVA, silicone, and other resins. By end-user industry, the market is segmented into building and construction, packaging, automotive, aerospace, woodworking and joinery, footwear, healthcare, and other end-user industries. For each segment, the market sizing and forecasts have been done based on revenue (USD).

By Technology

| Water-borne |

| Solvent-borne |

| Reactive |

| Hot Melt |

| UV Cured Adhesives |

By Resin

| Polyurethane |

| Epoxy |

| Acrylic |

| Cyanoacrylate |

| VAE/EVA |

| Silicone |

| Other Resins |

By End-User Industry

| Building and Construction |

| Packaging |

| Automotive |

| Aerospace |

| Woodworking and Joinery |

| Footwear |

| Healthcare |

| Other End-user Industries |

| By Technology | Water-borne |

| Solvent-borne | |

| Reactive | |

| Hot Melt | |

| UV Cured Adhesives | |

| By Resin | Polyurethane |

| Epoxy | |

| Acrylic | |

| Cyanoacrylate | |

| VAE/EVA | |

| Silicone | |

| Other Resins | |

| By End-User Industry | Building and Construction |

| Packaging | |

| Automotive | |

| Aerospace | |

| Woodworking and Joinery | |

| Footwear | |

| Healthcare | |

| Other End-user Industries |

Market Definition

- End-user Industry - Building & Construction, Packaging, Automotive, Aerospace, Woodworking & Joinery, Footwear & Leather, Healthcare, and Others are the end-user industries considered under the adhesives market.

- Product - All adhesive products are considered in the market studied

- Resin - Under the scope of the study, resins like Polyurethane, Epoxy, Acrylic, Cyanoacrylate, VAE/EVA, and Silicone are considered

- Technology - For the purpose of this study, Water-borne, Solvent-borne, Reactive, Hot Melt, and UV Cured adhesive technologies are taken into consideration.

| Keyword | Definition |

|---|---|

| Hot-melt Adhesive | Hot melt adhesives are generally 100% solid formulations, based on thermoplastic polymers. They are solid at room temperature and are activated upon heating above their softening point, at which stage they are liquid, and hence, can be processed. |

| Reactive Adhesive | A reactive adhesive is made up of monomers that react in the adhesive curing process and do not evaporate from the film during use. Instead, these volatile components become chemically incorporated into the adhesive. |

| Solvent-borne Adhesive | Solvent-borne adhesives are mixtures of solvents and thermoplastic, or slightly cross-linked polymers, such as polychloroprene, polyurethane, acrylic, silicone, and natural and synthetic rubbers (elastomers). |

| Water-borne Adhesive | Water-borne adhesives use water as a carrier or diluting medium to disperse a resin. They are set by allowing the water to evaporate or be absorbed by the substrate. These adhesives are compounded with water as a diluent, rather than a volatile organic solvent. |

| UV Cured Adhesive | UV curing adhesives induce curing and create a permanent bond without heating by using ultraviolet (UV) light or other radiation sources. An aggregation of monomers and oligomers is cured or polymerized by ultraviolet (UV) or visible light in a UV adhesive. Because UV is a radiating energy source, UV adhesives are often referred to as radiation curing or rad-cure adhesives. |

| Heat-resistant Adhesive | Heat-resistant Adhesives refer to those that do not break down under high temperatures. One aspect of a complicated system of circumstances is the adhesive's capacity to withstand disintegration brought on by high temperatures. As the temperature rises, adhesives may liquefy. They can withstand stresses resulting from differing coefficients of expansion and contraction, which might be an additional advantage. |

| Reshoring | Reshoring is the practice of moving commodity production and manufacturing back to the nation where the business was founded. Onshoring, inshoring, and back shoring are further terms used. Offshoring, the practice of producing items abroad to lower labor and manufacturing costs, is the opposite of this. |

| Oleochemicals | Oleochemicals are compounds produced from biological oils or fats. They resemble petrochemicals, which are substances made from petroleum. The oleochemical business is built on the hydrolysis of oils or fats. |

| Nonporous Materials | Nonporous materials are substances that do not permit the passage of liquid or air. Nonporous materials are those that are not porous, such as glass, plastic, metal, and varnished wood. Since no air can get through, less airflow is required to raise these materials, negating the requirement for high airflow. |

| EU-Vietnam Free Trade Agreement | A trade agreement and an investment protection agreement were concluded between the European Union and Vietnam on June 30, 2019. |

| VOC content | Compounds with limited solubility in water and high vapor pressure are known as Volatile Organic Compounds (VOCs). Many VOCs are human-made chemicals that are used and produced in the manufacture of paints, pharmaceuticals, and refrigerants. |

| Emulsion Polymerization | Emulsion polymerization is a method of producing polymers or connected groups of smaller chemical chains known as monomers, in a water solution. The method is often used to make water-based paints, adhesives, and varnishes, in which the water stays with the polymer and is marketed as a liquid product. |

| 2025 National Packaging Targets | In 2018, the Australian Environment Ministry set the following 2025 National Packaging Targets: 100% of the packaging must be reusable, recyclable, or compostable by 2025, 70% of plastic packaging must be recycled or composted by 2025, 50% of average recycled content must be included in packaging by 2025, and problematic and unnecessary single-use plastic packaging must be phased out by 2025. |

| Russian Government’s Import Substitution Policy | The Western sanctions suspended the distribution of several high-tech items to Russia, including those required by the raw material export sectors and the military-industrial complex. In response, the government launched an "import substitution" scheme, appointing a special commission to oversee its implementation in early 2015. |

| Paper Substrate | Paper substrates are paper sheets, reels, or boards with a base weight of up to 400 g/m2 that has not been converted, printed or otherwise altered. |

| Insulation Material | A material that inhibits or blocks heat, sound, or electrical transmission is known as Insulation Material. The variety of insulation materials includes thick fibers like fiberglass, rock and slag wool, cellulose, and natural fibers as well as stiff foam boards and sleek foils. |

| Thermal Shock | A temperature change known as thermal shock generates stress in a material. It commonly results in material breakdown and is especially prevalent in brittle materials like ceramics. When there is a quick temperature change, either from hot to cold or vice versa, this process occurs abruptly. It occurs more frequently in materials with poor heat conductivity and insufficient structural integrity. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms