Vacuum Interrupter Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.24 Billion |

| Market Size (2031) | USD 4.22 Billion |

| Growth Rate (2026 - 2031) | 5.42% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

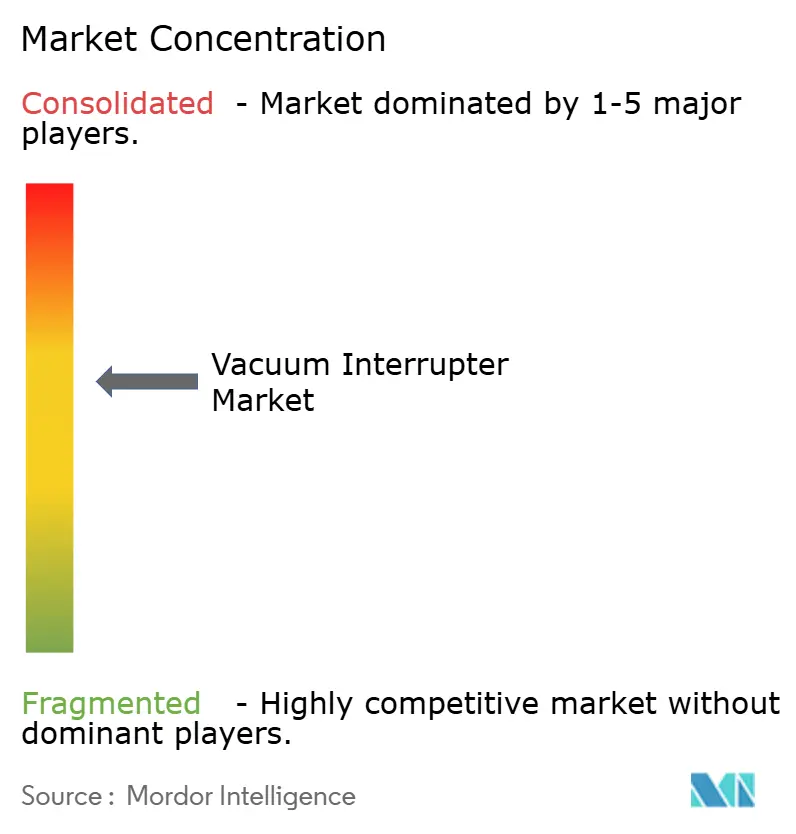

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vacuum Interrupter Market Analysis by Mordor Intelligence

Vacuum interrupter market size in 2026 is estimated at USD 3.24 billion, growing from 2025 value of USD 3.07 billion with 2031 projections showing USD 4.22 billion, growing at 5.42% CAGR over 2026-2031. This trajectory reflects utilities’ preference for maintenance-free medium-voltage switchgear, the push to modernize transmission and distribution grids, and the rapid electrification of railways and data-center campuses. Demand also benefits from tighter regulations on sulfur-hexafluoride (SF6) and the superior arc-extinction performance that underpins rising deployments in smart grid applications. Asia-Pacific remains the primary growth engine, yet North America and Europe provide a steady replacement market for legacy oil-filled gear. Competition is intensifying as manufacturers race to commercialize SF6-free high-voltage solutions and to localize production in India and the Middle East, but solid-state breakers remain in the pilot phase.

Key Report Takeaways

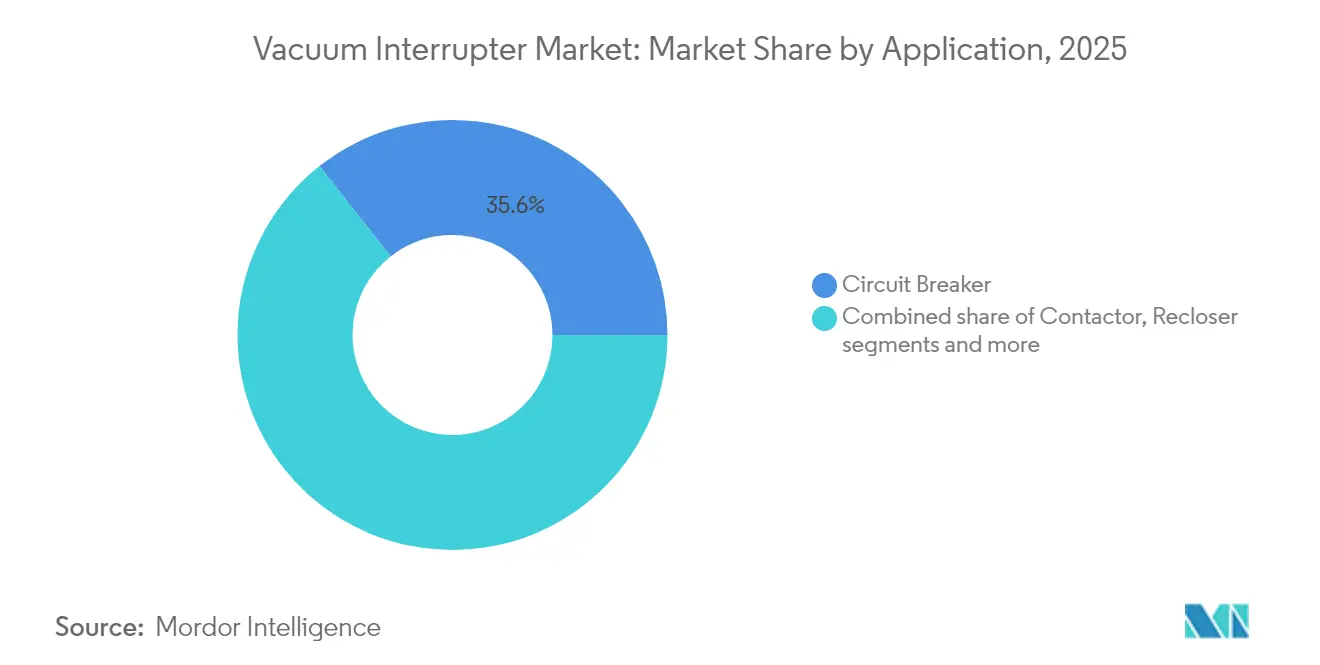

- By application, circuit breakers led with 35.62% revenue share in 2025, while reclosers recorded the highest projected CAGR at 5.72% through 2031.

- By voltage class, the 15.1–27 kV segment held 47.65% of the vacuum interrupter market share in 2025; above 38 kV applications are set to expand at a 6.21% CAGR.

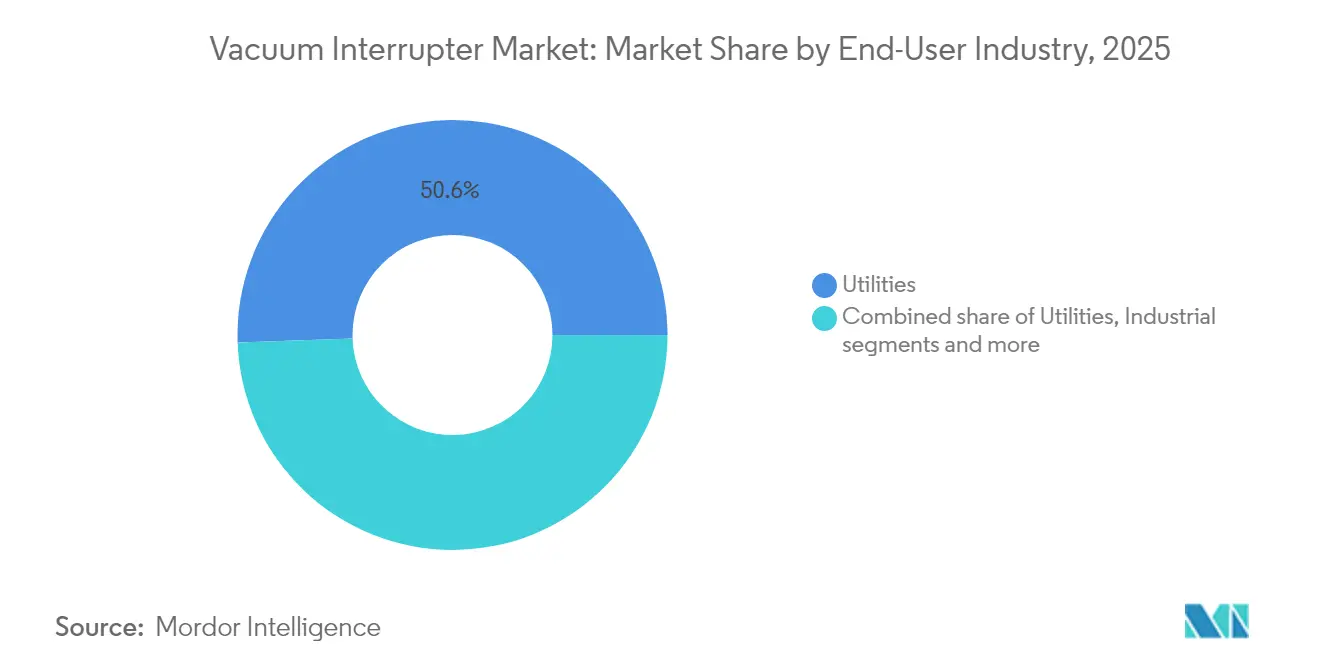

- By end-user industry, utilities captured 50.55% of the vacuum interrupter market size in 2025, yet renewables and independent power producers are advancing at a 5.94% CAGR to 2031.

- By installation type, indoor switchgear accounted for a 54.75% slice of the vacuum interrupter market size in 2025, while outdoor pole-mounted units are gaining at a 6.55% CAGR.

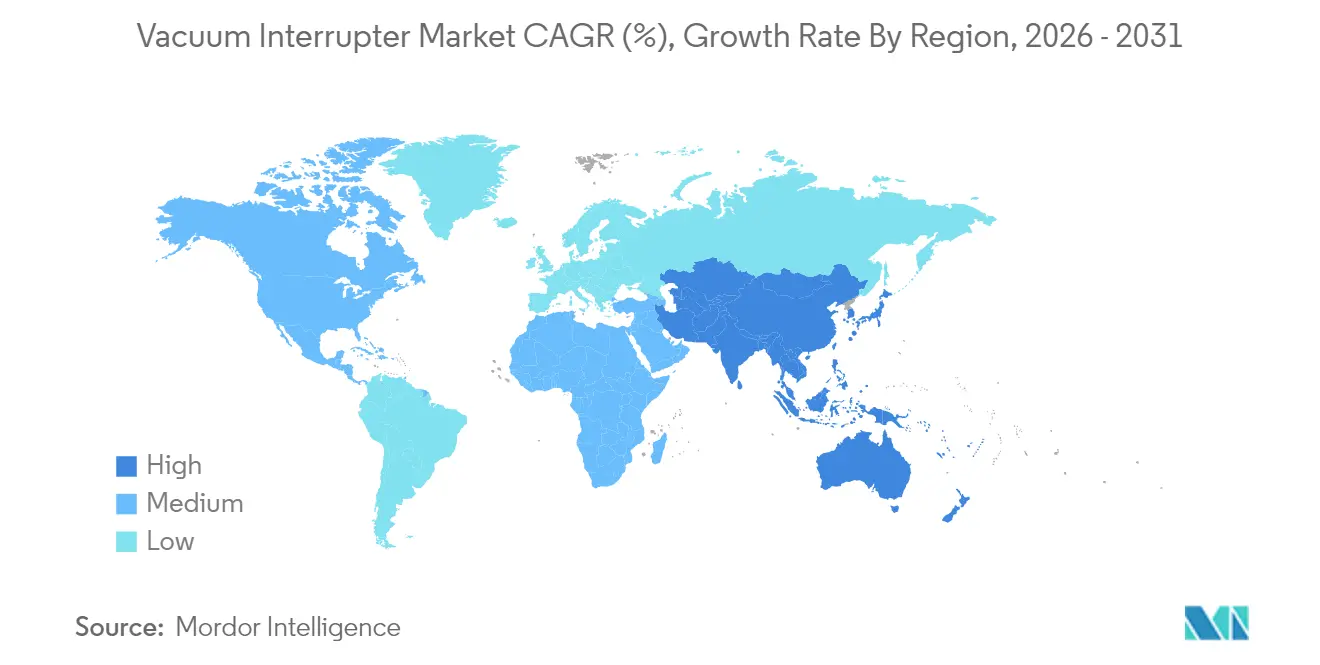

- By geography, Asia-Pacific commanded 41.05% of 2025 revenues and is outpacing all regions with a 5.88% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Vacuum Interrupter Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Smart-grid rollout and MV switchgear demand | +1.8% | Global, strongest in North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Aging T&D infrastructure replacements | +1.5% | North America, Europe, mature APAC markets | Long term (≥ 4 years) |

| Rapid expansion of data-center power networks | +1.2% | Global, with North America and Europe in the lead | Short term (≤ 2 years) |

| Electrification of railway feeders in Asia | +0.8% | China, India, ASEAN | Medium term (2-4 years) |

| Shift to SF6-free eco-designs by utilities | +0.6% | Europe, North America initially | Long term (≥ 4 years) |

| Localization mandates in India and MENA | +0.4% | India, Middle East & North Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Smart-grid rollout and MV switchgear demand

Proliferating distributed energy resources require switchgear that supports frequent on-load operations and instantaneous fault isolation. Utilities in the United States and Western Europe, therefore, prioritize vacuum interrupter-based switchgear for advanced feeder automation, driving a meaningful share of incremental orders in the vacuum interrupter market. Adoption accelerates where regulators link performance incentives to outage duration, and where federal stimulus packages finance grid resilience. Digital sensors embedded in modern interrupters provide utilities with the operational visibility needed for self-healing networks, while the maintenance-free vacuum device design trims lifecycle costs. These benefits collectively underpin a visible order pipeline that extends through 2028, particularly for 15 kV–27 kV feeder classes.

Aging T&D infrastructure replacements

North American and European utilities face equipment fleets averaging more than four decades, turning asset-management programs into sizable procurement funnels for the vacuum interrupter market. Operators retiring oil-filled or SF6-based breakers now specify vacuum devices to limit greenhouse-gas exposure and to reduce service truck rolls. Deferred maintenance backlogs compound the replacement cycle, and multiyear capital-expenditure plans already in execution point to stable retrofit volumes that stretch well beyond 2030. Higher-voltage multi-break designs are making inroads into 72 kV and 145 kV substations, boosting average selling prices and lifting the value mix toward premium contact-material alloys.

Rapid expansion of data-center power networks

Hyperscale operators building AI-optimized campuses can draw 200 MW to 400 MW per site and frequently reconfigure electrical loads. Vacuum interrupters enable the requisite high-duty switching with minimal contact erosion, a core reason why the segment is expanding roughly three times faster than general-industry demand in the vacuum interrupter market. Compact footprints suit double-stacked IT vaults, while remote-monitoring interfaces mesh with facility-management software. The steep growth curve in Europe’s FLAP-D corridor and the United States’ Midwest and Mountain regions signals sustained orders for at least the next five years.

Electrification of railway feeders in Asia

China’s 50 Hz, 27.5 kV single-phase traction networks and India’s 25 kV AC main-line corridors both require rugged interrupters that withstand repetitive load cycles and airborne dust. As route mileage under catenary expands, purpose-built pole-mounted breakers extend feeder-section reach, giving the vacuum interrupter market fresh volume streams[1]Hitachi Energy press office, “EconiQ SF6-Free Breaker Milestone,” hitachienergy.com. National plans to take another 17,000 km of Indian track under electrification by 2029 will keep demand elevated, and similar green-field trunk lines across ASEAN support the medium-term outlook.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High unit cost at above 40 kV ratings | -0.9% | Global, especially in cost-sensitive emerging markets | Medium term (2-4 years) |

| Substitution threat from solid-state breakers | -0.7% | Early adoption in OECD countries | Long term (≥ 4 years) |

| IP issues on contact-material alloys | -0.4% | Global | Short term (≤ 2 years) |

| Supply-chain fragility of ceramic envelopes | -0.3% | Asia-Pacific fabrication hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High unit cost at above 40 kV ratings

Above 40 kV, designs require multiple interruption gaps and sophisticated voltage-grading capacitors, which push capital cost to two-to-three times that of single-break formats. Utilities in Latin America and Africa—regions still price-sensitive—therefore stick with conventional air-insulated gear, muting volume growth for the high-voltage slice of the vacuum interrupter market. Although manufacturers pursue economies of scale at new Asian plants, significant price parity may not arrive before 2029, keeping this restraint in play through the forecast horizon.

Substitution threat from solid-state breakers

Startup advances in bilateral transistor (B-TRAN) devices promise sub-microsecond interruption and zero mechanical wear. Pilot installations at a leading Asian switchgear OEM show feasibility in 15 kV rack-mounted panels, and management targets a USD 1 billion serviceable niche within a decade[2]Ideal Power investor update, “B-TRAN Design Win Announcement,” idealpower.com. For now, power-loss penalties and component cost slow uptake, but if silicon-carbide wafer pricing declines as expected, the vacuum interrupter market could face sharper competition in renewables-rich microgrids and data-center switchboards.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Circuit Breakers Anchor Volumes as Reclosers Accelerate

Circuit breakers constitute the largest slice of the vacuum interrupter market size, retaining 35.62% of 2025 revenues. The category serves primary distribution substations where utilities value long electrical life and low maintenance cycles. Growth, however, tilts toward reclosers, which post a 5.72% CAGR through 2031 as distribution automation spreads. Utilities deploy reclosers on lateral feeders with rooftop solar and electric-vehicle loading, where rapid fault isolation and auto-reenergization boost reliability indices. Advanced microprocessor controls now allow multiple-shot profiles adapted to inverter-based resources, securing vacuum devices as the preferred arc-quenching core. Contactors and load-break switches deliver steady industrial demand, chiefly from motor control centers and capacitor-bank switching in cement, metals, and oil-refining complexes. These niches add resilience to the overall vacuum interrupter market because their order cycles correlate with general industrial capital expenditure.

The high duty cycle inherent to recloser operation underscores the superiority of vacuum contacts versus oil or SF6 puffer mechanisms, whose mechanical linkages degrade under repetitive trips. Field data from US Midwest utilities show maintenance call-outs per recloser dropping by 60% after migration to vacuum designs, directly lowering operating expenditure. That demonstrable cost advantage underpins vendor order books and propels software-enabled feeder automation solutions bundled with vacuum interrupter cores. As a result, the vacuum interrupter market continues to capture incremental feeder retrofit budgets even where overall capital plans remain flat.

By Voltage Class: Above-38 kV Installations Gain Pace

The 15.1 kV–27 kV bracket remains the workhorse, commanding 47.65% of 2025 revenues. Distribution-level feeders and industrial campuses typically fall in this range, and utilities prefer standardized footprints for quick truck roll replacements. Nevertheless, the above-38 kV segment is the fastest climber at a 6.21% CAGR, buoyed by renewable-rich transmission corridors. Multi-break 72 kV and 145 kV prototypes have proven dielectric strength in European climate chambers, and a 252 kV platform recently passed short-circuit tests at KEMA Laboratories, widening market scope. Where regional grid codes now ban new SF6 gas gear in 145 kV rings starting 2031, network owners pivot early to vacuum alternatives, inflating the premium end of the vacuum interrupter market.

Voltage scaling depends on refined CuCr50 contact alloys that resist high-energy arcing; patent filings suggest nanocrystalline microstructures cut cathode erosion by 35% compared with conventional formulations. Suppliers owning these alloys enjoy pricing power, further skewing revenue toward high-voltage SKUs. Meanwhile, the sub-15 kV slice caters to panel builders for commercial buildings and rooftop solar farms, a segment with shorter sales cycles that cushions cyclical swings in utility capital budgets. Overall, diverse voltage demand maintains a balanced growth profile across the vacuum interrupter market.

By End-User Industry: Renewables Outpace the Utility Core

Utilities still dominate spending, holding 50.55% in 2025, but independent power producers and renewable developers show the steepest trajectory at 5.94% CAGR. Solar-plus-storage parks and onshore wind clusters rely on vacuum interrupters to manage bidirectional flows and frequent connection cycling. Inverters now incorporate grid-forming capabilities, driving higher breaker operation counts and making mechanical endurance a purchase-selection criterion that vacuum technology meets comfortably. The mining, metals, and petrochemical verticals provide a stable baseline volume, as process electrification projects seek reliable interruption for large-horsepower drives. Commercial campuses and hyperscale data centers, meanwhile, scale their purchasing via long-term equipment master agreements, adding lumpiness—but also sizable blocks—to the vacuum interrupter market.

Developers in Spain and Australia report 5–7 switching events per day on breaker strings tied to battery-energy-storage systems; oil-filled devices rarely survive such cycling without mid-life overhauls. Vacuum contacts, conversely, carry a 30,000 mechanical operations rating, lowering the total cost of ownership. Such field evidence sustains procurement momentum even as tariffs on imported switchgear fluctuate. Hence, the vacuum interrupter industry benefits from the broader decarbonization push across multiple customer archetypes.

By Installation Type: Outdoor Gear Narrows the Gap

Indoor metal-clad switchgear held 54.75% of 2025 deployments, favored for enclosed environments such as utility substations, polished for urban real-estate constraints, or clean-room semiconductor fabs. Yet, outdoor pole-mounted units show a sharper 6.55% CAGR as rural electrification and railway feeders expand. Non-enclosed solid-insulated switchgear leverages silicone rubber and epoxy resins to withstand UV, salt fog, and seismic events; such robustness positions vacuum interrupters in feeder circuits that formerly used drop-out fuses. The trend also manifests in Africa’s mini-grid initiatives, where standalone pole-top reclosers and sectionalizers curtail outage scopes in sparsely populated districts.

Rail operators adopt compact outdoor cubicles integrating vacuum breakers for 25 kV autotransformer systems, avoiding costly brick-and-mortar houses near the right-of-way. Meanwhile, underground distribution in densely populated Asian megacities turns to vacuum interrupter modules designed for vaults flooded with diesel exhaust and moisture. Across these divergent site conditions, shared reliability requirements and lower maintenance burdens sustain market appeal, keeping the outdoor and indoor segments tightly linked in the vacuum interrupter market.

Geography Analysis

Asia-Pacific retained 41.05% of global revenue in 2025 and is expanding at 5.88% CAGR, benefiting from China’s internal grid reinforcement, India’s localization push, and Southeast Asia’s metro-rail build-outs. Government-backed manufacturing incentives cut procurement lead times for domestic utilities, enhancing the region’s self-sufficiency and undergirding regional demand. Localization is especially pronounced in India, where performance-linked incentive schemes reimburse up to 4% of ex-works value for indigenous switchgear, steering multinational suppliers toward joint ventures and licensing deals with local metal-clad panel fabricators.

North America shows steady replacement spending as equipment exceeding 40 years approaches the end of its life. Federal funding in the United States earmarks USD 13 billion for grid resilience, and parts of that allocation flow into medium-voltage breakers. Extreme-weather events in Texas, Louisiana, and California accelerate sectionalizer and recloser deployment, while hyperscale data-center clustering in Virginia and Ohio drives private capital spending. Consequently, the region preserves a healthy slice of the vacuum interrupter market despite lower headline growth.

Europe aligns policy with net-zero objectives, outlawing newly installed SF6 gear up to 24 kV from 2026 and above 52 kV from 2031, thereby mandating vacuum solutions for both distribution and transmission. Pilot installations at 420 kV prove technical feasibility, and multi-utility procurement consortia tender frameworks for million-euro contracts extending to 2029. South America and the Middle East, and Africa together account for a smaller base but deliver above-average percentage growth thanks to rural electrification, industrial diversification in the Gulf, and mining expansion in Chile and Peru. Each region’s demand profile relies on durable equipment that minimizes service visits, embedding long-life vacuum interrupters at the core of tender specifications.

Competitive Landscape

Established multinationals—ABB, Siemens Energy, Hitachi Energy, Mitsubishi Electric, Toshiba, and Schneider Electric—command technology leadership via vertically integrated contact-material production and global service networks. Combined, the top five control roughly 58% of 2024 revenues, giving the vacuum interrupter market a moderately concentrated structure. Major players pour capital into SF6-free product lines: Siemens invested EUR 100 million to upgrade its Frankfurt plant to manufacture blue-technology switchgear, while ABB’s USD 40 million Albuquerque facility focuses on fluoronitrile-filled panels destined for US grid-hardening projects. Hitachi Energy likewise earmarked USD 70 million for Pennsylvania capacity, adding a research and development lab to expedite material science breakthroughs.

Contact-material innovation is emerging as a primary differentiation lever. Research demonstrates that nanocrystalline CuCr50 powders elevate dielectric recovery by shortening arc-column collapse times, allowing higher interruption ratings without enlarging vacuum envelopes. Suppliers securing patents on these alloys command premium pricing and extend product life, particularly above 40 kV. Regional manufacturers in India and China strive to close the gap through technology-transfer licenses and government funding, yet remain largely focused on low- and mid-voltage ranges.

Solid-state circuit breakers represent the most visible disruptive threat. Ideal Power’s bilateral transistor modules passed type tests at a Tier-1 Asian OEM, aiming at the microgrid, marine, and high-speed rail traction segments. If manufacturing costs per ampere fall below USD 0.60 by 2028, analysts anticipate niche displacement within data-center UPS tie breakers. Incumbents mitigate risk by running parallel R&D on hybrid mechanical-solid-state architectures, but the broader vacuum interrupter market retains cost and energy-loss advantages that will likely hold in mainstream utility applications for most of the forecast window.

Vacuum Interrupter Industry Leaders

Eaton Corporation PLC

Meidensha Corporation

Mitsubishi Electric Corporation

Siemens AG

ABB Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: ABB opened a USD 40 million manufacturing facility in Albuquerque, New Mexico, focused on SF6-free switchgear and grid-hardening components.

- April 2025: Hitachi Energy committed USD 70 million to expand EconiQ SF6-free switchgear production in Pennsylvania, adding 100 skilled jobs.

- March 2025: Schneider Electric announced USD 700 million of additional US investments through 2027 across Tennessee, Massachusetts, and Texas plants.

- March 2025: ABB earmarked USD 120 million for low-voltage breaker capacity expansion in Tennessee and Mississippi, creating 250 jobs.

- March 2025: Hitachi Energy allotted USD 250 million to ease global transformer-component shortages by enlarging bushing and insulation output.

- January 2025: Hitachi Energy delivered the world’s first SF6-free 550 kV gas-insulated switchgear to China’s State Grid Corporation, demonstrating scalability of eco-friendly high-voltage technology.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global vacuum interrupter market as the total value of factory-built, hermetically sealed contact assemblies that extinguish current in a vacuum and are rated up to 40 kV for use in circuit breakers, contactors, reclosers, load-break switches, and tap changers serving utilities, industrial plants, transport systems, and commercial facilities.

Scope exclusion: solid-state interrupters, SF6 or oil-based breakers, and aftermarket repair kits are not counted.

Segmentation Overview

- By Application

- Circuit Breaker

- Contactor

- Recloser

- Load Break Switch

- Others (Capacitor bank, Earthing)

- By Voltage Class

- 15 kV

- 15.1-27 kV

- 27.1-38 kV

- above 38 kV

- By End-User Industry

- Utilities

- Industrial (Oil and Gas, Mining, Cement)

- Renewables and IPP

- Commercial and Data Centers

- By Installation Type

- Indoor Switchgear

- Outdoor Pole-mounted

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- ASEAN

- Australia and New Zealand

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Middle East

- Saudi Arabia

- UAE

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed protection engineers at Asian and European utilities, maintenance leads in rail electrification, and product managers at switchgear manufacturers across the Americas. These conversations validate volume assumptions, refine price corridors, and highlight emerging design preferences that seldom surface in public datasets.

Desk Research

We start by harvesting demand signals from tier-one public sources such as the International Energy Agency, IEC conformity lists, UN Comtrade shipment codes, and national customs dashboards, which reveal yearly trade tonnage and invoice values. Company filings, tender portals, and news archives accessed through D&B Hoovers and Dow Jones Factiva let us benchmark average selling prices and spot new switchgear projects. Grid statistics from the World Bank and regional transmission operators round out macro demand indicators. The sources named are illustrative, not exhaustive, and many more inform our desk analysis.

Market-Sizing & Forecasting

A top-down and bottom-up hybrid is applied. We begin with national production, import, and export data for medium-voltage switchgear, which are then linked to measured penetration rates of vacuum technology by voltage class. Supplier shipment roll-ups and installer channel checks provide bottom-up reasonableness for units and blended ASP. Key variables include grid capex pipelines, renewable capacity additions, substation build counts, ASP deflation, and equipment replacement cycles. Forecasts rely on multivariate regression that relates interrupter demand to real T&D investment, industrial production, and renewable build-out scenarios, followed by scenario analysis to adjust for policy or commodity shocks.

Data Validation & Update Cycle

Outputs pass anomaly checks against independent ratios, then a multi-step peer review, and any variance prompts source re-contact. Models refresh annually, with interim updates when material events occur, ensuring clients always see the latest calibrated view.

Why Mordor's Vacuum Interrupter Baseline Commands Reliability

Published estimates often diverge because each firm chooses different device sets, price bases, and refresh cadences.

Key gap drivers include the omission of indoor contactors by some publishers, frozen 2020 ASP benchmarks that ignore recent nickel price swings, and shorter historical windows that can overstate growth in fast-recovering regions.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 3.07 Bn (2025) | Mordor Intelligence | - |

| USD 3.10 Bn (2025) | Global Consultancy A | Excludes reclosers and tap changers; static 2020 price deck |

| USD 2.91 Bn (2025) | Trade Journal B | Counts utility demand only; omits industrial and transport volumes |

| USD 2.23 Bn (2023) | Industry Association C | Earlier base year; linear roll-forward without currency normalization |

The comparison shows that once scope breadth, dynamic pricing, and regular updates are aligned, Mordor's balanced baseline sits closest to observable shipment value and offers decision-makers a transparent, repeatable footing.

Key Questions Answered in the Report

What is the current value of the vacuum interrupter market?

The market is valued at USD 3.24 billion in 2026 and is projected to reach USD 4.22 billion by 2031, growing at a 5.42% CAGR.

Which application segment is growing fastest?

Reclosers record the highest growth at a 5.72% CAGR through 2031 due to distribution automation needs.

Why are vacuum interrupters preferred in data centers?

They handle frequent switching without contact wear, support compact layouts, and integrate with remote-monitoring systems, all critical for 99.99% uptime targets.

How are environmental regulations influencing adoption?

European bans on new SF6 equipment push utilities toward vacuum interrupter solutions, accelerating uptake in both distribution and high-voltage classes.

Do solid-state breakers threaten the vacuum interrupter industry?

They offer ultra-fast interruption and no mechanical parts, but high costs and energy-loss levels limit penetration to niche applications through most of the forecast period.

Which region commands the largest share of the vacuum interrupter market?

Asia-Pacific leads with 41.05% of global revenue in 2025, underpinned by large-scale grid investments in China and India.

Page last updated on: