Social And Emotional Learning Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

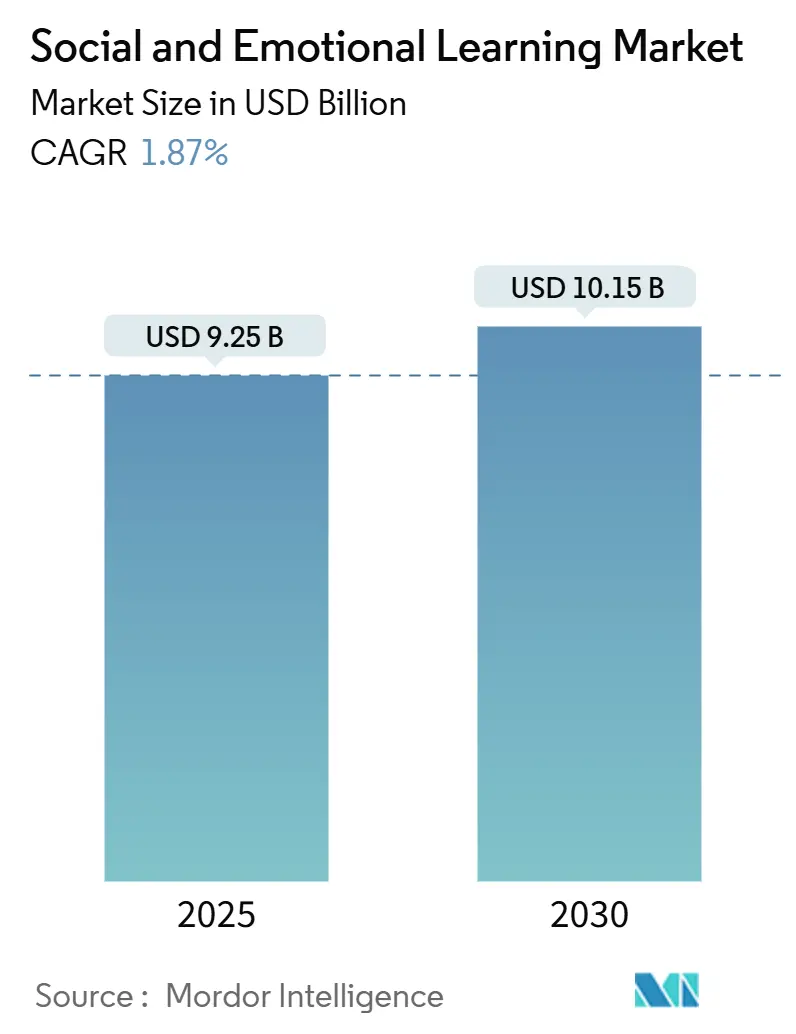

| Market Size (2025) | USD 9.25 Billion |

| Market Size (2030) | USD 10.15 Billion |

| Growth Rate (2025 - 2030) | 1.87% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Social And Emotional Learning Market Analysis by Mordor Intelligence

The Social and Emotional Learning Market size is estimated at USD 9.25 billion in 2025, and is expected to reach USD 10.15 billion by 2030, at a CAGR of 1.87% during the forecast period (2025-2030). Persistently strong public-sector demand, ongoing evidence generation, and measured post-pandemic budgeting underpin the outlook for the Social and Emotional Learning market. Districts are pivoting from short-lived ESSER grants to recurring operating budgets, which signals durable institutional commitment rather than stagnation. Evidence of impact on attendance, behavior, and academic recovery is now a prerequisite for multi-year contracts, forcing vendors to invest in rigorous efficacy studies. Cloud-based platforms that integrate assessments, curriculum, and analytics continue to win adoption, while AI-enabled personalization strengthens the business case for premium pricing. At the same time, privacy safeguards and cultural inclusivity standards are tightening, exerting upward pressure on product development costs in the Social and Emotional Learning market.

Key Report Takeaways

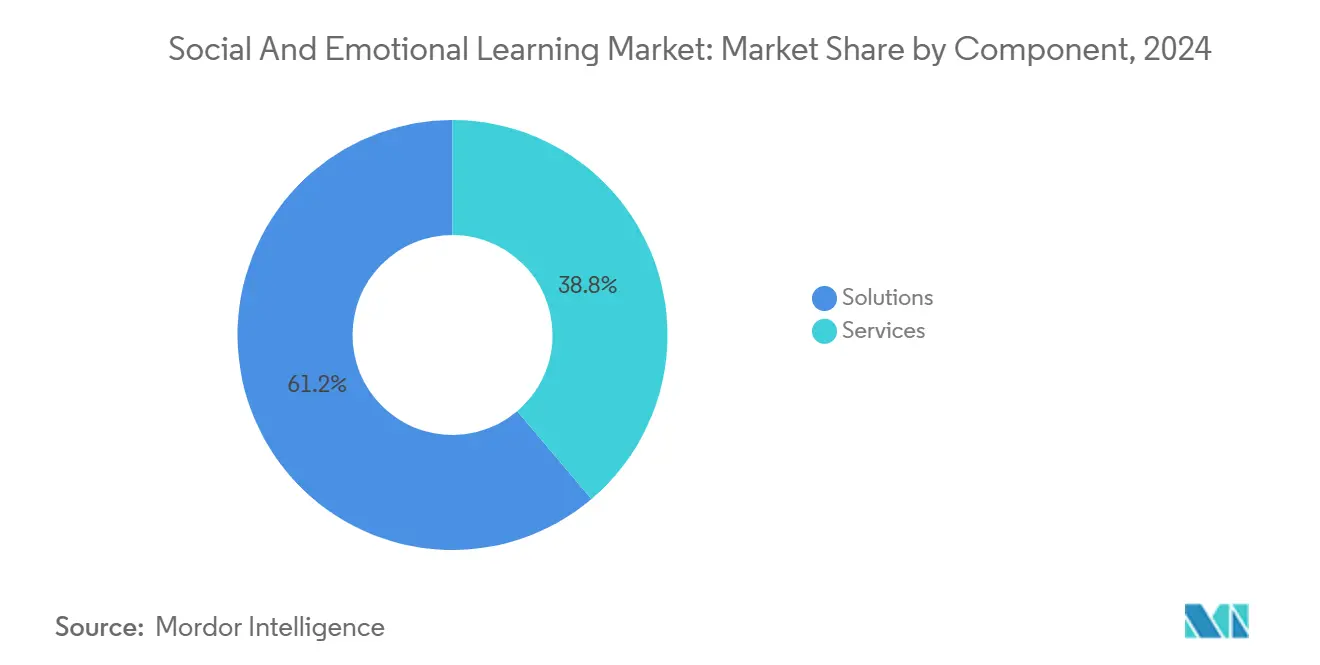

- By component, solutions led with a 61.20% share in 2024, whereas services are projected to grow at a 2.37% CAGR to 2030.

- By delivery mode, cloud or web-based platforms accounted for 45.67% of the Social and Emotional Learning market share in 2024, while mobile apps are forecast to expand at a 2.62% CAGR through 2030.

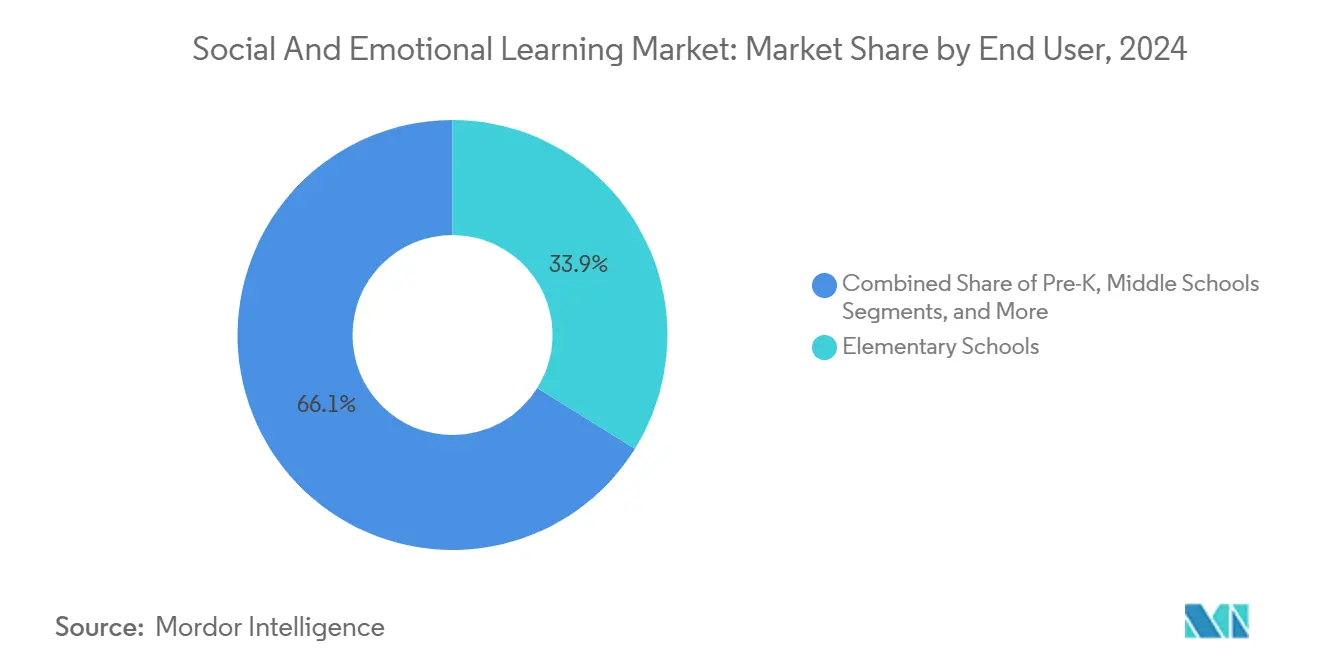

- By end user, elementary schools accounted for 33.88% of the Social and Emotional Learning market size in 2024, and corporate and workforce training is projected to post the fastest CAGR of 2.50% by 2030.

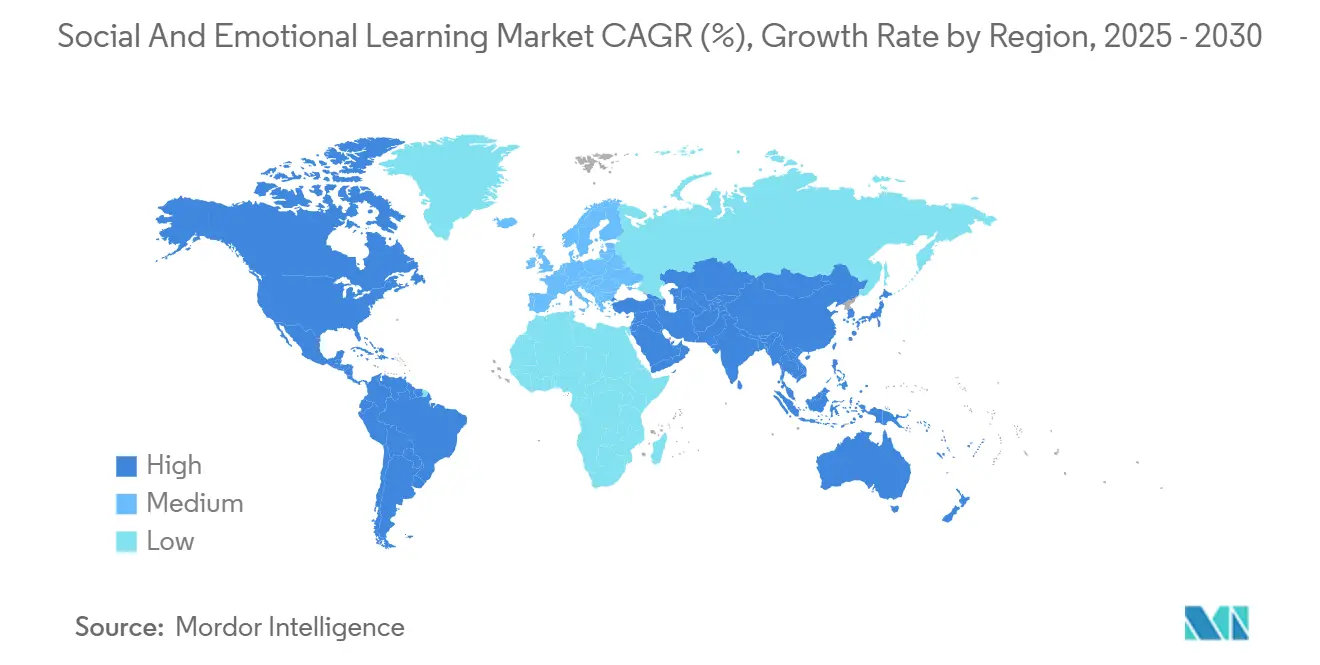

- By geography, North America commanded 38.32% revenue share in 2024, whereas the Asia-Pacific is poised to log a 2.87% CAGR during the same horizon.

Global Social And Emotional Learning Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government SEL mandates and funding proliferation | +0.6% | Global, with North America and Europe leading | Medium term (2-4 years) |

| Rising focus on student mental-health post-COVID | +0.4% | Global, concentrated in developed markets | Short term (≤ 2 years) |

| Evidence linking SEL to academic and workforce outcomes | +0.3% | Global, with strongest adoption in OECD countries | Long term (≥ 4 years) |

| AI-driven emotion analytics enable personalized SEL | +0.2% | North America and Asia-Pacific core, spill-over to Europe | Medium term (2-4 years) |

| Certified Wellness-Coach reimbursement models emerge | +0.2% | North America and Europe, early pilots in Australia | Long term (≥ 4 years) |

| Corporate soft-skills demand adopts SEL frameworks | +0.3% | Global, with enterprise concentration in North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government SEL Mandates and Funding Proliferation

Federal and state directives explicitly require districts to embed SEL competencies in core instruction, shifting the Social and Emotional Learning market toward long-term operating budgets rather than episodic stimulus grants. The Biden-Harris administration allocated USD 2.2 billion for school mental-health and safety programs in fiscal 2025, and portions of these resources are earmarked for SEL curriculum adoption [1]Maine Department of Education, “SEL Standards and Implementation Guidance,” maine.gov. Oregon’s statewide standards, effective in 2024, require districts to demonstrate measurable progress, while Japan’s Ministry of Education has selected standardized partners for a nationwide rollout [2]FCE, “World-Standard SEL to Japan Partnership Announcement,” prtimes.jp. Vendors able to quantify gains in behavior and academics are favored in request-for-proposal scoring, tightening competitive dynamics in the Social and Emotional Learning market.

Rising Focus on Student Mental Health Post COVID

Persistent anxiety, depression, and disruptive behaviors have prompted districts to treat SEL as core infrastructure. Surveys show 85% of U.S. educators rely on SEL platforms to flag at-risk learners before crises escalate. This shift from enrichment to necessity positions SEL budgets alongside those for technology and safety. Platforms that couple universal screeners with targeted interventions are seeing renewal rates above 90%, reinforcing predictable revenue streams in the Social and Emotional Learning market.

Evidence Linking SEL to Academic and Workforce Outcomes

Meta-analytic findings indicate an 11-point academic percentile gain for students receiving high-quality SEL instruction, which bolsters the value proposition for administrators and corporate learning leaders. In Kanagawa, six-month pilots reduced peer conflicts by 35%, validating the effectiveness of daily micro-lessons in elementary classrooms. Enterprises such as Microsoft apply the same frameworks in leadership training, reporting measurable improvements in employee engagement. Demonstrable cross-sector impact enlarges the Social and Emotional Learning market addressable base.

AI-Driven Emotion Analytics Enable Personalized SEL

Artificial intelligence now classifies sentiment in surveys, chat logs, and facial cues, generating tailored skill-building paths that cater to individual needs. Riverside Insights integrates Aperture Education’s data to deliver real-time risk alerts aligned with Multi-Tiered Systems of Support. Japanese ed-tech providers Smart Education and Cellbig pilot voice-tone analytics for student self-regulation drills. Adoption remains hindered by COPPA and FERPA compliance, as well as parental skepticism, yet districts recognize the potential for cost-efficient personalization, which can sustain premium growth pockets within the broader Social and Emotional Learning market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High implementation costs and teacher time constraints | -0.4% | Global, with acute impact in resource-constrained districts | Short term (≤ 2 years) |

| Political backlash and policy restrictions | -0.3% | North America core, with spillover to conservative regions globally | Medium term (2-4 years) |

| Data-privacy worries around emotion analytics | -0.2% | Global, with strictest enforcement in Europe and California | Long term (≥ 4 years) |

| Non-standard, culturally inclusive measurement gaps | -0.2% | Global, with particular challenges in diverse urban districts | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Implementation Costs and Teacher Time Constraints

Comprehensive SEL adoption requires 15-20 hours of initial educator training, plus quarterly coaching sessions, which creates labor burdens in systems already strained by substitute shortages. Districts juggling device replacement cycles and transportation costs often defer SEL unless vendors bundle professional development and progress monitoring. Because durable impact typically materializes after two years, superintendents face a misalignment between annual budgets and multi-year ROI, which tempers expansion velocity within the Social and Emotional Learning market.

Political Backlash and Policy Restrictions

Legislation in several US states limits classroom discussions on emotions and identity. The US Department of Education signaled a shift toward “patriotic education” priorities in competitive grants during September 2025, injecting uncertainty into district grant-writing pipelines [3]EdWeek Market Brief, “Elimination of Grants Alters Funding Landscape,” edweek.org. Vendors must localize content to varying statutes without diluting outcomes, diverting resources from innovation to compliance, and restraining near-term growth in the Social and Emotional Learning market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Solutions Anchor Long-Term Contracts

Solutions represented 61.20% of 2024 revenue, underscoring district preference for turnkey curriculum and assessment bundles that simplify procurement. Platforms like Second Step and Panorama tightly couple lessons, surveys, and dashboards, enabling holistic progress tracking across social awareness, self-management, and responsible decision-making. The Social and Emotional Learning market size for Services is projected to expand at a 2.37% CAGR as districts recognize that curriculum alone cannot change adult practice. Professional development, coaching, and managed services help teachers translate frameworks into daily routines, sustaining demand. Vendors that integrate fidelity tools and on-demand micro-coaching into existing learning management systems lower the total cost of ownership and deepen account stickiness.

Service acceleration signifies a maturing Social and Emotional Learning market, where decision-makers equate SEL with systemic improvement rather than add-on programs. Consulting partners align SEL with Positive Behavioral Interventions and Supports (PBIS) and Multi-Tiered Systems of Support (MTSS), optimizing resource allocation. Outsourced wellness-coach models are emerging in rural schools, offering subscription-based staff augmentation that parallels historical special-education contracting. As efficacy expectations rise, bundled implementation support is becoming non-negotiable in request-for-proposal scoring, thereby advantaging vendors with robust professional learning ecosystems.

By Delivery Mode: Cloud Platforms Dominate, Mobile Surges

Cloud or web-based platforms captured a 45.67% share in 2024 as districts sought centralized data, single sign-on convenience, and seamless integration of student information systems. The Social and Emotional Learning market share advantage stems from instant updates, automated reporting, and AI modules that cannot operate in isolated on-premise environments. Hybrid cloud architectures address bandwidth challenges in rural areas by caching content locally while syncing analytics to secure data centers overnight.

Mobile apps are forecast to post a 2.62% CAGR, fueled by the ubiquity of smartphones and bring-your-own-device policies. Just-in-time emotion check-ins and gamified micro-lessons extend practice beyond classroom walls, enriching personalized learning plans. Privacy hurdles remain significant because biometric and sentiment data traverse consumer devices. Vendors adhering to zero-knowledge encryption and parent dashboards are winning pilots, helping the Social and Emotional Learning market size expand among technology-forward districts.

By End User: Elementary Core Spurs Corporate Uptake

Elementary schools generated 33.88% of the revenue in 2024, reflecting the consensus that early interventions yield lifelong benefits. Educators report a stronger classroom climate and fewer behavioral referrals after integrating daily SEL routines in grades K-5. The Social and Emotional Learning market size among Corporate and workforce training users is projected to climb at a 2.50% CAGR through 2030. Enterprises turn to SEL frameworks to improve collaboration, empathy, and retention in hybrid workforces.

Higher education institutions embed SEL in teacher preparation curricula, ensuring future educators possess emotional literacy. Out-of-school providers and community organizations are pursuing grant-funded SEL to mitigate widening opportunity gaps, opening a new frontier for vendors willing to localize content and translate assessments. These cross-sector dynamics broaden the Social and Emotional Learning market beyond public K-12 classrooms.

Geography Analysis

North America retained 38.32% of 2024 revenue, anchored by USD 2.2 billion in federal mental-health allocations and state mandates that embed SEL into accountability frameworks. Centralized grant guidance and mature ed-tech ecosystems enable rapid procurement cycles. Multilingual content and research partnerships with universities further differentiate US vendors, fortifying the region’s leadership in the Social and Emotional Learning market.

Asia-Pacific is on track for a 2.87% CAGR through 2030. Japan’s Ministry of Education selected curriculum partners for national deployment, creating consistent learning progressions and predictable funding. China integrates emotional intelligence modules into digital learning super-apps, while South Korea pilots AI voice-tonality coaching tools in public middle schools. Local language adaptation and alignment with high-stakes examination cultures are essential for scale; however, public-private alliances reduce market-entry friction, thereby accelerating the trajectory of the Social and Emotional Learning market.

Europe follows with coordinated policy via the Pathways to School Success initiative, embedding SEL into digital citizenship instruction. Germany and France emphasize data privacy under GDPR, compelling vendors to host data within the European Economic Area. South America, the Middle East and Africa remain nascent but exhibit increasing interest among urban districts tackling post-pandemic learning loss. International development agencies promoting social cohesion view SEL as a low-cost lever, positioning these regions as long-run growth optionality for the Social and Emotional Learning market.

Competitive Landscape

The Social and Emotional Learning market remains fragmented, with no seller controlling more than 5% of global revenue. Traditional curriculum publishers, niche analytics start-ups, and AI emotion-recognition innovators vie for district budgets. Riverside Insights acquired Aperture Education in September 2024 to integrate assessments with cognitive diagnostics, and FullBloom acquired CharacterStrong in February 2025 to align counseling services with curriculum.

Competitive advantage increasingly hinges on evidence, interoperability, and privacy safeguards. Panorama Education connects SEL metrics with attendance and grade files, delivering multidimensional insights valued by superintendents. Smart Education and Cellbig co-develop bilingual AI companions that coach self-management in real time. Vendors lacking data warehousing and legal compliance infrastructure struggle to clear purchasing thresholds, prompting partnerships with cybersecurity specialists.

White-space opportunities lie in culturally responsive content for multilingual classrooms and in managed services that alleviate teacher workload. Investors prefer platforms that generate recurring revenue from both software and professional services. The Social and Emotional Learning market is expected to remain acquisition-heavy as private-equity sponsors guide portfolio roll-ups to reach scale and diversify geographic exposure.

Social And Emotional Learning Industry Leaders

Emotional ABCs Inc.

EVERFI Inc.

Second Step (Committee for Children)

The Social Express Inc.

Everyday Speech

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: The US Department of Education shifted competitive grants toward patriotic education priorities, reducing some SEL funding streams.

- June 2025: Smart Education signed an MOU with South Korea’s Cellbig to co-develop AI-enhanced SEL content for the Japanese market.

- February 2025: FullBloom acquired CharacterStrong, expanding its integrated student mental health and SEL programming.

- September 2024: Riverside Insights purchased Aperture Education, combining SEL assessments with cognitive analytics.

Global Social And Emotional Learning Market Report Scope

- Social and emotional learning (SEL) is a process developed to lead children and adults to understand and manage emotions, set and achieve positive goals, reduce anxiety, boost confidence, establish positive relationships, improve social interactions, etc. SEL helps students and adults succeed in school and life.

- The social and emotional learning market is segmented by component, end user, and geography. By component, the market is divided into solutions and services. By end user, the market is segmented into pre-K, elementary schools, and middle and high schools. By geography, the market is segmented by North America, Europe, Asia-Pacific, and Rest of the World.

- The market size and forecasts are provided in terms of value (USD) for all the above segments.

| Solutions | Curriculum/Content Platforms |

| Assessment and Analytics Tools | |

| Programmatic Implementation Bundles | |

| Stand-alone Lesson Modules | |

| Services | Professional Development and Coaching |

| Implementation and Consulting | |

| Managed SEL Services/Outsourcing |

| On-Premise Classroom-Based |

| Cloud/Web-Based Platforms |

| Mobile Apps |

| Pre-K |

| Elementary Schools |

| Middle Schools |

| High Schools |

| Higher Education |

| Out-of-School/After-School Programs |

| Corporate and Workforce Training |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East | GCC |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Rest of Africa |

| By Component | Solutions | Curriculum/Content Platforms |

| Assessment and Analytics Tools | ||

| Programmatic Implementation Bundles | ||

| Stand-alone Lesson Modules | ||

| Services | Professional Development and Coaching | |

| Implementation and Consulting | ||

| Managed SEL Services/Outsourcing | ||

| By Delivery Mode | On-Premise Classroom-Based | |

| Cloud/Web-Based Platforms | ||

| Mobile Apps | ||

| By End User | Pre-K | |

| Elementary Schools | ||

| Middle Schools | ||

| High Schools | ||

| Higher Education | ||

| Out-of-School/After-School Programs | ||

| Corporate and Workforce Training | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East | GCC | |

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

Key Questions Answered in the Report

How large is the Social and Emotional Learning market in 2025?

The Social and Emotional Learning market size reached USD 9.25 billion in 2025.

What is the expected growth rate for the Social and Emotional Learning market to 2030?

The Social and Emotional Learning market is projected to grow at a 1.87% CAGR, reaching USD 10.15 billion by 2030.

Which component dominates spending?

Solutions account for 61.20% of 2024 revenue, reflecting demand for bundled curriculum and assessment platforms.

Which region is growing fastest?

Asia-Pacific is forecast to post the fastest 2.87% CAGR through 2030 because of government-led initiatives in Japan, China and South Korea.

What restraints could slow adoption?

High implementation costs, teacher time constraints and political backlash create short- to medium-term headwinds.

How are vendors differentiating their offerings?

Leading providers integrate AI, real-time analytics and professional development to deliver measurable student outcomes while meeting privacy mandates.

Page last updated on: