Spa Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

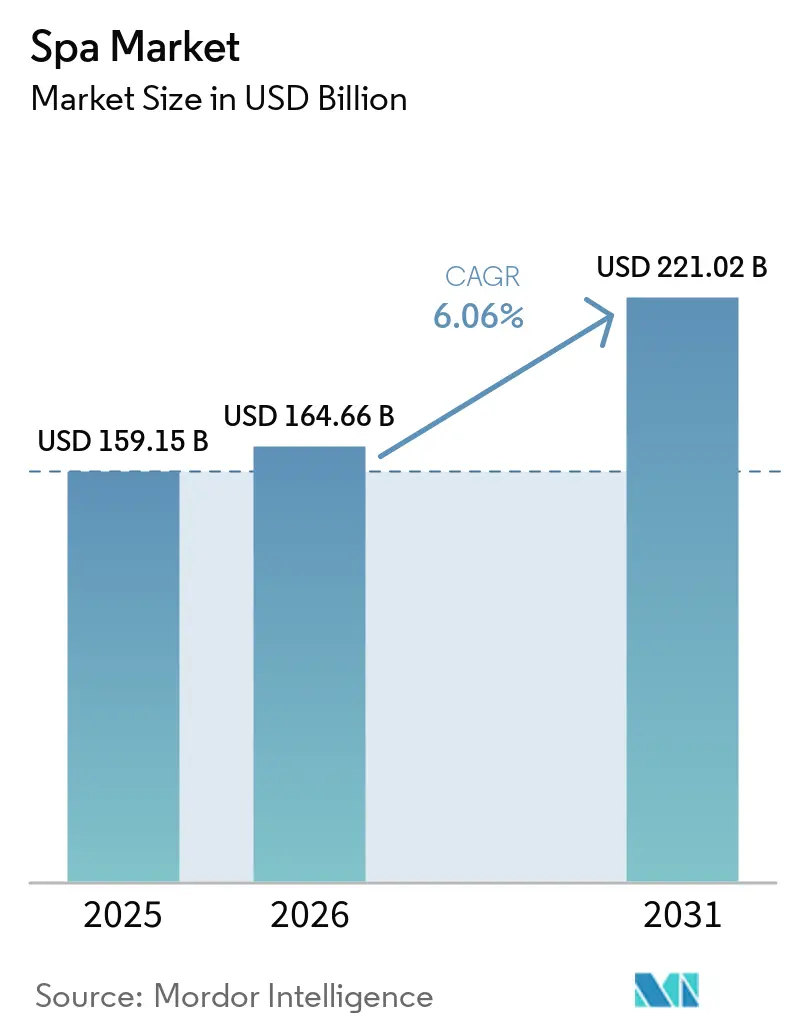

| Market Size (2026) | USD 164.66 Billion |

| Market Size (2031) | USD 221.02 Billion |

| Growth Rate (2026 - 2031) | 6.06% CAGR |

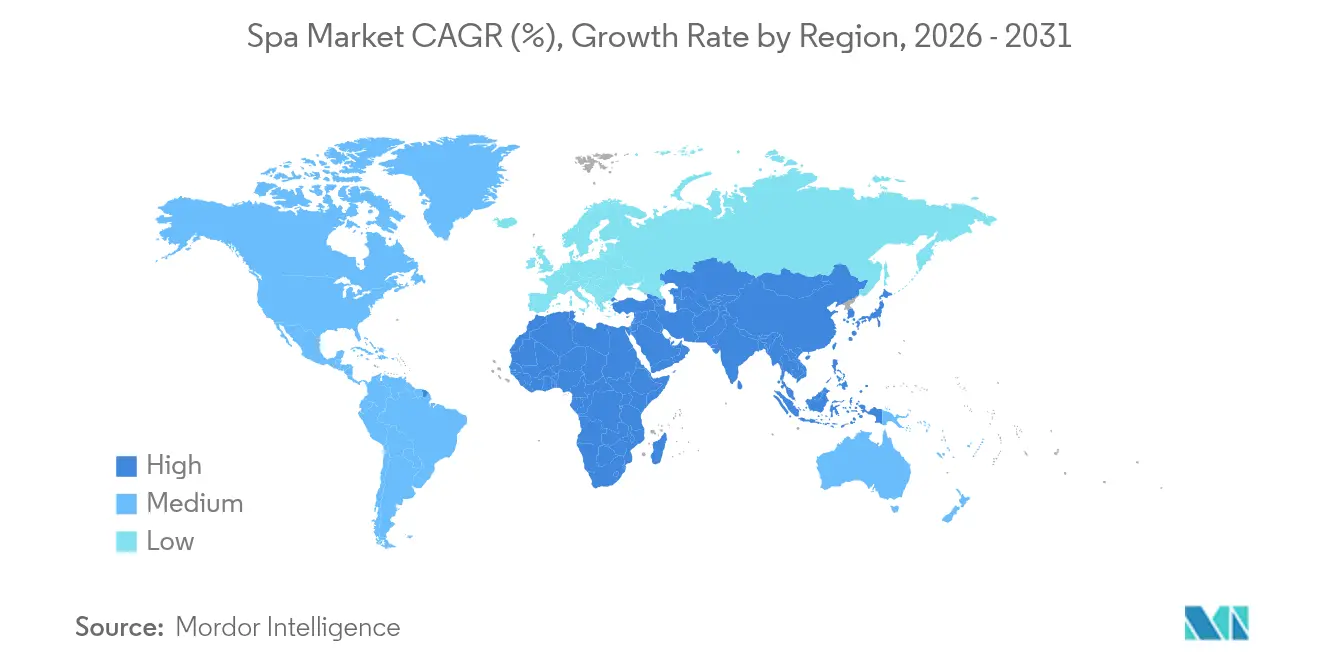

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Spa Market Analysis by Mordor Intelligence

The spa market size is expected to grow from USD 159.15 billion in 2025 to USD 164.66 billion in 2026 and is forecast to reach USD 221.02 billion by 2031 at 6.06% CAGR over 2026-2031. Demand continues to expand as consumers blend wellness with travel, technology reshapes service delivery, and regulatory frameworks expand the scope of medical-grade services within wellness environments. Wellness tourism momentum continues to drive on-site spa visitation, benefiting operators that integrate structured programs into premium itineraries and domestic retreats led by Asia-Pacific and Europe. Operators scale AI-powered skin diagnostics and robotic massage to address staffing constraints while preserving treatment consistency in the spa market. Aging populations drive sustained demand for therapeutic services and recovery protocols, with OECD markets increasingly aligning wellness and health-system objectives, including physician-guided hydrotherapy programs in select European countries.

Key Report Takeaways

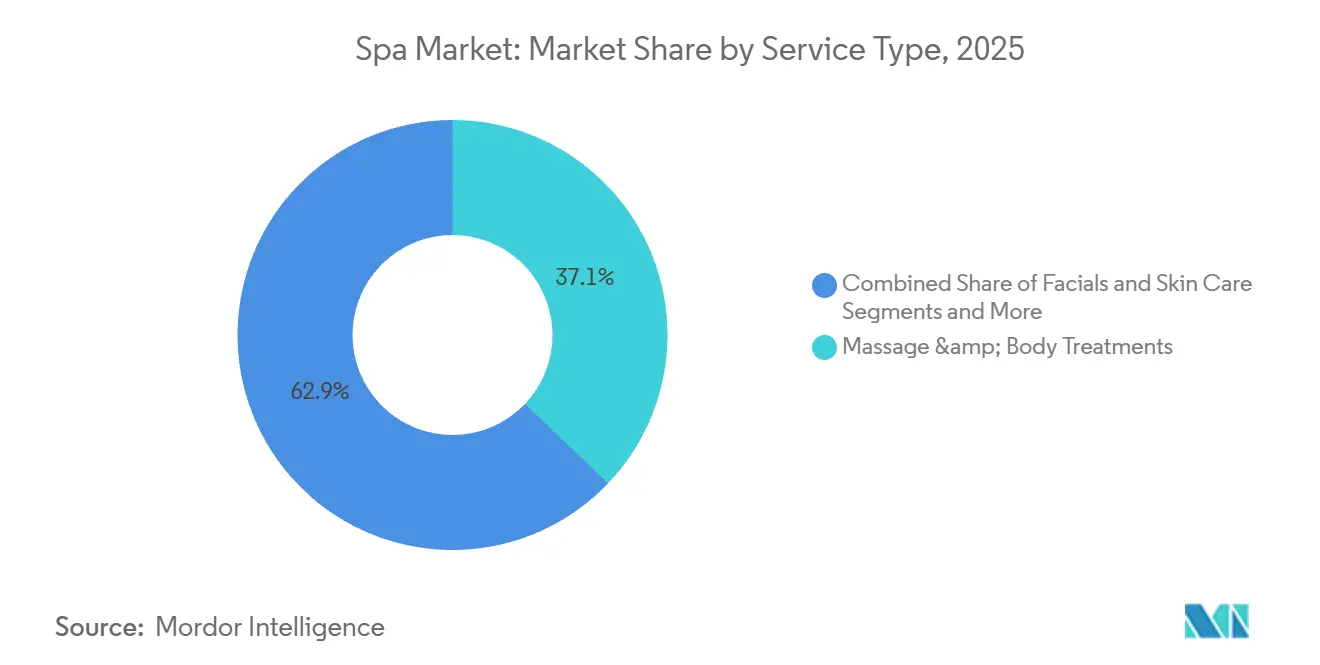

- By service type, massage and body treatments led with 37.12% of the Spa Market size in 2025, while medical and medi-spa treatments are forecast to expand at an 8.95% CAGR through 2031.

- By facility type, day and club spas held 43.68% of the Spa Market size in 2025, while medical spas recorded the fastest growth at a 9.95% CAGR through 2031.

- By booking channel, on-site and walk-in captured 71.35% of the Spa Market size in 2025, while online and mobile-app bookings advanced at an 8.05% CAGR.

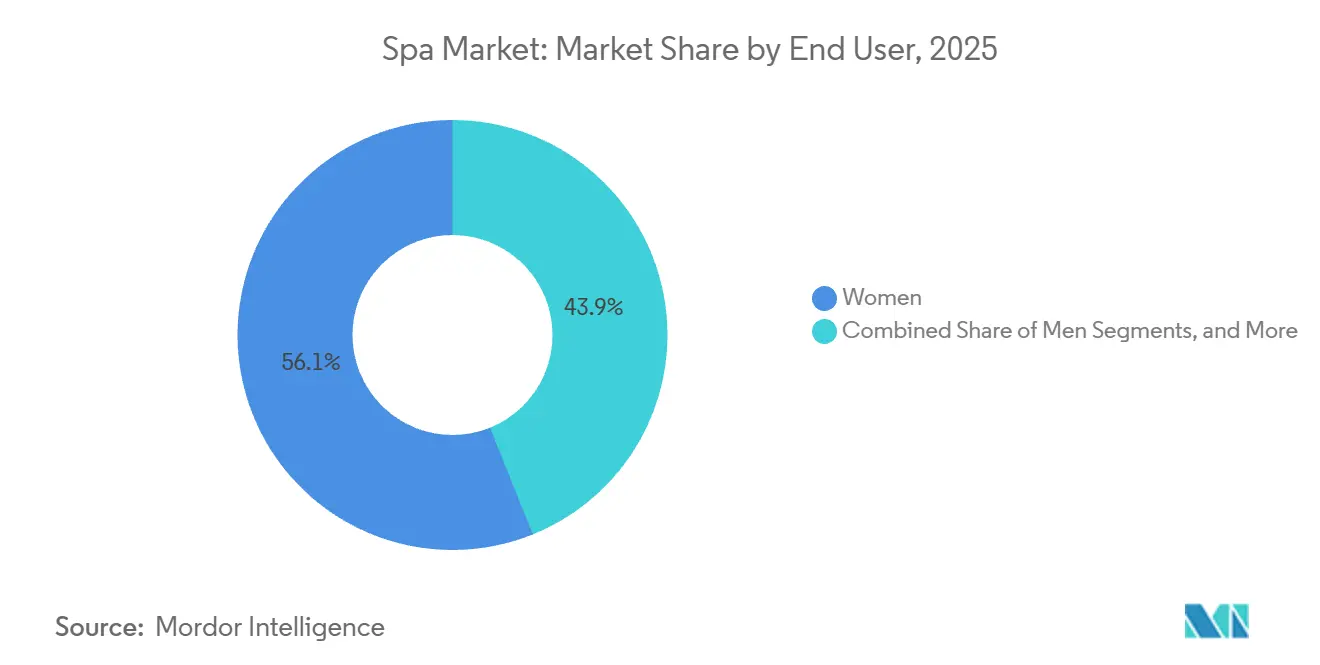

- By end user, women accounted for 56.10% of the Spa Market size in 2025, while family and group bookings posted the highest projected growth at an 8.56% CAGR.

- By geography, Europe contributed 36.35% of the Spa Market size in 2025, while Asia-Pacific is projected to grow at an 8.97% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Spa Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth in Wellness Tourism and Experiential Travel | +1.2% | Global, led by Asia-Pacific and Europe | Medium term (2-4 years) |

| Expansion of Disposable Income in Emerging Markets | +0.8% | Asia-Pacific core, spill-over to Middle East | Long term (≥ 4 years) |

| Ageing Demographics Boosting Health-Focused Spa Visits | +1.1% | Europe and North America, expanding to Japan and South Korea | Long term (≥ 4 years) |

| Adoption of Corporate Wellness Programs | +0.7% | North America and Europe | Medium term (2-4 years) |

| Implementation of AI-Driven Personalized Treatment Protocols | +0.9% | Global, early gains in United States, China, United Kingdom | Short term (≤ 2 years) |

| Emergence of Subscription-Based Urban Micro-Spa Models | +0.6% | National, with early gains in United States and Canada | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growth in Wellness Tourism and Experiential Travel

According to the Global Wellness Institute (GWI), the global wellness economy reached a record USD 6.8 trillion in 2024 and is projected to approach nearly USD 10 trillion by 2029, significantly outpacing overall global GDP growth. This rapid expansion is a key driver of growth in wellness tourism and experiential spa travel. Increasing consumer emphasis on preventive health, longevity, mental well-being, and holistic lifestyles is reshaping travel behavior, with more travelers prioritizing health-focused and restorative experiences. Wellness tourism has emerged as one of the fastest-growing segments within the broader wellness economy, supported by strong demand for immersive, personalized, and multi-day spa and retreat programs that combine relaxation with measurable well-being outcomes. Additionally, post-pandemic shifts toward self-care, sustainable living, and experiential spending particularly among younger demographics are accelerating demand for destination spas, thermal and mineral springs, and integrated wellness resorts, positioning experiential spa travel as a central growth engine within the global tourism market.[1]Source: Global Wellness Institute, “Wellness Market Hits $6.8T,” November 25, 2025, globalwellnessinstitute.org.

Expansion of Disposable Income in Emerging Markets

Rising incomes in China, India, Vietnam, and Indonesia are expanding the reachable audience for premium and preventive wellness services, lifting utilization rates at hot-spring resorts and urban wellness hubs that integrate traditional treatments with modern protocols. Spa revenue growth in Asia reflects this consumer expansion, with China’s spa market generating over $15 billion in revenues in 2024, while India and Indonesia recorded strong double-digit revenue growth rates of approximately 21.9% and 20.7%, respectively, as middle-income households adopt wellness services more routinely. China’s hot-spring destinations attracted 60 million domestic visitors in 2024 across more than 1,000 locations, providing steady throughput for spa facilities that anchor larger hospitality complexes. India’s spa economy grew 11.3% annually from 2019 to 2024, powered by Ayurveda-focused centers that package Panchakarma, yoga, and herbal therapies for both domestic and inbound guests.[2]Source: Global Wellness Institute, “Wellness Market Hits $6.8T,” November 25, 2025, globalwellnessinstitute.org. Operators localize format and pricing to capture middle-class households, while resort brands expand family and group offerings to raise average spend per stay. Regulatory standards vary across the region, and uneven licensing or product-safety enforcement can limit brand portability across borders without sustained investment in compliance, therapist certification, and training.

Ageing Population Driving Health-Focused Spa Visits

By 2030, one in six people will be 60 or older, and this demographic transition shifts spa programming toward therapeutic offerings, recovery services, and chronic-condition support delivered alongside traditional treatments.[3]Source: World Health Organization Communications, “Ageing and Health,” World Health Organization, who.int. Several European systems integrate reimbursed hydrotherapy and balneotherapy into care pathways, sustaining patient volumes at accredited thermal centers that work under physician guidance in countries such as France and Poland. The spa market also sees growth in strength, mobility, and lymphatic treatments that align with aging-well priorities, while urban medical spas add post-procedure recovery protocols that appeal to older adults seeking supervised care environments. Longevity-focused retreats add diagnostics and personalized regimens, and premium operators scale structured programs for cohorts that value measurable outcomes and clinician oversight. As reimbursement frameworks evolve and consumer health priorities mature, facilities that connect wellness services to validated benefits stand to capture higher retention and referral patterns within the spa market.

Adoption of Corporate Wellness Programs

Employers in North America and Europe expand wellness budgets and integrate spa partnerships into benefit design, which converts episodic leisure spend into recurring utilization tied to employee wellbeing goals in the spa market. Corporate off-sites now blend guided meditation, nutrition education, and forest bathing with physical recovery services to improve stress management and perceived productivity gains. Urban micro-spas near business districts offer express services that fit within workday schedules, which supports consistent midweek demand. Membership frameworks and digital management tools create a predictable appointment cadence for employee cohorts, improving capacity planning and service mix allocation across locations. While privacy regulations limit employers’ ability to link individual outcomes to performance metrics, measured engagement and utilization trends still support ongoing partnerships in the spa market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Operating and Labor Expenses | -0.9% | Global, acute in North America and Western Europe | Medium term (2-4 years) |

| Fluctuating Seasonal Demand in Resort Areas | -0.4% | Global, particularly affecting tropical and alpine locations | Short term (≤ 2 years) |

| Scarcity of Certified Therapists in Key Markets | -0.7% | North America, Australia, United Kingdom | Long term (≥ 4 years) |

| Privacy Risks in Biometric Diagnostics | -0.3% | Europe (GDPR), United States (HIPAA), expanding globally | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Operating and Labor Expenses

Labor represents the largest cost component for many resorts and premium urban spas, with payroll accounting for a substantial share of total operating expenses, placing pressure on margins when service pricing cannot increase in step with wage growth. Persistent shortages of qualified therapists have constrained appointment availability and extended booking lead times in key markets, limiting revenue capture during peak demand periods. At the same time, higher costs for utilities, laundry services, and premium skincare consumables continue to weigh on operating economics that depend on strong utilization rates and retail attachment. To offset these pressures, operators are implementing dynamic workforce scheduling, centralized procurement systems, and selective automation to improve productivity and reduce idle capacity. However, regulatory compliance related to wages, benefits, and gratuity structures limits pricing flexibility and cross-subsidization strategies, increasing the need for optimized service mixes and bundled offerings that raise average transaction values while preserving competitiveness.

Fluctuating Seasonal Demand in Resort Areas

Resort spas experience sharp swings in utilization due to weather cycles and travel patterns, which complicates staffing stability and inventory planning in the spa market. Off-peak periods reduce ancillary retail sales and tip revenue even when rate promotions stimulate bookings, which can dilute unit margins. Local-resident campaigns and corporate off-sites help fill midweek gaps in suburban and near-urban resorts, but pure destination properties often lack sufficient catchment to offset travel troughs. Climate variability increases planning uncertainty, with extended storm seasons in the Caribbean and shifting snow cover in alpine regions, which compresses peak windows. Some operators add conferences and training events to smooth revenue, but these require new marketing channels and operational adjustments that not all properties can support.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Medical Aesthetics Outpace Traditional Modalities

Massage and body treatments accounted for 37.12% of 2025 revenue, maintaining a broad base of recurring demand through standardized modalities and subscription models that fit urban lifestyles in the spa market. Medical and medi-spa treatments are projected to grow at an 8.95% CAGR to 2031 as non-invasive options like injectables and device-led skin rejuvenation formalize their role within wellness menus. Facials and skincare services benefit from AI diagnostics that inform regimen design, which improves retail attachment and course-of-care adherence across chains. Hydrotherapy and thermal springs continue to anchor national wellness traditions and public-health pathways in select European markets where physician oversight and reimbursement sustain utilization. Germany’s 350 medicinal baths illustrate the enduring role of regulated balneotherapy within a wider wellness ecosystem that coexists with modern medi-spa formats.

Growth within medical aesthetics shifts the mix toward higher-yield services, and operators reconfigure treatment rooms to accommodate device platforms and recovery protocols within the spa market. Cross-training and scope-of-practice rules influence staffing models as providers add nurse practitioners and physician assistants in jurisdictions that permit expanded practice under collaborative agreements. Standardized intake and photography support before-and-after documentation, which aligns with outcome-focused consumer expectations and informed consent requirements. Device procurement, maintenance, and quality controls require capital planning and vendor partnerships that protect uptime and safety while enabling menu refresh cycles. This segment dynamic supports sustained expansion of the spa market size as operators integrate clinical-grade services alongside traditional wellness experiences.

By Facility Type: Medical Spas Challenge Day-Spa Incumbency

Day and club spas held 43.68% of 2025 revenue, supported by dense urban coverage, after-work appointments, and membership economics that stabilize throughput in the spa market. Medical spas are expanding at a 9.95% CAGR through 2031, and state-level rules are reducing barriers to formation, including California’s AB-890, which allows qualifying nurse practitioners to hold majority ownership under defined parameters starting in 2026. Destination and resort spas rely on premium multi-day packages but face volatility tied to seasonal travel cycles and international airlift. Hotel and cruise-ship spas benefit from captive audiences and packaging with rooms and shore excursions, while revenue sharing with hospitality partners shapes margin profiles. Global concession operators scale through standardized protocols and technology platforms that deliver reliable service quality across fleets and resort portfolios.

Thermal and mineral-spring facilities maintain strongholds where reimbursement or medical referrals are established, preserving patient flows independent of discretionary cycles in the spa market. Hybrid formats blur boundaries as resorts add supervised injectables and urban medical spas pilot overnight recovery suites for select procedures. Scope-of-practice and supervision rules drive service differentiation across states and countries, and brands adjust menus accordingly to maintain compliance. Franchised medical-spa networks invest in training, credentialing oversight, and clinical governance to scale safely while protecting brand standards. These shifts support share capture by medical spas while day and club formats defend volume with convenience, access, and price transparency that fit weekly wellness routines.

By Booking Channel: Digital Platforms Erode Walk-In Dominance

On-site and walk-in bookings retained 71.35% of 2025 volume, a reflection of hotel-concierge upselling and spontaneous resort purchases that remain core to leisure-spa behavior in the spa market. Online and mobile-app bookings are advancing at an 8.05% CAGR, helped by real-time availability, automated reminders, and integrated payments that streamline the scheduling journey for guests and members. Mobile-first design dominates usage patterns, and social media booking flows shorten conversion paths by bringing scheduling inside discovery channels. Chatbots handle high volumes of routine questions and raise conversion when response times remain rapid, which reduces phone dependency and lowers no-show rates in the spa market. Accessibility and security requirements also shape product roadmaps for vendors and brands as PCI and ADA rules apply to digital properties as well as physical locations.

Walk-in traffic persists among older demographics and in resort settings, where spontaneity and on-property promotions drive impulse purchases in the spa market. Subscription models accelerate digital adoption as members manage recurring sessions, rollover credits, and retail bundles inside branded apps. Unified client profiles allow cross-location recognition for large chains, which improves personalization and inventory placement for high-turnover items. Integrations with hotel PMS and cruise POS systems support upselling and charge-to-room functionality, which lifts attach rates on packages. As mobile and AI features mature, the share of digital-originated appointments is likely to keep climbing, reducing idle capacity and strengthening yield management for operators.

By End User: Family Programming Challenges Female-Centric Models

Women represented 56.10% of 2025 spending, a result of long-standing service design that includes prenatal massage, hormone-support facials, and integrated skincare regimens tailored to female priorities in the spa market. Family and group bookings are projected to grow at an 8.56% CAGR, and operators expand intergenerational retreats and teen-friendly offerings to diversify beyond couples-only formats. Men’s services continue to widen from sports recovery to hair and skin treatments that emphasize outcomes and convenience. Couples suites and synchronized services remain core to romantic-getaway itineraries, though frequency is constrained by price sensitivity compared with individual bookings. This evolving mix pushes brands to adapt staffing, training, and product choices that address a broader set of needs within the spa market.

Expanding family and group formats introduce operational considerations, including guardian-consent processes, age-appropriate menus, and product safety for minors that require staff training and documentation. Group events such as bridal parties and corporate wellness days raise weekend occupancy but compress margins through volume discounts and peak-time congestion. Urban locations adjust scheduling to avoid family-program overlap with corporate peak hours, while resorts structure programming to stagger use of hydrothermal areas. Consistent experience across demographics depends on refining protocols and specializing staff to balance throughput with personalization in the spa market. As these segments mature, operators measure retention and referral effects to guide investment in spaces and services that support multi-guest itineraries.

Geography Analysis

Europe held 36.35% of global revenue in 2025, anchored by thermal-spa infrastructure and partial reimbursement models that integrate hydrotherapy into standard care pathways in select countries within the spa market. Germany operates more than 350 medicinal baths, where physician-prescribed treatments for chronic conditions sustain steady demand outside discretionary cycles. France’s 89 accredited thermal spas also benefit from public-health funding that supports physician-supervised programs, and that institutional linkage improves occupancy resilience through the year. Northern European operators emphasize sustainability through renewable energy, natural materials, and responsible sourcing to attract eco-conscious travelers. In Southern Europe, seasonality remains a structural headwind, which encourages yield management and resident-focused offers to maintain baseline throughput.

Asia-Pacific is projected to grow at an 8.97% CAGR, driven by domestic hot-spring tourism and traditional-medicine modalities that scale through modern hospitality in the spa market. China’s extensive hot-spring network attracts tens of millions of visitors annually across more than a thousand destinations, with provincial investment programs extending guest stays through integrated wellness, recreation, and retail offerings. India’s spa economy has expanded steadily in recent years, led by Ayurvedic centers in Kerala and Rajasthan that promote immersive, multi-week programs combining Panchakarma, yoga, and herbal therapies for both domestic and international guests. Across Southeast Asia, technology adoption enhances language accessibility, digital booking, and operating efficiency as destinations capture rising regional travel flows. At the same time, regulatory frameworks governing traditional medicine, product standards, and therapist licensing play a critical role in determining cross-border brand scalability and vendor partnerships.

North America reflects a bifurcated structure in which luxury hotel spas coexist with mass-market franchise concepts that broaden access and increase visit frequency. Hotel spas in the United States have recorded solid gains in revenue per available room as wellness becomes more deeply embedded in both business and leisure travel itineraries. Franchise-based micro-spa operators such as Massage Envy and Hand & Stone have expanded suburban penetration through membership-driven models that generate recurring revenue and stable utilization. Ongoing therapist shortages continue to shape capacity planning decisions and have accelerated experimentation with robotic and technology-assisted massage solutions in selected fitness and spa chains focused on standardized, on-demand delivery. In the Middle East, sovereign-supported destination developments are adding large-scale premium wellness facilities, reinforcing the region’s ambition to position itself as a global hub for luxury health and lifestyle tourism.

Competitive Landscape

The spa market remains moderately concentrated among leading global brands while highly fragmented overall, with major operators such as Four Seasons, Marriott, Mandarin Oriental, Hilton, and OneSpaWorld collectively representing a relatively small portion of total market share as independent and regional providers account for the majority of locations. Competitive strategy increasingly emphasizes technology enablement, longevity and recovery-focused programming, sustainability positioning, and membership-based models that create more predictable demand patterns. Large operators favor asset-light concession structures within cruise ships and integrated resorts, leveraging standardized operating frameworks and strategic vendor partnerships to scale efficiently with limited capital intensity. Digital infrastructure has become essential, with advanced scheduling, payment, and analytics platforms supporting consistency and yield optimization across multi-location networks. This blend of brand power and operational tooling allows larger groups to defend premium positioning while adapting to localized market conditions.

Expansion pipelines highlight continued investment in wellness-led hospitality concepts across both luxury and mass-market segments. Global luxury brands are advancing extensive development programs that integrate comprehensive spa programming into destination resorts and mixed-use projects, reinforcing wellness as a core brand pillar rather than a supplementary amenity. Franchise-based spa networks are simultaneously accelerating footprint growth through new unit openings and signed development agreements, supported by high-frequency membership models that drive recurring revenue and stable utilization. Performance metrics across these systems indicate strong consumer engagement with facials, massage therapy, and recurring treatment packages. Hotel groups are also expanding into new geographic markets with properties that embed signature spa concepts into full-service hospitality offerings, strengthening cross-selling opportunities between rooms, wellness, and food and beverage.

Operational innovation is increasingly visible as spa operators respond to labor constraints and rising digital expectations. Artificial intelligence–enabled diagnostics, automated booking interfaces, and early-stage robotic massage trials are being introduced to smooth capacity bottlenecks and enhance service consistency during peak periods. Destination-focused wellness brands continue to differentiate through curated signature programs, practitioner-led product standards, and international recognition that reinforces premium positioning. Branded wellness events and thematic activations across global portfolios further strengthen brand-level identity while showcasing holistic, integrated programming. Together, these strategic initiatives illustrate a market balancing scale expansion, service innovation, and experiential differentiation within an increasingly competitive global landscape.

Spa Industry Leaders

Four Seasons Hotels & Resorts

Marriott International (Incl. St. Regis, W, Ritz-Carlton spa brands

Mandarin Oriental Hotel Group

Steiner Leisure / OneSpaWorld

Hilton Worldwide (Eforea)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Four Seasons Hotels & Resorts announced its 65th-anniversary expansion pipeline, confirming over 60 projects in development globally, including wellness-focused resorts in Saudi Arabia at AMAALA and continued emphasis on integrated spa programming as a differentiator in luxury hospitality. Sixteen Four Seasons spas received Five-Star ratings in the 2026 Forbes Travel Guide.

- January 2026: Canyon Ranch unveiled its annual “Wellness Gold List,” recognizing wellness products and tools selected by integrative-health practitioners, and confirmed a new destination resort in the Austin, Texas, area scheduled to open in 2026. Canyon Ranch Tucson received three MICHELIN Keys and Lenox received two in the inaugural MICHELIN hotel ratings.

- January 2026: Hand & Stone Massage and Facial Spa opened 13 new locations and signed 12 franchise agreements in Q4 2025, reported average unit volume of USD 1.4 million, and completed more than 1.6 million facials during 2025 across 600+ locations. The brand targets further expansion to serve underserved suburban markets with its membership-driven model.

- December 2025: Hyatt announced the opening of Miraval The Red Sea in Saudi Arabia in Q1 2026, featuring a 40,000-square-foot spa positioned as the largest wellness facility in the Red Sea destination, signaling strategic entry into the Middle Eastern wellness-tourism sector.

Global Spa Market Report Scope

The spa market research report aims to provide a detailed analysis of the spa market. It focuses on spa industry statistics, market dynamics, customer trends, and insights into geographical segments. It also analyzes spa companies and the competitive landscape in the spa industry. The spa market is segmented by service type (salon/day spa, hotel/resort spa, medical spa, thermal/mineral spring spa, and destination spa ayurvedic/traditional spa) and geography (North America, Europe, Asia-Pacific, Latin America, and Middle East and Africa). The report offers the spa industry statistics, which include market size and forecasts for the spa market in value (USD) for all the above-mentioned segments.

| Massage and Body Treatments |

| Facials and Skin Care |

| Beauty and Grooming (Nails, Hair) |

| Hydrotherapy and Thermal/Mineral Springs |

| Medical / Medi-Spa Treatments |

| Others (Aromatherapy, Reiki, etc.) |

| Day / Club Spas |

| Destination and Resort Spas |

| Hotel / Cruise-Ship Spas |

| Medical Spas |

| Thermal and Mineral Spring Facilities |

| On-site / Walk-in |

| Online and Mobile App Bookings |

| Women |

| Men |

| Couples |

| Family / Group |

| North America | Canada |

| United States | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines) | |

| Rest of Asia-Pacific | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | |

| Russia | |

| Rest of Europe | |

| Middle East & Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East & Africa |

| By Service Type | Massage and Body Treatments | |

| Facials and Skin Care | ||

| Beauty and Grooming (Nails, Hair) | ||

| Hydrotherapy and Thermal/Mineral Springs | ||

| Medical / Medi-Spa Treatments | ||

| Others (Aromatherapy, Reiki, etc.) | ||

| By Facility Type | Day / Club Spas | |

| Destination and Resort Spas | ||

| Hotel / Cruise-Ship Spas | ||

| Medical Spas | ||

| Thermal and Mineral Spring Facilities | ||

| By Booking Channel | On-site / Walk-in | |

| Online and Mobile App Bookings | ||

| By End User | Women | |

| Men | ||

| Couples | ||

| Family / Group | ||

| By Region | North America | Canada |

| United States | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines) | ||

| Rest of Asia-Pacific | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | ||

| Russia | ||

| Rest of Europe | ||

| Middle East & Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East & Africa | ||

Key Questions Answered in the Report

What is the spa market size in 2025 and how fast is it growing?

The spa market size is USD 159.15 billion in 2025 and is projected to reach USD 221.02 billion by 2031 at a 6.06% CAGR, supported by wellness travel, technology adoption, and maturing regulatory frameworks.

Which service categories lead and which are growing fastest within the spa market?

Massage and body treatments lead with 37.12% of 2025 revenue, while medical and medi-spa treatments are the fastest-growing at an 8.95% CAGR through 2031, reflecting the rise of non-invasive, outcome-focused services.

Which regions are shaping near-term growth in the spa market?

Europe holds the largest revenue share at 36.35% in 2025 due to thermal-spa integration with public health, while Asia-Pacific is the fastest-growing region with an 8.97% projected CAGR driven by domestic demand and traditional modalities.

How is technology changing the spa market client journey and operations?

AI diagnostics, robotic massage, and predictive analytics improve personalization, capacity, and conversion, while mobile-first bookings and chatbots reduce no-shows and phone dependencies across chains and franchises.

What are the main constraints on spa market expansion?

The largest constraints are labor shortages, rising operating costs, seasonality in resort locations, and data-privacy compliance for biometric and health information that raise technology and governance overheads for independents and chains.

Which business models and formats are winning in the spa market today?

Subscription-based urban micro-spas and medical-spa formats show strong momentum due to predictable cash flow, higher visit frequency, and expanded scope of services enabled by state-level regulatory support and standardized operating playbooks.

Page last updated on: