Sauna And Spa Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

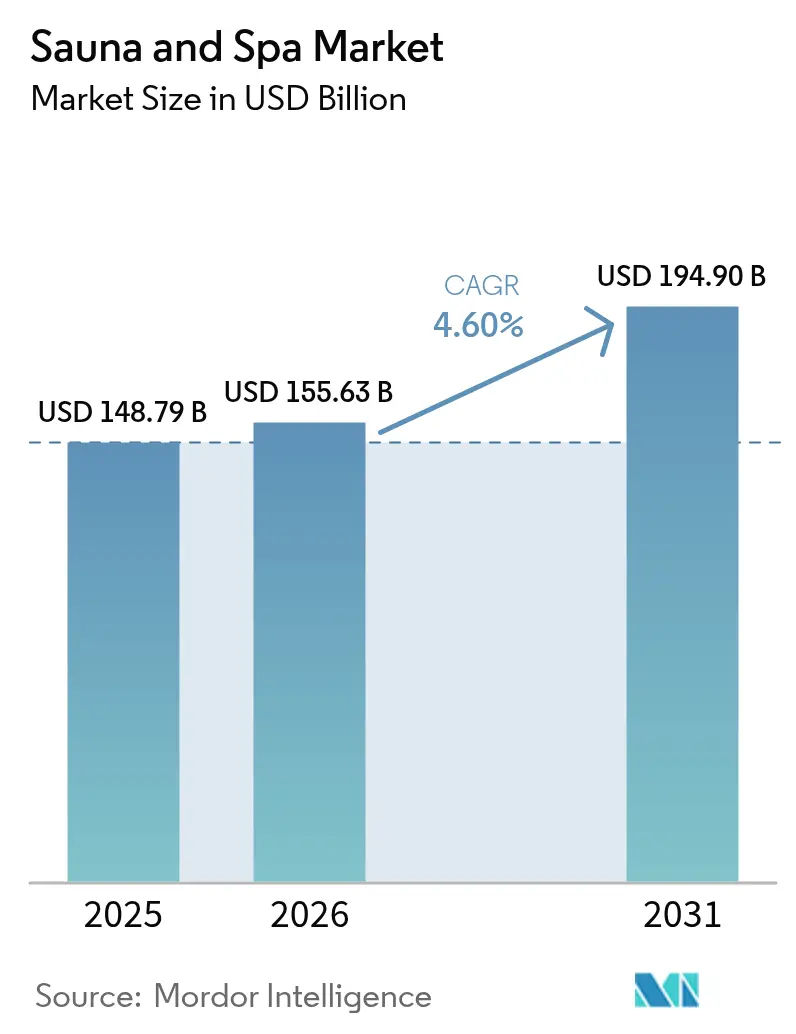

| Market Size (2026) | USD 155.63 Billion |

| Market Size (2031) | USD 194.9 Billion |

| Growth Rate (2026 - 2031) | 4.60% CAGR |

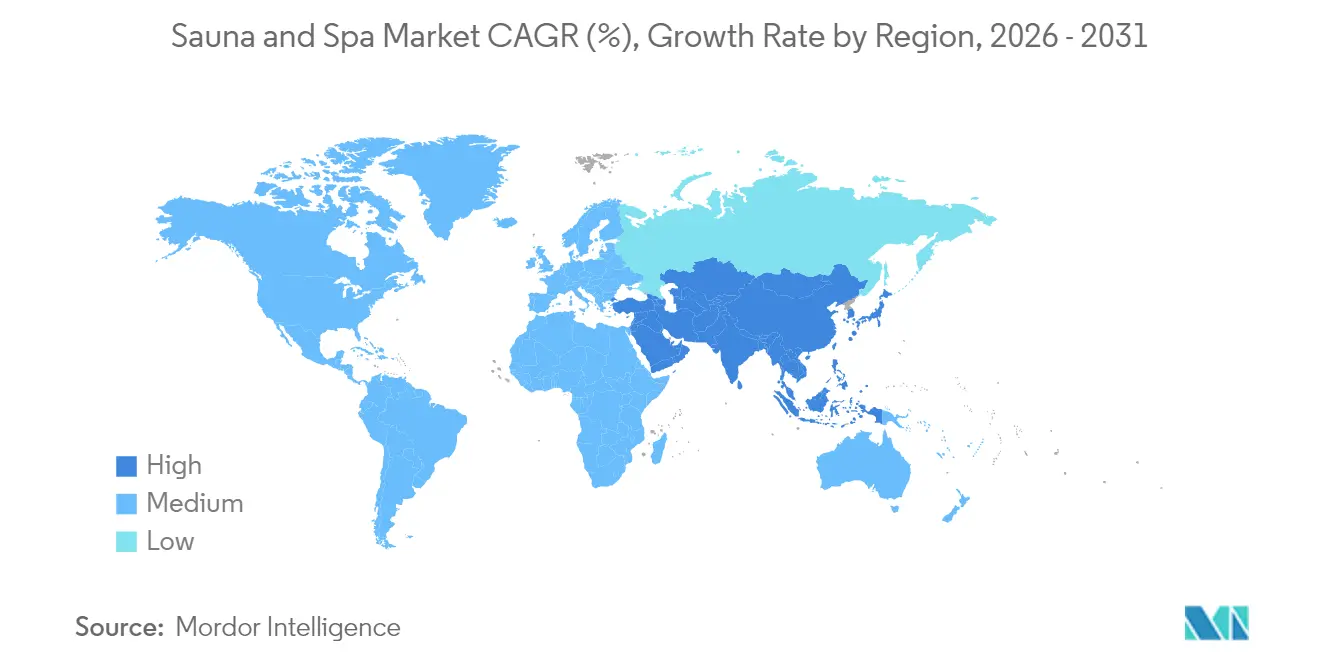

| Fastest Growing Market | Europe |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sauna And Spa Market Analysis by Mordor Intelligence

The sauna and spa market size in 2026 is estimated at USD 155.63 billion, growing from 2025 value of USD 148.79 billion with 2031 projections showing USD 194.9 billion, growing at 4.6% CAGR over 2026-2031. Post-pandemic demand for preventive health routines, surging wellness tourism spend, and ongoing corporate wellness investments are steering this steady expansion. Operators now view thermal suites as resilient dual-purpose assets producing high-margin hospitality revenues while doubling as therapeutic health infrastructure. Energy-efficient infrared cabins, mobile pop-ups, and smart-connected controls are widening access, while renovation activity is accelerating as facility owners retrofit older rooms to meet stricter sustainability mandates. Fragmented competitive dynamics further stimulate product innovation, regional specialization, and price differentiation.

Key Report Takeaways

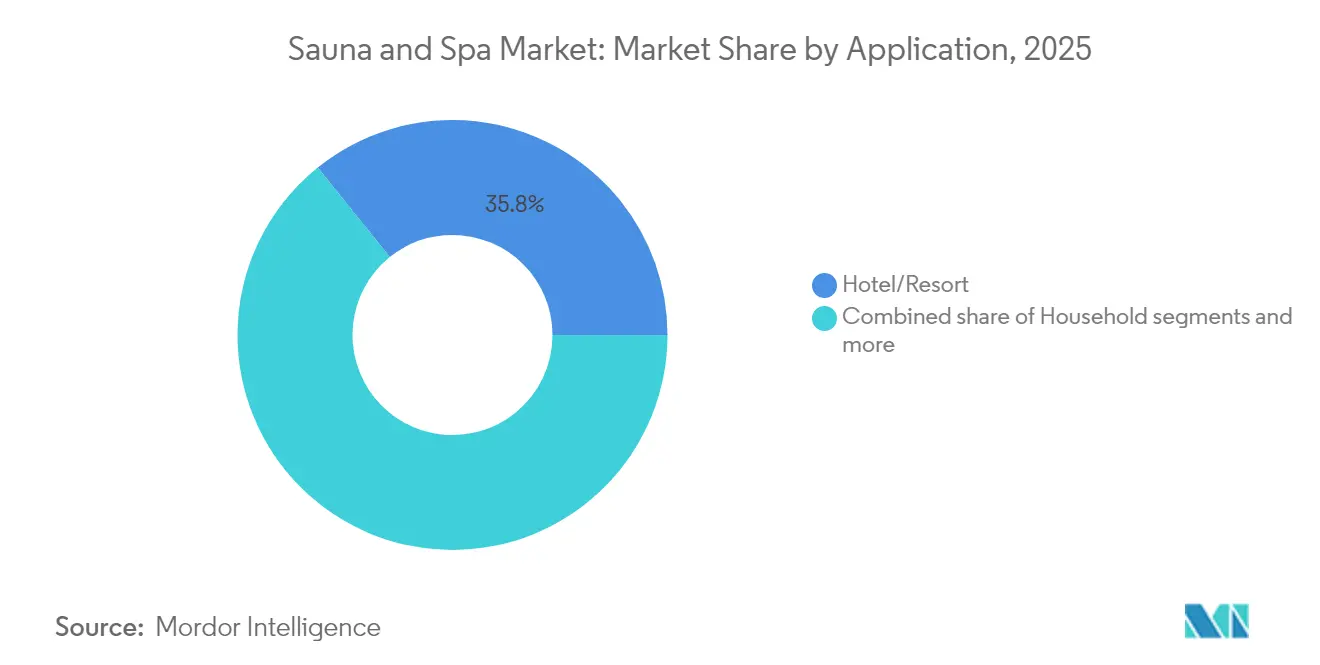

- By application, hotel and resort facilities led with 35.78% of the sauna and spa market share in 2025; household installations are forecast to expand at an 8.61% CAGR through 2031.

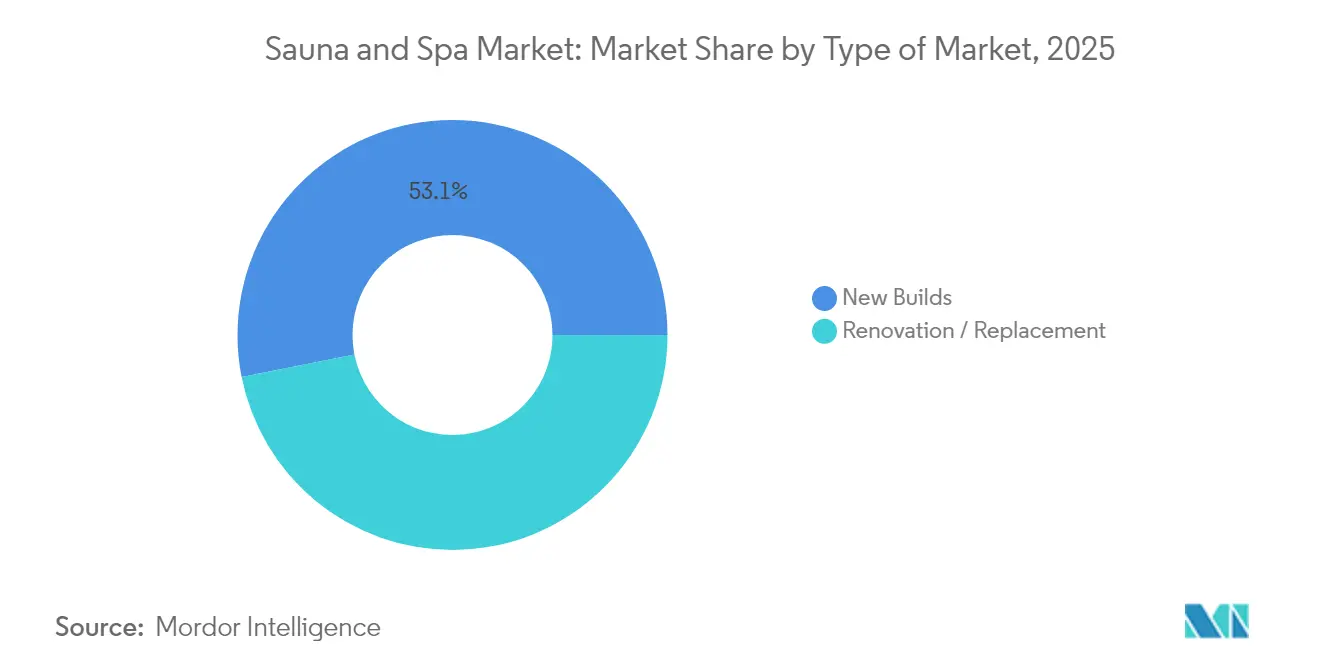

- By type of market, new construction commanded 53.12% share of the sauna and spa market size in 2025; renovation and replacement installations are projected to grow at a 7.12% CAGR to 2031.

- By product type, traditional Finnish units held 41.72% of the sauna and spa market size in 2025; infrared cabins are advancing at a 9.98% CAGR through 2031.

- By geography, Europe accounted for 31.88% of the sauna and spa market share in 2025; Asia-Pacific is set to register the hottest 9.05% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Sauna And Spa Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth of wellness tourism & hotel-led spa investments | +1.2% | Global, strongest in Europe & APAC | Medium term (2-4 years) |

| Rising consumer focus on longevity, sleep & immunity benefits | +0.9% | North America & Europe core, expanding to APAC | Long term (≥ 4 years) |

| Expansion of luxury real-estate wellness amenities | +0.8% | North America & Europe, emerging in APAC urban centers | Medium term (2-4 years) |

| Technology-enabled infrared & smart-sauna adoption | +0.7% | Global, led by North America tech integration | Short term (≤ 2 years) |

| Corporate wellness programmes funding on-site thermal suites | +0.5% | North America & Nordic countries, expanding globally | Medium term (2-4 years) |

| Urban pop-up / mobile saunas creating experiential demand | +0.3% | Europe & North America urban centers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growth of Wellness Tourism & Hotel-Led Spa Investments

Wellness tourism expenditure reached USD 651 billion globally, with thermal experiences commanding premium pricing that exceeds standard accommodation rates by 53%[1]CBI, “European Market Potential for Wellness Tourism,” cbi.eu. . Hotels increasingly position spa and sauna facilities as revenue centers rather than amenity costs, generating direct treatment income and extending average guest stays by 1.2 nights per visit. The integration of thermal circuits with dining and event programming creates compound revenue opportunities, particularly in destination resorts where spa services achieve 40-60% profit margins. European operators leverage established thermal traditions to attract international wellness tourists, while Asian markets develop hybrid concepts combining traditional bathing rituals with modern sauna technology. This trend accelerates as hospitality groups recognize thermal wellness as a key differentiator in competitive markets, driving systematic investments in facility upgrades and staff training programs.

Rising Consumer Focus on Longevity, Sleep & Immunity Benefits

Clinical research demonstrating sauna therapy's impact on cardiovascular health, sleep quality, and immune function drives mainstream adoption beyond traditional relaxation benefits. Regular sauna use correlates with a 27% reduction in cardiovascular disease risk and improved sleep efficiency scores, creating medical validation that supports consumer investment decisions[2]Global Wellness Summit, “The Future of Wellness 2023,” globalwellnesssummit.com. . Healthcare providers increasingly recommend thermal therapy as an adjunct treatment for chronic conditions, legitimizing sauna purchases as medical expenses eligible for health savings account reimbursement. The longevity economy, valued at USD 27 trillion globally, positions thermal wellness as a preventive healthcare infrastructure rather than a luxury amenity. Consumer behaviour shifts from occasional spa visits to routine home-based thermal therapy, supported by wearable technology that tracks physiological responses and optimizes session parameters. This medicalization of thermal wellness expands addressable markets to include health-conscious consumers who previously viewed saunas as indulgent rather than therapeutic.

Expansion of Luxury Real-Estate Wellness Amenities

Wellness real estate grew from USD 225.2 billion in 2019 to USD 438.2 billion in 2023, with thermal amenities becoming standard features in luxury residential developments[3]Spa Business, “Wellness Real-Estate Market Booming,” spabusiness.com. . High-net-worth individuals prioritize home wellness infrastructure that eliminates dependency on commercial facilities, particularly following pandemic-driven preferences for private health amenities. Property developers integrate sauna installations as value-add features that command 8-12% price premiums and reduce time-to-sale by 15-20% in competitive markets. The trend extends beyond individual residences to multi-family developments, corporate campuses, and senior living communities that position thermal wellness as lifestyle differentiators. Smart home integration enables remote monitoring and energy optimization, addressing operational concerns that previously limited residential adoption. This residential expansion creates sustained demand for compact, energy-efficient units that maintain commercial-grade performance standards while meeting residential building codes and homeowner association requirements.

Technology-Enabled Infrared & Smart-Sauna Adoption

Smart sauna technology integration reaches 35% of new installations, driven by energy management capabilities that reduce operational costs by 20-30% compared to traditional systems. IoT connectivity enables predictive maintenance, remote diagnostics, and usage optimization that appeals to commercial operators managing multiple facilities and homeowners seeking convenience features. Infrared technology achieves faster heat-up times and lower energy consumption, addressing sustainability concerns while maintaining therapeutic benefits through targeted tissue heating. Mobile applications provide session customization, health tracking integration, and social sharing features that enhance user engagement and support routine usage patterns. The convergence of thermal therapy with digital health platforms creates data-driven wellness experiences that justify premium pricing and support subscription-based service models. Manufacturers differentiate through proprietary heating technologies, advanced materials, and seamless smart home ecosystem integration that positions saunas as connected health devices rather than passive amenities.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront capex & OPEX for commercial facilities | -0.8% | Global; acute in emerging markets | Short term (≤ 2 years) |

| Energy-cost volatility & sustainability scrutiny | -0.6% | Europe & North America; expanding globally | Medium term (2-4 years) |

| Retrofit compliance hurdles (HVAC / fire / ventilation codes) | -0.5% | North America & Europe; tightening in APAC | Medium term (2–4 years) |

| Shortage of skilled thermal-spa technicians | -0.4% | Global; especially critical in resort regions | Short to Medium term (1–3 years) |

| Source: Mordor Intelligence | |||

High Upfront Capex & OPEX for Commercial Facilities

Commercial sauna installations require a USD 15,000-50,000 initial investment plus ongoing energy costs averaging USD 2,000-8,000 annually, creating barriers for small operators and independent facilities. Installation complexity increases in retrofit applications where HVAC modifications, electrical upgrades, and structural reinforcements add 30-50% to base equipment costs[4]International Code Council, “Building Codes and Standards,” iccsafe.org.. Operating expenses include energy consumption, maintenance contracts, and specialized technician services that strain profit margins for facilities with limited utilization rates. Insurance and liability considerations add recurring costs, particularly for commercial operators serving diverse customer populations with varying health conditions. Small spa operators increasingly partner with equipment manufacturers offering lease-to-own financing and maintenance packages that reduce upfront barriers while ensuring operational support. This capital intensity favors established operators with access to commercial financing and creates consolidation pressure among independent facilities lacking scale economies.

Energy-Cost Volatility & Sustainability Scrutiny

Rising energy costs and environmental regulations increasingly influence facility design and operational decisions, with traditional saunas consuming 4.5-6 kW per session compared to 1.5-2 kW for infrared alternatives. Sustainability-focused consumers and corporate wellness programs prioritize energy-efficient solutions that demonstrate measurable environmental impact reductions. Regulatory frameworks in Europe and California mandate energy efficiency standards for commercial thermal facilities, requiring operators to invest in upgraded systems or face compliance penalties. Carbon footprint concerns drive demand for renewable energy integration, heat recovery systems, and smart controls that optimize energy consumption based on usage patterns. Operators respond by implementing solar heating systems, thermal storage solutions, and demand-response programs that reduce peak energy costs while maintaining service quality. This transition creates opportunities for technology providers offering integrated energy management solutions while challenging traditional manufacturers to develop more efficient heating systems.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Hotels Sustain Revenue While Homes Accelerate Growth

The hotel segment captured 35.78% of the sauna and spa market share in 2025, banking on premium room-rate uplifts and bundled wellness itineraries that encourage longer stays. Resorts leverage thermal circuits, cold plunges, and aromatherapy lounges to lift ancillary revenues per occupied room. Conversely, household installations are projected to post an 8.61% CAGR, underpinned by e-commerce availability, smart-home compatibility, and deferred tax benefits in certain countries. Corporate campuses and medical centers collectively form a mid-sized niche, where therapeutic protocols and employee-wellness KPIs justify the capital outlay.

Corporate wellness programs increasingly fund on-site thermal facilities as employee retention tools, with companies reporting 15-20% reduction in healthcare costs among regular sauna users. The International Swimming Pool and Spa Code provides standardized safety requirements that facilitate commercial installations while ensuring consistent operational standards across applications. Home installations benefit from simplified permitting processes and energy-efficient designs that reduce operational barriers, while commercial applications require specialized ventilation systems and accessibility compliance that increase complexity and costs.

By Type of Market: Renovation Gains Momentum Against New Construction

New construction projects dominated with 53.12% market share in 2025, benefiting from integrated design opportunities that optimize space utilization and energy systems from project inception. Renovation and replacement installations accelerate at 7.12% CAGR, driven by facility modernization needs and energy efficiency upgrades that reduce operational costs while improving user experiences. The renovation segment reflects market maturation where existing facilities upgrade aging equipment to meet contemporary performance and sustainability standards. New construction benefits from streamlined permitting and installation processes, while renovation projects face complexity from building code compliance and structural modifications.

Smart technology integration favors renovation projects where operators upgrade traditional systems with IoT connectivity and energy management features without complete facility reconstruction. Building codes increasingly mandate energy efficiency standards that drive renovation activity as operators comply with updated regulations. The renovation trend creates opportunities for modular systems and prefabricated components that simplify installation in existing structures while maintaining commercial-grade performance standards.

By Product Type: Infrared Innovation Challenges Traditional Dominance

Traditional Finnish saunas maintained 41.72% market share in 2025, supported by established consumer preferences and proven therapeutic benefits associated with high-temperature dry heat experiences. Infrared technology surges at 9.98% CAGR, driven by energy efficiency advantages, faster heat-up times, and lower installation complexity that appeals to residential and commercial operators. Steam and hybrid systems serve niche applications where humidity control and aromatherapy integration create differentiated experiences. Traditional saunas require 4.5 kW heating systems and 30-40 minute preheat times, while infrared alternatives operate on 1.5-2 kW systems with immediate usability.

The product type competition reflects broader market trends toward energy efficiency and convenience features that reduce operational barriers. Infrared technology enables compact installations suitable for residential applications where space and energy constraints limit traditional sauna viability. Hybrid systems combining traditional and infrared heating methods emerge as compromise solutions that provide temperature flexibility while maintaining authentic sauna experiences. Smart controls and mobile connectivity become standard features across product types, with manufacturers differentiating through proprietary heating technologies and integrated health monitoring capabilities.

Geography Analysis

Europe commands 31.88% market share in 2025, leveraging centuries-old thermal wellness traditions and supportive regulatory frameworks that facilitate commercial sauna operations. Nordic countries drive regional leadership through established sauna culture and government wellness initiatives, including Sweden's wellness allowance program that subsidizes employee thermal therapy expenses. The European market benefits from standardized building codes and safety regulations that streamline installation processes while ensuring consistent operational standards across member countries. Germany and Finland anchor regional manufacturing capabilities, with companies like KLAFS and Harvia maintaining global market positions through technological innovation and quality engineering.

Asia-Pacific emerges as the fastest-growing region at 9.05% CAGR through 2031, driven by rising disposable incomes and cultural integration of thermal wellness practices in hospitality and residential developments. Japan leads regional adoption through traditional onsen culture that translates to modern sauna acceptance, while China's expanding middle class creates substantial demand for luxury wellness amenities. The region's growth reflects urbanization trends where space-constrained environments favor compact infrared systems over traditional installations requiring larger footprints. South Korea and Singapore drive commercial adoption through corporate wellness programs and luxury hotel developments that position thermal amenities as competitive differentiators.

North America maintains steady growth through corporate wellness investments and luxury residential developments that integrate thermal amenities as standard features. The region's emphasis on energy efficiency and smart home technology drives demand for connected sauna systems with advanced monitoring and control capabilities. Middle East and Africa represent emerging opportunities where luxury hospitality developments and wellness tourism initiatives create demand for premium thermal installations. South America shows modest growth potential, primarily concentrated in Brazil's spa tourism sector and Argentina's thermal resort developments, though economic volatility limits large-scale commercial investments.

Competitive Landscape

The sauna and spa market is characterized by high fragmentation, with the top five players capturing only a small share of the overall market. This indicates a competitive landscape with low entry barriers, creating significant opportunities for regional specialists and tech-driven startups. The diversity of consumer preferences across price points, applications, and geographies makes large-scale consolidation challenging. Differentiated offerings ranging from personalized wellness experiences to eco-conscious designs and smart features have become key growth drivers. Market leaders like Harvia and KLAFS maintain their edge through vertical integration, brand recognition, and manufacturing efficiency, while smaller players thrive by focusing on niche applications and innovation.

Strategic trends in the market increasingly center on technology adoption, energy efficiency, and customizable solutions that cater to modern consumer expectations. Customers are demanding more sustainable operations and smart connectivity in their wellness experiences, prompting suppliers to invest in intelligent systems and digital platforms. There are white-space opportunities in areas such as modular retrofitting solutions, AI-enabled thermal circuits, and comprehensive wellness platforms that incorporate health monitoring alongside traditional thermal therapies. Emerging business models are shifting toward direct-to-consumer channels, flexible subscription services, and mobile spa concepts that allow for greater accessibility. These trends are redefining market dynamics and expanding the customer base beyond traditional spa installations.

Regulatory frameworks like the International Swimming Pool and Spa Code are helping level the playing field, ensuring smaller manufacturers can compete on safety and quality with established players. These standardized guidelines also support global market harmonization, fostering trust among consumers and commercial buyers alike. At the same time, the evolution of wellness as a lifestyle choice, rather than a luxury, is opening new avenues in hospitality, residential, and corporate wellness sectors. Smaller firms leveraging localized expertise and agile production processes are well-positioned to meet this demand. As the market continues to evolve, success will depend on balancing operational excellence with innovation and consumer-centric design.

Sauna And Spa Industry Leaders

Harvia Plc

KLAFS GmbH

Sauna360 Group Oy (TyloHelo)

Sunlighten Inc.

ThermaSol Steam Bath LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Kohler Co. completed the acquisition of KLAFS GmbH for undisclosed terms, combining Kohler's bathroom and kitchen expertise with KLAFS's premium sauna and spa room capabilities to create integrated wellness solutions for luxury residential and commercial markets.

- January 2025: Therme Group acquired Therme Erding for USD 345 million, reinforcing its strategy of developing large-scale urban thermal wellness centers. The move highlights the scalability of thermal wellness as public infrastructure, not just luxury. Therme Erding generates over EUR 100 (USD 117.9) million annually through a mix of spa, dining, and entertainment services.

- January 2025: Vagaro acquired Schedulicity to enhance business management services across spa, beauty, and fitness industries, creating comprehensive technology platforms that support facility operations, customer management, and payment processing for thermal wellness operators.

- December 2024: MySauna announced international expansion into North American markets with focus on mobile sauna services and pop-up installations that serve festivals, corporate events, and temporary wellness activations. The expansion reflects growing demand for experiential thermal wellness that extends beyond fixed facility models.

Global Sauna And Spa Market Report Scope

The report aims to provide a detailed analysis of the Suana and Spa market. It focuses on market dynamics, customer trends, and insights into geographical segments. Also, it analyzes the major players and the competitive landscape in the market. The Sauna and Spa Market is Segmented By Application into Hotel/Hospitality, Gym/Fitness and Spas, Household, Other Applications, by Type of Market into New, and Renovation/Replacement and by Geography into North America, Europe, Asia-Pacific, Latin America, Middle East & Africa. The report offers market size and forecast in value (USD billion) for all the above segments.

| Hotel / Hospitality |

| Gym / Fitness & Spas |

| Household |

| Other Applications |

| New |

| Renovation / Replacement |

| Traditional (Finnish) |

| Infrared |

| Steam / Hybrid |

| North America | Canada |

| United States | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South-East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines) | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Application | Hotel / Hospitality | |

| Gym / Fitness & Spas | ||

| Household | ||

| Other Applications | ||

| By Type of Market | New | |

| Renovation / Replacement | ||

| By Product Type | Traditional (Finnish) | |

| Infrared | ||

| Steam / Hybrid | ||

| By Geography | North America | Canada |

| United States | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South-East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines) | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the global sauna and spa market in 2026?

It stands at USD 155.63 billion, with value projected to reach USD 194.9 billion by 2031.

What CAGR is forecast for the sector through 2031?

The market is expected to expand at a steady 4.60% CAGR over the 2026-2031 horizon.

Which application captures the highest revenue?

Hotel and resort facilities hold the top slot, commanding 35.78% of 2025 revenue.

Which region will grow fastest by 2031?

Asia-Pacific is slated to post the strongest 9.05% CAGR, fueled by rising disposable income and robust hotel construction.

Why are infrared cabins gaining popularity?

They cut energy use by two-thirds, heat up faster, and integrate easily into smart-home ecosystems.

What is the main barrier for small commercial spa owners?

High upfront equipment costs and recurring energy bills often extend payback periods beyond five years.

Page last updated on: