Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

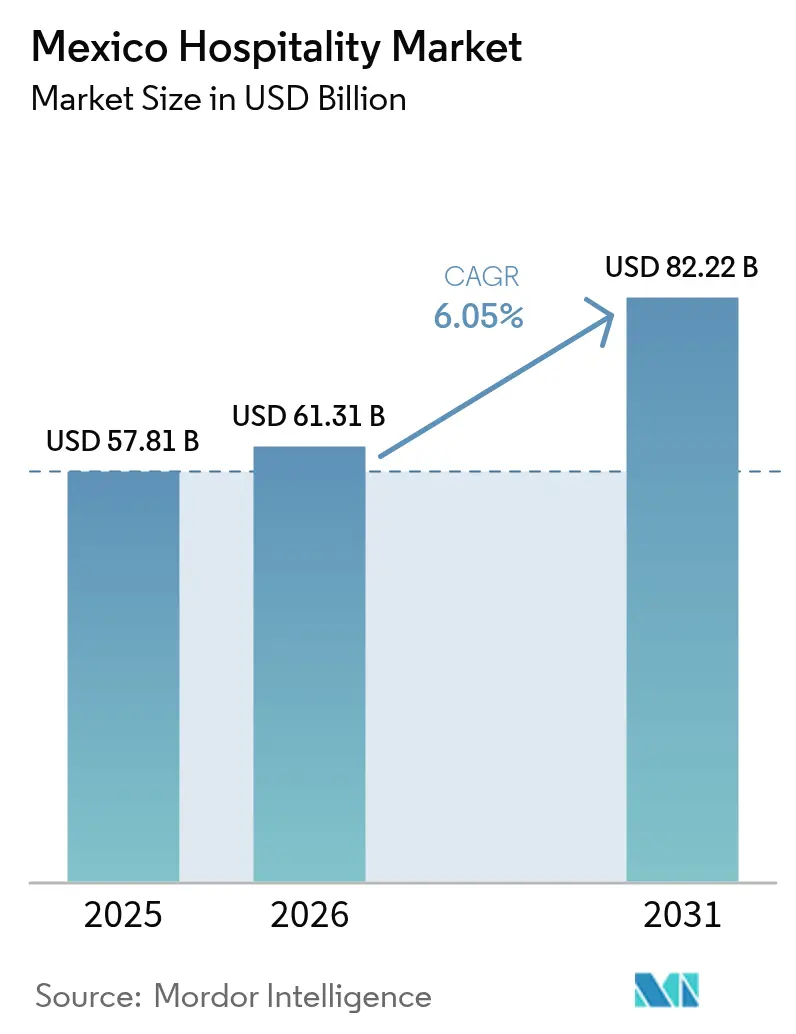

| Base Year Market Size (2025) | USD 57.81 Billion |

| Market Size (2026) | USD 61.31 Billion |

| Market Size (2031) | USD 82.22 Billion |

| Growth Rate (2026 - 2031) | 6.05% CAGR |

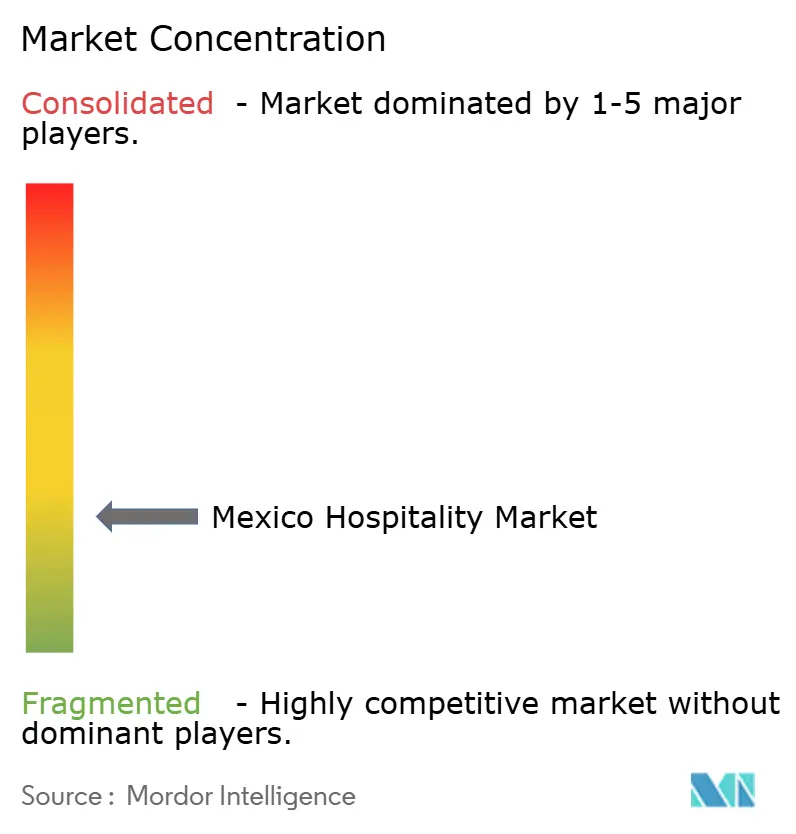

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Mexico Hospitality Market Analysis by Mordor Intelligence

The Mexico Hospitality Market size in 2026 is estimated at USD 61.31 billion, growing from 2025 value of USD 57.81 billion with 2031 projections showing USD 82.22 billion, growing at 6.05% CAGR over 2026-2031.

The forecast is backed by the sector’s robust rebound from the pandemic and its renewed strategic importance for regional tourism and business travel. Much of the current momentum is anchored in the dual influence of resurgent leisure demand and sustained corporate activity linked to nearshoring, a combination that diversifies revenue streams and lowers seasonality risk across the Mexico hospitality market. Macro forces reshaping the sector include Mexico's emergence as a nearshoring hub, with Nuevo León alone attracting USD 4 billion in foreign direct investment and creating 500,000 new jobs. This manufacturing boom extends beyond traditional industrial corridors into the Bajío region, generating sustained corporate travel demand. Simultaneously, the Maya Train's operational launch connects 34 stations across five states, fundamentally altering accessibility patterns to previously underserved archaeological and cultural sites.

Key Report Takeaways

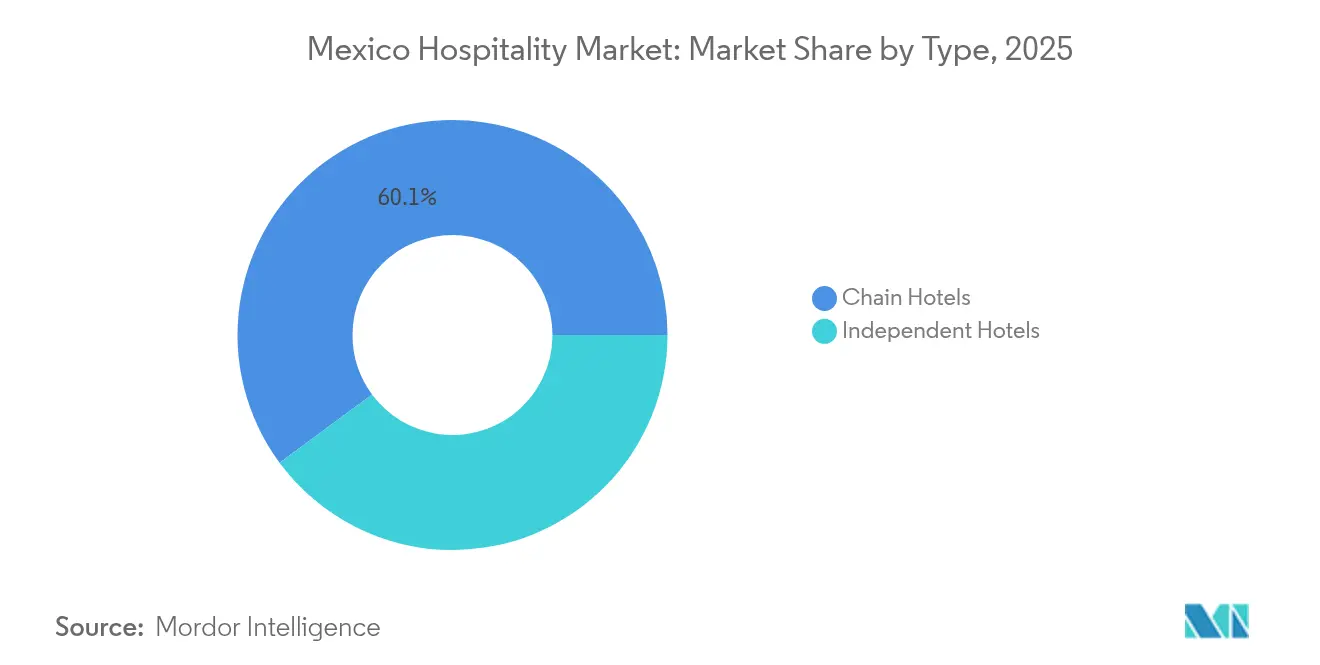

- By type, chain hotels led with 60.12% of the Mexico hospitality market share in 2025 and are forecast to advance at an 7.98% CAGR through 2031, comfortably outpacing independents.

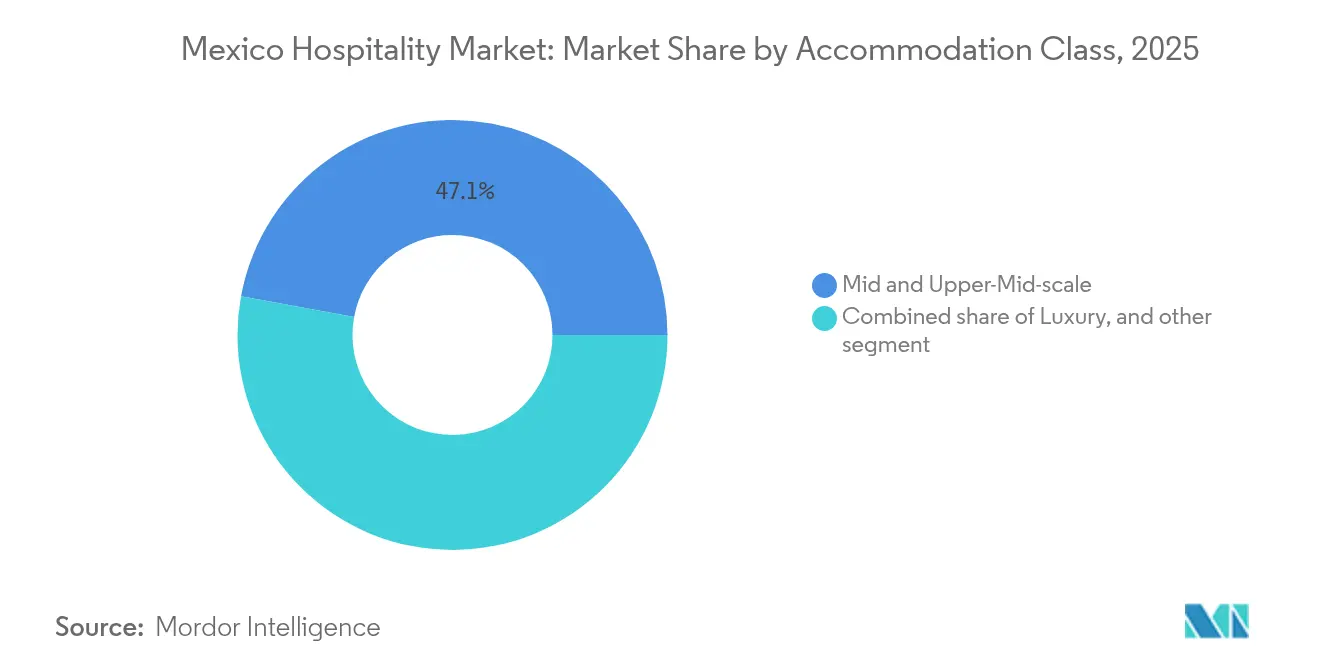

- By accommodation class, service apartments accounted for the quickest growth trajectory at a 9.44% CAGR from 2026 to 2031, while mid- and upper-mid-scale held 47.11% of of the Mexico hospitality market share in 2025 , demonstrating the segment’s broad appeal.

- By booking channel, OTAs captured 55.10% of of the Mexico hospitality market share in 2025, yet direct digital platforms are projected to rise at a 10.62% CAGR, closing the distribution gap by 2031.

- By geography, the Yucatán Peninsula and Caribbean maintained 28.40% of the Mexico hospitality market share in 2025; however, the Northwest posts the fastest expansion at 6.55% CAGR, driven by nearshoring-related travel.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Mexico Hospitality Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| United States Proximity Advantage Supporting Consistent Leisure Travel | 1.10% | Cancún, Los Cabos, border gateways | Short term (≤ 2 years) |

| All-Inclusive Resort Ecosystem Driving Coastal Hospitality Investment | 1.00% | Riviera Maya and Pacific resorts | Short term (≤ 2 years) |

| Nearshoring Activity Creating New Corporate Accommodation Demand | 0.80% | Northern and Bajío industrial corridors | Medium term (2–4 years) |

| Cruise Port Network Expanding Coastal Hospitality Opportunities | 0.60% | Major cruise port destinations | Medium term (2–4 years) |

| Medical and Wellness Tourism Creating Specialized Hospitality Demand | 0.70% | Monterrey, Guadalajara medical tourism hubs | Long term (≥ 4 years) |

| Cultural Heritage Routes Supporting Regional Destination Development | 0.50% | UNESCO heritage and Maya circuit | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

United States Proximity Advantage Supporting Consistent Leisure Travel

Mexico's proximity to the United States provides a structural advantage, generating consistent year-round cross-border leisure travel. The United States remains Mexico's largest international source market, supported by extensive air connectivity and short travel times. Rising visitor spending continues to strengthen hotel revenues across beach destinations. Canada further diversifies North American demand as visitor arrivals grow. Strong bilateral tourism supports stable occupancy and long-term hospitality investment[1]Secretaría de Turismo (SECTUR), "Results of International Visitors to Mexico 2025," DataTur, datatur.sectur.gob.mx.

All-Inclusive Resort Ecosystem Driving Coastal Hospitality Investment

Mexico's all-inclusive resort model continues to attract significant international hotel investment across the Riviera Maya, Cancún, and Los Cabos. Global brands, including Marriott, Hyatt, and Posadas, are expanding premium coastal resort portfolios. Beach destinations consistently outperform inland markets in occupancy and profitability. Strong foreign investment reflects investor confidence in Mexico's leisure tourism sector. The all-inclusive segment remains the country's primary driver of hospitality growth.

Nearshoring Activity Creating New Corporate Accommodation Demand

Mexico's position as a leading nearshoring destination is increasing demand for corporate hotels and extended-stay accommodation. Manufacturing hubs such as Monterrey, Querétaro, Tijuana, and Ciudad Juárez are attracting multinational investments. Engineers, consultants, and business travelers are driving year-round hotel occupancy. Hospitality developers are expanding executive hotels and serviced apartments near industrial corridors. Nearshoring is diversifying Mexico's hospitality demand beyond leisure tourism[2]Secretaría de Economía, "Nearshoring Opportunities and Foreign Direct Investment in Mexico," Government of Mexico, gob.mx/se.

Cruise Port Network Expanding Coastal Hospitality Opportunities

Mexico's expanding cruise industry is generating new hospitality opportunities across major coastal destinations. Ports including Cozumel, Progreso, Mazatlán, and Ensenada continue recording strong passenger growth. Cruise tourism stimulates hotel stays, retail spending, and the development of destination infrastructure. New port investments are enhancing tourism ecosystems beyond cruise terminals. Growing cruise traffic supports hotel investment across secondary coastal markets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Security Concerns Influence Destination Perception and Tourism Investment Decisions | −0.9% | Guerrero, Sinaloa, high-risk regions | Short term (≤ 2 years) |

| Overdependence on Major Coastal Tourism Destinations Creates Concentration Risk | −0.7% | Quintana Roo and Los Cabos dependence | Medium term (2–4 years) |

| Exposure to North American Travel Cycle Fluctuations | −0.8% | Cancún and Los Cabos demand | Short term (≤ 2 years) |

| Infrastructure and Connectivity Gaps Limit Expansion Into Emerging Tourism Regions | −0.6% | Southern ecotourism connectivity gaps | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Security Concerns Influence Destination Perception and Tourism Investment Decisions

Security concerns remain a significant challenge for Mexico's hospitality industry. Crime perceptions increase operating costs, insurance expenses, and investment risks for hotel developers. Negative international media coverage can influence destination choice despite strong tourism demand. Some resort regions continue investing heavily in tourism security and visitor protection. Perception management remains critical for sustaining long-term hospitality growth[3]Instituto Nacional de Estadística y Geografía (INEGI), "Encuesta Nacional de Seguridad Pública Urbana (ENSU) 2025," INEGI, inegi.org.mx.

Overdependence on Major Coastal Tourism Destinations Creates Concentration Risk

Mexico's hospitality investment remains heavily concentrated in Cancún, Riviera Maya, and Los Cabos. Interior destinations continue attracting significantly lower occupancy and investment levels. Heavy reliance on coastal markets increases exposure to hurricanes, environmental disruptions, and localized demand shocks. Continued resort development may intensify competition and pricing pressure in established destinations. Geographic diversification remains essential for sustainable market growth[4]Secretaría de Infraestructura, Comunicaciones y Transportes (SICT), "National Infrastructure Program for Tourism Connectivity," Government of Mexico, gob.mx/sct.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Branded Properties Accelerate Market Consolidation

Chain hotels held 60.12% of value in 2025 and are projected to grow at 7.98% CAGR, ensuring their slice of the Mexico hospitality market size widens as foreign brands court both leisure and corporate demand. Their expansion strategy leans heavily on conversions, leveraging capital-light management agreements to secure inventory quickly and sidestep permitting delays. Loyalty ecosystems funnel international guests into Mexican resorts, lifting shoulder-season occupancy and smoothing revenue. Independent operators, by contrast, confront escalating technology investment requirements, digital check-in, omnichannel distribution, and AI-driven revenue management that erode margins without scale. Many independents now explore soft-brand affiliations to retain ownership yet gain platform advantages. Bank lenders perceive branded assets as lower risk, granting preferential financing terms that further tilt the playing field. As consolidation advances, the Mexico hospitality market share held by branded operators should climb beyond 65.10% within five years, narrowing the scope for pure independents but expanding opportunities for joint-venture asset management specialists.

The migration toward branding also reshapes labor markets, as international chains import standardized training programs that lift service consistency and talent mobility across regions. Corporate travel managers increasingly stipulate brand-level safety protocols and loyalty benefits as prerequisites for preferred hotel status, steering RFP volume toward chains. On the cost side, central procurement and global distribution agreements compress per-unit expenses below what stand-alone hotels can secure. Technology partnerships with big-tech providers offer experimental capabilities predictive maintenance, digital concierge that smaller entities cannot feasibly pilot.

By Accommodation Class: Mid-Scale Dominance Reflects Accessibility Strategy

Mid- and upper-mid-scale hotels commanded 47.11% of the 2025 market value, a testament to Mexico’s equilibrium between affordability and elevated service that broadens audience reach across leisure and corporate segments. Average length of stay for this cohort sits at four nights, higher than luxury’s three-night norm, buoying total revenue per available room. Service apartments, while representing a smaller base, post a 9.44% CAGR and are on track to gain an outsized chunk of the Mexico hospitality market size by 2031 as companies prefer cost-effective monthly rates for project teams. Luxury stock, concentrated in coastal enclaves, aims to raise rate ceilings through experiential positioning such as culinary workshops and indigenous wellness rituals, strategies that partially insulate ADR from macro shocks. Budget hotels confront rising energy and staffing costs, compressing margins unless offset by franchised efficiency models.

Developers weighing class allocation increasingly factor in environmental regulations that heighten capex for beach-front luxury projects due to water scarcity and wastewater mandates under NOM 001 SEMARNAT 2021. Conversely, mid-scale inland assets enjoy lower compliance overheads and quicker breakeven timelines. Consumer-perception surveys indicate travelers assign higher value to free high-speed internet and co-working space than to high-thread-count linens, signaling sustained appetite for upgraded mid-scale attributes.

By Booking Channel: Direct Digital Gains Challenge OTA Dominance

OTAs held 55.10% of 2025 booking value, yet the direct digital pathway climbs at 10.62% CAGR, propelled by hotels sweetening loyalty discounts and deploying AI-led personalization to uplift conversion rates. OTA commission rates averaging 18-25% incentivize properties to re-route demand, a margin recapture that directly elevates EBITDA. Mobile-first redesigns, one-click payment, and upsell widgets increase direct-channel revenue per booking by 12% year-on-year. Corporate and MICE segments maintain negotiated contracts, supplying a steady pipeline outside transient leisure streams. Wholesale and traditional agents persist for group allotments and long-haul markets but their share slides annually. Rate-parity enforcement narrows price differentials, making loyalty perks the swing factor for digital consumers. In parallel, metasearch engines funnel price-conscious travelers toward brand sites as cost-per-click bidding turns prohibitive for OTAs, accelerating the rebalancing of distribution economics within the Mexico hospitality market.

Channel shift brings data-ownership dividends: properties leverage first-party data to orchestrate post-stay marketing and dynamic packaging of spa or excursion add-ons, boosting total spend per guest. Robust customer-data platforms feed predictive analytics that refine promotional cadence, delivering incremental uplift in repeat visitation. Over time, the narrowing dominance of OTAs should translate into significantly healthier profit margins for operators across the Mexico hospitality market size spectrum, provided they maintain tech investment and loyalty innovation momentum.

Geography Analysis

The Yucatán Peninsula and Caribbean dominant the market share with 28.40% market share, yet water-scarcity mandates and strict environmental compliance increase development barriers, nudging investors toward adaptive reuse and eco-certified upgrades rather than greenfield luxury builds. Maya Train connectivity is elongating visitor itineraries from single-resort stays to multi-stop cultural loops that funnel revenue deeper into inland towns. Hoteliers respond with hub-and-spoke packages that combine beach stays with heritage excursions, raising total spend per guest. Hurricane preparedness, guided by the Hydrometeorological Operational Committee, reduces risk premiums, but insurers still factor storm exposure into policy pricing, elevating operating costs that shape ADR strategies.

The Northwest’s 6.55% CAGR owes much to industrial corridors attracting U.S. manufacturing partners who embed travel patterns into project lifecycles, thus supplying predictable midweek demand. Border infrastructure modernization shortens transit times, fuelling weekend leisure traffic from California and Arizona that complements corporate volume. Sonora’s state incentives for hotel construction in Free Trade Zones expedite approvals, allowing branded limited-service hotels to open within 24 months, a timeline that sharpens IRR in comparison with coastal resorts. Multimodal cargo hubs spur ancillary service demand conference centers, catering, transport that widens non-room revenue channels, augmenting the Mexico hospitality market size in an area historically underpenetrated by international brands.

Regulatory Landscape

Mexico's hospitality sector operates under the Ley General de Turismo and its implementing regulation, with oversight led by the Secretaria de Turismo (SECTUR). Reforms published in the Diario Oficial de la Federacion in November 2025 updated the Ley General de Turismo (14 Nov 2025) and introduced changes to the Reglamento de la Ley General de Turismo (25 Nov 2025), including provisions tied to hotel classification and administration of the Registro Nacional de Turismo (RNT). This increases the importance of standardized registration and classification compliance for operators.

Policy direction is also framed by the Programa Sectorial de Turismo (PROSECTUR 2025-2030), published in September 2025, which sets federal priorities around investment attraction, regional development, and sustainability. On environmental compliance, PROFEPA monitors applicable obligations and runs the voluntary Programa Nacional de Auditoria Ambiental (PNAA), issuing the Certificado de Calidad Ambiental Turistica. SECTUR and PROFEPA also recognize higher-performing operators through the Distintivo S, which has become a visible benchmark in destination marketing and procurement decisions for tourism services.

Value Chain Analysis

Mexico's hospitality value chain starts with planning and enabling institutions (SECTUR, FONATUR, state tourism boards, and municipal authorities), then moves through developers, contractors, and equipment suppliers for new-builds and conversions. The chain continues with operators managing rooms, food and beverage, leisure services, and staffing. Distribution is increasingly technology-led, spanning brand websites and apps, loyalty platforms, OTAs, metasearch, and corporate/MICE intermediaries, while transport linkages (airports and the Maya Train corridor) shape catchment areas and seasonality by redirecting flows toward new nodes.

Operational inputs and procurement remain a key friction point, as hotels import a large share of consumables (about 75%), increasing exposure to FX, lead times, and cross-border logistics performance. Recent coordination between FONATUR and BBVA Mexico around land-use diagnostics and project identification also points to a more data-driven approach to de-risking tourism investments and related supply chains. Multimodal integrations, such as Tren Maya ticketing availability on the global Flix platform, further tighten the connection between mobility and lodging demand. As a result, local supplier development, centralized procurement, and digital channel capabilities matter for both chain and independent operators.

Competitive Landscape

The hospitality market in Mexico is highly fragmented, with the top five operators holding only a limited share of total hotel inventory. This fragmentation creates space for emerging brands and niche operators to expand their footprint. A leading domestic player benefits from strong brand loyalty and flexible franchise models that align well with local ownership preferences. Meanwhile, major international groups maintain a solid presence by leveraging global recognition and well-established loyalty programs to attract both domestic and international travelers. The landscape remains competitive but open, offering significant potential for both consolidation and innovation.

Technology has become a major differentiator across the sector, as larger chains increase investments in AI-driven revenue management systems, digital keys, and contactless services. These advancements create a growing capabilities gap between global operators and independent hotels. Many brands are adopting conversion-led strategies to reduce capital expenditures and accelerate market entry, a compelling approach in light of rising interest rates and regulatory challenges. Growth opportunities are particularly strong in extended-stay and serviced apartment formats, especially in underpenetrated secondary cities attracting foreign direct investment. In these markets, asset-light models and local development partnerships are proving especially effective.

New market entrants and disruptors are also shaping the competitive dynamics. Budget-oriented chains are expanding rapidly across dozens of cities through standardized, scalable models, while lifestyle brands appeal to digital nomads by combining co-living and co-working environments. Ancillary revenue streams are becoming increasingly important, with urban hotels transforming rooftops and common spaces into revenue-generating dining and event venues. These initiatives help diversify income beyond room rates, enhancing asset performance. Overall, Mexico’s hospitality sector is evolving into a more dynamic, tech-driven, and opportunity-rich environment where adaptability and innovation are key to success.

Mexico Hospitality Industry Leaders

-

Grupo Posadas

-

Marriott International

-

Hilton Worldwide

-

Grupo Real Turismo

-

AccorHotels

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Opportunities are shaped by Mexico's formal policy push to broaden demand sources, modernize governance, and channel capital into a larger project pipeline. SECTUR's Ventanilla de Tramites de Turismo, launched in April 2026 with the Agencia de Transformacion Digital y Telecomunicaciones, creates room for hotels and smaller operators to standardize registration and operational processes digitally, supporting faster onboarding of new supply and formalization of smaller accommodation providers. PROSECTUR 2025-2030 also anchors public programs around sustainable and community-based tourism, creating differentiation for operators that can document compliance and point to recognized environmental practices, including PROFEPA's Certificado de Calidad Ambiental Turistica and the SECTUR-PROFEPA Distintivo S.

Investment and promotion initiatives add additional evidence-backed growth pathways. In April 2026, SECTUR presented a USD 42 billion tourism investment pipeline covering 773 projects, with roughly 60% focused on hotel or residential infrastructure. This supports expansion beyond legacy coastal hubs into emerging states and corridors that benefit from transport upgrades. On demand creation, SECTUR launched a five-pillar national tourism promotion strategy in July 2026 to diversify outreach beyond North America toward Europe, South America, and Asia, which rewards operators that tailor product, language, and distribution to new origin markets while also capturing extended-stay and serviced-apartment demand tied to remote work and project-based corporate travel.

Recent Industry Developments

- July 2026: Hilton partnered with Fuerte Group Hotels to debut the Amare Cancun Adults Only All-Inclusive Resort as a Curio by Hilton property, with an opening date set for Oct 31, 2026. The addition brings branded, conversion-led supply into a core leisure corridor and strengthens Hilton's position in Mexico's all-inclusive and adults-only segment.

- June 2026: Marriott officially inaugurated the St. Regis Costa Mujeres in Quintana Roo, a 213-room luxury resort developed with AB Living and reported at around USD 250 million investment. The opening increases top-end inventory in the Mexican Caribbean and reinforces luxury-led destination development in Costa Mujeres.

- April 2026: Grupo Posadas announced five new hotel and resort openings during Tianguis Turistico 2026, including Izla by Fiesta Americana, Live Aqua Centro Historico Ciudad de Mexico, and Grand Fiesta Americana Riviera Maya. The pipeline reflects continued domestic-brand expansion across both urban and resort demand centers, supporting Posadas' push to balance premium offerings with broader segment coverage.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenue generated from paid lodging stays and closely linked guest services across Mexico, supported by leisure and business travel flows. The sizing is anchored to accommodation activity sold through direct and intermediary channels, then converted to USD using a consistent year-average FX approach.

Scope exclusions: Excludes passenger air travel, attractions and tours, and standalone restaurant and bar spending that is not bundled with an accommodation stay.

Segmentation Overview

-

By Type

- Chain Hotels

- Independent Hotels

-

By Accommodation Class

- Luxury

- Mid & Upper-Mid-scale

- Budget & Economy

- Service Apartments

-

By Booking Channel

- Direct Digital

- OTAs

- Corporate / MICE

- Wholesale & Traditional Agents

-

By Geographic Region

- Northwest

- Northern Border

- Central

- Mexico City Metro

- Bajío-Pacific Coast

- Southern

- Yucatán Peninsula & Caribbean

Data Sources, Market Sizing, and Validation

Desk Research

Desk research started with public baselines that can be checked and repeated, and we used them to set the demand pool and operating context in Mexico. Sources that helped here include Mexico tourism statistics (such as the national tourism ministry), national statistics and price indices (such as INEGI), central bank series on FX and macro activity, and immigration or border-crossing releases where available. We also reviewed airport and port traffic dashboards and public hotel inventory notes from industry groups to understand how supply has moved across major tourism corridors.

For the business side, company filings, investor decks, and earnings call transcripts were used to translate operating indicators into revenue expectations. News and financials subscriptions were used to track openings, refurbishments, and brand activity, and an import/export shipment-level database was used selectively to sanity-check renovation cycles through furnishings and equipment movements. The sources listed above are illustrative only, and many other public documents and datasets were also referred to for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary interviews were used to pressure-test the desk assumptions, especially where public data is delayed or reported in mixed formats. We spoke with operators, owners, asset managers, travel intermediaries, and advisors to validate occupancy patterns, ADR movements, channel mix, and the role of corporate and group demand across key Mexican regions. Where the story did not align with the model, we revisited the relevant inputs and then rechecked the revised numbers with a smaller set of respondents.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 12% | |

| Mid tier: 55% | Functional/Unit leaders: 34% | |

| Smaller Players: 18% | Managers: 54% |

Market-Sizing & Forecasting

Sizing was built using top-down and bottom-up logic, with the backbone coming from a top-down reconstruction of lodging revenue using travel demand and hotel operating metrics. The model starts by aligning room supply and active inventory with observed travel inflows, then converts expected stay activity into revenue using ADR and occupancy. Those outputs are adjusted for seasonality and the destination-region mix.

To keep totals realistic, we corroborated the results with selective bottom-up checks, such as sampled property revenue reviews, rate card comparisons by class, and channel checks for intermediary commissions. Model inputs include hotel supply growth and openings, occupancy and ADR trends by destination cluster, mix shifts between chain and independent properties, the split of direct digital versus OTA bookings, and the share of corporate and MICE stays in major metros. For forecasting, we ran scenarios around tourism arrivals, domestic travel resilience, and pricing power, and selected the final path based on what operators and intermediaries described as achievable under the base case. Where bottom-up evidence was thin in smaller destinations, we filled gaps with conservative ranges anchored to comparable regions, then revalidated through follow-up calls.

Data Validation & Update Cycle

Model outputs were cross-checked against independent signals, including tourism arrival series, hotel inventory movement, and broad price and FX trends, to keep the result consistent with on-the-ground conditions in Mexico. If any variance looked too large, we traced it back to occupancy, ADR, or channel mix assumptions and recalibrated the relevant inputs before sign-off.

A second analyst review is completed to confirm calculations, year alignment, and currency conversions, and then the narrative is checked to ensure it matches the numbers. The report is refreshed annually, and interim updates are triggered when material events occur, such as sharp FX swings, major supply additions, or policy changes affecting travel. Before delivery, we do a final data pass so clients receive the latest updated view.

Mordor Intelligence's Mexico Hospitality Market Size Compared Against Other Published Estimates

Published market sizes for Mexico hospitality can look far apart, even when they are trying to describe the same industry. This usually happens because counted revenue streams are not identical, the base year differs, and the way pricing is converted into USD can change results.

Standalone restaurants and bars that are not part of an accommodation bill sit outside Mordor Intelligence's scope here, which is one reason the value does not match figures that merge all foodservice into hospitality. Another driver is how each publisher treats service apartments and all-inclusive properties, where some count them fully as lodging and others split out parts of the spend into leisure services. Differences also come from whether the estimate leans on hotel operating metrics (occupancy and ADR) versus broad macro proxies, and from how frequently assumptions are refreshed when travel conditions change quickly.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 57.81 B (2025) | |

| Regional Consultancy A | USD 26.00 B (2024) | Uses a narrower base that appears closer to lodging-only revenues and may undercount chain-to-independent spillover in secondary destinations. The definition also blends years (2024 base with later-period CAGR), which can compress the starting value versus a 2025-aligned model. |

| Industry Publisher B | USD 28.40 B (2024) | Folds accommodation, food and beverage, and tourism-related services into one umbrella, yet the reported value is still closer to an accommodation-led view. Limited clarity on how ADR inflation, FX conversion timing, and channel commission treatment are applied can shift the USD total materially. |

Taken together, the spread is mainly explained by what is counted as in-stay lodging revenue versus broader visitor spend, and by how pricing and channel effects are translated into USD. Our approach keeps the estimate traceable to room supply, occupancy, ADR, and channel mix, which makes the final number easier to reconcile and update when conditions change.

Key Questions Answered in the Report

What is the projected value of the Mexico hospitality market in 2031?

Forecasts indicate the sector will reach USD 82.22 billion by 2031, driven by a 6.05% CAGR rooted in diversified leisure and business demand

How large is the service-apartment opportunity in Mexico?

Service apartments are expanding at a 9.44% CAGR and increasingly capture long-stay digital nomads and project teams, making them the fastest-growing accommodation format.

Which region is expected to grow quickest between 2026 and 2031?

The Northwest, propelled by nearshoring facilities and cross-border traffic, posts the fastest regional CAGR at 6.55%.

Why are hotel chains focusing on conversion projects?

Conversions enable faster market entry, lower capex, and quicker revenue stabilization compared with ground-up development amid rising construction costs.

Page last updated on: