Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 8.44 Billion |

| Market Size (2026) | USD 8.9 Billion |

| Market Size (2031) | USD 11.59 Billion |

| Growth Rate (2026 - 2031) | 5.44% CAGR |

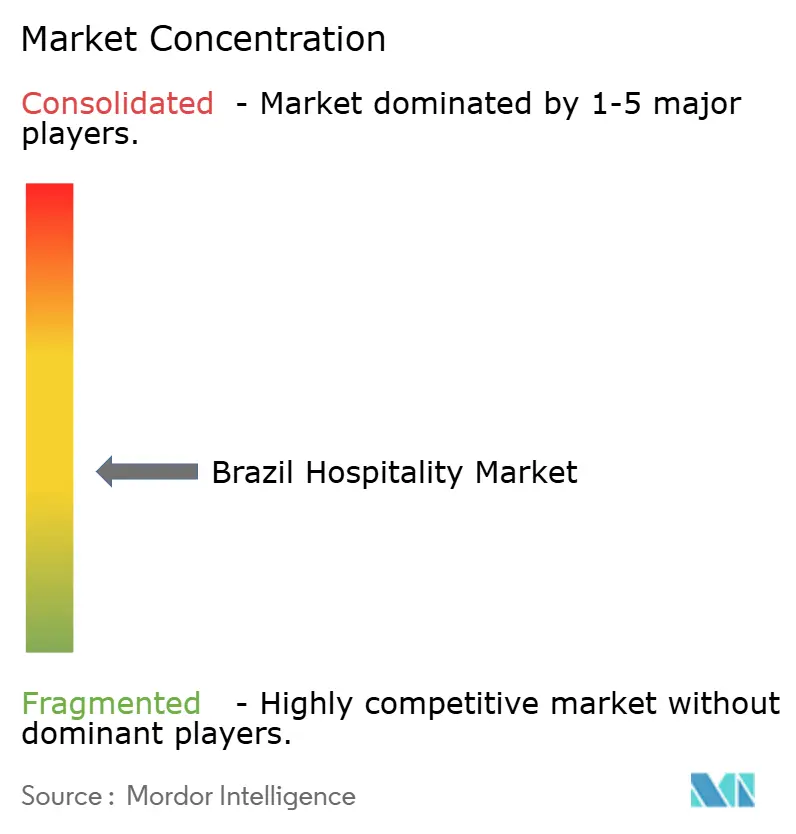

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brazil Hospitality Market Analysis by Mordor Intelligence

Brazil Hospitality Market size in 2026 is estimated at USD 8.9 billion, growing from 2025 value of USD 8.44 billion with 2031 projections showing USD 11.59 billion, growing at 5.44% CAGR over 2026-2031.

Rising domestic disposable income, accelerated PIX adoption, and pre-COP-30 infrastructure spending are creating a virtuous demand cycle that keeps room revenue on an upward trajectory. Chain operators are capitalizing on franchise conversions and loyalty-program scale, while independent players leverage local character to attract high-spending leisure guests. Direct digital channels continue to erode intermediary dependency, and the pipeline of new rooms remains well-balanced relative to expected arrivals, ensuring disciplined rate growth. Persistent airport slot limits and service-tax complexity weigh on profitability, yet sustained capital inflows from both foreign and local investors signal confidence in the long-term fundamentals of the Brazil hospitality market.

Key Report Takeaways

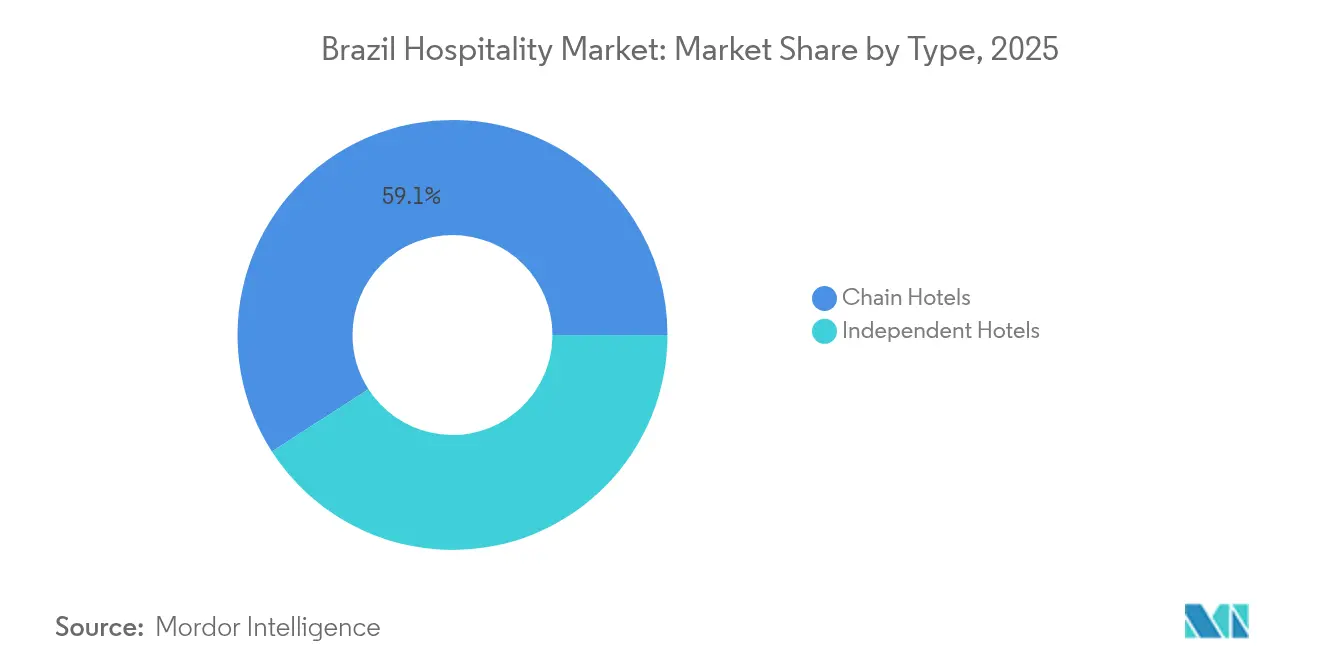

- By type, chain hotels captured 59.12% of the Brazil hospitality market share in 2025, and they are also projected to remain the fastest-growing sub-segment with a 7.29% CAGR from 2026 to 2031.

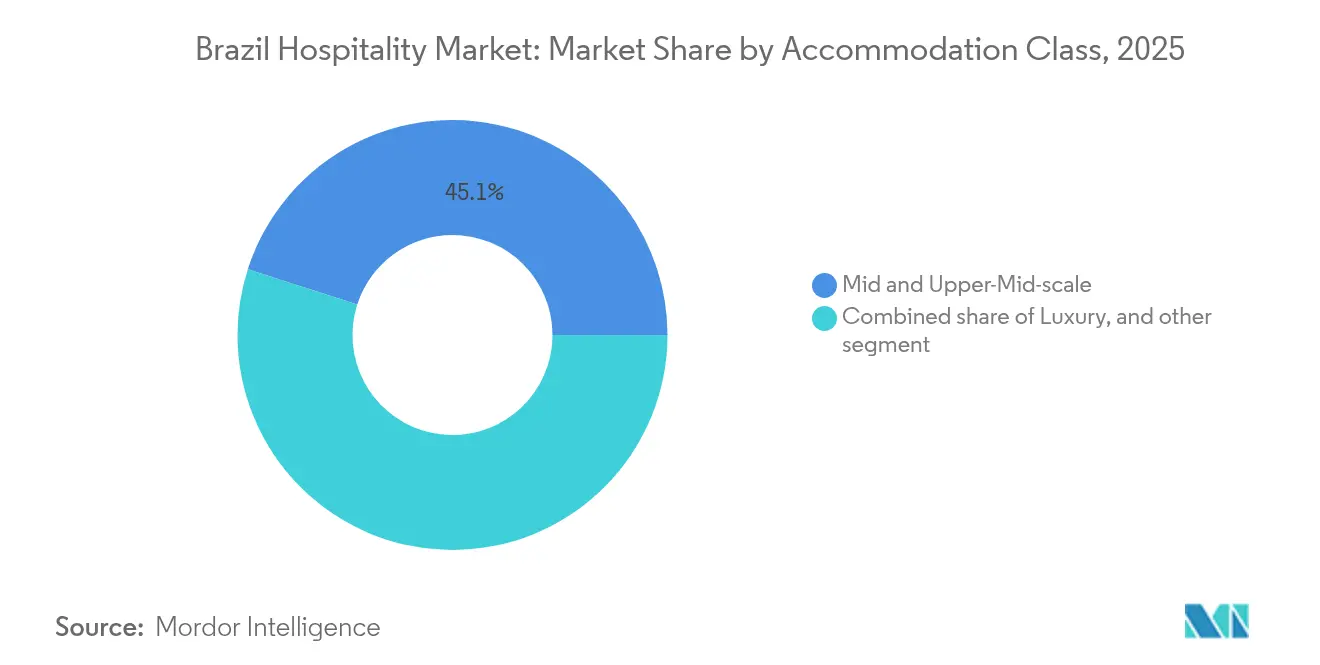

- By accommodation class, mid and upper-mid-scale properties accounted for 45.05% of the Brazil hospitality market share in 2025, while service apartments are expected to lead growth with the highest CAGR of 11.05% over 2026–2031.

- By booking channel, OTAs represented 42.60% of the Brazil hospitality market size in 2025, but direct digital channels are forecasted to expand the fastest with a 13.48% CAGR during 2026–2031.

- By geographic region, Southeast Brazil contributed 54.75% of the Brazil hospitality market share in 2025, whereas the North region is anticipated to register the fastest growth at 7.24% CAGR in the 2026–2031 period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Brazil Hospitality Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Post-Covid inbound surge from Chile, Argentina & USA | +1.2% | Southeast, South | Short term (≤ 2 years) |

| Domestic leisure boom tied to PIX instant-payment adoption | +0.9% | National | Medium term (2-4 years) |

| RevPAR lift from large-scale events | +0.7% | Southeast, North | Short term (≤ 2 years) |

| Expansion of low-cost regional airlines | +0.6% | North, Northeast, Central-West | Medium term (2-4 years) |

| Lula’s green-credit line for eco-lodges | +0.4% | Amazon, Pantanal | Long term (≥ 4 years) |

| Second-home hotelisation in northeast beach towns | +0.3% | Northeast | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Post-Covid inbound surge from Chile, Argentina & USA

International arrivals eclipsed pre-pandemic peaks in 2024 as Argentina, Chile, and the USA accelerated outbound travel to Brazil, propelling Rio de Janeiro and São Paulo to eight-year RevPAR highs during Carnival 2025. LATAM Airlines expanded trans-Atlantic capacity by 36%, signaling durable demand from the Spain and Portugal corridors[1]Aviation Direct, “LATAM Airlines Expands Long-Haul Service,” aviation. direct. . November 2024 saw 2.1 million international passengers, a 14% jump versus 2023, and average visitor spend reached USD 2,177, the world’s seventh-highest. The favorable BRL exchange rate made Brazil comparatively inexpensive, redirecting Brazil travelers toward domestic destinations and reinforcing hotel occupancy uplift in gateway cities. Hotels leveraged loyalty promotions and bundled event packages to capture incremental demand around mega-events, boosting ADRs well beyond 2019 benchmarks. Industry stakeholders anticipate sustained momentum as airlift rebuilds and visa policies streamline group-travel facilitation.

Domestic leisure boom tied to PIX instant-payment adoption

PIX processed over BRL 1 trillion (USD 200 billion) monthly transactions in 2024 and attracted 170 million unique users, democratizing online travel booking and triggering spontaneous weekend getaways. Hotels integrating PIX at checkout reported 16% revenue gains and 25% customer-base growth, underscoring the linkage between instant settlement and booking conversion rates. Financial inclusion enabled first-time travelers from lower-income brackets to access dynamic pricing, expanding shoulder-period demand. Cross-border PIX pilots with Paraguay and Argentina further enlarged Brazil’s regional tourism catchment, as 236,320 Paraguayan visitors used PIX in 2024 alone. By 2025 PIX is on track to represent 44% of domestic digital commerce, surpassing credit cards for the first time. Hospitality operators are refining revenue-management algorithms to reflect PIX-driven booking velocity and micro-segmented stay patterns that prioritize two-night breaks in secondary markets[2]Agencia Gov, “Hotel Sector Investment to Reach R$ 8.4 Billion,” agenciagov.ebc.com.br.

RevPAR lift from large-scale events (Rock in Rio, COP-30)

Mega-events consistently drive occupancy and average daily rate (ADR) far above seasonal norms. Rock in Rio 2024 pushed Rio’s ADR to approximately USD 181.44, marking a 35.5% year-over-year increase, while the G20 summit elevated ADR above USD 232, with peak rates nearing USD 560. COP-30 is prompting Belém to more than double its room supply to 50,000 beds, with projected ADR approaching USD 500. The federal government has allocated about USD 44.8 million for the development of a 500-room leaders’ village, underscoring the synergy between event-driven demand and infrastructure investment. Long-term benefits include improved urban mobility, strengthened public security, and extensive international exposure through destination marketing—effects that endure well beyond the event timelines. To maximize revenue during these high-compression periods, operators are launching pop-up F&B concepts and premium experiential packages, resulting in significant RevPAR spikes that substantially boost annual profitability.

Expansion of low-cost regional airlines

LATAM’s addition of 2,000 monthly domestic flights and GOL’s new Belém–Miami service are examples of network growth that activate latent hotel demand in tier-2 and tier-3 markets. Twenty-six new aircraft scheduled for Brazilian deployment equate to 13% fleet growth, opening point-to-point connections between secondary hubs and Guarulhos. Parallel USD 250 million investments in Guarulhos’ new passenger pier boost runway capacity and operational resilience during peak traffic. Enhanced connectivity reduces travel time and cost for leisure and corporate guests alike, encouraging developers to consider mid-scale hotels in agribusiness corridors. Hotel pipelines in Goiania, Cuiabá, and Manaus illustrate how aviation liberalization is recalibrating geographic revenue distribution across the Brazil hospitality market.

Lula’s green-credit line for eco-lodges

The federal green-credit scheme subsidizes sustainability-certified lodge developments in the Amazon and Pantanal, lowering borrowing costs by up to 300 basis points compared with commercial rates. Investors leverage these incentives to retrofit existing jungle lodges with solar arrays and wastewater recycling, enhancing operating margins and eligibility for global tour operator partnerships. Demand for low-impact travel experiences aligns with post-pandemic consumer preferences toward wellness and nature, allowing operators to command ADR premiums while diversifying Brazil’s tourism portfolio. The program also stimulates local supply chains through timber certification and indigenous community engagement, creating shared value that resonates with ESG-focused asset managers. The long-term timeline indicates a gradual but steady contribution to national occupancy growth.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chronic airport slot constraints at Congonhas & Santos-Dumont | -0.8% | Southeast | Medium term (2-4 years) |

| Persistent double-digit service-tax burden (ISS + ICMS) | -1.1% | National | Long term (≥ 4 years) |

| Elevated real-estate costs in prime Southeast markets | -0.5% | São Paulo Faria Lima and Rio Zona Sul | Medium term (2-4 years) |

| High OTA commission structures eroding independent-hotel margins | -0.4% | Nationwide, acute for leisure destinations | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Chronic airport slot constraints at Congonhas & Santos-Dumont

Slot caps at Santos-Dumont restrict annual throughput to 6.5 million passengers, distancing corporate travelers from central Rio and deflecting traffic to Galeão, whose financial viability depends on hitting 25 million travelers yet remains below 9 million[3]G1, “Government Studies More Flights for Santos Dumont,” g1.globo.com. . Congonhas expansion debates mirror Rio’s gridlock as Aena’s redevelopment plan fails to unlock substantial additional slots before 2027. Limited peak-hour frequencies push business clients toward higher-fare windows or alternative transport, compressing weekday occupancy in premium hotels located near financial districts. Hotel investors are delaying upgrades to meeting-space inventory pending clarity on slot policy, slowing capex cycles that would otherwise enhance Brazil's hospitality market competitiveness. Airlines advocate for slot reallocation mechanisms, but municipal opposition tied to noise-abatement weighs on policy change probability.

Persistent double-digit service-tax burden (ISS + ICMS)

Cumulative tax takes often exceed 20% when municipal ISS rates of up to 5% stack atop state ICMS ranging 17%–19%, squeezing net operating income. The 10-year phased replacement of ISS/ICMS with IBS and CBS should lower compliance complexity, yet uncertainty over apportionment keys and transition credits fosters investor hesitation[4]BDO Global, “Brazil Indirect Tax Reform: A Work in Progress,” bdo. global. . Smaller operators divert managerial resources to reconcile split invoicing of accommodation (ISS-taxed) versus F&B (ICMS-taxed), raising administrative overhead. Transfer-pricing scrutiny on management-fee flows constrains multinational chains’ ability to centralize services, adding friction to portfolio expansion. Although recent rulings exclude municipal tax from PIS/COFINS-Import bases, relief benefits import-heavy luxury properties more than domestic mid-scale operators, perpetuating uneven impact across segments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Chain dominance and conversion momentum

Chain Hotels accounted for 59.12% of the Brazil hospitality market size in 2025, benefiting from strong brand recall and nationwide distribution. Their 7.29% CAGR outlook reflects robust franchise demand and pipeline additions by Accor, Hilton, and Marriott. Loyalty programs funnel repeat guests, while centralized procurement lowers cost per available room. Independent properties, holding the remaining 40.88%, leverage local charm in beach and eco-destinations but struggle with marketing scale. Conversion activity accelerates as owners seek the revenue premium derived from brand affiliation. Franchise agreements now include technology bundles such as integrated channel managers and PIX-enabled direct booking engines that boost net ADR. Independent hoteliers who resist branding focus on niche positioning and partnerships with regional OTAs to defend occupancy. The divergent strategies keep both segments relevant, yet the Brazil hospitality market continues to skew toward professionally managed chains in gateway and secondary cities.

Chain operators deploy asset-light models to extend reach without balance-sheet burden, aligning with investors’ preference for annuity-style income. Management contracts increasingly include ESG performance clauses that tie incentive fees to energy-efficiency metrics, a trend that resonates with global capital allocators. Independent clusters in heritage centers like Paraty differentiate through cultural programming and farm-to-table gastronomy, scoring top guest-satisfaction indexes despite lower marketing budgets. Both segments contend with rising labor costs, prompting experimentation with contactless check-in and housekeeping on demand. Ultimately, hybrid alliances—where independents join soft brands—could blend brand power with local authenticity and further reshape competitive dynamics within the Brazil hospitality market.

By Accommodation Class: Mid-scale breadth and serviced-apartment acceleration

Mid & Upper-Mid-scale hotels captured 45.05% share of the Brazil hospitality market size in 2025, serving price-sensitive business travelers and an expanding middle class. Average pipeline length sits at 24 months, faster than luxury projects, enabling timely response to demand spikes from regional events. Service Apartments, while holding smaller base inventory, are projected to log an 11.05% CAGR through 2031, the fastest among all classes, as relocation assignments, digital nomadism, and extended tourist stays gain traction. Brands such as Adagio and Hyatt House roll out modular designs that cut development time by 15% and allow flexible unit mix.

Luxury demand rebounds in destinations such as Ceará, where four resorts with nightly rates of up to R$15,000 open by 2026, catering to high-net-worth adventure seekers. Deep-pocketed guests drive clusters of ancillary revenue from private surf charters to heli-tours lifting total-spend per occupied room. Budget & Economy hotels face compression of net ADR as tax and utility costs rise, but they remain indispensable in transport corridors frequented by truck drivers and domestic tour groups. With eco-lodges gaining access to subsidized green finance, a new sub-segment of rustic-luxury emerges, enabling rate premiums while meeting sustainability goals. The resulting class stratification enhances choice for consumers and diversifies revenue streams across the Brazil hospitality market.

By Booking Channel: Disintermediation gains pace

Online Travel Agencies retained 42.60% share of the Brazil hospitality market size in 2025, leveraging search aggregation and marketing heft. Yet Direct Digital bookings are rising at 13.48% CAGR as hotels integrate PIX, chatbot-driven customer service, and loyalty-driven rate parity on their websites. Net ADR can improve up to 8 percentage points when reservations bypass intermediaries, prompting chains to offer member-exclusive discounts. Corporate/MICE platforms rebound as multinationals reinstate in-person meetings; however, virtual-hybrid event formats temper long-haul group demand. Wholesale & Traditional Agents persist in handling government delegations and pilgrimage groups but confront shrinking commissions.

Mobile-first Brazilians increasingly rely on social-media-linked booking widgets that convert inspiration into instant transactions, shortening the look-to-book window. OTAs counter by bundling airfare and ground transport, deepening loyalty through tiered reward schemes. Hotels employ CRM analytics to mine repeat-guest data, tailoring upsell offers such as late-checkout and co-working passes. The resulting tug-of-war cultivates healthier channel-mix discipline, positioning the Brazil hospitality market for higher margin resilience.

Geography Analysis

The Southeast region represented 54.75% of the Brazil hospitality market share in 2025 on the strength of São Paulo’s corporate hub and Rio de Janeiro’s event magnetism. Congonhas and Santos-Dumont slots constrain weekday frequency, yet Guarulhos’ USD 250 million terminal project will ease international surges by 2028. Hotel pipelines concentrate on conversion opportunities near financial districts, where land scarcity heightens barriers to entry. Rate ceilings are tested during mega-events, reaffirming the region’s pricing power.

The North posts the fastest 7.24% CAGR through 2031, buoyed by COP-30 preparations that will raise Belém’s room count from 18,000 to 50,000. Federal investments extend beyond hospitality to urban mobility, enhancing tourist mobility within the Amazon gateway. Eco-cruise operators collaborate with lodges to offer multi-modal itineraries, lengthening average stay. Local authorities facilitate expedited licensing for projects using sustainable materials, expediting supply timelines. The boom seeds long-term potential for biodiversity tourism and scientific expeditions that demand specialized lodging.

In the Northeast, established sun-and-sand corridors continue to attract domestic families and European charters. Ceará’s high-end pipeline, including branded golf-resorts and private-villa enclaves, signals confidence in premium leisure demand. South and Central-West regions rely on agribusiness-driven corporate demand; occupancy stabilizes on weekdays but dips on holidays, resulting in balanced yet modest growth rates. Overall, geographic diversification cushions operators against regional shocks and maintains aggregate stability for the Brazil hospitality market.

Competitive Landscape

The leading hotel groups hold a significant share of the Brazil hospitality market, yet the landscape remains sufficiently open to support the entry and growth of new competitors. Accor holds a leading position, thanks to its diversified brand portfolio ranging from budget-friendly options like Ibis to high-end offerings such as Fairmont. A well-established loyalty program with millions of members in Brazil further reinforces its strong presence. Hilton is pursuing an ambitious growth strategy, aiming to significantly expand its presence by the end of the decade, with a focus on secondary coastal cities using its Hampton and Curio Collection brands. Marriott, meanwhile, is rolling out its City Express brand to attract cost-conscious business travelers and small enterprises, signaling a targeted push into more affordable, utilitarian segments.

Local group WAM accelerates with a RMB 500 million (USD 69.76 million) resort complex in Paraíba, exemplifying domestic capital’s appetite for greenfield development. Aparthotel innovators like HQ Hotels enter São Paulo via asset-light partnerships with Wyndham and sbe, blending extended-stay layouts with celebrity chef venues. Technology funnels differentiate players: cloud-based revenue management, AI-driven demand forecasting, and PIX-integrated check-out streamline operations. ESG performance becomes a tender criterion for corporate RFPs, rewarding chains that embed carbon-tracking dashboards.

M&A potential remains high as family-owned independents seek exit options post-pandemic. Franchise conversions proceed swiftly due to standardized PIP (property improvement plan) templates that reduce downtime. Legislative progress on VAT reform could unlock additional deal flow by clarifying cross-border tax credits. As product-class adjacency blurs think luxury tented camps or branded residences operators refine portfolio strategies to defend RevPAR and capture share in the evolving Brazil hospitality market.

Brazil Hospitality Industry Leaders

Accor SA

Atlantica Hospitality

Intercity Hotels

Marriott International Inc.

Hilton Worldwide Holdings Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Hampton by Hilton confirms 100-room seaside property in Praia Grande’s Litoral Plaza complex, launching alongside a private cruise terminal worth BRL 1 billion (USD 200 million).

- April 2025: Hilton debuts three Curio Collection properties across Curitiba, Pinhais, and São Paulo, marking lifestyle-segment expansion.

- March 2025: BWH Hotels schedules eight openings in secondary and tertiary Brazilian cities, half slated for 2025 activation.

- February 2025: Accor evaluates up to five Faena luxury hotels, signaling intent to upscale brand mix beyond Rio-São Paulo corridor.

Brazil Hospitality Market Report Scope

The hospitality industry encompasses businesses and establishments primarily engaged in providing accommodation, food and beverage services, entertainment, event planning, and other related services to travelers, tourists, and local patrons. The Brazilian hospitality industry is segmented by type and segment. By type, the market is segmented into chain hotels, independent hotels, and service apartments. By segment, the market is segmented into budget and economy hotels, mid and upper-mid-scale hotels, and luxury hotels. The report offers market size and forecasts for the Brazilian hospitality industry in value (USD) for all the above segments.

By Type

| Chain Hotels |

| Independent Hotels |

By Accommodation Class

| Luxury |

| Mid & Upper-Mid-scale |

| Budget & Economy |

| Service Apartments |

By Booking Channel

| Direct Digital |

| OTAs |

| Corporate / MICE |

| Wholesale & Traditional Agents |

By Geographic Region

| North Region |

| Northeast Region |

| Central-West Region |

| Southeast Region |

| South Region |

| By Type | Chain Hotels |

| Independent Hotels | |

| By Accommodation Class | Luxury |

| Mid & Upper-Mid-scale | |

| Budget & Economy | |

| Service Apartments | |

| By Booking Channel | Direct Digital |

| OTAs | |

| Corporate / MICE | |

| Wholesale & Traditional Agents | |

| By Geographic Region | North Region |

| Northeast Region | |

| Central-West Region | |

| Southeast Region | |

| South Region |

Key Questions Answered in the Report

What revenue figure is Brazil’s hospitality forecast to reach by 2031?

Sector value is set to climb to USD 11.59 billion by 2031, reflecting a 5.44% CAGR.

Which accommodation class is expanding the quickest across the country?

Service Apartments are leading growth with an 11.05% CAGR projected through 2031.

How is PIX instant payment reshaping hotel booking behavior in Brazil?

PIX drives spontaneous domestic trips by removing card-fee friction, boosting weekend occupancy and helping hotels record revenue gains of roughly 16% after adoption.

What hotel demand spike is expected from COP-30 in Belém?

Delegates and visitors linked to the 2028 summit will nearly triple local room supply needs, pushing projected ADR toward USD 500.

Which Brazil region currently generates the greatest share of hotel revenue in 2025?

The Southeast region, anchored by São Paulo and Rio de Janeiro, commanded 54.75% of national revenue in 2025.

Page last updated on: