Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

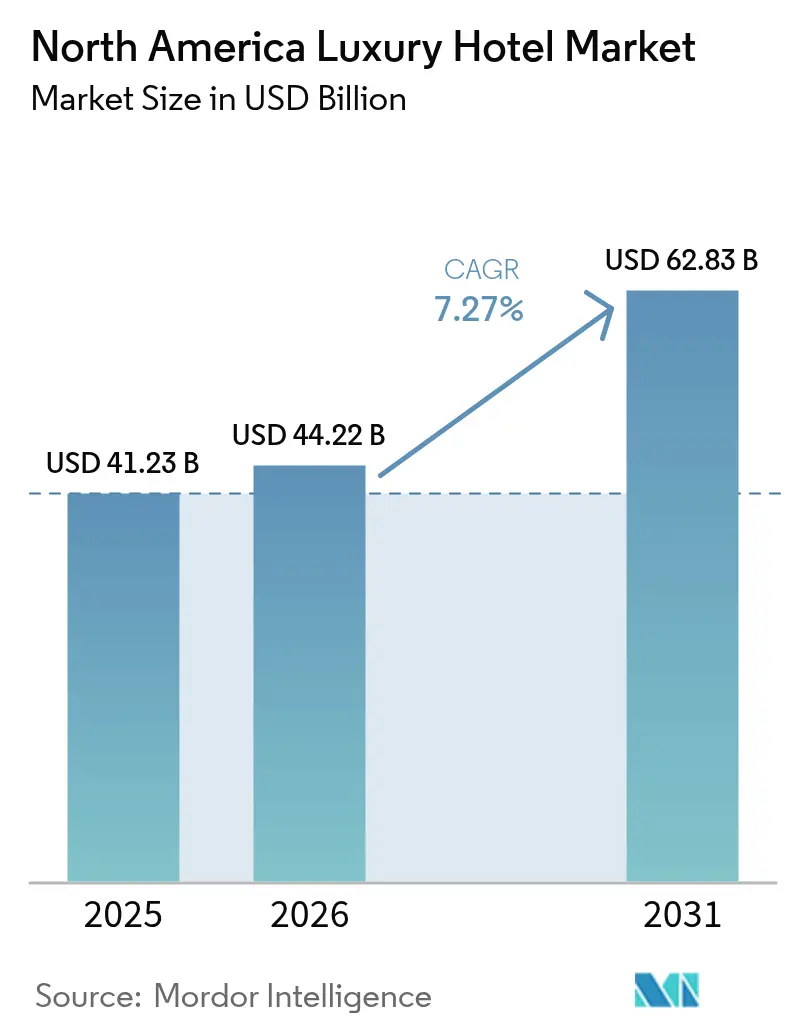

| Base Year Market Size (2025) | USD 41.23 Billion |

| Market Size (2026) | USD 44.22 Billion |

| Market Size (2031) | USD 62.83 Billion |

| Growth Rate (2026 - 2031) | 7.27% CAGR |

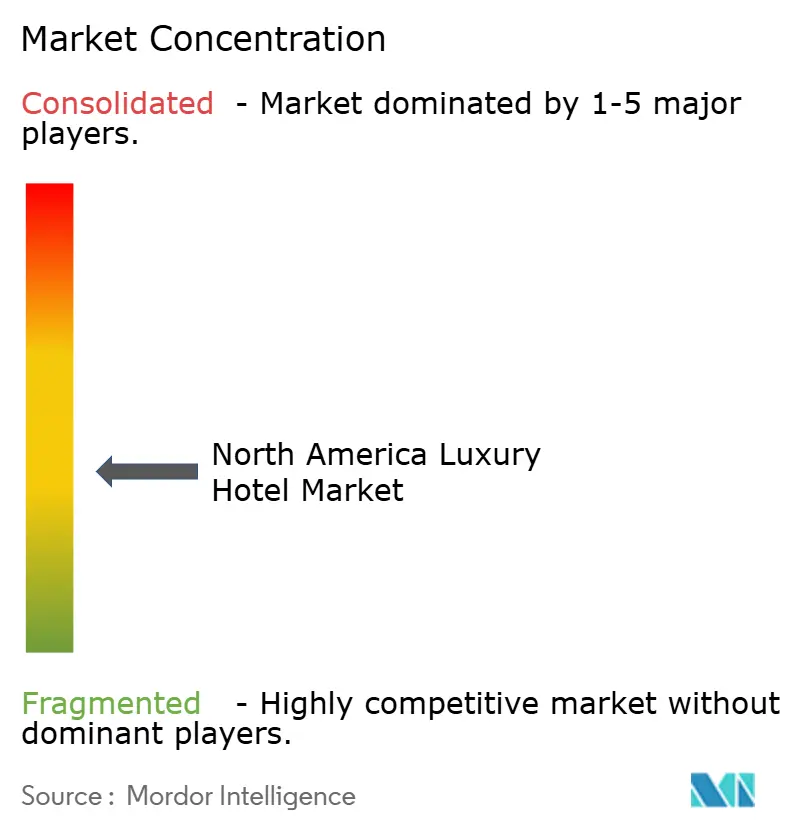

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Luxury Hotel Market Analysis by Mordor Intelligence

The North America luxury hotels market size in 2026 is estimated at USD 44.22 billion, growing from 2025 value of USD 41.23 billion with 2031 projections showing USD 62.83 billion, growing at 7.27% CAGR over 2026-2031. Demand rebounds in every gateway city as affluent travelers rediscover long-haul trips, and resorts capture spending tied to wellness retreats. Operators accelerate pipeline additions, with Marriott alone signing 61 new luxury deals in 2024, while adaptive-reuse conversions bring new supply online at lower capital intensity. Government spending shows the region’s total international visitor exports rising 19% year-over-year in 2024, a figure that exceeded overall services-export growth by more than 7 percentage points, reaffirming luxury hospitality’s out-sized contribution to trade surplus generation [1]Source: U.S. Department of Commerce, “International Trade in Services 2024,” commerce.gov. . Franchise reliance deepens because asset-light growth supports speed to market, yet soft-brand collections gain favor by pairing global distribution with preserved property character. Technology adoption, especially AI-driven revenue management, nudges average daily rate (ADR) higher and cushions margin pressure created by development-cost inflation and short-term rental competition.

Key Report Takeaways

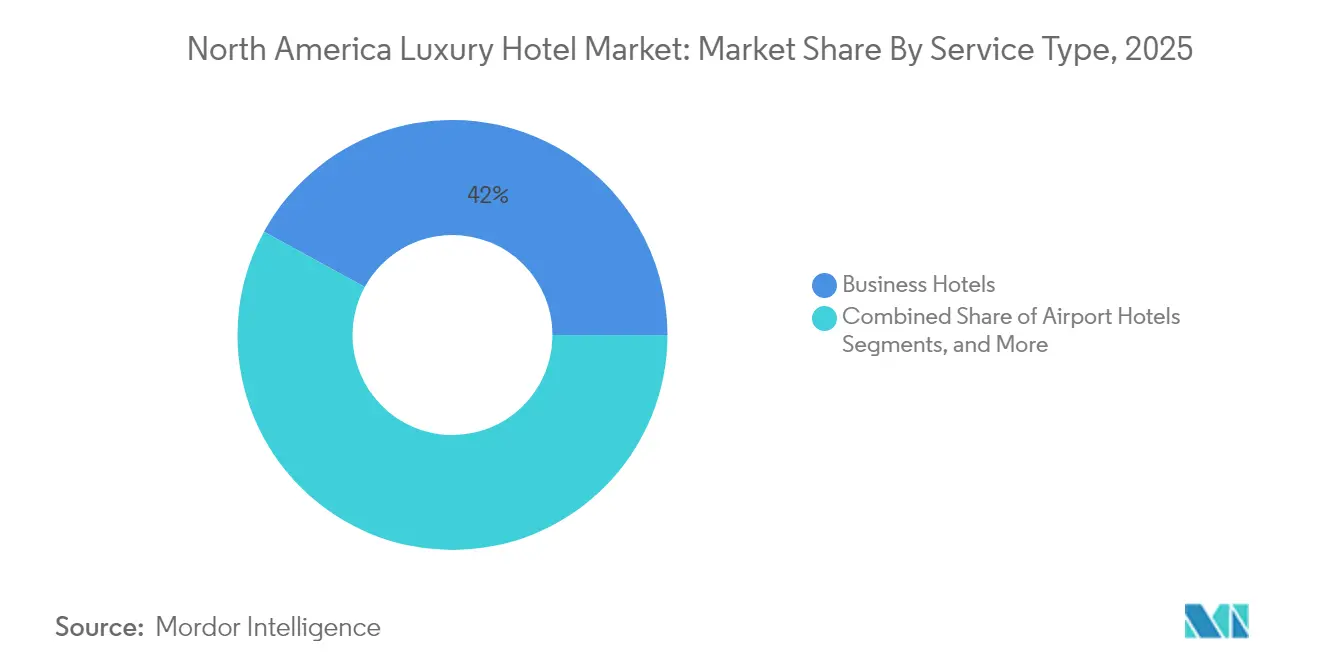

- By service type, business hotels led with 42.02% revenue share of the North America luxury hotels market in 2025; resorts are projected to post the fastest 7.45% CAGR through 2031.

- By ownership model, the franchise format captured 66.01% of the North America luxury hotels market share in 2025, whereas soft-brand collections are set to expand at an 7.93% CAGR to 2031.

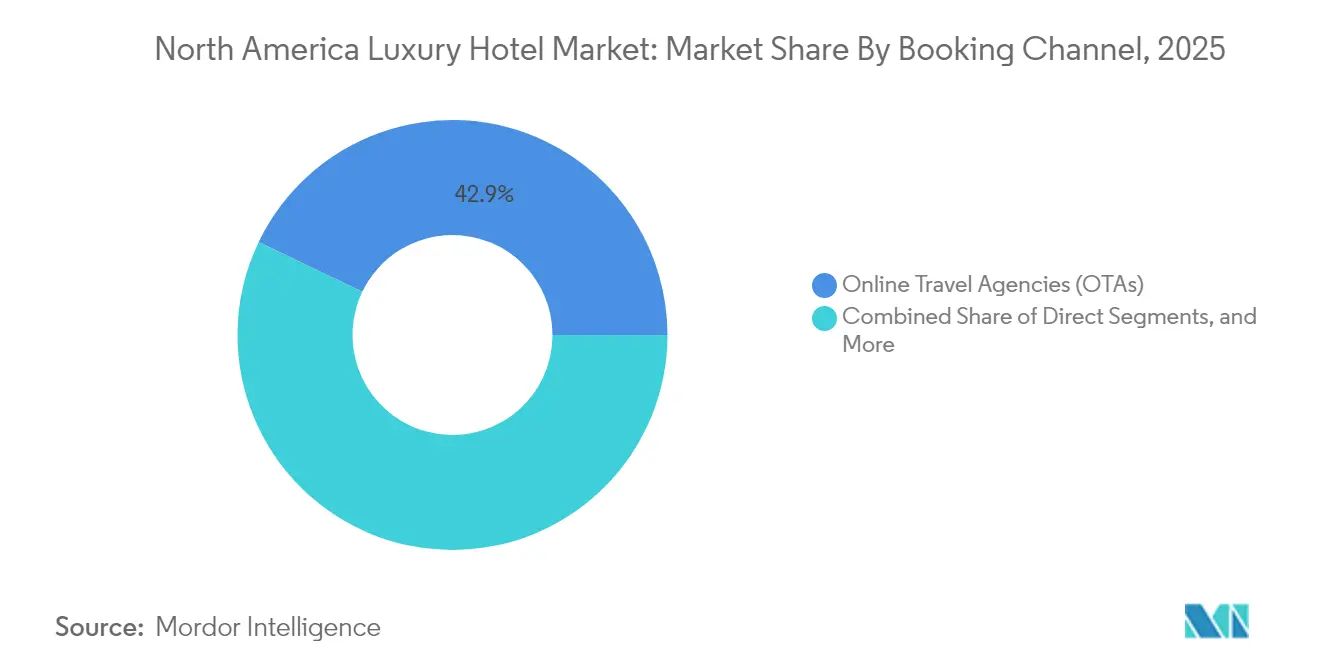

- By booking channel, online travel agencies (OTAs) controlled 42.88% of bookings in 2025, but direct digital channels are forecast to grow at 7.32% CAGR in the North America luxury hotels market.

- By customer segment, leisure travelers generated 61.54% of 2025 room demand, while bleisure demand is expected to rise at an 8.08% CAGR through 2031 in the North America luxury hotels market.

- By geography, the United States accounted for 79.75% share of the North America luxury hotels market size in 2025; Mexico will record the highest 7.86% CAGR to 2031.

- The North America luxury hotels market exhibits moderate concentration with the top 5 operators including Marriott International, Hilton Worldwide, Hyatt Hotels Corporation, Four Seasons Hotels & Resorts, and Accor SA, holding major market shares.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Luxury Hotel Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Post-pandemic rebound in inbound and domestic high-net-worth travel | +1.8% | North America, with strongest impact in US gateway cities | Medium term (2-4 years) |

| Record luxury-brand pipeline expansion by global chains | +1.5% | US and Mexico primary markets, Canada secondary | Long term (≥ 4 years) |

| Rise of soft-brand collections empowering independent luxury assets | +1.2% | US and Canada urban markets, Mexico emerging | Medium term (2-4 years) |

| Ultra-affluent demand for immersive "bleisure" & wellness retreats | +1.0% | Global, with concentration in US leisure destinations | Short term (≤ 2 years) |

| Adaptive reuse of vacant Class-A offices into urban luxury hotels | +0.8% | US metropolitan areas, Toronto and Vancouver | Long term (≥ 4 years) |

| AI-enabled total revenue management boosting ADR lift | +0.9% | North America technology-forward markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Post-pandemic rebound in inbound and domestic high-net-worth travel

Luxury RevPAR climbed 12% year-on-year in January 2025 as affluent guests resumed international itineraries and shifted budgets from goods to experiences. The addressable affluent base widens because individuals with USD 100,000–1 million in net worth now constitute 35% of luxury demand. Mexico’s Secretariat of Tourism (SECTUR) documented USD 30.8 billion in international receipts, a historic peak, 63% of which originated from U.S. residents [2]Source: Secretariat of Tourism (Mexico), “Resultados del Turismo 2024,” sectur.gob.mx. . Younger travelers under 60 already generate 80% of luxury leisure bookings, spurring hotels to introduce digital concierge functions and immersive local programming. Mexico welcomed USD 30.8 billion in international visitor spend in 2024, 63% originating from the United States, underscoring strong cross-border luxury flows.

Record luxury-brand pipeline expansion by global chains

Marriott signed 61 luxury projects in 2024 and has 266 properties in its development pipeline, illustrating the premium segment’s pricing resilience. Hilton sharpened its lifestyle push by acquiring Graduate Hotels for USD 210 million and taking majority control of Sydell Group to scale the NoMad flag globally. Pipeline density is most apparent in Mexico, where 25% of 191 hotels under construction fall in the luxury tier, supported by infrastructure upgrades such as the Maya Train and Tulum International Airport. Although new builds intensify competition for talent, expanded distribution readies chains to capture the full travel rebound.

Rise of soft-brand collections empowering independent luxury assets

Soft-brand inventory reached 101,452 rooms across 601 U.S. hotels in 2024, with luxury accounting for 8% of the total. Financial analysis shows soft-branded assets enjoy higher EBITDA margins than unaffiliated independents while preserving architectural individuality. IHG’s Vignette Collection targets a USD 100 billion white space, aiming to add 100 properties in a decade. Hilton’s alliance with Small Luxury Hotels of the World widens distribution without diluting flagship names, confirming that soft-brand affiliation is now mainstream for upscale independents.

Ultra-affluent demand for immersive “bleisure” and wellness retreats

Two-thirds of travelers now blend work and leisure, lifting the global blended-travel market toward USD 731 billion by 2032. Wellness tourism is on a parallel upswing, projected to reach USD 8.5 trillion in 2027, growing 8.6% annually. Luxury resorts reply with longevity clinics, biometric diagnostics, and spa-plus-nutrition packages; Banyan Tree Veya in Mexico’s Valle de Guadalupe exemplifies the crossover. The younger affluent cohort values sustainable and authentic programming, pressing operators to curate nature-immersive itineraries and culinary concepts featuring local sourcing.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| > USD 1 million per-room development and retrofit costs | -1.4% | US and Canada primary markets, Mexico secondary | Long term (≥ 4 years) |

| Intensifying competition from upscale short-term rental platforms | -1.1% | North America leisure destinations and urban markets | Medium term (2-4 years) |

| Escalating franchise and loyalty fees compressing owner margins | -0.8% | US franchised properties, expanding to Canada | Short term (≤ 2 years) |

| Shortage of luxury-trained hospitality talent inflating wages | -0.7% | Canada acute shortage, US selective markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Less than USD 1 million per-room development and retrofit costs

Prime-city projects now exceed USD 1 million per key, stalling many independents and shifting capital to conversions. Only 150,000 rooms sit in the US active pipeline, and developers favor adaptive reuse in Dallas and Atlanta where land remains comparatively affordable. Conversions curtail build times but demand sophisticated engineering to meet five-star standards, thus favoring seasoned global chains.

Intensifying competition from upscale short-term rental platforms

Luxury rentals priced beyond USD 1,000 per night saw demand increase 8% in 2024, siphoning leisure travelers who want privacy and expansive floor plans. Platforms such as Wander and Mint House now deliver hotel-grade housekeeping, narrowing service gaps. Hotels counter with exclusive culinary residencies, branded kids’ clubs, and loyalty-based perks, yet margin erosion persists where rate ceilings collide with rising costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Business hotels anchor demand while resorts accelerate

Business hotels generated 42.02% of 2025 revenue in the North America luxury hotels market, underpinned by revived corporate gatherings and improved group RevPAR at leading chains. Conference-ready urban properties continue to command premium ADR because proximity to headquarters clusters shortens travel windows. The segment secures weekday base occupancy, letting revenue managers flex resort-style pricing on weekends. Still, the resorts sub-category records the fastest 7.45% growth as affluent guests extend stays and opt for integrated wellness itineraries.

Resorts capture length-of-stay advantages, spend on spa treatments, and rising work-from-anywhere demand. A growing share of extended trips ends in coastal Mexico, luxe mountain enclaves in British Columbia, and U.S. desert wellness retreats. As a result, resorts could reach 34.72% of the North America luxury hotels market size by 2031. Operators are repurposing meeting pavilions into indoor-outdoor co-working lounges to court the same bleisure guest, thereby blurring the line between traditional business and resort typologies.

By Ownership Model: Franchise scale collides with soft-brand agility

Franchise contracts represented 66.01% of the North America luxury hotels market in 2025, validating the asset-light expansion route. These deals let brands seed smaller U.S. metros and Mexican secondary resorts without over-leveraging corporate balance sheets. However, soft-brands will expand to 7.93% annually, enabling owners to win luxury-seeking travelers who prize individuality. Chain-managed properties maintain premium positioning through direct operational control, while independent hotels face increasing pressure to affiliate with major brands for distribution access.

Independent flags still matter in legacy destinations, yet funding constraints and distribution challenges push many to soft-brand affiliation. The North America luxury hotels industry therefore trends toward mixed portfolios where the same parent company distributes standardized luxury along financial centers and bespoke concepts in arts districts.

By Booking Channel: OTA reach meets direct engagement

OTAs delivered 42.88% of 2025 upscale bookings, providing vital visibility for new Mexican shoreline projects and urban boutiques alike. Commission drag remains a pain point, yet hotels tolerate OTA dependence to backfill shoulder-night demand. According to the U.S. Federal Trade Commission, new regulations requiring transparent resort-fee disclosure may push price-sensitive guests toward direct booking where pricing appears clearer . Direct portals are growing 7.32% a year as loyalty apps integrate mobile keys, personalized upgrade offers, and one-tap ancillary purchases, nudging guests to bypass intermediaries.

GDS platforms stay relevant for managed corporate programs, but leisure-heavy properties push exclusive website-only wellness packages. Over time, the direct channel could equal OTA volumes, shifting the North America luxury hotels market size mix and boosting owner margins. The North America luxury hotels industry recognizes that first-party data powers segmented marketing, so capex allocation tilts toward digital personalization engines and user-experience overhauls.

By Customer Segment: Leisure foundation with bleisure innovation

Leisure travelers delivered 61.54% of 2025 room nights and remain the revenue spine of the North America luxury hotels market. High-net-worth households dedicate larger wallet share to experiential travel, prompting hotels to diversify F&B, partner with local artisans, and curate adventure excursions. Corporate transient segments revive but still trail 2019 volume, pushing properties to repurpose underused club floors into hybrid event studios.

Bleisure trips are scaling fastest at 8.08% annually as 66% of travelers blend business with leisure extensions. Hotels now design “work-from-suite” layouts featuring ergonomic desks, 10-gig Wi-Fi, and wellness breaks. If momentum holds, bleisure stays could command 14.65% of the North America luxury hotels market size by 2031. Ultra-high-net-worth travelers continue to anchor top-tier suite demand, but most incremental gains originate from rising-affluent demographics seeking aspirational experiences.

Geography Analysis

North America’s luxury hospitality environment hinges on a mature United States base and accelerating Mexican beach and culture circuits. U.S. assets generated the bulk of the North America luxury hotels market size in 2025, with urban flags leveraging global distribution systems to optimize rate integrity while suburban resorts capture domestic leisure surges. The pipeline stays active in Sun Belt metros where cost-of-living advantages lure corporate relocations that feed midweek bookings. Conversion projects repurpose dormant offices in San Francisco and Philadelphia, injecting luxury inventory without extensive permitting delays.

Mexico advances at an 7.86% CAGR as operators channel fresh capital into Pacific Coast and Caribbean Riviera sub-markets. Marriott, Hilton, and Hyatt collectively supervise more than 40 luxury projects, wagering on robust U.S. outbound travel and an emerging domestic affluent class. Government infrastructure budgets expand airport capacity and rail connectivity, positioning inland heritage cities such as Mérida for upscale boutique expansion. Sustainability regulation tightens along coastal biospheres, compelling developers to adopt low-impact building methods and marine-life protection programs that resonate with eco-conscious guests.

Canada’s gateway clusters sustain healthy ADR even as cost per room constructed surpasses USD 1 million in top districts. Toronto’s Entertainment District will welcome the Nobu Hotel in summer 2025, enriching the city’s five-star palette and tempting U.S. weekend travelers. Vancouver capitalizes on its cruise-port status to convert pre- and post-voyage guests into extended luxury stays. Labor shortfalls, immigration policy shifts, and lengthy entitlement processes temper supply growth, yet high barriers preserve pricing power for existing assets.

Regulatory Landscape

Luxury hotel operators in North America operate under layered compliance requirements that vary by jurisdiction, spanning lodging rules, employment requirements, and guest-information obligations. In Canada, Ontario is a key example of rising operational compliance: new 2026 requirements for accommodation providers and platforms extend guest-registration and record-keeping expectations, increasing documentation and retention burdens that can affect front-desk workflows and vendor selection for property-management and identity capture tools.

Public-sector travel policy also shapes demand and border friction. In the United States, travel and tourism policy is supported through the Department of Commerce and statutory responsibilities for travel and tourism leadership (15 U.S. Code Section 9803), alongside the 2022 National Travel and Tourism Strategy, which frames actions to improve the visitor experience and international competitiveness. Luxury operators track these priorities when planning gateway-city capacity, staffing, and service standards.

Value Chain Analysis

The North America luxury hotel value chain starts with real estate owners and developers securing sites or conversion candidates, arranging financing, and partnering with architects, designers, and contractors to deliver five-star specifications. FF&E and OS&E sourcing is a key midstream node, often coordinated through hospitality procurement specialists such as Avendra, R-W Purchasing Partners, Pineapple Procurement, Haute Procurement, and Hotel Procurement & Design Services. These firms connect ownership groups with global manufacturers, logistics providers, and installers while supporting brand standards and property improvement plan (PIP) requirements.

Distribution and demand generation flow through brand.com and loyalty ecosystems, OTAs, global distribution systems (GDS) for corporate travel, and tour and wholesale channels. Property-level operations then convert demand into room and ancillary revenue (F&B, spa, experiences). Lead times and budget volatility are amplified by trade exposure for imported furnishings and limited domestic capacity for high-end hospitality manufacturing, which pushes owners and operators to diversify country-of-origin, lock specifications early, and use multi-vendor contracting to stabilize PIP and new-build execution. Recent Miami luxury activity, including the debut of Brickell Arch as a Luxury Collection hotel and the announcement of Anantara Miami Resort & Residences, highlights how brand operators, developers, and procurement partners align redesigns and launches in prime markets.

Competitive Landscape

Marriott International, Hilton Worldwide, Hyatt Hotels Corporation, Four Seasons Hotels & Resorts, and Accor SA collectively dominate regional luxury distribution networks. Their combined scale enables preferred-supplier status with corporate buyers and deep loyalty engagement that directs bookings into brand ecosystems. Hilton’s USD 210 million acquisition of Graduate Hotels broadens campus-adjacent lifestyle coverage, while the majority stake in Sydell Group signals ambition to seed the NoMad brand across global capitals. Marriott’s purchase of Postcard Cabins highlights a tactic to absorb outdoor-immersive demand without diluting core luxury credentials.

Technology is a chief arms race variable. AI-powered revenue platforms raise ADR 6–10% by recommending rate adjustments in sub-hourly bursts and cross-selling spa or experience bundles. Guests expect digital keys and messaging apps; brands unwilling to fund these upgrades risk occupancy erosion to tech-forward rivals. Independent properties differentiate through hyper-local designs and chef-driven dining but must join soft-brands or consortiums to preserve visibility on meta-search engines.

White-space expansion thrives in secondary U.S. cities where corporate relocations spur upscale business travel. Adaptive reuse of Class-A offices into luxury hotels unlocks centrally located inventory, though design challenges demand experienced firms. Wellness-centric product segmentation grows, with Four Seasons adding medical-grade longevity suites and Montage collaborating with fitness brands for retreat experiences. Consequently, competitive advantage hinges on harmonizing personalized human service with data-driven precision, ensuring that luxury stays feel bespoke yet operationally efficient.

North America Luxury Hotel Industry Leaders

Marriott International

Hilton Worldwide

Hyatt Hotels Corp.

Four Seasons Hotels & Resorts

Accor SA

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Technology modernization remains a clear opportunity as operators standardize cloud-native property platforms and revenue tools to strengthen distribution control, guest recognition, and operational coordination across multi-property portfolios. In 2026, Loews Hotels expanded Oracle Hospitality OPERA Cloud across its U.S. portfolio, and IHG completed a multi-year core systems overhaul that included a new reservation platform and AI-driven revenue management. Together, these changes point to integrated data and automation moving from pilots into routine hotel operations and franchise support.

Capital formation and large-scale project execution also open room for luxury supply in high-barrier destinations, especially when mixed-use structures help unlock funding and broaden demand sources. In March 2026, One Beverly Hills finalized USD 4.3 billion in financing led by J.P. Morgan and VICI Properties to advance a destination anchored by Aman Beverly Hills and The Beverly Hilton. Resort-led demand is supported by major expansions and renovations as well, including Turning Stone Resort Casino opening its 258-room Crescent Hotel as part of a USD 400 million multi-year expansion, and OUTRIGGER commencing a USD 100 million transformation of OUTRIGGER Waikiki Beach Resort. These initiatives reflect continued investment in premium assets and experiences across U.S. gateway and resort markets, with implications for brand pipeline strategy, owner ROI models, and luxury product segmentation (wellness, experiential, and bleisure-ready stays).

Recent Industry Developments

- July 2026: Marriott International completed the transaction to bring the Lefay luxury wellness brand into its global portfolio through a joint venture, with integration into Marriott Bonvoy planned for later in 2026. The deal extends Marriott's reach in luxury wellness, a segment aligned with retreats and experiential stays that are gaining share within luxury demand.

- March 2026: Marriott International and the Leali family announced a milestone joint venture to incorporate the Lefay brand into Marriott's portfolio. It formalized a path for specialized wellness luxury to scale through a major loyalty and distribution platform while keeping a distinct brand identity.

- January 2026: Hyatt Hotels Corporation reported a record global pipeline of approximately 148,000 rooms at year-end 2025, with U.S. room signings up 30% versus 2024. The update points to continued new-build and development momentum that feeds luxury and upper-upscale supply planning across North America.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this report, we size the value generated by luxury hotels operating in North America, counted as guest-facing lodging revenue from rooms plus in-house services that are billed by the property (for example, food and beverage, spa, and other on-property amenities).

Scope exclusions: We exclude non-luxury lodging, branded residences sold mainly as real estate, serviced apartments, and shared-economy vacation rentals.

Segmentation Overview

- By Service Type

- Business Hotels

- Airport Hotels

- Suite Hotels

- Resorts

- Other Service Types

- By Ownership / Management Model

- Chain-Managed

- Franchise

- Independent

- Soft-Brand Collections

- By Booking Channel

- Direct

- Online Travel Agencies (OTAs)

- Global Distribution Systems / Corporate Travel

- Tour Operators & Wholesale

- By Customer Segment

- Leisure

- Business

- Bleisure

- Group / MICE

- Ultra-High-Net-Worth (UHNWI)

- By Geography

- United States

- Canada

- Mexico

Data Sources, Market Sizing, and Validation

Desk Research

Desk research started with building the demand and supply backdrop for luxury stays across the United States, Canada, and Mexico, and then mapping it back to hotel performance indicators. Public sources such as national tourism ministries and statistical agencies, airport passenger traffic releases, and central bank or government inflation series were used to set a consistent time-series view for travel intensity and pricing.

We also referenced materials from organizations such as UN Tourism, the World Travel and Tourism Council, and hotel industry performance summaries from reputable trade bodies, along with company annual reports, investor presentations, and credible business press. Where helpful, paid subscriptions that aggregate company financials, news and financials, and import or export shipment data were used to speed up cross-checks and reduce the risk of missing material events that affect openings, closures, and pricing. These examples are not exhaustive, and many other public sources were reviewed to collect data, validate assumptions, and clarify open questions.

Primary Interviews and Surveys

Primary work was used to pressure-test desk findings and fill gaps that are common in luxury lodging, especially around effective average daily rate movement, occupancy recovery patterns, and amenity revenue capture. We spoke with a mix of hotel owners and operators, asset managers, revenue management leaders, and travel buyers across North America so the model reflects differences between gateway cities, resort destinations, and secondary markets.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 30% | CXOs: 17% | |

| Mid tier: 51% | Functional/Unit leaders: 24% | |

| Smaller Players: 19% | Managers: 59% |

Market-Sizing & Forecasting

The market size was first reconstructed using a top-down approach that translates the luxury room supply and utilization picture into revenue, and then layers in typical on-property spend. In practice, we used a demand pool logic where available luxury room inventory, occupancy trends, and ADR movement set the core room revenue, which is then adjusted using ancillary revenue share patterns that were validated through interviews.

To keep the totals realistic, the output was corroborated with selective bottom-up approximations such as sampled property revenue per available room checks, observed rate positioning versus upper upscale hotels, and roll-ups from a limited set of publicly discussed portfolios. Where coverage was thin, gaps were adjusted using the same revenue share logic. Inputs that mattered most included luxury room inventory and openings, occupancy and length-of-stay direction, ADR and inflation-adjusted pricing, mix of business versus leisure demand by market type, and the share of revenue coming from food and beverage and wellness services. Forecasts were built using scenario analysis, where baseline, softer, and faster recovery paths were tied to expert views on travel demand, rate discipline, and new supply timing.

Data Validation & Update Cycle

We ran multiple checks before sign-off so the size lines up with real-world signals and does not drift due to a single optimistic assumption. Model outputs were compared against independent indicators such as reported RevPAR direction, lodging price inflation, and announced pipeline and renovation activity, and then outliers were reworked with a second analyst review.

When a variance could not be explained cleanly, the assumption was revisited and, where needed, primary contacts were re-engaged to confirm the driver (for example, rate reset timing or amenity revenue rebound). Reports refresh annually, with interim updates triggered by material events such as sharp demand shocks, major policy changes affecting travel, or step changes in supply. Before delivery, a final analyst pass is completed so clients receive the latest updated view.

Mordor Intelligence's North America Luxury Hotel Market Size Compared With Other Published Estimates

Published market values for luxury hotels can differ even when the region sounds the same, because the inclusion rules and the revenue items counted are not always aligned. Differences in what is treated as "luxury," whether ancillary hotel revenue is included, and how exchange rates and inflation are handled can all shift the final number.

By tracking room inventory changes, ADR and occupancy paths, and then refreshing the inclusion rules for branded residences and short-term rentals, Mordor Intelligence keeps the estimate tied to operating luxury hotels rather than adjacent lodging and real estate revenues.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 41.23 B (2025) | |

| Industry Association A | USD 37.80 B (2025) | Counts primarily room revenue and tends to exclude spa, food and beverage, and other on-property services, which pulls the total down in luxury-heavy resort and wellness properties. |

| Global Consultancy B | USD 49.60 B (2025) | Uses a broader luxury boundary that can blend upper upscale hotels and branded residence-linked revenues, and it may apply more aggressive ADR progression that lifts the 2025 value. |

The table shows that the spread is mostly explained by what gets counted as luxury and which revenue lines are included in the hotel value. When scope is kept to operating luxury hotels in the United States, Canada, and Mexico, and the rate and occupancy logic is checked against standard performance indicators, the resulting size stays easier to trace and repeat year to year.

Key Questions Answered in the Report

What is the current size of the North America luxury hotels market?

The market is valued at USD 44.22 billion in 2026 and is on track to hit USD 62.83 billion by 2031.

Which segment is growing fastest within the North America luxury hotels market?

Resorts are forecast to expand at a 7.45% CAGR, benefitting from wellness and experiential travel trends.

How significant are soft-brand collections in luxury hotel growth?

Soft-brands are the fastest-growing ownership model, projected at an 7.93% CAGR as independents seek global distribution with brand flexibility.

Why is Mexico the most dynamic geography for luxury hotel development?

Luxury investment in Mexico rose 50% in 2024, aided by new infrastructure such as the Maya Train and Tulum International Airport that improves access for U.S. travelers.

How are luxury hotels addressing competition from upscale vacation rentals?

Operators invest in distinctive experiential programming, personalized service, and advanced loyalty benefits to differentiate from rental properties demanding over USD 1,000 nightly rates.

What role does technology play in luxury hotel profitability?

AI-driven revenue management delivers 6-10% ADR lifts and, combined with mobile keys and guest-messaging apps, boosts direct bookings and margins.

Page last updated on: