Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

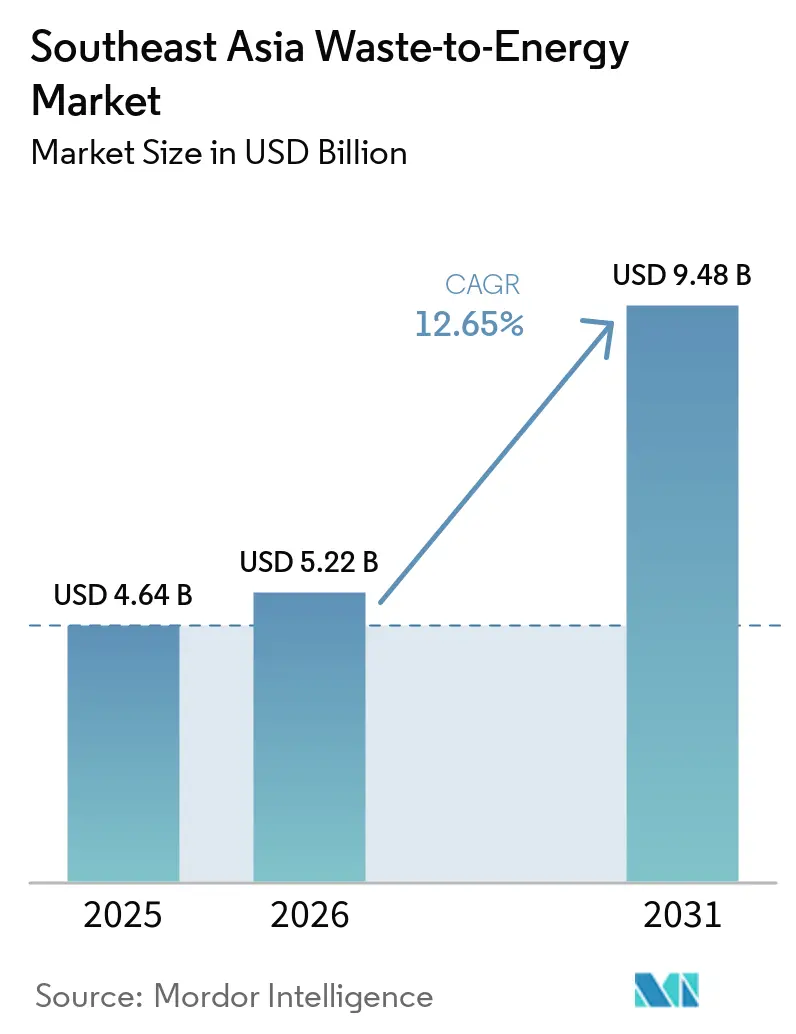

| Base Year Market Size (2025) | USD 4.64 Billion |

| Market Size (2026) | USD 5.22 Billion |

| Market Size (2031) | USD 9.48 Billion |

| Growth Rate (2026 - 2031) | 12.65% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Southeast Asia Waste-to-Energy Market Analysis by Mordor Intelligence

The Southeast Asia Waste-to-Energy Market size is expected to increase from USD 4.64 billion in 2025 to USD 5.22 billion in 2026 and reach USD 9.48 billion by 2031, growing at a CAGR of 12.65% over 2026-2031. Urban growth is raising waste volumes across Southeast Asia, and many city systems no longer have enough landfill headroom to absorb rising collection loads. At the same time, power demand is increasing across the region, so governments are treating waste conversion as both a disposal solution and a source of firm electricity supply. Policy support is becoming more practical in several countries, with clearer procurement structures, utility-linked offtake, and public-private delivery models now shaping project pipelines. Competition is also becoming more organized, as larger developers combine technology, engineering, financing, and operations into one offer. This leaves the Southeast Asia waste-to-energy market with durable long-term demand support, even though returns still depend on feedstock quality, tariff design, and capital discipline.

Key Report Takeaways

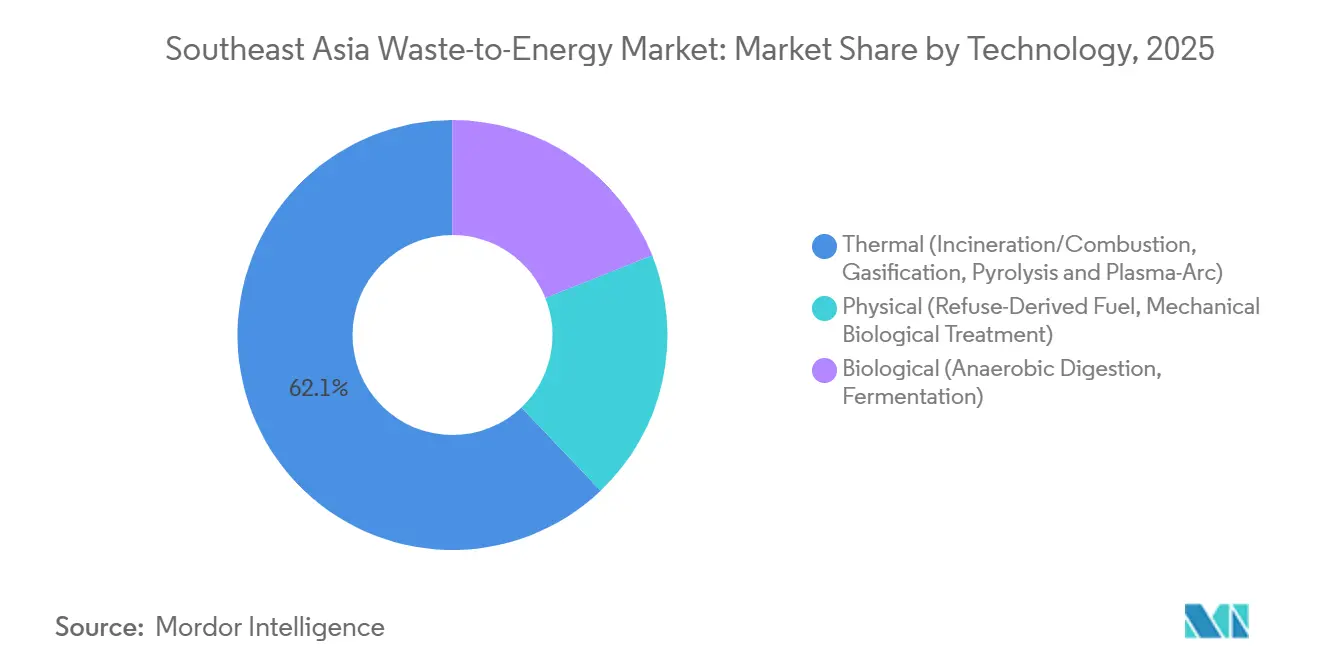

- By technology, thermal technology led with a 62.1% share in 2025, while biological technology is projected to record the highest CAGR at 14.3% through 2031.

- By waste type, municipal solid waste held a 56.4% share in 2025, while agricultural and agro-industrial residues are forecast to expand at a 13.8% CAGR through 2031.

- By energy output, electricity accounted for a 52.1% share in 2025, while transport fuels are expected to advance at a 15.8% CAGR through 2031.

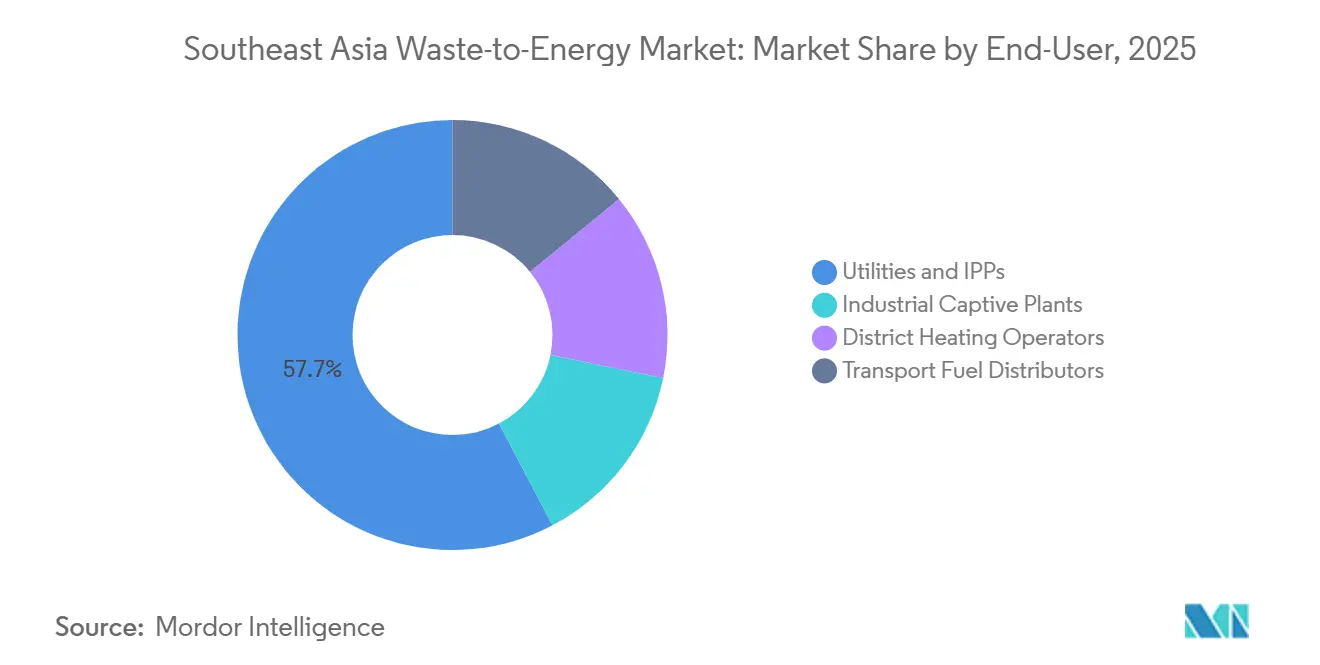

- By end-user, utilities and independent power producers held 57.7% in 2025, while transport fuel distributors are projected to grow at a CAGR of 15.3% through 2031.

- By geography, Indonesia held 31.6% of the regional market value in 2025, while Vietnam is forecast to grow at a 14.8% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Southeast Asia Waste-to-Energy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing waste generation in fast-growing urban hubs | +3.5% | APAC core, especially Indonesia, Vietnam, Thailand, and the Philippines | Short term (≤ 2 years) |

| Renewable energy and sustainability targets | +2.2% | Singapore, Malaysia, Thailand, and Vietnam | Medium term (2-4 years) |

| Government incentives and PPP frameworks | +2.8% | Indonesia, Vietnam, the Philippines, and Malaysia | Short term (≤ 2 years) to Medium term (2-4 years) |

| Rising landfill tipping fees and closure mandates | +1.5% | Jakarta, Bandung, Penang, Hanoi, and Bangkok | Short term (≤ 2 years) |

| Carbon credit monetization via voluntary markets | +1.3% | Malaysia and Indonesia, with wider regional relevance over time | Medium term (2-4 years) to Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Waste Generation Pressure Outpaces Landfill Absorption Capacity

Indonesia generated 56.63 million tonnes of municipal solid waste in 2023, and only 39% of that volume was properly managed, which shows how far collection and treatment systems still lag the waste stream itself.[1]Ministry of Environment and Forestry, “Presiden Tetapkan Perpres 109/2025, Langkah Nyata Atasi Sampah Perkotaan,” Government of Indonesia, kemenlh.go.id The core issue is not only the rise in waste volumes, but the widening gap between collection, treatment, and final disposal capacity across large cities and second-tier urban centers. That gap is becoming more important because waste growth is no longer concentrated only in megacities, and smaller urban clusters are now large enough to support commercial treatment assets. This is why plant formats in the 200 to 500 tpd range are becoming more viable in parts of the region where collection networks cannot yet support very large centralized projects. These local conditions make imported large-plant models less transferable without changes in scale, logistics, and financing. As a result, the Southeast Asia waste-to-energy market is expanding from a narrow metropolitan solution into a wider municipal infrastructure category.

Government Incentives and PPP Frameworks Unlocking Financing

Indonesia's Presidential Regulation No. 109 of 2025 replaced the earlier dual tipping-fee and power-purchase structure with a single fixed tariff of USD 0.20/kWh under a 30-year power purchase agreement, which materially changed project bankability. The regulation also moved procurement into a more centralized framework, which reduced fragmentation between municipal decision-making and project execution. In Thailand, an Asian Development Bank-backed THB 16.6 billion package, equal to USD 521.5 million, for 12 industrial waste-to-energy plants showed how multilateral backing can unlock projects that had previously faced financing constraints.[2]Asian Development Bank, “ADB, GWTE Sign 16.6 Billion Baht Deal To Advance Industrial Waste Management In Thailand,” Asian Development Bank, adb.org These policy steps matter because private capital moves faster when tariffs, waste delivery, and concession terms are defined early. They also favor sponsors that can move from financing to engineering to plant operations without depending on a long chain of counterparties. This is one of the clearest reasons the Southeast Asia waste-to-energy market is moving from scattered pilots toward larger and more repeatable project pipelines.

Renewable Energy and Sustainability Targets Raising Mandatory WtE Throughput

Thailand's Waste Management Sector Taxonomy, published in May 2025, formally classified waste-to-energy as a green activity that can qualify for sustainability-linked lending, which gives lenders a clearer basis for funding eligible projects. This matters because the financing question in the Southeast Asia waste-to-energy market is no longer only about waste disposal, but also about whether projects fit national decarbonization frameworks. Vietnam also moved in this direction, and Ho Chi Minh City is targeting more than 90% of household waste to be processed through waste-to-energy incineration between 2025 and 2030. Once waste-to-energy is tied to formal renewable energy targets, plant throughput becomes less discretionary and more embedded in public infrastructure planning. This also creates an opening for industrial buyers that need traceable low-carbon electricity or certificates to support factory decarbonization claims. The result is that the Southeast Asia waste-to-energy market is gaining support from both public utility demand and private sustainability demand.

Landfill Closure Mandates Creating Captive Feedstock for New Plants

Jakarta's Bantargebang landfill has accumulated 55 million tonnes of waste since 1989, and nearby communities have reported 40% higher asthma prevalence and 72% higher diarrheal incidence, which has turned landfill pressure into a public-health issue as much as a waste issue. That matters because landfill closure is no longer a distant environmental goal in the region's largest urban markets. Indonesia's Ministry of Environment also identified 343 open-dumping sites whose closure could unlock annual waste-to-energy economic potential worth IDR 26.5 trillion, equal to USD 1.5 billion. In Malaysia, Penang closed the Jelutong landfill in November 2025 after 40 years of operation, which added practical momentum to alternative treatment planning. Once landfill closures start to bind, plant operators gain a more secure residual waste stream within defined catchment areas. This improves long-run utilization and strengthens project economics across the Southeast Asia waste-to-energy market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront capex and long payback periods | -1.8% | Most acute in Indonesia, the Philippines, and Vietnam for greenfield projects | Long term (≥ 4 years) |

| Public opposition over dioxin and NOx emissions | -1.2% | Strongest in Indonesia and Thailand | Medium term (2-4 years) |

| Low-calorific, high-moisture feedstock variability | -0.9% | Indonesia, the Philippines, and early-stage Vietnam | Short term (≤ 2 years) to Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Capex Strains Project Bankability Across the Region

Recent project announcements show that 1,000 tpd class plants in the region still require capital commitments in the hundreds of millions of dollars, which keeps financing barriers high for new entrants. Malaysia's Sungai Udang facility carries a project cost of RM660 million, equal to USD 149 million, for 1,056 tpd and 22 MW under a 34-year concession. Hanoi's Phase 2 expansion at Soc Son adds 1,600 tpd and carries an investment of VND 5,830 billion, equal to USD 239 million. Long concession terms help revenue visibility, but lenders remain cautious when tariffs do not adjust for inflation over the operating life of the asset. Pretreatment systems, emissions controls, and construction risk raise the entry cost even before a plant reaches stable utilization. This means the Southeast Asia waste-to-energy market still favors sponsors with stronger balance sheets, better contractor control, and access to sovereign or multilateral support.

Feedstock Variability Imposes Hidden Technology Adaptation Costs

Municipal waste streams in Indonesia and the Philippines carry high organic content and high moisture, which lowers calorific value and makes stable combustion harder to maintain. This creates a mismatch between local waste characteristics and conventional European equipment assumptions, especially when plants are designed around drier and more homogeneous input streams. In Thailand, C&G Environmental Protection adapted Hitachi Zosen Inova stoker technology for local waste conditions, which shows that technology localization is already necessary at a commercial scale. Seasonal swings add another layer of difficulty because wet-season loads can change boiler performance and maintenance cycles inside the same plant. Where regulation does not clearly allocate composition risk, developers and local authorities must settle that issue through direct concession negotiations. This hidden adaptation burden slows replication and raises execution risk across the Southeast Asia waste-to-energy market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Thermal Maintains Scale Advantage as Biological Accelerates

Thermal technology held 62.1% of the Southeast Asia waste-to-energy market share in 2025, which kept it as the dominant route for large urban treatment systems. That lead comes from the fit between grate-furnace incineration and high-throughput municipal waste, especially where project economics depend on continuous intake and firm power offtake. Hanoi's Soc Son facility was already processing 70% of the city's daily household waste when it was inaugurated in October 2025, which shows how well thermal systems can absorb large city waste streams. Thermal plants also benefit from more mature operating models, deeper contractor pools, and a clearer commercial interface with utilities and local authorities.

Biological technology is projected to expand at 14.3% CAGR from 2026 to 2031, making it the fastest-growing technology segment in the Southeast Asia waste-to-energy market. The segment is being driven mainly by palm oil mill effluent projects in Malaysia and Indonesia, where waste streams are concentrated and methane capture is commercially meaningful. Malaysia and Indonesia were expected to produce 80.4 million metric tonnes of crude palm oil in 2025, or 83% of global output, which supports a very large residue base for anaerobic digestion and biogas systems. Yet fewer than 10% of Indonesian palm oil mills had installed anaerobic digestion by early 2026, so growth is starting from a low installed base even though feedstock availability is high. Physical technologies such as refuse-derived fuel production and mechanical biological treatment still support co-firing and recovery pathways, but they remain secondary to thermal and biological routes in the Southeast Asia waste-to-energy industry.

By Waste Type: Municipal Solid Waste Anchors Market as Agricultural Residues Accelerate

Municipal solid waste accounted for 56.4% of the Southeast Asia waste-to-energy market size in 2025, which kept it at the center of project development across the region. This position reflects the direct link between city waste collection systems and government-backed concession models. Indonesia's national programme is targeting 34 cities and 30 agglomeration zones by 2029, with planned waste intake of 33,000 tpd, which reinforces municipal waste as the main volume base for future plants. Industrial waste is also gaining weight in Thailand and Vietnam as environmental compliance standards tighten in industrial parks and export manufacturing zones.

Agricultural and agro-industrial residues are projected to grow at 13.8% CAGR from 2026 to 2031, making them the fastest-growing waste stream in the Southeast Asia waste-to-energy market. The strongest opportunity sits in the palm oil economy, where large volumes of methane-rich residue remain underused. In October 2025, Malaysia's Bioeconomy Corporation signed an MOU with Polaris Bio for a RM700 million network, equal to USD 158 million, of more than 20 Bio-CNG facilities, which highlighted growing commercial interest in residue monetization. The Philippines is also testing decentralized residue conversion, and the Biosfair pilot in Laguna is set to process 1,200 tonnes of organic waste annually while generating 250,000 kWh per year. These projects show that residue-based systems can scale quickly where feedstock is concentrated, and collection logistics are simpler than in mixed municipal waste systems.

By Energy Output: Electricity Prevails While Transport Fuels Reshape Value Chains

Electricity held 52.1% of the Southeast Asia waste-to-energy market size in 2025, which made it the largest output category by a clear margin. The segment benefits from long-term utility contracts, easier settlement structures, and the ability to monetize large volumes through existing grid systems. Hanoi's Soc Son plant processes 5,000 tpd and generates 90 MW, which illustrates the scale advantage of power-oriented waste-to-energy projects in dense urban settings. Singapore's Tuas Nexus Integrated Waste Management Facility will generate 2,565 MWh of electricity daily when fully operational, and that output can meet up to 3% of national electricity demand.

Transport fuels are forecast to grow at 15.8% CAGR from 2026 to 2031, making them the fastest-rising output stream in the Southeast Asia waste-to-energy market. This reflects a shift away from a pure electricity model toward low-carbon fuels that can serve freight, shipping, and industrial users. Indonesia moved from a B40 biodiesel mandate in 2025 to B50 in 2026, which strengthens the wider policy case for renewable fuel pathways from waste and biomass. PT Prakarsa Energi Sejahtera is developing a pyrolysis plant at Benowo landfill in Surabaya that is designed to produce 60 to 70 kiloliters of diesel-equivalent renewable fuel per day, which gives the segment a visible commercial example. This part of the Southeast Asia waste-to-energy industry is still at an earlier stage, but it is broadening the revenue model beyond grid-tied generation alone.

By End-User: Utilities and IPPs Dominate but Transport Fuel Distributors Gain Fastest

Utilities and independent power producers held 57.7% of the Southeast Asia waste-to-energy market share in 2025, which confirms that the dominant commercial model still runs through long-term utility offtake. This segment remains the largest because municipal and national procurement systems are designed around grid dispatch, predictable settlement, and concession-backed power sales. Keppel Infrastructure Trust treated more than 35% of Singapore's municipal incinerable waste in FY2025, diverted 97% of processed waste from landfills, and recovered 6,000 tonnes of scrap metal from bottom ash, which shows how large operators can combine disposal, recovery, and utility-linked monetization in one platform. Industrial captive projects are also expanding in Vietnam and Thailand as manufacturers seek tighter control over waste handling and emissions reporting.

Transport fuel distributors are projected to grow at 15.3% CAGR from 2026 to 2031, making them the fastest-growing end-user group in the Southeast Asia waste-to-energy market. Their growth follows the same change seen in output markets, where bio-LNG, bio-SNG, and renewable liquid fuels are moving toward commercial relevance. Demand from road freight and shipping is especially important because these buyers need compliant low-carbon fuel options at usable volumes. In Thailand, Gulf Waste to Energy Holdings secured ADB-backed financing for 12 industrial plants with 96 MW of contracted capacity, which shows that non-utility commercial pathways can still reach financial close when project structures are strong. Over time, this wider buyer base should make the Southeast Asia waste-to-energy market less dependent on a single end-user channel.

Geography Analysis

Indonesia accounted for 31.6% of the Southeast Asia waste-to-energy market size in 2025, which kept it as the largest country market in the region. The current pipeline centers on 34 planned plants across 34 cities, and groundbreaking for 5 priority agglomerations was targeted for June 2026, with each facility designed to process more than 1,000 tpd. The Indonesian buildout is important because it shifts the market from isolated city projects toward a nationally coordinated program. Vietnam is projected to grow at 14.8% CAGR from 2026 to 2031, making it the fastest-growing geography in the Southeast Asia waste-to-energy market. Hanoi broke ground on the Nui Thoong plant in May 2026 with a planned processing capacity of 2,000 tpd and a generation capacity of 45 MW, while the city also advanced the next phase of Soc Son to lift total output to 135 MW when complete.

Singapore has the region's most mature waste-to-energy ecosystem, with operational incineration capacity already embedded in national waste management. When fully operational, Tuas Nexus will process 5,800 tpd and generate 2,565 MWh of electricity each day, which will reduce landfill loads by 30% from 2018 levels. The market also showed continued depth in May 2026 when AECOM, Binnies, and Ramboll were appointed as owners' engineer for Phase 2 of the facility. Malaysia is moving from pilot activity to a broader program, led by the Sungai Udang PPP plant and a parallel push into Bio-CNG linked to palm waste.

Thailand stands out for the breadth of its activity across both municipal and industrial waste streams, which gives it a more diversified demand base than several regional peers. In February 2026, ADB signed a THB 16.6 billion financing package, equal to USD 521.5 million, for 12 industrial waste-to-energy plants with 96 MW of contracted capacity, marking Thailand's first large-scale industrial buildout in this field. The Philippines remains at an earlier stage, but decentralized digestion pilots and formal auction steps are beginning to create a clearer development route. The rest of Southeast Asia, including Myanmar, Cambodia, and parts of the Mekong sub-region, still has limited plant infrastructure and early-stage policy support. This leaves the Southeast Asia waste-to-energy market with a mix of mature urban systems, accelerated buildout markets, and long-horizon frontier opportunities.

Competitive Landscape

The Southeast Asia waste-to-energy market is moderately fragmented, and competitive advantage is shaped more by technology strength and execution capability than by regional volume alone. Japanese OEMs retain a durable position in high-throughput grate-furnace systems, especially in Singapore and Thailand, where reliability and emissions performance carry more weight. Keppel's infrastructure business shows the value of integrated operating models, with FY2025 recurring income at USD 703 million and decarbonization and sustainability solutions EBITDA up 32% year over year to USD 101.35 million. These results matter because they show that operators with waste treatment, energy, and resource recovery capabilities can earn from more than gate fees alone. In practical terms, the market rewards companies that can keep plant performance high across long concession periods.

Chinese developers are expanding aggressively in Vietnam and Indonesia, using domestic EPC scale and manufacturing depth to offer sharper pricing and faster rollout. That strategy is visible in Indonesia's January 2026 partnerships between BPI Danantara and Wangneng Environment Co. and Zhejiang Weiming Environment Protection Co. for projects in Bekasi and Denpasar. European firms still hold an important position, but their role is moving toward emissions-control engineering, owner-engineer mandates, and specialized process support. The May 2026 appointment of AECOM, Binnies, and Ramboll for Tuas Nexus Phase 2 is a clear example of that higher-value positioning.

White-space opportunities are strongest in industrial gasification and pyrolysis, modular biological treatment for agricultural residues, and transport-fuel conversion pathways. These areas are attractive because they fit waste streams that are harder to monetize through traditional grid-linked incineration alone. Carbon credit monetization is also becoming more relevant, where methane capture or certified bioenergy pathways can add a second revenue stream. In Malaysia, Monsoon Carbon's Verra-registered program was already generating credits that traded at USD 10 per tonne of CO2e, which suggests that certification can materially improve project economics for early movers. Overall, the Southeast Asia waste-to-energy market favors sponsors that can combine feedstock control, financing, technology adaptation, and compliance management within a single delivery platform.

Southeast Asia Waste-to-Energy Industry Leaders

Mitsubishi Heavy Industries Ltd

Keppel Infrastructure Holdings

Hitachi Zosen Corp

China Everbright Environment Group

Veolia Environment SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: The Xuan Mai Urban Environment Company and Green Marble JSC have commenced construction of the Nui Thoong high-tech waste treatment and waste-to-energy plant in Xuan Mai commune, Hanoi, with a total investment of approximately USD 200 million. The facility is designed to process 2,000 tonnes of waste daily and generate 45 MW of electricity for the national grid. This project marks the first high-tech waste-to-energy plant in southwestern Hanoi, addressing the long-standing absence of large-scale solid waste treatment facilities in the area.

- May 2026: AECOM, Binnies, and Ramboll joint venture was appointed by Singapore's National Environment Agency (NEA) as owners' engineer for Phase 2 of the Tuas Nexus Integrated Waste Management Facility, extending a multi-year engineering mandate that underpins Singapore's USD 1.5 billion+ flagship WtE infrastructure programme. The appointment follows prior Phase 1 works and positions the JV to oversee 2,900 tpd additional WtE capacity, including future carbon capture integration at the site

- April 2026: Hanoi commenced Phase 2 expansion of the Soc Son Waste-to-Energy Plant, adding 1,600 tpd of capacity to treat previously landfilled waste and increasing total output to 135 MW; total investment for this expansion is approximately VND 5,830 billion (USD 239 million). Full plant completion is targeted for Q4 2027, making Soc Son one of the largest WtE facilities globally by installed capacity.

- March 2026: In Da Nang City, the Vietnam Bank for Agriculture and Rural Development (Agribank) and Vietnam Environment Joint Stock Company (a member of Amaccao Group) conducted a Credit Contract Signing Ceremony for the implementation of the Solid Waste Incineration Plant project in Khanh Son, a significant environmental initiative for the city.

Southeast Asia Waste-to-Energy Market Report Scope

Waste-to-energy (WtE) refers to converting various waste materials into usable forms of energy, such as electricity, heat, or fuel. It involves the application of different technologies to extract energy from waste, thereby reducing the volume of waste that needs to be landfilled or incinerated. The most common waste materials used in waste-to-energy processes include municipal solid waste (MSW), biomass, agricultural residues, industrial waste, and wastewater sludge. These waste materials are typically rich in organic content, which can be harnessed for energy generation.

The Southeast Asia Waste-to-Energy Market is segmented into technology, waste type, energy output, end-user, and geography. By technology, the market is segmented into physical, thermal, and biological technologies. The physical segment includes refuse-derived fuel and mechanical-biological treatment systems. The thermal segment includes incineration/combustion, gasification, pyrolysis, and plasma-arc technologies. The biological segment includes anaerobic digestion and fermentation technologies. By waste type, the market is segmented into municipal solid waste, industrial waste, agricultural and agro-industrial residues, sewage sludge, and others, including commercial, construction, and hazardous waste. By energy output, the market is segmented into electricity, heat, combined heat and power (CHP), and transportation fuels including bio-SNG, bio-LNG, and ethanol. By end-user, the market is segmented into utilities and independent power producers (IPPs), industrial captive plants, district heating operators, and transport fuel distributors. The report also covers the market size and forecasts for the Southeast Asia waste-to-energy market in 6 countries across the region. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

By Technology

| Physical (Refuse-Derived Fuel, Mechanical Biological Treatment) |

| Thermal (Incineration/Combustion, Gasification, Pyrolysis and Plasma-Arc) |

| Biological (Anaerobic Digestion, Fermentation) |

By Waste Type

| Municipal Solid Waste |

| Industrial Waste |

| Agricultural and Agro-industrial Residues |

| Sewage Sludge |

| Others (Commercial, Construction, Hazardous) |

By Energy Output

| Electricity |

| Heat |

| Combined Heat and Power (CHP) |

| Transportation Fuels (Bio-SNG, Bio-LNG, Ethanol) |

By End-user

| Utilities and IPPs |

| Industrial Captive Plants |

| District Heating Operators |

| Transport Fuel Distributors |

By Geography

| Indonesia |

| Malaysia |

| Thailand |

| Singapore |

| Vietnam |

| Philippines |

| Rest of Southeast Asia |

| By Technology | Physical (Refuse-Derived Fuel, Mechanical Biological Treatment) |

| Thermal (Incineration/Combustion, Gasification, Pyrolysis and Plasma-Arc) | |

| Biological (Anaerobic Digestion, Fermentation) | |

| By Waste Type | Municipal Solid Waste |

| Industrial Waste | |

| Agricultural and Agro-industrial Residues | |

| Sewage Sludge | |

| Others (Commercial, Construction, Hazardous) | |

| By Energy Output | Electricity |

| Heat | |

| Combined Heat and Power (CHP) | |

| Transportation Fuels (Bio-SNG, Bio-LNG, Ethanol) | |

| By End-user | Utilities and IPPs |

| Industrial Captive Plants | |

| District Heating Operators | |

| Transport Fuel Distributors | |

| By Geography | Indonesia |

| Malaysia | |

| Thailand | |

| Singapore | |

| Vietnam | |

| Philippines | |

| Rest of Southeast Asia |

Key Questions Answered in the Report

What is the current outlook for waste-to-energy in Southeast Asia?

The Southeast Asia waste-to-energy market was valued at USD 4.64 billion in 2025, reached USD 5.22 billion in 2026, and is forecast to reach USD 9.48 billion by 2031 at a 12.65% CAGR.

Which country leads regional demand?

Indonesia held the largest country share at 31.6% in 2025, supported by a nationally coordinated buildout program across multiple cities.

Which technology is expanding fastest?

Thermal technology remained the largest segment in 2025 with 62.1%, but biological technology is projected to grow fastest at 14.3% through 2031.

Why are transport fuels gaining attention from investors?

Transport fuels are forecast to grow at 15.8% CAGR through 2031 because policy support, shipping demand, and renewable fuel needs are creating a wider revenue base than electricity alone.

What is the main financial challenge for project developers?

The biggest hurdle remains high upfront capital cost, since large plants still require investments in the hundreds of millions of USD and depend on long concession periods to recover capital.

Which end-user group dominates project revenues today?

Utilities and independent power producers led with 57.7% in 2025 because most large projects are still structured around long-term grid offtake and utility-linked concession models.

Page last updated on: