Southeast Asia Telematics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

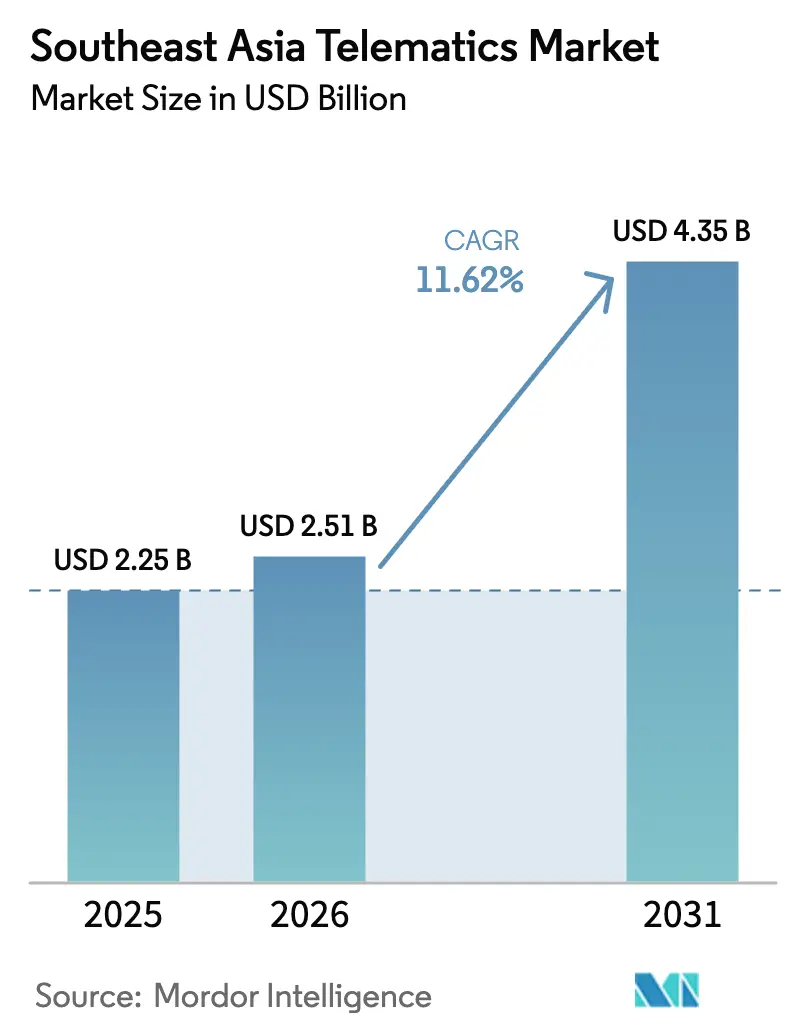

| Base Year Market Size (2025) | USD 2.25 Billion |

| Market Size (2026) | USD 2.51 Billion |

| Market Size (2031) | USD 4.35 Billion |

| Growth Rate (2026 - 2031) | 11.62% CAGR |

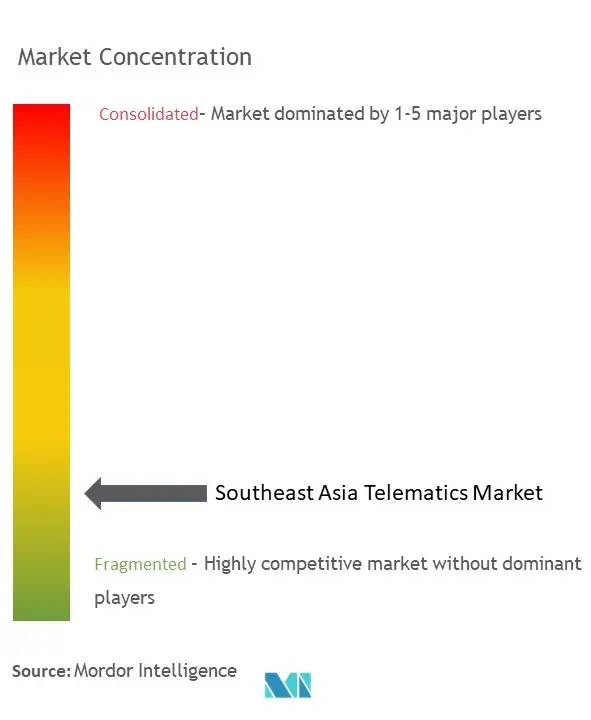

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Southeast Asia Telematics Market Analysis by Mordor Intelligence

The Southeast Asia telematics market size was valued at USD 2.25 billion in 2025 and estimated to grow from USD 2.51 billion in 2026 to reach USD 4.35 billion by 2031, at a CAGR of 11.62% during the forecast period (2026-2031). Product demand is pulling ahead of earlier projections as regulators tighten fuel-economy and emissions rules, e-commerce drives record parcel volumes, and 4G/5G coverage reaches secondary cities. Thailand’s 30@30 policy for electric-vehicle production, Indonesia’s target of 1 million EVs by 2035, and the ASEAN Fuel Economy Roadmap’s 26% fleet-wide fuel-savings mandate together set a compelling compliance timetable that makes telematics a non-negotiable fleet investment. The region’s telecom operators are rolling out low-latency 5G, unlocking predictive maintenance, V2X applications, and advanced driver-assistance add-ons. Multinational and local suppliers continue to enter the market despite hardware-cost inflation, resulting in a fragmented but fast-maturing competitive field.

Key Report Takeaways

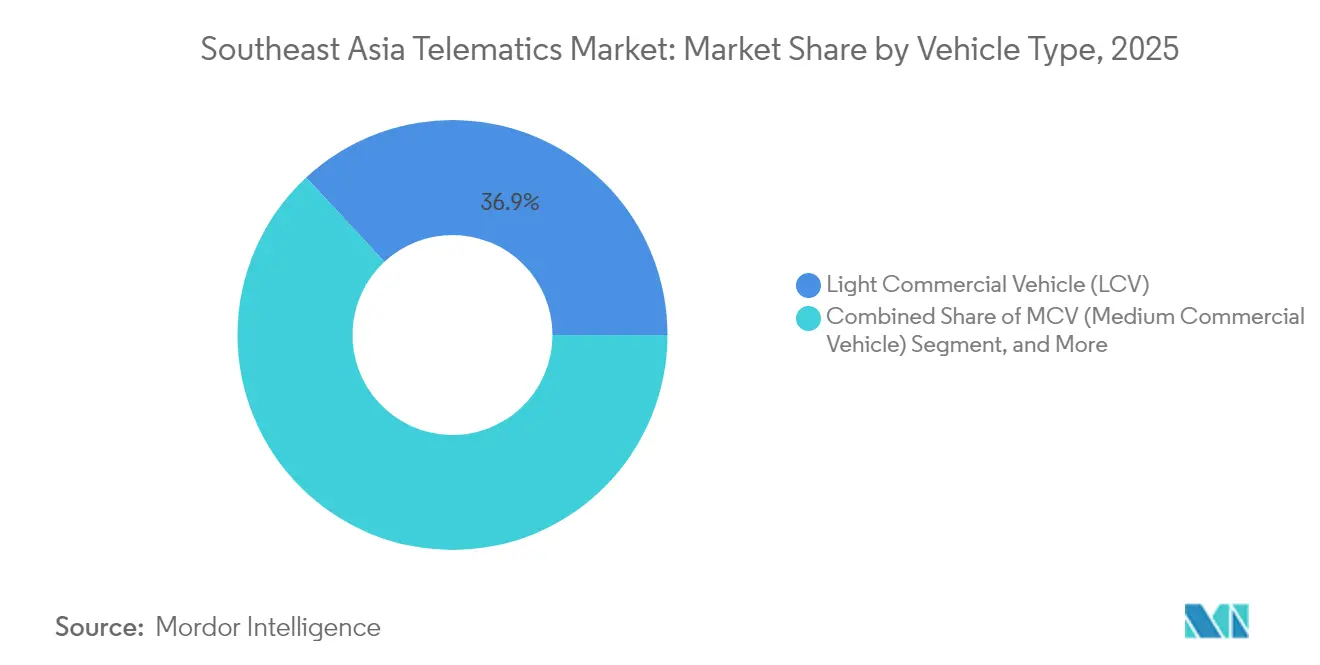

- By vehicle type, Light Commercial Vehicles led with 36.92% revenue share in 2025; Two-Wheelers are forecast to expand at a 12.05% CAGR through 2031.

- By solution, Fleet and Vehicle Management held 41.55% revenue share in 2025, while Telematics Insurance is projected to grow at 13.14% CAGR to 2031.

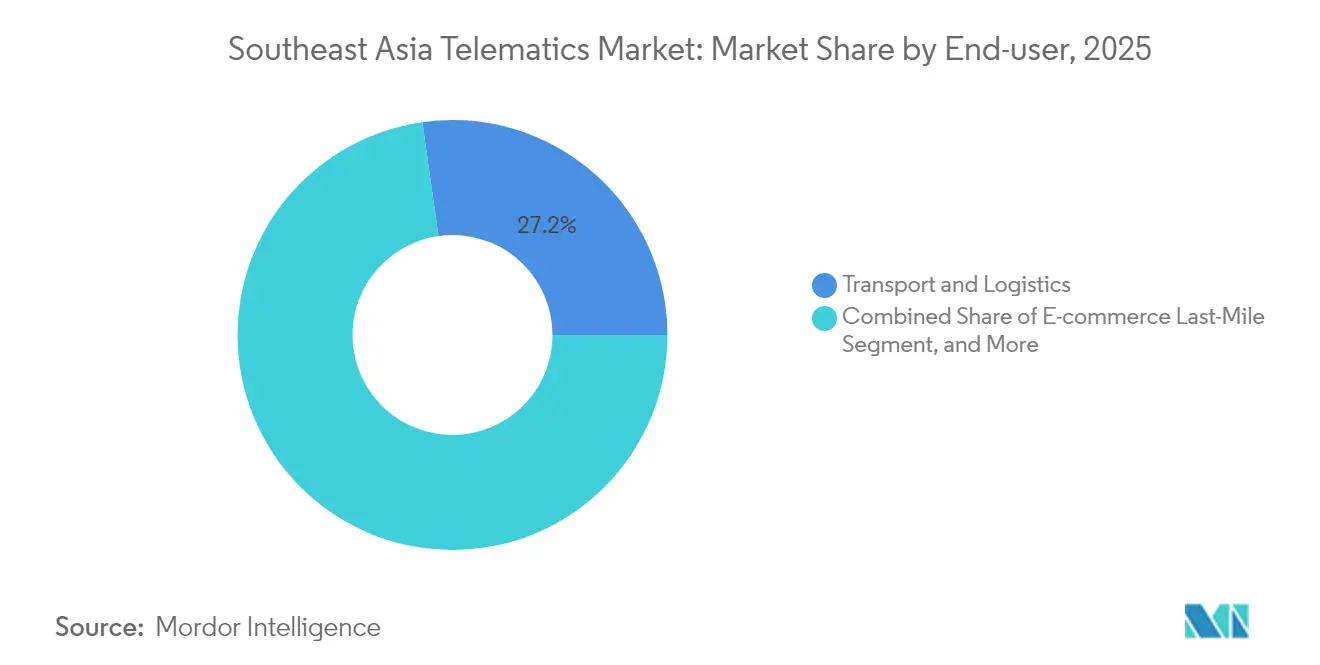

- By end-user industry, Transport and Logistics captured 27.24% revenue share in 2025, whereas E-commerce Last-Mile delivery is advancing at a 12.42% CAGR through 2031.

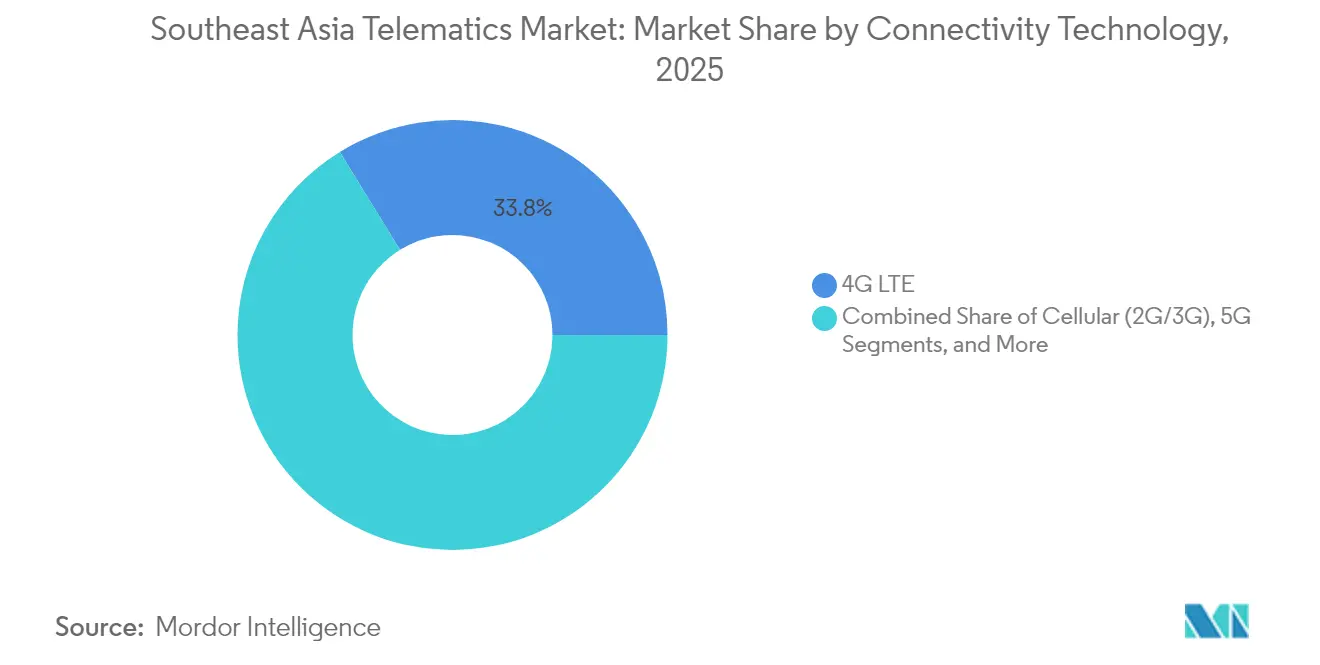

- By connectivity technology, 4G LTE dominated with 33.78% revenue share in 2025; 5G is set to rise at a 13.47% CAGR through 2031.

- By country, Thailand commanded 22.48% revenue share in 2025, while Vietnam is forecast to register the fastest 12.74% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Southeast Asia Telematics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Four-tier safety and emissions mandates drive adoption | + 2.8% | Global, strongest in Thailand and Indonesia | Medium term (2-4 years) |

| E-commerce last-mile boom fuels LCV telematics | + 3.2% | ASEAN core, spill-over to Philippines | Short term (≤ 2 years) |

| 4G/5G rollout enables real-time data services | + 2.1% | Singapore and Malaysia leading, regional expansion | Long term (≥ 4 years) |

| Fleet cost-reduction amid diesel volatility and carbon tax | + 1.9% | Thailand, Indonesia, Malaysia | Medium term (2-4 years) |

| Mileage-based road-tax pilots (Indonesia) | + 1.2% | National, with early gains in Jakarta, Surabaya | Long term (≥ 4 years) |

| Vietnam PAYD insurance-telco alliances | + 0.8% | National, expanding to regional markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Four-tier Safety and Emissions Mandates Drive Adoption

Governments across Southeast Asia are layering fuel-economy targets, CO₂-based taxes, local-content rules, and zero-emission commitments, turning telematics from an efficiency option into a regulatory requirement. The ASEAN Fuel Economy Roadmap insists on a 26% reduction in average fleet fuel consumption by 2025, obliging operators to monitor vehicle usage in real time.[1]ASEAN Secretariat, “ASEAN Fuel Economy Roadmap for the Transport Sector,” asean.orgThailand’s excise system rewards CO₂ cuts, while Indonesia’s local-content thresholds steer buyers toward domestically integrated telematics modules. Emerging hydrogen and biofuel pilots under the Asia Zero Emission Community also require granular operating data for compliance, further embedding telematics in fleet workflows. As a result, adoption no longer hinges on ROI alone; fleets must connect or face non-compliance penalties, sustaining double-digit growth for the Southeast Asia telematics market.

E-commerce Last-mile Boom Fuels LCV Telematics

Online retail platforms continue to set delivery-speed benchmarks that require point-to-point visibility from warehouse to doorstep. Grab’s super-app services in 800+ cities rely on connected LCV and two-wheeler fleets to hit sub-one-hour delivery windows. Malaysia’s digital economy already contributed 22.6% of GDP in 2020 and is expanding 8.5% per year, pressuring logistics providers to upgrade tracking systems.[2]Huawei, “Malaysia’s Digital Economy Progress Update 2024,” huawei.comVietnam’s electric two-wheelers crossed 9% market share in 2024, adding battery-health and range-management datasets to fleet dashboards. These dynamics underpin sustained demand for real-time routing, driver-behavior scoring, and charge-cycle analytics, all of which expand the Southeast Asia telematics market.

4G/5G Rollout Enables Real-time Data Services

Singapore’s Tuas Port went live with 5G slices for mission-critical crane and AGV operations, showcasing how low-latency networks elevate telematics from reactive tracking to predictive orchestration.[3]Singtel, “Singtel, Ericsson Collaborate to Deploy 5G at Tuas Port,” singtel.comThe ASEAN Digital Masterplan calls for regional 5G coverage of at least 35% of the population by 2025, with spectrum-sharing frameworks accelerating rollouts. Malaysia’s ambition to become the ASEAN Digital Capital is pulling forward 5G timelines, giving fleets access to V2X services and over-the-air OTA updates. As coverage grows, edge-analytics and AI-based maintenance models will unlock new revenue streams, broadening the addressable base for the Southeast Asia telematics market.

Fleet Cost-reduction Amid Diesel Volatility and Carbon Tax

Fuel makes up more than 30% of many fleet budgets, and diesel price swings now combine with early-stage carbon taxes to squeeze margins. Thailand links its fuel-economy rules to excise rebates that favor connected vehicles able to demonstrate lower CO₂ per kilometer. The International Transport Forum shows declining fuel-tax proceeds as EV adoption rises, pushing governments toward distance-based tolling that depends on telematics odometer feeds.[4]International Transport Forum, “Distance-based Road-Charging Study,” internationaltransportforum.orgIndonesia’s biofuel mandates similarly compel operators to log blend ratios and route data to claim fiscal incentives. These economic levers make connected dashboards central to cost control, lifting penetration rates across segments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront hardware and integration cost | -1.8% | Regional, acute in smaller markets | Short term (≤ 2 years) |

| Patchy cross-border network roaming | -1.2% | Cross-border corridors, rural areas | Medium term (2-4 years) |

| Data-sovereignty bottlenecks on telemetry export | -0.9% | Vietnam, Indonesia, Thailand | Long term (≥ 4 years) |

| Shortage of certified installers outside tier-1 cities | -0.7% | Rural and secondary urban areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Hardware and Integration Cost

Global chip shortages linger, with automotive semiconductor lead times stretching to 50 weeks, inflating device prices and limiting SKU availability. Fleet operators face a widening cost-of-capital gap: larger firms lock multi-year supply contracts, while SMEs postpone deployments or opt for stripped-down feature sets. Production shortfalls hit 8.2 million vehicles in 2021 and still ripple through 2025 order books, keeping average hardware ASPs elevated and dampening the Southeast Asia telematics market’s near-term growth trajectory.

Data-sovereignty Bottlenecks on Telemetry Export

Vietnam’s personal-data decree forces foreign providers to process and store information domestically, adding data-center CapEx and operational overheads. Indonesia and Thailand impose sector-specific localization clauses that require complex onboarding workflows for cross-border fleets. The resulting patchwork erodes scale efficiencies, obliges country-specific device SKUs, and raises compliance risk, weighing on market expansion despite surging demand.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Commercial Fleets Drive Electrification

Light Commercial Vehicles commanded 36.92% of the Southeast Asia telematics market size in 2025, anchored in parcel and grocery delivery runs that demand granular route analytics. Operators deploy camera-based driver scoring, cold-chain temperature probes, and ePOD integrations to hit tight service-level agreements. Two-Wheelers are registering the fastest 12.05% CAGR to 2031 as Vietnam and Indonesia electrify ride-hailing and courier fleets, adding battery state-of-charge alerts and swap-station mapping features.

Zapp’s micro-factory in Thailand can build 21,500 electric motorcycles per year, each shipping with CAN-bus ports for real-time power-train data. For Medium Commercial Vehicles in mining and construction, uptime dashboards and geofencing ensure equipment-site compliance. Passenger Cars round out demand as insurers bundle connected-policy discounts and ride-sharing platforms fit aftermarket OBD dongles. Collectively these dynamics reinforce the Southeast Asia telematics industry’s multi-segment nature, keeping solution providers agile across payload classes.

By Solution: Insurance Innovation Accelerates Growth

Fleet and Vehicle Management accounted for 41.55% of the Southeast Asia telematics market size in 2025, offering core GPS tracking, maintenance scheduling, and driver alerts. Adoption is nearly universal among long-haul and regional haul operators seeking 3%–5% fuel-burn cuts per vehicle. Telematics Insurance, growing at 13.14% CAGR, is redefining risk pricing by aligning premiums with behavioral scores and mileage, a shift highlighted by NTUC Income’s pay-as-you-drive launch with Carro. MS&AD’s 1.85 million connected policies expand the actuarial dataset, enabling AI to benchmark risk corridors. These use cases underscore how analytics extensions not hardware alone differentiate vendors in the Southeast Asia telematics industry.

Location-Based Services tie into mapping and dispatch platforms, while Predictive Maintenance gains momentum through edge-AI fault detection. Vendors that pull usage, vibration, and fluid-temperature data into cloud ML models reduce unplanned downtime and enhance residual-value calculations. Competitive advantage now lies in API openness, over-the-air feature upgrades, and integration speed with third-party TMS or ERP suites.

By End-user Industry: E-commerce Reshapes Logistics

Transport and Logistics contributed 27.24% of the Southeast Asia telematics market size in 2025, spanning trucking, public transit, and bulk commodity haulage. Route-planning engines cut empty miles, while driver coaching reduces harsh-braking events by 15%–20%. E-commerce Last-Mile operations, expanding at a 12.42% CAGR, overlay parcel-level ETA push notifications and dock-door sequencing to trim dwell time. Grab’s multi-modal network exemplifies these blended use cases, requiring unified dashboards across taxis, bikes, and delivery vans.

Public Transportation agencies deploy CCTV-enabled telematics for real-time passenger counts and accident forensics. Construction and Mining rely on RFID zone alerts to prevent blind-spot collisions, whereas Oil and Gas fleets use sensor-verified journey-management plans to satisfy hazardous-goods regulations. Each vertical adds proprietary data layers, making configurable rule engines a must-have for vendors scaling within the Southeast Asia telematics industry.

By Connectivity Technology: 5G Transformation Accelerates

4G LTE represented 33.78% of the Southeast Asia telematics market size in 2025, giving fleets ubiquitous SIM coverage at sustainable data tariffs. Yet 5G, advancing at a 13.47% CAGR, is set to handle machine-vision uploads, over-the-air firmware packages, and V2X safety pings. Ericsson’s research shows software-defined vehicles generate 30 times more data than traditional telematics boxes, necessitating dedicated network slices and edge-compute gateways.

Legacy 2G/3G sunsets push operators in rural corridors to adopt multibearer modems that fall back to NB-IoT or satellite, especially for cross-border long-haul into Laos or Myanmar. Satellite links remain indispensable for forestry, mining, and maritime use cases, though price-per-megabyte keeps them niche. The winners are chipset suppliers and platform vendors that abstract these heterogeneous pipes behind a unified device-management stack and predictive-billing engine.

Geography Analysis

Thailand’s 22.48% revenue lead stems from its deep automotive supply chain and supportive CO₂-linked excise structure that rewards connected fleets. Its 30@30 target to produce 30% EVs by 2030 layers on battery-health monitoring requirements, giving telematics extra pull across OEM assembly lines and retrofits alike. The installed base surged from 6 million passenger and LCV units in 2000 to nearly 19 million in 2022, broadening retrofit opportunities at dealerships and service centers.

Indonesia ranks second on volume, leveraging a domestic fleet exceeding 23 million vehicles and a production goal of 1 million EVs by 2035 that necessitates local telematics modules for content-rule compliance. An Omnibus Law easing foreign-investment caps spurs joint ventures, while mileage-based road-tax pilots in Jakarta and Surabaya validate usage-based charging models reliant on OBD mileage feeds. Malaysia and Singapore punch above fleet size, thanks to advanced 5G coverage and digital-economy incentives such as Malaysia’s Digital Nasional Berhad wholesale model that lowers connectivity barriers.

Vietnam posts the fastest 12.74% CAGR from 2026 to 2031 as the government positions ICT as a growth pillar, helping the country leap from rudimentary copper networks in 1986 to fiber and 5G backbones today. Electric two-wheelers hit 250,000 sales in 2024, growing the addressable pool for battery-state dashboards and pay-as-you-charge subscriptions iea.org. Data-localization rules complicate cross-border dashboards, yet they also tilt enterprise buyers toward domestic providers, accelerating a home-grown ecosystem. The Philippines plus smaller ASEAN markets continue to record double-digit growth but await clearer regulatory alignment before large-scale telematics rollouts reach rural routes.

Competitive Landscape

The Southeast Asia telematics market remains moderately fragmented: no single vendor exceeds a 10% revenue share region-wide, and at least 25 local system integrators compete with global brands on cost and localization. Cross-border players form alliances with telecom operators to gain SIM bulk rates and on-the-ground installer networks; CelcomDigi’s i-Fleet is a case in point for Malaysia. Hardware vendors differentiate on AI accelerators and multi-GNSS chipsets, while platform specialists emphasize open APIs that plug into TMS and ERP suites in less than two weeks.

Technology maturity, not device price alone, is becoming the decisive factor. Proof points include AROBS Transilvania’s TachoAnalytics, which automates driver-hour compliance across EU and ASEAN tachograph standards and is now ported into Thai and Indonesian time-zone rules. Predictive-maintenance patents that integrate tire pressure, humidity, and shock data give early-warning windows of 1,000–1,500 km before component failure [google.com/patents/US202400].

Strategic moves in 2024-2025 reveal three patterns:

- Telecom–telematics partnerships (e.g., Singtel–Ericsson, CelcomDigi–iFleet) accelerate 5G monetization while lowering customer-acquisition costs.

- Insurer alliances (NTUC–Carro, MS&AD data-driven underwriting) open new premium pools.

- Hardware start-ups place micro-factories (Zapp in Thailand) near OEM clusters, shortening supply chains and qualifying for local-content incentives. Together these actions sustain innovation velocity and keep the Southeast Asia telematics market highly dynamic.

Southeast Asia Telematics Industry Leaders

Foxlogger

Onelink Technology

Foxlogger

DTC Enterprise

Tramigo Singapore

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Trimble invested USD 10 million in Xona Space Systems to integrate high-accuracy correction signals with the PULSAR navigation service, targeting commercial fleets that operate in cellular dead zones.

- February 2025: Olam Group sold a 44.58% stake in Olam Agri to SALIC for USD 1.78 billion, freeing capital for digital fleet-optimization rollouts across its agrilogistics network.

- November 2024: Singtel and Ericsson began deploying 5G at Singapore’s Tuas Port to support full automation and real-time asset tracking.

- April 2025: AROBS Transilvania Software launched TachoAnalytics, extending its TrackGPS brand into advanced driver-hour analytics.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Southeast Asian telematics market as revenue generated from hardware-enabled, network-connected solutions fitted to light, medium, and heavy commercial vehicles for tracking, diagnostics, driver behavior, and fleet automation. Devices covered include GPS trackers, OBD dongles, back-boxes, and embedded telematics control units shipped through OEM and aftermarket channels.

Scope Exclusion: Passenger car infotainment systems and smartphone-only tracking apps with no vehicle interface are excluded.

Segmentation Overview

- By Vehicle Type

- Light Commercial Vehicle (LCV)

- Medium Commercial Vehicle (MCV)

- Passenger Cars

- Others

- By Solution

- Fleet/Vehicle Management

- Location-Based Services

- Telematics Insurance

- Predictive Maintenance

- Others

- By End-user Industry

- Transport and Logistics

- E-commerce Last-Mile

- Public Transportation

- Construction and Mining

- Oil and Gas

- Others

- By Connectivity Technology

- Cellular (2G/3G)

- 4G LTE

- 5G

- Satellite

- Others

- By Country

- Thailand

- Indonesia

- Malaysia

- Singapore

- Vietnam

- Rest of Southeast Asia

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts conducted structured interviews and surveys with fleet managers, aftermarket installers, regional telco MVNOs, and usage-based insurers across Indonesia, Thailand, Vietnam, and Singapore. Insights on realistic device penetration, typical service fees, and deployment bottlenecks closed data gaps and aligned model assumptions with on-ground realities.

Desk Research

We collect foundational numbers from transport ministries' vehicle registration ledgers, ASEAN Automotive Federation statistics, customs import data for positioning hardware, and 4G coverage releases by national telecom regulators. Analysts then mine peer-reviewed SAE papers on device lifecycles, pull patent sets through Questel, and follow fleet contract awards via Dow Jones Factiva and D&B Hoovers financials to map supplier flows and pricing signals.

Company filings, investor decks, and trade association white papers such as those from the Chartered Institute of Logistics provide further context that rounds out supply-demand dynamics.

The sources named are illustrative, and many additional materials fed our desk research, validation, and clarifications.

Market-Sizing & Forecasting

A top-down build begins with the active commercial vehicle parc in each country, multiplied by verified telematics penetration and average recurring revenue, while selective bottom-up cross-checks of control-unit shipments and sampled ASPs fine-tune totals. Key variables like new LCV registrations, 4G SIM activation growth, diesel price index movements, e-commerce parcel volumes, and statutory GPS mandates shape both base year and outlook.

Forecasts rely on a multivariate regression blended with scenario analysis, capturing step changes when 5G rollouts or carbon-pricing rules accelerate adoption. Where hard shipment data is thin, regional analogs are adjusted for fleet age and income elasticity, then revalidated with primary respondents before finalization.

Data Validation & Update Cycle

Our team runs variance screens against historical series and cross-market ratios, with anomalies resolved through secondary queries or fresh interviews before sign-off. Reports refresh annually, and interim updates are triggered by material events such as new regulatory mandates or major telco-OEM partnerships.

Why Mordor's Southeast Asia Telematics Baseline Commands Reliability

Published estimates often diverge because firms frame scope, conversion rates, and refresh timing in different ways.

Some publishers bundle passenger car or APAC-wide revenues; others assume uniform 5G penetration or aggressive price escalation.

Mordor Intelligence focuses strictly on commercial-vehicle telematics revenue, applies transparent unit mixes, and updates currency and macro inputs each cycle, producing a balanced figure decision-makers can trust.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.25 billion (2025) | Mordor Intelligence | N/A |

| USD 4.50 billion (2025) | Regional Consultancy A | Includes passenger cars and assumes uniform 5G coverage |

| USD 70.13 billion (2024) | Global Consultancy B | Aggregates wider APAC scope and uses single-year ASP inflation |

This comparison shows that when scope alignment and transparent variables are enforced, our disciplined approach delivers a repeatable, verifiable baseline for strategic planning.

Key Questions Answered in the Report

What is the current value of the Southeast Asia vehicle telematics market?

The market stands at USD 2.51 billion in 2026 and is projected to reach USD 4.35 billion by 2031.

Which vehicle segment accounts for the largest share?

Light Commercial Vehicles hold the lead with 36.92% of 2025 revenue, reflecting last-mile delivery growth.

How fast is telematics insurance growing in the region?

Telematics Insurance is set to expand at a 13.14% CAGR through 2031, driven by pay-as-you-drive models.

Why is Vietnam the fastest-growing geography?

Robust ICT investment, 250,000 electric two-wheeler sales in 2024, and supportive digital policies push Vietnam to a 12.74% CAGR.

Page last updated on: