Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

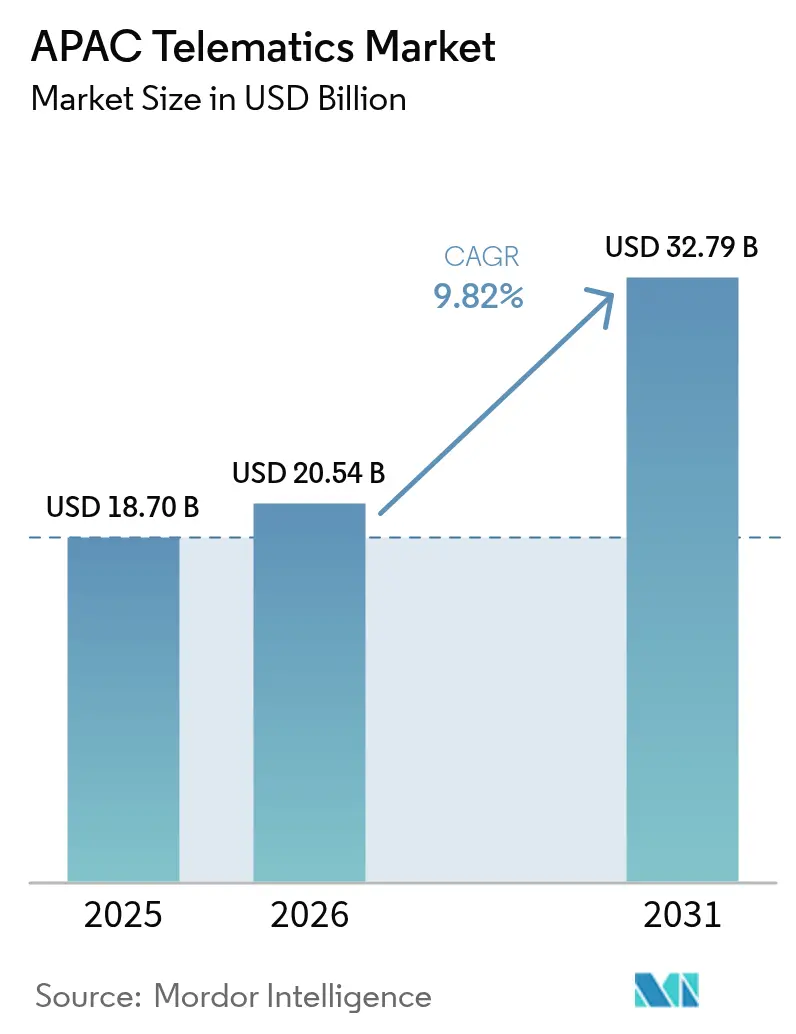

| Base Year Market Size (2025) | USD 18.70 Billion |

| Market Size (2026) | USD 20.54 Billion |

| Market Size (2031) | USD 32.79 Billion |

| Growth Rate (2026 - 2031) | 9.82% CAGR |

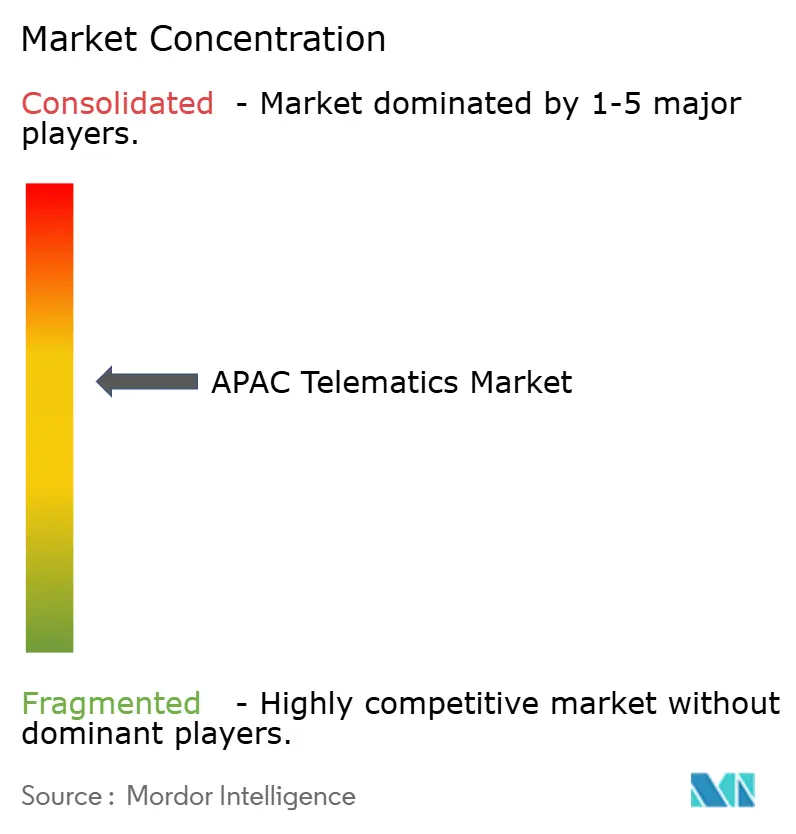

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

APAC Telematics Market Analysis by Mordor Intelligence

The APAC Telematics Market size was valued at USD 18.70 billion in 2025 and estimated to grow from USD 20.54 billion in 2026 to reach USD 32.79 billion by 2031, at a CAGR of 9.82% during the forecast period (2026-2031). The robust trajectory stems from national digital-mobility programs that push connected-vehicle penetration across commercial fleets, regulatory mandates such as India’s AIS-140, and sustained e-commerce parcel growth that requires real-time fleet visibility. China’s leadership in factory-installed connectivity modules, an accelerating shift toward usage-based insurance, and ongoing smart-city pilots further reinforce demand for sophisticated data platforms. OEMs and fintechs are bundling telematics with leasing products to ease upfront hardware costs, while semiconductor supply-chain resilience initiatives help vendors buffer against the periodic shortages that constrained deliveries in 2024.

Key Report Takeaways

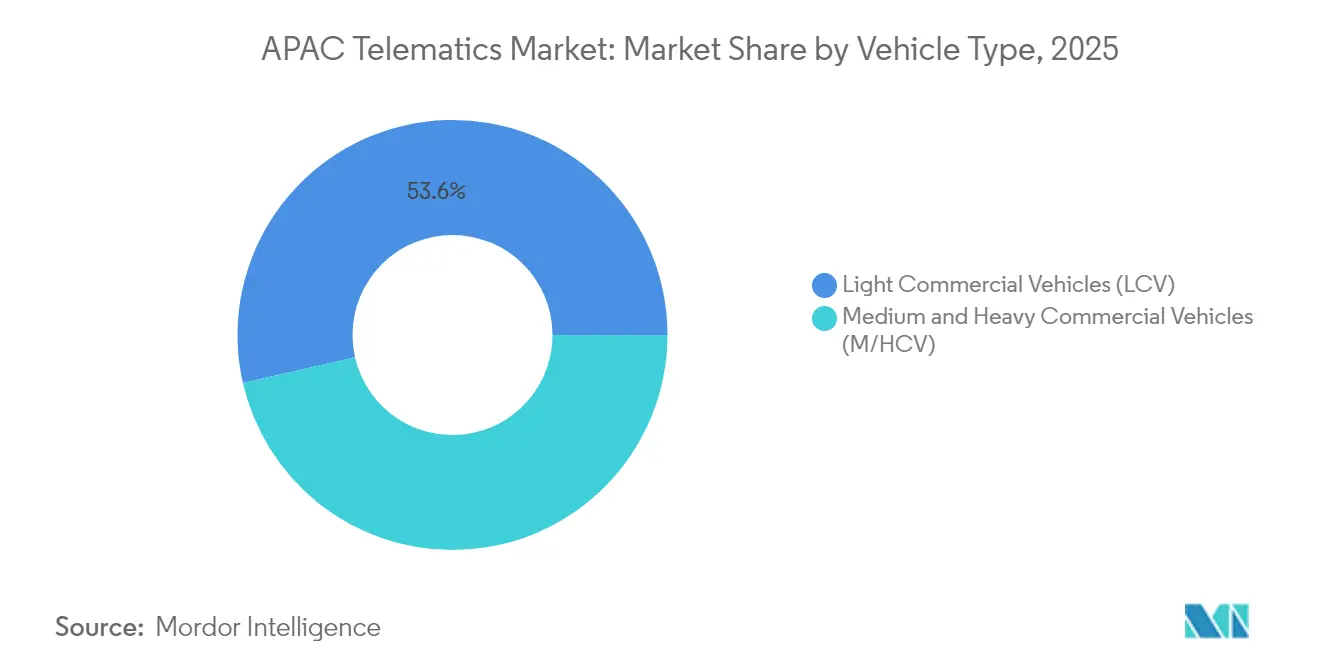

- By vehicle type, Light Commercial Vehicles led with 53.58% of APAC telematics market share in 2025, while Medium and Heavy Commercial Vehicles are projected to compound at 10.41% CAGR through 2031.

- By channel, OEM-embedded solutions held 41.89% revenue share in 2025; After-market OBD-II dongles are forecast to accelerate at a 10.02% CAGR to 2031.

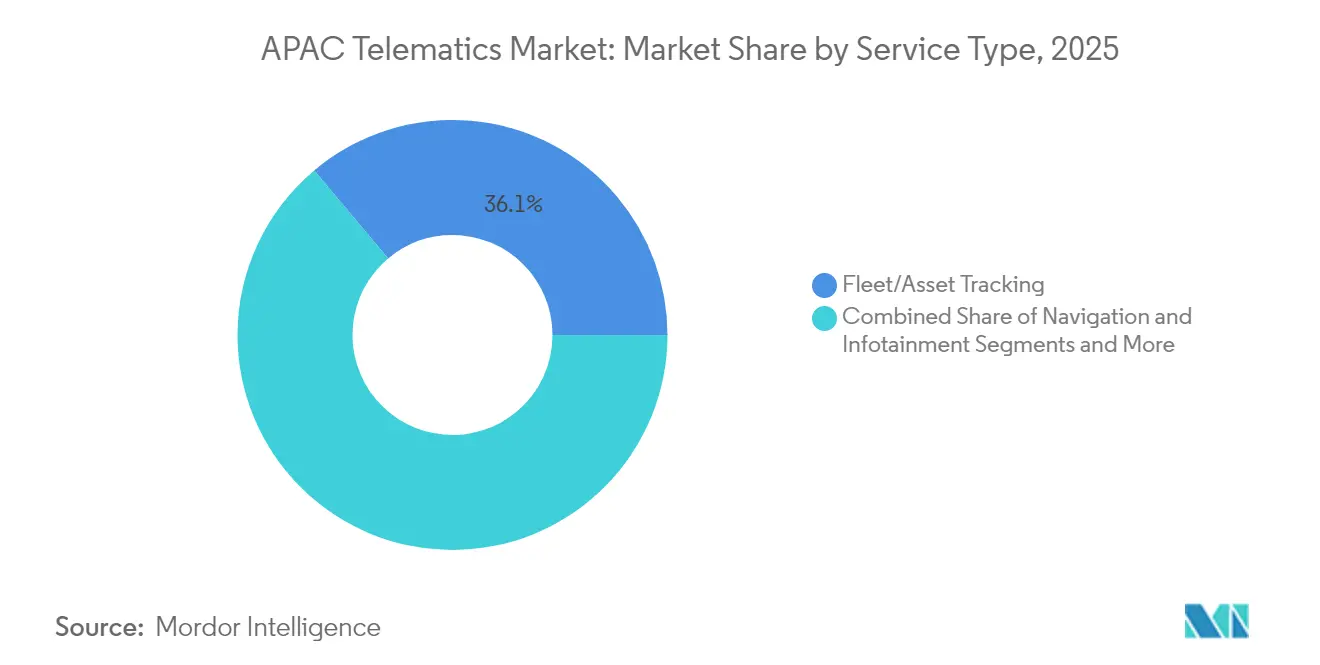

- By service type, Fleet and Asset Tracking accounted for a 36.12% slice of the APAC telematics market size in 2025, and Insurance Telematics is set to surge at 11.02% CAGR during the same period.

- By communication technology, GNSS/GPS retained 48.11% share of the APAC telematics market size in 2025, but DSRC/C-V2X is on track for a 12.08% CAGR through 2031.

- By geography, China captured 37.62% of the APAC telematics market share in 2025 and is advancing at a 9.96% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

APAC Telematics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of OEM-installed connectivity modules | +2.1% | China, Japan, South Korea, ASEAN | Medium term (2-4 years) |

| Regulatory mandates on AIS-140 and eCall | +1.8% | India, Japan, South Korea, ASEAN | Short term (≤ 2 years) |

| Rising demand for usage-based insurance (UBI) | +1.4% | India, China, Australia | Medium term (2-4 years) |

| Growth of e-commerce last-mile fleets | +2.3% | China, India, Southeast Asia | Short term (≤ 2 years) |

| Smart-city ITS pilots driving data partnerships | +1.2% | Singapore, Seoul, Beijing, Tokyo | Long term (≥ 4 years) |

| OEM-fintech leasing models bundling telematics | +0.8% | China, India, Thailand | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Proliferation of OEM-installed connectivity modules

Factory-fitted telematics units are increasingly standard across new commercial vehicles as attach rates rise toward 94% by 2028. Chinese manufacturers collaborate with domestic mobile-network operators to integrate embedded SIMs, while Japanese OEMs layer Android Automotive OS to deliver cloud-native services. The shift simplifies regulatory compliance, enables over-the-air software updates, and supports predictive maintenance that cuts unplanned downtime. Aftermarket vendors face pricing pressure as fleets favor deeper vehicle-bus integration that only embedded hardware can provide.

Regulatory mandates on AIS-140 and eCall

India’s transport ministry requires GPS tracking and panic buttons under AIS-140 for all commercial vehicles, and from April 2026, will extend emergency braking and drowsiness warnings to larger passenger vehicles. Japan and South Korea have rolled out eCall, driving uniform emergency-response capabilities. This convergence allows platform vendors to scale compliance solutions region-wide, though varying technical formats still demand modular software architectures.

Rising demand for usage-based insurance (UBI)

Insurers are shifting from demographics to data-driven premium calculations. Telematics programs now incorporate harsh-braking scores, night-driving ratios, and AI-assisted crash reconstruction. Leading carriers in India and Australia report lower loss ratios and stronger customer retention when mileage-linked policies replace flat premiums. Privacy laws, however, differ sharply across APAC, prompting insurers to invest in consent-management modules and localized data storage [1]NRMA Insurance, “UBI Product Disclosure Statement,” nrma.com.au.

Growth of e-commerce last-mile fleets

Parcel volumes continue to climb amid the proliferation of rapid-delivery promises. Dark-store and micro-fulfillment models amplify the need for dynamic routing and battery-health tracking as urban delivery fleets electrify. Vendors integrate driver productivity dashboards and geo-fencing alerts to curb idle time, while AI route optimizers cut fuel or energy consumption. For many operators, telematics has become core infrastructure rather than optional expenditure.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cyber-security and data-privacy concerns | -1.6% | Japan, South Korea, Australia | Short term (≤ 2 years) |

| High upfront hardware/communication cost | -1.2% | India, Southeast Asia | Medium term (2-4 years) |

| Fragmented interoperability standards | -0.9% | APAC cross-border fleets | Long term (≥ 4 years) |

| Semiconductor supply-chain volatility post-2025 | -1.4% | Global manufacturing hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Cyber-security and data-privacy concerns

Fleet operators worry about remote hacking and unauthorized access to location or CAN bus data. Several APAC governments enforce strict rules on data localization and impose penalties for breaches, raising compliance budgets. Hardware vendors now integrate root-of-trust chips and collaborate with telecom carriers to deploy end-to-end encryption. Managed security operations center services are also emerging to monitor anomalies and coordinate rapid patching [2]1NCE GmbH, “Understanding U.S. Government Rules on Connected Vehicle Cybersecurity,” 1nce.com.

Semiconductor supply-chain volatility post-2025

Automotive-grade MCU and DRAM availability tightened after renewed AI demand absorbed advanced-node capacity. Memory price spikes lifted telematics-unit costs, forcing vendors to renegotiate supply agreements and increase safety stocks. Greater packaging reliance on Taiwanese and Korean foundries exposes fleets to geopolitical risk, prompting dual-sourcing strategies and cross-licensing of design files to secondary fabs [3]Amble Electronics, “Electronics Supply Chain Insights July 2025,” ambleelec.com .

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Commercial Fleets Drive Adoption

Medium and Heavy Commercial Vehicles account for the fastest expansion at 10.41% CAGR to 2031, whereas Light Commercial Vehicles held 53.58% of the APAC telematics market share in 2025. The higher average revenue per installed unit on long-haul trucks comes from advanced fuel analytics, brake-wear prediction, and compliance modules that reduce costly roadside inspections. Conversely, LCV operators prioritize low-cost GPS tracking to safeguard parcels and streamline urban drops. Regulatory momentum, such as India’s incoming ADAS rules for buses and trucks, further lifts M/HCV penetration. Platform consolidation, evident in Platform Science’s 2025 acquisition of Trimble’s fleet unit, signals that integrated offerings spanning ELD compliance and battery-health dashboards will dominate future growth.

M/HCV electrification projects necessitate concurrent telematics deployment to extend driving range and optimize charging windows. LCV fleet managers, pressed by e-commerce service-level agreements, adopt camera-based driver-behavior analytics to cut accident rates. Although the overall installed-base majority remains within LCVs, revenue share tilts toward M/HCVs because of feature-rich solutions bundled with subscription analytics platforms. The segment interplay, therefore, shapes differentiated go-to-market strategies for hardware OEMs and platform providers.

By Channel: Aftermarket Innovation Challenges OEM Dominance

OEM-embedded units retained 41.89% revenue share in 2025, yet Aftermarket OBD-II dongles are on pace for 10.02% CAGR. Cost-conscious fleets value the ease of self-installation and the ability to switch vendors without forfeiting warranties. In contrast, embedded modules offer deeper vehicle-bus integration that supports over-the-air firmware downloads and factory-grade diagnostics. OEMs increasingly open APIs to third-party software platforms, narrowing the historical gap in flexibility and encouraging hybrid deployment models.

Certified aftermarket devices remain pivotal for retrofitting older assets and meeting AIS-140 in India. Hard-wired black boxes serve fleets demanding tamper-proof records or satellite fallback. Cloud-native telematics vendors bridge the channel divide by delivering a unified dashboard that ingests both embedded and aftermarket data streams. As 5G modems become standard from 2026 onward, vendors expect hardware refresh cycles to accelerate, allowing capex-light subscription bundles to spur adoption among small operators.

By Service Type: Insurance Innovation Drives Growth

Fleet and Asset Tracking contributed 36.12% of the APAC telematics market size in 2025, while Insurance Telematics tops growth with an 11.02% CAGR. Insurer appetite for granular risk scoring enlarges the serviceable addressable market: pay-how-you-drive policies in Australia now factor aggressive acceleration counts and phone-distraction metrics. Vendors add AI crash reconstruction, enabling rapid claims automation that cuts settlement times. Meanwhile, Navigation and Infotainment services benefit from closed-loop feedback between cloud mapping engines and OEM in-dash displays, enhancing driver experience without increasing hardware SKU complexity.

Remote Diagnostics adoption rises as vehicle electronics proliferate; predictive maintenance algorithms tap sensor fusion data to forecast component life. Safety and Security services evolve into compliance necessities, with eCall mandates spreading beyond passenger cars to minibuses in Japan and Korea. The converging suite of services transforms telematics from a location-tracking utility into a holistic mobility intelligence platform that commands recurring subscription revenue.

By Communication Technology: Next-Generation Connectivity Emerges

GNSS/GPS still underpins 48.11% of installed units, yet DSRC/C-V2X is forecast for a brisk 12.08% CAGR, reflecting regional plans for cooperative traffic ecosystems. China scales C-V2X roadside units along major logistics corridors, while Japan integrates ITS-G5 to support automated lane-merge pilots. 5G mid-band coverage accelerates real-time video offload and edge AI analytics for driver-facing ADAS. Satellite-based links serve remote mining and trans-Pacific shipping fleets where terrestrial networks remain patchy, ensuring persistent coverage across APAC’s vast geography.

Component price declines and rising throughput speeds make multi-mode modems economical, encouraging device makers to bundle cellular, GNSS, and C-V2X in a single board. Fleet operators thereby future-proof hardware investments, and governments gain a standards-ready installed base to meet long-term V2X safety objectives.

Geography Analysis

China commanded 37.62% of the APAC telematics market share in 2025 and is on a 9.96% CAGR path through 2031. Government subsidies for intelligent-transport components and mandatory installation on new commercial vehicles shorten payback for fleets. Domestic semiconductor fabrication capacity lowers bill-of-materials costs, ensuring hardware affordability at scale. Data-localization statutes, however, oblige foreign cloud providers to co-locate servers, increasing market-entry complexity but safeguarding local data sovereignty.

Japan and South Korea feature high-penetration environments characterized by premium service mixes such as eCall integration, C-V2X field trials, and AI-enabled predictive maintenance. Mature telecom infrastructure and stringent safety regulations yield advanced service adoption, though incremental growth rates remain modest compared with emerging peers. Nonetheless, vendors leverage these markets as test beds for sophisticated analytics before rolling offers into other APAC countries. India shows outsized growth potential as AIS-140 migrates from mandate to enforcement, ensuring nearly every commercial vehicle above 3.5 tons installs GPS, panic buttons, and driver-behaviour analytics. Fintech leasing bundles lower capex hurdles for small fleet owners, while e-commerce expansion creates density that justifies routing optimization investments. Southeast Asia comprises heterogeneous opportunities: Singapore pilots smart-mobility sandboxes; Indonesia’s archipelago spurs satellite-backed solutions; Thailand and Vietnam focus on cross-border lane compliance for regional trade. Australia and New Zealand adopt telematics primarily for mining, agriculture, and extended line-haul operations, anchoring demand in ruggedized hardware with satellite redundancy.

Competitive Landscape

The APAC telematics industry displays moderate concentration. Global suppliers such as Bosch, Continental, and Harman leverage OEM design wins to embed telematics control units at the factory, providing integrated dashboards that sync with infotainment stacks. Regional specialists, MiTAC Digital in Taiwan or SinoTrack in China, compete on price and localized support. Software-centric entrants, including Tech Mahindra, deploy cloud-agnostic platforms that aggregate diverse hardware feeds into unified analytics suites, fostering vendor-agnostic ecosystems.

Strategic moves illustrate a tilt toward platform scale: Platform Science’s 2025 acquisition of Trimble’s transportation unit expanded its software reach into APAC, while Ctrack’s 2024 purchase of Inseego’s telematics arm broadened device portfolios for ASEAN markets. Partnerships flourish between module makers and insurers to co-create UBI products, and between fintechs and OEMs for subscription-based leasing. Vendors race to integrate edge AI and 5G to differentiate on low-latency decision support that can boost driver safety scores or powertrain efficiency. Moderate barriers to entry persist in certification, data-sovereignty compliance, and capital requisites for large-scale hardware rollouts.

APAC Telematics Industry Leaders

LG Electronics Inc.

MiX Telematics India Private Limited (Powerfleet)

Tata Consultancy Services Limited (TCS)

Trimble Inc.

Tech Mahindra Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Tech Mahindra entered a partnership with Aduna to commercialize telco network APIs, opening new monetization avenues for telematics service delivery in APAC.

- February 2025: Platform Science completed the acquisition of Trimble’s transportation and logistics telematics business, expanding its data analytics platform across APAC commercial-vehicle fleets.

- January 2025: ZF Group showcased connected-vehicle solutions at Bharat Mobility Expo 2025, including AIS-140-ready telematics tailored for Indian regulation.

- August 2024: Lynrock Lake took CalAmp private to accelerate product development and APAC expansion efforts.

- August 2024: Ctrack finalized the global acquisition of Inseego’s telematics division, reinforcing its fleet-management footprint in key APAC countries.

APAC Telematics Market Report Scope

Telematics refers to the set of technologies used to monitor a wide range of information for an individual vehicle or fleet. A Telematics system is able to gather the information, including driver behavior, location, engine diagnostics, vehicle activity, and help the fleet operators to visualize the data generated on the software platform to manage their resources.

The Asia Pacific Telematics Market is Segmented by type of vehicle (commercial (truck) LCV Vs. M/HCV, passenger (Car), by channel (OEM, newsprint, aftermarket), by Country (China, Japan, South Korea, Southeast Asia, and Rest of Asia Pacific). The report offers market forecasts and size in value (USD) for all the above segments.

By Vehicle Type

| Light Commercial Vehicles (LCV) |

| Medium and Heavy Commercial Vehicles (M/HCV) |

By Channel

| OEM-embedded |

| Aftermarket Hard-wired |

| Aftermarket OBD-II Dongle |

By Service Type

| Fleet/Asset Tracking |

| Navigation and Infotainment |

| Remote Diagnostics |

| Safety and Security (eCall, SVR) |

| Insurance Telematics (UBI/PAYD) |

By Communication Technology

| GNSS/GPS |

| Cellular (2G/3G/4G/5G) |

| Satellite-based |

| DSRC/C-V2X |

By Country

| China |

| Japan |

| South Korea |

| India |

| Australia and New Zealand |

| South-East Asia (Indonesia, Thailand, Malaysia, Singapore, Vietnam, Philippines) |

| By Vehicle Type | Light Commercial Vehicles (LCV) |

| Medium and Heavy Commercial Vehicles (M/HCV) | |

| By Channel | OEM-embedded |

| Aftermarket Hard-wired | |

| Aftermarket OBD-II Dongle | |

| By Service Type | Fleet/Asset Tracking |

| Navigation and Infotainment | |

| Remote Diagnostics | |

| Safety and Security (eCall, SVR) | |

| Insurance Telematics (UBI/PAYD) | |

| By Communication Technology | GNSS/GPS |

| Cellular (2G/3G/4G/5G) | |

| Satellite-based | |

| DSRC/C-V2X | |

| By Country | China |

| Japan | |

| South Korea | |

| India | |

| Australia and New Zealand | |

| South-East Asia (Indonesia, Thailand, Malaysia, Singapore, Vietnam, Philippines) |

Key Questions Answered in the Report

How large is the APAC telematics market in 2026 and what growth rate is expected?

The market stands at USD 20.54 billion in 2026 and is projected to grow at a 9.82% CAGR to reach USD 32.79 billion by 2031.

Which vehicle category shows the fastest telematics adoption across APAC?

Medium and Heavy Commercial Vehicles exhibit the fastest rise, expanding at 10.41% CAGR through 2031 on account of higher ROI from fuel analytics and compliance modules.

What service type is growing quickest within the region?

Insurance Telematics leads growth with an 11.02% CAGR as insurers deploy usage-based policies and AI-driven claims automation.

Why is China the largest market for telematics in APAC?

China combines policy incentives, local semiconductor supply, and booming e-commerce fleets, capturing 37.62% share in 2025 while advancing at a 9.96% CAGR.

How are regulatory mandates influencing adoption in India?

India’s AIS-140 and upcoming ADAS requirements make telematics compulsory on most commercial vehicles, driving significant fleet retrofits and new-vehicle installations.

What connectivity technology is rising fastest?

DSRC/C-V2X registers the highest growth at 12.08% CAGR as governments deploy roadside units to enable cooperative safety and smart-city applications.

Page last updated on: