Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

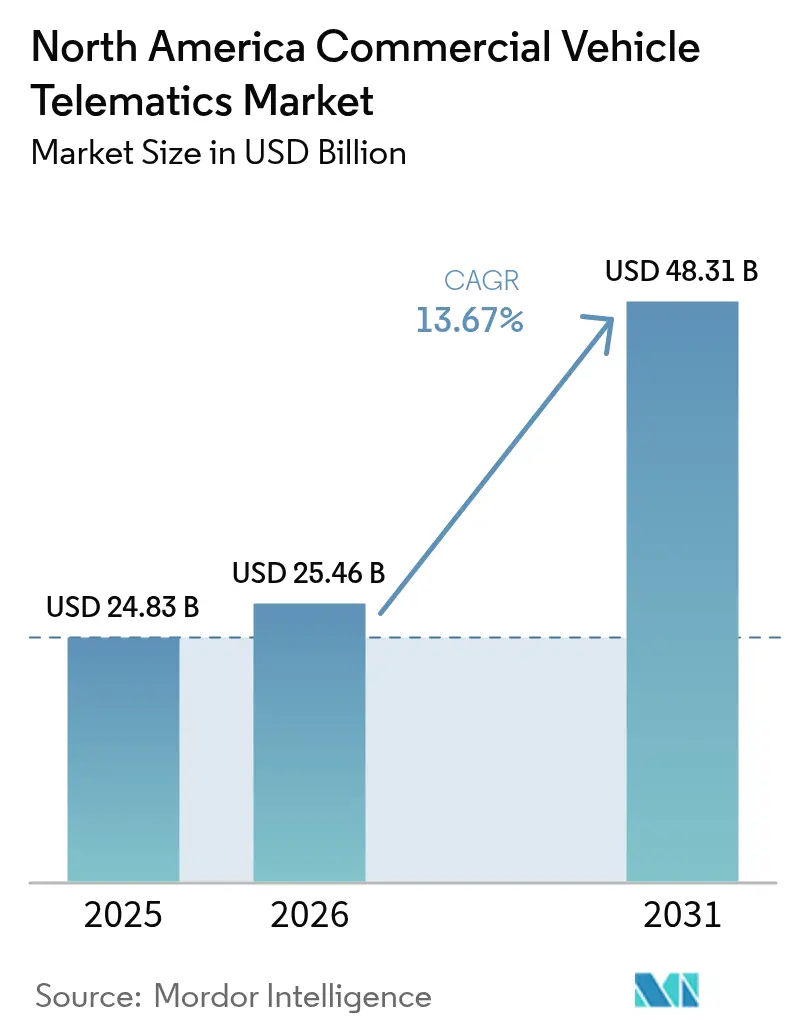

| Base Year Market Size (2025) | USD 24.83 Billion |

| Market Size (2026) | USD 25.46 Billion |

| Market Size (2031) | USD 48.31 Billion |

| Growth Rate (2026 - 2031) | 13.67% CAGR |

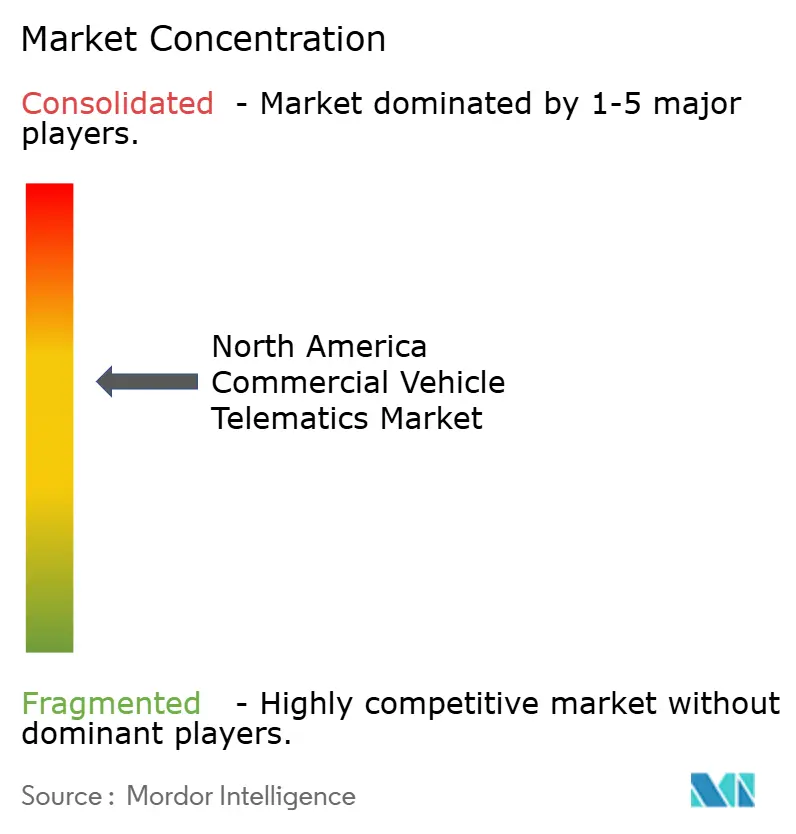

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Commercial Vehicle Telematics Market Analysis by Mordor Intelligence

The North America commercial vehicle telematics market size is projected to expand from USD 24.83 billion in 2025 and USD 25.46 billion in 2026 to USD 48.31 billion by 2031, registering a CAGR of 13.67% between 2026 and 2031. The growth trajectory is anchored in three reinforcing forces. First, Environmental Protection Agency Phase 3 greenhouse-gas requirements for model-year 2027 trucks have turned real-time emissions data into a compliance necessity, prompting fleets to upgrade from location-only boxes to full telematics platforms. Second, insurers are granting double-digit premium discounts when fleets share video-verified safety data, a shift that makes dash-cam deployments self-funding within twelve months for many operators. Third, freight-recession margin pressure heightened in 2025, with marginal operating costs climbing to USD 2.25 per mile, so fleets now view telematics-enabled fuel and maintenance optimization as existential rather than optional. Together, these factors are transforming telematics from a compliance purchase into a strategic profit-protection tool, accelerating system renewal cycles across the region. Competitive dynamics are intensifying as cloud-native entrants add artificial-intelligence analytics and as original equipment manufacturers pre-install hardware that streams standardized controller-area-network data, lowering integration friction for multibrand fleets.

Key Report Takeaways

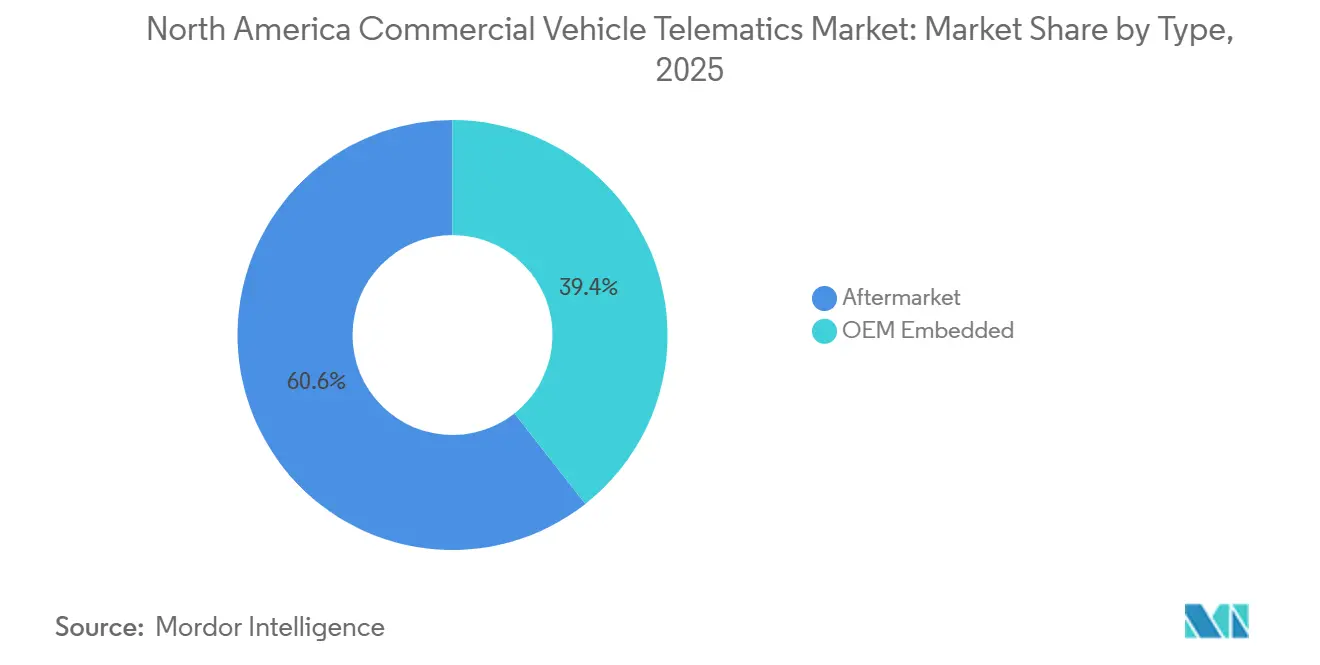

- By type, aftermarket solutions led with 60.62% revenue share in 2025, while original equipment manufacturer embedded systems are projected to expand at a 13.83% CAGR through 2031.

- By solution, fleet tracking and monitoring held 33.74% share in 2025 and video telematics is advancing at a 13.95% CAGR through 2031.

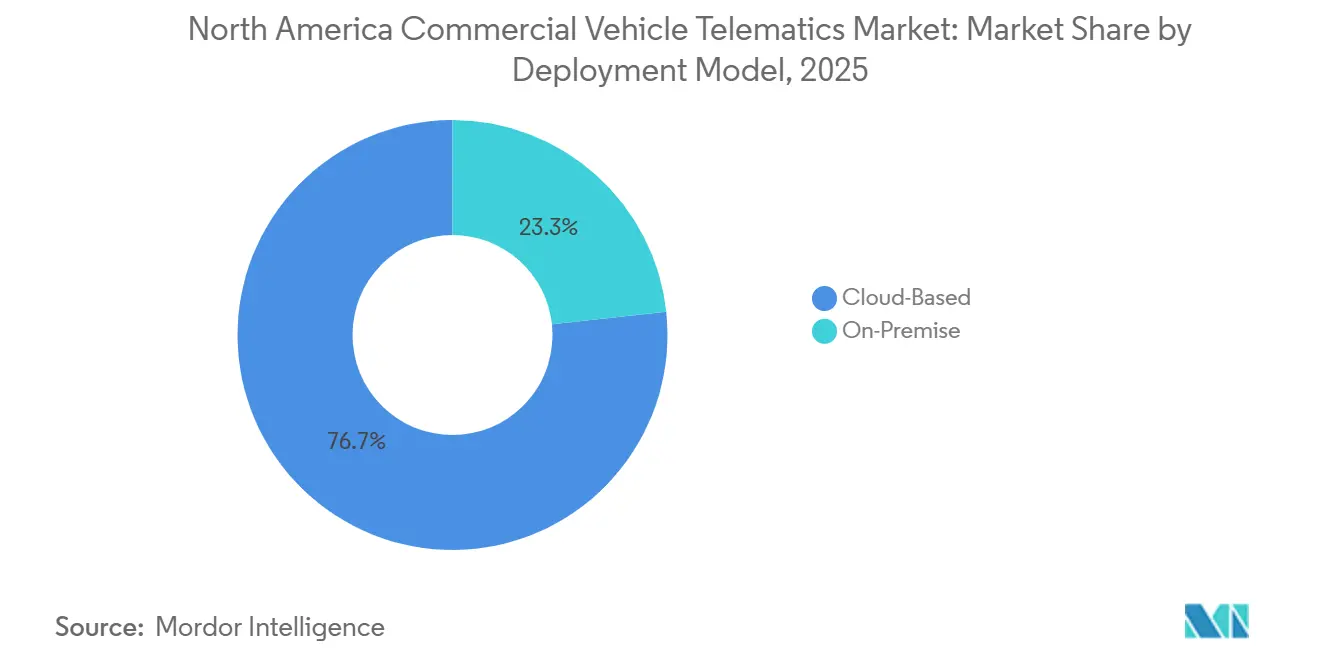

- By deployment model, cloud-based deployment commanded 76.73% share in 2025 and is forecast to grow at a 14.11% CAGR to 2031.

- By vehicle class, light commercial vehicles accounted for 46.84% of the North America commercial vehicle telematics market size in 2025, whereas medium commercials are poised to grow at a 14.02% CAGR over 2026-2031.

- By geography, the United States dominated with 77.64% North America commercial vehicle telematics market share in 2025, while Mexico is set to record the fastest 14.33% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Commercial Vehicle Telematics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory Mandates For Compliance | +3.2% | United States and Canada, with California Air Resources Board rules extending to 10 Advanced Clean Trucks states | Medium term (2-4 years) |

| Video-Based Safety And AI Analytics | +2.8% | United States dominant; Canada adoption rising post-Canadian Council of Motor Transport Administrators electronic logging device Technical Standard v1.3 | Short term (≤ 2 years) |

| Fleet Electrification Analytics | +2.1% | United States (California, New York, Washington leading); Mexico infrastructure-constrained until 2028 | Long term (≥ 4 years) |

| OEM Factory-Fit Telematics Standardisation | +1.9% | United States and Canada; Mexico delayed by United States-Mexico-Canada Agreement review uncertainty | Medium term (2-4 years) |

| 5G-Enabled Real-Time V2X Data | +1.5% | United States metropolitan freight corridors; rural Canada and Mexico coverage gaps persist | Long term (≥ 4 years) |

| Freight-Recession Cost Optimisation | +2.2% | United States and Canada; Mexico benefits from nearshoring but faces peso-appreciation margin pressure | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Regulatory Mandates for Compliance

Federal and state emissions rules now compel fleets to capture ton-mile carbon-dioxide telemetry, diesel-exhaust-fluid quality, and battery state-of-health in order to prove compliance with Phase 3 greenhouse-gas limits that start with model-year 2027 engines. The California Air Resources Board’s Clean Truck Partnership lets manufacturers pool over-compliance credits across states, so telematics must track where each zero-emission truck operates to simplify credit accounting. Canada tightened enforcement by mandating third-party certification under its September 2025 Electronic Logging Device v1.3 specification, pushing fleets to adopt certified platforms rather than in-house builds. The Bureau of Industry and Security rule on connected-vehicle information bars hardware sourced from foreign adversaries, increasing vendor audit costs yet shielding domestic suppliers from low-price imports. Collectively, these policies enlarge the compliance feature set, ensuring that North America commercial vehicle telematics market demand remains price-inelastic through the forecast period.

Video-Based Safety and AI Analytics

Insurers now embed telematics-derived risk scores into underwriting and grant up to 20% premium relief when fleets submit dash-cam footage after collisions, which turned cameras from discretionary to mandatory investments in 2025.[1]SambaSafety, “2025 Telematics Benchmarking Report,” sambasafety.com Usage-based pricing amplified operator savings as claims frequency fell 22% and accident severity declined 25% among video-enabled fleets operating in dense urban corridors such as New York. Verizon Connect’s 2025 survey reported that 75% of fleets that added cameras also doubled their average fuel-economy gains to 16% because event-driven coaching reduced harsh accelerations. The September 2025 launch of Lytx+ with Geotab demonstrates a hybrid artificial-intelligence model where machine vision flags lane departures in real time and human analysts validate footage within minutes to maintain driver trust.[2]Lytx Inc., “Lytx+ with Geotab Integration Launches,” lytx.com As underwriting models mature, analysts expect video uptake to outpace other telematics functions, lifting the North America commercial vehicle telematics market far above basic GPS-tracking volumes during 2026-2031.

Fleet Electrification Analytics

Environmental Protection Agency modelling projects that zero-emission powertrains will capture half of vocational classes and one-quarter of heavy sleepers by 2032, creating a data need for battery state-of-charge monitoring, charge-event logging, and route-energy prediction. Geotab’s suitability-assessment tool is already analysing duty cycles for 28% of United States fleets, flagging which internal-combustion units can be swapped with battery trucks without range anxiety. Samsara’s Smart Trailers reduce rolling resistance and parasitic electrical loads, adding 5% to electric-tractor range on multi-stop routes. Department of Energy research shows depot infrastructure costs of USD 50,000–150,000 per truck along major corridors, so granular telematics evidence is crucial for utilities to approve incentive packages. Hydrogen fuel-cell diagnostics remain an untapped niche but Phase 3 rules now credit hydrogen engines, spurring early-stage telematics prototypes that track stack temperature and refuelling leakage events.

OEM Factory-Fit Telematics Standardisation

Manufacturers have pivoted toward recurring software revenue, so they are embedding telematics devices at the assembly line. Autocar factory-installs Geotab GO hardware on every internal-combustion truck, backing Always Up uptime guarantees with real-time diagnostics that cut roadside events by 15% in pilot fleets. Samsara’s Pre-Delivery Installation program with Daimler Truck and Fontaine removes aftermarket fit-out delay, allowing fleets to activate software on day one and monetize data for maintenance scheduling. Environmental Protection Agency on-board-diagnostic rules for model-year 2027 engines standardize diesel-particulate-filter soot-load broadcasts, so third-party platforms can ingest those signals without proprietary decoding fees. Factory integration narrows the aftermarket lead, but open application-programming interfaces protect operator choice, preventing full vendor lock-in and ensuring the North America commercial vehicle telematics market remains multi-sourced as volumes scale.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cyber-Security And Data-Sovereignty Liability | -1.8% | United States (Texas Attorney General litigation precedent); Canada Federal Trade Commission guidance; Mexico data-residency rules emerging | Medium term (2-4 years) |

| Rising 5G And AI Hardware Costs | -1.3% | United States and Canada urban corridors; Mexico infrastructure gaps delay 5G return on investment | Short term (≤ 2 years) |

| Integration Debt With Legacy IT | -0.9% | United States and Canada incumbent fleets with 10-plus-year-old transportation management systems; Mexico greenfield advantage | Medium term (2-4 years) |

| Driver Privacy Litigation Risk | -1.1% | United States (California Consumer Privacy Act, Illinois Biometric Information Privacy Act); Canada Personal Information Protection and Electronic Documents Act; Mexico Federal Law on Protection of Personal Data | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cyber-Security and Data-Sovereignty Liability

A 2024 Texas lawsuit alleged that General Motors and OnStar sold real-time location traces to brokers without explicit consent, establishing a precedent that exposes fleets to class-action suits if driver data leaves contractual bounds.[3]Texas Attorney General, “Lawsuit Against General Motors and OnStar,” texasattorneygeneral.gov The Cybersecurity and Infrastructure Security Agency’s 2025 advisory highlighted vulnerabilities that allow remote immobilisation of unpatched fleet-management platforms, prompting the National Motor Freight Traffic Association to publish best-practice checklists including mandatory encryption and annual penetration tests CISA.GOV. The Bureau of Industry and Security now bans components from foreign adversaries in connected-vehicle stacks, pushing vendors to reshore supply chains and raising compliance overhead by up to 25% BIS.DOC.GOV. Insurers have responded with cyber-liability exclusions that place the onus on fleets to certify vendor controls, so some operators are shifting sensitive datasets to on-premise servers behind corporate firewalls. Unless harmonised privacy frameworks emerge, these legal cross-currents could slow the North America commercial vehicle telematics market cloud-migration wave after 2028.

Rising 5G and AI Hardware Costs

Edge-analytics telematics units require 5G modems, high-resolution image sensors, and graphics processors that cost two-to-three-times more than legacy GPS-only hardware, yet spot freight rates remained in deflation during 2025, squeezing fleet cash flows DAT.COM. Federal Communications Commission vehicle-to-everything spectrum is available, but roadside units outside major cities will not reach scale for at least three years, delaying return on investment for countryside haulers FCC.GOV. RXO’s 2025 forecast shows contract rates climbing only 2.1%, insufficient to fund wholesale retrofits among fleets with sub-5% net margins RXO.COM. The paradox is acute: the fleets that most need telematics to shave operating costs often lack the liquidity to modernise. Vendors are countering with device-leasing models bundled into software subscriptions, but hardware inflation still trims 130 basis points from the North America commercial vehicle telematics market CAGR during 2026-2028.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Factory Integration Narrows Aftermarket Lead

Aftermarket solutions accounted for 60.62% of the North America commercial vehicle telematics market size in 2025, reflecting the region’s huge legacy truck population. However, original equipment manufacturer embedded systems are growing at a 13.83% CAGR because factory-fit devices give manufacturers a line-of-sight to warranty events, uptime contracts, and over-the-air updates. Autocar’s 2025 move to factory-install Geotab GO devices illustrates how integration yields near-real-time diagnostics that reduce roadside failures by double digits. Samsara’s Pre-Delivery Installation with Daimler Truck achieves the same time-to-value advantage, prompting mixed-age fleets to adopt a dual-sourcing strategy that blends factory hardware with retrofit boxes to preserve data continuity.

Regulatory factors reinforce the shift, 40 CFR 1036 obliges 2027 engines to broadcast diesel exhaust fluid quality, particulate-filter soot load, and torque over the controller-area network, so proprietary decoding becomes unnecessary. That levelling of the data-access field erodes the historical moat of aftermarket specialists. In response, leading retrofit vendors emphasise device-agnostic software that ingests both factory and third-party streams, while also negotiating open-application-programming-interface clauses with truck makers. Whether embedded solutions eclipse retrofit volumes before 2031 hinges on how aggressively manufacturers monetise subscriptions once free trial periods expire. For now, the aftermarket retains scale leadership, but the competitive centre of gravity is drifting toward factory dashboards.

By Vehicle Class: Medium Commercials Accelerate Ahead Of Light And Heavy Segments

Light commercials captured 46.84% North America commercial vehicle telematics market share in 2025, buoyed by parcel-delivery routes where every minute of dwell time erodes profit. Medium commercials nevertheless post the fastest 14.02% CAGR because regional distributors face chronic driver shortages and rely on gamified scorecards plus real-time coaching to curb turnover. Heavy Class 8 tractors grow more slowly, having already installed first-generation black boxes under the 2017 electronic-logging-device mandate.

Medium trucks also anchor many zero-emission pilots, given their predictable daily range, so telematics functions such as charge-event logging and regenerative-brake heat-mapping carry immediate payback. Environmental Protection Agency Phase 3 splits compliance targets by subclass, meaning medium vocational trucks must hit steeper zero-emission percentages than long-haul sleepers, amplifying analytics complexity. Camera-based blind-spot monitoring like Verizon Connect Extended View appeals most to mid-box fleets weaving through congested boroughs where insurance claims run high. Consequently, investment intensity gravitates toward medium-duty platforms, confirming their role as the North America commercial vehicle telematics market bellwether for next-generation capability rollouts.

By Deployment Model: Cloud Dominance Encounters Hybrid Pushback

Cloud instances delivered 76.73% of 2025 revenue because software-as-a-service subscriptions remove server-maintenance headaches and offer near-weekly feature releases. That footprint is expected to grow at a 14.11% CAGR through 2031 as artificial-intelligence workloads scale and as insurers demand continuous data feeds for usage-based pricing. Yet legal events such as the Texas Attorney General data-privacy suit and the Bureau of Industry and Security residency rule spur large shippers to reconsider pure public-cloud strategies in favour of split-tunnel designs that keep driver identities on-premise.

Vendors are reacting by provisioning geo-fenced storage nodes, earning Federal Risk and Authorization Management Program clearances, and enabling customer-managed encryption keys to satisfy auditors. Hybrid architectures let carriers run latency-sensitive video analytics on edge gateways while pushing anonymised fuel and maintenance statistics to the public cloud for aggregation. Such patterns will moderate the North America commercial vehicle telematics market’s cloud-growth slope after 2028 yet should not reverse the dominant trajectory because total cost of ownership for on-premise clusters remains prohibitive for small and mid-sized operators.

By Solution: Video Telematics Outpaces Legacy Tracking

Legacy tracking maintained 33.74% share of 2025 revenue, but video telematics posts a blistering 13.95% CAGR through 2031 as insurance economics make cameras indispensable. Eighty-eight percent of fleets now deploy video for safety improvement and 30% share footage with insurers, establishing a virtuous cycle where fewer accidents further cut premiums. Driver-management dashboards that gamify safe behaviour are surging as fleets fight a regional driver-turnover rate above 90% in some last-mile segments. Insurance telematics services deepen this integration by piping driver scores straight to underwriters, who in turn lower deductibles.

Safety-compliance modules remain baseline functionality, but growth has plateaued because most fleets achieved electronic-logging parity by 2023. Vehicle-to-everything still garners publicity after the Federal Communications Commission unlocked 5.9 gigahertz spectrum, yet roadside units trail schedule, so revenue contribution will materialise late in the forecast window. Platform convergence is the watchword, the September 2025 Lytx and Geotab integration collapses multiple dashboards into one view, cutting administrative workload and anchoring customer loyalty. Similar bundling will define competitive positioning across the North America commercial vehicle telematics market as solution boundaries blur.

Geography Analysis

The United States anchored 77.64% of 2025 spending because the Federal Motor Carrier Safety Administration enforced electronic-logging compliance and Environmental Protection Agency Phase 3 standards make telematics the easiest route to regulatory proof. Houlihan Lokey calculated marginal truck-operating costs of USD 2.25 per mile in 2025, a jump that pushed many smaller carriers out of business and left survivors racing to embed telematics-driven efficiency. Tender rejections climbed in early 2026 and roughly 350 carriers continue to exit each week, leading shippers to favor data-rich fleets that demonstrate capacity reliability. Privacy litigation, like the Texas Attorney General suit,, and the Environmental Protection Agency Phase 3 standards made now influence procurement, with contracts mandating vendor cyber-liability indemnities. Adoption saturation is high, yet hardware refresh cycles tied to 5G and advanced cameras will sustain mid-teen growth inside the North America commercial vehicle telematics market over the outlook.

Canada contributes a smaller revenue pool yet offers harmonised rule-sets that simplify cross-border fleet operations. The September 2025 Electronic Logging Device v1.3 standard obliges third-party certification, closing loopholes that once let fleets self-approve devices. Quebec’s January 2026 125-hour Class 1 driver-training mandate fuels demand for telematics-recorded behind-the-wheel logs to verify compliance. Transport Canada’s February 2025 connected-vehicle safety framework signals governmental support for vehicle-to-everything pilots, which positions Canada as a testbed for rural connectivity ventures. Samsara’s Sterling Crane case study demonstrated CAD 1.5 million (USD 1.1 million) annual savings on roadable equipment, reinforcing value perception among industrial fleets. Exchange-rate volatility is muted compared with Mexico, so capital allocation decisions focus on regulatory certainty rather than currency risk.

Mexico is the growth champion, forecast to advance at 14.33% CAGR through 2031 as nearshoring reorients supply chains toward computing equipment and electronics exports that surpassed automotive shipments in 2025. Freight volumes surged 17.2% year over year in December 2025, stretching capacity and forcing carriers to digitalise cross-border documentation workflows. The Mexican peso appreciated 17% against the United States dollar in January 2026, which squeezed exporter margins and amplified interest in telematics-enabled fuel and maintenance savings. Infrastructure deficits persist, 5G coverage outside Mexico City, Monterrey, and Guadalajara is patchy and depot charging networks lag United States build-outs by up to seven years. Nonetheless, telematics vendors that bundle customs-clearance integration, Spanish-language driver interfaces, and hybrid cloud-residency options stand to gain first-mover advantage as regulatory clarity improves after the scheduled 2026 United States–Mexico–Canada Agreement review.

Competitive Landscape

The North America commercial vehicle telematics market is moderately fragmented but consolidating as vendors race to own the widest data graphs and the largest insurance integrations. Platform Science bought Trimble’s telematics division in February 2025, creating an end-to-end stack that spans factory-embedded devices and aftermarket retrofits, thereby widening cross-sell potential. Lytx and Geotab followed with a unified video-plus-tracking platform that eliminates multi-dashboard fatigue for mid-market fleets and supports more than 300 electric vehicle models. Geotab, Verizon Connect, and Samsara defend share through truck-maker alliances: Autocar ships Geotab hardware as standard, while Daimler Truck lets fleets receive Samsara software fully activated at delivery.

White-space specialists such as Netradyne and IntelliShift target artificial-intelligence edge inference, while GPS Insight and Spireon serve price-sensitive small operators with stripped-down yet scalable options. Competitive advantage is drifting from hardware design to data intellect; the vendor that amasses the deepest video library gains model-training superiority, which improves false-positive rejection rates and boosts driver acceptance.

Federal Risk and Authorization Management Program certification is an emerging moat because state and federal agencies demand high-assurance cloud hosting. At the same time, 40 CFR 1036 standardised controller-area-network outputs erode hardware decoding moats, forcing players to shift energy toward analytics, user-experience refinement, and ecosystem breadth. Cyber-security posture is a gatekeeper, the Cybersecurity and Infrastructure Security Agency advisory propelled multi-factor authentication and encrypted streaming to baseline status, squeezing under-capitalised newcomers that cannot fund 24-hour security-operations centres.

North America Commercial Vehicle Telematics Industry Leaders

Geotab Inc.

Verizon Connect Inc.

Samsara Inc.

Trimble Inc.

Solera Holdings LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Quebec implemented mandatory 125-hour Class 1 driver training, triggering demand for telematics-integrated training modules.

- October 2025: Lytx and Geotab launched Lytx+ with Geotab, unifying video and telematics under one contract and interface.

- September 2025: Canadian Council of Motor Transport Administrators released Electronic Logging Device Technical Standard v1.3 requiring third-party certification.

- August 2025: Samsara and Daimler Truck introduced Pre-Delivery Installation so trucks arrive with telematics pre-configured.

North America Commercial Vehicle Telematics Market Report Scope

Commercial vehicle telematics leverages telecommunication and informatics technologies to oversee and optimize commercial vehicle fleets. This technology facilitates real-time data exchanges between vehicles and central systems, enhancing efficiency, safety, and cost-effectiveness. Typically utilizing GPS and various sensors, telematics systems deliver real-time location data, empowering fleet managers to monitor vehicles and drivers instantaneously.

The North America Commercial Vehicle Telematics Market Report is Segmented by Type (OEM Embedded, Aftermarket), Vehicle Type (Light Commercial Vehicles, Medium Commercial Vehicles, Heavy Commercial Vehicles, Off-Highway Vehicles), Deployment Model (Cloud-based, On-premise), Solution (Fleet Tracking and Monitoring, Driver Management, Insurance Telematics, Safety and Compliance, Video Telematics, V2X Solutions, Other Solutions), and Geography (United States, Canada, Mexico). The Market Forecasts are Provided in Terms of Value (USD).

By Type

| OEM Embedded |

| Aftermarket |

By Vehicle Type

| Light Commercial Vehicles |

| Medium Commercial Vehicles |

| Heavy Commercial Vehicles |

| Off-Highway Vehicles |

By Deployment Model

| Cloud-based |

| On-premise |

By Solution

| Fleet Tracking and Monitoring |

| Driver Management |

| Insurance Telematics |

| Safety and Compliance |

| Video Telematics |

| V2X Solutions |

| Other Solutions |

By Country

| United States |

| Canada |

| Mexico |

| By Type | OEM Embedded |

| Aftermarket | |

| By Vehicle Type | Light Commercial Vehicles |

| Medium Commercial Vehicles | |

| Heavy Commercial Vehicles | |

| Off-Highway Vehicles | |

| By Deployment Model | Cloud-based |

| On-premise | |

| By Solution | Fleet Tracking and Monitoring |

| Driver Management | |

| Insurance Telematics | |

| Safety and Compliance | |

| Video Telematics | |

| V2X Solutions | |

| Other Solutions | |

| By Country | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

What is the projected value of the North America commercial vehicle telematics market in 2031?

It is expected to reach USD 48.31 billion by 2031, expanding at a 13.67% CAGR from 2026 to 2031.

Which vehicle class will grow fastest through 2031?

Medium commercial trucks are forecast to post the quickest 14.02% CAGR because regional distributors use telematics to ease driver shortages and optimise multi-stop routes.

Why are insurers accelerating video telematics adoption?

They offer premium discounts of up to 20% when fleets share dash-cam footage, which cuts crash frequency and lowers total claims costs.

How will Environmental Protection Agency Phase 3 rules influence telematics demand?

The rules require real-time emissions and battery-health reporting starting with model-year 2027 vehicles, making advanced telematics essential for regulatory compliance.

Which country will register the highest telematics growth rate in North America?

Mexico is on track for a 14.33% CAGR through 2031, fueled by nearshoring-related freight expansion and the need to streamline cross-border operations.

Page last updated on: