Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

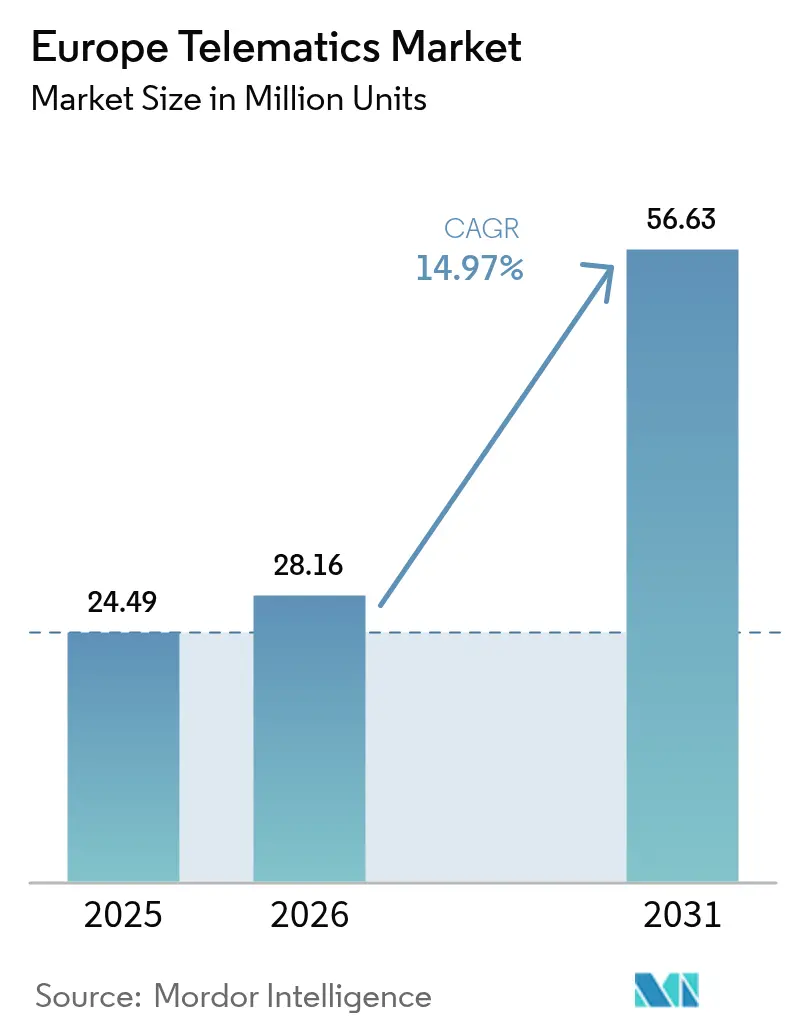

| Base Year Market Size (2025) | 24.49 Million units |

| Market Volume (2026) | 28.16 Million units |

| Market Volume (2031) | 56.63 Million units |

| Growth Rate (2026 - 2031) | 14.97% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Telematics Market Analysis by Mordor Intelligence

The Europe telematics market size is expected to grow from 24.49 million installed units in 2025 to 28.16 million installed units in 2026 and is forecast to reach 56.63 million installed units by 2031 at 14.97% CAGR over 2026-2031. Growth is underpinned by synchronized European Union (EU) mandates, original-equipment-manufacturer (OEM) connectivity strategies, and fast-moving fleet-digitization programs that pull telematics from a discretionary add-on to a core mobility infrastructure layer. Rising embedded connectivity in passenger cars, the ongoing logistics boom, and the regulatory migration from 2G/3G to 4G/5G collectively set a robust baseline for the Europe telematics market, while declining sensor costs broaden adoption beyond large fleets. Competitive intensity is reshaping around direct OEM data pipes, evidenced by Volkswagen Group’s line-fit partnerships, even as aftermarket specialists position themselves with cross-fleet analytics to defend share. Data privacy obligations and retrofit complexity temper rollout speed, but overall momentum remains firmly positive thanks to overlapping technology, regulatory, and business case catalysts across the continent.

Key Report Takeaways

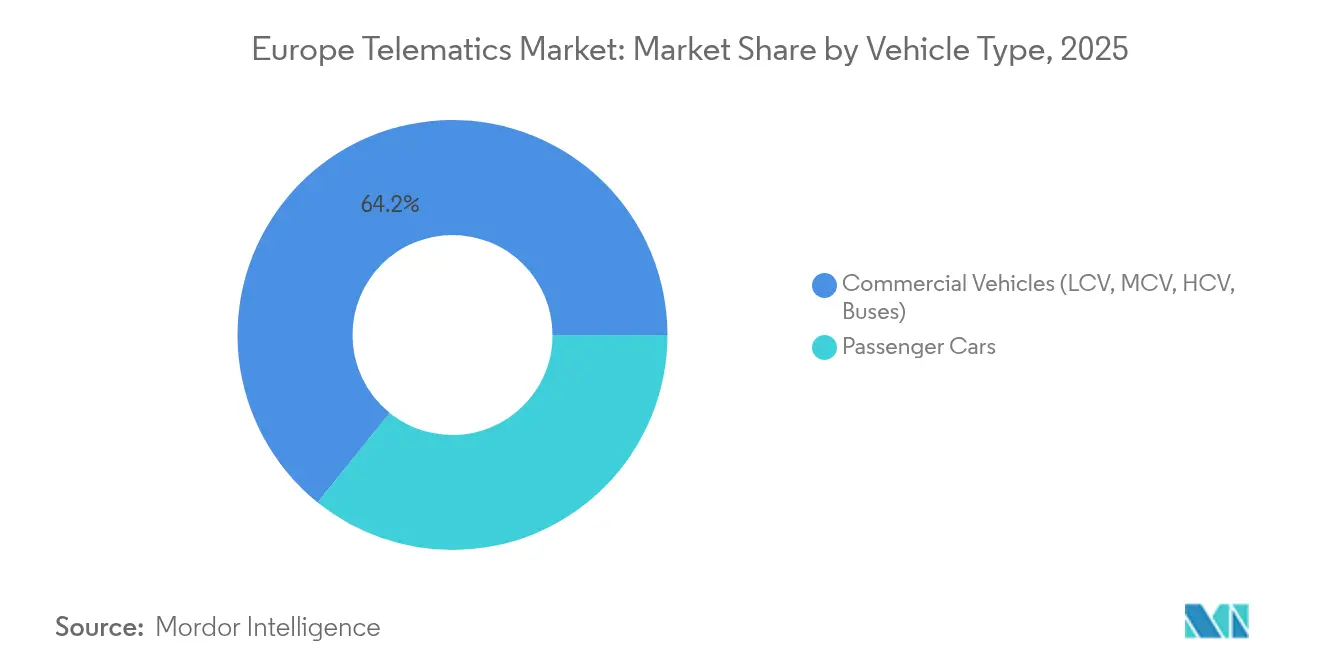

- By vehicle type, commercial vehicles led with 64.21% of the Europe telematics market share in 2025, while passenger cars are projected to expand at a 16.79% CAGR through 2031.

- By solution type, fleet management and asset tracking captured 37.12% share of the Europe telematics market size in 2025, whereas insurance and usage-based telematics are advancing at a 15.61% CAGR to 2031.

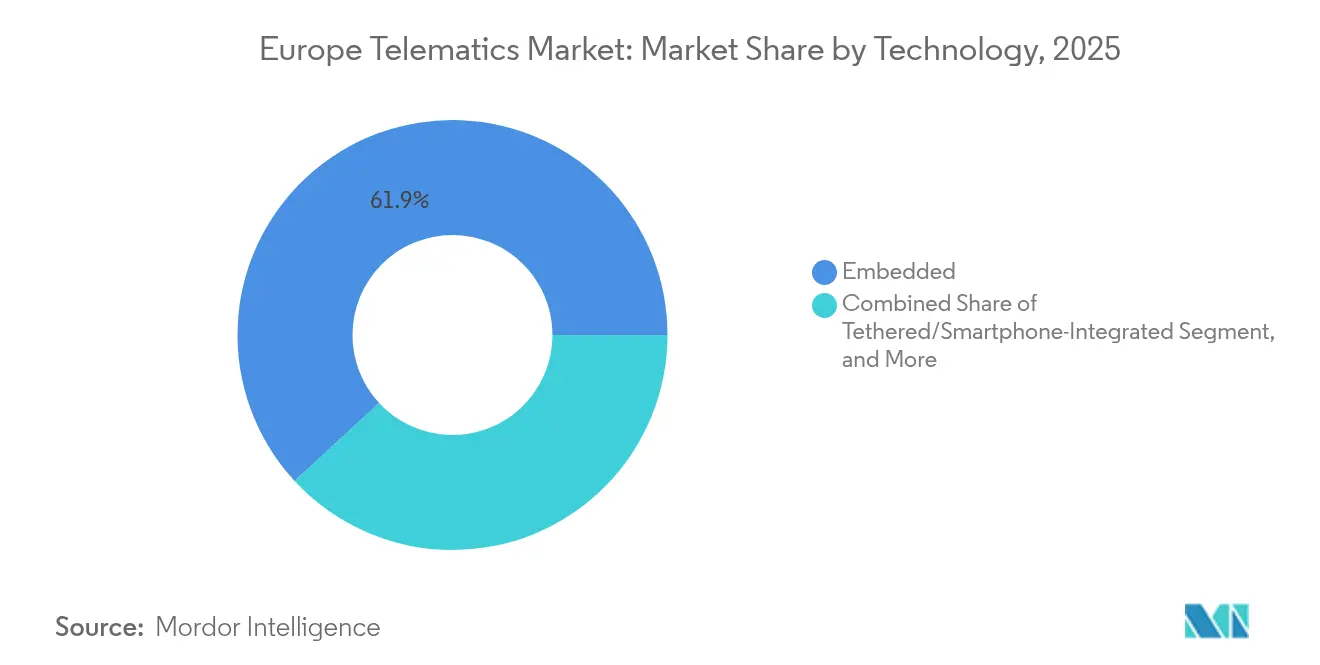

- By technology, embedded telematics commanded 61.88% share in 2025 in the Europe telematics market and is growing at a 16.76% CAGR through 2031.

- By deployment mode, OEM line-fit platforms accounted for 55.93% share in 2025 in the European Telematics market and are recording a 16.31% CAGR over the forecast horizon.

- By geography, Germany dominated with 28.52% share in 2025 and is sustaining 15.41% growth through 2031, supported by domestic OEM presence and strong compliance momentum.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Telematics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU eCall and Smart Tachograph compliance timeline | +2.8% | EU-wide, strongest in Germany, France, Italy | Medium term (2-4 years) |

| Rapid OEM shift to embedded connectivity platforms | +3.2% | Germany, UK, Nordic countries | Long term (≥ 4 years) |

| E-commerce and last-mile logistics optimisation push | +2.1% | Urban centers across EU, strongest in Netherlands, UK | Short term (≤ 2 years) |

| Falling connectivity and sensor costs for fleet owners | +1.9% | Global with EU adoption acceleration | Medium term (2-4 years) |

| Next-Gen (4G/5G) eCall migration mandate | +1.5% | EU-wide regulatory requirement | Short term (≤ 2 years) |

| HDV CO₂ monitoring rules nudging eco-driving analytics | +0.8% | EU commercial vehicle operators | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EU eCall and Smart Tachograph Compliance Timeline

The Europe telematics market receives a direct uplift from synchronized EU directives that stipulate Next Generation eCall readiness and Smart Tachograph 2 installation across vans above 2.5 tonnes. Hardware refresh cycles concentrate around the July 2026 tachograph deadline and the January 2027 4G/5G eCall cut-over, giving providers reliable demand visibility while allowing bundling of compliance modules with higher-margin analytics services.[1]TÜV Rheinland, “TÜV Rheinland Supports Flairmicro in Achieving NG eCall Certification,” tuv.com As operators consolidate procurement to meet these immovable milestones, solution vendors benefit from fewer stakeholder objections and clearer budget approvals, effectively flattening lengthy sales funnels and accelerating unit run-rates across the Europe telematics market.

Rapid OEM Shift to Embedded Connectivity Platforms

OEMs now view connected-vehicle data as a strategic asset for lifetime customer monetization. Partnerships such as Targa Telematics and Volkswagen Group demonstrate a structural pivot: line-fit modules ship with the vehicle, streamlining fleet onboarding, enabling weekly feature drops, and reducing support queries tied to aftermarket device faults. Embedded channels also unlock proprietary diagnostics, over-the-air (OTA) updates, and energy-management controls, extending revenue streams long after initial sale. Consequently, the Europe telematics market increasingly rewards providers that master OEM data ingestion and analytic enrichment at scale.

E-commerce and Last-Mile Logistics Optimization Push

Same-day and one-hour delivery promises in dense European cities raise fleet-efficiency stakes. Telematics platforms link dynamic routing engines with inventory and parcel-locker networks, squeezing idle time and shrinking miles driven per drop. Electric vans compound complexity because charging schedules, battery health, and low-emission-zone rules must slot into dispatch algorithms in real time. As urban regulators tighten sustainability benchmarks, logistics operators turn to telematics dashboards for carbon-scorecard reporting, cementing demand among parcel and grocery chains that already underpin more than one-third of all commercial deliveries in major EU metros. This operational nexus keeps the Europe telematics market firmly on an upward trajectory.

Falling Connectivity and Sensor Costs for Fleet Owners

Volume manufacturing pushes telematics hardware bill-of-materials below the psychological EUR 100 threshold, while multi-carrier SIM bundles and 5G bandwidth price erosion slash monthly operating costs. Lower entry barriers pull small and mid-sized hauliers into the adoption funnel, expanding the Europe telematics market addressable base. Richer sensor payloads, gyroscopes, high-G accelerometers, and tire-pressure probes, elevate predictive maintenance accuracy, translating hardware savings into faster ROI payback periods. In parallel, cloud-native analytics spread fixed costs across thousands of vehicles, letting vendors tier offerings so that budget-constrained fleets can upgrade à-la-carte.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High retrofit and integration costs for mixed fleets | -1.7% | EU-wide, particularly affecting SME fleets | Short term (≤ 2 years) |

| Data-privacy and GDPR-driven vendor liability risk | -1.2% | EU-wide regulatory compliance requirement | Medium term (2-4 years) |

| 2G/3G sunset forcing premature hardware replacement | -2.1% | Germany, UK, Nordic countries with early shutdown timelines | Short term (≤ 2 years) |

| Shortage of telematics data-science talent | -0.9% | Germany, France, Netherlands tech hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Retrofit and Integration Costs for Mixed Fleets

European fleets seldom buy homogenous vehicle batches; age, make, and engine technology vary widely. Installing disparate black-box devices leads to data silos and support churn, especially for owner-operators juggling thin profit margins. Integration expenses roll beyond hardware, driver onboarding, firmware updates, and legacy CAN-bus quirks consume scarce operating capital. Consequently, smaller fleets defer deployments or restrict rollouts to regulatory minimums, shaving a potential rate off the Europe telematics market CAGR in the near term.

Data-Privacy and GDPR-Driven Vendor Liability Risk

Continuous collection of vehicle coordinates and driver behavior invokes strict “personal data” obligations under GDPR and the EU Data Act. Telematics firms become data controllers, assuming breach-notification responsibilities and consent-management overheads. Insurance-telematics programs face heightened scrutiny because usage-based premiums can reveal sensitive patterns. Compliance frameworks add legal and engineering costs that smaller providers struggle to absorb, nudging sector consolidation even as established players embed robust encryption and anonymization routines to protect their positions in the Europe telematics market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Commercial Dominance Meets Passenger Acceleration

Commercial vehicles accounted for 64.21% of the Europe telematics market share in 2025, delivering predictable ROI through fuel saving, route adherence, and driver-behavior improvements. Demand stays resilient as regulatory reporting aligns with freight-capacity expansion across pan-European corridors, anchoring the Europe telematics market size to a stable, heavy-duty foundation. Buses and coaches add incremental revenue as electrified public-transport fleets require battery-state-of-charge monitoring and depot-charging orchestration, tasks unserved by legacy ticketing systems.

Passenger cars, while smaller today, post the highest growth pace at a 16.79% CAGR to 2031 as embedded SIM penetration and usage-based insurance (UBI) unlock consumer segments. Active UBI policies are set to climb from 13.0 million in 2023 to 17.6 million in 2028, funneling fresh data volumes into actuarial models that reward safe driving with tangible premium discounts. Light commercial vehicles (LCVs) bridge both worlds, absorbing passenger-car electronics while satisfying business-grade logistics metrics, ensuring sustained double-digit adoption rates throughout the forecast window.

By Solution Type: Fleet Management Leadership Faces Insurance Disruption

Fleet-management and asset-tracking platforms held 37.12% of the Europe telematics market size in 2025, reflecting mature value proofs around fuel costs, maintenance scheduling, and duty-of-care compliance. Continuous feature enrichment, video‐based driver coaching, cargo-temperature validation, and multi-modal dashboard aggregation, keeps renewal rates high among large logistics operators.

Insurance and usage-based telematics, however, top the growth chart at a 15.61% CAGR as actuarial models migrate from static demographics to real-time behavioral scoring. Italy alone hosts 9.5 million active insurance-telematics policies, propagating best practices to Germany, the UK, and France. Safety-and-security sub-verticals ride mandatory eCall adoption, while remote diagnostics gain traction as OEMs expose prognostic code libraries to third-party developers, widening the solutions funnel across the Europe telematics market.

By Technology: Embedded Solutions Dominate Integration Strategies

Embedded units captured 61.88% of the Europe telematics market share in 2025 and are slated to grow at 16.76% CAGR, solidifying OEMs’ long-term stake in data stewardship. Such factory-installed modules enable bi-directional gateways for OTA recalls, feature paywalls, and subscription-based comfort upgrades. As a result, suppliers such as Proemion advocate OEM-grade integrations over retrofits, citing access to proprietary engine-control data that elevates service accuracy.

Tethered and smartphone solutions remain relevant for older vehicles or cost-sensitive users, but continuous price erosion in embedded-module electronics narrows that niche. Aftermarket black boxes must therefore pivot to software-first offerings, AI-powered anomaly detection, multi-fleet data aggregation, and regulatory dashboards, to retain their foothold within the evolving Europe telematics market.

By Deployment Mode: OEM Line-Fit Platforms Reshape Market Dynamics

OEM line-fit platforms constituted 55.93% of the Europe telematics market size in 2025 and expand at a 16.31% CAGR as connectivity migrates from optional upgrade to default vehicle architecture. Direct data pipes simplify fleet integrations and eliminate installation downtime, unlocking faster time-to-value for end users. Still, aftermarket providers hold strategic ground where mixed fleets require single-pane-of-glass analytics that merge line-fit feeds with legacy vehicles.

Integration middleware from firms such as Geotab helps fleets normalize heterogeneous data, a critical step when scaling analytics across brands and model years. Ultimately, the Europe telematics market rewards providers that orchestrate flexible deployments, blending OEM endpoints with value-added cloud services rather than relying solely on hardware attachments.

Geography Analysis

Germany anchored 28.52% of the Europe telematics market in 2025, assisted by OEM headquarters, industrial fleet density, and clear regulatory roadmaps that incentivize compliance-driven upgrades. The Smart Tachograph 2 rollout and Deutsche Telekom’s phased 2G shutdown accelerate hardware refreshes, locking in a 15.41% national CAGR through 2031.

Across the Channel, the United Kingdom sustains solid demand buoyed by its dynamic motor-insurance market, where UBI policies support high telematics penetration and competitive pricing. France follows closely: Direct Assurance’s YouDrive program doubled in size within two years, underscoring consumer readiness to exchange data for savings. Italy’s mature insurance-telematics ecosystem offers a template for neighboring Spain and Portugal, each witnessing fleet-modernization initiatives tied to EU recovery funds. Nordic countries present advanced digital-fleet landscapes, with ABAX tracking 500,000 assets across Sweden, Norway, Denmark, and Finland. High environmental standards support carbon-analytics dashboards, while public subsidies for electric vehicles push telematics deeper into small-business delivery fleets. Eastern Europe, though from a lower base, benefits from rising cross-border commerce and EU infrastructure grants, ensuring steady, if heterogeneous, contribution to the overall Europe telematics market.

Competitive Landscape

The Europe telematics industry shows moderate fragmentation: the top five vendors jointly hold just under 40% of installed units, leaving room for regional specialists and vertical-focused entrants. Aftermarket stalwarts such as Webfleet Solutions and Verizon Connect face disruptive OEM–supplier tie-ups like the Targa Telematics–Volkswagen accord that bypass plug-in hardware and give fleets direct access to richer, warranty-grade data streams.

Insurance-telematics niches display higher consolidation; OCTO Telematics, Targa Telematics, and CMT collectively underwrite a majority of active policies, leveraging actuarial depth to fend off newcomers. Fleet-management, by contrast, remains regionally diverse, with southern European fleets still opting for local vendors able to navigate multi-lingual compliance forms. Strategic M&A, Ctrack buying Inseego’s telematics unit and AddSecure absorbing Astrata Europe, signals a race to scale service portfolios and balance-sheet strength in anticipation of larger OEM-data licensing fees.

Technology convergence shifts competitive emphasis toward advanced analytics and AI-driven insights: route-level carbon footprint scoring, predictive brake-wear alerts, and dynamic toll optimization. Players unable to invest in cloud-native development risk margin compression as connectivity becomes commoditized. Those forging deep API partnerships with OEMs or mobility-payments platforms stand to capture recurring revenue streams, reinforcing competitive moats across the Europe telematics market.

Europe Telematics Industry Leaders

Verizon Communications Inc.

Masternaut Limited

Webfleet Solutions B.V.

ABAX UK Ltd.

Targa Telematics S.p.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Targa Telematics and Volkswagen Group Info Services AG ink partnership to ingest OEM vehicle data directly into Targa’s fleet portal, enabling hardware-free services spanning maintenance, theft-recovery, and EV energy management.

- February 2025: TÜV Rheinland certifies Flaircomm Microelectronics’ 4G/5G-ready T-Box for Next Generation eCall, ensuring compliance with EU Regulation 2024/1180 ahead of the January 2027 cutoff.

- January 2025: Cambridge Mobile Telematics powers Direct Assurance’s YouDrive, France’s largest connected-insurance program, serving 60,000 customers and saving drivers EUR 200 annually on average.

- January 2025: AXA Partners enters talks to acquire EBTS Pro Assist, aiming to build Europe’s top truck-assistance provider through digital-workflow integration.

Europe Telematics Market Report Scope

Telematics refers to the set of technologies used to monitor a wide range of information concerning an individual vehicle or fleet. A Telematics system can gather information, including driver behavior, location, engine diagnostics, and vehicle activity, and help fleet operators to visualize the data generated on the software platform to manage their resources. The scope of the study includes the vehicle type, including passenger and commercial.

The Europe Telematics Market is segmented by Vehicle Type (Commercial (Current Market Scenario and Installed Base, Penetration of LCV vs. MCV/HCV, Telematics Service Revenue Analysis, Country (United Kingdom, Germany, France, Italy, Spain, Benelux, Norway, Sweden, Poland, Denmark, Finland, Rest of Europe)), Passenger Vehicle (Current Market Scenario and Installed Base of Embedded OEM Telematics Systems, and Region Analysis - Qualitative Analysis of Trends and Dynamics)). The market sizes and forecasts are provided in terms of the installed base of telematics systems for all the segments.

By Vehicle Type

| Commercial Vehicles (LCV, MCV, HCV, Buses) |

| Passenger Cars |

By Solution Type

| Fleet Management and Asset Tracking |

| Safety and Security (eCall, SVT) |

| Insurance / Usage-Based Telematics |

| Infotainment and Navigation |

| Remote Diagnostics and Predictive Maintenance |

By Technology

| Embedded |

| Tethered / Smartphone-Integrated |

| Aftermarket Black-Box |

By Deployment Mode

| OEM Line-Fit Platforms |

| Aftermarket Service Providers |

By Country

| United Kingdom |

| Germany |

| France |

| Italy |

| Spain |

| Netherlands |

| Sweden |

| Norway |

| Denmark |

| Finland |

| Poland |

| Russia |

| Rest of Europe |

| By Vehicle Type | Commercial Vehicles (LCV, MCV, HCV, Buses) |

| Passenger Cars | |

| By Solution Type | Fleet Management and Asset Tracking |

| Safety and Security (eCall, SVT) | |

| Insurance / Usage-Based Telematics | |

| Infotainment and Navigation | |

| Remote Diagnostics and Predictive Maintenance | |

| By Technology | Embedded |

| Tethered / Smartphone-Integrated | |

| Aftermarket Black-Box | |

| By Deployment Mode | OEM Line-Fit Platforms |

| Aftermarket Service Providers | |

| By Country | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Sweden | |

| Norway | |

| Denmark | |

| Finland | |

| Poland | |

| Russia | |

| Rest of Europe |

Key Questions Answered in the Report

How large is the Europe telematics market in 2026?

The Europe telematics market size is 28.16 million installed units in 2026.

What is the forecast CAGR for telematics adoption in Europe to 2031?

Installed units are projected to grow at a 14.97% CAGR between 2026 and 2031.

Which vehicle segment is expanding the fastest?

Passenger cars lead growth at a 16.79% CAGR due to embedded connectivity and insurance telematics.

Why are embedded solutions gaining share over aftermarket hardware?

Factory-fitted modules provide direct OEM data, enable OTA updates, and remove installation downtime, supporting a 16.76% CAGR for embedded technology.

What regulatory changes most influence adoption through 2027?

Next Generation eCall and Smart Tachograph 2 mandates require 4G/5G-ready units and digital driver records across light-duty vans and trucks.

Page last updated on: