Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 17.16 Billion |

| Market Size (2026) | USD 18.42 Billion |

| Market Size (2031) | USD 23.02 Billion |

| Growth Rate (2026 - 2031) | 4.56% CAGR |

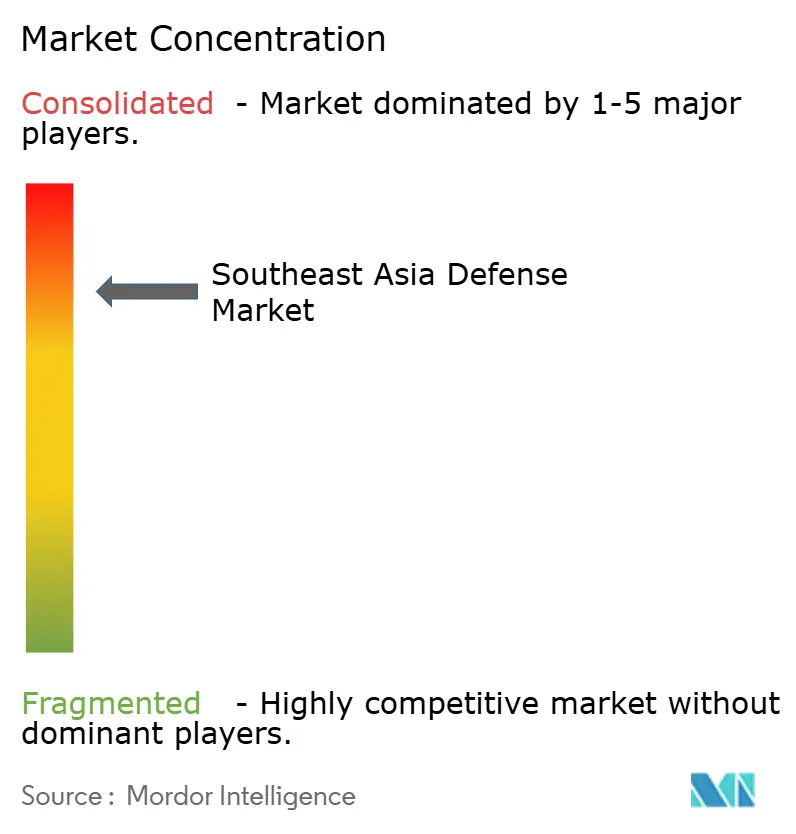

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Southeast Asia Defense Market Analysis by Mordor Intelligence

The Southeast Asia defense market size is expected to grow from USD 17.16 billion in 2025 to USD 18.42 billion in 2026 and is forecasted to reach USD 23.02 billion by 2031 at a 4.56% CAGR over 2026-2031. As territorial coercion in the South China Sea collides with budget pressures, pushing capitals toward selective modernization, this growth is expected to continue. Escalating gray-zone incidents, joint procurement initiatives, and widening technology transfer clauses are reshaping acquisition priorities, tilting budgets toward network-centric assets, loitering munitions, and integrated air defense systems. Western primes still dominate headline platform awards, yet South Korean, Israeli, and Turkish suppliers are eroding their lead by promising faster delivery schedules and deeper industrial offsets. At the same time, sovereign-capability mandates are beginning to redirect procurement dollars to local yards and assembly lines, signaling a measured but persistent shift away from dependence on imported systems. Overall, the Southeast Asia defense market is shifting from opportunistic fleet upgrades to long-range force-structure planning that integrates external deterrence with domestic economic multipliers.

Key Report Takeaways

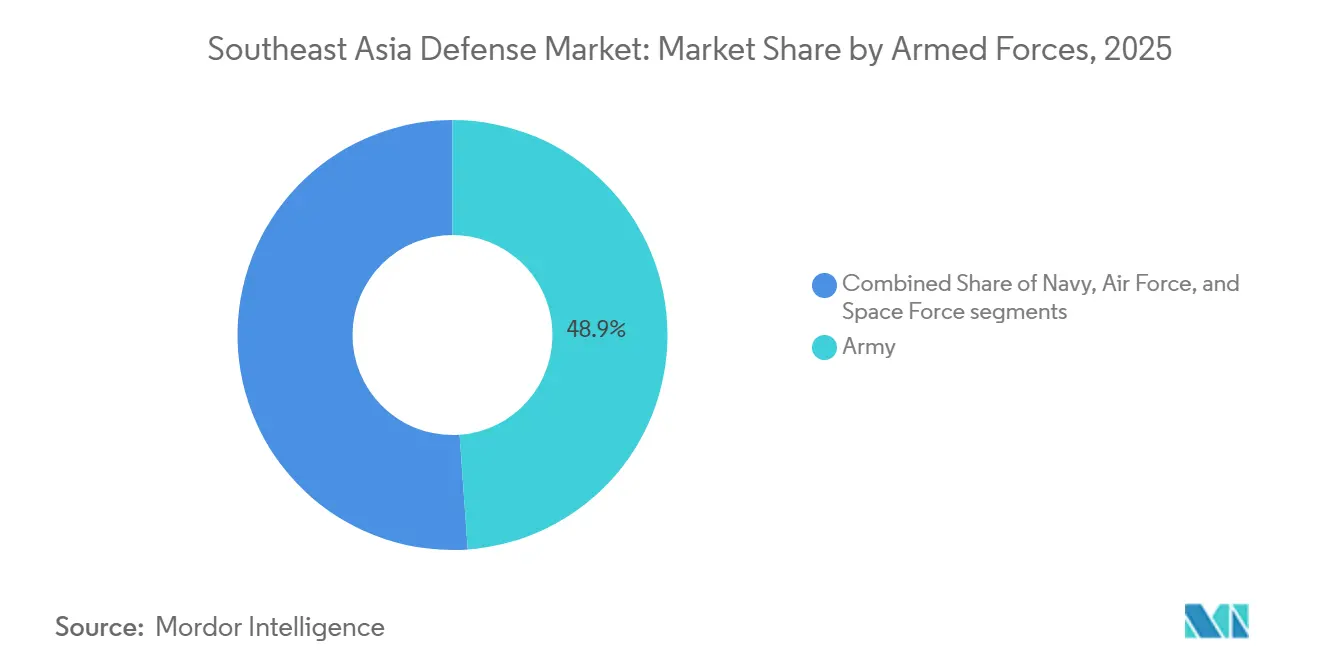

- By armed forces, the army led with 48.87% of the Southeast Asia defense market share in 2025, while the air force is projected to expand at a 5.29% CAGR through 2031.

- By type, vehicles accounted for 42.87% of the Southeast Asia defense market in 2025; unmanned systems are expected to grow the fastest, at a 6.22% CAGR, to 2031.

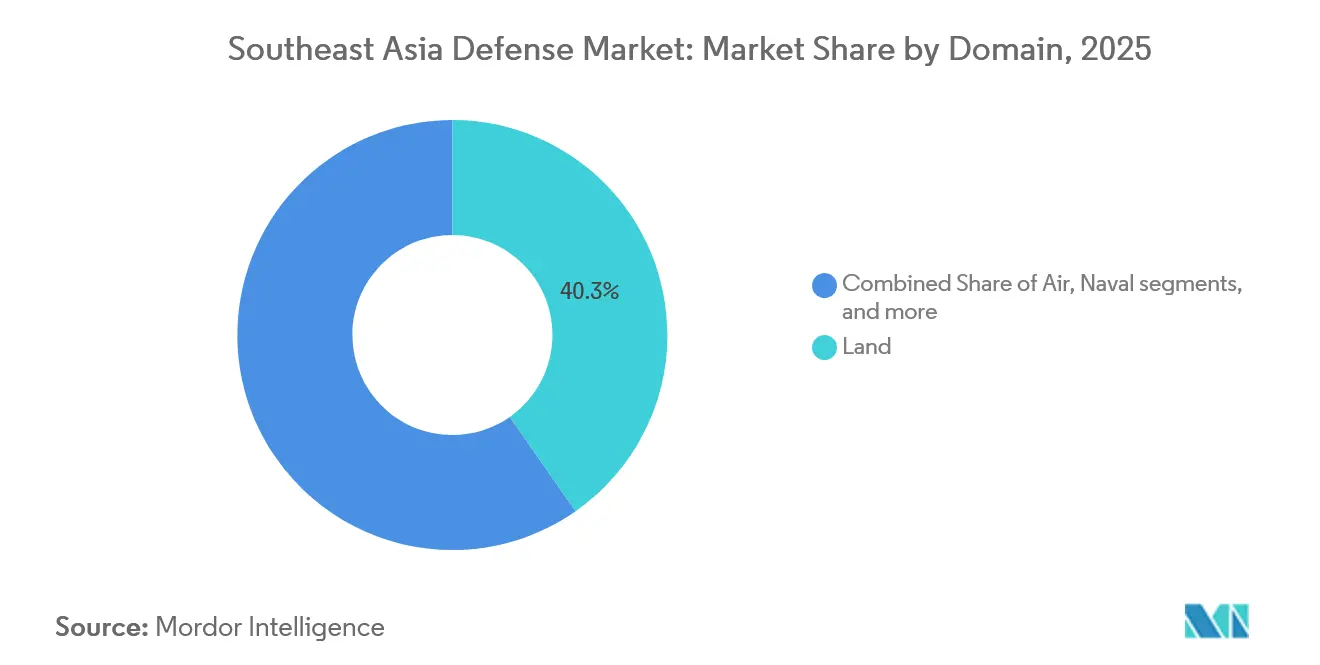

- By domain, the land segment captured 40.29% of spending in 2025, whereas the air domain is set to rise at a 4.95% CAGR, underpinned by multi-role fighter and UAV procurement.

- By procurement nature, foreign procurement still accounted for 53.87% of outlays in 2025, yet indigenous production will accelerate at a 5.12% CAGR through 2031 as technology-transfer clauses expand.

- By geography, Indonesia accounted for 36.78% of regional expenditure in 2025, while the Philippines will register the fastest growth at a 4.87% CAGR over the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Southeast Asia Defense Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating territorial disputes in the South China Sea | +1.20% | Philippines, Vietnam, Indonesia, Malaysia | Medium term (2-4 years) |

| Modernization of ASEAN defense budgets | +0.90% | Indonesia, Singapore, Thailand, Vietnam | Long term (≥ 4 years) |

| Shift toward network-centric warfare and C4ISR procurement | +0.70% | Singapore, Malaysia, Thailand, Indonesia | Medium term (2-4 years) |

| Rising counterterrorism and maritime security needs | +0.60% | Philippines, Indonesia, Malaysia, Thailand | Short term (≤ 2 years) |

| Incentives for indigenous defense-industrial capabilities | +0.50% | Philippines, Indonesia, Malaysia, Thailand | Long term (≥ 4 years) |

| Regional joint-procurement and interoperability initiatives | +0.30% | ASEAN-wide (notably Singapore, Malaysia, Thailand) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating Territorial Disputes in the South China Sea

China’s expanded coast-guard patrols have reduced the procurement cycle from a decade to just 18 months as frontline states prioritize missiles, maritime-patrol UAVs, and multi-role fighters that impose cost without escalating to open conflict.[1]Reuters Staff, “Philippines Says China Coast Guard Fired Water Cannon at its Boats,” reuters.com The Philippine Coast Guard recorded 187 Chinese interference episodes in 2024, a 34% increase over 2023, prompting Manila to fast-track the acquisition of BrahMos shore batteries and Hermes 900 UAVs. Vietnam discreetly expanded its Kilo-class submarine inventory, while Indonesia accelerated the delivery of 42 Rafale fighters to patrol the Natuna Sea. Budget reallocations are shifting money away from legacy armor toward ISR, anti-access, and long-range strike capabilities, anchoring the Southeast Asia defense market to those that deter gray-zone incursions. Consequently, procurement dialogue now begins with sensor fusion, precision engagement, and interoperability, relegating traditional platform counts to secondary status.

Modernization of ASEAN Defense Budgets

Defense allocations across ASEAN increased by 7.5% to USD 54.9 billion in 2024, outpacing global growth and signaling a sustained political commitment despite macroeconomic and fiscal headwinds.[2]SIPRI, “Military Expenditure Database 2024,” sipri.org Indonesia alone spends USD 20.3 billion annually under its Minimum Essential Force blueprint, which aims to procure 8 submarines, 12 frigates, and 144 fighters by 2029. Singapore, with the region’s highest per-capita defense bill, is integrating F-35Bs, Aster 30 missiles, and autonomous surface craft into a seamless multi-layer shield. Thailand is repurposing a flat THB 227 billion (USD 6.5 billion) budget toward network-enabled artillery and counter-drone systems. At the same time, the Philippines has enacted a 5% R&D reinvestment clause to prime its budding defense industrial base. These moves underscore how modernization now straddles capability ambition and economic multiplier, hardwiring domestic-industry incentives into every significant order.

Shift Toward Network-Centric Warfare and C4ISR Procurement

Singapore’s Integrated Knowledge-based Command and Control (IKC2) architecture, in service since 2024, compresses the sensor-to-shooter loop to 90 seconds and has become the regional benchmark for joint-force integration.[3]ST Engineering, “Annual Report 2024,” stengg.com Malaysia’s Network Centric Operations Capability mirrors the concept by linking FA-50s, Scorpene submarines, and Kedah-class cutters via Link 16, reducing target engagement cycles to under 4 minutes. Thailand’s USD 340 million Saab contract stitches Gripen E fighters into ground SAM batteries, while Indonesia is investing in a military-only satellite to bridge archipelagic connectivity gaps. Non-traditional suppliers, particularly Israel Aerospace Industries, are capitalizing on this opportunity, displacing older US radar suites with turnkey multi-mission sensors that bundle electronic-attack functions. As a result, C4ISR now commands nearly one-fifth of new-start budgets across the Southeast Asia defense market, and integration readiness is eclipsing unit cost as the decisive award metric.

Rising Counterterrorism and Maritime Security Needs

Despite a pivot toward external defense, terrorism and piracy still siphon resources. The 2024 Jolo bombing propelled Manila to acquire 120 MRAPs and six AW109 helicopters for rapid response in Mindanao. Indonesia logged a 22% uptick in Malacca Strait piracy, triggering orders for eight fast-attack craft with thermal imagers and stabilized guns. Malaysia's Eastern Sabah Security Command now accounts for 18% of the Royal Malaysian Navy's operations budget, maintaining 18 OPVs and a dozen UAVs to interdict Abu Sayyaf militants. Persistent low-intensity threats, therefore, remain a parallel driver that channels funding into ISR, protected lift, and precision fires even as nations reorient toward conventional deterrence.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fiscal pressures constraining defense outlays | -0.80% | Thailand, Malaysia, Philippines | Short term (≤ 2 years) |

| Dependence on foreign technology and related delays | -0.60% | Vietnam, Indonesia, Malaysia, Thailand | Medium term (2-4 years) |

| Supply-chain disruptions affecting critical components | -0.40% | Singapore, Indonesia, Malaysia | Medium term (2-4 years) |

| Procurement paralysis driven by US-China competition | -0.30% | Vietnam, Malaysia, Thailand, Philippines | Short to medium term (≤ 4 years) |

| Source: Mordor Intelligence | |||

Fiscal Pressures Constraining Defense Outlays

Tourism-led revenue softness kept Thailand's 2025 budget flat at THB 227 billion (USD 7.31 billion), forcing the army to postpone a second VT-4 tank tranche and suspend submarine talks with China. Malaysia's MYR 9 billion (USD 2.31 billion) Littoral Combat Ship program is five years late after corruption probes froze payments, leaving only four operational frigates to cover a 4,675 km coastline. The Philippines missed 2025 disbursement targets by 18% as debt service swallowed 9.3% of GDP, stretching BrahMos payments across three fiscal years. Indonesia's plan assumes 5% annual growth, but 2025 allocations rose just 3.2%, nudging frigate and tank projects into the 2027-2029 window. These funding squeezes are trimming near-term procurement appetites and could shave almost 1 percentage point off the Southeast Asia defense market's five-year growth trajectory.

Dependence on Foreign Technology and Related Delays

Semiconductor shortages pushed Singapore’s first Type 218SG submarine commissioning from Q2 2025 to Q4 2026, underscoring how supply-chain fragility can derail even well-funded programs. Indonesia’s Scorpene project demonstrates that the promised 40% local content remains aspirational, as PT PAL lacks the capability to machine pressure hulls, compelling France to ship pre-fabricated modules. Malaysia’s KAI FA-50s were delivered without Link 16 cryptos because US export licenses were delayed by 18 months, and Vietnam’s outreach for F-16s remains in limbo as Washington weighs the optics of replacing Russian hardware. Such bottlenecks magnify schedule risk, inflate sustainment costs, and temper the otherwise solid demand fundamentals underpinning the Southeast Asia defense market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Armed Forces: Air Power Gains as Maritime Threats Escalate

The Air Force segment is expected to grow at a 5.29% CAGR, driven by the rapid procurement of multi-role fighters, maritime patrol aircraft, and integrated air defense networks. Singapore’s eight-unit F-35B package, Indonesia’s 42 Rafales, and Malaysia’s FA-50s collectively represent more than USD 8 billion in near-term obligations, a testament to the primacy of the air domain. In contrast, the Army held 48.87% of 2025 spending, but heavy-armor programs are plateauing as capitals favor network-enabled, quick-reaction vehicles such as Strykers and MRAPs. The Navy’s roughly 28% share is protected by submarine and frigate pipelines that now include local workshare provisions.

Growth momentum in the Air Force lineage is anchored in contested-airspace scenarios over the South China Sea, driving demand for AESA radars, beyond-visual-range missiles, and Link 16 connectivity. Thailand is negotiating for six additional Gripen E fighters that can integrate into Saab-led C2 networks, while the Philippines is weighing the Gripen E against the F-16V for a 12-jet requirement with a focus on anti-ship strike capabilities. The Southeast Asia defense market size for Air Force assets is projected to reach USD 9.1 billion by 2031, marking a significant increase that will further shift regional power balances.

By Type: Unmanned Systems Surge on ISR and Loitering-Munition Demand

In 2025, vehicles accounted for 42.87% of the expenditure. However, with slowing armor refresh cycles and a shift toward lighter protected mobility, growth is expected to level off. Unmanned systems, by contrast, will expand at a 6.22% CAGR, becoming the standout gainer inside the Southeast Asia defense market. Twelve Hermes 900s for the Philippines, six Anka-S UAVs for Malaysia, and the upcoming Elang Hitam production run in Indonesia demonstrate how governments are embracing drones to patrol vast maritime zones without risking their crews.

C4ISR and EW allocations now account for 18% of spending and are expected to increase as joint-force data fusion becomes standard practice. Weapons and ammunition hover at 15% but will escalate once the Philippines and Vietnam lock in surface-to-surface missile options. Personnel Training and Protection account for around 8%, yet immersive simulation suites linked to remote-learning nodes could unlock new demand. Space and cyber systems remain embryonic but are increasingly bundled into network-centric bids, ensuring they claim a growing slice of the Southeast Asia defense market over the long run.

By Domain: Air Domain Strengthens, Land Moderates

The land domain captured 40.29% of the 2025 funding, thanks to legacy armor and artillery; however, its share will erode as budgets shift toward air-denial and undersea warfare. High-ticket fighter programs, ISR platforms, and layered SAM networks fuel the Air domain’s projected 4.95% CAGR. Naval allocations, roughly 32% today, will climb marginally on the back of Indonesia’s Scorpene submarines and Malaysia’s catch-up frigate builds.

Space lingers below 2%, a figure likely to double once Indonesia launches its military satellite in 2027, while cyber and electromagnetic investments approach 4% as capitals hedge against electronic warfare threats. The Southeast Asia defense market size tied to the Air domain is expected to eclipse USD 10 billion by 2031, eclipsing Land by mid-decade if current ordering trends persist.

By Procurement Nature: Indigenous Production Accelerates on Sovereignty Mandates

Foreign procurement still accounts for 53.87% of spending, primarily in submarines, fighters, and complex missiles. Yet Indigenous Production is forecast to expand at 5.12% annually as content quotas tighten. Indonesia’s PT Pindad, Malaysia’s Mildef, and Thailand’s Lopburi ammunition plant collectively symbolize a regional determination to anchor value locally. Philippine legislation that channels 5% of every contract into domestic research and development is already seeding new drone and armored-vehicle prototypes.

Sustainment economics amplify the shift: Singapore Technologies Engineering captures a 40% MRO share by offering multi-OEM certification under one roof, reducing turnaround time by 30% compared to shipping airframes back to Europe or the US. As these ecosystems mature, the Southeast Asia defense market is expected to see the foreign-procurement ratio shift toward parity with locally produced content shortly after 2030.

Geography Analysis

Indonesia’s USD 6.8 billion allocation in 2025 confirms its dominance; however, only sustained budget growth of 3-4% will keep pace with its 17,000-island operational theater. Jakarta’s Minimum Essential Force plan earmarks 42 Rafales, 6 Scorpenes, and 8 FREMM frigates; local content requirements are creating a robust tier-2 supplier network that will support everything from pressure-hull assembly to mission-system software. Despite leadership in absolute dollars, delivery timelines, and technology-transfer friction could temper Indonesia’s contribution to the collective Southeast Asia defense market over the next five years.

The Philippines, growing from a smaller base, is racing to field credible deterrence assets before 2030. Contracts awarded since 2024 already top USD 2.1 billion and include BrahMos batteries, Hermes 900 UAVs, and two Hyundai-built frigates. The Revised AFP Modernization Program’s 4.87% CAGR ensures Luzon and Palawan will host new missile regiments, while Clark Air Base prepares for 12 multi-role fighters. If execution matches ambition, Manila will add nearly USD 2 billion to the Southeast Asia defense market size by 2031, outpacing every neighbor on a percentage basis.

Singapore’s military remains the region’s technological vanguard. The initial pair of F-35Bs arrived in 2026, joining Type 218SG submarines, Heron 1 UAVs, and the IKC2 backbone to deliver real-time joint fires. With defense spending protected by bipartisan consensus, Singapore will continue to invest in cyber, space-based ISR, and autonomous surface craft. Although small in dollar terms, its laboratory role means that systems first proven here often migrate to wider ASEAN fleets, indirectly multiplying its impact on the Southeast Asia defense market.

Competitive Landscape

Western primes, including Lockheed Martin Corporation, Airbus SE, The Boeing Company, Singapore Technologies Engineering Ltd, and Thales Group, continue to win the most visible platform contracts. Still, regional buyers now evaluate offers through the triple lens of delivery speed, financing flexibility, and the depth of technology transfer. US Foreign Military Sales timelines often extend beyond three years, creating opportunities for South Korea’s KAI and Hanwha, as well as Israel Aerospace Industries, to secure orders with delivery cycles of 15 to 24 months. Russian firms are losing ground amid parts shortages driven by sanctions.

Singapore Technologies Engineering Ltd. leverages its proximity and multi-OEM certifications to dominate the maintenance, repair, and overhaul market. Servicing 14 air forces, it captures 40% of the region’s MRO revenue and cements local control over sustainment, often the most significant lifetime cost driver. In the artillery and ammunition sector, Hanwha’s partnership with Indonesia’s PT Pindad is shifting market share away from legacy US providers, underscoring how co-production can trump brand prestige.

Cyber-defense, EW, and space ISR remain white spaces. Elbit Systems’ 2025 radar deal in the Philippines illustrates how bundling electronic-attack capabilities with standard sensors can influence award decisions. Suppliers prepared to deliver integrated kill chains and open-architecture software are best positioned to capture the next wave of growth in the Southeast Asia defense market.

Southeast Asia Defense Industry Leaders

Lockheed Martin Corporation

Airbus SE

The Boeing Company

Singapore Technologies Engineering Ltd.

Thales Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Navantia and Thales inked a deal at Defense & Security 2025 in Bangkok. The agreement centers on supplying Thales' IFF systems, set to upgrade two Pattani-class OPVs and the HTMS Chang LPD. This collaboration not only marks their inaugural partnership in Thailand but also bolsters the Royal Thai Navy's ongoing fleet modernization efforts.

- September 2025: Thales and Malaysia's ADS inked a deal at DSEI 2025 to supply vehicle-mounted HF XL TRC 3900 radio systems. This move positions Malaysia as the inaugural Asian client for the HF XL technology, which was showcased at Eurosatory 2024 and boasts enhanced data rates and robust long-range communication capabilities.

Southeast Asia Defense Market Report Scope

The Southeast defense market spans all primary armed services, from the Army and Navy to the Air Force and the newly emerging Space Force, underscoring the region's commitment to multi-domain defense readiness. Key focus areas encompass personnel training and protection, C4ISR and electronic warfare, vehicles, weapons and ammunition, unmanned systems, and space and cyber systems, catering to both conventional and asymmetric operational needs.

These capabilities span land, air, naval, space, and cyber domains, emphasizing the region's pivot towards integrated, network-centric operations. Procurement strategies strike a balance between indigenous production, driven by the goals of national industrial base development and technology sovereignty, and foreign procurement, which is crucial for accessing advanced platforms, sensors, and systems that are not available domestically.

The Southeast defense market is segmented by armed forces, type, domain, procurement nature, and geography. By armed forces, the market is segmented into the Air Force, Army, Navy, and Space Force. By type, the market is segmented into personnel training and protection, C4ISR and electronic warfare, vehicles, weapons and ammunition, unmanned systems, and space and cyber systems. By domain, the market is segmented into land, air, naval, space, and cyber and electromagnetic spectrum. By procurement nature, the market is segmented into indigenous production and foreign procurement. The report also offers the market size and forecasts for seven countries across the region. For each segment, the market sizing and forecasts have been done based on value (USD)

Source: https://www.mordorintelligence.com/industry-reports/europe-defense-market

By Armed Forces

| Air Force |

| Army |

| Navy |

| Space Force |

By Type

| Personnel Training and Protection |

| C4ISR and Electronic Warfare (EW) |

| Vehicles |

| Weapons and Ammunition |

| Unmanned Systems |

| Space and Cyber Systems |

By Domain

| Land |

| Air |

| Naval |

| Space |

| Cyber and Electromagnetic Spectrum |

By Procurement Nature

| Indigenous Production |

| Foreign Procurement |

By Geography

| Indonesia |

| Singapore |

| Thailand |

| Malaysia |

| Vietnam |

| Philippines |

| Rest of Southeast Asia |

| By Armed Forces | Air Force |

| Army | |

| Navy | |

| Space Force | |

| By Type | Personnel Training and Protection |

| C4ISR and Electronic Warfare (EW) | |

| Vehicles | |

| Weapons and Ammunition | |

| Unmanned Systems | |

| Space and Cyber Systems | |

| By Domain | Land |

| Air | |

| Naval | |

| Space | |

| Cyber and Electromagnetic Spectrum | |

| By Procurement Nature | Indigenous Production |

| Foreign Procurement | |

| By Geography | Indonesia |

| Singapore | |

| Thailand | |

| Malaysia | |

| Vietnam | |

| Philippines | |

| Rest of Southeast Asia |

Key Questions Answered in the Report

How large is the Southeast Asia defense market in 2026?

The Southeast Asia defense market size stands at USD 18.42 billion in 2026 and is projected to reach USD 23.02 billion by 2031.

Which armed-forces branch is growing the fastest?

The Air Force segment is expected to post the highest CAGR at 5.29% through 2031 on continuing fighter, UAV, and air-defense procurements.

What drives demand for unmanned systems?

Maritime-domain awareness and the need to monitor disputed reefs without risking crews are pushing Unmanned Systems to a 6.22% CAGR.

Why are indigenous-production mandates important?

Clauses that require 35–40% local content shift value-addition to domestic plants, cutting sustainment costs and reducing export-control risk.

Which country will grow spending the quickest?

The Philippines is forecasted to record a 4.87% CAGR through 2031 as its USD 35 billion modernization plan prioritizes external-defense capabilities.

Which suppliers are filling gaps created by long US delivery timelines?

Korea Aerospace Industries, Hanwha Defense, and Israel Aerospace Industries are winning contracts by offering 15- to 24-month delivery windows and flexible financing.

Page last updated on: