Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

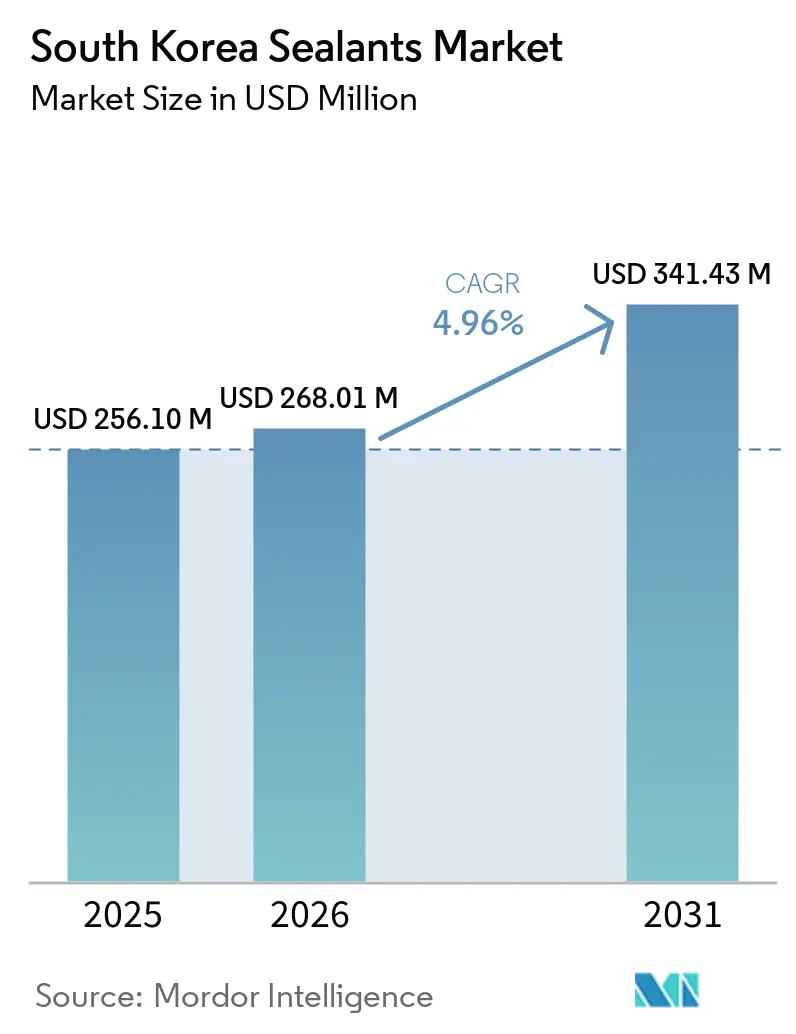

| Base Year Market Size (2025) | USD 256.10 Million |

| Market Size (2026) | USD 268.01 Million |

| Market Size (2031) | USD 341.43 Million |

| Growth Rate (2026 - 2031) | 4.96% CAGR |

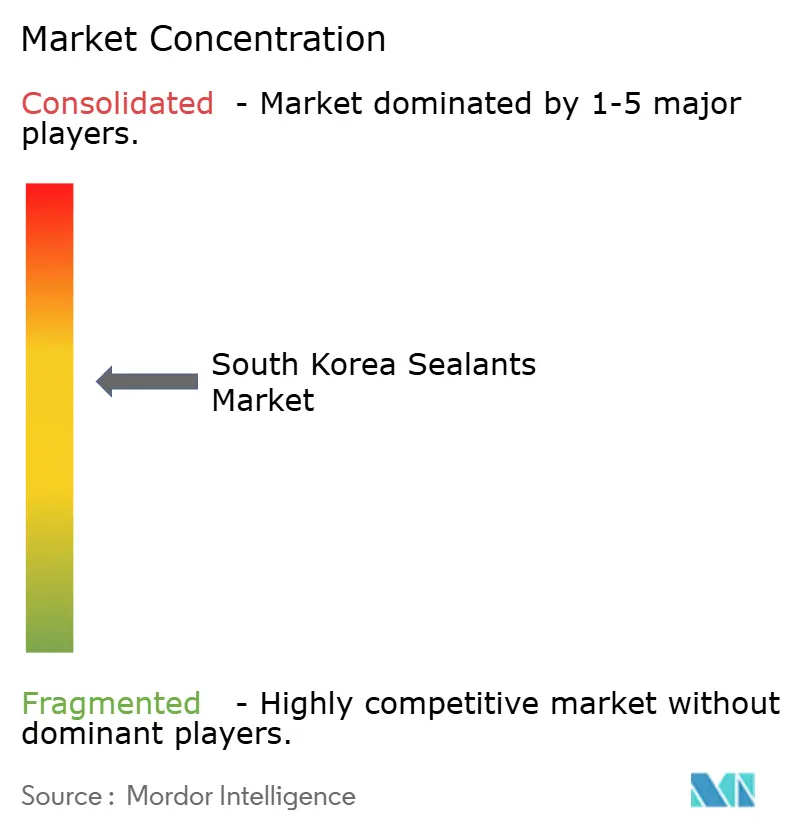

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Korea Sealants Market Analysis by Mordor Intelligence

The South Korea Sealants Market size is projected to expand from USD 256.10 million in 2025 and USD 268.01 million in 2026 to USD 341.43 million by 2031, registering a CAGR of 4.96% during 2026-2031. Accelerating adoption of multi-material bonding in autos, a pivot to low-VOC chemistries in construction, and the rise of advanced semiconductor packaging are reshaping demand patterns. Local OEMs now prize sealants that resist galvanic corrosion, cure at ambient temperatures, and tolerate dissimilar-material interfaces, prompting formulators to widen portfolios around silicone, MS-polymer, polyurethane, and epoxy technologies. Public spending on modular housing and infrastructure retrofits fortifies baseline consumption, while battery-pack thermal-gap sealing and defense MRO create premium niches that lift average realized prices. Competitive rivalry remains intense as multinational producers expand local capacity and domestic specialists push into electronics and medical-grade opportunities despite raw-material price swings and tighter K-REACH compliance.

Key Report Takeaways

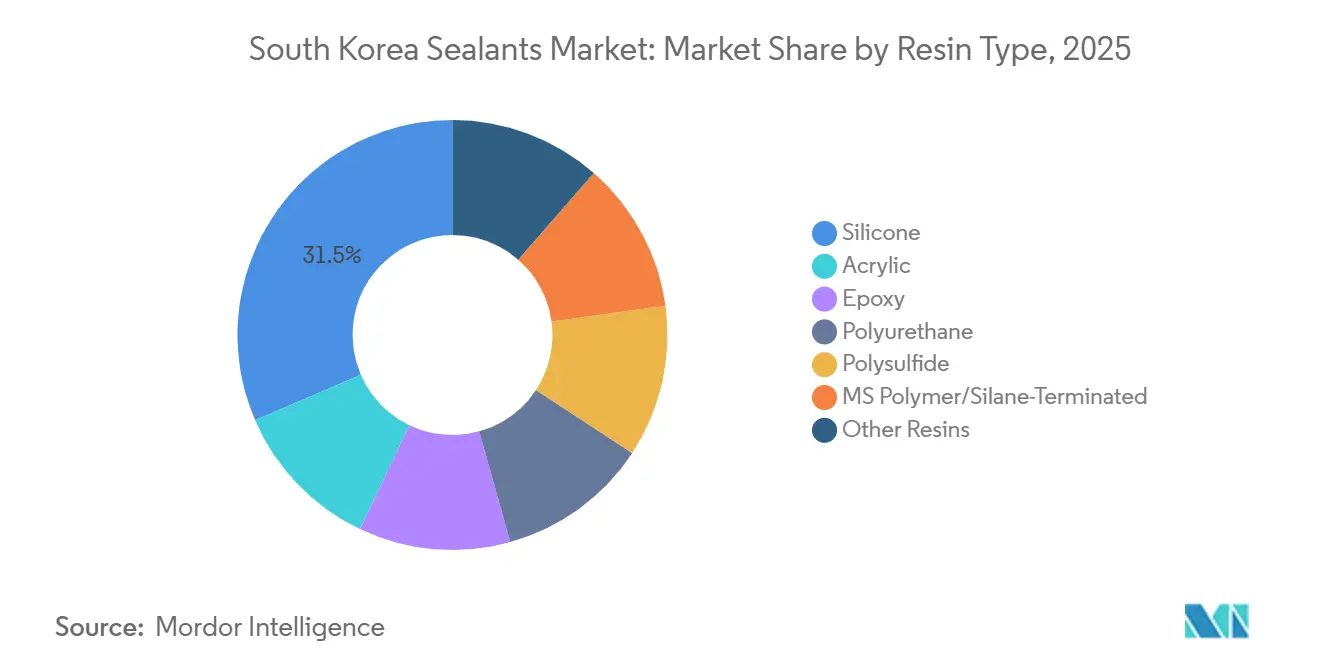

- Silicone led with 31.50% of 2025 resin-type revenue, while MS polymer/silane-terminated formulations are projected to deliver the fastest growth at a 6.45% CAGR to 2031.

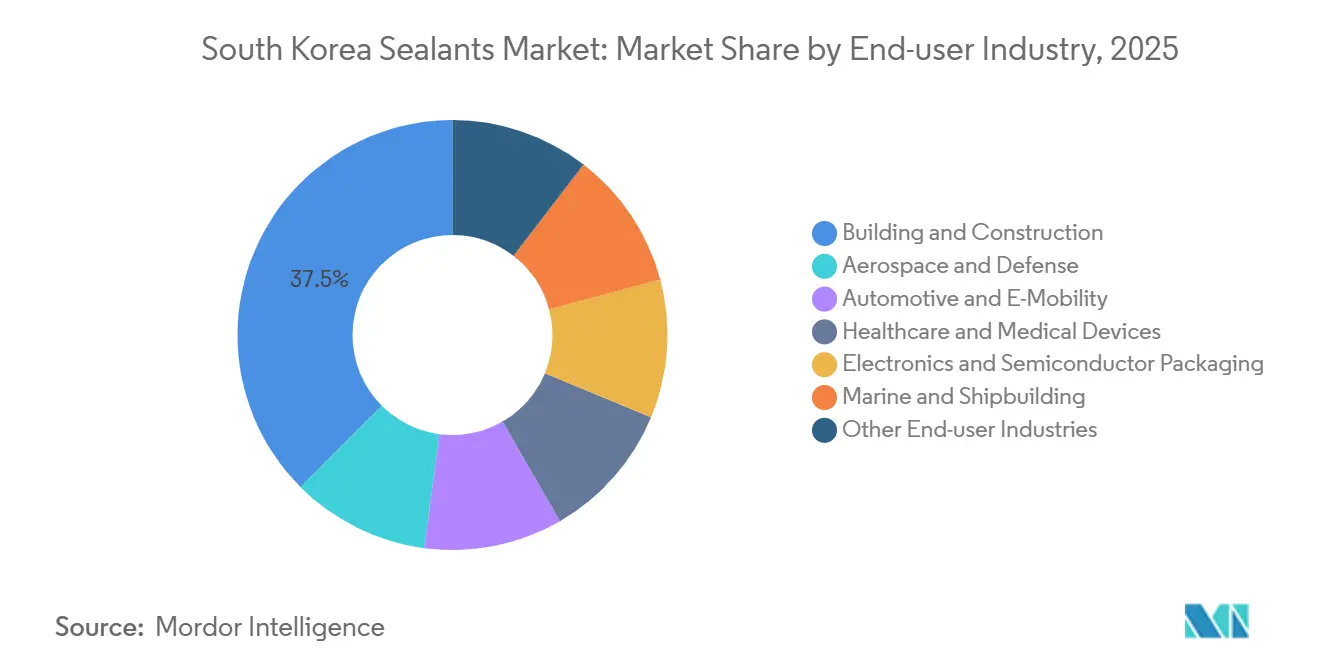

- Building and construction captured 37.50% of the 2025 end-user value; electronics and semiconductor packaging are forecast to advance at a 6.41% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South Korea Sealants Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| OEM platform-wide shift to lightweight multi-material bonding | +1.2% | National, concentrated in Ulsan, Gwangju automotive clusters | Medium term (2-4 years) |

| Rapid scaling of prefabricated modular construction in high-seismic zones | +0.9% | National, early gains in Seoul, Busan, Incheon metro areas | Short term (≤ 2 years) |

| EV battery-pack thermal-gap sealing mandates | +1.4% | National, with spillover to export-oriented battery plants | Medium term (2-4 years) |

| Defense composite-skin MRO boom | +0.6% | National, centered on Sacheon F-35 depot and Hanwha facilities | Long term (≥ 4 years) |

| Aging civil infrastructure retrofit subsidies | +0.8% | National, prioritizing Seoul metro, provincial highways | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

OEM Platform-Wide Shift to Lightweight Multi-Material Bonding

Carmakers are replacing spot welding with structural adhesives to join aluminum, carbon fiber, and ultra-high-strength steel without galvanic corrosion. Hyundai Mobis recorded an 18% year-on-year rise in adhesive and sealant use per vehicle in 2024 as modular platforms proliferated. The move increases demand for two-component epoxies that cure on moving lines and elastic MS-polymer bead sealants that absorb differential expansion. LG Chem and HL Mando signed a joint agreement in February 2025 to co-develop thermal gap fillers and insulating adhesives for ADAS electronics, underscoring convergence between sealing, thermal management, and electrical insulation[1]Business Korea, “LG Chem, HL Mando Team Up on Thermal Gap Fillers,” businesskorea.co.kr.

Rapid Scaling of Prefabricated Modular Construction in High-Seismic Zones

Government-backed modular housing legislation from 2024 drives prefabrication adoption, requiring factory-applied sealants that remain watertight during lifting and seismic cycles. Demonstrations by the Korea Institute of Civil Engineering and Building Technology cut on-site labor 40% through pre-cured silicone and MS-polymer joints[2]Korea Institute of Civil Engineering and Building Technology, “Modular Housing Demonstration,” kict.re.kr. The Ministry of Land, Infrastructure and Transport allocated KRW 62.4 trillion (USD 46.8 billion) for 2026, with dedicated retrofit and modular pilot funding that guarantees near-term volume lift.

EV Battery-Pack Thermal-Gap Sealing Mandates

Thermal runaway mitigation elevates gap-filling sealants to safety-critical status in 800 V packs. Arkema unveiled Bostik gasketing and debond-on-demand adhesives at Interbattery 2026 in Seoul, targeting cell-to-pack assembly requiring 3 W/m·K conductivity. LG Chem’s gap fillers passed harsh-condition trials for ADAS modules, illustrating higher thermal and dielectric standards for next-generation mobility electronics.

Defense Composite-Skin MRO Boom

South Korea’s F-35 depot status raises demand for polysulfide and epoxy sealants certified for composite-skin repairs. Hanwha Aerospace expanded MRO capacity in 2024, needing non-exothermic cures that preserve radar-absorbent laminates. Low-volume, high-margin military approvals create barriers that favor incumbents with qualified materials.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Import-price volatility of specialty silicones | -0.7% | National, affecting all end-use sectors | Short term (≤ 2 years) |

| Deficit of local GMP-grade clean-room compounding capacity | -0.4% | National, concentrated impact on pharmaceutical and medical-device segments | Medium term (2-4 years) |

| PFAS phase-out compliance costs | -0.5% | National, acute in semiconductor and aerospace applications | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Import-Price Volatility of Specialty Silicones

South Korea relies on imported chlorosilane intermediates, exposing formulators to feedstock swings. Liquid silicone rubber prices spiked in August 2025 and cooled by December, squeezing margins on fixed-price construction contracts. Wacker Chemie’s Jincheon expansion hedges some risk but still depends on imported silicon metal. Price pressure is steering commodity users toward domestically available acrylic and MS-polymer options when performance allows.

Deficit of Local GMP-Grade Clean-Room Compounding Capacity

Few Korean sealant makers run ISO Class 7 lines certified under the Ministry of Food and Drug Safety’s February 2026 KGMP revision. Pharmaceutical OEMs therefore import medical-grade silicones from Japan and Germany, facing long lead times and currency exposure. High capital cost and multi-year validation deter local entrants, slowing penetration of domestic medical sealants.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin Type: MS Polymer Leads Growth Amid Silicone Dominance

Silicone accounted for 31.50% of 2025 revenue, supported by broad operating-temperature tolerance and primer-free adhesion. The chemistry anchors curtain-wall glazing, auto powertrain gasketing, and electronics potting, preserving its leading South Korea sealants market share through 2031. Yet specification priorities are quietly shifting. Contractors replacing neutral-cure silicone with MS polymer hybrids avoid acetic-acid byproducts, cut VOCs, and protect aluminum curtain walls under stricter K-REACH thresholds. MS polymer sealants are forecast to expand at a 6.45% CAGR through 2031, as evidenced by DNV-approved shipbuilding grades such as MTG COATWEL SEAL 211 that promise faster paint-over times and low odor.

Polyurethane remains preferred in below-grade waterproofing and expansion joints thanks to superior elongation and hydrolysis resistance. Roadseal’s two-component UC-261 membrane meets KS F 3211 and secures rooftops and balconies. Epoxy chemistries dominate semiconductor underfill, die-attach, and molding compounds, where COFA’s low-CTE products cure at 80 °C while limiting warpage to protect high-bandwidth memory stacks. Acrylic latex sealants retain share in interior soundproofing and gypsum board joints but face margin pressure from commodity pricing. Polysulfide stays irreplaceable in fuel-tank sealing and marine below-waterline interfaces due to unmatched fuel and saltwater resistance, sustaining a small but lucrative niche.

By End-User Industry: Electronics Outpaces Construction

Building and Construction generated 37.50% of the 2025 value, driven by curtain walls and infrastructure joints. Permit declines and a softer housing cycle, however, temper growth, as seen in Ogong’s 34.9% operating-profit fall in 2025. In sharp contrast, the electronics and semiconductor packaging segment is projected to grow at a 6.41% CAGR through 2031, outstripping the overall South Korea sealants market. SK Hynix’s USD 13 billion high-bandwidth memory complex plus Samsung’s advanced packaging lines require sub-10 µm gap-fill sealants with tight viscosity windows and zero-void performance, pulling specialized epoxy, silicone, and acrylic materials.

Automotive and E-Mobility presents a bifurcated outlook: declining internal-combustion demand lowers body sealer tonnage while electric-vehicle battery packs, ADAS cameras, and 800 V drivetrains need flame-retardant potting and gap-filling grades. LG Chem-HL Mando collaboration targets these niches with UL 94 V-0 silicones entering volume production in 2026. Aerospace and Defense, though with just a single-digit share, delivers superior margins through certified polysulfide and epoxy systems for F-35 composite repairs and shipboard composite retrofits. Healthcare and Medical Devices will remain supply-constrained until additional GMP-grade capacity arrives, giving foreign suppliers short-term pricing power.

Geography Analysis

Seventy percent of South Korea sealants market demand concentrates along the Seoul–Incheon–Busan industrial corridor. The 2026 MOLIT budget hike channels KRW 2.9 trillion to rail safety and KRW 2.6 trillion to road maintenance, ensuring steady polyurethane and acrylic injection volumes for void filling and crack sealing. Modular housing pilots in metropolitan areas install factory-cured silicone and MS-polymer joints that bypass sub-5 °C on-site curing bottlenecks, expanding urban uptake.

Ulsan and Gwangju clusters intensify lightweight bonding, with Hyundai Mobis citing an 18% climb in adhesive and sealant kilograms per vehicle in 2024, anchoring automotive consumption. Battery-cell and module plants in Ochang, Gumi, and Cheongju consume thermal gap fillers and dielectric potting grades that satisfy 800 V breakdown thresholds for European and North American OEM export contracts.

Regional disparities persist. Rural provinces adopt modular methods more slowly due to scarce crane fleets and limited contractor familiarity, curbing immediate sealant conversion. Busan has emerged as an application-engineering hub following Henkel’s February 2025 center opening that co-develops sustainable formulations with Korean brand owners. Sacheon’s defense depot for F-35 composite work fuels niche demand for polysulfide sealants qualified to MIL-S-8802, while Incheon’s shipyards seek cryogenic-rated silicones for LNG and future hydrogen carriers.

Competitive Landscape

The South Korea sealants market is moderately consolidated. Scale investments reinforce incumbency. Wacker Chemie’s Jincheon line, opened January 2025, ranks among Asia’s largest silicone sealant assets, combining high-throughput mixers and automated cartridge filling for automotive and glazing grades. Henkel’s Busan Application Center tailors bio-based and circular-design adhesives for sporting goods and electronics brands, signaling a sustainability-centric value pitch. Niche innovators emerge in electronics: COFA supplies underfill and die-attach epoxy for 2.5D and 3D memory stacks, while LG Chem leverages HL Mando’s systems know-how to merge thermal management and sealing in ADAS modules.

White-space plays revolve around GMP-grade medical silicones and PFAS-free semiconductor sealants. New MFDS rules from February 2026 tighten traceability, advantaging producers with validated clean rooms. The K-REACH PFAS ban drives demand for high-purity fluorine-free alternatives in wet-process equipment, where Dow and 3M leverage global research and development while domestic firms explore hybrid silicones with equal plasma resistance.

South Korea Sealants Industry Leaders

KCC SILICONE CORPORATION

Dow

Henkel AG & Co. KGaA

3M

Sika AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: The Ministry of Food and Drug Safety updated KGMP to require lot-level traceability and validated Class 7 mixing for pharmaceutical and medical-device sealants

- February 2025: LG Chem and HL Mando signed a joint-development pact to commercialize thermal gap fillers for ADAS control units and insulating adhesives for steering systems, with first mass production slated for 2026.

South Korea Sealants Market Report Scope

Sealants are elastomeric materials used to fill gaps, joints, or cracks, preventing water, air, dust, and fluid passage. Widely applied in construction and industrial sectors, they ensure waterproofing and structural flexibility in buildings, windows, automotive components, and appliances.

The South Korea sealants market is segmented by resin type and end-user industry. By resin type, the market is segmented into acrylic, epoxy, polyurethane, silicone, polysulfide, MS polymer/silane-terminated, and other resins. By end-user industry, the market is segmented into aerospace and defense, automotive and E-mobility, building and construction, healthcare and medical devices, electronics and semiconductor packaging, marine and shipbuilding, and other end-user industries. For each segment, the market sizing and forecasts have been done based on revenue (USD).

By Resin Type

| Acrylic |

| Epoxy |

| Polyurethane |

| Silicone |

| Polysulfide |

| MS Polymer/Silane-Terminated |

| Other Resins |

By End-user Industry

| Aerospace and Defense |

| Automotive and E-Mobility |

| Building and Construction |

| Healthcare and Medical Devices |

| Electronics and Semiconductor Packaging |

| Marine and Shipbuilding |

| Other End-user Industries |

| By Resin Type | Acrylic |

| Epoxy | |

| Polyurethane | |

| Silicone | |

| Polysulfide | |

| MS Polymer/Silane-Terminated | |

| Other Resins | |

| By End-user Industry | Aerospace and Defense |

| Automotive and E-Mobility | |

| Building and Construction | |

| Healthcare and Medical Devices | |

| Electronics and Semiconductor Packaging | |

| Marine and Shipbuilding | |

| Other End-user Industries |

Market Definition

- End-user Industry - Building & Construction, Automotive, Aerospace, Healthcare, and Others are the end-user industries considered under the sealants market.

- Product - All sealant products are considered in the market studied

- Resin - Under the scope of the study, resins like Polyurethane, Epoxy, Acrylic, Silicone, and Others are considered

- Technology - For the purpose of this study, One component and Two component sealant technologies are taken into consideration.

| Keyword | Definition |

|---|---|

| Hot-melt Adhesive | Hot melt adhesives are generally 100% solid formulations, based on thermoplastic polymers. They are solid at room temperature and are activated upon heating above their softening point, at which stage they are liquid, and hence, can be processed. |

| Reactive Adhesive | A reactive adhesive is made up of monomers that react in the adhesive curing process and do not evaporate from the film during use. Instead, these volatile components become chemically incorporated into the adhesive. |

| Solvent-borne Adhesive | Solvent-borne adhesives are mixtures of solvents and thermoplastic, or slightly cross-linked polymers, such as polychloroprene, polyurethane, acrylic, silicone, and natural and synthetic rubbers (elastomers). |

| Water-borne Adhesive | Water-borne adhesives use water as a carrier or diluting medium to disperse a resin. They are set by allowing the water to evaporate or be absorbed by the substrate. These adhesives are compounded with water as a diluent, rather than a volatile organic solvent. |

| UV Cured Adhesive | UV curing adhesives induce curing and create a permanent bond without heating by using ultraviolet (UV) light or other radiation sources. An aggregation of monomers and oligomers is cured or polymerized by ultraviolet (UV) or visible light in a UV adhesive. Because UV is a radiating energy source, UV adhesives are often referred to as radiation curing or rad-cure adhesives. |

| Heat-resistant Adhesive | Heat-resistant Adhesives refer to those that do not break down under high temperatures. One aspect of a complicated system of circumstances is the adhesive's capacity to withstand disintegration brought on by high temperatures. As the temperature rises, adhesives may liquefy. They can withstand stresses resulting from differing coefficients of expansion and contraction, which might be an additional advantage. |

| Reshoring | Reshoring is the practice of moving commodity production and manufacturing back to the nation where the business was founded. Onshoring, inshoring, and back shoring are further terms used. Offshoring, the practice of producing items abroad to lower labor and manufacturing costs, is the opposite of this. |

| Oleochemicals | Oleochemicals are compounds produced from biological oils or fats. They resemble petrochemicals, which are substances made from petroleum. The oleochemical business is built on the hydrolysis of oils or fats. |

| Nonporous Materials | Nonporous materials are substances that do not permit the passage of liquid or air. Nonporous materials are those that are not porous, such as glass, plastic, metal, and varnished wood. Since no air can get through, less airflow is required to raise these materials, negating the requirement for high airflow. |

| EU-Vietnam Free Trade Agreement | A trade agreement and an investment protection agreement were concluded between the European Union and Vietnam on June 30, 2019. |

| VOC content | Compounds with limited solubility in water and high vapor pressure are known as Volatile Organic Compounds (VOCs). Many VOCs are human-made chemicals that are used and produced in the manufacture of paints, pharmaceuticals, and refrigerants. |

| Emulsion Polymerization | Emulsion polymerization is a method of producing polymers or connected groups of smaller chemical chains known as monomers, in a water solution. The method is often used to make water-based paints, adhesives, and varnishes, in which the water stays with the polymer and is marketed as a liquid product. |

| 2025 National Packaging Targets | In 2018, the Australian Environment Ministry set the following 2025 National Packaging Targets: 100% of the packaging must be reusable, recyclable, or compostable by 2025, 70% of plastic packaging must be recycled or composted by 2025, 50% of average recycled content must be included in packaging by 2025, and problematic and unnecessary single-use plastic packaging must be phased out by 2025. |

| Russian Government’s Import Substitution Policy | The Western sanctions suspended the distribution of several high-tech items to Russia, including those required by the raw material export sectors and the military-industrial complex. In response, the government launched an "import substitution" scheme, appointing a special commission to oversee its implementation in early 2015. |

| Paper Substrate | Paper substrates are paper sheets, reels, or boards with a base weight of up to 400 g/m2 that has not been converted, printed or otherwise altered. |

| Insulation Material | A material that inhibits or blocks heat, sound, or electrical transmission is known as Insulation Material. The variety of insulation materials includes thick fibers like fiberglass, rock and slag wool, cellulose, and natural fibers as well as stiff foam boards and sleek foils. |

| Thermal Shock | A temperature change known as thermal shock generates stress in a material. It commonly results in material breakdown and is especially prevalent in brittle materials like ceramics. When there is a quick temperature change, either from hot to cold or vice versa, this process occurs abruptly. It occurs more frequently in materials with poor heat conductivity and insufficient structural integrity. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms