Global Western Blotting Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.79 Billion |

| Market Size (2031) | USD 2.39 Billion |

| Growth Rate (2026 - 2031) | 5.92% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

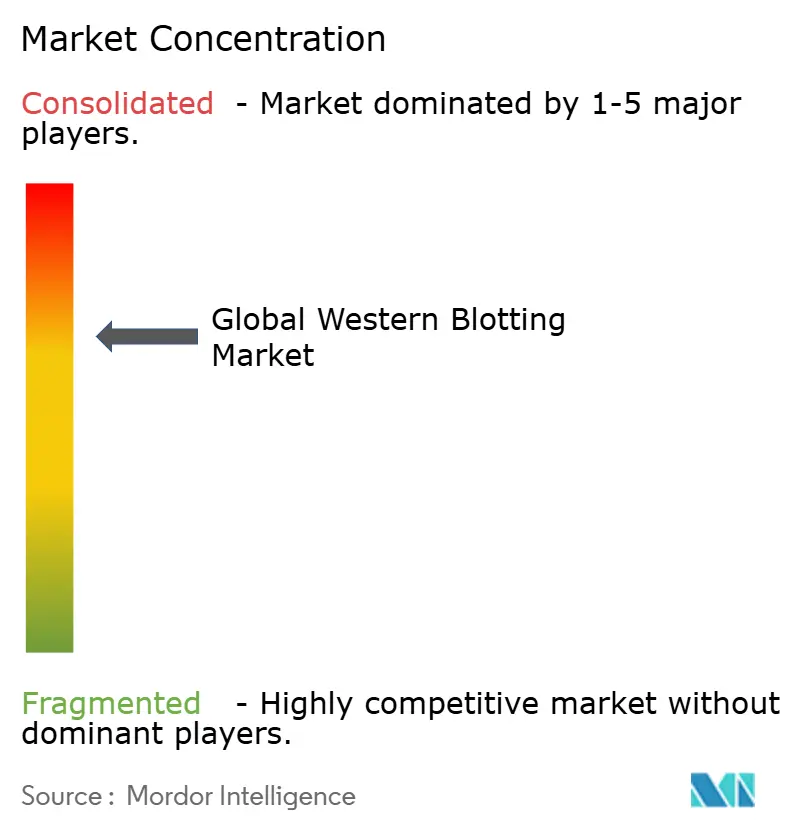

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Global Western Blotting Market Analysis by Mordor Intelligence

The western blot market size was valued at USD 1.69 billion in 2025 and estimated to grow from USD 1.79 billion in 2026 to reach USD 2.39 billion by 2031, at a CAGR of 5.92% during the forecast period (2026-2031). Increased chronic-disease incidence, the expansion of proteomics pipelines, and a wave of automation investments reinforce demand for protein confirmation assays in research and diagnostic workflows. Automated and microfluidic platforms are attracting laboratories that need higher throughput, less reagent consumption, and better reproducibility, while the ongoing preference for validated antibody-based techniques protects the core consumables business. Integration of artificial intelligence (AI) in antibody validation, tighter regulatory guidance on analytical robustness, and sustained life-sciences funding collectively anchor future growth for the Western blot market. Competitive pressure from multiplex immunoassays and mass-spectrometry-based approaches is intensifying, yet western blotting remains a benchmark method for confirming protein expression, post-translational modifications, and therapeutic product quality.

Key Report Takeaways

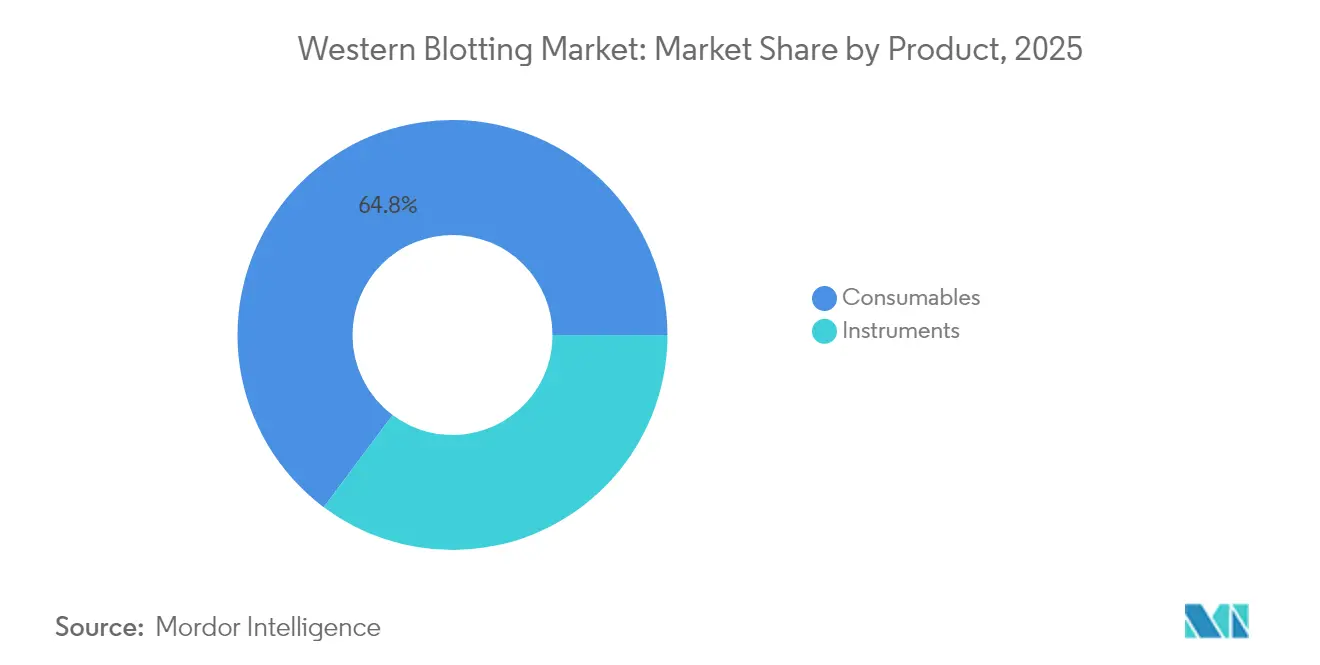

- By product type, consumables held 64.78% of the western blot market share in 2025, while automated and microfluidic instruments are projected to expand at a 7.68% CAGR through 2031.

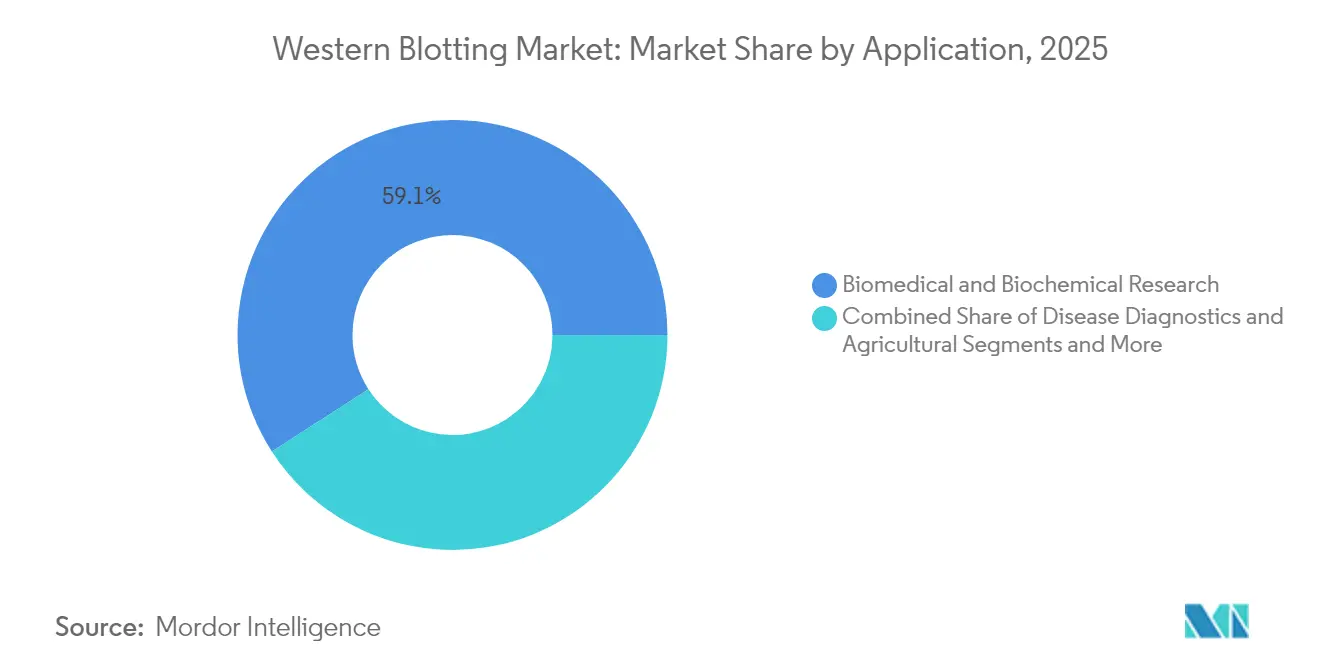

- By application, biomedical and biochemical research commanded a 59.12% share of the western blot market size in 2025; disease diagnostics is forecast to post a 7.12% CAGR to 2031.

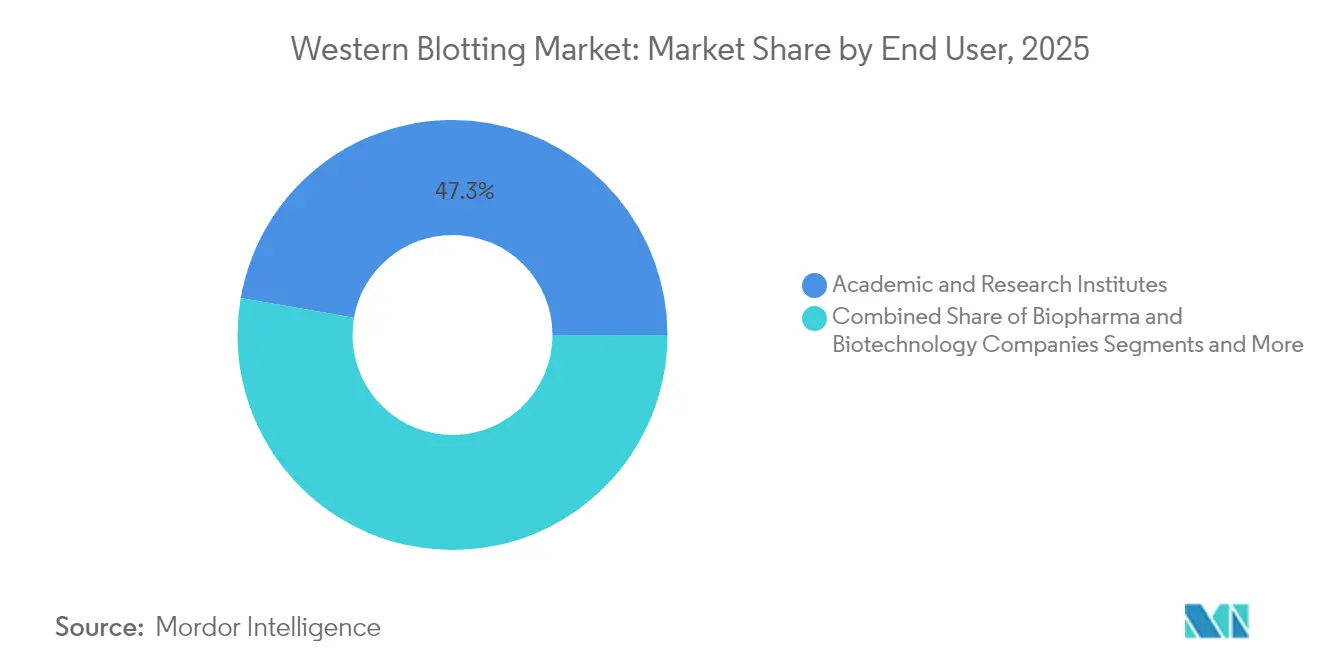

- By end-user, academic and research institutes led with 47.25% of the western blot market share in 2025, whereas hospitals and diagnostic laboratories are growing fastest at 6.93% CAGR.

- By geography, North America accounted for 41.62% revenue in 2025; Asia Pacific is the fastest-growing region, advancing at an 8.28% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Western Blotting Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence of Chronic Diseases | +1.20% | Global, North America & Europe focus | Long term (≥ 4 years) |

| Expansion of Proteomics & Biomarker Discovery Pipelines | +0.90% | Global, led by APAC & North America | Medium term (2-4 years) |

| Escalating Pharma/Biotech R&D Budgets | +0.80% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Adoption of Automated & Microfluidic WB Platforms | +1.10% | Global, early adoption in developed markets | Short term (≤ 2 years) |

| AI-Driven Antibody Validation Workflows | +0.70% | North America & EU, selective APAC | Medium term (2-4 years) |

| Regulatory Focus on Reproducible Protein Data | +0.60% | Global, stricter in North America & EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Chronic Diseases

Cancer incidence climbed 58% in Europe between 1995 and 2022, creating sustained demand for protein biomarker confirmation in tumor biology and metabolic-disorder studies.[1]Institute of Health Economics, “Cancer Incidence in Europe 1995-2022,” ihe.ieOncology research now requires the detection of low-abundance proteins and subtle post-translational changes, functions that western blotting supports reliably. The growing elderly population further enlarges case volumes for chronic conditions, reinforcing routine use of blot consumables and imaging reagents. As precision-medicine programs multiply, laboratories integrate automated blot platforms that handle higher throughput with minimal manual error. These patterns together lengthen the revenue runway for the Western blot market.

Expansion of Proteomics & Biomarker Discovery Pipelines

Large-scale proteomics initiatives are reshaping pharmaceutical discovery. Thermo Fisher Scientific’s USD 3.1 billion purchase of Olink added more than 5,300 validated biomarker targets to its portfolio.[2]BioPharm International, “Thermo Fisher Completes Olink Acquisition,” biopharminternational.com Single-cell protein assays enabled by microfluidic western blotting now reveal heterogeneity that bulk analyses miss. AI-driven antibody screening accelerates candidate selection, cutting validation time and widening use cases. Rising sales of tandem-mass-tag reagents, up 18% to USD 4.01 million in 2024, indicate vigorous spending on complementary proteomics tools. These trends underpin continuous platform upgrades within the Western blot market.

Escalating Pharma / Biotech R&D Budgets

Global pharmaceutical R&D spending remains robust, particularly in biologics where protein confirmation assays are mandated. Thermo Fisher recorded USD 42.879 billion in 2024 revenue, reflecting instrumentation demand across discovery and quality-control labs. Bio-Rad’s ChemiDoc Go system launch shows manufacturers allocating capital toward next-generation blot imaging workflows. Venture funding recovery in Asia is noticeable, funneling capital into start-ups that require standardized blot protocols to support regulatory submissions. As clinical pipelines diversify, validated western blot methods remain a foundational analytical step, bolstering long-term equipment and consumable sales.

Adoption of Automated & Microfluidic WB Platforms

Microfluidic western blot instruments can evaluate multiple proteins simultaneously while consuming roughly 1% of the antibody volumes used by conventional setups.[3]Analytical Chemistry, “Antibody-Efficient Microfluidic Western Blot,” acs.orgThese devices reduce total assay time from several hours to 10–60 minutes and deliver quantitative data with lower variability. Fully integrated centrifugal microfluidic systems now isolate and analyze exosomes within 45 minutes. Laboratories pursuing error-free workflows adopt automated sample loading and AI-enabled image analysis, supporting reproducibility mandates. While new platforms partially cannibalize legacy hardware, they expand the total addressable Western blot market by converting throughput-limited users.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Uptake of Alternative Immunoassay & Alpha Technologies | -1.40% | Global, faster adoption in developed markets | Medium term (2-4 years) |

| High Capital & Operating Cost of Western Blot Instruments & Antibodies | -0.80% | Global, more pronounced in emerging markets | Long term (≥ 4 years) |

| Antibody Batch-To-Batch Variability Undermining Reproducibility | -0.60% | Global, acute in academic & resource-limited settings | Short term (≤ 2 years) |

| Laboratory Decarbonization Targets Favoring Low-Reagent Assays | -0.30% | Europe, North America, select APAC countries | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Uptake of Alternative Immunoassay & Alpha Technologies

Parallel-reaction-monitoring mass spectrometry now offers antibody-free detection with enhanced sensitivity, directly challenging conventional immunoblotting. Multiplex platforms such as MSD, Luminex, and AlphaLISA permit simultaneous cytokine measurements with femtogram-level detection. These systems shorten assay time, simplify quantity, and align with high-throughput screening needs. Laboratories focused on speed and multiplexing migrate certain workflows away from western blotting, pressuring manufacturers to innovate with microfluidic chips and integrated imaging. While western blotting retains validation roles, the alternative technologies limit expansion in routine quantitation segments of the western blot market.

High Capital & Operating Cost of Western Blot Instruments & Antibodies

Advanced imaging platforms and capillary-based blots can exceed USD 120,000 initial cost, dampening purchase intent in smaller or emerging-market laboratories. Antibody catalogs have grown from 10,000 to over 6 million products in 15 years, but pricing and batch variability remain concerns. NIH grants awarded for ChemDoc MP systems illustrate the funding needed even for academic users. Non-animal-derived antibody formats promise unlimited supply and improved consistency yet still require awareness campaigns and upfront investment. Maintenance contracts, reagent replenishment, and operator training inflate lifetime ownership costs, leading cost-sensitive labs to postpone upgrades or adopt alternative assays.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Automation Broadens Capability and Efficiency

Consumables generated 64.78% of revenue in 2025, reflecting recurring sales of membranes, antibodies, buffers, and chemiluminescent substrates. This broad installed base secures stable cash flow for suppliers in the Western blot market. Automated and microfluidic instruments, while representing a smaller absolute revenue pool, are expanding at 7.68% CAGR to 2031 as users prioritize speed and low reagent footprints. Kit-based solutions further streamline workflows, lowering user variability and facilitating regulatory documentation. The segment’s resilience resides in unavoidable consumable replacement cycles, regardless of platform sophistication.

Microfluidic devices reduce antibody usage to 1% of conventional volumes, trimming per-assay costs and easing supply constraints. Imaging systems now include embedded AI algorithms that assess band intensity, reducing interpretation subjectivity. Traditional wet-transfer equipment still serves academic labs where capital budgets limit the adoption of high-end automation. Gel and capillary electrophoresis modules continue to bridge sample preparation with downstream blotting, supporting overall western blot market continuity.

By Application: Diagnostics Gains Momentum beside Research Dominance

Biomedical and biochemical research contributed 59.12% of demand in 2025 and remains critical for hypothesis testing, antibody screening, and pathway elucidation. The western blot market size for diagnostic applications, however, is anticipated to climb 7.12% CAGR through 2031 as hospitals adopt validated blot assays for therapeutic monitoring and rare-disease confirmation. Oncology, neurology, and infectious-disease labs prefer blotting for post-translational modification analysis, safeguarding its clinical relevance.

Regulatory focus on evidence-based biomarker validation prompts diagnostic labs to purchase fully validated kits, reducing assay-development timelines. Single-cell analysis advances expand the research scope, feeding incremental reagent demand and sustaining the Western blot market share. Agricultural and food-testing applications, although smaller, use blots to monitor allergen presence and genetically modified organism expression, thus broadening the method’s footprint.

By End-User: Academic Core Meets Clinical Uptake

Academic and research institutes controlled 47.25% of revenue in 2025, supported by public funding and long-standing curricular reliance on Western blot protocols. These centers maintain diverse instrument fleets and create consistent consumable pull-through. Hospitals and diagnostic laboratories exhibit a 6.93% CAGR as personalized medicine programs call for high-confidence protein conformation, pushing the western blot market size upward within clinical settings.

Pharmaceutical and biotechnology companies rely on western blotting for product characterization, stability studies, and regulatory submissions, allocating capital toward high-throughput, 21 CFR Part 11-ready instrumentation. Contract research and testing laboratories supplement capacity for smaller firms, amplifying consumables turnover and expanding geographical reach. The mixture of academic teaching demand and regulated-industry compliance needs secures a balanced growth pathway for the western blot market.

Geography Analysis

North America generated 41.62% of worldwide revenue in 2025, underpinned by mature research infrastructure, substantial biopharmaceutical R&D outlays, and rigorous regulatory oversight that values validated protein methods. The United States accounts for most sales, while Canada and Mexico contribute incremental gains through growing biotech clusters and clinical-trial activity. Government grants, venture capital flow, and an advanced supplier ecosystem foster early adoption of automated blot platforms, sustaining regional leadership.

Europe follows with well-established biotechnology hubs in Germany, the United Kingdom, France, and Switzerland. European regulators now demand reproducible analytics, reinforcing preferences for validated antibody sources and standard operating procedures. Switzerland’s biotech network of more than 1,500 companies and 60,000 jobs illustrates how concentrated innovation feeds equipment demand. Markets such as Italy and Spain add volume via pharmaceutical manufacturing and university research, though budget constraints influence instrument penetration rates.

Asia Pacific is the fastest-growing territory, projected at an 8.28% CAGR through 2031. China’s significant venture investments and state-sponsored life-sciences parks drive substantial procurement of blotting consumables and automated imaging systems. India accelerates adoption through government initiatives supporting translational research and domestic biologics production. Japan and South Korea leverage strong pharmaceutical bases and regulatory alignment with global standards to sustain replacement cycles. Australia and Southeast Asian countries, while smaller, are channeling grant funding toward proteomics facilities, strengthening regional participation in the western blot market. Collaborative models linking academia, government, and industry bolster infrastructure, ensuring long-term growth momentum.

Competitive Landscape

The western blot market shows moderate concentration, with a core set of global companies complemented by regional specialists and emerging innovators. Established suppliers compete on workflow integration, offering end-to-end platforms that span sample preparation to data analysis. Automation, AI-enabled imaging, and compliance-ready software are key differentiators. The August 2024 release of Bio-Rad’s ChemiDoc Go illustrates continued investment in compact, high-resolution imaging that targets both research and clinical labs.

Mergers and acquisitions accelerate technology consolidation. Thermo Fisher’s Olink acquisition expanded its proteomics footprint, creating bundled offerings that combine proximity-extension assays with blot verification. Roche’s plan to launch 75 new assays by 2029 signals a pipeline focus on high-value diagnostic solutions that may incorporate western blot readouts. Meanwhile, new entrants developing non-animal-derived antibodies challenge incumbents by promising batch-to-batch consistency and animal-welfare benefits.

Innovation hotspots include single-cell microfluidic blotting and exosome-specific transfer systems, areas where start-ups pilot disruptive platforms that shrink assay time and reagent cost. Mass-spectrometry vendors and multiplex immunoassay providers intensify competitive pressure, compelling western blot companies to emphasize validation pedigree and visual confirmation strengths. Overall, sustained R&D investment, strategic partnerships, and a pivot toward data-rich, automated workflows characterize competitive maneuvering within the western blot market.

Global Western Blotting Industry Leaders

Thermo Fisher Scientific, Inc.

Bio-Rad Laboratories, Inc.

PerkinElmer, Inc.

Merck & Co., Inc.,

Danaher Corporation (Cytiva)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Roche Diagnostics announced plans to launch 75 novel assays by 2029, including formats aligned with western blot testing applications.

- August 2024: Bio-Rad Laboratories introduced the ChemiDoc Go Imaging System for gels and western blots, expanding its life-science instrumentation portfolio.

- July 2024: Thermo Fisher Scientific completed the USD 3.1 billion acquisition of Olink Holding, adding over 5,300 validated protein biomarkers to its life-science solutions segment.

- June 2024: The FDA updated analytical method-validation guidance, clarifying expectations for specificity, range, and accuracy in protein analysis workflows.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Mordor Intelligence defines the western blotting market as the global revenue generated from instruments (gel and capillary electrophoresis units, semi-dry or wet transfer systems, imaging platforms) and consumables (membranes, reagents, primary and secondary antibodies, ready-to-use kits) that support protein separation, transfer, and immunodetection in research, diagnostics, agriculture, and quality-control workflows.

Scope exclusion: revenues from stand-alone research antibodies that are never used in blotting, as well as service outsourcing fees, sit outside this study.

Segmentation Overview

- By Product

- Instruments

- Gel & Capillary Electrophoresis Systems

- Traditional Wet / Semi-dry / Dry Blotting Systems

- Automated & Microfluidic Platforms

- Imagers

- Consumables

- Reagent and Buffers

- Kits

- Instruments

- By Application

- Biomedical & Biochemical Research

- Disease Diagnostics

- Agricultural & Food Safety Testing

- By End-User

- Academic & Research Institutes

- Biopharma & Biotechnology Companies

- Hospitals & Diagnostic Laboratories

- CROs & Contract Testing Labs

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Our analysts interviewed laboratory managers, clinical microbiologists, biotech procurement leads, and western-blot instrument product managers across North America, Europe, and Asia-Pacific. These discussions tested reagent consumption rates, price dispersion, and automation uptake, and they double-checked the assumptions drawn from desk work.

Desk Research

We began with publicly available life-sciences statistics from the NIH, CDC, Eurostat, and China's NHC, which quantify test volumes for HIV, Lyme disease, and other conditions routinely confirmed by western blot. Trade data from UN Comtrade and customs portals clarified annual imports of key membranes and precast gels, while professional societies such as the Human Proteome Organization and the American Society for Biochemistry provided adoption trend insights. Company 10-Ks, investor decks, and product catalogs informed average selling prices. Finally, paid databases, D&B Hoovers for company revenues and Questel for patent momentum, supplied further guardrails. This list is illustrative; many additional sources were reviewed to validate figures and narrative context.

Market-Sizing & Forecasting

A top-down build starts with disease testing volumes, proteomics grant outlays, and academic publication counts, which are then mapped to western-blot utilization coefficients. Select bottom-up checks, sampled instrument shipments and reagent kit roll-ups at prevailing ASPs, anchor totals. Key variables feeding the model include: (1) HIV confirmatory test volume, (2) per-lab blot frequency in proteomics projects, (3) automation penetration rates, (4) average kit ASP trajectories, and (5) regional research funding growth. Multivariate regression links these drivers to historical revenue, while scenario analysis adjusts for technology substitution. Data gaps in shipment tracking are bridged by triangulating import codes against primary-research estimates.

Data Validation & Update Cycle

Outputs pass two analyst reviews, variance alerts flag outliers versus prior editions, and material events, such as major reimbursement shifts, trigger interim revisions. The dataset is refreshed annually, after which an analyst performs a final sense-check before release to clients.

Why Mordor's Western Blotting Baseline commands reliability

Published values differ because firms choose contrasting scopes, price stacks, and refresh cadences.

Key gap drivers here include whether consumable revenues cover only core reagents or adjacent antibody portfolios, the treatment of regional ASP swings, and the depth of on-ground interview validation that Mordor analysts incorporate before locking the model.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.69 B (2025) | Mordor Intelligence | - |

| USD 1.97 B (2024) | Regional Consultancy A | Adds custom antibody services and lacks end-user interviews |

| USD 1.50 B (2023) | Trade Journal B | Counts consumables only and relies on literature averages |

| USD 2.02 B (2024) | Global Consultancy C | Applies uniform ASP growth and omits currency-conversion adjustments |

Taken together, the comparison shows that Mordor's disciplined scope definition, balanced driver selection, and yearly validation furnish decision-makers with a dependable, transparent baseline they can retrace and stress-test with confidence.

Key Questions Answered in the Report

What is the current size of the western blot market?

The market is valued at USD 1.79 billion in 2026 and is projected to reach USD 2.39 billion by 2031 at a 5.92% CAGR.

Which product category leads revenue in the western blot market?

Consumables dominate with 64.78% revenue share in 2025 owing to repeat purchases of membranes, antibodies, and buffers.

Why are automated and microfluidic systems growing so quickly?

They reduce reagent consumption, shorten assay time to as little as 10 minutes, and improve data reproducibility, driving an 7.68% CAGR through 2031.

Which region is expanding fastest for western blot adoption?

Asia Pacific shows the highest growth at an 8.28% CAGR, propelled by biotechnology investments in China, India, Japan, and South Korea.

How are regulatory changes influencing the western blot market?

Updated FDA and USP guidelines emphasize analytical reproducibility, favoring validated western blot platforms that include compliance-ready software and documentation.

What major competitive trends are shaping the western blot market?

Key trends include platform automation, AI-based antibody validation, strategic acquisitions like Thermo Fisher’s Olink deal, and emerging non-animal-derived antibody technologies.

Page last updated on: