Ligation Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.63 Billion |

| Market Size (2031) | USD 2.31 Billion |

| Growth Rate (2026 - 2031) | 7.18% CAGR |

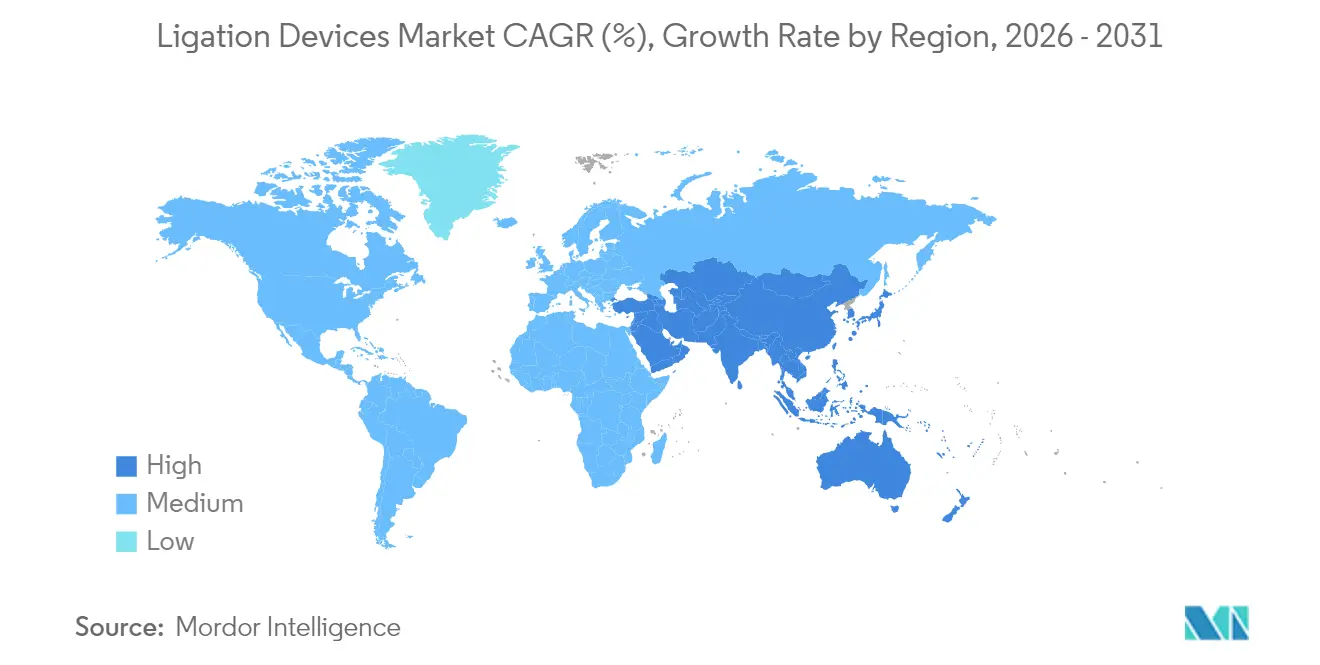

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

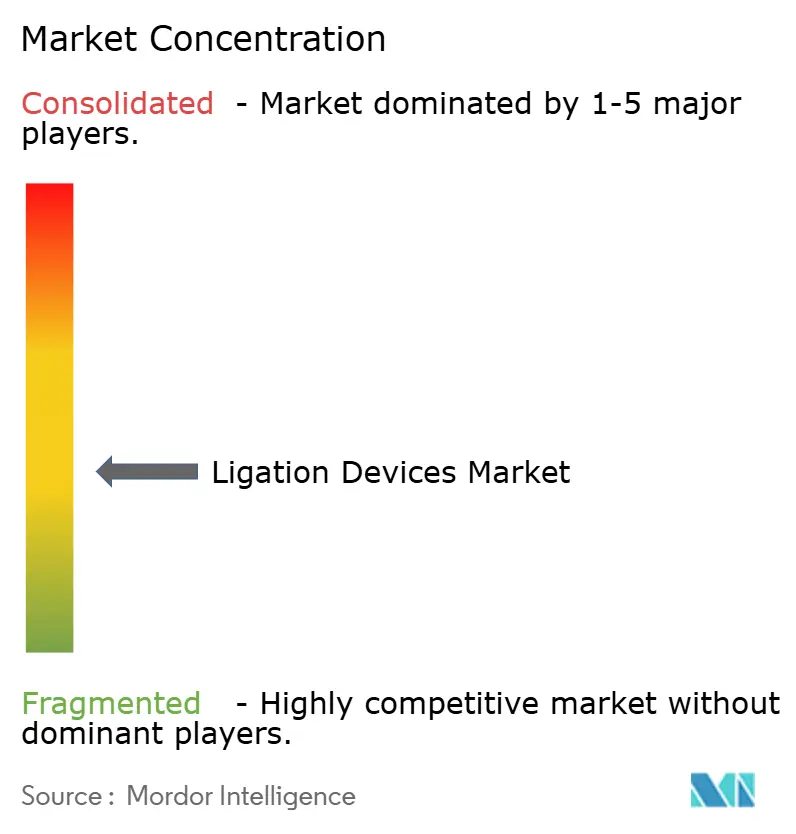

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ligation Devices Market Analysis by Mordor Intelligence

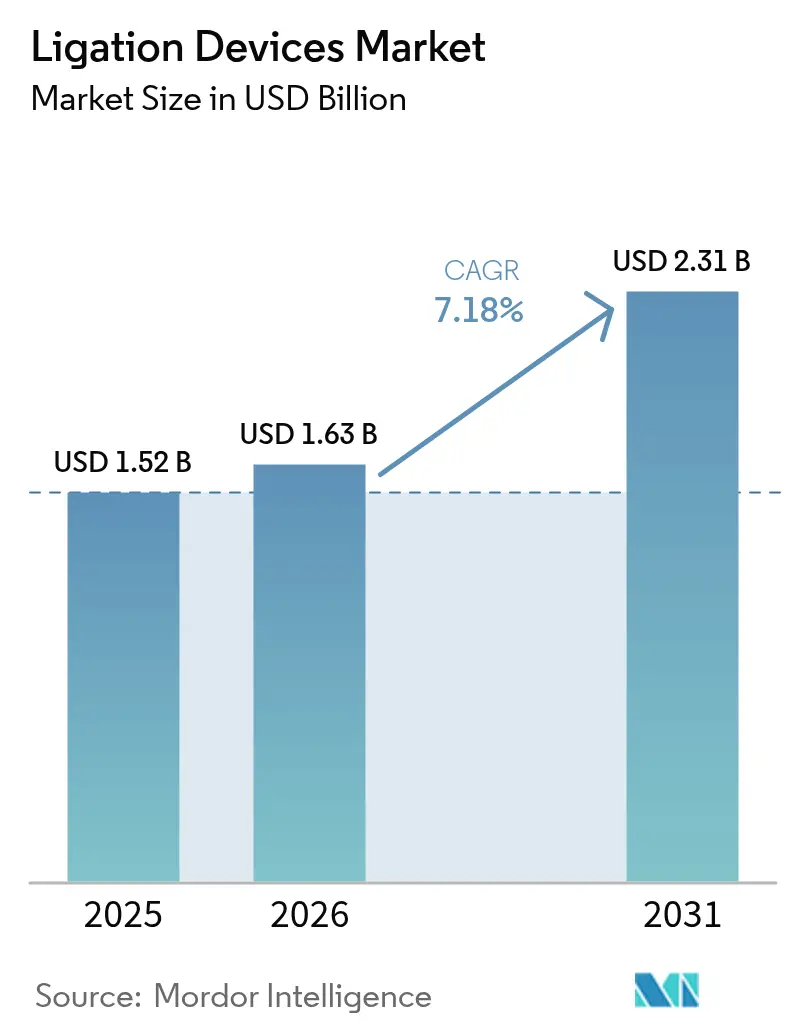

The Ligation Devices Market size is expected to grow from USD 1.52 billion in 2025 to USD 1.63 billion in 2026 and is forecast to reach USD 2.31 billion by 2031 at 7.18% CAGR over 2026-2031.

This momentum stems from rapid uptake of minimally invasive surgery, rising cardiovascular and urological caseloads, and continuous improvements in energy-based vessel-sealing systems that shorten seal time while boosting burst-pressure strength. Intensifying hospital emphasis on reduced length of stay, alongside payer incentives that reward lower peri-operative complication rates, further strengthens purchasing appetite for premium sealing platforms. Competitive differentiation now revolves around AI-enabled energy modulation, ergonomic hand instruments, and eco-friendly clip materials that address both surgical performance and sustainability mandates.

Key Report Takeaways

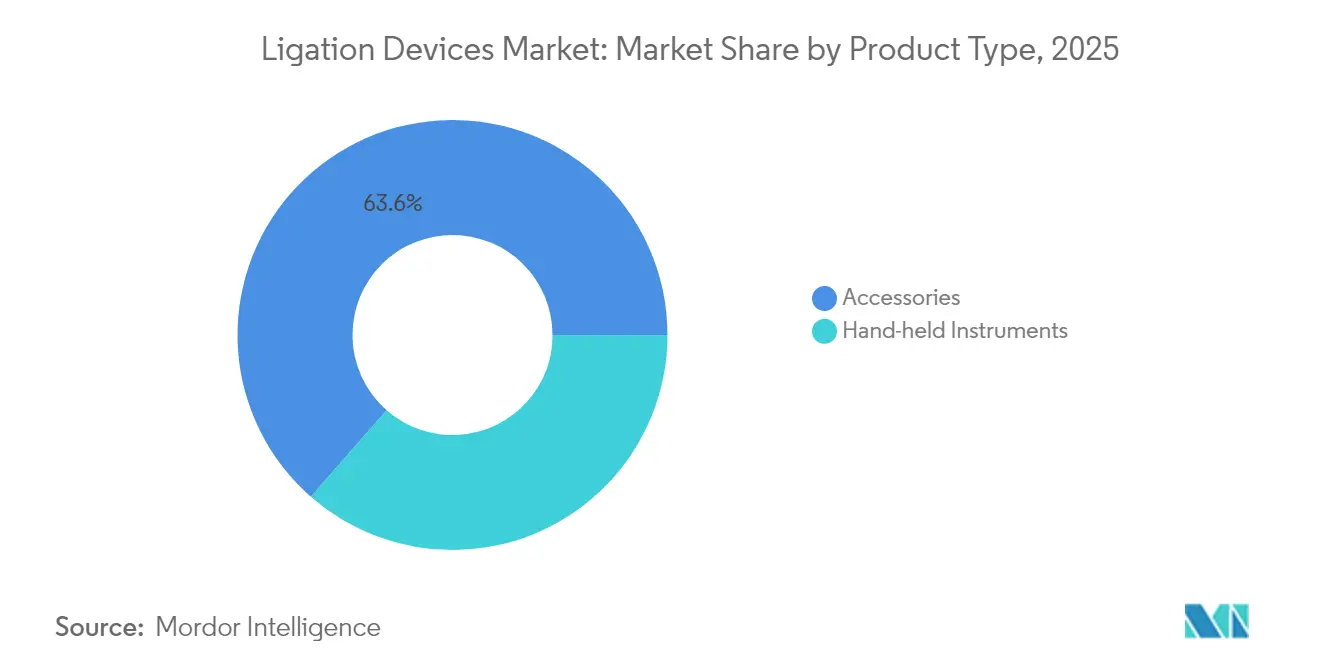

- By product type, accessories controlled 63.55% of the ligation devices market share in 2025; hand-held instruments are expanding at a 8.79% CAGR through 2031.

- By procedure, minimally invasive procedures represented 71.20% of the ligation devices market in 2025, while robotic-assisted surgery is poised for a 12.05% CAGR to 2031.

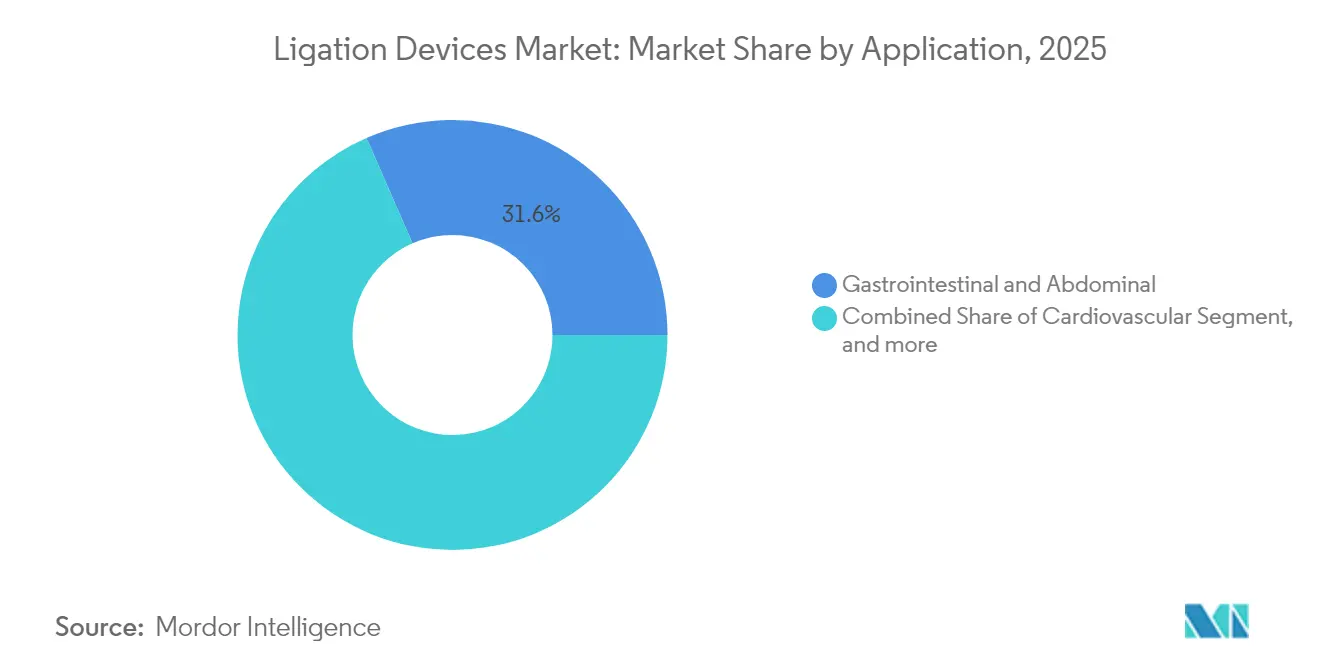

- By application, gastrointestinal and abdominal surgery held 31.55% of the ligation devices market share in 2025; bariatric and metabolic procedures are projected to advance at a 13.1% CAGR to 2031.

- By end user, hospitals accounted for 58.95% of the ligation devices market in 2025; ambulatory surgical centers are climbing at an 11.25% CAGR to 2031.

- By geography, North America captured 41.35% of the ligation devices market size in 2025, whereas Asia-Pacific is forecast to grow at an 8.43% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Ligation Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of CV & urologic diseases | +1.8% | North America, Europe | Long term (≥ 4 years) |

| Growth in minimally invasive procedures | +2.1% | North America, Asia-Pacific | Medium term (2-4 years) |

| Surge in bariatric & aesthetic surgeries | +1.3% | North America, Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Rapid tech advances in vessel-sealing energy devices | +1.5% | Developed markets worldwide | Short term (≤ 2 years) |

| Magnet-assisted anastomosis adoption | +0.7% | North America, Europe | Long term (≥ 4 years) |

| Shift to absorbable polymer clips | +0.9% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of CV & Urologic Diseases

Cardiologists and urologists are increasingly turning to advanced vessel-sealing platforms that can secure arteries up to 7 mm while lowering intra-operative blood loss compared with sutures.[1]X. Author, “Comparative Vessel Sealing Burst Pressures,” ScienceDirect, Sciencedirect.com Urology has moved beyond excisional methods; systems such as UroLift use mechanical tissue lifting to relieve benign prostatic hyperplasia, sustaining sexual function and driving surgeon preference.[2]Teleflex Incorporated, “UroLift System Clinical Outcomes,” Teleflex.com An aging global population intensifies procedure volume, and value-based payment programs reward technology that trims transfusion rates and shortens ICU stays. These factors lock in long-term demand for premium sealing solutions able to manage fragile, calcified or inflamed vessels with minimal thermal spread.

Growth in Minimally Invasive Procedures

Ambulatory centers are posting 5.7% annual growth in case counts, benefiting from 25-50% cost savings over hospital outpatient units.[3]Medicare Payment Advisory Commission, “Report to the Congress: Medicare Payment Policy,” Medpac.gov. Concurrently, robotic platforms add precise vessel-sealing hardware; FDA clearance for Intuitive’s curved sealer now allows confined-space work on da Vinci systems. Smaller incisions speed discharge and promote quicker return to work, encouraging payers to endorse laparoscopic and robotic approaches. Surgeons, in turn, demand sealing instruments that fit through 5-mm ports yet maintain burst pressures above 360 mmHg. These dynamics place the ligation devices market at the center of the minimally invasive ecosystem.

Surge in Bariatric & Aesthetic Surgeries

More than 25 million adults qualified for metabolic procedures in 2025 under expanded BMI criteria, fueling unprecedented orders for high-performance energy devices capable of controlling thick gastric tissue. Magnetic compression tools such as MagDI create side-to-side duodeno-ileal anastomoses without staples, achieving cleaner luminal patency and fewer leaks. Parallel growth in body-contouring lifts cosmetic demand for fine-tip vessel sealers that minimize scarring. Reduced travel restrictions have revived medical tourism, particularly in Mexico and Turkey, prompting clinics to stock versatile, single-use clip assortments that support both weight-loss and aesthetic cases within one schedule block.

Rapid Tech Advances in Vessel-Sealing Energy Devices

Intelligent generators now adjust wattage in milliseconds by reading tissue impedance, raising burst pressure while cutting collateral thermal injury by up to 43%. Ferromagnetic heating achieves ≥710 mmHg seals at one-third the power of ultrasonic devices, lowering smoke and preserving surrounding collagen. Early microwave prototypes complete seals in 3 seconds at 30 watts, promising time savings in lengthy colorectal resections. Machine-learning overlays standardize energy curves, flattening the training curve between novice and expert surgeons. These breakthroughs accelerate replacement cycles, a significant upside for the ligation devices market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of advanced ligation systems | -1.2% | Emerging markets | Medium term (2-4 years) |

| Regulatory / reimbursement hurdles | -0.8% | Global | Long term (≥ 4 years) |

| Emergence of suture-less bio-adhesive sealants | -0.6% | North America, Europe | Medium term (2-4 years) |

| Sustainability push vs single-use clips | -0.4% | Europe, North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost of Advanced Ligation Systems

Capital-intensive generators and disposable handpieces often exceed equipment budgets in smaller hospitals, prompting value committees to demand rigorous cost-effectiveness data before granting conversion. Bundled-payment contracts further squeeze margins, discouraging purchase of technology that lacks demonstrable return within the episode-of-care window. In lower-income economies, public tenders rate price over performance, delaying penetration of AI-directed sealing units and dampening near-term revenue for the ligation devices market.

Regulatory / Reimbursement Hurdles

Re-engineered FDA Quality System Regulation requirements enacted in 2024 increase documentation and post-market surveillance burdens, adding six to nine months to average submission timelines. Novel magnetic tools often debut without established CPT codes, forcing hospitals to absorb costs until payer schedules catch up. In the European Union, divergent interpretations of the Medical Device Regulation among Notified Bodies prolong CE marking, complicating synchronized global launches. These complexities elevate go-to-market costs and can delay revenue realization for new entrants.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Accessories Drive Volume While Innovation Fuels Hand-Held Growth

Accessories generated 63.55% of the ligation devices market size in 2025 as single-use clips, bands and cartridges drove repeat purchasing. Infection-control policies and elimination of reprocessing overhead keep this category essential to hospital supply chains. Hand-held instruments, however, are on track for a 8.79% CAGR through 2031, underpinned by smarter energy delivery and lighter ergonomics that reduce surgeon fatigue.

Second-generation clip appliers fashioned from magnesium alloys appear artifact-free on MRI and fully absorb within 12 months while maintaining tensile strength. Band ligators now incorporate torque-limiting triggers for consistent ring placement in endoscopic variceal ligation. Meanwhile, AI-ready generators sense tissue type in real time and calibrate voltage ranges, an advance that keeps hand-held sales brisk in the ligation devices market.

By Procedure: Robotic-Assisted Surgery Transforms Minimally Invasive Landscape

Minimally invasive surgery accounted for 71.20% of the ligation devices market in 2025. Surgeons favor small-port approaches that shorten recovery times and permit same-day discharge. Robotic cases are set for a 12.05% CAGR as da Vinci 5 adds haptic feedback and new curved sealers capable of sub-millimeter thermal margins.

Laparoscopic teams continue to upgrade visualization platforms, with infrared overlays unveiling otherwise hidden vasculature for safer sealing. Endoscopic use of magnetic compression devices accelerates pouch-to-limb anastomosis without staples, opening new frontiers in scarless revision bariatrics. Open surgery remains vital for trauma and oncology, sustaining baseline demand for high-throughput clip cartridges within the ligation devices market.

By Application: Bariatric Surge Reshapes Gastrointestinal Dominance

Gastrointestinal and abdominal surgery retained 31.55% of the ligation devices market share in 2025 thanks to voluminous colorectal and hepatobiliary procedures that rely on rapid, smoke-free sealing. Bariatric operations will post a 13.1% CAGR as broader BMI indications and self-pay patients in Asia accelerate sleeve gastrectomy volumes.

Cardiac teams adopt longer-jaw sealers for arterial graft harvest that preserve endothelial integrity, improving bypass patency. Gynecology units report shorter hysterectomy times when bipolar sealers replace suture ties, lowering postoperative anemia. Urology sees sustained adoption of clip-less lifts for benign prostatic hyperplasia, while thoracic surgeons test microwave sealing on segmental pulmonary arteries. Each advance feeds recurring orders in the ligation devices market.

By End User: ASC Growth Challenges Hospital Dominance

Hospitals held 58.95% of the ligation devices market in 2025, leveraging bulk purchasing and case complexity to justify generator investments. They also host robotics fleets that depend on proprietary sealing handpieces, reinforcing demand.

Ambulatory surgical centers are scaling at an 11.25% CAGR, benefiting from Medicare’s expanding outpatient code list and consumer preference for convenient, lower-cost care. Specialty clinics target niche volumes urology or ENT, for example pushing suppliers to create procedure-specific clip packs. Academic institutions pilot biodegradable clip trials, paving the way for future commercial rollouts while anchoring early volume for the ligation devices market.

Geography Analysis

North America commanded 41.35% of the ligation devices market size in 2025 on the strength of high disposable-income patients and robust reimbursement. Large GPO contracts favor bundled clip-and-generator deals, further entrenching incumbent brands.

Asia-Pacific posts the fastest 8.43% CAGR to 2031 as China streamlines hospital licensing and India expands insurance coverage. Domestic manufacturers such as EziSurg introduce competitively priced sealers tailored to local budgets. Japan’s super-aged society underpins steady robotic-assisted adoption, while South-Korean tender reforms open private-sector routes for premium generators.

Europe maintains disciplined technology rotation, with clinicians prioritizing CE-marked sealers that carry peer-reviewed data on thermal spread. Sustainability directives push hospitals toward absorbable polymer clips. Latin America and the Middle East & Africa remain price-sensitive yet invest in high-volume bariatric centers, slowly broadening the addressable ligation devices market.

Regulatory Landscape

In the United States, ligation devices marketed as surgical instruments and accessories operate under FDA medical device controls, with quality and post-market expectations shaped by the Quality Management System Regulation (QMSR). The QMSR became effective on February 2, 2026 and incorporates ISO 13485:2016 by reference. This shifts manufacturers from legacy 21 CFR Part 820 requirements toward a more globally harmonized QMS framework, while FDA oversight continues for design controls, CAPA, and complaint handling.

In Europe, ligation devices fall under the Medical Device Regulation (EU) 2017/745, where clinical evidence requirements and Notified Body capacity affect time-to-market. The European Commission adopted delegated regulations on March 20, 2026 expanding the MDR Well-Established Technologies (WET) list, which can reduce mandatory clinical investigation requirements for specific technologies when robust clinical evaluation and post-market data support safety and performance. Separately, MDR transition provisions for certain legacy devices extend to December 31, 2027 or December 31, 2028 for manufacturers that met required application and agreement milestones by May 26, 2024 and September 26, 2024, respectively.

Competitive Landscape

Moderate fragmentation characterizes the ligation devices industry as the top five suppliers control significant global revenue. Ethicon leverages its Harmonic and Enseal lines for dominance in high-volume hospitals, whereas Medtronic pairs LigaSure handpieces with its Hugo robotic platform to capture integrated-suite bids. Teleflex focuses on urologic lifts, differentiating through specialty clinically backed outcome data.

Emerging entrants pursue white-space opportunities: magnetic anastomosis systems from startups such as Mateon promise staple-free intestinal joins, and polymer-based clip developers target MRI compatibility. Patent filings for magnetic compression climbed 38% year-on-year following FDA product code addition. Sustainability has become a marketable feature; companies pilot bio-resorbable implants that dissolve after six months, eliminating follow-up removal.

Strategic alliances now hinge on AI integration. Generator makers partner with vision-system vendors to embed tissue analytics, creating closed-loop energy delivery ecosystems. Mid-size firms seek acquisition exits to scale distribution, maintaining churn yet ensuring continual technological refresh within the ligation devices market.

Ligation Devices Industry Leaders

Johnson & Johnson

Olympus Corporation

Medtronic

Teleflex Inc.

B. Braun Melsungen AG

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Robot-compatible vessel sealing stands out as a procurement whitespace where buyers prioritize integrated suites rather than standalone hand instruments. Medtronic secured CE Mark positioning for LigaSure technology on the Hugo robotic-assisted surgery system and continued to build clinical and user adoption through surgeon-facing programs, including a symposium highlighting clinical integration at the Society of Robotic Surgery Annual Meeting in Strasbourg in July 2026. As a result, demand is more concentrated around proprietary energy instruments, compatible generators, and procedure-specific accessory packs that fit robotic workflows across general surgery and gynecology.

Opportunities also extend into adjacent fixation and anastomosis workflows, where ligation-like fastening, clip alternatives, and intracorporeal techniques reduce steps in minimally invasive procedures. The FDA 510(k) pathway continues to be used for Class II devices in this space, as shown by Riverpoint Medicals May 2026 510(k) clearance for LigaMend, supporting new entrants and portfolio extensions that emphasize ease-of-use alongside standardized performance. Parallel R and D activity in colorectal intracorporeal anastomosis is visible as NICE Surgical Solutions received a US patent in July 2026 for a purse-string stapler concept and announced plans for human clinical studies in Q4 2026, which reinforces development momentum around fully intracorporeal procedures and can expand demand for complementary ligation and sealing tools.

Recent Industry Developments

- June 2026: Medtronic submitted a 510(k) filing to the US FDA to expand the Hugo robotic-assisted surgery system into general and gynecologic specialties, including the LigaSure RAS Maryland instrument. The submission supports a broader installed-base pathway for robot-compatible vessel sealing, where energy instruments and related accessories are tied to platform adoption. It also increases competitive pressure on integrated energy ecosystems in minimally invasive surgery.

- December 2025: Olympus initiated a voluntary medical device corrective action for its Single-Use Ligating Device (PolyLoop) due to potential failure to release or detach. The action highlights the importance of reliability, release mechanisms, and post-market surveillance for single-use ligation accessories used in high-throughput settings. It can also affect hospital value analysis and supplier qualification for disposable ligating devices.

- October 2024: Johnson and Johnson MedTech launched the ECHELON ENDOPATH Staple Line Reinforcement device for use with ECHELON FLEX Powered Staplers in bariatric, thoracic, and general surgery. The launch strengthens stapling ecosystems aimed at reducing bleeding and leak-related complications in staple lines, where adjunct reinforcement competes with or complements vessel sealing and ligation approaches. It also expands bundled selling opportunities around procedure-specific consumables in high-volume service lines such as bariatrics.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenue earned from ligation devices used during surgical procedures to close, clip, or tie off vessels and tissue bundles to control bleeding and secure ducts. The sizing is value based in USD and reflects sales into routine clinical use across major care settings.

Scope exclusions: We exclude sutures and general wound closure products that are not intended for vessel or tissue ligation, and we also exclude procedure service revenue.

Segmentation Overview

- By Product Type

- Hand-held Instruments

- Ligating clip appliers

- Endoscopic band ligators

- Vessel-sealing generators

- Accessories

- Hand-held Instruments

- By Procedure

- Minimally Invasive Surgery

- Laparoscopic

- Endoscopic

- Robotic-assisted

- Open Surgery

- Minimally Invasive Surgery

- By Application

- Gastrointestinal & Abdominal

- Cardiovascular

- Gynecology

- Urology

- Bariatric / Metabolic

- Others

- By End User

- Hospitals

- Ambulatory Surgical Centres

- Specialty Clinics

- Academic & Research Institutes

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with building the demand context for ligation procedures and the supply context for device availability and pricing. We used public sources such as the US CDC, the WHO, the OECD health statistics, and national health ministries for surgery volumes and care access signals, then relied on trade publications and peer reviewed clinical journals to understand how ligation methods are used in practice.

To ground the commercial side, we reviewed company annual reports, investor presentations, press releases, and product documentation to map device categories and typical use settings. Where available, we checked patent databases for technology direction, and used an import export shipment level database selectively to sanity check cross border movement patterns for relevant device categories. These examples are not exhaustive, and we referenced additional public sources for data collection, validation, and clarification during the research.

Primary Interviews and Surveys

Primary work focused on validating adoption and pricing assumptions across hospitals and ambulatory surgical centers, then stress testing the split between open and minimally invasive procedures. We spoke with clinicians, procurement teams, distributors, and product managers across APAC, EMEA, and the Americas to confirm utilization per procedure, typical replacement and accessory attachment rates, and near term demand shifts.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 13% | APAC: 41% |

| Mid tier: 53% | Functional/Unit leaders: 31% | EMEA: 34% |

| Smaller Players: 16% | Managers: 56% | Americas: 25% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where procedure volumes and care setting mix are reconstructed by region, then converted into a ligation device demand pool using penetration and usage per procedure assumptions. Because not every surgery uses the same ligation method, the model separates minimally invasive and open procedure pathways. It also applies different attachment rates for accessories where they are typically used.

Key inputs include surgical procedure volumes by specialty, the share of minimally invasive procedures, average devices used per case (including replacement frequency for clip systems), average selling price ranges by device type, and the hospital versus ambulatory surgical center purchase mix. When the data series is incomplete in a country, regional proxies are used and then corrected using interview feedback and trade flow signals.

Forecasts are produced using scenario analysis supported by near term indicators such as elective surgery recovery, operating room throughput, and expected shifts toward minimally invasive techniques. These scenarios are cross checked with pricing direction and procurement behavior. Results are corroborated with selective bottom-up approximations such as sampled ASP times implied volumes and channel checks, which helps adjust totals when the top-down build shows unusual jumps.

Data Validation & Update Cycle

Outputs are validated through multiple checks that look for mismatches between procedure growth, device spend intensity, and regional care delivery patterns. When a region shows an unexpected change, we review the underlying assumptions, re-contact relevant respondents, and rerun the model before internal sign-off.

Before publication, a separate analyst review confirms that the market definition, conversions, and year-over-year movements are consistent and explainable. The report is refreshed annually, and interim updates are triggered when material events occur, such as major regulatory changes, large price moves, or notable shifts in elective surgery volumes. Right before delivery, a final pass is done so clients receive the most current view available.

Mordor Intelligence's Ligation Devices Market Sizing Compared With Other Published Estimates

Published market sizes for ligation devices can vary even when the topic sounds identical, because each publisher draws the line differently on what products count and how procedure demand is translated into device revenue. Differences also show up from the year chosen as the base, currency conversion timing, and whether pricing is assumed to move with inflation or remain flat.

The main gap comes from whether energy-based vessel sealing systems are counted inside ligation. Mordor Intelligence treats them as out of scope unless they are sold and used as dedicated ligation devices rather than broader electrosurgical platforms. Another common driver is utilization logic, where some estimates apply a uniform devices per procedure factor across specialties. Our approach varies it by procedure type and care setting, based on interview-backed usage patterns.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.52 B (2025) | |

| Global Consultancy A | USD 1.84 B (2025) | Uses a broader product boundary that can bundle energy-based vessel sealing within ligation, and may apply higher average selling prices without separating hospital versus ambulatory purchasing mix. |

| Industry Publisher B | USD 1.43 B (2025) | Leans on a narrower revenue capture approach that can undercount accessory pull-through and replacement demand, and it may use conservative utilization per procedure assumptions across specialties. |

The spread in estimates is mostly explained by product scope choices and by how procedure demand is converted into device volumes and pricing. By keeping the scope tied to dedicated ligation devices and by checking assumptions against care setting mix and adoption signals, the final number stays traceable to clear inputs and repeatable steps.

Key Questions Answered in the Report

What is the current Ligation Devices Market size?

The Ligation Devices Market size is USD 1.63 billion in 2026 and is projected to register a CAGR of 7.18% during the forecast period (2026-2031)

Who are the key players in Ligation Devices Market?

Johnson & Johnson, Medtronic plc, Teleflex Incorporated, Olympus Corporation and Applied Medical are the major companies operating in the Ligation Devices Market.

Which is the fastest growing region in Ligation Devices Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

Which region has the biggest share in Ligation Devices Market?

In 2025, the North America accounts for the largest market share in Ligation Devices Market.

What years does this Ligation Devices Market cover?

The report covers the Ligation Devices Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Ligation Devices Market size for years: 2026, 2027, 2028, 2029, 2030 and 2031.

Page last updated on: