Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 15.28 Billion |

| Market Size (2026) | USD 17.62 Billion |

| Market Size (2031) | USD 22.91 Billion |

| Growth Rate (2026 - 2031) | 5.39% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

South Korea Luxury Goods Market Analysis by Mordor Intelligence

The South Korea luxury goods market size was valued at USD 15.28 billion in 2025 and is estimated to grow from USD 17.62 billion in 2026 to reach USD 22.91 billion by 2031, at a CAGR of 5.39% during the forecast period (2026-2031). Climbing income levels, a weak won that redirects outbound shoppers to domestic boutiques, and K-pop–powered celebrity campaigns are sustaining premium demand even as overall fashion growth moderates. Watches are emerging as the fastest-growing category, hard luxury counters in the three leading department-store chains posted 35–43% year-over-year sales gains in 1Q 2025, and limited-edition drops from European maisons continue to sell out within hours, reinforcing scarcity-based pricing. Online marketplaces are expanding briskly, yet the abrupt 2024 collapse of Balaan shows that scale and curated authenticity matter more than raw traffic in this channel. Meanwhile, counterfeit seizures reached 117,000 items in 2025, prompting tougher Trademark Act enforcement that raises compliance costs but also nudges consumers toward authorized stores.

Key Report Takeaways

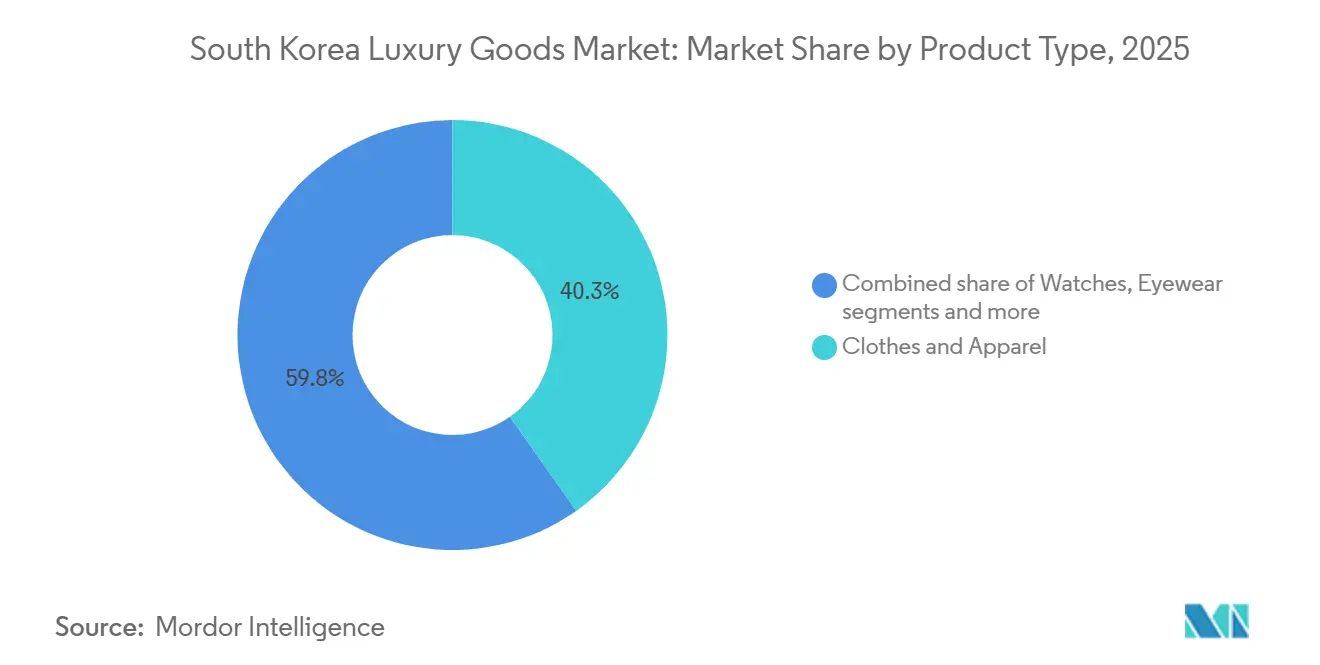

- By product type, clothing and apparel led with 40.25% revenue share of the South Korea luxury goods market in 2025; watches are forecast to expand at a 6.45% CAGR through 2031.

- By end user, women held 61.28% of the South Korean luxury goods market share in 2025, while the men’s segment records the fastest projected 6.16% CAGR to 2031.

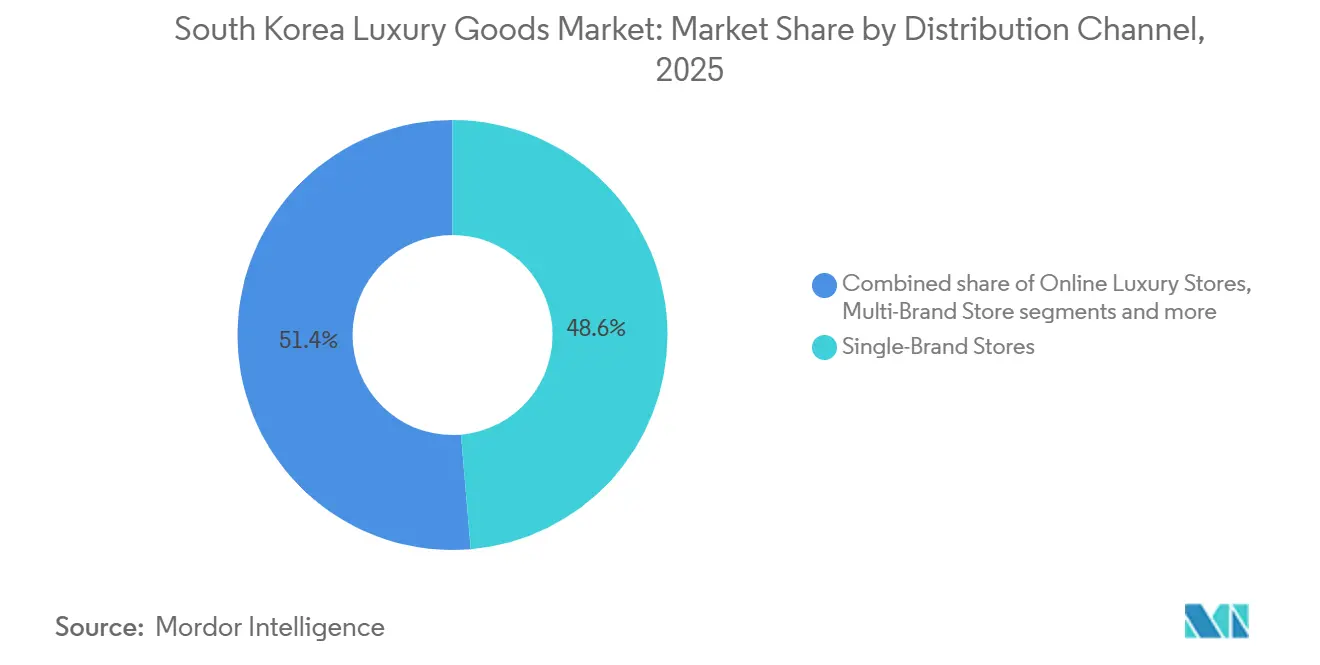

- By distribution channel, single-brand stores accounted for 48.64% of the South Korean luxury goods market size in 2025, and online luxury stores are advancing at an 7.69% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South Korea Luxury Goods Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift Toward Sustainable and Eco-Certified Luxury Goods | +0.6% | National, with early adoption in Seoul and Busan | Medium term (2-4 years) |

| Impact of Social Media and Celebrity Endorsements | +1.2% | National, amplified by K-pop global reach | Short term (≤ 2 years) |

| Growth in Disposable Incomes and Wealth Accumulation | +0.9% | National, concentrated in metropolitan areas | Long term (≥ 4 years) |

| Innovations in Raw Materials and Product Design | +0.5% | National, with Seoul as design hub | Medium term (2-4 years) |

| Preference for Limited-Edition Offerings | +0.8% | National, strongest in Seoul Cheongdam and Gangnam districts | Short term (≤ 2 years) |

| Surge in Demand for K-Luxury Designer Brands | +1.0% | National, with export spillover to Japan and China | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shift Toward Sustainable and Eco-Certified Luxury Goods

Korean consumers are demanding verifiable sustainability credentials, pushing brands to adopt refillable packaging, traceable supply chains, and third-party certifications. Louis Vuitton's La Beaute beauty line, launched in Korea with refillable containers, signals a pivot from symbolic green messaging to operational redesign. The Ministry of Trade, Industry, and Energy allocated approximately USD 27 million in 2025 to raise digital transformation in the textile value chain from 35% to 60% and increase the global share of Korean fashion from 2-3% to 10% by 2030, embedding sustainability metrics into export competitiveness[1]Source: Ministry of Trade, Industry and Energy, “Textile Digital Transformation Plan 2025,” motie.go.kr. Younger cohorts, who represent 55% of luxury buyers in a Spanish Gen Z study and 67% of whom would purchase to support an idol's endorsed sustainable product, are treating eco-certifications as non-negotiable table stakes rather than premium differentiators. This shift is compressing margins for brands that rely on opaque sourcing, while rewarding those that publish annual impact reports aligned with ISO 14001 environmental management standards.

Impact of Social Media and Celebrity Endorsements

K-pop idols have become a key driver of customer acquisition for Korean luxury brands, with their influence leading to significant revenue growth that justifies high endorsement fees. For example, BTS collaborations boosted McDonald's Korea sales by 250%. Similarly, Bodyfriend achieved record sales volumes for their recliners through such partnerships. In 2025, Felix Lee's role as a Louis Vuitton muse coincided with a 5.8% rise in sales, reaching 1.78 trillion won (approximately USD 1.26 billion) for Louis Vuitton Korea in 2024. Bulgari took a strategic approach by launching its Seoul creator platform featuring K-pop stars like Lisa and Mingyu. This initiative integrates idols into product narratives rather than relying on short-term campaigns, reflecting the belief that fans' emotional connections (parasocial relationships) can drive sustained purchasing behavior. In 2025, influencer marketing spending in Korea reached USD 489 million. A survey, with 93.4% social-media penetration, showed that 71% of consumers were directly influenced by social media in their luxury purchase decisions. However, the Cha Eun-woo controversy highlights the risks of celebrity endorsements, as a single misstep can harm brand reputation. This underscores the importance of brands maintaining strong crisis-management strategies and diversifying their ambassador portfolios.

Growth in Disposable Incomes and Wealth Accumulation

From 2012 to 2025, Korea's household disposable income surged from 750.2 trillion won to a projected 1,293.4 trillion won. However, real purchasing power grapples with inflation and high household debt, as noted by the OECD Economic Outlook[2]Source: OECD, "OECD Economic Outlook - Korea Household Income." oecd.org. The Bank of Korea forecasts GDP growth rates of 1.0% for 2025 and 1.8% for 2026, trailing the 2.2% growth seen in 2024. Meanwhile, consumer price inflation is anticipated to stabilize at 2.1% for both 2025 and 2026. Wealth is increasingly concentrated among high-net-worth individuals and chaebol families. These affluent groups are pivoting from traditional logo-centric consumption to personalized experiences and ultra-premium items, including high-end jewelry and exclusive watches. Cartier Korea achieved a historic milestone, recording sales of approximately USD 1.1 billion for the fiscal year ending March 2024. This surge, attributed to wedding-related gifts, coincided with an 8.4% uptick in marriages in July 2025, marking 16 months of consistent growth. This trend has birthed a "barbell market": while ultra-luxury brands like Hermès enjoyed a 20.9% sales boost, reaching 964.2 billion won in 2024, mid-tier brands such as Fendi and Ferragamo faced declines of 20% and 12.7%, respectively.

Surge in Demand for K-Luxury Designer Brands

Korean luxury brands are seamlessly merging traditional craftsmanship with modern design, bolstered by government-backed export initiatives and a robust digital framework. In a significant move, Gentle Monster, an eyewear brand hailing from Seoul, clinched a USD 100 million investment from tech giant Google in early 2025. This funding, aimed at developing Android XR smart glasses, not only valued Gentle Monster's parent company, IICombined, at an impressive USD 560 million but also underscored the potential of technology integration in propelling fashion brands into influential platform players. Both We11Done and HYEIN SEO, emerging players in the competitive landscape, are tapping into Musinsa's vast ecosystem to connect with younger audiences who favor distinctive silhouettes over traditional logos. The Ministry of Trade, Industry, and Energy is backing these ambitions with a substantial investment of around USD 27 million in 2025. Their goal is to elevate the global share of Korean fashion from its current 2-3% to a target of 10% by 2030, emphasizing digital transformation and sustainability as key metrics for export competitiveness. With this strategic policy support and the global allure of K-pop, Korean luxury brands are poised to carve out a niche in markets where European counterparts are often viewed as overpriced or culturally aloof.

Restraint Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Spread of Counterfeit Products | -0.7% | National, with seizures concentrated at Incheon and Myeongdong | Short term (≤ 2 years) |

| Declining Demand from Price-Sensitive Buyers | -0.9% | National, affecting mid-tier luxury segments | Medium term (2-4 years) |

| Rigorous Regulations and Rising Compliance Costs | -0.4% | National, with customs and e-commerce focus | Long term (≥ 4 years) |

| Economic Volatility and Inflation's Effect on Spending | -1.1% | National, exacerbated by weak won and global uncertainty | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Spread of Counterfeit Products

Korea Customs seized 117,000 counterfeit Korean-brand items in 2025, 97.7% of which originated from China, while total counterfeit seizures across all brands reached 102,219 cases in 2024, a 19.9% year-over-year increase, according to the Korea Customs Service[3]Source: Korea Customs Service, “Trademark Act Enforcement Update,” customs.go.kr. Over the five years from 2019 to 2023, authorities confiscated counterfeits worth 2.09 trillion won (USD 1.48 billion), with Louis Vuitton accounting for 246.4 billion won, Rolex 213.7 billion won, and Chanel 113.5 billion won. A February 2025 operation in Myeongdong seized 3,544 items valued at 20 billion won, and Incheon Customs confiscated 49,487 items between April and June 2024 Korea Customs Service. The Trademark Act amendment, effective May 27, 2025, tightens enforcement on overseas direct purchases and expands liability for e-commerce platforms, yet the OECD estimates global counterfeit trade at USD 467 billion—2.3% of global imports—suggesting that supply-side enforcement alone cannot eliminate the problem

Economic Volatility and Inflation's Effect on Spending

The Bank of Korea's projection of 1.0% GDP growth in 2025 and 1.8% in 2026, combined with 2.1% inflation in both years, compresses real disposable income and forces consumers to trade down or delay purchases. The won weakened past 1,480 per U.S. dollar in late 2025, raising import costs for European luxury goods and redirecting cross-border shoppers back to domestic boutiques, which paradoxically benefited single-brand stores but eroded duty-free operators' margins. All four major duty-free operators, Lotte, Shilla, Shinsegae, and Hyundai, posted losses in 2024 despite foreign-visitor arrivals rising 59.4% to 8.57 million, as spending increased only 0.8% to 10.10 trillion won. Gold prices surged roughly 80% year-over-year to approximately 245,000 won per gram (USD 168) by February 2026, reshaping wedding-gift customs and prompting Lotte and Shinsegae to curate ultra-premium gift sets priced above 100 million won, effectively pricing out middle-income buyers. Luxury fashion growth decelerated to 5-11% in 2024 from the 20-40% annual rates seen between 2018 and 2022, and Bain's 2025 report noted that the Rest of Asia, including Korea, declined 1% to 2% in 2024 as post-pandemic revenge spending corrected and consumer confidence remained subdued.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Watches Outpace Apparel Despite Smaller Base

In 2025, clothing and apparel led with a 40.25% market share, driven by demand for seasonal lines and celebrity-endorsed collections. Watches, growing at a 6.45% CAGR through 2031, became the fastest-expanding category. Jewelry and watch counters in department stores recorded strong year-over-year sales growth: Lotte at 35%, Shinsegae at 36%, and Hyundai at 38.4% in Q3 2025, supported by an 8.4% rise in marriages in July and 16 months of sustained growth. Cartier Korea achieved record sales of USD 1.1 billion for the fiscal year ending March 2024. Vacheron Constantin opened a flagship store in Seoul in June 2025, while Hyundai Department Store plans to launch a Chaumet boutique in Pangyo this December. Gold prices surged 80% year-over-year to 245,000 won per gram (USD 168) by February 2026, enhancing the appeal of hard luxury as both adornment and a store of value, a trend capitalized on more effectively by jewelry and watches than apparel.

Leather goods, jewelry, and eyewear are experiencing moderate growth. Leather goods benefited from brand-specific gains: Hermès Korea's sales rose 20.9% to 964.2 billion won in 2024, while Louis Vuitton Korea and Chanel Korea grew 5.8% to 1.78 trillion won, and 8.2% to 1.84 trillion won, respectively. Eyewear is evolving, with Gentle Monster securing a USD 100 million investment from Google in early 2025 to develop Android XR smart glasses, signaling a shift toward wearable technology. Footwear, the smallest segment, remains constrained by limited differentiation and price sensitivity, though Korean brands like Andersson Bell and Kusikohc are gaining traction with oversized silhouettes and gender-fluid designs. The Ministry of Trade, Industry, and Energy's 2025 investment of USD 27 million aims to increase digital transformation in the textile value chain from 35% to 60% and raise Korea's global fashion share from 2-3% to 10% by 2030, boosting footwear and apparel exports.

By End User: Men's Segment Accelerates as Gender Norms Shift

Women accounted for 61.28% of luxury end-user demand in 2025, reflecting higher per-capita spending on handbags, jewelry, and cosmetics, yet men's luxury consumption is expanding at a 6.16% CAGR through 2031, the fastest rate among end-user segments. Menswear imports reached USD 5.08 billion in 2024 out of total clothing imports of USD 12.37 billion, and exports approached USD 2 billion, including USD 1.7 billion in synthetic textiles, underscoring Korea's dual role as importer and exporter. Korean menswear brands such as Wooyoungmi, ThisIsNeverThat, 87MM, Recto, and Amomento are leveraging oversized cuts, unique patterns, bright colors, and sustainable materials to capture younger male consumers who prioritize self-expression over traditional tailoring. The government's target to raise the global share of Korean fashion from 2-3% to 10% by 2030 includes menswear as a strategic priority, supported by digital transformation initiatives and export financing.

Unisex offerings are gaining traction as brands such as Gentle Monster, Ader Error, and PushButton blur gender boundaries, appealing to Gen Z consumers who reject binary categorization. Felix Lee's appointment as Louis Vuitton muse in 2025 and Jennie's role as Gentle Monster's first ambassador illustrate how brands are using K-pop idols to normalize gender-fluid aesthetics. Women's dominance in the segment reflects entrenched spending patterns. Chanel Korea's 1.84 trillion won in 2024 sales, and Hermès Korea's 964.2 billion won were driven primarily by female buyers, but the accelerating men's CAGR suggests that the gender gap will narrow by 2031. Brands that fail to develop credible menswear and unisex lines risk ceding market share to Korean disruptors who are native to these categories.

By Distribution Channel: Online Platforms Surge Despite Balaan's Collapse

In 2025, single-brand stores accounted for 48.64% of the distribution share, driven by flagship expansions from Hermès, Louis Vuitton, Cartier, and Bulgari in Seoul's Cheongdam district, where limited real estate and high foot traffic justify premium rents. Hermès relocated and expanded its flagship in August 2025, while Vacheron Constantin opened its flagship in June 2025. Tiffany also announced plans for a Cheongdam flagship in 2027, highlighting the continued importance of physical retail for ultra-luxury brands reliant on in-person service and experiential storytelling. Multi-brand stores, primarily department stores operated by Lotte, Shinsegae, and Hyundai, saw luxury sales growth slow to 5-11% in 2024, down from the 20-40% annual growth seen between 2018 and 2022, as post-pandemic spending normalized and consumer confidence remained weak.

Online luxury platforms are growing at a 7.69% CAGR through 2031, the fastest among distribution channels, but the segment is sharply divided between leaders and laggards. Musinsa reported USD 3.3 billion in gross merchandise value and USD 910 million in revenue in 2024, a 25.1% year-over-year increase. Its global arm saw transaction volumes in Japan rise 145%, with monthly sales surpassing 10 billion won in October 2025. In contrast, Balaan, despite 3.2 million monthly active users and 6 million app downloads, filed for corporate rehabilitation in 2024 due to operating losses of 10 billion won on 2023 sales of 39.2 billion won. The company entered investment talks with Alibaba for several hundred billion won, according to its financial disclosures. Must It saw sales drop 52.2% to 11.9 billion won in 2024, while Trenbe lost market share to secondhand platform GUGUS, whose transaction volume now rivals Balaan's.

Geography Analysis

Seoul’s Cheongdam, Gangnam, and Myeongdong districts have firmly established themselves as the central hubs of South Korea's luxury goods market, hosting 70% of flagship store openings since 2024. High-profile developments, such as Hermès’ expansion in August 2025 and Tiffany’s planned boutique launch in 2027, along with the steady customer flow at Vacheron, highlight the continued dominance and prestige of physical retail spaces in the luxury segment. Additionally, Busan and the suburban area of Pangyo are gradually gaining prominence. Hyundai Department Store plans to open a Chaumet salon in Pangyo by December 2025, aiming to tap into the affluent commuter population in the area.

Duty-free zones are experiencing a decline in their traditional dominance within the luxury market. Although the number of visitors rebounded significantly in 2024, increasing by 59.4% to reach 8.57 million, overall spending rose by only 0.8%. This limited growth is attributed to reduced Chinese tourist arrivals and the appreciation of the won, which has discouraged foreign spending. In response to shifting consumer behavior, Incheon Airport has transitioned toward online pick-up counters, reflecting a broader trend of luxury shoppers moving to digital platforms such as Musinsa and other e-commerce marketplaces.

Emerging cities like Daegu and Gwangju remain underdeveloped in terms of luxury market penetration. However, the Ministry of Trade, Industry, and Energy’s (MOTIE) allocation of USD 27 million to a textile fund could foster the development of local manufacturing clusters, potentially driving the establishment of regional luxury boutiques. The ability of K-luxury brands to rapidly implement omnichannel strategies will play a pivotal role in capturing market share outside Seoul and expanding their presence in these underrepresented regions.

Competitive Landscape

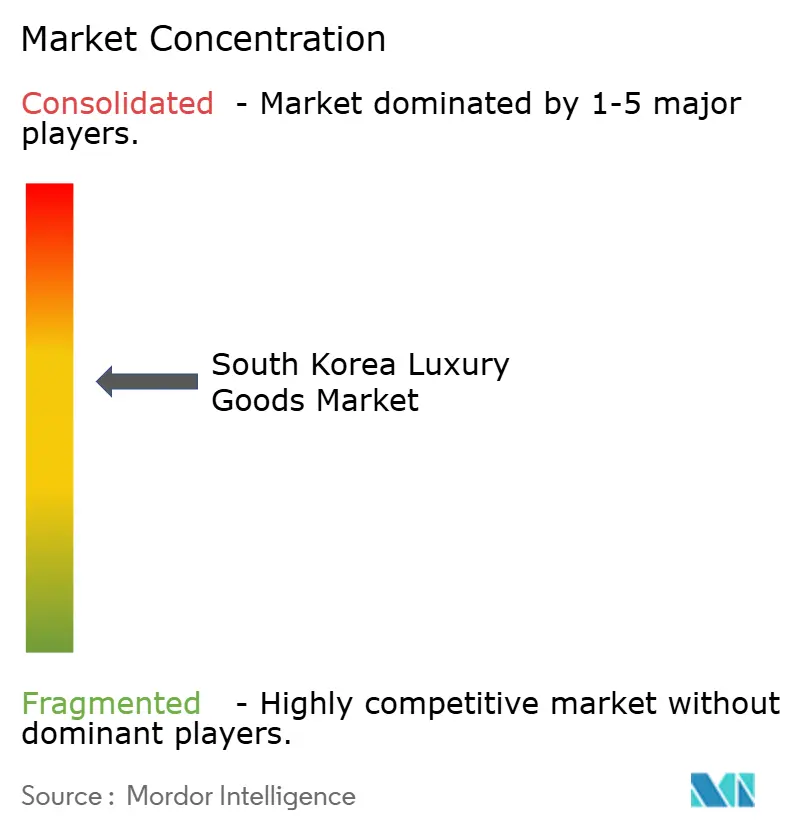

South Korea's luxury goods market is moderately concentrated, with global leaders such as LVMH, Kering, and Richemont dominating leather goods, jewelry, and watches through flagship stores in Seoul's Cheongdam district. However, Korean brands like Gentle Monster, We11Done, and HYEIN SEO are disrupting the market by innovating in eyewear, apparel, and experiential retail. These brands combine traditional craftsmanship with modern design while leveraging K-pop's global influence. The market's barbell structure, where consumers either opt for ultra-luxury or turn to Korean brands offering unique designs at accessible prices, has led to sales declines of 20% and 12.7% for mid-tier labels Fendi and Ferragamo, respectively, in 2024. Gentle Monster's USD 100 million investment from Google in early 2025 to develop Android XR smart glasses highlights the potential of integrating technology to elevate fashion brands into platform players, a strategy European incumbents have been slower to adopt.

Strategic trends reveal a split between global brands focusing on flagship expansions and limited-edition releases to sustain margins, and Korean brands leveraging digital platforms, celebrity endorsements, and omnichannel strategies to attract younger consumers. Bulgari's Seoul creator platform, launched with K-pop stars Lisa and Mingyu, integrates idols into product storytelling rather than relying on one-off campaigns, reflecting a strategic belief that parasocial relationships can drive sustained purchase intent. Musinsa, an online fashion platform, achieved USD 3.3 billion in gross merchandise value and USD 910 million in revenue in 2024, representing a 25.1% year-over-year growth. Its global division experienced a 145% surge in transaction volume in Japan, with monthly sales exceeding 10 billion won in October 2025, demonstrating the scalability of digital-first brands compared to traditional retailers.

Growth opportunities include menswear, which is forecasted to grow at a 6.16% CAGR through 2031, and the secondhand luxury market, where platform GUGUS now rivals Balaan in transaction volume. This indicates that circular-economy models can attract price-sensitive buyers without cannibalizing primary sales. The Aicel Korea Luxury Index highlights regulatory changes, including the Trademark Act amendment effective May 27, 2025, which tightens enforcement on overseas direct purchases and increases liability for e-commerce platforms. These changes create a regulatory environment favoring established players with robust compliance infrastructure over new entrants.

South Korea Luxury Goods Industry Leaders

-

Chanel SA

-

Hermès International SA

-

Rolex SA

-

The Swatch Group Ltd.

-

LVMH Moët Hennessy Louis Vuitton SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: LVMH expanded its presence in South Korea through flagship store upgrades for Louis Vuitton and Christian Dior in Seoul’s Cheongdam district. The expansion was targeted at the tourists who visited from China, Japan, and the United States.

- August 2025: Lotte Duty Free reopened a redesigned, doubled-in-size Damiani boutique at its Myeongdong flagship in Seoul. The store features the brand's collections like Belle Époque and Mimosa. The expansions align with Lotte's strategy to enhance premium offerings and shopping experiences.

- May 2025: Swiss luxury watchmaker H. Moser & Cie. opened its fifth global standalone boutique at Galleria Department Store in Seoul's Gangnam. The store offers a wide range of watches for men and women in different designs and styles.

South Korea Luxury Goods Market Report Scope

As per the study scope, luxury goods refer to high-end or premium products like luxury watches, luxury footwear, luxury clothing, apparel , and other such products that are of superior quality and are priced higher than other goods available in the market. South Korea luxury goods market is segmented by type and distribution channel. By type, the market is segmented into clothing and apparel, footwear, bags, jewelry, watches, and other accessories. In terms of distribution channels, the market is segmented into single-brand stores, multi-brand stores, online stores, and other distribution channels. The report offers market size and forecasts for the luxury goods market in value (USD million) for all the above segments.

By Product Type

| Clothing and Apparel |

| Footwear |

| Leather Goods |

| Watches |

| Jewellery |

| Eyewear |

| Other Product Types |

By End User

| Men |

| Women |

| Unisex |

By Distribution Channel

| Single-Brand Stores |

| Multi-Brand Stores |

| Online Luxury Stores |

| Other Distribution Channels |

| By Product Type | Clothing and Apparel |

| Footwear | |

| Leather Goods | |

| Watches | |

| Jewellery | |

| Eyewear | |

| Other Product Types | |

| By End User | Men |

| Women | |

| Unisex | |

| By Distribution Channel | Single-Brand Stores |

| Multi-Brand Stores | |

| Online Luxury Stores | |

| Other Distribution Channels |

Key Questions Answered in the Report

What is the projected value of the South Korea luxury goods market in 2031?

The market is forecast to reach USD 22.91 billion by 2031, growing at a 5.39% CAGR from 2026 to 2031.

Which product category is growing fastest in South Korean luxury retail?

Watches are expanding at a 6.45% CAGR through 2031, outpacing apparel and leather goods.

How important are online channels for premium brands in Korea?

Online luxury stores are recording a 7.69% CAGR and are expected to handle USD 6 billion in sales by 2031, led by platforms like Musinsa.

Why are Korean designer brands gaining traction globally?

Government export incentives, K-pop endorsements, and digital-first retail models enable labels such as Gentle Monster and We11Done to compete with European houses.

Page last updated on: