China Logic Integrated Circuits Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

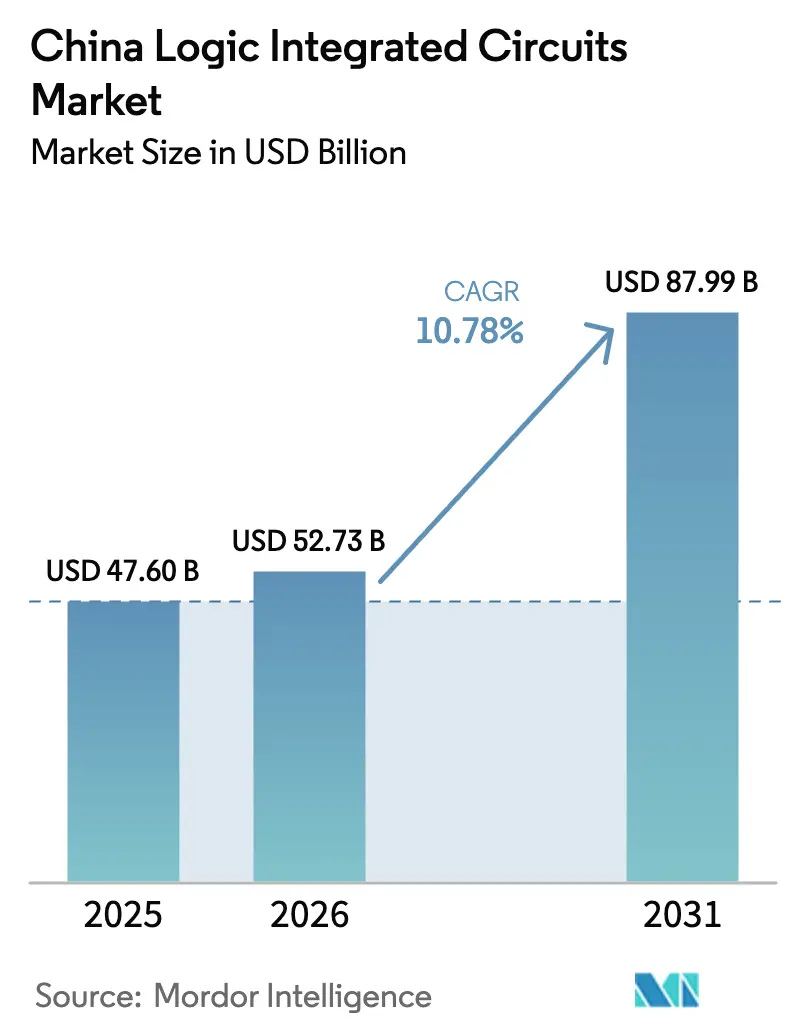

| Base Year Market Size (2025) | USD 47.60 Billion |

| Market Size (2026) | USD 52.73 Billion |

| Market Size (2031) | USD 87.99 Billion |

| Growth Rate (2026 - 2031) | 10.78% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

China Logic Integrated Circuits Market Analysis by Mordor Intelligence

The China logic integrated circuits market size is expected to grow from USD 47.60 billion in 2025 to USD 52.73 billion in 2026 and is forecast to reach USD 87.99 billion by 2031 at 10.78% CAGR over 2026-2031. Sustained state-backed funding, large‐scale provincial fabrication projects, and a rising domestic content requirement are propelling revenue expansion even as advanced tool restrictions persist. Intensifying 5G handset output in Guangdong, surging electric-vehicle penetration, and hyperscale data-centre construction are broadening demand pools. Mature-node capacity additions secure near-term supply, while breakthroughs in 5 nm production without EUV signal an upward technology trajectory. Competitive tensions remain high because capital requirements for sub-10 nm design exceed USD 449 million per tape-out, and a 200,000-person skills gap fuels wage inflation.

Key Report Takeaways

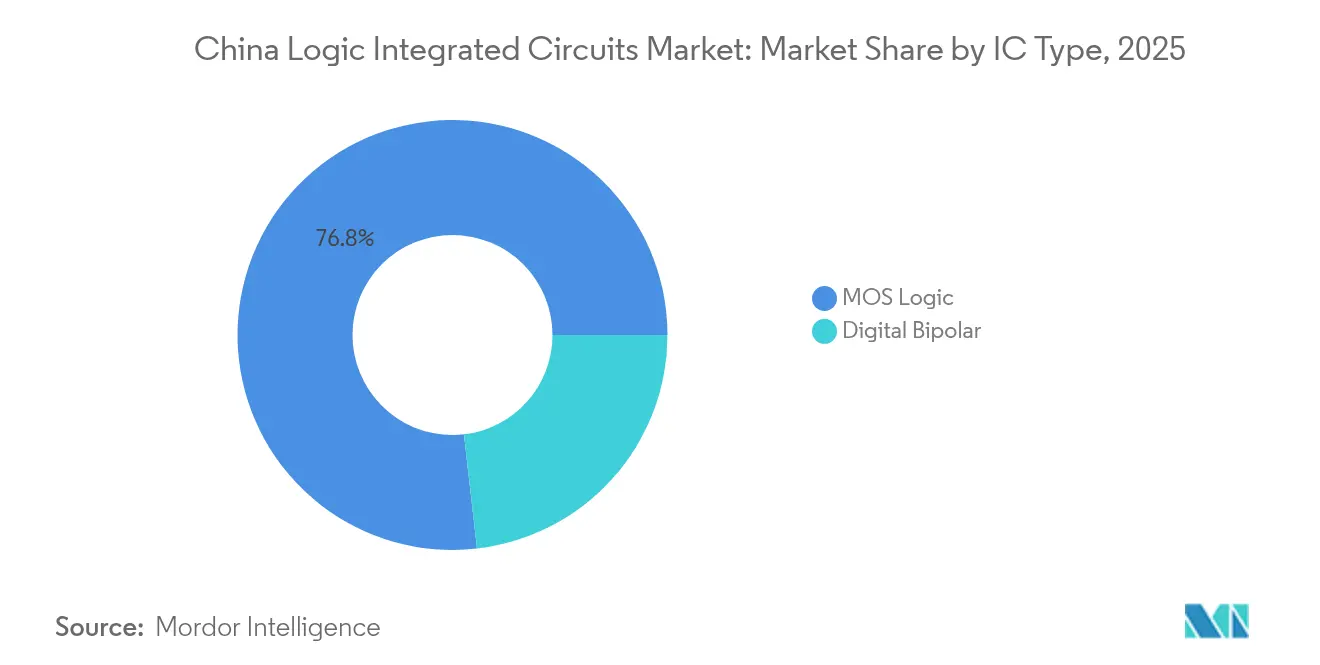

- By IC type, MOS Logic captured 76.82% of the China logic integrated circuits market share in 2025, while Drivers/Controllers are projected to advance at 11.08% CAGR to 2031.

- By technology node, 22/20 nm held 34.25% revenue in 2025; ≤10 nm nodes are set to expand at a 12.41% CAGR through 2031.

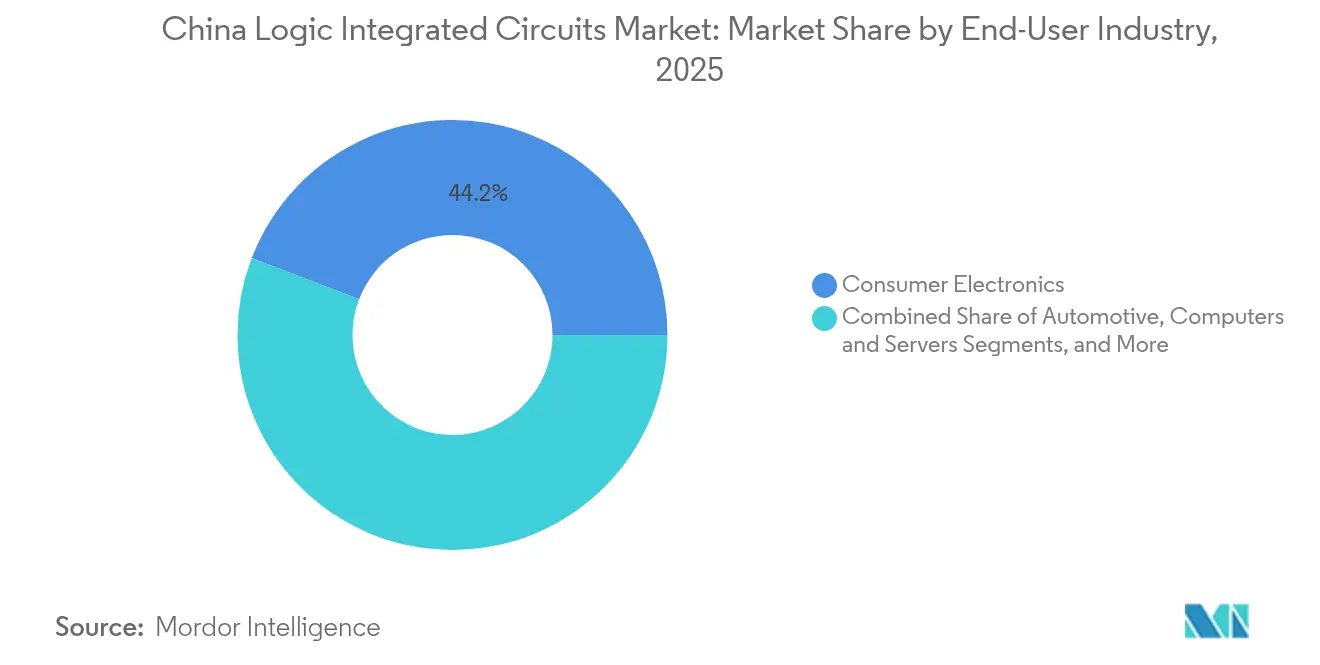

- By end-user industry, consumer electronics led with 44.18% revenue in 2025, whereas automotive applications are forecast to grow at 14.08% CAGR to 2031.

- By business model, the design/fabless segment accounted for 67.05% of the China logic integrated circuits market size in 2025 and is projected to record a 12.88% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Logic Integrated Circuits Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| State-led "Made in China 2025" Self-Sufficiency Mandate | +2.8% | National, with a concentration in the Yangtze River Delta and the Pearl River Delta | Long term (≥ 4 years) |

| 5G Smartphone and Wearable Production Upswing in Guangdong/Zhejiang | +1.9% | Guangdong and Zhejiang provinces, spillover to Jiangsu | Medium term (2-4 years) |

| NEV/ADAS Demand Catalysing Automotive Logic IC Content | +2.1% | National, with early gains in Shanghai, Shenzhen, Guangzhou | Medium term (2-4 years) |

| Hyperscale Data-Centre Build-out by BAT + C Drives High-End Logic | +1.5% | National, concentrated in Beijing, Shanghai, Hangzhou | Short term (≤ 2 years) |

| Government Subsidies for 28nm → 7nm Domestic Fab Lines | +1.4% | National, focused on major semiconductor hubs | Long term (≥ 4 years) |

| Rapid Proliferation of Smart-Home and Industrial IoT Modules | +1.0% | National, with manufacturing concentration in eastern provinces | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

State-led "Made in China 2025" Self-Sufficiency Mandate

Central and municipal authorities coordinated record incentives that lifted domestic chip production from 23% in 2024 toward a 70% policy target by 2025. Local funds in Beijing and Shanghai each set investment pools exceeding USD 20 billion, while Chengdu and Jiangsu offered annual subsidies topping USD 70 million. Ten-year tax holidays for 28 nm and better nodes reduced effective production costs and accelerated fab ramp-ups. As a result, the China logic integrated circuits market logged swift capacity gains at 28-65 nm, where domestic share rose to 31.5% in 2024.

5G Smartphone and Wearable Production Upswing in Guangdong/Zhejiang

Guangdong’s import bill of CNY 1 trillion (USD 140 billion) of semiconductors in 2024 spurred 40 new fabrication projects worth USD 74 billion, anchoring large orders for logic devices in 5G handsets. Smarter Micro’s STAR Market listing raised CNY 1.5 billion (USD 210 billion) to scale RF logic for premium smartphones, while Zhejiang’s CNY 28.6 billion (USD 3.99 billion) semiconductor sales underscored a packaging and materials specialization that improved supply resilience. This coastal hub synergy trimmed device lead times and drove incremental unit demand inside the China logic integrated circuits market.

NEV/ADAS Demand Catalysing Automotive Logic IC Content

Electric vehicle penetration surpassed 39% in 2024, prompting over 300 domestic automotive-grade chip makers to enter the field, up from 30 three years earlier. BYD invested CNY 100 billion (USD 13.96 billion) in smart driving R&D and produced 70% of components in-house, showcasing vertical integration that lifted driver and controller IC volumes. Horizon Robotics and Volkswagen launched a USD 950 million joint venture, further increasing demand for high-performance logic in ADAS stacks. Forecast NEV penetration of 72% by 2030 cements a structural pull for the China logic integrated circuits market.

Hyperscale Data-Centre Build-out by BAT + C Drives High-End Logic

China’s “East Data West Computing” program sought to raise installed data-centre racks from 30,000 in 2020 to 720,000 by 2025, unlocking yearly investments of CNY 400 billion (USD 55.82 billion) for AI-oriented logic chips.[1]MERICS, “Oceans of Data Lift All Boats,” merics.org Alibaba Cloud deployed liquid-cooled facilities in Zhangbei, while China Mobile and Tencent established 5G-integrated campuses that consumed growing volumes of high-core-count processors. Although some installations remained underutilized, aggregate server demand still lifted near-term orders for advanced logic.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| US Export Controls on <14nm Tools and EDA | -1.8% | National, with concentrated impact on advanced node fabs | Long term (≥ 4 years) |

| Acute Design-Talent Shortage at Advanced Nodes | -1.2% | National, particularly acute in Beijing, Shanghai, Shenzhen | Medium term (2-4 years) |

| Capital-Intensity and Lengthy ROI of Leading-Edge Fabs | -0.9% | National, with primary impact on major foundry operators | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

US Export Controls on <14 nm Tools and EDA

Successive BIS rulings in 2024 curbed access to EUV equipment and mandated licences for Cadence and Synopsys software exports, delaying sub-14 nm process commercialization by an estimated two to three years. SMIC’s 5 nm production via deep-UV quadruple patterning achieved functional chips but endured 40-50% cost penalties and lower yield versus overseas peers. These constraints moderate the long-term CAGR of the China logic integrated circuits market.

Acute Design-Talent Shortage at Advanced Nodes

The industry’s skills gap exceeded 200,000 engineers in 2024, with chip-design salaries reaching CNY 1.2 million (USD 170 thousand) annually and 17% turnover at top foundries. While university enrolments in integrated-circuit majors nearly doubled, more than 60% of graduates lacked hands-on experience, lengthening ramp-up cycles for new design houses. Persistent labour deficits weigh on the China logic integrated circuits market growth outlook.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By IC Type: MOS Logic Remains Predominant

MOS Logic accounted for 76.82% revenue in 2025, anchored by ubiquitous system-on-chip designs for phones, EVs, and IoT gateways. Drivers/Controllers registered the fastest 11.08% CAGR, sustained by high-voltage traction inverters and motor controls used in NEVs. Standard Cells and Special-Purpose MOS held stable demand from cloud servers, whereas Gate Arrays filled niche customised logic needs. Digital Bipolar solutions persisted in optical-network backbones yet saw a shrinking footprint due to higher power draw.

Sophisticated Drivers/Controllers benefited from 3D multi-die integration, capitalised by SJSemi’s USD 700 million funding, enhancing local supply resilience against foreign alternatives. BYD Semiconductor’s BF1181 1200 V driver advances domestic automotive-grade reliability, supporting China's logic integrated circuits market size returns at the component level.

By Technology Node: Advanced Scaling Push Intensifies

The 22/20 nm bracket captured 34.25% revenue in 2025, while ≤10 nm output grew at 12.41% CAGR as indigenous equipment matured. Domestic 28 nm lines, enabled by Shanghai Micro Electronics DUV lithography, reached 31% global capacity share by 2027, bolstering China's logic integrated circuits market resilience. Mature ≥65 nm nodes stayed relevant for power devices and industrial IoT, whereas 16/14 nm acted as a stepping-stone for FINFET learning curves.

SMIC and Huawei collaborated on a 5 nm Kirin processor, demonstrating deep-UV patterning prowess, albeit with cost premiums. Parallel R&D into 14 nm FINFET tools underpinned longer-term autonomy for the Chinese logic integrated circuits market.

By End-User Industry: Automotive Outpaces Consumer Electronics

Consumer electronics held 44.18% revenue in 2025, yet automotive logic IC demand posted a 14.08% CAGR to 2031 on rising ADAS complexity. IT and communication infrastructure maintained solid growth from the 5G rollout, while industrial IoT expanded through smart-factory upgrades. Automotive design wins drove larger die sizes and higher ASPs, lifting the China logic integrated circuits market size per vehicle.

BYD, Tesla China, and Horizon Robotics expanded ecosystem partnerships, accelerating localisation of MCU, power management, and perception processors. Policy targets for a 72% NEV share by 2030 indicated a durable pipeline for high-reliability logic.

By Business Model: Fabless Design Leads Value Creation

Fabless firms commanded 67.05% revenue in 2025 and projected a 12.88% CAGR, aligning with China’s IP-centric ambition. Lower capex allowed rapid pivots toward AI accelerators and edge computing. IDM operations persisted in power and sensor niches, where tight process control is mandatory. Leading IDM Silan Microelectronics shipped 220,000 wafers monthly, signaling a nascent domestic balance.

Elevated design activity fed consistent wafer starts for SMIC and Hua Hong, reinforcing a virtuous cycle that enlarged the China logic integrated circuits market.

Geography Analysis

The Yangtze River Delta and Pearl River Delta together hosted the bulk of fabrication, assembly, and design capacity. Guangdong unveiled 40 semiconductor projects worth USD 74 billion and imported CNY 1 trillion (USD 140 billion) chips in 2024, catalysing local sourcing programmes. Shanghai posted CNY 300 billion (USD 41.87 billion) sector sales, Jiangsu excelled in back-end services with Wuxi targeting CNY 280 billion (USD 39.08 billion) output by 2025, while Zhejiang specialised in materials and advanced packaging.

Beijing functioned as a policy, R&D, and design nucleus, anchoring SMIC’s headquarters and Huawei’s HiSilicon labs. Subsidy programmes and university clusters supplied talent, yet the capital region mirrored the nationwide engineer shortfall. Western provinces attracted data-centre investment under “East Data West Computing,” though power and skills constraints slowed chip-ecosystem migration. Emerging hubs such as Suzhou and Ganzhou rolled out tax holidays and land grants, broadening the territorial scope of the Chinese logic integrated circuits market.

Competitive Landscape

Competition remained moderate as top domestic players consolidated share yet faced strong global incumbents. SMIC attained 6% worldwide foundry quota in 2024, overtaking GlobalFoundries and UMC on mature-node strength.[4]CNBC, “SMIC Now the No. 3 Foundry in the World,” cnbc.com Hua Hong invested USD 6.7 billion in a Wuxi fab focused on 65-40 nm, reinforcing domestic supply. BYD Semiconductor leveraged 70% in-house sourcing to capture EV logic margins, while Huawei pursued an end-to-end chip stack despite sanctions.

Price competition surfaced in silicon-carbide wafers, where local vendors undercut Wolfspeed by 30%, signalling a “China shock” in mature semiconductors. SJSemi and TongFu Microelectronics raced to commercialise hybrid bonding and 3D die stacking, addressing packaging bottlenecks. Intellectual-property filings in smart home subsystems broadened application diversity.

China Logic Integrated Circuits Industry Leaders

-

STMicroelectronics N.V.

-

Texas Instruments Inc

-

Renesas Electronics Corporation

-

Analog Devices Inc.

-

Intel Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: GlobalFoundries unveiled a USD 16 billion US expansion to reclaim mature-node volumes from Asian rivals.

- May 2025: SMIC disclosed four new 12-inch fabs scheduled after 2025 aimed at 28 nm and above production.

- April 2025: Micron received USD 6.1 billion CHIPS Act support for domestic memory fabs.

- March 2025: Tata Electronics allied with Himax and PSMC to create an Indian display and AI sensing cluster.

China Logic Integrated Circuits Market Report Scope

Logic Integrated Circuits (ICs) are semiconductor devices that perform basic logical operations on digital input signals to produce digital output signals. They are a core component of logic circuits widely used in various applications, including digital electronics, computers, and communication systems. These ICs operate based on logic levels, which are voltage ranges corresponding to logical conditions. These levels determine whether a signal is interpreted as a high or low state. It is essential for communicating ICs to use the same logic levels to ensure proper communication and avoid potential issues.

The study tracks the revenue accrued through the sale of logic integrated cicruits products by various players in China. The study also tracks the key market parameters, underlying growth influencers, and major vendors operating in the industry, which supports the market estimations and growth rates over the forecast period. The study further analyses the overall impact of COVID-19 aftereffects and other macroeconomic factors on the market. The report's scope encompasses market sizing and forecasts for the various market segments.

The China logic integrated circuits market is segmented by IC type (digital bipolar, MOS logic [MOS general purpose, MOS gate arrays, MOS drivers/controllers, MOS standard cells, and MOS special purpose]), and by application (consumer electronics, automotive, IT and communication, computer, and other applications). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Digital Bipolar | |

| MOS Logic | General-Purpose |

| Gate Arrays | |

| Drivers / Controllers | |

| Standard Cells | |

| Special-Purpose |

| ≥65 nm |

| 45/40 nm |

| 32/28 nm |

| 22/20 nm |

| 16/14 nm |

| ≤10 nm |

| Consumer Electronics |

| Automotive |

| IT and Communication Infrastructure |

| Computers and Servers |

| Industrial and IoT |

| Other Applications |

| IDM |

| Design/ Fabless Vendor |

| By IC Type | Digital Bipolar | |

| MOS Logic | General-Purpose | |

| Gate Arrays | ||

| Drivers / Controllers | ||

| Standard Cells | ||

| Special-Purpose | ||

| By Technology Node | ≥65 nm | |

| 45/40 nm | ||

| 32/28 nm | ||

| 22/20 nm | ||

| 16/14 nm | ||

| ≤10 nm | ||

| By End-User Industry | Consumer Electronics | |

| Automotive | ||

| IT and Communication Infrastructure | ||

| Computers and Servers | ||

| Industrial and IoT | ||

| Other Applications | ||

| By Business Model | IDM | |

| Design/ Fabless Vendor | ||

Key Questions Answered in the Report

What is the size and growth rate of the Chinese logic integrated circuits market?

The market was valued at USD 52.73 billion in 2026 and is projected to reach USD 87.99 billion by 2031, reflecting a 10.78% CAGR.

Which product category currently dominates revenue?

MOS Logic held 76.82% of market share in 2025, driven by broad system-on-chip adoption in smartphones, EVs, and data-centre hardware.

How do U.S. export controls influence China’s advanced-node roadmap?

Licence requirements on sub-14 nm tools and EDA software have extended time-to-market by an estimated two to three years and raised 5 nm production costs by 40-50%.

Why is automotive demand reshaping the market’s long-term outlook?

Electric-vehicle penetration surpassed 39% in 2024 and is forecast to hit 72% by 2030, pushing automotive logic IC shipments to a 14.08% CAGR—the fastest among all end-user groups.

Where are the principal manufacturing clusters located?

The Yangtze River Delta (Shanghai-Jiangsu-Zhejiang) and Pearl River Delta (Guangdong) host the majority of fabs, design houses, and packaging plants, supported by provincial subsidy programmes.

Page last updated on: