Taiwan Integrated Circuits Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

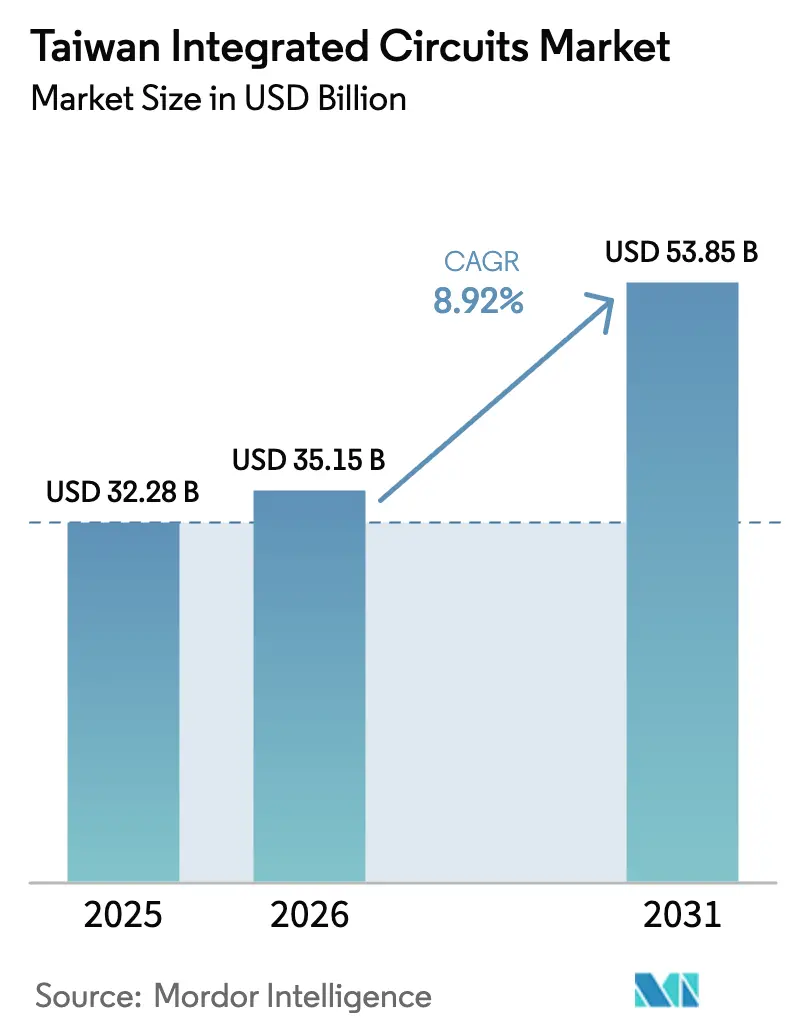

| Base Year Market Size (2025) | USD 32.28 Billion |

| Market Size (2026) | USD 35.15 Billion |

| Market Size (2031) | USD 53.85 Billion |

| Growth Rate (2026 - 2031) | 8.92% CAGR |

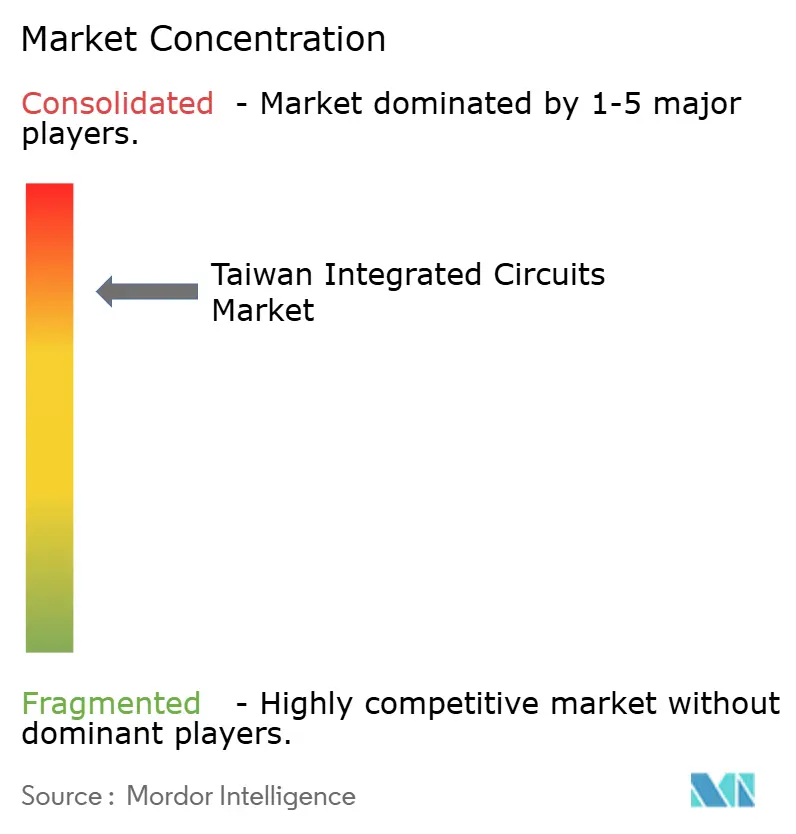

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Taiwan Integrated Circuits Market Analysis by Mordor Intelligence

Taiwan integrated circuits market size in 2026 is estimated at USD 35.15 billion, growing from 2025 value of USD 32.28 billion with 2031 projections showing USD 53.85 billion, growing at 8.92% CAGR over 2026-2031. Growth has been propelled by the island’s dominance in sub-7 nm production, comprehensive policy incentives under the Taiwan Chip Act, and brisk demand for AI servers that rely on cutting-edge logic and memory devices. Logic ICs maintained leadership in 2024, while microcontrollers led growth as vehicle electrification accelerated, and ≤5 nm nodes expanded fastest on the back of AI accelerators and GPUs. Widespread 300 mm adoption, strong consumer-electronics pull, and the resilience of integrated device manufacturers (IDMs) reinforce the competitive advantage of the Taiwan integrated circuits market.

Key Report Takeaways

- By IC type: Logic devices held 55.12% of Taiwan integrated circuits market share in 2025, while microcontrollers recorded the fastest 10.62% CAGR through 2031.

- By technology node: The 14-28 nm bracket led with 34.05% revenue share in 2025; ≤5 nm nodes are forecast to grow at 14.45% CAGR.

- By wafer size: 300 mm substrates accounted for 62.18% of the Taiwan integrated circuits market size in 2025 and are expanding at a 9.62% CAGR.

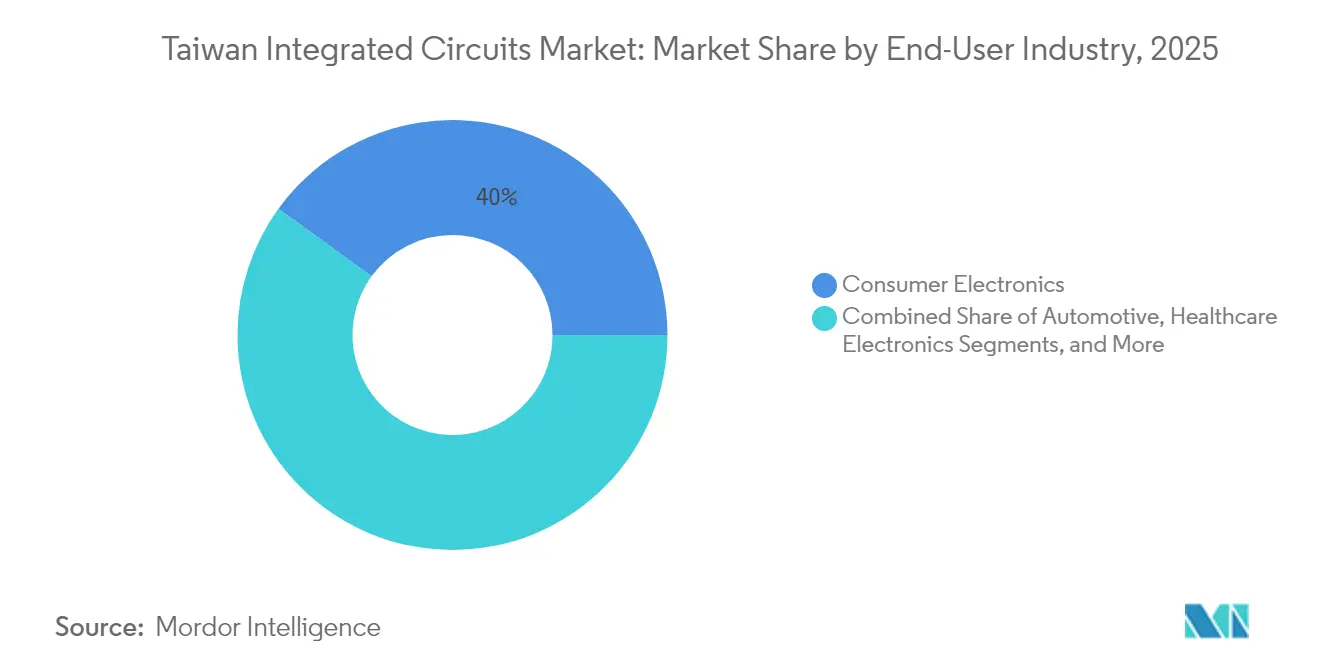

- By end-user industry: Consumer electronics captured 40.02% share in 2025, while automotive applications are advancing at 12.38% CAGR.

- By business model: IDMs commanded 66.15% Taiwan integrated circuits market share in 2025; design-fabless vendors are growing at 11.47% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Proportional positioning is established by comparing country level and regional contributions against the global total, including that of Taiwan. The integrated circuits market share in our global report expresses these relative weights.

Taiwan Integrated Circuits Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of AI/ML accelerator demand from Taiwanese hyperscalers | +1.5% | Global, with concentration in Taiwan and US data centers | Medium term (2-4 years) |

| Government "Chip-Based Precision Health" initiative accelerating medical IC uptake | +0.9% | Taiwan domestic market, spillover to APAC | Long term (≥ 4 years) |

| Reshoring incentives under Taiwan Chip Act attracting advanced-node production | +1.8% | Taiwan domestic, US partnership facilities | Medium term (2-4 years) |

| Electric two-wheeler boom spurring automotive-grade MCU demand | +1.2% | APAC core markets, emerging in Southeast Asia | Short term (≤ 2 years) |

| Rapid 5G SA rollout driving RF-front-end and base-band IC volumes | +2.1% | Global, with early adoption in Taiwan and South Korea | Short term (≤ 2 years) |

| Adoption of Chiplet-based heterogeneous integration in local OSATs | +0.8% | Taiwan domestic, expanding to global OSAT operations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expansion of AI/ML Accelerator Demand from Taiwanese Hyperscalers

Hyperscalers headquartered in Taiwan and the United States ramped capital outlays for AI infrastructure, with global spending expected to reach USD 270 billion by 2025. Taiwan Semiconductor Manufacturing Company (TSMC) indicated that AI accelerators and GPUs contributed 15% of 2024 revenue and that the figure should double in 2025. Demand concentrates on advanced packaging—such as chip-on-wafer-on-substrate—to maximize bandwidth and thermal performance. MediaTek’s forthcoming GB10 Grace Blackwell Superchip, slated for 2 nm tape-out in September 2025, underscores how local design houses depend on Taiwan’s leading-edge fabs and packaging clusters. Broader AI-PC rollouts, rising from 19% penetration in 2024 to a forecast 60% by 2027, reinforce steady pull on 3 nm and 5 nm capacity. The sustained surge in accelerator demand is therefore a structural growth driver for the Taiwan integrated circuits market.

Government “Chip-Based Precision Health” Initiative Accelerating Medical IC Uptake

Taipei’s precision-health blueprint has bolstered local med-tech, where biomedical companies increased from 1,355 in 2010 to 2,143 by 2024 and exports reached USD 6 billion.[1]Research Institute for Democracy, Society and Emerging Technology, “From Critical Chips to International Alliances,” dset.tw The program incentivizes secure flash memories, low-power microcontrollers, and mixed-signal front ends tailored to diagnostic devices. Winbond positioned its TrustME Secure Flash for regulated medical equipment, ensuring data integrity in point-of-care analyzers. Start-ups such as Haiim and iXensor adopted Taiwanese sensors and AFE chips for portable diagnostics, demonstrating local design-to-manufacturing agility. As healthcare digitization progresses, recurring demand for secure, power-efficient ICs broadens the Taiwan integrated circuits market beyond consumer handsets. Over the long term, the initiative diversifies revenue streams and cushions cyclicality.

Rapid 5G SA Rollout Driving RF-Front-End and Base-Band IC Volumes

Taiwan’s 5G standalone build-out accelerated in 2024, triggering new orders for RF switches, power amplifiers, and base-band SoCs. WIN Semiconductors introduced a moisture-rugged 0.1 µm GaAs pHEMT platform for 5G macro base stations, addressing reliability in subtropical climates. Local test-equipment vendor TMYTEK delivered mmWave solutions operating up to 40 GHz, intensifying demand for high-linearity front-end modules. Gallium nitride adoption improved efficiency in 5G power amplifiers, an area where Taiwan’s compound-semiconductor ecosystem has matured rapidly. MediaTek’s inclusion of dialect-specific AI speech models in 5G chipsets highlighted the interplay of RF and AI innovation. Collectively, these deployments enlarged revenue opportunities for mid-band and mmWave components inside the Taiwan integrated circuits market.

Electric Two-Wheeler Boom Spurring Automotive-Grade MCU Demand

Electrification of scooters across Taiwan, Vietnam, and Indonesia lifted shipments of automotive-grade microcontrollers that manage battery systems, motor inverters, and connectivity modules. Premium two-wheelers began integrating NVIDIA Drive Thor chips for advanced rider-assist functions, generating incremental MCU demand for sensor fusion and safety monitoring. Taiwanese MCU suppliers leveraged proximity to assemblers to tailor devices for tropical heat dissipation and cost efficiency. IoT connectivity requirements propagated Bluetooth and cellular co-processors, expanding system BOM content per vehicle. Short-term volume spikes in regional markets position automotive MCUs as a double-digit growth category for the Taiwan integrated circuits market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| U.S.–China export-license constraints on EUV tool imports | -0.7% | Taiwan domestic, affecting advanced node capacity | Short term (≤ 2 years) |

| Water-supply volatility in Central and Southern Science Parks | -0.5% | Taiwan Central and Southern regions | Medium term (2-4 years) |

| Tight talent pool for 2-nm process engineers | -0.4% | Taiwan domestic, spillover to global operations | Long term (≥ 4 years) |

| Rising electricity tariffs eroding fab cost advantage | -0.3% | Taiwan domestic manufacturing facilities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

U.S.–China Export-License Constraints on EUV Tool Imports

Taiwan added 601 entities to its restricted-export list in June 2025, mirroring U.S. measures on advanced lithography transfers. The policy constrained short-term deliveries of extreme-ultraviolet scanners from ASML, compelling fabs to prioritize existing toolsets for 2 nm ramp schedules. Any deviation lengthens cycle times and could defer volume shipments of 1.6 nm A16 platforms slated for 2026, thereby tempering growth in the Taiwan integrated circuits market. While strategic stockpiling mitigated immediate shortages, ongoing regulatory shifts insert planning uncertainty and may accelerate overseas diversification.

Tight Talent Pool for 2 nm Process Engineers

The industry estimated a requirement for an additional 88,000 semiconductor engineers by 2029 to support node migration, yet recruitment lagged demand. TSMC alone sought 8,000 hires in 2025, intensifying competition among foundries, OSATs, and EDA vendors. Declining birth rates and cross-strait poaching further depleted the local talent reservoir. Companies responded by tapping graduates from Southeast Asia, but onboarding and up-skilling extended ramp timelines. The structural shortage constrains R&D throughput and could slow the long-term CAGR of the Taiwan integrated circuits market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By IC Type: Logic Dominance Amid MCU Surge

Logic ICs anchored the Taiwan integrated circuits market in 2025 with a 55.12% share, reflecting heavy procurement of AI accelerators and HPC processors by hyperscalers. Sustained back-end capacity and 3 nm production competence supported high yields in logic production. Microcontrollers grew fastest at 10.62% CAGR, powered by vehicle electrification, smart appliances, and industrial IoT nodes. Analog power-management chips sustained demand in motor drives and battery systems, while specialty memory suppliers such as Winbond shipped niche DRAM and NAND for automotive dashboards.

Through 2031, the segment mix will continue to evolve. AI inference moving to edge devices keeps logic volumes high, whereas MCU adoption widens into residential energy-storage systems and robotics. The Taiwan integrated circuits market size for microcontrollers is projected to expand steadily as government incentives foster smart-mobility applications. Memory and analog houses expect incremental volumes from precision-health equipment and renewable-energy converters. Collectively, the breadth of IC types underpins Taiwan’s role as a one-stop supply hub, insulating the ecosystem against cyclical swings.

By Technology Node: Advanced Nodes Drive Innovation

The 14-28 nm category delivered 34.05% revenue share in 2025 and remains the workhorse for automotive, industrial, and mid-range mobile devices. Yield maturity and cost efficiency favour its continued use in ADAS controllers and industrial PLCs. However, ≤5 nm processes carried the highest 14.45% CAGR outlook as AI accelerators, flagship smartphones, and cloud CPUs migrated to dense libraries. TSMC’s A16 1.6 nm roadmap, announced in April 2025, promises 8-10% performance uplift with 15-20% lower power draw.

From 2026 onward, mass-production of 2 nm devices will buttress the Taiwan integrated circuits market size for advanced-node wafers. Legacy nodes ≥45 nm remain viable for mixed-signal and sensor ICs, especially in automotive environments that require voltage tolerance. This multi-node equilibrium allows foundries to optimize fab utilization by routing products to cost-appropriate lines, sustaining profitability across cycles.

By Wafer Size: 300 mm Efficiency Gains

In 2025, 300 mm fabs contributed 62.18% of revenues and produced mainstream logic and memory dies at competitive cost per bit. Scale economies and mature equipment sets underpin the 9.62% CAGR expected for 300 mm capacity through 2031. Dedicated 12-inch greenfield investments by Powerchip and United Semiconductor have reinforced local supply.

Smaller 200 mm fabs continued to fulfil analog, power, and RF orders where design migrations carry prohibitive NRE. Compound-semiconductor makers also retained <200 mm lines due to substrate constraints. Over the forecast period, 300 mm will dominate volume production, yet 200 mm will stay relevant for discrete power devices and GaAs/GaN RF chips. The balanced wafer-size mix stabilises capacity utilisation and cushions the Taiwan integrated circuits market against sharp demand swings.

By End-User Industry: Consumer Electronics Leadership

Consumer electronics commanded 40.02% share in 2025, with smartphones and wearables as anchor products for advanced SoCs and connectivity ICs. MediaTek maintained robust shipment momentum across 4 nm and 3 nm mobile platforms aimed at global OEMs. Automotive demand, climbing at 12.38% CAGR, continued to outpace other sectors owing to electric-vehicle architectures requiring high-reliability microcontrollers, power converters, and sensor interfaces.

The rollout of 800 V drivetrains and Level-2+ autonomy amplifies semiconductor content per vehicle, expanding average bill of materials. Industrial and factory automation leverages rugged MCUs and AI-enabled vision processors for quality inspection. Healthcare electronics, driven by precision-health policy, accelerates uptake of secure memories and mixed-signal ASICs. Collectively, the diverse consumption base secures long-term growth for the Taiwan integrated circuits market.

By Business Model: IDM Resilience Amid Fabless Growth

IDMs preserved 66.15% revenue share in 2025, benefiting from tight integration of R&D, fab, and test. TSMC’s scale and technical breadth remained pivotal, while Vanguard International Semiconductor and Powerchip supplied speciality logic and DRAM. The design-fabless cohort grew at 11.47% CAGR, as firms such as MediaTek and Novatek released custom AI edge processors tailored to client workloads.

Fabless houses exploited Taiwan’s foundry density to iterate designs rapidly, enhancing time-to-market. The ecosystem also nurtured IP and EDA tool vendors specialising in 3D-IC partitioning. Going forward, chiplet architectures encourage collaborative development between IDMs and fabless players, bolstering supply-chain resilience and sustaining the Taiwan integrated circuits market.

Geography Analysis

Taiwan contributed 63.8% of global semiconductor output and over 70% of sub-7 nm production in 2025, positioning the Taiwan integrated circuits market as a strategic cornerstone of the worldwide electronics supply chain. Central and Southern Science Parks anchored wafer-fabrication clusters, though drought cycles prompted water-recycling investments to secure operations.

The government’s “AI-Island” infrastructure plan, comprising ten national projects, expanded data-center, photonics, and high-bandwidth network capacity, attracting new design starts. Overseas footprints in Arizona, Kumamoto, and Dresden offered geopolitical hedge while keeping advanced R&D in Hsinchu. Joint ventures such as the VSMC 300 mm fab in Singapore illustrated outward expansion of Taiwanese process know-how.

An emergent drone-manufacturing corridor, backed by USD 1.35 billion from 2024-2028, fortified diversification, using local sensors and flight-control ASICs to reach 15,000 units per month by 2028. Strategic location, policy backing, and integrated supply networks collectively reinforce competitiveness and resilience of the Taiwan integrated circuits market.

Mordor Intelligence examines the integrated circuits market across diverse other regional markets as well, including Europe, while also offering granular country-level perspectives for South Korea, China, and United States and more.

Competitive Landscape

The market remained highly concentrated, with TSMC owning 60% of advanced logic production and 90% of bleeding-edge capacity, establishing a formidable competitive barrier.[4]The Indo-Pacific Studies Center, “Beyond Chips: Will the U.S. Still Defend Taiwan?,” indo-pacificstudiescenter.org The firm earmarked USD 38–42 billion capex for 2025 to support 2 nm and 1.6 nm transitions. ASE Technology, the world’s largest OSAT, invested in VIPack chiplet interconnects achieving sub-5 pJ/bit power, cementing packaging leadership.

WIN Semiconductors preserved dominance in GaAs and GaN RF foundry services, while GlobalWafers scaled silicon-on-insulator substrates for RF front-end and automotive radar. Alliances rose in importance: MediaTek teamed with Ranovus for 6.4 Tbps co-packaged optics targeting AI clusters, and ASE joined the Silicon Photonics Industry Alliance to standardise optical I/O. Players navigated geopolitical headwinds by diversifying production footprints yet retained core R&D in Taiwan, underscoring the centrality of the Taiwan integrated circuits market to global semiconductor innovation.

Smaller firms exploited niches: Andes Technology advanced 64-bit RISC-V cores for edge AI at nearly 30% long-term CAGR, and Etron Technology focused on in-package memory buffers for chiplet assembly. Competitive intensity remains elevated as design complexity soars and capital requirements mount, yet shared ecosystem benefits sustain collaborative innovation.

Taiwan Integrated Circuits Industry Leaders

-

STMicroelectronics N.V.

-

NXP Semiconductors N.V.

-

Intel Corporation

-

Samsung Electronics Co Ltd

-

SK Hynix Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: TSMC announced volume production of A16 technology with Super Power Rail and NanoFLEX transistors, promising 8–10% higher performance and 15–20% lower power.

- June 2025: ITRI projected Taiwan will become the global core base for co-packaged optics as silicon-photonics switches enter mass production.

- May 2025: Winbond’s chairman highlighted AI and security as strategic focuses while cautioning on long-term New Taiwan dollar appreciation.

- April 2025: TSMC posted Q1 revenue of NT$839.25 billion (USD 25.85 billion) and EPS of NT$13.94, driven by AI accelerator demand.

Taiwan Integrated Circuits Market Report Scope

Integrated circuits (ICs) are compact electronic devices that integrate multiple components, such as transistors, resistors, capacitors, and diodes—onto a single piece of semiconductor material, typically silicon. This integration facilitates the creation of complex circuits capable of performing various functions within a small physical footprint.

For market estimation, the revenue generated from sales of various types of integrated circuits used in various industries, such as consumer electronics, automotive, IT and telecommunication, manufacturing, and automation, across Taiwan is being tracked. The market trends are evaluated by analyzing the investments made in product innovation, diversification, and expansion.

The Taiwan integrated circuits market is segmented by type (analog IC, logic IC, memory, and micro [microprocessor, microcontrollers, and digital signal processors]) and end-user industry (consumer electronics, automotive, IT & telecommunications, manufacturing & automation, and Other end-user industries). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Analog IC | |

| Logic IC | |

| Memory IC | |

| Microcomponents | Microprocessors (MPU) |

| Microcontrollers (MCU) | |

| Digital Signal Processors (DSP) |

| ≥45 nm |

| 28–45 nm |

| 14–28 nm |

| 7–14 nm |

| ≤5 nm |

| 200 mm (8-inch) |

| 300 mm (12-inch) |

| <200 mm Legacy |

| Consumer Electronics | Smartphones and Tablets |

| Wearables and AR/VR Devices | |

| Automotive | ADAS and EV Powertrain |

| Infotainment and Telematics | |

| IT and Telecommunications | Data-Center and Server |

| Networking and 5G Infrastructure | |

| Industrial and Factory Automation | |

| Healthcare Electronics | |

| Aerospace and Defense |

| Integrated Device Manufacturers (IDM) |

| Design/ Fabless Vendor |

| By IC Type | Analog IC | |

| Logic IC | ||

| Memory IC | ||

| Microcomponents | Microprocessors (MPU) | |

| Microcontrollers (MCU) | ||

| Digital Signal Processors (DSP) | ||

| By Technology Node | ≥45 nm | |

| 28–45 nm | ||

| 14–28 nm | ||

| 7–14 nm | ||

| ≤5 nm | ||

| By Wafer Size | 200 mm (8-inch) | |

| 300 mm (12-inch) | ||

| <200 mm Legacy | ||

| By End-user Industry | Consumer Electronics | Smartphones and Tablets |

| Wearables and AR/VR Devices | ||

| Automotive | ADAS and EV Powertrain | |

| Infotainment and Telematics | ||

| IT and Telecommunications | Data-Center and Server | |

| Networking and 5G Infrastructure | ||

| Industrial and Factory Automation | ||

| Healthcare Electronics | ||

| Aerospace and Defense | ||

| By Business Model | Integrated Device Manufacturers (IDM) | |

| Design/ Fabless Vendor | ||

Key Questions Answered in the Report

What is the current value of the Taiwan integrated circuits market?

It was valued at USD 35.15 billion in 2026.

How fast is the Taiwan integrated circuits market expected to grow?

The forecast CAGR is 8.92% between 2026 and 2031.

Which IC type leads the Taiwan integrated circuits market?

Logic devices held 55.12% share in 2025, reflecting strong AI and HPC demand.

Why are ≤5 nm nodes important for Taiwan’s growth?

They show the fastest 14.45% CAGR because AI accelerators and flagship smartphones require higher transistor density.

How significant is automotive demand for Taiwanese chip makers?

Automotive applications are the fastest-growing end-user segment at 12.38% CAGR, driven by electric vehicle and ADAS adoption.

What risks could slow Taiwan’s semiconductor expansion?

Export-license limits on EUV tools, water-supply volatility, talent shortages, and higher electricity tariffs each constrain capacity growth.

Page last updated on: