South Korea Analog Integrated Circuits Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

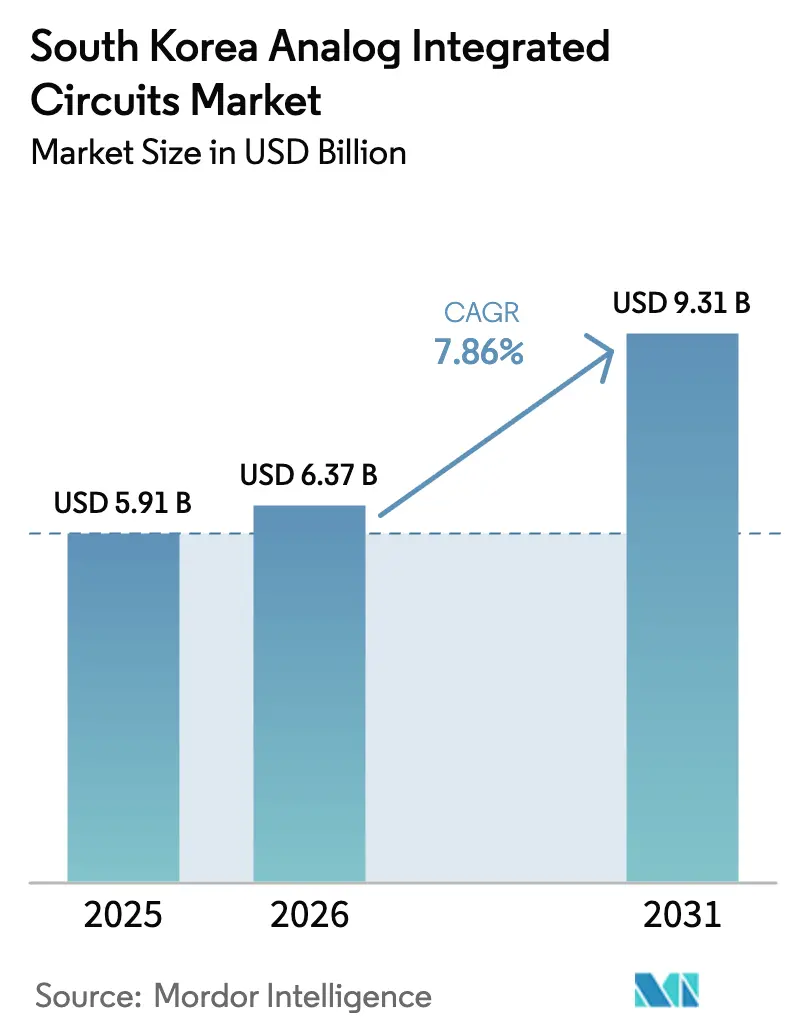

| Base Year Market Size (2025) | USD 5.91 Billion |

| Market Size (2026) | USD 6.37 Billion |

| Market Size (2031) | USD 9.31 Billion |

| Growth Rate (2026 - 2031) | 7.86% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

South Korea Analog Integrated Circuits Market Analysis by Mordor Intelligence

The South Korea analog integrated circuits market size is expected to grow from USD 5.91 billion in 2025 to USD 6.37 billion in 2026 and is forecast to reach USD 9.31 billion by 2031 at 7.86% CAGR over 2026-2031. The expansion reflected record government subsidies under the K-Semiconductor Vision, accelerating 5G base-station deployments, and stronger demand for power-efficient chips in electric vehicles and edge-AI devices. Samsung Electronics overtook Intel as the world’s largest semiconductor supplier in January 2025, confirming national leadership in premium wafer capacity and RF innovation. Government tax credits of up to 50% on R&D, combined with targeted funds for fabless design houses, lowered entry barriers, and set the tone for sustained capital expenditure in analog fabrication. Structural tailwinds also included the roll-out of 53,000 Samsung 5G base stations, Hyundai–Kia’s ramp-up of E-GMP electric vehicles, and KAIST’s neuromorphic breakthroughs, all of which multiplied demand for RF, power-management, and sensor interfaces. Risks centered on skilled-engineer shortages, legacy-node wafer tightness, and intensifying price competition from Chinese foundries offering discounted 28 nm processes.

Key Report Takeaways

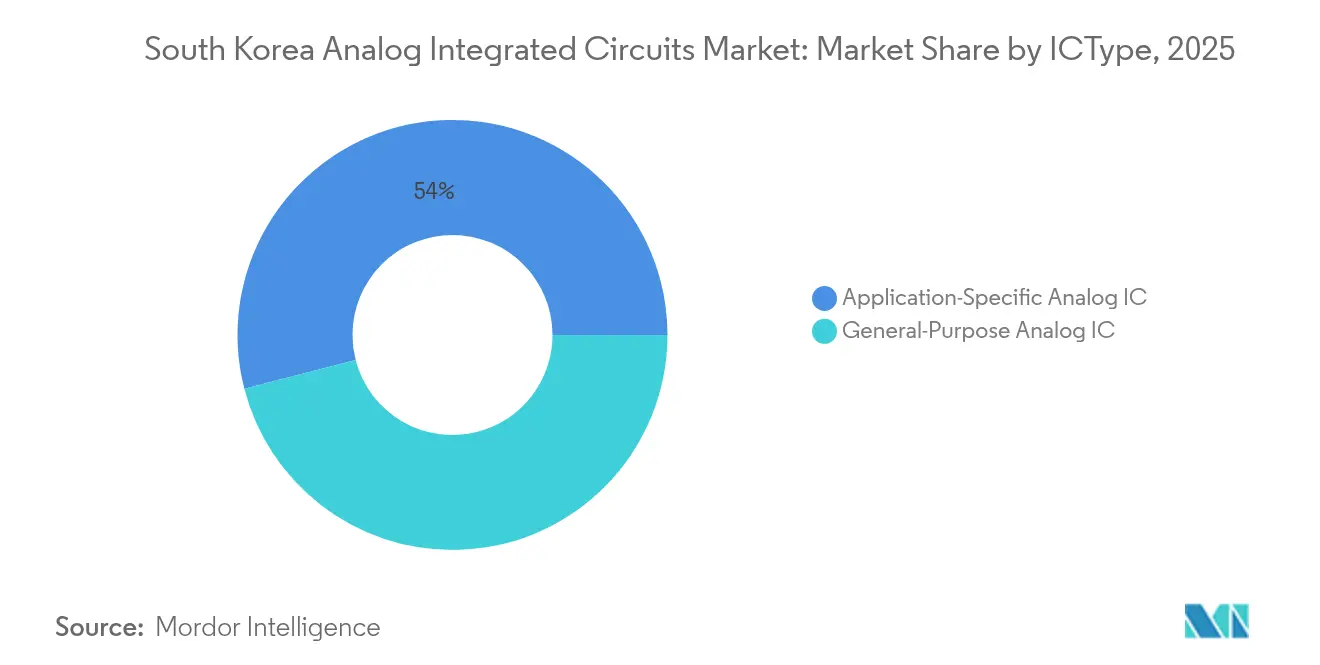

- By IC type, application-specific devices led with 54.02% revenue in 2025 while also logging a 12.32% CAGR through 2031, underscoring dual dominance in automotive and edge-AI verticals.

- By wafer size, the 200-300 mm category captured 50.12% of South Korea's analog integrated circuits market share in 2025, whereas 300 mm output is projected to rise at 13.71% CAGR to 2031.

- By technology node, processes above 180 nm held 58.11% share of the South Korea analog integrated circuits market size in 2025, yet mixed-signal nodes below 28 nm are set to expand at 14.63% CAGR through 2031.

- By business model, IDM vendors commanded 65.05% share in 2025, but fabless players are the fastest movers with 12.74% CAGR on the back of design-specialization incentives.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global valuation is built by aggregating outputs from multiple countries and regions, with South korea being one of the contributors. Our global analog integrated circuit market size represents that cumulative total.

South Korea Analog Integrated Circuits Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid 5G infrastructure rollout elevating RF analog IC demand | +2.1% | National, concentrated in Seoul, Busan, and Incheon | Short term (≤ 2 years) |

| Government "K-Semiconductor Vision" tax and CAPEX incentives | +1.8% | National, with a cluster focus in Gyeonggi Province | Medium term (2-4 years) |

| EV and xEV production surge by Hyundai/Kia, boosting power-management ICs | +1.5% | National manufacturing hubs in Ulsan, Asan | Medium term (2-4 years) |

| Edge-AI and IoT device proliferation in the Korean smart-home ecosystem | +1.2% | National, early adoption in metropolitan areas | Long term (≥ 4 years) |

| Localization push to cut analog IC import dependence | +0.9% | National, supply chain diversification focus | Long term (≥ 4 years) |

| High-resolution OLED/µLED display fabs driving precision analog front-ends | +0.7% | Regional, Samsung Display, and LG Display facilities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid 5G Infrastructure Rollout Elevating RF Analog IC Demand

Nationwide 5G adoption, which crossed 1 million subscribers in only 69 days, immediately boosted orders for high-frequency RF front ends. Samsung’s third-generation mmWave RFIC doubled output power and reduced form factor by 25%, enabling denser radio-access units within constrained base-station footprints.[1]Samsung Electronics, “Samsung unveils new chipsets to enhance next-generation 5G RAN portfolio,” samsung.com Tier-one operators subsequently increased capital expenditure, driving KRW 1.8 trillion (USD 1.3 billion) in combined 2024 revenue at local equipment makers KMW, SeoJin System, and Ace Technologies. RF analog IC vendors benefited from shorter design-in cycles because 3.5 GHz, 28 GHz, and 39 GHz bands all required new gain blocks, phase shifters, and power amplifiers. The effect cascaded into industrial IoT and connected-car platforms, where sub-6 GHz back-up radios complement mmWave links. Consequently, the South Korean analog integrated circuits market witnessed a near-term surge in fab utilization, especially at Samsung Foundry’s 300 mm RF lines.

Government K-Semiconductor Vision Tax and CAPEX Incentives

Tax credits that rose to 50% for R&D expenditures and seven-year duty exemptions for capital goods compressed pay-back periods on new analog fabs. A KRW 1 trillion (USD 730 million) fund earmarked for fabless start-ups lowered prototype costs and expanded the local IP pool. Large enterprises responded with KRW 510 trillion (USD 370 billion) in announced private investments, while SMEs secured low-interest loans that covered clean-room retrofits and test-equipment upgrades. The incentives accelerated process-migration plans toward BCD platforms that integrate analog, digital, and power domains on a single die, thus increasing chip content per automotive module. Over the medium term, the package is expected to raise total installed wafer starts to 7.7 million per month by 2030 and reinforce the South Korean analog integrated circuits market as a key export pillar.

EV and xEV Production Surge by Hyundai/Kia Boosting Power-Management ICs

Hyundai Motor Group’s E-GMP architecture required high-voltage gate drivers, battery-management ICs, and onboard charger controllers. Hyundai Mobis began mass production of lamp-driving and power-integration semiconductors in early 2025, outsourcing wafers to Samsung yet retaining in-house test and packaging. Domestic automotive exports reached USD 70.9 billion in 2023, and policy targets call for 4.5 million zero-emission vehicles by 2030. Power-train electrification pushed analog suppliers to prioritize 200 V–800 V battery-system ASICs with thermal shut-down features that meet ISO 26262 functional-safety standards. The resulting volume uplift broadened the order backlog for 0.18 µm BCD lines, now running at near-full capacity, and reinforced the revenue base of the South Korea analog integrated circuits market.

Edge-AI and IoT Device Proliferation in the Smart-Home Ecosystem

KAIST’s neuromorphic chip achieved 625-fold energy savings versus leading GPUs, validating local expertise in spiking neural networks for always-on audio and vision tasks. Start-ups such as Rebellions and FuriosaAI drew high-profile engineering talent and closed multi-million-dollar funding rounds, injecting diverse IP into low-power sensor hubs. OHSUNG Electronics piloted a Home IoT Edge Hub that embeds voice-command accelerators, indicating strong domestic pull for mixed-signal audio front ends. System-in-package solutions combining Arm Cortex-M0+ microcontrollers with AI coprocessors demonstrated that analog ICs remain indispensable for sensor interfacing, clock generation, and power supervision. These design wins spread over consumer appliances and security systems, widening the total addressable portion of the South Korean analog integrated circuits market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited domestic analog design talent base | -1.4% | National, acute in Seoul, Daejeon tech clusters | Short term (≤ 2 years) |

| Incumbent global suppliers' scale raises entry barriers | -1.1% | Global competition, local market penetration challenges | Medium term (2-4 years) |

| Legacy-node wafer scarcity at Korean foundries | -0.8% | National, concentrated in Gyeonggi manufacturing hubs | Short term (≤ 2 years) |

| Volatile raw-wafer and specialty substrate pricing | -0.6% | Global supply chain, Korean fab operations impact | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Limited Domestic Analog Design Talent Base

Analog design requires deep experience in continuous-time signal integrity, layout-parasitic control, and reliability testing. Small and midsize firms reported 64-hour peak workloads, revealing acute staffing gaps despite premium wage offers. While mega-cluster projects fund university chairs and vocational curricula, the pipeline will not fully close until after 2027. Consequently, several SMEs postponed tape-outs, slowing revenue conversion and softening near-term growth of the South Korea analog integrated circuits market.

Incumbent Global Suppliers’ Scale Raises Entry Barriers

Texas Instruments, Analog Devices, and Infineon maintain decades-long customer qualifications, broad product portfolios, and multibillion-dollar capital budgets that yield cost advantages. At the same time, Chinese foundries cut 28 nm wafer prices, undercutting local IDMs on legacy nodes. Analog customers rarely switch suppliers due to costly re-qualification, which places volume constraints on domestic entrants and tempers price-realization potential across the South Korea analog integrated circuits market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By IC Type: Application-Specific Dominance Drives Specialization

Application-Specific Analog ICs captured 54.02% of South Korea's analog integrated circuits market share in 2025, with automotive, RF, and sensor-interface categories leading the mix. The segment delivered the fastest 12.32% CAGR because vehicle electrification required integrated gate drivers and battery monitors, while 5G base-station roll-outs ordered bespoke LNA and phase-array controllers. Consumer smart-home appliances added volume through audio CODECs and camera-control ASICs. Samsung and Hyundai Mobis secured most of the early production slots, reinforcing localized supply chains that shield key industries from external disruptions.

General-purpose analog ICs remained crucial for power management, signal conversion, and interface bridging across diverse electronics. Data-center UPS upgrades and fast-charging stations lifted demand for synchronous buck controllers and high-side current sensors. Interface ICs riding on USB-PD, HDMI 2.1, and DisplayPort 2.1 upgrades kept ADC and op-amp volumes steady. Although the category trailed application-specific devices in growth, its broad demand base ensured recurrent wafer starts that stabilized foundry loading. The South Korea analog integrated circuits market size for general-purpose devices is projected to expand at mid-single-digit rates through 2031, underpinned by industrial automation retrofits and 6G test-equipment pilots.

By Wafer Size: 300 mm Transition Accelerates Production Scaling

The 200-300 mm segment accounted for 50.12% of South Korea's analog integrated circuits market size in 2025 because legacy power-management and display-driver wafers continued to ship on mature lines. Capacity-optimization efforts nevertheless favored 300 mm migration, raising capital efficiency via higher die-per-wafer ratios. Samsung’s Pyeongtaek campus increased 300 mm analog wafer starts after a 45% CAPEX surge, and DB Hitek approved a KRW 2.5 trillion (USD 1.8 billion) greenfield line targeting 20,000 wafers per month.

Equipment deliveries for the new lines included high-current implant tools and CMP modules configured for thick-oxide BCD stacks. Yield learning on wide-body trench-MOS layouts improved after synchronous design-for-manufacturability workshops among fabless designers and process engineers. Over the forecast horizon, 300 mm wafers are expected to log a 13.71% CAGR, supported by automotive, 5G, and AI accelerators that exceed 100 mm² die areas. Conversely, ≤200 mm fabs will continue producing niche sensor interfaces and legacy mixed-signal ASICs that do not justify line transfers, preserving a balanced wafer-size distribution within the South Korean analog integrated circuits market.

By Technology Node: Legacy Nodes Anchor Market With Advanced Integration Emerging

Processes above 180 nm held 58.11% of South Korea's analog integrated circuits market size in 2025 due to their proven high-voltage tolerance and cost efficiency. Designers favored these nodes for power diodes, LED drivers, and RF power amplifiers, where device physics, not scaling, limits performance. Enhanced mixed-signal nodes below 28 nm, however, posted a 14.63% CAGR by integrating ADCs, DACs, and DSP blocks on advanced FinFET and GAA platforms. Samsung Foundry secured AI accelerator tape-outs at 2 nm that embed low-jitter PLLs and high-dynamic-range LDO regulators, uniting digital cores with precision analog peripherals.

Intermediate 90-180 nm nodes served robust markets in industrial automation and automotive radar front ends. Researchers at ETRI demonstrated C-band GaN LNAs on 90 nm SiGe that achieved below-2 dB noise figures, proving the node’s viability for high-frequency analog gain stages. Over the long term, hybrid chiplets interconnected via 2.5D packaging could further decouple node selection from system integration, allowing designers to mix FinFET logic with high-voltage BCD analog on separate substrates while still benefiting the South Korean analog integrated circuits market.

By Business Model: IDM Leadership Faces Fabless Innovation Challenge

IDMs retained 65.05% revenue share, with Samsung and SK hynix leveraging vertically integrated supply chains that cover process R&D, volume manufacturing, and advanced test. Tight integration allowed direct optimization of analog device layout to manufacturing feeds, raising yield and reliability metrics vital for automotive contracts. The South Korean analog integrated circuits industry nevertheless experienced brisk fabless growth at 12.74% CAGR. SemiFive, a Samsung Foundry DSP partner, crossed USD 70 million sales on the strength of reusable analog IP blocks, including high-accuracy temperature sensors, spread-spectrum DC-DC controllers, and sub-GHz PLLs.

Rebellions-Sapeon’s merger produced the first domestic AI chip unicorn and signaled market appetite for domain-specific designs that ride outsourced silicon. Emerging chiplet methodologies allowed fabless firms to package analog I/O dies alongside compute tiles, easing tape-out risk and shortening validation cycles. The mutually beneficial IDM-fabless ecosystem, therefore, underpins the next wave of mixed-signal innovation within the South Korean analog integrated circuits market.

Geography Analysis

Gyeonggi Province hosted the bulk of wafer capacity thanks to the Yongin mega-cluster and established fabs in Pyeongtaek, Hwaseong, and Icheon. The KRW 471 billion (USD 350 million) public-private initiative will add 16 fabs and expand output to 7.7 million wafers each month by 2030. Utility upgrades, including 4 GW of additional substation capacity and a 300 km reclaimed-water pipeline, addressed chronic power and water constraints that previously capped expansion. Road and rail links to Incheon Port shortened export lead times for high-value analog IC shipments destined for automotive and consumer clients in Europe and North America.

The Chungcheong region emerged as a specialist hub for compound semiconductor epitaxy and MEMS sensor packaging, aided by grants for GaN and SiC pilot lines. Daejeon’s research triangle combined KAIST, ETRI, and multiple start-ups, enabling cross-fertilization between lab-scale innovations and commercial tape-outs. In the southeast, Ulsan and Busan focused on automotive and shipbuilding electronics, creating steady demand for power-train control ICs and maritime radar front ends. These complementary clusters strengthened supply-chain resilience and diffused economic benefits of the South Korea analog integrated circuits market beyond the primary Gyeonggi corridor.

Government fast-track permits simplified land acquisition and environmental reviews, accelerating construction timelines for new fabs. Local authorities offered tax holidays and workforce-training subsidies to entice ancillary suppliers in wet chemicals, specialty gases, and CMP slurries. Together, the geographic ecosystem reduced logistics overhead and boosted knowledge spillovers, reinforcing South Korea’s goal of surpassing Taiwan as the world’s second-largest chip producer by 2032.

Coverage of the analog integrated circuit market by Mordor Intelligence spans a wide geographic footprint, with detailed country-level intelligence for Taiwan and United States, each shaped by local operating conditions.

Competitive Landscape

Samsung Electronics cemented global leadership when it passed Intel in semiconductor revenue at the start of 2025, buoyed by strong 5G equipment sales and accelerating 2 nm foundry engagements. Strategic alliances with NAVER in hyperscale AI and with AMD in fifth-generation HBM created value-chain breadth that smaller rivals could not easily replicate. SK hynix advanced into analog adjacent spaces through joint HBM work with TSMC and the board-approved Yongin cluster that integrates memory and mixed-signal logic lines.

Fabless champions challenged the status quo. Rebellions–Sapeon’s combined valuation exceeded KRW 1.4 trillion (USD 950 million), directing fresh capital to edge inference ASICs that integrate low-power PLLs and high-speed ADCs.[4]KED Global, “Rebellions · Sapeon Korea merge to form AI chip unicorn,” kedglobal.com FuriosaAI’s refusal of Meta’s USD 800 million offer underlined confidence in domestic scale-up pathways and signaled that proprietary IP can anchor long-term independence. SemiFive’s acquisition of Analog Bits extended its IP catalog and positioned the firm as a one-stop shop for mixed-signal chiplets, facilitating turnkey designs for consumer and industrial customers.

Foreign entrants adapted through acquisition; Microchip’s purchase of VSI Co. Ltd. secured Automotive SerDes capability critical for ADAS and digital cockpits. Tower Semiconductor showcased next-generation BCD technology at APEC 2025, courting Korean automotive suppliers that require 40 V–100 V rated devices on 180 nm bulk lines. The interplay of globally scaled IDMs and agile Korean fabless houses has therefore defined a moderately concentrated yet rapidly evolving South Korea analog integrated circuits market.

South Korea Analog Integrated Circuits Industry Leaders

-

Analog Devices Inc.

-

Infineon Technologies AG

-

STMicroelectronics N.V.

-

Texas Instruments Inc.

-

NXP Semiconductors N.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Reports emerged that Samsung considered outsourcing memory photomask production, raising debate over domestic supply-chain robustness.

- March 2025: Tower Semiconductor presented advanced BCD platforms capable of handling automotive and AI power densities at APEC 2025.

- March 2025: Meta pursued FuriosaAI in a USD 800 million bid, which was rejected to preserve local ownership.

- January 2025: Microchip Technology acquired automotive connectivity pioneer VSI Co. Ltd. to expand ADAS and digital-cockpit networking portfolios.

South Korea Analog Integrated Circuits Market Report Scope

Analog integrated circuits (ICs) are essential components in many electronic devices. They are designed to process continuous signals representing real-world phenomena such as sound, light, and temperature.

For market estimation, the revenue generated from sales of various types of analog integrated circuits used in various industries, such as consumer, automotive, communication, computer, industrial, etc., is tracked. Market trends are evaluated by analyzing investments made in product innovation, diversification, and expansion. Enhancements in 5G, IoT, AI, energy efficiency, artificial intelligence, autonomous systems, electric vehicles, and biomedical devices are also crucial in determining the growth of the market studied.

The South Korean analog integrated circuits market is segmented by type (general-purpose IC [interface, power management, signal conversion, and amplifiers/comparators], application-specific IC (consumer [audio/video, digital still camera & camcorder, and other consumers], automotive [infotainment and other infotainment], communication [cell phone, infrastructure, wired communication, short range, and other wireless], computer [computer system & display, computer periphery, storage, and other computers], and industrial and others]). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| General-Purpose Analog IC | Interface | |

| Power Management | ||

| Signal Conversion | ||

| Amplifiers / Comparators | ||

| Application-Specific Analog IC | Consumer | Audio / Video |

| Digital Still Camera and Camcorder | ||

| Other Consumer | ||

| Automotive | Infotainment | |

| Powertrain and Safety | ||

| Communication | Cell Phone | |

| Infrastructure | ||

| Wired Communication | ||

| Short Range | ||

| Other Wireless | ||

| Computer | System and Display | |

| Peripherals | ||

| Storage | ||

| Other Computers | ||

| Industrial and Others | ||

| ≤ 200 mm |

| 200–300 mm |

| 300 mm |

| ≥ 450 mm |

| > 180 nm |

| 90 – 180 nm |

| 28 – 90 nm |

| < 28 nm (mixed-signal) |

| Integrated Device Manufacturer (IDM) |

| Design/ Fabless Vendor |

| By IC Type | General-Purpose Analog IC | Interface | |

| Power Management | |||

| Signal Conversion | |||

| Amplifiers / Comparators | |||

| Application-Specific Analog IC | Consumer | Audio / Video | |

| Digital Still Camera and Camcorder | |||

| Other Consumer | |||

| Automotive | Infotainment | ||

| Powertrain and Safety | |||

| Communication | Cell Phone | ||

| Infrastructure | |||

| Wired Communication | |||

| Short Range | |||

| Other Wireless | |||

| Computer | System and Display | ||

| Peripherals | |||

| Storage | |||

| Other Computers | |||

| Industrial and Others | |||

| By Wafer Size | ≤ 200 mm | ||

| 200–300 mm | |||

| 300 mm | |||

| ≥ 450 mm | |||

| By Technology Node | > 180 nm | ||

| 90 – 180 nm | |||

| 28 – 90 nm | |||

| < 28 nm (mixed-signal) | |||

| By Business Model | Integrated Device Manufacturer (IDM) | ||

| Design/ Fabless Vendor | |||

Key Questions Answered in the Report

What is the current value of the South Korean analog integrated circuits market?

The market stood at USD 6.37 billion in 2026 and is forecast to reach USD 9.31 billion by 2031.

Which segment leads the market in revenue and growth?

Application-specific analog ICs held 54.02% revenue in 2025 and are projected to grow at 12.32% CAGR through 2031.

How fast is 300 mm wafer adoption growing?

Shipments of 300 mm analog wafers are expected to increase at a 13.71% CAGR between 2026 and 2031.

What government incentives support domestic analog production?

The K-Semiconductor Vision offers tax credits up to 50% for R&D, cash subsidies of up to 80% of capital costs, and a KRW 1 trillion fund for fabless start-ups.

Why is talent shortage a restraint for analog design?

Specialized analog engineering skills are scarce; SMEs struggle to attract experienced designers, leading to project delays and slower capacity ramp-up.

Who are emerging competitors to established IDMs?

Fabless start-ups such as Rebellions, SemiFive, and FuriosaAI are attracting investment and partnering with Samsung Foundry to release specialized mixed-signal SoCs.

Page last updated on: