Aerospace and Defense Materials Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

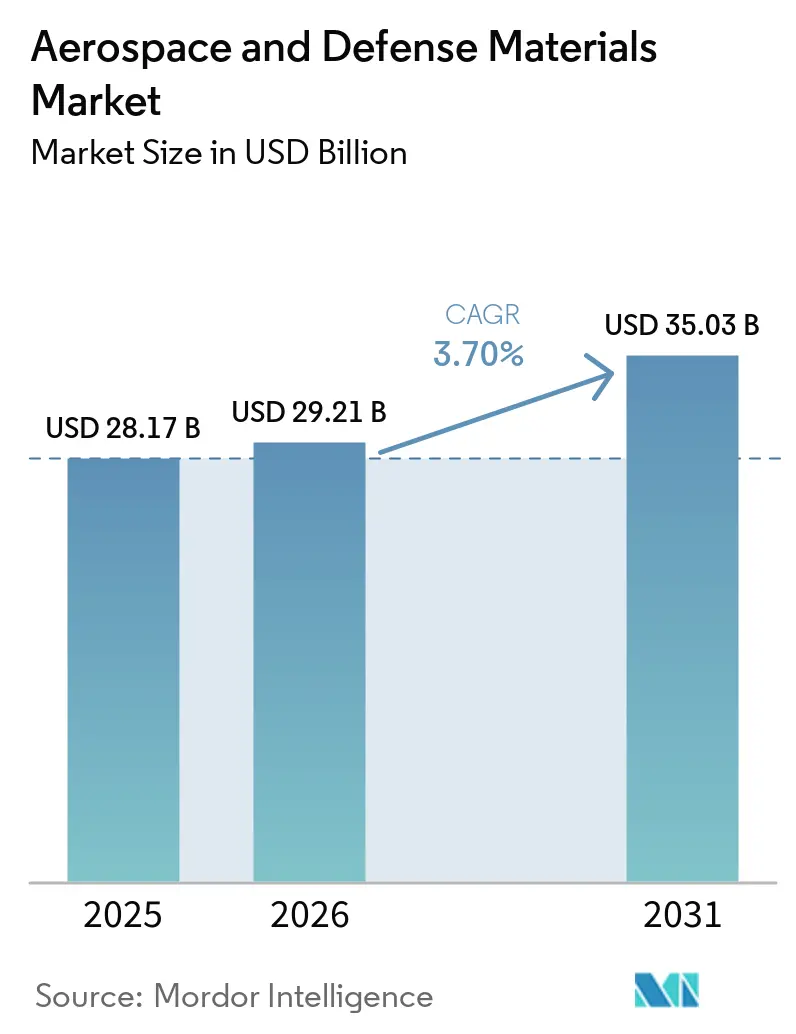

| Market Size (2026) | USD 29.21 Billion |

| Market Size (2031) | USD 35.03 Billion |

| Growth Rate (2026 - 2031) | 3.70% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aerospace and Defense Materials Market Analysis by Mordor Intelligence

Aerospace and Defense Materials market size in 2026 is estimated at USD 29.21 billion, growing from 2025 value of USD 28.17 billion with 2031 projections showing USD 35.03 billion, growing at 3.70% CAGR over 2026-2031. The measured expansion reflects the sector’s shift from post-pandemic recovery toward steady growth anchored in record defense modernization programs and a rejuvenated commercial aviation fleet pipeline. The Pentagon’s fiscal-2025 budget directs USD 3.5 Billion to the F-47 Next Generation Air Dominance program and USD 3.1 Billion to F-15EX production, amplifying demand for heat-resistant alloys, aluminum-lithium plate, and ceramic matrix composites. Parallel momentum on the civil side is driven by Boeing’s long-term projection for nearly 44,000 new aircraft deliveries through 2043, with single-aisle models accounting for 76% of the total. Regulators are compounding material innovation pressure by mandating 10% fuel-efficiency gains by 2031 and 35% gains by 2050 relative to 2000-era aircraft. Composite adoption is further encouraged by the counterfeit titanium crisis, which exposed a fragile supply chain where the United States imports more than 90% of the titanium sponge used in defense applications.

Key Report Takeaways

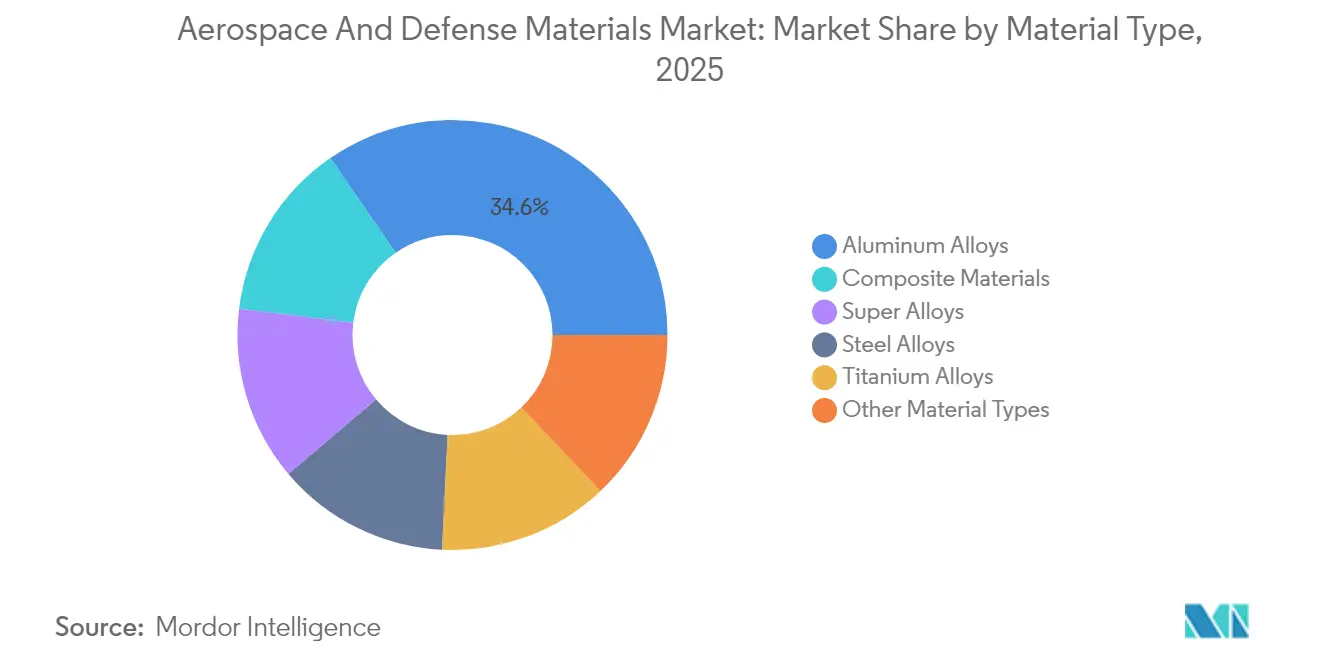

- By material type, aluminum alloys led with 34.62% of the Aerospace and Defense Materials market share in 2025, whereas composite materials are forecast to rise at a 4.58% CAGR through 2031.

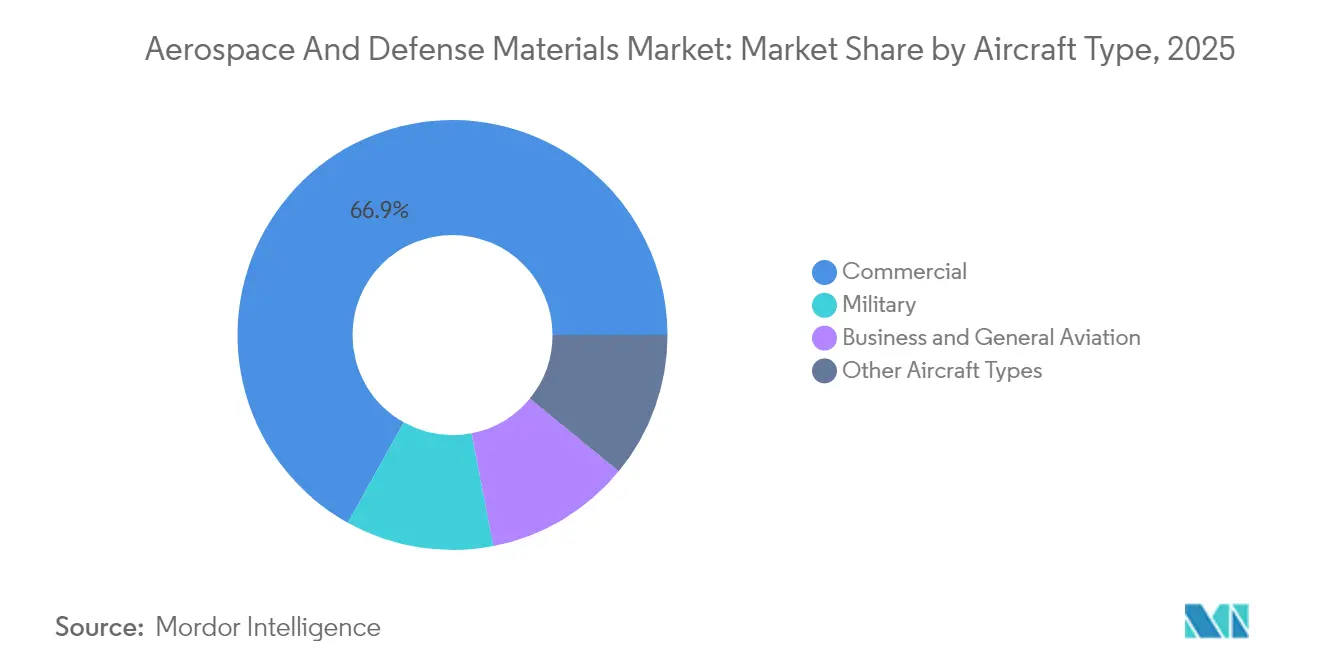

- By aircraft type, commercial aviation accounted for 66.90% of the Aerospace and Defense Materials market size in 2025, while military aircraft are expected to post the fastest 4.63% CAGR to 2031.

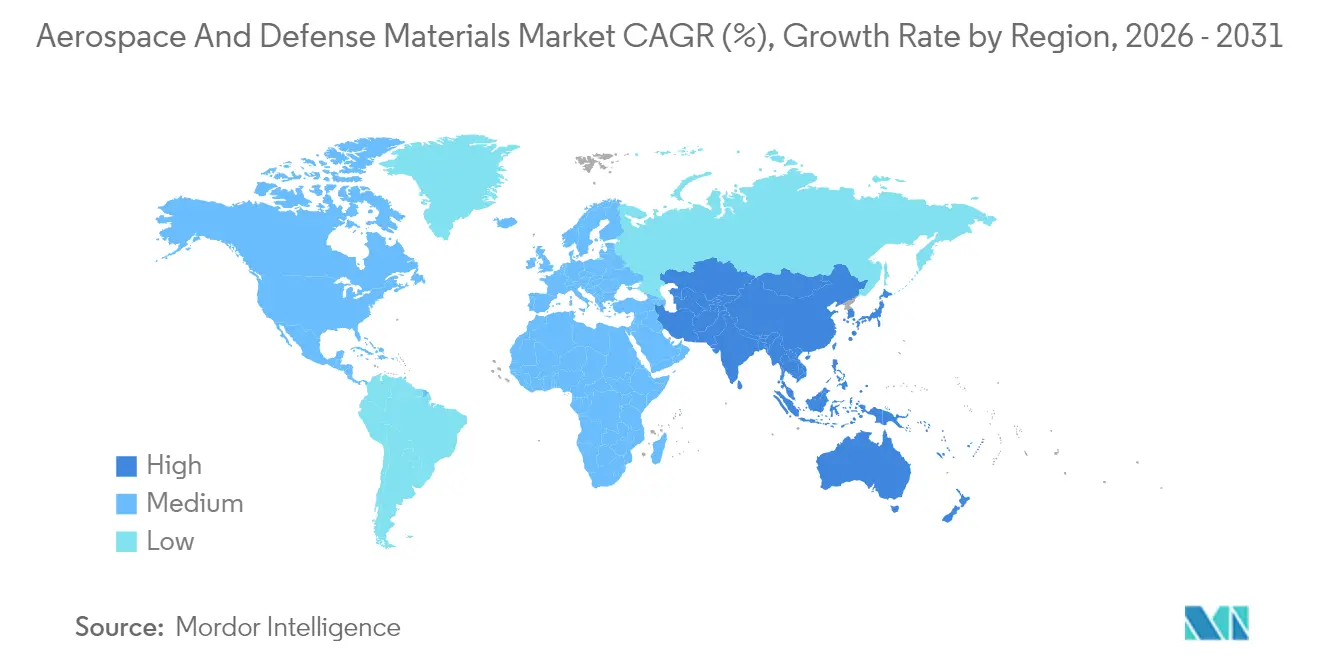

- By geography, North America commanded 35.84% of 2025 revenue, yet Asia-Pacific is projected to expand at the quickest 4.34% CAGR during the outlook window.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Aerospace and Defense Materials Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging Production Backlog for Single-Aisle Commercial Aircraft | +0.8% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Rising Defense Budgets for Next-gen Fighter and Transport Programs | +0.7% | North America, Europe, Asia-Pacific defense corridors | Long term (≥ 4 years) |

| Weight-reduction Mandates Accelerating Composite Adoption | +0.6% | Global, led by ICAO member states | Medium term (2-4 years) |

| Hypersonic R&D Ramping Demand for Refractory Alloys and Superalloys | +0.4% | United States, China, Russia primary; spillover to allied nations | Long term (≥ 4 years) |

| Megaconstellations Scaling Demand for Space-grade Polymers | +0.3% | Global, with manufacturing concentrated in North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surging Production Backlog for Single-Aisle Commercial Aircraft

Order books stand at nearly 15,700 jets, with Airbus alone holding about 8,700 A320neo-family commitments. Long wait times push airframers to secure multi-year supply contracts covering aluminum-lithium plate and advanced carbon fiber laminates, supporting growth in the aerospace and defense materials market and moving procurement away from just-in-time models toward strategic stockpiles. Each single-aisle frame now integrates greater volumes of high-strength 7000-series aluminum extrusions and resin-infused wing skins that reduce up to 10% structural weight together. Production interruptions, such as Boeing’s trim to 26 units per month on the 737 line amid supplier capacity gaps, underline how raw-material availability regulates final-assembly cadence.

Rising Defense Budgets for Next-Generation Fighter and Transport Programs

Global defense outlays surpassed USD 2.4 Trillion in 2024, propelling procurement of sixth-generation fighters and stealth transports that rely on ceramic matrix composites, radar-absorbing titanium aluminides, and refractory alloys capable of withstanding skin temperatures above 1,000°C. The Pentagon allocates USD 6.9 Billion in 2025 to hypersonic materials science and prototype missiles, while Spain’s EUR 2 Billion order for 25 additional Eurofighters highlights Europe’s parallel commitment to material-intensive platforms [1]Airbus Defence & Space, “Eurofighter Contract Expansion,” airbus.com. China’s breakthrough in superalloy disc processing, achieving cooling rates 3.75 times faster than legacy methods, underscores the unfolding global race for metallurgical leadership.

Weight-Reduction Mandates Accelerating Composite Adoption

The International Civil Aviation Organization (ICAO) performance standards require commercial aircraft certified after 2024 to demonstrate lower fuel burn on a specific-air-range basis, intensifying the adoption of carbon fibers, thermoplastic tapes, and high-temperature oxide-oxide ceramics across the aerospace and defense materials market. The rule dovetails with ReFuelEU Aviation, which phases in sustainable aviation fuel quotas from 2% in 2025 to 70% by 2050, rewarding airframers that shed mass and cut lifecycle emissions. Novel ceramic matrix composites able to resist 2,800°C allow hotter core gas turbines that raise thermal efficiency and reduce metallic shielding, while carbon-nanofiber reinforcements pioneered at Oak Ridge National Laboratory boost tensile strength by 50% and double fracture toughness for load-bearing structures.

Hypersonic R&D Ramping Demand for Refractory Alloys and Superalloys

Programs such as the Hypersonic Air-breathing Weapon Concept require ultra-high-temperature ceramics and niobium-hafnium carbides that remain stable at velocities exceeding Mach 5. Laboratory work at Southwest Research Institute validates material survivability at 2,200°C boundary-layer conditions, and POSTECH’s high-entropy nickel alloy maintains ductility from (-196)°C to 600°C, a key attribute for thermal-shock resistance during boost-glide phases. GE Aerospace’s rotating-detonation demonstrator drives interest in cobalt-rich superalloys that withstand cyclic combustion waves.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Prices of Critical Metals | -0.4% | Global, with acute impact in import-dependent regions | Short term (≤ 2 years) |

| Lengthy Qualification Cycles and Capital Intensity of New Materials | -0.3% | Global, most severe in highly regulated markets | Long term (≥ 4 years) |

| Casting/Forging Supply-chain Bottlenecks and Labor Shortages | -0.5% | North America and Europe manufacturing hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Prices of Critical Metals

World Bank data show a 9% rise in the metals and minerals price index through April 2024, and the Producer Price Index for titanium reached 190.106 in May 2024 [2]World Bank Group, “Commodity Markets Outlook April 2024,” worldbank.org. Tariffs of 25% on incoming steel and aluminum pushed imported steel prices up 22.7%, prompting original equipment manufacturers (OEMs) to diversify suppliers and negotiate hedging clauses. Russia’s exit from the titanium sponge market redirected buyers to Kazakhstan and Saudi Arabia, tightening spot availability. The counterfeit titanium incident that hit Boeing and Airbus operations illustrated how cost inflation can erode compliance controls and allow fraudulent alloys into critical parts.

Lengthy Qualification Cycles and Capital Intensity of New Materials

Complex standards such as AS9100 and RTCA/DO-160 lengthen time-to-market for novel resins and alloys, often taking three to five years to pass flight-test gates. The International Aerospace Quality Group has shifted toward risk-based surveillance, yet still requires extensive process capability demonstrations that raise upfront costs. GKN Aerospace supplier manuals mandate counterfeit mitigation plans and continuous disclosure of process tweaks, illustrating the governance burden on small and medium enterprises. Stratasys took multiple years of mechanical, flammability, and outgassing trials before Boeing cleared its Antero family of polyether ketone ketone (PEKK)-based filaments for cabin and propulsion parts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Aluminum Dominance Faces a Composite Challenge

Aluminum alloys retained 34.62% of 2025 revenue, driven by well-proven performance, wide supplier bases, and lower kilogram cost than exotic metals. Constellium’s multi-year contract to ship plate from Ravenswood and its Airware aluminum-lithium range shows how incumbents refresh portfolios with higher modulus and corrosion resistance. Steel alloys remain indispensable for landing gear, with Carpenter Technology’s modified 4340 and AerMet 100 scoring high fracture-toughness values for arrestor-hook assemblies. Titanium alloys occupy the hot-section, exhaust, and critical fastener niche, though price swings force primes to trial titanium-metal-matrix composites as lower-density substitutes.

Composite materials headline the growth story at a forecast 4.58% CAGR through 2031. Ceramic matrix composites at 2,800°C enable hotter turbine cores without heavy metallic cooling parts, directly meeting ICAO fuel-burn rules. Carbon-fiber reinforced polyetheretherketone (PEEK) and PEKK thermoplastics cut assembly time because they can be welded instead of riveted, a benefit accentuated in high-rate single-aisle lines. Superalloys form the fastest-rising traditional metal subset as hypersonic research and development (R&D) pulls in nickel-cobalt-rhenium systems offering high strength above 1,150°C. Researchers are also scaling high-entropy alloys such as POSTECH’s Hyperadaptor, which demonstrates a stable gamma-prime structure across a 796°C temperature swing. Other material types, ranging from radiation-hardened polymers to graphene-enhanced paints, are expanding on the back of a commercial space market that could hit USD 1 Trillion inside ten years.

By Aircraft Type: Commercial Aviation Leads as Military Modernization Accelerates

Commercial applications generated 66.90% of 2025 sales, reflecting the massive narrow-body fleet renewal that underpins the aerospace and defense materials market. Airbus delivered 766 jets in 2024 and posted EUR 69.2 Billion revenue, setting a voracious appetite for aluminum plate, carbon-fiber wing covers, and glass fiber interior panels. Business and general aviation continues to absorb innovations filtering down from large commercial programs, notably autoclave-cured thermoset fuselages and titanium 3D-printed brackets.

Military aircraft log the fastest 4.63% CAGR because advanced materials unlock stealth shaping, thermal protection, and directed-energy payloads. The USD 3.5 Billion F-47 NGAD allocation underscores the scale of planned consumables such as radar-absorbing carbon nanotube composites and boron carbides suited for hypersonic edge panels. The convergence of commercial and defense needs is evident where dual-use alloys qualified for civil engines migrate into F-15EX afterburner hardware, creating volume leverage that encourages suppliers to approve higher-throughput melt routes.

Unmanned aircraft and urban air mobility projects open new demand pockets for low-cost thermoplastic ribs, additive-manufactured wire harness brackets, and lithium-sulfur battery casings. Space launch vehicles contribute a rising share through carbon-fiber cryogenic tanks and SiC nozzle skirts, with SpaceX scaling Starship production that relies on stainless steel clad in thermal protection tiles.

Geography Analysis

North America controlled 35.84% of 2025 revenue due to the United States' defense budget, expansive civil fleet, and vertically integrated metals ecosystem. Alcoa’s USD 548 Million Q1-2025 net income and its USD 2.2 Billion Alumina Limited acquisition highlight upstream consolidation that secures bauxite and alumina supply. Canada and Mexico add cost-efficient machining, with Mexico nurturing more than 300 qualified suppliers and vocational programs that alleviate the region’s aging-workforce gap. Challenges stem from counterfeit titanium exposure and tight forging capacity, yet sustained hypersonic funding at USD 6.9 Billion keeps research sites busy.

Asia-Pacific is the fastest-growing region with a 4.34% CAGR through 2031, supported by China’s C919 narrow-body entry and investments in superalloy processing lines that triple cooling rates during turbine-disc quench stages. Japan boosted aerospace-grade titanium sponge output to 55,000 tons in 2024, supplementing 19,000 tons from Kazakhstan and 15,000 tons from Saudi Arabia. India, South Korea, and emerging ASEAN hubs draw component work as primes diversify away from concentrated sources. Regional airlines expanding narrow-body fleets for domestic routes generate sticky demand for plate, extrusion, and interior panels.

Europe retains a balanced profile thanks to Airbus’s civil backlog and rising collective defense budgets. Delivery of 766 aircraft in 2024 coupled with EUR 16.7 Billion Defense and Space division orders indicates durable materials pull. The European Defence Fund granted over EUR 1 Billion to 54 technology programs, including hypersonic vehicle research that consumes ultra-high-temperature ceramics. Regulatory leadership through ReFuelEU Aviation stimulates rapid composite adoption as carriers seek lower lifecycle emissions. Casting and forging capacity tightens as program mix shifts toward high-temperature metals, motivating joint ventures to open new hot-isostatic-press assets in France and Germany.

Competitive Landscape

The Aerospace and Defense Materials Market is moderately consolidated, with incumbent suppliers integrating upstream and downstream assets while niche entrants focus on disruptive manufacturing. The major players in the industry include Toray Industries Inc., Hexcel Corporation, Carpenter Co., and Alcoa Corporation. Alcoa’s Alumina Limited purchase gives it captive feedstock and reduces external bauxite exposure. Hexcel posted USD 474 Million sales in Q4 2024, up 12% in commercial aerospace, confirming sustained prepreg demand. Constellium’s Airware series attracts next-generation fuselage work owing to weight savings over legacy 2000-series alloys. Emerging opportunities lie in hypersonic materials and space-grade polymers where qualification barriers remain high. Sustainability is gaining traction too, with resin recyclability and zero-emission smelting methods becoming competitive differentiators.

Aerospace and Defense Materials Industry Leaders

Alcoa Corporation

Carpenter Co.

Hexcel Corporation

Toray Industries Inc.

Solvay

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: India's Defense Ministry inaugurated Aerolloy Technologies' titanium and superalloy materials plant in Lucknow, Uttar Pradesh, with a 6,000-tonne annual capacity, making it the world's largest single-site titanium remelting facility for aerospace-grade materials.

- September 2024: Toray Advanced Composites launched Toray Cetex TC1130 PESU thermoplastic composite, addressing the demand for lightweight, sustainable materials in aircraft interiors, benefiting the aerospace and defense sector.

Global Aerospace and Defense Materials Market Report Scope

The aerospace and defense materials market is segmented by material type, aircraft type, and geography. By Material Type, the market is segmented into Aluminum Alloys, Steel Alloys, Titanium Alloys, Super Alloys, Composite Materials, and Other Material Types. By Aircraft Type, the market is segmented into Commercial, Military, Business and General Aviation, and Other Aircraft Types. The report also covers the market size and forecasts for the Aerospace and Defence Materials Market in 15 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of revenue (USD Million).

| Aluminum Alloys |

| Steel Alloys |

| Titanium Alloys |

| Super Alloys |

| Composite Materials |

| Other Material Types |

| Commercial |

| Military |

| Business and General Aviation |

| Other Aircraft Types |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| Material Type | Aluminum Alloys | |

| Steel Alloys | ||

| Titanium Alloys | ||

| Super Alloys | ||

| Composite Materials | ||

| Other Material Types | ||

| Aircraft Type | Commercial | |

| Military | ||

| Business and General Aviation | ||

| Other Aircraft Types | ||

| Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the Aerospace and Defense Materials Market?

The Aerospace and Defense Materials market size reached USD 29.21 Billion in 2026 and is projected to rise to USD 35.03 Billion by 2031.

Which material segment is expanding fastest?

Composite materials are expected to post the fastest 4.58% CAGR through 2031 due to stringent fuel-efficiency standards and weight-reduction mandates.

Which region is growing the quickest?

Asia-Pacific leads with a forecast 4.34% CAGR, supported by China’s C919 program and regional defense spending.

What are the chief restraints on future growth?

Volatile prices of critical metals, lengthy qualification cycles, and limited forging capacity combined with skilled-labor shortages are the main headwinds.

How are sustainability goals influencing material choices?

Regulatory targets for fuel burn and sustainable aviation fuel are accelerating the transition to lightweight composites and recyclable thermoplastics, reshaping supply priorities.

Page last updated on: