Industrial Hemp Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

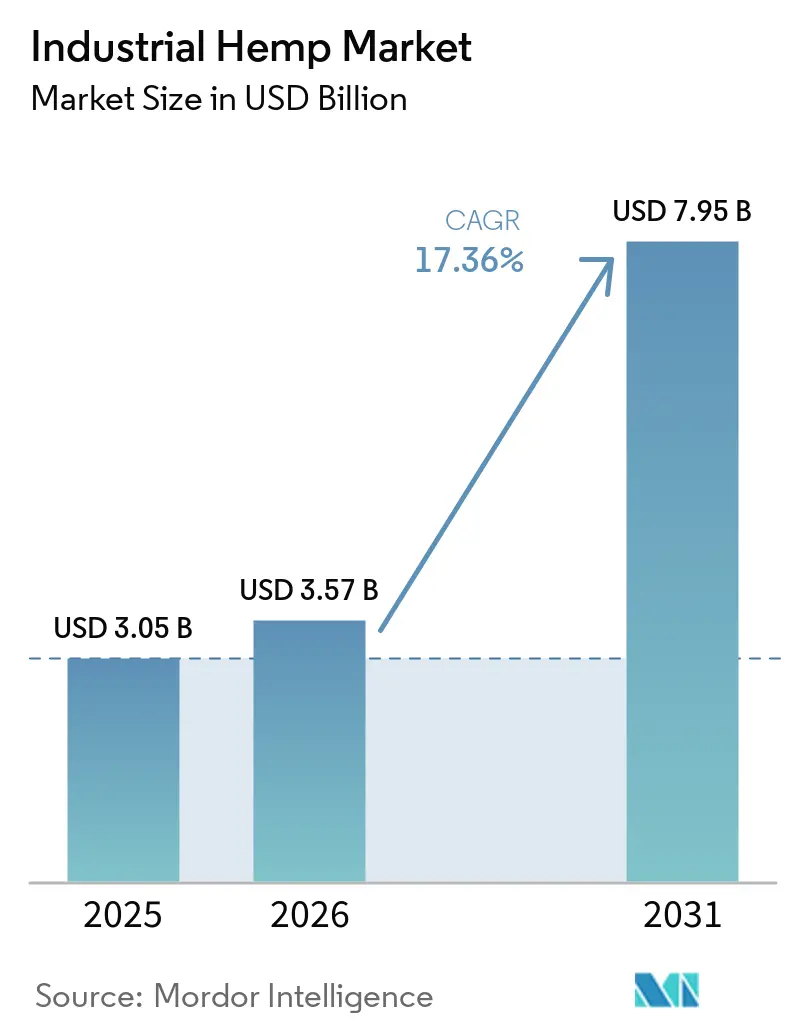

| Market Size (2026) | USD 3.57 Billion |

| Market Size (2031) | USD 7.95 Billion |

| Growth Rate (2026 - 2031) | 17.36% CAGR |

| Fastest Growing Market | North America |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Industrial Hemp Market Analysis by Mordor Intelligence

The Industrial Hemp Market size is projected to be USD 3.05 billion in 2025, USD 3.57 billion in 2026, and reach USD 7.95 billion by 2031, growing at a CAGR of 17.36% from 2026 to 2031. This growth rests on regulatory tailwinds that preserve the crop’s legal status while easing consumer access to hemp-derived food, wellness, and building materials. In North America, net-zero construction codes are steering builders toward hempcrete, and pharmacies are mainstreaming cannabidiol topicals. Europe’s provisional daily intake limit for cannabidiol signals a path to Novel Food approvals, even as testing rules remain fragmented. Mid-tier processors able to document batch consistency are attracting capital, yet small farms face price swings and land-use competition that limit acreage expansion.

Key Report Takeaways

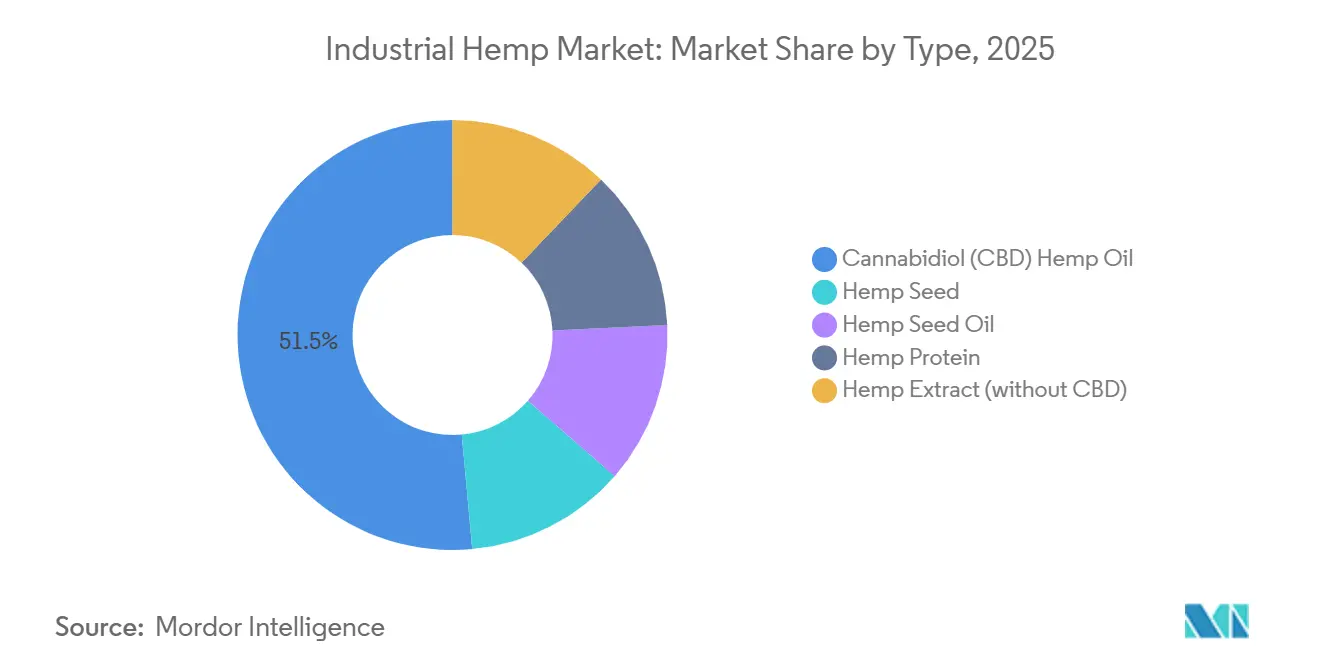

- By type, cannabidiol (CBD) hemp oil held 51.47% of the hemp market share in 2025 and is projected to compound at a 18.36% CAGR to 2031, reflecting sustained therapeutic adoption in the industrial hemp industry.

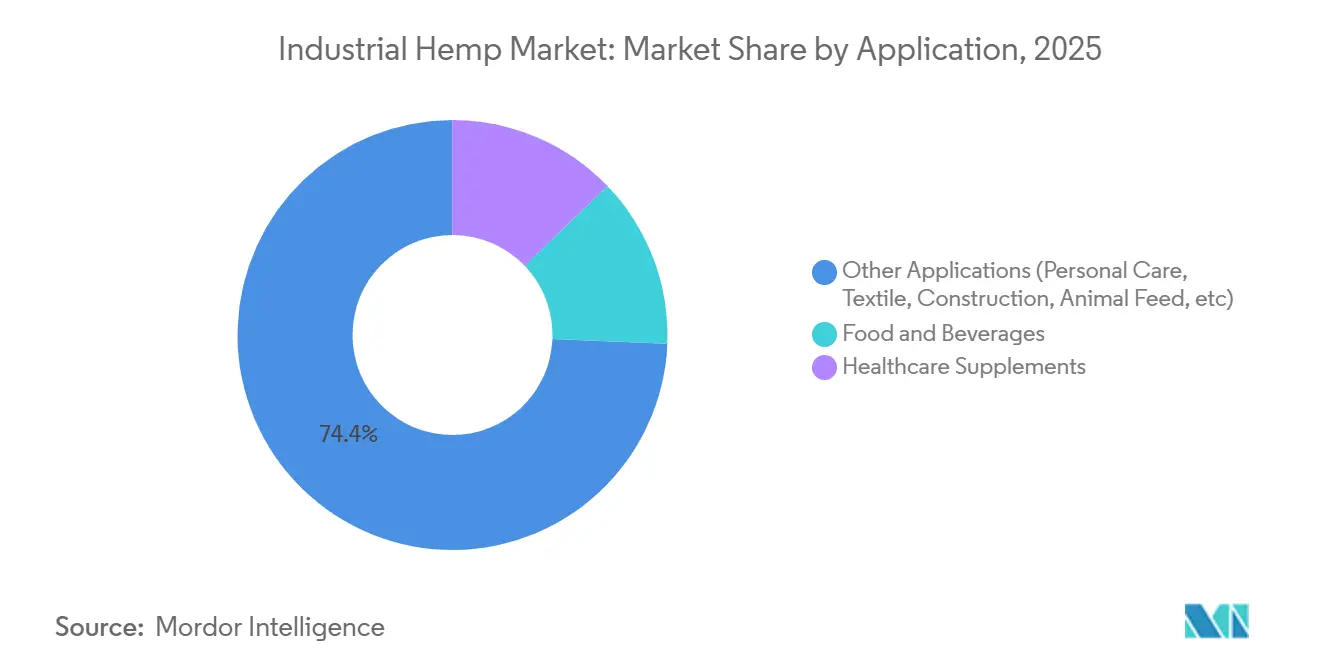

- By application, the other applications bucket, including personal care, textiles, construction, and animal feed, accounted for 74.35% of the hemp market size in 2025 and is expected to expand at an 18.51% CAGR.

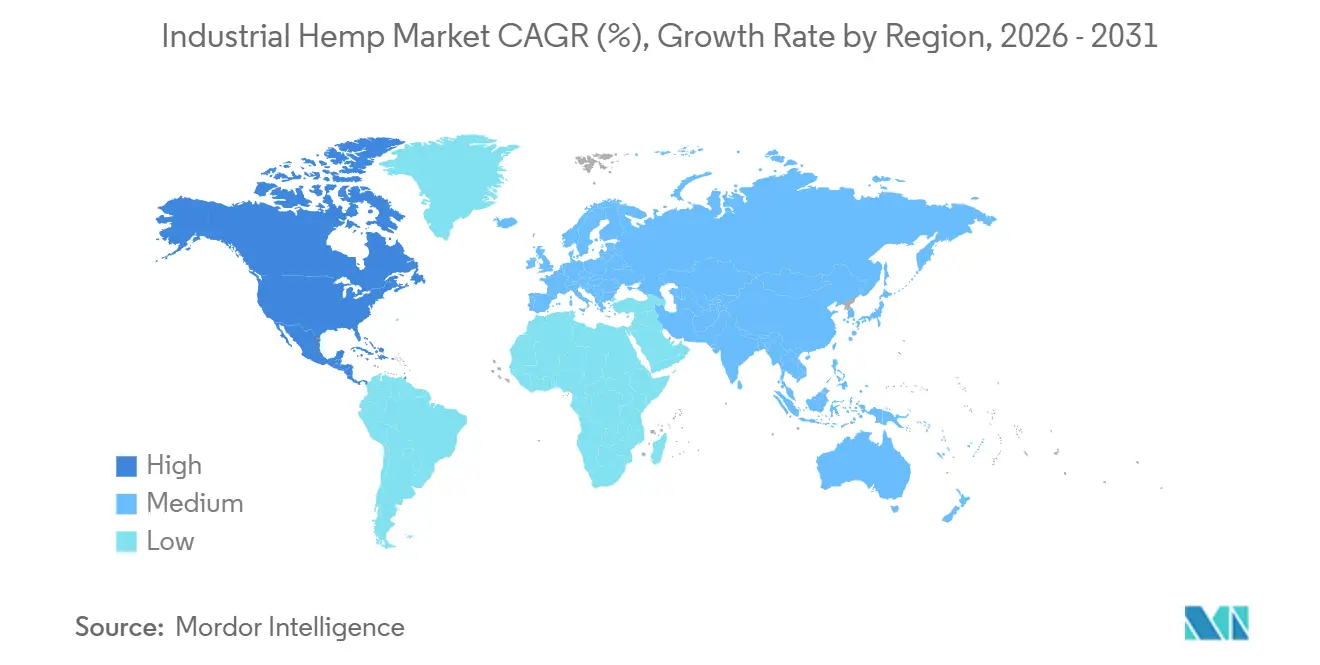

- By geography, North America led the hemp market with a 55.99% revenue share in 2025 in the industrial hemp industry, also registering the fastest regional CAGR of 18.09% from 2025 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Industrial Hemp Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legalization in Major Economies | +3.8% | North America, EU, Japan, Thailand | Medium term (2-4 years) |

| Rising Demand for Plant-Based Food & Beverages | +2.9% | North America, EU, Asia-Pacific cities | Long term (≥4 years) |

| CBD Adoption in Wellness & OTC Channels | +4.2% | North America, Western Europe, Australia, Japan, South Korea | Short term (≤2 years) |

| Hempcrete Demand in Net-Zero Construction | +2.6% | France, UK, Netherlands, United States, Canada | Long term (≥4 years) |

| Automation in Fiber Decortication & Processing | +1.7% | China, France, Netherlands, Canada | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Legalization in Major Economies

Legislative continuity in the United States kept hemp legal under a December 2024 continuing resolution, although a pending bill would tighten interstate testing rules[1]. Japan’s December 2024 Cannabis Control Act amendment opened a cannabidiol pathway for 120 million consumers. Thailand’s 2025 policy reversal, which imposed prescriptions on products with more than 0.2% cannabidiol, illustrates regulatory whiplash that can erase retail shelves overnight in the industrial hemp industry. Europe’s February 2026 safe-intake limit of 2 mg per day clarifies dosage ceilings, yet keeps Novel Food reviews lengthy. Brands nimble enough to manage documentation across borders can arbitrage supply gaps, but uneven rules still deter some institutional investors.

Rising Demand for Plant-Based Food and Beverages

Hemp protein isolates now match pea and soy at 90% protein content while providing all nine essential amino acids. Manitoba Harvest expanded to 16,000 North American stores by 2025 with a hemp-milk line co-branded by a leading coffee chain. Nutiva’s cold-pressed hemp-seed oil, launched in 2024, sells at a 40% premium to canola because it preserves chlorophyll and tocopherols, emphasizing premiumization within the industrial hemp industry. Consumer confusion still lingers; 38% of US shoppers wrongly link hemp protein to intoxication, but transparent labeling that shows tetrahydrocannabinol below 0.01% doubles conversion rates. Continued nutrition education, therefore, underpins future shelf gains.

CBD Adoption in Wellness and OTC Channels

Major US pharmacy chains stocked cannabidiol products in more than 8,000 outlets by end-2024, a tenfold rise in five years in the industrial hemp industry. Charlotte’s Web placed gummies in vitamin aisles to sidestep cannabis stigma. The UK’s Food Standards Agency granted conditional Novel Food clearances, letting approved products stay on shelves during final reviews. Japan starts pharmacy sales in 2025 for cannabidiol supplements traced with QR-coded batch certificates. A 2025 US health-plan pilot that reimbursed cannabidiol cut opioid use by 18%, hinting that payer coverage could shift cannabidiol from the wellness aisle to the formulary.

Hempcrete Demand in Net-Zero Construction

The 2024 International Residential Code added Appendix S for hemp-lime walls, giving builders a prescriptive route and shaving six-week permit cycles in the industrial hemp industry.[2]. A UK three-story residence used 150 tonnes of hempcrete and locked away 30 tonnes of carbon during construction. Walmart’s 2024 North Carolina prototype reinforced retail interest in bio-based blocks. France’s RE2020 law forces whole-life carbon counts from 2025, nudging developers toward materials that carry embedded sequestration. Slow curing remains the hurdle, as hempcrete walls need 6-8 weeks to harden versus 28 days for concrete.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory Uncertainty on THC/CBD Limits | -2.4% | Asia-Pacific, EU, United States | Short term (≤2 years) |

| Fragmented Supply Chain & Quality Variability | -1.8% | North America, EU, Asia-Pacific | Medium term (2-4 years) |

| Land-Use Competition with Specialty Crops | -1.1% | United States, France, Romania | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Regulatory Uncertainty on THC/CBD Limits

The US Food and Drug Administration still has not finalized cannabidiol dietary-supplement guidance, leaving brands unable to make structure-function claims in the industrial hemp industry. Thailand’s June 2025 prescription rule triggered USD 150 million in write-offs as retailers scrambled to comply. Europe’s 2 mg daily limit excludes sensitive groups, shrinking the addressable base. South Korea bans cannabidiol entirely, forcing global brands to run separate product lines. Testing gaps persist; a 2024 US study found 23% of cannabidiol products exceeded the 0.3% tetrahydrocannabinol cap, exposing firms to recalls.

Fragmented Supply Chain and Quality Variability

Lack of unified traceability lets pesticide-treated biomass slip into food-grade streams, threatening ISO 22000 compliance. Ecofibre rejected 18% of third-party seed lots in 2025 due to mycotoxins, raising costs by 12%. Weather volatility cut Colorado cannabidiol yields 22% for Charlotte’s Web in 2024 in the industrial hemp industry. A blockchain pilot by the European Industrial Hemp Association saw under 10% member uptake because the USD 50,000 fee is steep for small cooperatives. An AOAC round-robin test in 2025 showed 15% lab-to-lab variation in cannabidiol assays, undermining label accuracy.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Cannabidiol Hemp Oil Maintains Volume Leadership

Cannabidiol Hemp Oil delivered 51.47% of the Hemp market size for type in 2025 and is set for an 18.36% CAGR through 2031 in the industrial hemp industry. Charlotte’s Web introduced a water-soluble powder in 2024 with four-fold bioavailability, letting formulators cut serving sizes without losing effect. Hemp Seed remained the volume anchor; Manitoba Harvest’s dehulled seeds reached 16,000 stores and supplied 10 g of protein per 30 g serving. Hemp Seed Oil faces commodity-oil pricing pressure even though it carries a 1:3 omega-3 to omega-6 ratio superior to canola. Hemp Protein isolates at 90% purity gained shelf space in sports nutrition, while full-spectrum hemp extract, though under 5% of revenue, commands 60% price premiums because of terpene richness.

Despite fragmented testing standards, the European safe-intake ceiling encourages brands to sell higher-concentration isolates that keep daily doses within 2 mg. This trend lifts average selling prices and reinforces vertical integration among processors that can certify input purity. Smallholders relying on spot-market biomass risk exclusion from premium isolate supply chains unless they adopt Good Agricultural Practices and provide pesticide histories.

By Application: Industrial Uses Eclipse Food and Beverage

Other Applications accounted for 74.35% of the Hemp market size in 2025 and will expand at an 18.51% CAGR to 2031 in the industrial hemp industry. Hempcrete builders accept 20% higher material costs because carbon-negative walls help them meet net-zero codes. Personal-care formulators favor hemp-seed oil for its linoleic acid; a 2024 clinical trial showed an 18% drop in water loss after four weeks of lotion use. Textile mills in Heilongjiang processed 15,000 tonnes of bast fiber in 2024, feeding European fashion houses that want cotton alternatives. Animal feed makers also add hemp hurd to boost fiber content, diversifying revenue streams.

Food and Beverages, at under 20% share, enjoy cleaner rules as hemp seeds are Generally Recognized as Safe in the United States and hold Novel Food status in Europe in the industrial hemp industry. Healthcare Supplements, centered on cannabidiol tinctures, face retail price compression but keep growing because pharmacies add private-label stock. The pivot to industrial uses means future Hemp market growth will lean on construction sites and textile looms rather than grocery aisles, rewarding processors with low-carbon life-cycle data.

Geography Analysis

North America generated 55.99% of the Industrial Hemp market revenue in 2025 and should post an 18.09% CAGR through 2031. US planted area slipped from 146,000 acres in 2019 to 54,000 acres in 2024, yet cannabidiol acreage steadied at 22,000 because processors pay premiums for high-resin varieties. Canada sowed 84,000 acres, splitting 60% grain and 40% fiber, and sells seeds to European bakers. Mexico’s slow licensing kept issued permits below 50 by 2025, delaying field-scale output.

In Europe, France led with 18,000 hectares cultivated, mainly for fiber that feeds construction firms chasing RE2020 carbon targets in the industrial hemp industry. Germany imported 4,200 tonnes of Canadian seed for bakery mixes, while the UK’s conditional Novel Food list pulled multinational nutraceutical investment. Nordic rules allow hemp fiber but cap cannabidiol at zero, fragmenting product lines and limiting regional sales.

Asia-Pacific is the fastest-growing region on a smaller base. China farmed more than 30,000 hectares in three northern provinces, yet still forbids cannabidiol extraction. India’s Uttarakhand issued 1,200 hemp licenses by 2025, but local processing remains scarce in the industrial hemp industry. Japan’s 2025 pharmacy launch creates a vast wellness channel, whereas Thailand’s June 2025 rule change froze 3,000 cannabidiol stores. South America and the Middle East & Africa together hold a low market share, and Colombia eyes hemp as a coca alternative, and South Africa allows only home cultivation.

Competitive Landscape

Competitive Landscape

The Industrial Hemp market is moderately fragmented. Canopy Growth’s 12% hemp-revenue slide in fiscal 2025 steered it toward THC-dominant products in legalized US states. Charlotte’s Web pursues seed-to-shelf genetics and direct e-commerce, while Ecofibre scales ISO 22000-certified proteins from 10,000 hectares in Tasmania. Private-equity funds scout mid-tier processors holding stranded extraction lines yet lacking working capital for multiyear Novel Food dossiers. Supply-chain transparency and regulatory compliance, rather than celebrity branding, now decide contract wins.

Industrial Hemp Industry Leaders

HempFlax Group BV

Charlotte's Web, Inc

Manitoba Harvest Hemp Foods.

Ecofibre

Canopy Growth Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Chief Minister of Himachal Pradesh, India, launched the 'Green to Gold' initiative, aiming to reshape the state's economic landscape. This initiative seeks to pivot the state from a history of illicit trade to a forefront position in the global bio-economy by legalizing and regulating the cultivation of industrial hemp.

- November 2025: Congress of the United States, through the Continuing Resolution and Appropriations Package (H.R. 5371) (CR), introduced major changes to the regulation of hemp-derived products, including those related to cannabidiol (CBD). These alterations mark the most substantial shift in hemp regulation since the 2018 Farm Bill, particularly highlighted in Section 781 of the CR.

Global Industrial Hemp Market Report Scope

Industrial hemp is a non-drug variety of Cannabis sativa with very low delta-9-tetrahydrocannabinol (THC) content. It is an agricultural commodity that comes from the same plant species but from different cultivars bred for different uses. There are genetically distinct forms of Cannabis that are differentiated by their usage, chemical makeup, and practices of cultivation. Industrial hemp has been a source of fiber and oilseed for centuries and is extensively used to produce a variety of industrial and consumer products across the world. It is a dual-purpose crop and can be grown as a seed and fiber.

The industrial hemp market is segmented on the basis of type, application, and geography. By type, the market is segmented into hemp seed, hemp seed oil, cannabidiol (CBD) hemp oil, hemp protein, and hemp extract (without CBD). By application, the market is segmented into food and beverages, healthcare supplements, and other applications (personal care, textile, construction, animal feed, and more). The report also covers the market size and forecasts for the industrial hemp market in 27 countries across major regions. For each segment, the market sizes and forecasts are provided in terms of revenue (USD).

| Hemp Seed |

| Hemp Seed Oil |

| Cannabidiol (CBD) Hemp Oil |

| Hemp Protein |

| Hemp Extract (without CBD) |

| Food & Beverages |

| Healthcare Supplements |

| Other Applications (Personal Care, Textile, Construction, Animal Feed, etc) |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Thailand | |

| Indonesia | |

| Vietnam | |

| Malaysia | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| NORDIC Countries | |

| Turkey | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Egypt | |

| Nigeria | |

| South Africa | |

| Rest of Middle East and Africa |

| By Type | Hemp Seed | |

| Hemp Seed Oil | ||

| Cannabidiol (CBD) Hemp Oil | ||

| Hemp Protein | ||

| Hemp Extract (without CBD) | ||

| By Application | Food & Beverages | |

| Healthcare Supplements | ||

| Other Applications (Personal Care, Textile, Construction, Animal Feed, etc) | ||

| Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Thailand | ||

| Indonesia | ||

| Vietnam | ||

| Malaysia | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| NORDIC Countries | ||

| Turkey | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| Egypt | ||

| Nigeria | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How fast is the Industrial hemp industry projected to grow between 2026 and 2031?

The Hemp market is forecast to expand at a 17.36% CAGR from 2026 to 2031, and reach USD 7.95 Billion from 2031.

Which region currently leads global industrial hemp industry revenue?

North America held 55.99% of worldwide revenue in 2025 and remains the largest regional contributor.

What segment in the industrial hemp industry holds the largest market share by application?

Industrial uses such as personal care, textiles, construction, and animal feed captured 74.35% share in 2025.

Why is Cannabidiol Hemp Oil important for future growth?

Cannabidiol Hemp Oil combines wellness demand with premium pricing and is expected to grow at 18.36% through 2031.

What is the main regulatory hurdle for cannabidiol products in the European Union?

Brands must navigate an 18-month Novel Food review cycle and comply with a provisional adult intake limit of 2 mg per day.

Page last updated on: