Anti-Corrosion Coatings Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 25.62 Billion |

| Market Size (2031) | USD 29.87 Billion |

| Growth Rate (2026 - 2031) | 3.12% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

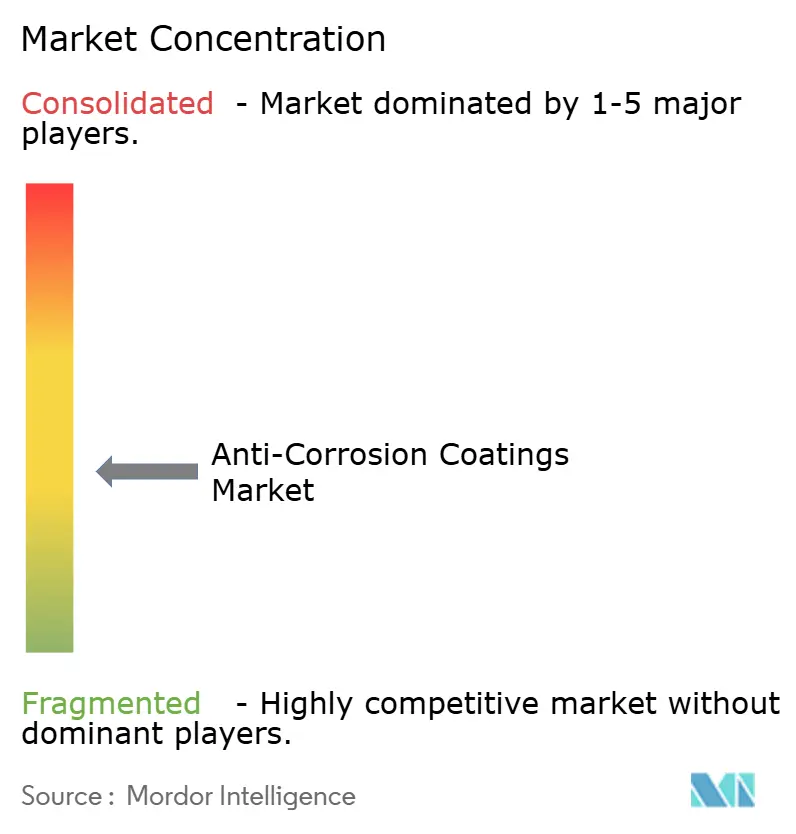

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Anti-Corrosion Coatings Market Analysis by Mordor Intelligence

The Anti-Corrosion Coatings Market size was valued at USD 24.84 billion in 2025 and is estimated to grow from USD 25.62 billion in 2026 to reach USD 29.87 billion by 2031, at a CAGR of 3.12% during the forecast period (2026-2031). Demand is advancing because governments are tightening volatile-organic-compound thresholds, ship operators must meet the International Maritime Organization’s new Carbon Intensity Indicator grades, and asset owners are shortening recoating cycles to protect higher-value infrastructure. In parallel, epoxy raw-material volatility and anti-dumping duties on Asian resin imports are squeezing formulators, prompting a shift toward water-borne and high-solids chemistries that reduce exposure to diisocyanates. Capital allocated to highway, bridge, and offshore-wind projects in the United States, European Union, and Japan is anchoring long-duration volume, while Asia-Pacific’s petrochemical and pipeline workstreams keep the Anti-Corrosion Coatings market on a solid baseline. Competition remains moderate: the five largest suppliers hold about 40% of global capacity, yet regional specialists win niche contracts by offering powder, UV-cured, and foul-release systems that deliver faster cure and zero VOCs.

Key Report Takeaways

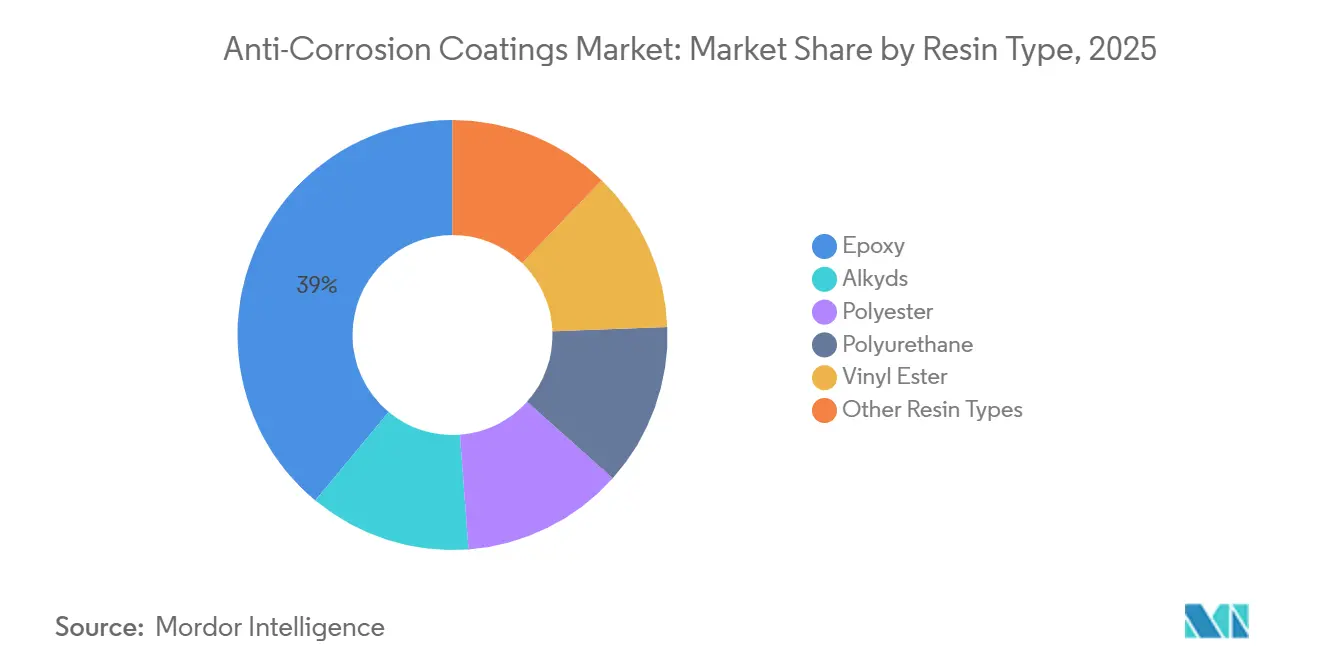

- By resin type, epoxy captured 38.98% of the anti-corrosion coatings market share in 2025, while polyurethane is projected to post the fastest 3.81% CAGR through 2031.

- By technology, solvent-borne systems retained 57.66% revenue share in 2025; water-borne alternatives are set to expand at a 3.72% CAGR to 2031.

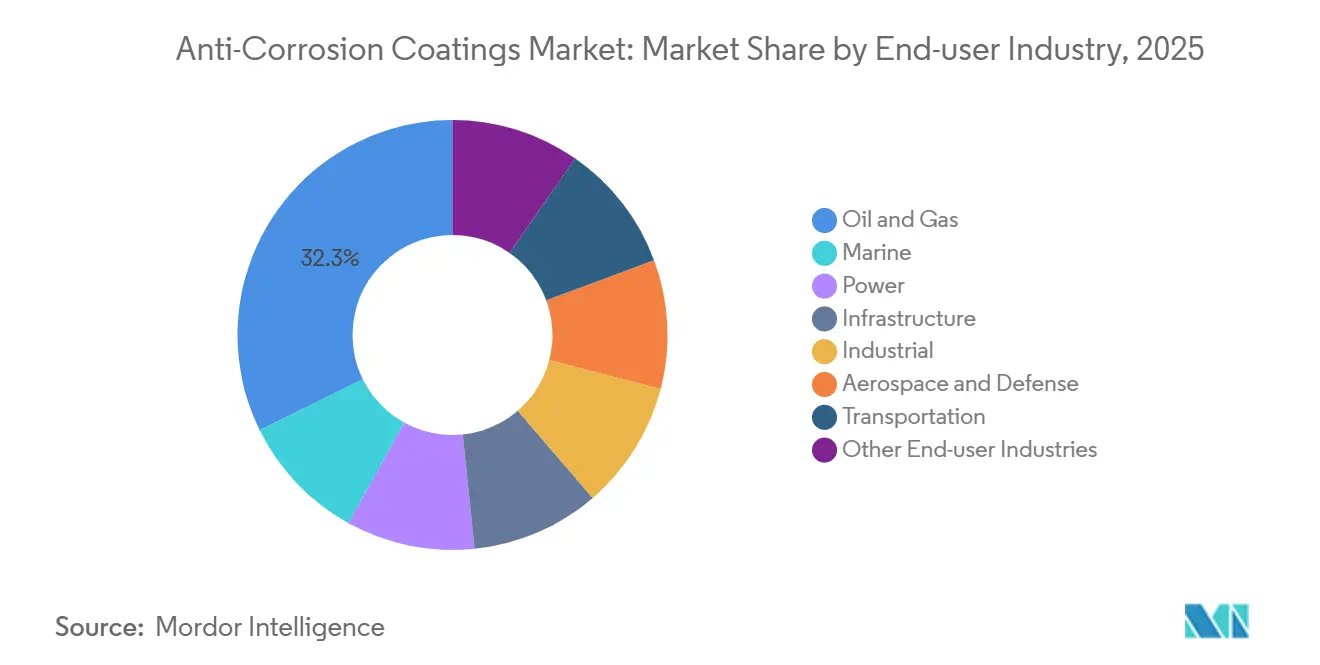

- By end-user industry, oil and gas held 32.29% of the anti-corrosion coatings market size in 2025, whereas infrastructure projects are advancing at a 4.12% CAGR over 2026-2031.

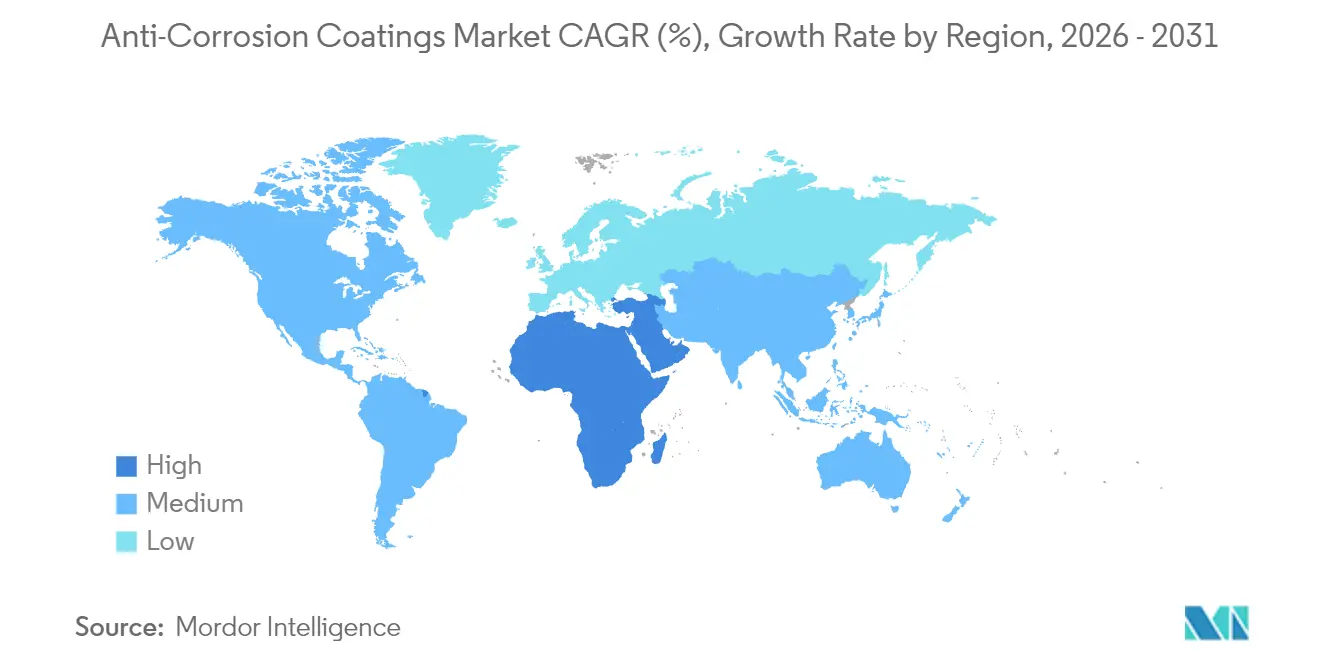

- By geography, Asia-Pacific commanded 46.72% revenue in 2025; the Middle East and Africa region is forecast to grow at a 3.41% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Anti-Corrosion Coatings Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Infrastructure-renewal super-cycle in U.S., European Union and Japan | +0.8% | North America, Europe, Japan | Long term (≥ 4 years) |

| Offshore wind-farm coating boom | +0.6% | Europe, APAC coastal regions, North America Atlantic seaboard | Medium term (2-4 years) |

| Offshore pipeline life-extension spend in Asia-Pacific | +0.5% | APAC core, spill-over to Middle East | Medium term (2-4 years) |

| IMO CII rules driving more frequent hull recoating | +0.4% | Global, with concentration in major shipping registries | Short term (≤ 2 years) |

| CUI-driven specification upgrades at LNG terminals | +0.3% | Global, with early gains in Qatar, Australia, U.S. Gulf Coast | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Infrastructure-Renewal Super-Cycle in US, European Union and Japan

Bridge, tunnel, and rail assets are aging in lockstep across three mature economies. The United States has earmarked USD 110 billion for roads and bridges; state transportation agencies now require three-coat epoxy-polyurethane systems that meet SSPC-Paint 36 for steel structures. Japan’s Ministry of Land, Infrastructure, Transport and Tourism reported in 2025 that 63% of the nation’s 730,000 bridges exceed 50 years of age, unlocking JPY 5.3 trillion (USD 35 billion) for corrosion remediation through 2030[1]MLIT Japan, “National Bridge Statistics 2025,” mlit.go.jp. Meanwhile, Germany alone is replacing 4,000 Autobahn bridges under an EUR 2.8 billion initiative. These synchronized budgets create a durable floor for the Anti-Corrosion Coatings market, as steel recoating cycles last 15-25 years and specification bodies insist on ISO 12944-C5-M compliance.

Offshore Wind-Farm Coating Boom

Installed offshore-wind capacity reached 75 GW by late 2025, and every monopile, transition piece, and offshore substation demands multi-layer zinc-epoxy-polysiloxane protection[2]Global Wind Energy Council, “Global Offshore Wind Report 2026,” gwec.net. Ørsted’s 2.9 GW Hornsea Three project requires 25-year service-life coatings approved after 10,000-hour salt-spray testing. On the US side, six Atlantic lease areas auctioned in 2024 will need roughly 180,000 tons of coatings through 2032. Because fewer than 20 global yards hold DNV certification for offshore-wind fabrication, coating specifications are tightly controlled, pushing the Anti-Corrosion Coatings market toward premium chemistries that command 30-40% price premiums.

Offshore Pipeline Life-Extension Spend in Asia-Pacific

More than 45,000 km of subsea pipelines installed during the 1990s now face corrosion fatigue. Petronas let a USD 320 million rehabilitation contract in 2025, mandating fusion-bonded epoxy and polypropylene overwrap in accordance with ISO 21809. Woodside Energy is spending AUD 1.2 billion (USD 780 million) to extend North West Shelf assets by 15 years, with coatings grabbing 18% of that budget. These projects favor suppliers that can mobilize offshore crews and validate coating integrity in real time, deepening loyalty to multinational brands in the Anti-Corrosion Coatings market.

IMO CII Rules Driving More Frequent Hull Recoating

The Carbon Intensity Indicator applies letter grades that affect charter rates and port-state control. Hull fouling degrades scores, so operators are cutting dry-dock intervals from 60 months to as little as 36 months. Maersk advanced 42 dockings in 2025 and spent USD 180 million on silicone foul-release technology, citing an 8% fleetwide fuel-cut. Nippon Paint Marine’s hydrogel system claimed a 12% saving in Japan’s National Maritime Research Institute trials. These moves reinforce the Anti-Corrosion Coatings market’s cadence in marine segments, accelerating throughput for suppliers with advanced R&D capabilities.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Global VOC / isocyanate exposure caps tightening | -0.5% | Europe, North America, with Asia-Pacific adoption by 2028 | Medium term (2-4 years) |

| Epoxy raw-material price spikes (Bis-A, ECH) | -0.4% | Global, with acute pressure in Europe post-tariff | Short term (≤ 2 years) |

| Deferred CAPEX in oil-&-gas downturn cycles | -0.3% | Global, concentrated in offshore and upstream segments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Global VOC / Isocyanate Exposure Caps Tightening

Directive 2020/1149 compels every European worker handling >0.1% diisocyanate to complete certified training, adding EUR 5,000-15,000 per facility in compliance costs. The European Chemicals Agency will enforce a 6 µg NCO/m³ limit by 2029, roughly 10 times stricter than prior levels. The United States is following with a proposed OSHA 5 µg NCO/m³ limit. These caps penalize solvent polyurethane lines and nudge buyers toward water-borne dispersions, though 4-6 hour dry times hamper throughput in fabrication shops.

Epoxy Raw-Material Price Spikes (Bis-A, ECH)

Unplanned cracker outages pushed liquid epoxy resin spot prices in Asia to USD 2,450/t in Q1 2026, up 18% YoY. Europe imposed anti-dumping duties of 10-170% on imports from China, South Korea, Taiwan, and Thailand in January 2025. Huntsman disclosed USD 42 million in added costs during 2025, forcing three price surcharges totaling 12%. Formulators with backward integration, such as Olin, fared better, widening the cost gap inside the Anti-Corrosion Coatings market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin Type: Epoxy Dominance Meets Polyurethane Momentum

Epoxy systems represented 38.98% of the Anti-Corrosion Coatings market share in 2025, underscoring the chemistry’s adhesion to steel and compatibility with cathodic-protection schemes. The Anti-Corrosion Coatings market size attributable to epoxy is projected to climb at a steady clip as refiners, pipeline operators, and offshore platforms renew tank linings and splash-zone barriers. Polyurethane demand is rising faster, expanding 3.81% CAGR, because onshore wind towers, solar frames, and façade steel require UV stability and color retention.

Alkyd and polyester resins persist in cost-sensitive niches, yet their growth trails the overall Anti-Corrosion Coatings market. Hybrid epoxy-primer plus polyurethane topcoat systems are blurring category lines, rewarding suppliers that validate cross-link compatibility through accelerated weathering. Self-healing and corrosion-sensing pigments, highlighted by 14 Akzo Nobel patents in 2024-25, point to next-generation chemistries that could elongate maintenance intervals beyond 25 years, strengthening premium positions within the Anti-Corrosion Coatings industry.

By Technology: Solvent-Borne Retreat, Water-Borne Advance

Solvent-borne platforms held 57.66% of the Anti-Corrosion Coatings market in 2025, thanks to rapid dry times and robust performance in humid marine yards. However, regulatory pressure and worker-exposure limits are steering asset owners toward 85-90% solids or water-borne systems that cut VOCs by up to 60%. Water-borne volumes will grow at 3.72% through 2031, gradually eroding solvent-borne share within the overall Anti-Corrosion Coatings market size.

Powder and UV-cured systems remain single-digit slices, constrained by oven-curing footprints and line-of-sight limitations, yet they thrive in appliances, rebar, and flat-panel sub-sectors where zero VOCs unlock air-permit exemptions. These eco-friendly niches, while small, deliver above-average margins, attracting R&D funds from both multinationals and agile regional players determined to capture specialty Anti-Corrosion Coatings market value.

By End-User Industry: Oil and Gas Leadership, Infrastructure Acceleration

Oil and gas dominated 32.29% of 2025 demand, reflecting nonstop maintenance of offshore jackets, storage tanks, and gathering lines. That slice fluctuates with crude prices, so suppliers diversify toward infrastructure segments that are forecast to expand at a 4.12% CAGR and add durable tonnage to the Anti-Corrosion Coatings market size.

Marine, power generation, and industrial facilities together occupy the balance. IMO hull-recoating cycles and LNG CUI standards are ratcheting performance thresholds upward, pushing buyers toward high-solids epoxies and silicone foul-release topcoats. Infrastructure’s bridge-and-tunnel backlog makes it the steadiest growth vector, enabling the Anti-Corrosion Coatings industry to cushion cyclical oil-price swings with government-funded workstreams.

Geography Analysis

Asia-Pacific generated 46.72% of the Anti-Corrosion Coatings market revenue in 2025, backed by China’s eight new refineries totaling 2.4 million b/d and India’s coastal pipeline rehabilitation initiatives. The Anti-Corrosion Coatings market size in the region swells further as Southeast Asian operators extend 18,000 km of subsea lines and Japanese authorities funnel JPY 5.3 trillion into bridge lifeline upgrades.

In North America, the USD 110 billion US bridge budget is channeling demand for SSPC-certified three-coat systems, while Canada’s oil sands keep high-temperature epoxy-phenolic orders consistent. Europe’s 20% share rides on North Sea offshore wind and Autobahn bridge replacements, both specifying ISO 12944-C5-M coatings that drive premium pricing.

The Middle East & Africa is the fastest rising geography at 3.41% CAGR. Saudi Aramco’s USD 12 billion Marjan and Berri expansions, ADNOC’s sour-gas megaproject, and Gulf desalination plants collectively ensure steady throughput for suppliers able to meet hydrogen-sulfide and brine-exposure criteria. Latin America and South Asia trail but offer episodic surges tied to Petrobras pre-salt maintenance and Indian port construction. This mosaic keeps the Anti-Corrosion Coatings market geographically diversified, limiting overreliance on a single demand hub.

Competitive Landscape

The Anti-Corrosion Coatings market is moderately fragmented. Regional challengers carve profitable corners with powder, UV-cured, and niche epoxy-novolac systems, offering fast turnaround and zero VOCs that bypass new air permits. Digital platforms are emerging as tie-breakers; Hempel’s Oceanics software schedules hull-cleaning windows based on real-world vessel data, embedding service revenue beyond the coating gallon. M&A remains a favored route, these transactions reveal a market where scale plus specialized chemistry is the winning formula, preserving moderate concentration while allowing agile entrants to flourish in high-growth pockets of the Anti-Corrosion Coatings market.

Anti-Corrosion Coatings Industry Leaders

Akzo Nobel N.V.

Hempel A/S

Jotun

PPG Industries, Inc.

The Sherwin-Williams Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Researchers integrated PEDOT into UV-curable acrylics, enabling solvent-free corrosion protection with improved conductivity, targeting electronics housings subject to salt atmosphere exposure.

- March 2025: Hebrew University unveiled a dual-layer coating using N-heterocyclic carbene monolayers plus polymer topcoats, achieving 99.6% corrosion inhibition on carbon steel coupons.

Global Anti-Corrosion Coatings Market Report Scope

Anti-corrosion coatings provide protection to metal components from rust, salt spray, moisture, oxidation, and other industrial chemicals and corrosive environments. The anti-corrosive properties of these coatings ensure the longer lifespan of metal components.

The anti-corrosion coatings market is segmented by resin type, technology, end-user industry, and geography. By resin type, the market is segmented into epoxy, polyester, polyurethane, vinyl ester, and other resin types. By technology, the market is segmented into water-borne, solvent-borne, powder, and UV-cured. By end-user industry, the market is segmented into oil & gas, marine, power, infrastructure, industrial, aerospace and defense, transportation, and other end-user industries. The report also covers the market size and forecasts for the anti-corrosion coatings market in 18 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of revenue (USD).

| Epoxy |

| Alkyds |

| Polyester |

| Polyurethane |

| Vinyl Ester |

| Other Resin Types |

| Water-borne |

| Solvent-borne |

| Powder |

| UV-cured |

| Oil and Gas |

| Marine |

| Power |

| Infrastructure |

| Industrial |

| Aerospace and Defense |

| Transportation |

| Other End-user Industries |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Spain | |

| Italy | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Nigeria | |

| Rest of Middle-East and Africa |

| By Resin Type | Epoxy | |

| Alkyds | ||

| Polyester | ||

| Polyurethane | ||

| Vinyl Ester | ||

| Other Resin Types | ||

| By Technology | Water-borne | |

| Solvent-borne | ||

| Powder | ||

| UV-cured | ||

| By End-user Industry | Oil and Gas | |

| Marine | ||

| Power | ||

| Infrastructure | ||

| Industrial | ||

| Aerospace and Defense | ||

| Transportation | ||

| Other End-user Industries | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Spain | ||

| Italy | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How large will global demand for Anti-Corrosion Coatings be by 2031?

The Anti-Corrosion Coatings market is projected to reach USD 29.87 billion by 2031, reflecting a 3.12% CAGR from 2026 to 2031.

Which resin class dominates protective-coating applications?

Epoxy systems led the market with 38.98% share in 2025, driven by strong adhesion and chemical resistance on steel substrates.

Why are shipowners recoating hulls more frequently?

The International Maritime Organization’s Carbon Intensity Indicator grades penalize hull fouling, prompting operators to shorten dry-dock intervals and apply low-friction silicone or hydrogel coatings that cut fuel burn.

What region will add coatings demand fastest through 2031?

The Middle East & Africa segment is forecast to grow at 3.41% CAGR thanks to Saudi Aramco, ADNOC, and Gulf desalination investments.

How are regulations shaping technology choices?

Stricter VOC and isocyanate exposure limits are steering buyers toward water-borne, high-solids, and powder offerings that slash emissions without sacrificing corrosion protection.

Page last updated on: