Colostrum Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

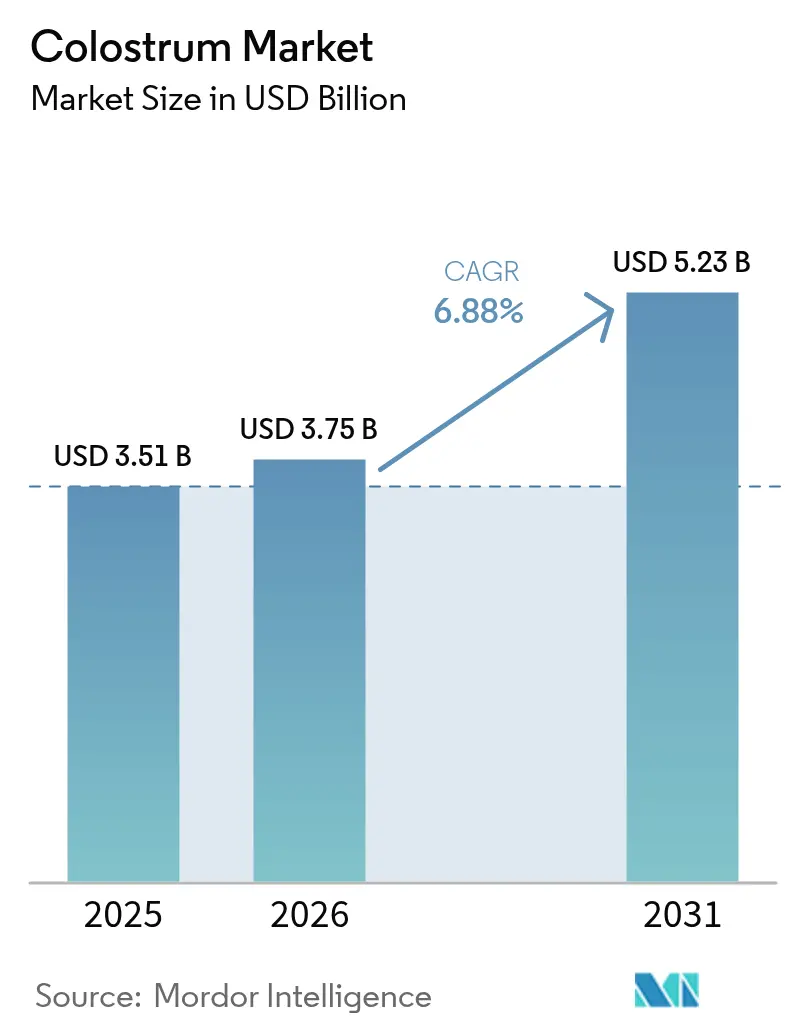

| Market Size (2026) | USD 3.75 Billion |

| Market Size (2031) | USD 5.23 Billion |

| Growth Rate (2026 - 2031) | 6.88% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Colostrum Market Analysis by Mordor Intelligence

The colostrum market size is expected to grow from USD 3.51 billion in 2025 to USD 3.75 billion in 2026 and is forecast to reach USD 5.23 billion by 2031 at 6.88% CAGR over 2026-2031. This growth is fueled by increasing awareness of colostrum's bioactive components, a rising focus on immune health post-pandemic, and its expanding applications across dietary supplements, functional foods, infant nutrition, and cosmetics. North America is experiencing accelerated approvals for new products, while Asia-Pacific is witnessing growth driven by increasing disposable incomes and evolving consumer preferences. Technological advancements, particularly in precision fermentation, are reshaping the competitive landscape by enabling innovative product development. Furthermore, the market is seeing a shift towards premium, organic, and minimally processed products, as consumers increasingly associate colostrum with preventive health benefits and clean-label nutrition. These factors collectively contribute to the market's sustained value growth and evolving dynamics.

Key Report Takeaways

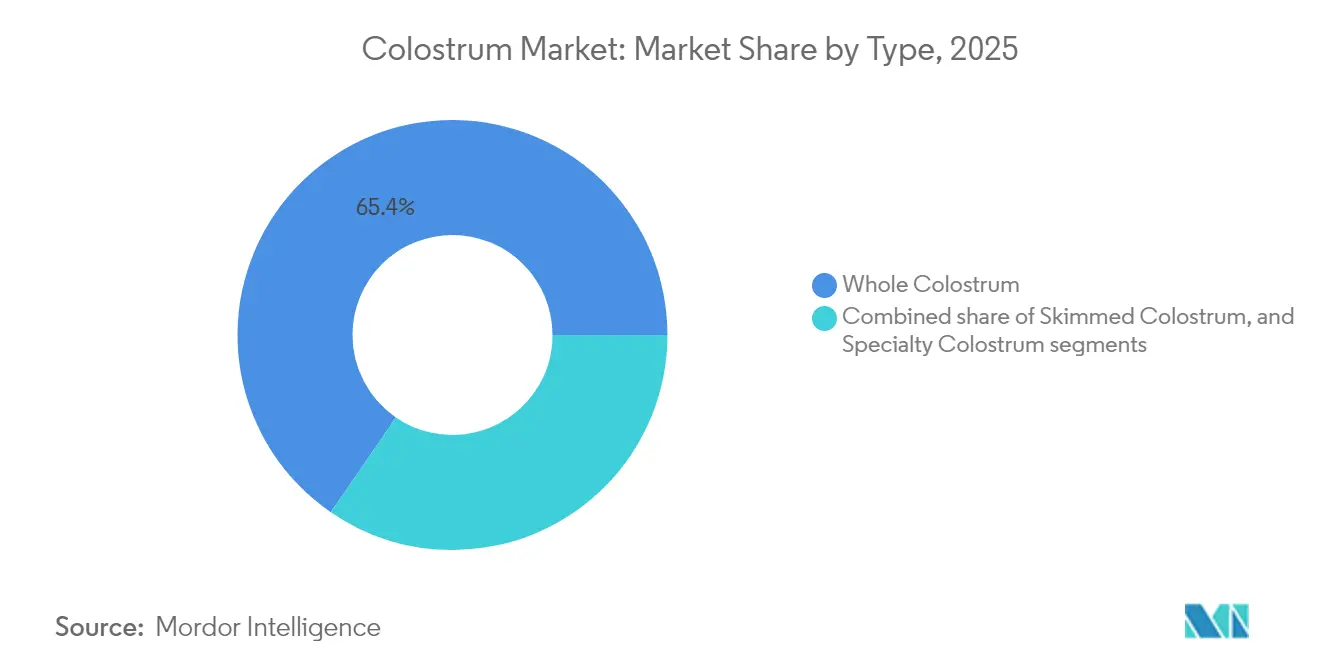

- By type, whole colostrum held 65.42% of the colostrum market share in 2025, while specialty formulations are expanding at a 8.85% CAGR through 2031.

- By form, powder commanded 69.60% of the colostrum market in 2025; liquid form is advancing fastest at 8.76% CAGR over 2026-2031.

- By source, bovine segment dominated with a 90.85% share in 2025 and continues to pace the colostrum market with an 8.62% CAGR through 2031.

- By nature, the organic segment is growing at 10.02% CAGR in the colostrum market, while conventional retains 75.80% share in 2025.

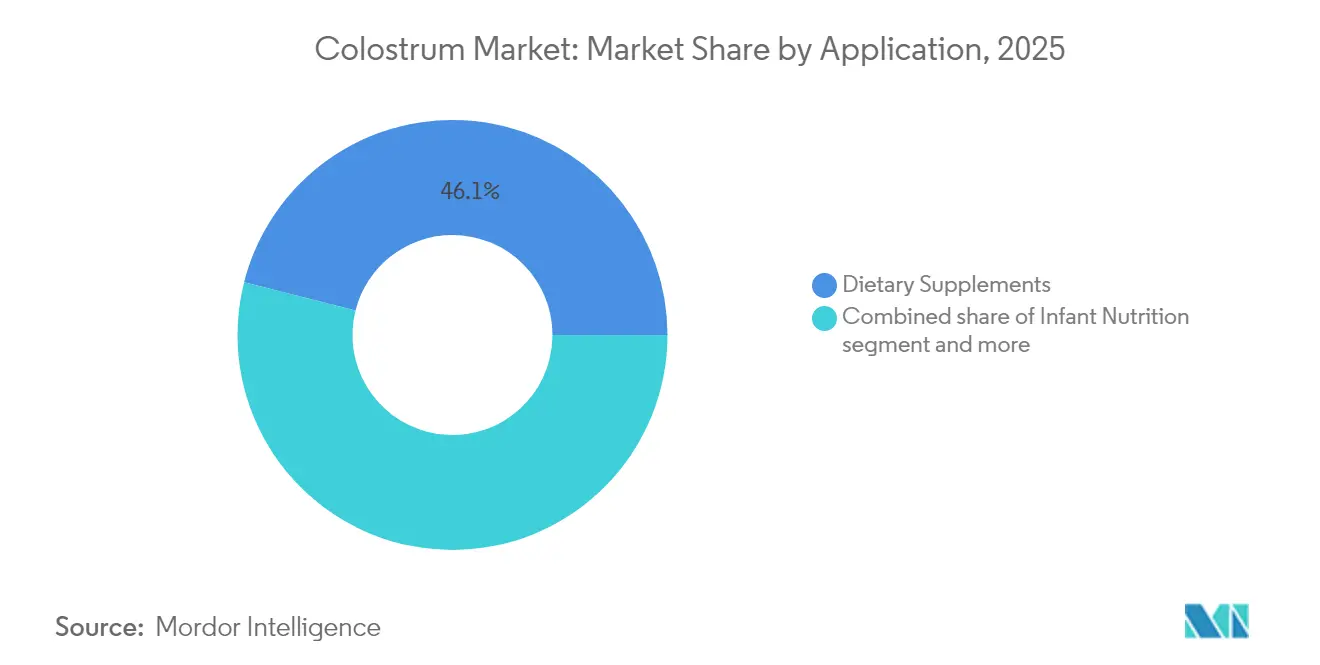

- By application, dietary supplements accounted for 46.05% share of the colostrum market size in 2025 and post a 9.74% CAGR through 2031.

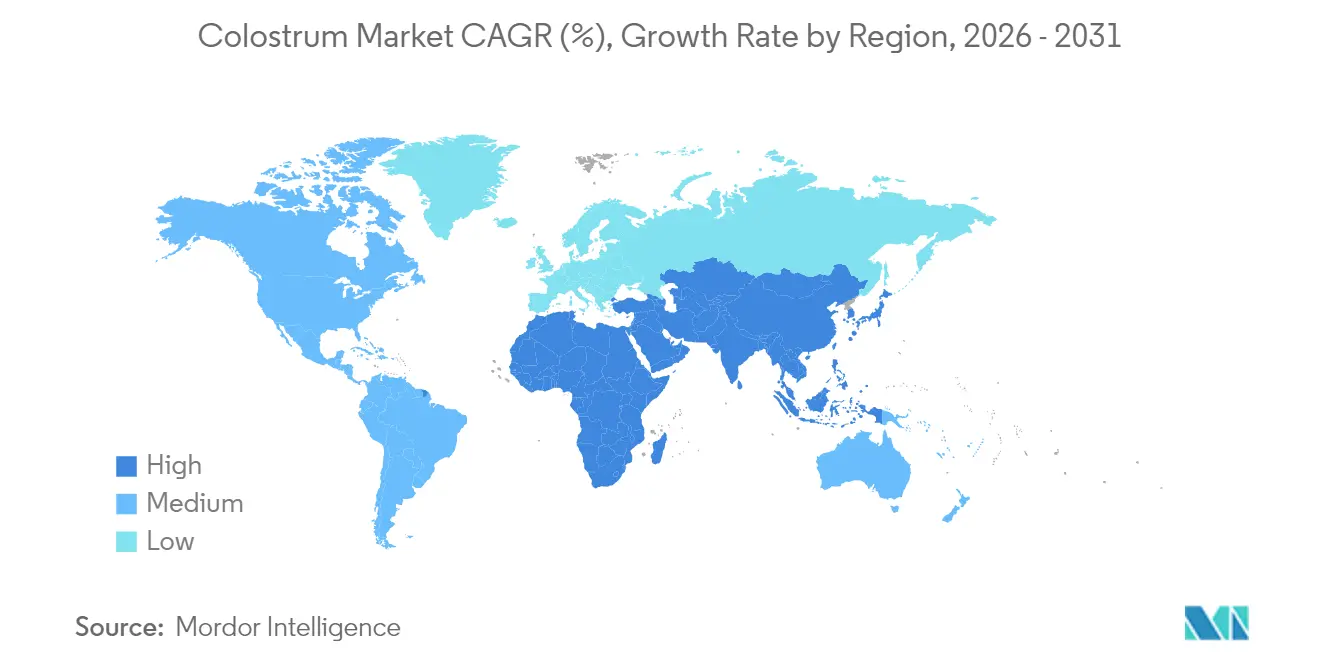

- By geography, North America led with 43.90% revenue share in 2025; Asia-Pacific is the fastest-growing region at a 10.25% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Colostrum Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for immune-boosting supplements | +1.8% | Global, with peak demand in North America and Europe | Short term (≤ 2 years) |

| Increasing demand for natural and functional food | +1.5% | Global, particularly strong in Asia-Pacific and North America | Medium term (2-4 years) |

| Expanding use in infant formula and baby food products | +1.2% | Asia-Pacific core, spill-over to North America and Europe | Medium term (2-4 years) |

| Rising prevalence of digestive health issues driving supplement demand | +1.0% | Global, with higher impact in developed markets | Long term (≥ 4 years) |

| Increasing focus on preventive healthcare | +0.9% | North America and Europe, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Rising demand for natural alternatives to antibiotics | +0.7% | Global, with regulatory support in Europe and North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising demand for immune-boosting supplements

The post-pandemic health landscape has significantly reshaped consumer priorities, driving a strong demand for proactive immune support solutions. This shift has positioned colostrum as a premium ingredient within the nutraceutical sector. Scientific studies have demonstrated that bovine colostrum supplementation effectively enhances salivary secretory IgA levels following exercise. This biomarker plays a pivotal role in mucosal immunity and is directly associated with a reduced risk of upper respiratory tract infections. Beyond athletic populations, colostrum's immune-modulating properties have shown promise in the treatment and prevention of COVID-19, attributed to its high immunoglobulin content. The regulatory environment has also evolved to support this growing market. The FDA's updated guidance on new dietary ingredient notifications, which will take effect in May 2024, has streamlined the approval process for colostrum-based supplements[1]United States Food and Drug Administration, "Guidance for Industry: New Dietary Ingredient Notification Procedures and Timeframes - Dietary Supplements", www.fda.gov. This regulatory shift reduces barriers and accelerates the market entry of innovative formulations, fostering growth in the sector. Market dynamics reveal a willingness among consumers to invest in scientifically validated immune support products.

Increasing demand for natural and functional food

Consumer demand for clean-label and naturally-derived functional ingredients is reshaping food formulation strategies across multiple categories, positioning colostrum as a key bioactive ingredient. The organic dairy sector continues to demonstrate strong growth, as evidenced by a 10.3% increase in organic whole milk sales in January 2025 compared to the previous year, according to the Northeast Organic Dairy Producers Alliance[2]Northeast Organic Dairy Producers Alliance, "Pay and Feed Price, May, 2025", www.nodpa.com. This growth reflects a broader consumer shift toward premium natural products. Food manufacturers are leveraging colostrum's proven health benefits and clean-label appeal by incorporating it into functional beverages, protein bars, and dairy alternatives, aligning with evolving consumer preferences. In March 2024, the European Food Safety Agency approved osteopontin for use in infant formulas, marking a significant regulatory milestone for milk-derived bioactive compounds. This approval not only validates the safety and efficacy of such ingredients but also sets the stage for broader applications of colostrum in functional food products. The combination of regulatory support and increasing consumer awareness of functional ingredients is driving innovation in colostrum-fortified products, expanding their use beyond traditional supplement formats.

Expanding use in infant formula and baby food products

The infant nutrition sector is emerging as a high-value growth area for colostrum applications, driven by increasing parental awareness of the critical role of early-life immune development and the nutritional limitations of conventional formulas compared to breast milk. Human milk oligosaccharides (HMOs), which mimic components of breast milk, are gaining regulatory approval across Asia-Pacific markets. For instance, in June 2025, Indonesia approved dsm-firmenich's 2'-FL for use in liquid milk, signaling a broader acceptance of breast milk-mimicking ingredients in the region. Bovine colostrum, known for its high natural IgG content, plays a pivotal role in providing passive immunity transfer, closely replicating the benefits of maternal colostrum. This has positioned colostrum as a key ingredient in premium infant nutrition products. In December 2024, Vinamilk launched Optimum Colos, a premium infant formula that integrates IgG from colostrum alongside multiple HMOs, highlighting the growing trend of combining colostrum with advanced nutritional components to support immune and digestive health.

Rising prevalence of digestive health issues driving supplement demand

In developed markets, gastrointestinal health issues are escalating, creating a sustained demand for therapies that address underlying causes rather than merely managing symptoms. Colostrum, known for its unique bioactive composition—particularly its high concentrations of lactoferrin and immunoglobulins—has demonstrated significant efficacy in enhancing gut barrier integrity and regulating inflammatory responses. Studies indicate that colostrum supplementation effectively reduces pro-inflammatory cytokine levels while promoting the growth of beneficial gut bacteria, thereby addressing the dysbiosis commonly associated with modern digestive disorders. The FDA's acquisition of global rights to VOWST in 2024, a microbiota-based therapeutic designed to prevent Clostridioides difficile infections, highlights increasing regulatory support for microbiome-targeted interventions. This development could positively impact colostrum products that contribute to gut microbiota balance. Colostrum's prebiotic oligosaccharides act as selective growth substrates for beneficial bacteria, fostering a healthier gut microbiome. Concurrently, its antimicrobial peptides help control pathogenic microorganisms without disrupting the balance of commensal bacteria. This dual-action mechanism positions colostrum as an advanced solution for gut health, addressing both microbial imbalances and intestinal barrier dysfunction.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited availability of raw materials | -1.2% | Global, particularly acute in regions with declining dairy herds | Medium term (2-4 years) |

| High production costs | -0.9% | Global, with higher impact in developed markets | Short term (≤ 2 years) |

| Competition from alternative nutritional supplements and functional food products | -0.8% | North America and Europe primarily | Medium term (2-4 years) |

| Storage and preservation challenges due to perishable nature | -0.6% | Global, with greater impact in regions with limited cold chain infrastructure | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Limited availability of raw materials

The colostrum supply chain faces significant structural challenges that hinder market expansion. Bovine colostrum accounts for only a small fraction of the annual dairy cow output, creating an inherent scarcity of raw materials. For instance, Australia's dairy industry illustrates these challenges, as extreme weather events and a declining number of farms have reduced the national dairy herd, increasing reliance on imported dairy products. This situation is further complicated by the industry's "peak milk" scenario, where production capacity struggles to meet rising demand. The specialized nature of colostrum collection adds to the complexity, requiring precise timing—within 24 hours of calving—and strict adherence to quality protocols to ensure product viability. Climate change exacerbates these issues, with extreme weather events disrupting milk production schedules and potentially compromising colostrum quality and yield. Additionally, the geographic concentration of dairy production in specific regions heightens vulnerability, as disruptions in these areas can have a cascading impact on the global colostrum supply chain. Companies like Zinpro Corporation are addressing this scarcity by purchasing colostrum from dairy farms at prices double that of commercial milk, underscoring the premium value of this limited resource. This persistent supply-demand imbalance is driving the development of alternative production methods.

High production costs

Processing colostrum involves specialized equipment and stringent quality controls, which significantly increase production costs compared to conventional dairy products. Advanced processing technologies, such as freeze-drying and spray-drying, are critical for preserving bioactive components. Studies reveal that freeze-drying retains higher levels of immunoglobulins but requires considerably more energy and time than spray-drying, making it a more resource-intensive option. Additionally, maintaining a cold chain throughout the supply chain is essential, as colostrum's bioactive components are highly sensitive to temperature fluctuations. This necessitates continuous refrigeration from collection to final processing, adding multiple cost layers. The collection process for colostrum is labor-intensive, requiring trained personnel and precise timing, which limits the ability to achieve economies of scale.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Whole Colostrum Dominates While Specialty Formulations Accelerate

In 2025, whole colostrum holds a dominant 65.42% share of the market, driven by its comprehensive nutritional profile and the presence of a mature, cost-efficient processing infrastructure. This segment's leadership is rooted in its rich bioactive composition, which includes over 90 beneficial compounds such as immunoglobulins, lactoferrin, growth factors, and oligosaccharides. These components work synergistically to deliver a wide range of health benefits. The processing methods for whole colostrum are optimized to preserve the natural balance of these bioactive elements, enhancing its suitability for diverse applications, including dietary supplements and functional foods.

Specialty colostrum formulations are witnessing significant growth, with a projected CAGR of 8.85% through 2031, fueled by their expanding use in sports nutrition, cosmetics, and therapeutic applications. This growth reflects advancements in colostrum processing technologies and the development of targeted formulations tailored to specific health conditions and demographic needs. For instance, research conducted by Magna Graecia University in 2024 highlights colostrum's potential in mesenchymal stem cell therapy, demonstrating its ability to promote cellular regeneration and tissue repair. Such findings are opening new therapeutic avenues beyond traditional nutritional uses.

By Form: Powder Leads While Liquid Gains Momentum

In 2025, powders maintain a commanding 69.60% market share, driven by their extended shelf life, cost-efficient transportation, and wide-ranging applications in supplements and food products. These formulations leverage advanced spray-drying and freeze-drying technologies, which not only preserve critical bioactive components but also enable economical storage and distribution. Their dominance is further reinforced by their seamless adaptability to the supplement industry's manufacturing processes, making them highly suitable for capsules, tablets, and functional food formulations. Notably, freeze-drying retains a higher concentration of immunoglobulins compared to other methods; however, it requires more energy and time than spray-drying, which is a more efficient alternative.

Liquid colostrum formulations are experiencing rapid growth, with a projected CAGR of 8.76% through 2031. This growth is fueled by their superior bioavailability and a strong consumer perception of freshness and potency. Research on milk fat globule structures highlights that thermal processing can reduce bioactivity, whereas minimal processing techniques, as employed in liquid formulations, effectively preserve these functional components. The liquid segment benefits significantly from advancements in cold-chain logistics and innovative packaging solutions, which not only extend shelf life but also protect the integrity of bioactive compounds. Positioned as a premium product, liquid colostrum offers manufacturers higher profit margins by catering to health-conscious consumers who prioritize minimally processed, natural products.

By Nature: Conventional Dominance Versus Organic Acceleration

In 2025, conventional colostrum holds a dominant 75.80% market share, driven by well-established supply chains, lower production costs, and broad availability across diverse price points. This segment's leadership reflects the maturity of traditional dairy farming practices and processing infrastructure, which efficiently manage large-scale production while maintaining consistent quality standards. The production of conventional colostrum benefits significantly from economies of scale and streamlined regulatory processes, enabling cost-effective manufacturing and distribution.

The organic colostrum segment, while holding a smaller market share, is experiencing rapid growth with a remarkable 10.02% CAGR projected through 2031, significantly outpacing the conventional segment. This growth aligns with broader consumer preferences for organic and sustainably produced food products, as evidenced by the consistent year-over-year increase in organic whole milk sales. By early 2025, the average retail price of organic milk is expected to exceed USD 5 per half gallon, highlighting consumers' willingness to pay a premium for organic dairy products. Additionally, competition among processors for organic milk is intensifying, with pay prices ranging between USD 33 and USD 50 per hundredweight. This robust demand for organic dairy inputs extends to colostrum production, reflecting the growing importance of sustainability and premium quality in consumer purchasing decisions.

By Application: Dietary Supplements' Comprehensive Leadership

In 2025, dietary supplements hold a commanding 46.05% share of the market, underscoring colostrum's critical role in enhancing immunity and its growing applications in sports nutrition. The supplement sector benefits significantly from favorable regulatory frameworks, particularly the FDA's streamlined procedures for new dietary ingredient notifications, which simplify market entry for manufacturers. Clinical trials consistently demonstrate colostrum's effectiveness in strengthening immune function, reducing exercise-induced immune suppression, and expediting recovery for athletes, further driving its demand in sports nutrition.

Dietary supplements not only dominate the market but also represent the fastest-growing application, with a projected compound annual growth rate (CAGR) of 9.74% through 2031. This robust growth trajectory, even from a leading position, is driven by an increasing consumer focus on preventive healthcare. The COVID-19 pandemic has amplified the demand for natural immunity-boosting supplements, further accelerating market expansion. Ongoing clinical research continues to uncover additional health benefits and applications of colostrum, including its potential to support digestive health, enhance cognitive function, and promote healthy aging.

By Source: Bovine Colostrum's Dual Leadership

In 2025, bovine colostrum holds a dominant 90.85% market share and is projected to grow at a robust CAGR of 8.62% through 2031. This growth is driven by its strong supply chains, regulatory approvals, and extensive research confirming its safety and efficacy across various applications. The market dominance of bovine colostrum is primarily attributed to its abundant availability compared to alternative sources, a well-established processing infrastructure, and comprehensive clinical studies that emphasize its significant health benefits. The structural similarity between bovine and human immunoglobulins enables effective passive immunity transfer, making bovine colostrum particularly valuable in critical applications such as infant nutrition and immune system support. Decades of safety data and widespread regulatory acceptance across major markets further solidify its position, providing manufacturers with a dependable platform for product development and commercialization strategies.

Continuous innovation in bovine colostrum applications is further driving market growth. Its uses have expanded from traditional dietary supplements to emerging sectors such as cosmetics and therapeutics. Additionally, numerous studies have demonstrated its efficacy in enhancing athletic performance, particularly by improving immune function and recovery markers, which is increasing its adoption beyond conventional health-focused markets.

Geography Analysis

In 2025, North America leads the colostrum market with a 43.90% share. This leadership is bolstered by established regulatory frameworks, heightened consumer awareness, and the presence of key colostrum processing firms. North America's growth is further fueled by a thriving organic dairy sector and a robust sports nutrition market, both significant consumers of colostrum ingredients. Clearer FDA regulations on dietary supplement ingredients have not only streamlined product innovation but also facilitated market entry, reinforcing North America's status as a global innovation leader. Moreover, strategic investments in cold chain infrastructure and cutting-edge processing technologies have empowered North American companies to uphold product quality and broaden their distribution networks.

Asia-Pacific is set to be the fastest-growing region, projected to grow at a 10.25% CAGR from 2026 to 2031. This growth is driven by increasing disposable incomes, swift urbanization, and a heightened demand for premium infant nutrition, especially in China, India, and Southeast Asia. Regulatory changes, like Japan's revamped dairy governance and China's prohibition on reconstituted milk in shelf-stable items, are elevating quality benchmarks and paving the way for premium colostrum ingredients. The rise of colostrum-enhanced infant formulas and functional foods in the region signals a shift towards preventive healthcare and natural nutrition. Notable milestones include Indonesia's June 2025 endorsement of 2'-FL for flavored liquid milk and Vietnam's swift embrace of HMOs and colostrum in infant nutrition, highlighting the region's innovative drive.

Europe stands as a pivotal market for colostrum, leveraging stringent regulatory oversight, a well-established organic dairy sector, and a robust consumer appetite for clean-label functional foods. The European Food Safety Authority's nod to new bioactive ingredients in infant formulas and functional foods is spurring innovation and market growth. Europe's commitment to sustainability and animal welfare resonates with the burgeoning organic colostrum market. Furthermore, ongoing research into preservation and processing techniques is addressing traditional challenges like cold chain logistics and shelf-life limitations. Meanwhile, smaller markets in South America, the Middle East, and Africa are gradually warming up to colostrum products, often targeting premium segments and relying on imports from seasoned suppliers.

Regulatory Landscape

Regulation of colostrum varies by end use (food, supplement, infant nutrition) and by region, with hygiene, labeling, and import controls shaping market access. In the European Union, colostrum is defined within the framework for food of animal origin and is governed by specific hygiene rules that treat it as a regulated animal-derived product, requiring production in officially approved establishments and use of an oval identification mark. The EU definition covers secretion within three to five days post-parturition. For infant nutrition and other specialized uses, EFSA opinions and EU legal acts also influence how milk-derived bioactives and associated claims can be positioned, affecting how colostrum-derived ingredients are marketed in functional foods and baby nutrition.

Cross-border trade compliance is an operational requirement. In Great Britain, imports of colostrum and colostrum-based products for human consumption require model health certification (for example, GBHC414 C/CBP) and sourcing from authorized third countries or regions listed by authorities. When colostrum is not intended for human consumption, it is treated under animal by-product rules (Category 3 material) with its own documentation pathway. In the United States, classification and import conditions can vary by composition and processing, and certain colostrum-based products may interact with the USDA Dairy Import Licensing Program to access low-tier tariff rates, adding another layer of commercial planning for importers.

Value Chain Analysis

The colostrum value chain begins at dairy farms, where collection must occur within a short post-calving window to preserve immunoglobulins and other bioactives, then shifts to chilled aggregation and rapid primary handling. Processors commonly apply heat-treatment steps such as flash pasteurization, then convert product into shelf-stable formats, predominantly powders, using spray-drying or freeze-drying. Bioactive-retention choices influence cost, throughput, and product positioning across dietary supplements, functional foods, and infant nutrition. The chain then moves into ingredient standardization (testing, blending, and specification setting), packaging, and distribution through B2B ingredient channels, contract manufacturers for finished supplements, and direct-to-consumer brands.

Constraints cluster around raw-material scarcity and processing capacity. Colostrum supply remains structurally limited by calving cycles and competes with conventional dairy processing for low-temperature drying capacity. At the same time, compliance requirements such as facility approvals, GMP systems, and export documentation create high barriers for new processing assets. As a result, processors have leaned toward tighter integration with farm networks to secure collection volumes and quality, alongside investments in processing upgrades and logistics to reduce spoilage and improve bioactive consistency for global shipments.

Competitive Landscape

The global colostrum market is moderately fragmented, characterized by competition among multinational dairy giants, specialized nutraceutical companies, and regionally focused players. Prominent companies such as Saskatoon Colostrum Company Ltd., PanTheryx, Inc., PanTheryx, Inc., Glanbia plc, and SwissBioColostrum AG, among others, maintain a significant global presence through large-scale production capabilities and extensive distribution networks. Meanwhile, smaller firms and niche brands thrive by targeting specific applications, including infant nutrition, sports recovery, and immunity enhancement, catering to specialized consumer needs.

Market concentration is on the rise as leading players increasingly invest in vertical integration, proprietary processing technologies, and strategic partnerships. These efforts aim to secure raw material supplies and maximize value across the supply chain. For instance, Fonterra’s strategic focus on B2B dairy nutrition and its investments in processing capacity reflect a broader industry trend toward ingredient specialization and supply chain optimization. Similarly, Glanbia’s Nutritionals segment reported a 14.4% revenue growth in 2024, driven by strong demand for protein and premix solutions, underscoring the growing significance of colostrum and related bioactives in the evolving nutrition landscape.

Technological advancements are reshaping the market, particularly in preservation techniques. Innovations such as advanced freeze-drying and encapsulation methods are extending product shelf life and enabling the development of new formats. Additionally, colostrum’s unique bioactive profile presents significant opportunities in emerging sectors like cosmetics, regenerative medicine, and targeted medical nutrition, where differentiation is key. This competitive environment fosters the creation of diverse colostrum-derived products, including powders, chewable tablets, and liquids. However, brand differentiation increasingly depends on factors such as sourcing transparency, advanced processing methods, and clinical validation. The rising consumer demand for immune-boosting and functional foods continues to drive growth opportunities across the market, benefiting both established players and smaller entrants.

Colostrum Industry Leaders

-

The Saskatoon Colostrum Company Ltd.

-

PanTheryx, Inc.

-

NOW Health Group, Inc.

-

SwissBioColostrum AG

-

Glanbia plc

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Premiumization and formulation-led differentiation create near-term whitespace in specialty colostrum formats that emphasize bioactive retention, traceable sourcing, and fit with health-positioned products. A clear indicator of supply-side tension and opportunity is the May 2026 confirmation by The Saskatoon Colostrum Company Ltd. that it is expanding plant capacity to address a temporary shortage of powdered bovine colostrum. The announcement points to ingredient availability and processing throughput becoming competitive advantages for brands supplying dietary supplements and functional foods.

Expansion into targeted digestive-health positioning also opens additional commercialization routes that connect colostrum with broader gut-health and microbiome categories. In February 2025, PanTheryx launched Relesium, a patented formulation combining chicken egg powder and bovine colostrum for gastrointestinal support in GLP-1 medication users, showing how branded ingredient systems can move colostrum beyond commodity powders and into condition- or cohort-specific solutions. Regulatory and labeling frameworks remain a practical lever for market access and product design, with examples such as Health Canada Natural Health Products requirements and New Zealand MPI labeling guidance for colostrum products underscoring the need for specification control, validated quality testing, and compliant claims strategies when scaling internationally.

Recent Industry Developments

- May 2026: The Saskatoon Colostrum Company Ltd. confirmed it is expanding plant capacity and increasing production capabilities to address a temporary shortage of powdered bovine colostrum. The move highlights ongoing supply tightness tied to constrained collection windows and processing throughput, and it strengthens the companys ability to support larger, more consistent ingredient programs for supplement and nutrition customers.

- February 2025: PanTheryx launched Relesium, a patented formulation combining chicken egg powder and bovine colostrum positioned for gastrointestinal support in GLP-1 medication users. This expands colostrums role from general immune and sports nutrition applications into targeted digestive-health use cases and supports higher-value branded-ingredient strategies.

- November 2024: PanTheryx introduced Relesium as an all-natural ingredient addressing gastrointestinal side effects associated with GLP-1 weight-loss drugs. The announcement signaled increased competitive focus on pairing colostrum with adjacent bioactives to create differentiated, condition-specific formulations for finished-product manufacturers.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market covers commercial sales of colostrum and colostrum-based ingredients, measured in revenue terms, across human nutrition, personal care, and animal nutrition. We treat the market as a packaged and traded output, whether it is sold as an ingredient or in consumer-ready formats.

Scope exclusions: Excludes informal on-farm consumption and non-commercial transfers that are not priced and recorded through regular trade or retail channels.

Segmentation Overview

-

By Type

- Whole Colostrum

- Skimmed Colostrum

- Specialty Colostrum

-

By Form

- Powder

- Chewable Tablets

- Liquid

- Others

-

By Source

- Bovine

- Caprine

- Others

-

By Nature

- Conventional

- Organic

-

By Application

- Dietary Supplements

- Functional Foods and Beverages

- Infant Nutrition

- Cosmetics and Personal-Care

- Others

-

Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

South America

- Brazil

- Argentina

- Colombia

- Chile

- Peru

- Rest of South America

-

Europe

- Germany

- United Kingdom

- Italy

- France

- Netherlands

- Poland

- Belgium

- Sweden

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- Australia

- Indonesia

- South Korea

- Thailand

- Singapore

- Rest of Asia-Pacific

-

Middle East and Africa

- South Africa

- Saudi Arabia

- United Arab Emirates

- Nigeria

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the guardrails for the model, especially around supply availability, trade flow direction, and the category definitions used by manufacturers and buyers. Sources included USDA and ERS dairy statistics, Eurostat agri-food data, FAOSTAT, UN Comtrade trade lines for dairy categories, and Codex Alimentarius or similar food standards depending on the region focus.

To translate those signals into a usable sizing structure, we also used company annual reports, investor presentations, product specification sheets, and reputable press coverage for launch activity and capacity commentary. In a few cases, subscription databases were used for company financials and intelligence, shipment-level import export checks, and patent look-ups to clarify ingredient positioning. These desk sources are not exhaustive, and additional public and paid references were reviewed for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on confirming what is counted as colostrum in procurement and in finished-product labeling, and how pricing changes by form and grade. We spoke with stakeholders across ingredient suppliers, brand owners, distributors, and downstream users in supplements, infant nutrition, functional foods, cosmetics, and animal feed, with coverage across major consuming and producing regions to test assumptions from more than one angle.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 37% | CXOs: 15% | APAC: 38% |

| Mid tier: 45% | Functional/Unit leaders: 41% | EMEA: 37% |

| Smaller Players: 18% | Managers: 44% | Americas: 25% |

Market-Sizing & Forecasting

Sizing starts with a top-down build using dairy output context, trade direction, and end-use adoption to reconstruct the addressable demand pool for commercial colostrum products. The total is then split using observed mix patterns for form and grade, followed by application weighting that is checked using buyer conversations.

To keep the model grounded, we corroborate totals with selective bottom-up approximations, such as sampled supplier revenue lines where disclosures exist, channel checks on retail and practitioner-led supplement ranges, and an ASP-times-volume logic for powder and liquid formats in key regions. Inputs that matter in this market include the share of bovine-sourced supply versus other sources, conversion and yield assumptions from raw collection into sellable formats, typical potency or standardization practices that influence pricing, regional demand pull from supplements and infant nutrition, and the pace of organic adoption where applicable.

For forecasting, we use scenario analysis, supported by simple trend fitting across demand indicators and the expert view on how pricing and availability are moving. Where bottom-up checks are thin for private companies or fragmented channels, we use conservative share-of-channel assumptions, then re-test the outcome against trade and production signals before finalizing the trajectory.

Data Validation & Update Cycle

Validation uses cross-checks so the final value is not dependent on a single data stream. Analysts compare model outputs against independent signals such as trade flow direction, category growth patterns in core end uses, and supplier commentary on availability, then follow up on any outliers that do not fit the broader data story.

Before sign-off, the model is reviewed in more than one step, and assumptions are re-tested when large variances appear across regions or forms. Reports are refreshed annually, with interim updates triggered when material events occur, such as sharp dairy input price shifts, regulatory changes that affect claims, or major capacity additions. Right before delivery, we do a final pass to ensure clients receive the latest updated view that still maps back to the same repeatable steps.

Mordor Intelligence's Colostrum Market Sizing Compared With Other Published Estimates

Published market sizes for colostrum do not always match, even when they appear close at first glance, because the boundary of what is counted can shift and base years are not aligned. Differences also come from how each publisher treats form factors, pricing progression, and how frequently assumptions are updated.

Trade-flow direction, application mix checks, and price band validation by form are the signals that connect the Mordor Intelligence estimate to a commercially recorded demand pool, rather than a broader wellness proxy. In practice, the largest gaps tend to come from whether infant nutrition and animal feed are fully included, how capsules and chewables are classified versus general supplements, and whether the model uses a single blended price or separate ASP tracks for powder and liquid that move differently over time.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.75 B (2026) | |

| Global Research Publisher A | USD 3.81 B (2025) | Uses a different base year and appears to anchor the model to a broader consumer wellness demand curve, with less clarity on how colostrum sold into animal feed and cosmetics is netted out from ingredient totals. |

| Industry Research Publisher B | USD 3.84 B (2024) | Starts from an earlier base year and can overstate comparability if mixed forms (powder, liquid, capsules, chewables) are priced through a single blended ASP, which changes the value outcome when premium grades expand faster. |

Taken together, the spread is mostly explained by timing and scope boundaries, not by a single right or wrong number. Our approach stays repeatable because each step is tied to a clear demand pool, then checked with form-level pricing logic and end-use mix validation before the final total is published.

Key Questions Answered in the Report

What is the projected value of the colostrum market by 2031?

The colostrum market size is forecast to reach USD 5.23 billion by 2031, growing at a 6.88% CAGR.

Which application currently leads global demand for colostrum?

Dietary supplements hold 46.05% of 2025 revenue and remain the fastest-growing application segment.

Why is Asia-Pacific considered the fastest-growing region?

Rising disposable incomes, stricter quality regulations, and booming infant-formula sales are propelling a 10.25% regional CAGR.

How significant is bovine colostrum within overall supply?

Bovine sources account for 90.85% of global volumes and underpin most commercial products due to extensive safety research.

Page last updated on: