Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

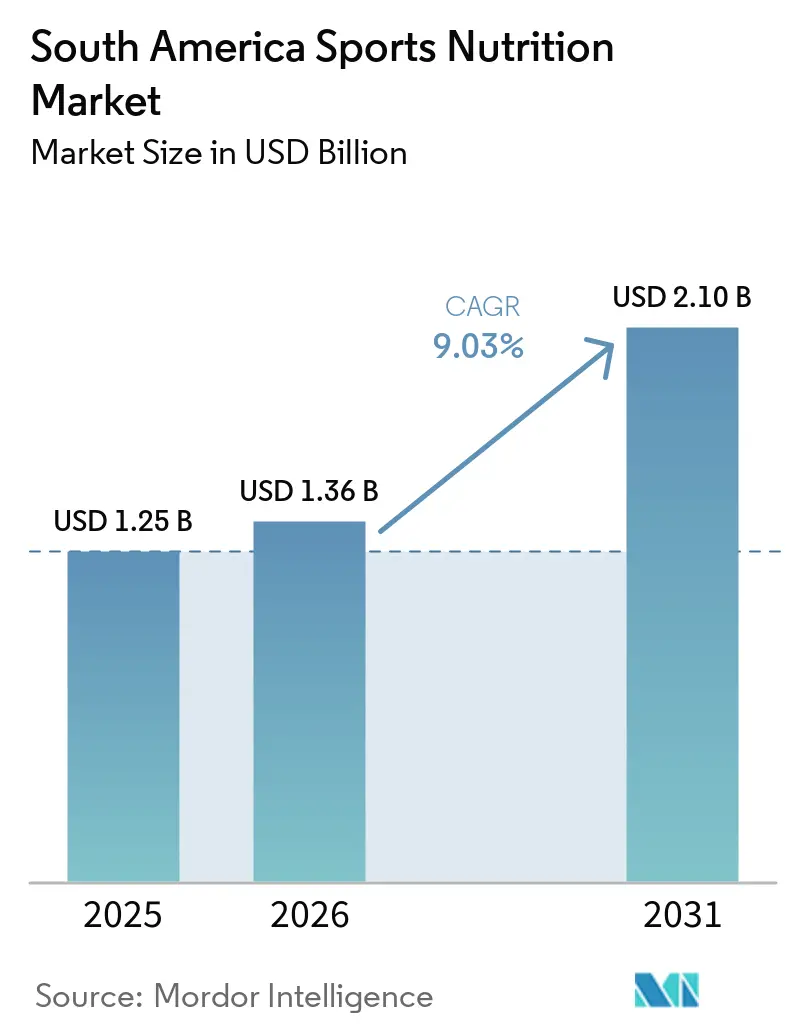

| Base Year Market Size (2025) | USD 1.25 Billion |

| Market Size (2026) | USD 1.36 Billion |

| Market Size (2031) | USD 2.10 Billion |

| Growth Rate (2026 - 2031) | 9.03% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

South America Sports Nutrition Market Analysis by Mordor Intelligence

South American sports nutrition market size in 2026 is estimated at USD 1.36 billion, growing from 2025 value of USD 1.25 billion with 2031 projections showing USD 2.1 billion, growing at 9.03% CAGR over 2026-2031. Brazil emerges as the dominant force in the regional market, commanding the leading market share in 2024 and exhibiting the highest growth rate over the forecast period. The market's expansion is primarily driven by traditional consumers such as athletes and bodybuilders, while witnessing increased adoption among recreational and lifestyle users. Several factors contribute to this growth, including rising disposable income levels across the region, evolving lifestyle patterns, and heightened awareness regarding the benefits of protein-based sports nutrition products. This combination of factors positions the South American sports nutrition market for sustained growth in the coming years.

Key Report Takeaways

- By product type, sports protein products led with 80.12% of the South American sports nutrition market share in 2025; non-protein products are projected to advance at a 9.65% CAGR through 2031.

- By protein source, animal-based offerings captured 65.82% revenue share in 2025, whereas plant-based alternatives are forecast to grow at a 9.88% CAGR to 2031.

- By distribution channel, supermarkets/hypermarkets accounted for 35.15% of the South American sports nutrition market size in 2025 and online retail sales expected to post a 10.06% CAGR between 2026-2031.

- By geography, Brazil dominated with an 83.25% share of the South America sports nutrition market size in 2025 while also registering the highest CAGR at 9.08% for 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South America Sports Nutrition Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth of Urban Fitness Culture | +2.10% | Brazil, Argentina, Chile | Medium term (3-4 years) |

| Rising Awareness of Sports Nutrition Benefits among Athletes | +1.80% | Brazil, Argentina | Medium term (3-4 years) |

| Expansion of Sports Events and Endurance Races | +1.50% | Brazil, Chile | Short term (≤ 2 years) |

| Personalized Sports Nutrition Products | +2.30% | Brazil, Argentina | Long term (≥ 4 years) |

| Social Media Influence Promoting Sports Nutrition Products | +1.70% | Brazil, Argentina, Chile | Medium term (3-4 years) |

| Expansion of E-commerce and Specialty Nutrition Stores | +1.90% | Brazil, Argentina | Medium term (3-4 years) |

| Source: Mordor Intelligence | |||

Growth of Urban Fitness Culture

The growth of urban fitness culture is changing consumption patterns in South America's sports nutrition market. Gym membership growth in metropolitan areas is three times higher than population growth. This shift has created a consumer base that prioritizes performance enhancement over basic nutrition needs, driving increased product demand across segments. According to the Ministry of Tourism and Sports of Argentina in 2023, 50.1% of surveyed individuals were physically active, showing the relationship between professional fitness practices and supplement use [1]Source: Ministry of Tourism and Sports of Argentina, "National Survey of Physical Activity and Sports 2023", www.argentina.gob.ar. This trend is most evident in Brazil's southeast region, where the high concentration of fitness facilities and manufacturing infrastructure supports both product development and consumer education.

Rising Awareness of Sports Nutrition Benefits among Athletes

The growing awareness of sports nutrition benefits among athletes is driving the South American sports nutrition market growth. Both professional and amateur athletes increasingly understand the importance of specialized nutrition for performance enhancement, recovery, and overall health. The expansion of fitness centers, gyms, and health clubs across the region supports this trend, as these facilities actively promote products such as protein supplements, energy drinks, and nutrition bars, often with guidance from in-house dieticians. The fitness industry continues to expand in response to consumer demand. For example, Brazilian franchise Smart Fit operated 706 fitness clubs in Brazil by the end of 2023, showing an 11% increase from 2022. Additionally, social media fitness influencers and content creators have contributed to consumer education and market expansion, particularly in emerging urban and semi-urban markets.

Expansion of Sports Events and Endurance Races

The expansion of mass participation sporting events throughout South America is generating significant periods of concentrated demand, which organizations are strategically utilizing for product introductions and consumer education initiatives. According to official data from the Ministry of Tourism and Sports of Argentina, walking emerged as the predominant form of physical activity in Argentina during 2023, with 71.7% of physically active respondents engaging in this exercise. Running and cycling maintained secondary positions with participation rates of 55.4% and 49.2%, respectively. The proliferation of sporting events is facilitating cross-category product development, as organizations formulate comprehensive solutions addressing pre-event preparation, in-event sustenance, and post-event recuperation requirements, resulting in increased consumer expenditure per athletic pursuit.

Personalized Sports Nutrition Products

The personalized sports nutrition market in South America demonstrates significant expansion due to consumer demand for individualized dietary protocols aligned with specific health objectives, genetic compositions, and lifestyle requirements. The increased emphasis on preventive healthcare measures, prevalence of lifestyle-associated medical conditions, and requirements for optimized athletic performance constitute primary market drivers. Professional athletes and fitness practitioners acknowledge the limitations of standardized nutritional protocols in addressing their distinct physiological requirements and performance objectives. The implementation of genetic analysis systems, physiological monitoring devices, and nutritional management applications facilitates the delivery of individualized dietary recommendations and performance assessment protocols.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost Associated with Sports Nutrition | -1.20% | Argentina, Chile, Rest of South America | Short term (≤ 2 years) |

| Stringent Regulatory Framework | -1.50% | Brazil, Argentina | Medium term (3-4 years) |

| Economic Instability Impacts Purchasing Power | -1.30% | Argentina, Brazil, Chile | Short term (≤ 2 years) |

| Limited Consumer Awareness in Rural and Semi-Urban Areas | -0.90% | Brazil, Argentina, Rest of South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost Associated with Sports Nutrition

The elevated pricing structure of sports nutrition products restricts market penetration beyond affluent consumer segments, particularly in Argentina and Chile where economic conditions have diminished consumer purchasing capacity. Imported products encounter additional financial barriers through tariffs and multilayered distribution networks, resulting in higher retail prices compared to domestic alternatives. This market segmentation has resulted in international premium brands concentrating on high-income demographics, while domestic manufacturers utilize competitive pricing strategies to capture the expanding middle-class consumer base. Consequently, manufacturers have implemented strategic packaging innovations, incorporating single-serve sachets and reduced unit volumes, to enhance product accessibility for price-sensitive consumers while maintaining profit margins.

Stringent Regulatory Framework

The sports nutrition regulatory environment in South America continues to develop, with key regulatory bodies implementing more stringent requirements. Brazil's National Health Surveillance Agency (ANVISA) and Argentina's National Administration of Drugs, Foods, and Medical Devices (ANMAT) have enhanced their oversight of product claims, ingredient safety, and labeling requirements. Brazil introduced RDC 839/2023 in December 2023, which established new regulations for novel ingredients and foods, affecting product formulation processes [2]Source: International Bar Association, "The approval of Anvisa’s RDC 839/2023", www.ibanet.org. Argentina implemented a mandatory front-of-package warning labeling law that restricts marketing activities and prohibits health claims for products carrying warning labels, affecting how sports nutrition companies communicate product benefits. The varying regulatory requirements across South American countries increase operational costs and present challenges for market expansion, particularly affecting smaller companies without dedicated regulatory teams, while benefiting larger multinational corporations with established regulatory capabilities.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

Product Type: Non-Protein Products Gain Momentum

The sports nutrition market shows a significant shift in product dynamics, with non-protein products projected to grow at a 9.65% CAGR (2026-2031). While sports protein products maintain market dominance with an 80.12% share in 2025, consumers are expanding their nutritional choices beyond protein supplementation. Plant-based proteins are gaining market share in the traditionally whey-dominated segment, with 92% of South American performance nutrition consumers reporting use of plant protein products according to Glanbia Nutritionals.

The market shows increased demand for energy gels and creatine powder, driven by the rising popularity of endurance sports in the region. Consumers prefer powder formats due to their cost-effectiveness and flexible dosing options. The ready-to-drink protein segment benefits from established beverage distribution networks, particularly through PepsiCo and Coca-Cola's extensive regional infrastructure in refrigerated product distribution.

Source: Plant-Based Alternatives Challenge Animal Dominance

Animal-based products constitute 65.82% of the market share in 2025, whereas plant-based alternatives demonstrate substantial growth potential, exhibiting a projected CAGR of 9.88% (2026-2031), exceeding the overall market growth rate. This expansion is attributed to shifting consumer preferences and substantial manufacturer investments in plant protein technology for enhanced taste profiles and amino acid composition. The Pan American Health Organization (PAHO) recognizes the significance of plant-based products in promoting sustainability and endorses sustainable procurement practices to enhance the accessibility and affordability of plant-based food products.

The adoption of plant proteins demonstrates distinct regional variations, with Colombia, Brazil, and Argentina exhibiting substantial market penetration. Although individual plant-based proteins may not achieve equivalence with animal proteins in muscle protein synthesis, carefully formulated combinations featuring complementary amino acid profiles can achieve comparable efficacy. This technological advancement enables manufacturers to develop plant-based products that demonstrate competitive advantages in both performance metrics and sustainability parameters, thereby attracting environmentally conscious consumers and athletic populations.

By Distribution Channel: Supermarkets Lead, Online Surges

Supermarkets and hypermarkets delivered 35.15% of the South American sports nutrition market size in 2025, maintaining leadership through high footfall, strong price promotions and prominent in-aisle displays that encourage impulse purchases. Their loyalty programmes and expanding private-label portfolios further cement shopper trust, turning weekly grocery trips into reliable purchase occasions for protein powders, energy bars and hydration products.

Online retail stores form the fastest-growing outlet, forecast to register a 10.06% CAGR between 2026-2031. Mobile-first sites, subscription replenishment plans and rapid last-mile delivery enhance convenience, particularly in secondary cities where specialist stores remain limited. Brands leverage direct-to-consumer portals to gather first-party data, tailor bundle offerings and launch limited-edition flavours that spark social engagement. Click-and-collect services routed through supermarket chains close the loop between digital discovery and physical fulfilment, reinforcing an omnichannel experience that supports long-term customer loyalty.

Geography Analysis

Brazil commands 83.25% of the South American Sports Nutrition Market in 2025 and exhibits the highest growth rate at 9.08% CAGR (2026-2031), influencing regional product development and distribution strategies. This dominance is supported by Brazil's extensive fitness infrastructure, with the Brazilian Association of Gyms (ACAD Brasil) data showing the Southeast region's high concentration of fitness facilities and manufacturing units. Brazil's National Health Surveillance Agency (ANVISA) implemented RDC 839/2023 in December 2023, providing a structured framework for new ingredients and foods that streamlines the registration process. This regulatory update promotes innovation while maintaining consumer safety standards, benefiting companies that effectively manage compliance requirements.

Argentina and Chile, though smaller markets, hold strategic importance with unique consumer patterns and regulatory frameworks. The sports nutrition segment in these countries is expanding from athletic-focused consumers to the general population, aligning with broader health trends. Chile's Institute of Public Health (ISP) enforces strict regulations requiring health permits for supplements, creating market entry challenges that benefit established companies with regulatory knowledge. South America health and fitness club sector is developing, with the Ministry of Sports' 2024 National Health and Fitness Trends Survey highlighting personal trainers, weight loss exercises, and certified exercise professionals as key trends, driving sports nutrition consumption.

The Rest of South America, despite its current smaller market share, offers growth potential as fitness awareness spreads beyond urban areas. The region shows increasing adoption of healthy lifestyles, with sports nutrition products becoming integrated into daily wellness routines rather than remaining exclusive to athletes. E-commerce platforms are essential in market expansion across these countries, addressing traditional distribution limitations and providing consumers direct access to international brands. This digital shift enhances market education and product adoption, particularly in regions with limited specialty retail presence.

Competitive Landscape

The South American sports nutrition market demonstrates a moderately fragmented structure, with companies competing through protein specialization, distribution capabilities, and product innovation. Global corporations such as PepsiCo, Coca-Cola, and Nestlé S.A. utilize their extensive distribution networks and marketing resources to reach mainstream consumers. Meanwhile, specialized companies like Glanbia and Abbott target performance-oriented segments with scientifically formulated products.

The protein segment shows the most intense competition, where companies differentiate themselves through ingredient quality, bioavailability, and flavor innovation. Market opportunities emerge at the intersection of sports nutrition and related categories, including functional foods, personalized nutrition, and sustainable products.

Plant-based products present significant growth potential, particularly through zero-sugar protein drinks that combine performance benefits with health considerations. With players focusing on technology investments, it underpins competitive reshaping. Subscription e-commerce, CRM-driven personalization engines, and manufacturing automation enhance responsiveness to micro-segments. Players unable to integrate data loops into R&D risk losing relevance in the South America sports nutrition industry’s evolving value chain.

South America Sports Nutrition Industry Leaders

-

PepsiCo, Inc.

-

The Coca-Cola Company

-

Nestlé S.A.

-

Glanbia, Plc

-

Abbott Laboratories

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Nutrex introduced its first functional food product at the Arnold Sports Festival in Brazil. The company offers two flavors - Chocolate Brownie and Cookies and Cream - with each 50g bar containing 13g of protein.

- July 2024: NotCo introduced Not Shake Protein, a range of protein-enriched sports drinks. The product line features specialty flavors, including Banana Pancakes with Cinnamon and Strawberry with Dates, alongside traditional options such as chocolate, coffee caramel, and vanilla with coconut.

- April 2024: MuscleTech, a global sports nutrition supplement manufacturer, has established a strategic manufacturing and marketing partnership with Trust Group to facilitate its market expansion into Brazil.

- March 2024: Glanbia has launched a direct-to-consumer platform in Brazil, incorporating an algorithm to provide personalized product recommendations. This initiative aims to improve the shopping experience for Brazilian consumers by offering tailored suggestions based on their preferences and needs.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the South America sports nutrition market as retail and online sales of sports protein powders, ready-to-drink shakes, bars, and selected non-protein products formulated to improve athletic performance or support active lifestyles. The definition captures value generated within Brazil, Argentina, Chile, Colombia, Peru, and the remaining countries in the sub-continent, and it tracks finished-goods revenue at consumer price levels rather than ingredient trade.

Scope Exclusion: Therapeutic enteral feeds, infant formulas, and animal feed additives are outside the study scope.

Segmentation Overview

-

By Product Type

-

Sports Protein Products

-

Powder

- Whey And Casein Powder

- Plant based Protein Powder

- Other Sports Protein Powder

- Protein Ready to Drink

- Protein/Energy Bars

-

Powder

-

Sports Non Protein Products

- Energy Gels

- BCAA Powder

- Creatine Powder

- Other Sports Non Protein Products

-

Sports Protein Products

-

By Source

- Animal-based

- Plant-based

-

By Distribution Channel

- Supermarkets/Hypermarkets

- Pharmacy/Health Stores

- Online Retail Stores

- Other Distribution Channels

-

By Geography

- Brazil

- Chile

- Argentina

- Rest of South America

Detailed Research Methodology and Data Validation

Primary Research

Our analysts interviewed sports dietitians, specialty-store buyers, contract manufacturers, and e-commerce category managers across Brazil, Chile, and Argentina. These discussions validated consumption shifts toward plant proteins, typical retail margins, and the speed at which online channels gain share, thereby closing gaps left by secondary data and guiding assumption fine-tuning.

Desk Research

We first gathered publicly available statistics from bodies such as ANVISA's product registry, PAHO physical-activity surveys, Brazil's IBGE household budget studies, and IHRSA health-club membership data, which together outline demand drivers and price bands. Trade flows from UN Comtrade and shipment micro-data accessed through Volza helped us map import penetration of whey, BCAA, and creatine, while D&B Hoovers supplied high-level company revenue splits that anchor channel checks. Additional context came from regional sports federations, fiscal bulletins, and mainstream business press. The sources listed are illustrative only; many further documents were reviewed for cross-verification and clarification.

Market-Sizing & Forecasting

A top-down model starts with official retail sales series and import-export data, which are then adjusted for informal trade and converted into constant-currency values. Bottom-up checks, drawn from sampled supplier revenues and average selling price multiplied by volume calculations, temper the totals before finalization. Key variables include average spend per gym member, fitness-club penetration, whey import prices, discretionary income per capita, and e-commerce order frequency. We forecast through multivariate regression, linking these drivers to historical consumption patterns and expert consensus on regulatory shifts, and we use scenario analysis to test sensitivity around currency volatility.

Data Validation & Update Cycle

Outputs pass a two-tier analyst review that screens for anomalies against independent indicators such as energy-drink excise collections or protein import duties. Models refresh every twelve months, with interim updates triggered by major policy or macroeconomic events, and an analyst rechecks numbers just before report delivery so clients receive the latest view.

Why Mordor's South America Sports Nutrition Baseline Is Trusted

Published market values often diverge because firms select different geographic cuts, product baskets, and inflation treatments. According to Mordor Intelligence, clarity on these choices is the first step toward comparability.

Key gap drivers include some publishers bundling functional foods and vitamin tonics with sports nutrition, others valuing shipments at factory gate rather than retail, and a few extending the scope to all of Latin America, which inflates totals.

Our study reports consumer-level revenue for sports-specific products only and is refreshed annually, which keeps the baseline current.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.25 B (2025) | Mordor Intelligence | - |

| USD 4.60 B (2024) | Global Consultancy A | Includes functional foods and nutraceuticals alongside sports lines |

| USD 2.62 B (2025) | Industry Tracker B | Values sell-in shipments and omits Peru and Colombia retail markets |

These comparisons show that once scope and valuation points are aligned, our 1.25 billion baseline sits at the center of a credible range, giving decision-makers a balanced figure grounded in transparent variables and repeatable steps.

Key Questions Answered in the Report

What is the current value of the South America sports nutrition market?

The South America sports nutrition market is valued at USD 1.36 billion in 2026.

Which country leads spending on sports nutrition in South America?

Brazil commands 83.25% of regional revenue and is also the fastest-growing country market at a 9.08% CAGR through 2031.

Are plant-based proteins gaining ground on whey in South America?

Yes. Plant-based alternatives are projected to grow at a 9.88% CAGR, faster than any other protein source—thanks to improved taste profiles and sustainability appeal.

How big is e-commerce in regional supplement sales?

Online retail already accounts for 14.92% of the category’s revenue and is forecast to expand at a 10.06% CAGR, making it the leading growth channel.

Page last updated on: