South America Pet Diet Market Size and Share

Market Overview

| Study Period | 2018 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

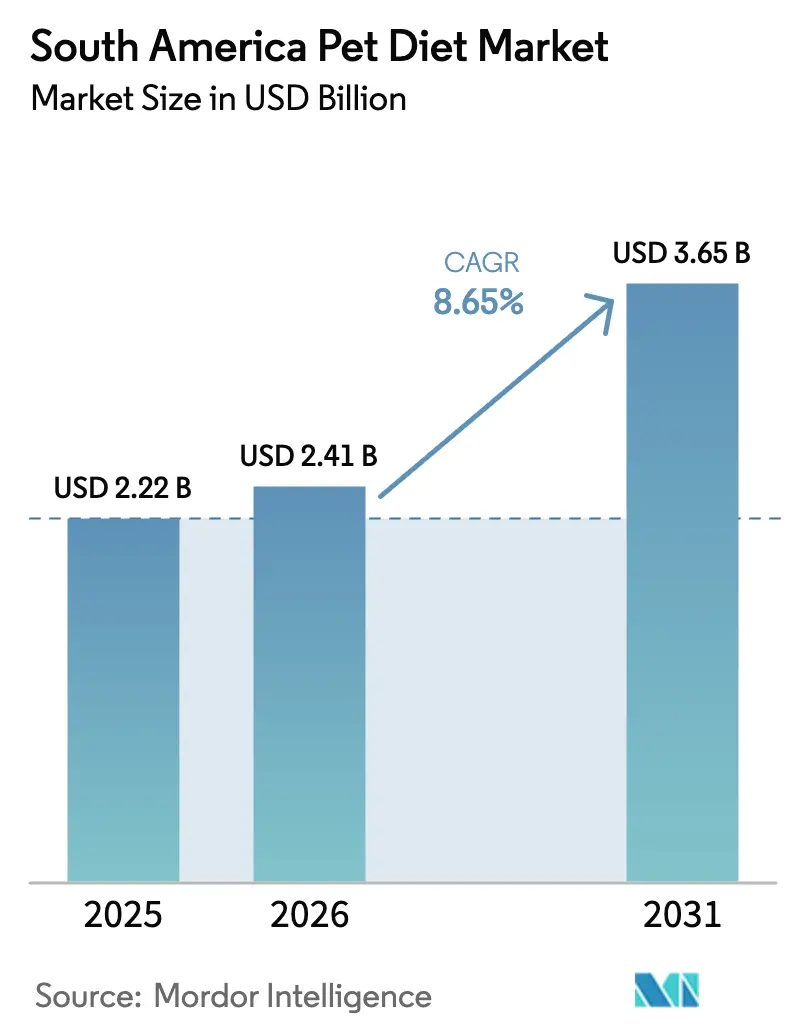

| Base Year Market Size (2025) | USD 2.22 Billion |

| Market Size (2026) | USD 2.41 Billion |

| Market Size (2031) | USD 3.65 Billion |

| Growth Rate (2026 - 2031) | 8.65% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Pet Diet Market Analysis by Mordor Intelligence

The South America pet diet market size is expected to grow from USD 2.22 billion in 2025 to USD 2.41 billion in 2026 and is forecast to reach USD 3.65 billion by 2031 at 8.65% CAGR over 2026-2031. This expansion underscores how premiumization, veterinarian-led prescription habits, and robust e-commerce ecosystems all converge to propel market size forward. Rising disposable incomes in Brazil, Argentina, and Chile let owners transition from conventional fare toward purpose-built therapeutic formulations. Regulatory debate on tax relief, coupled with a regional push to localize high-value ingredients, boosts affordability and supply chain resilience. Meanwhile, strategic acquisitions and capacity additions illustrate an increasingly competitive yet opportunity-rich landscape for global and domestic brands eager to scale in therapeutic niches within the South America pet diet market.

Key Report Takeaways

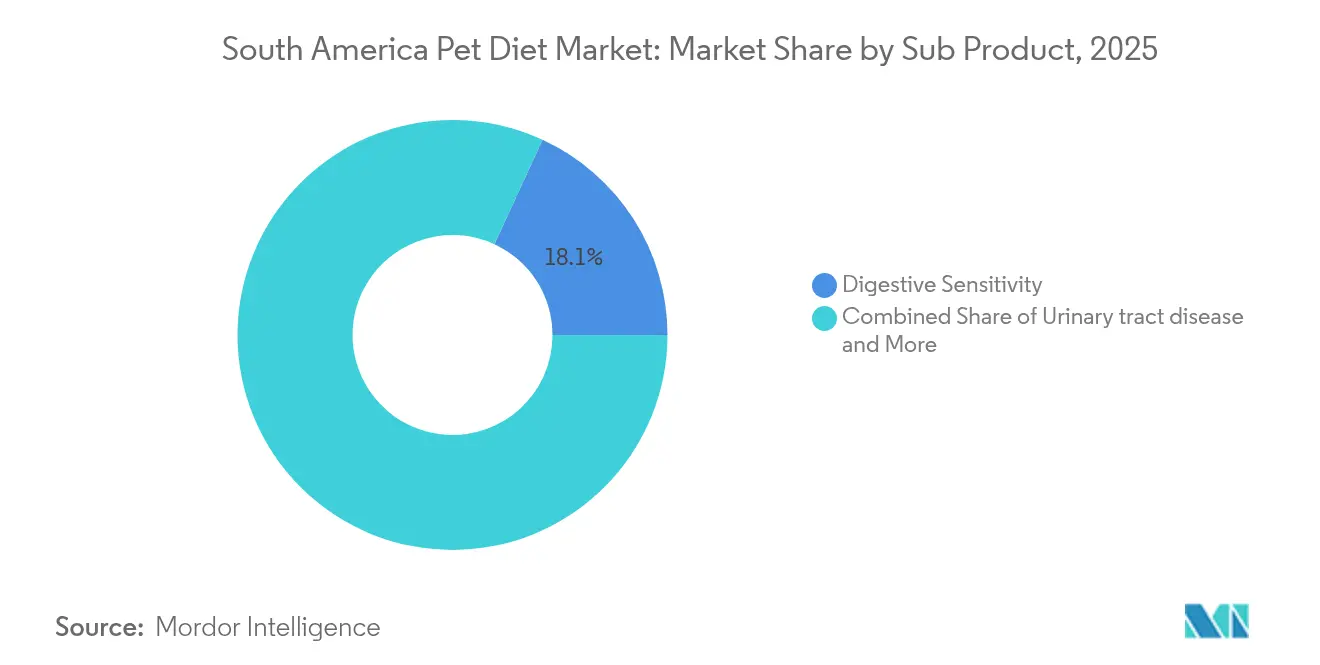

- By sub-product, digestive sensitivity diets accounted for 18.12% of the South America pet diet market share in 2025, whereas urinary tract disease diets are projected to grow at the fastest rate, with a 9.15% CAGR through 2031.

- By pets, dogs captured 56.63% of the South America pet diet market size in 2025, while cats are projected to log a superior 9.95% CAGR to 2031.

- By distribution channel, specialty stores accounted for 34.12% of the revenue in 2025, and online platforms are projected to post the highest CAGR of 11.35% by 2031.

- By geography, Brazil accounted for 59.02% of regional revenue in 2025 and is projected to expand at a 9.55% CAGR over the same period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South America Pet Diet Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating premiumization and humanization of pets | +2.1% | Brazil, Argentina, Chile | Medium term (2-4 years) |

| Veterinarian-led prescription uptake for chronic diseases | +1.8% | Global, strongest in urban centers | Long term (≥ 4 years) |

| Rapid expansion of e-commerce and DTC (Direct-to-Consumer) fulfillment | +1.5% | Brazil, Colombia, Argentina | Short term (≤ 2 years) |

| Tax-reform talks lowering effective pet-food VAT (Value Added Tax) | +1.2% | Brazil primarily | Medium term (2-4 years) |

| Local ingredient biorefineries cutting therapeutic-diet costs | +0.9% | Brazil, Argentina | Long term (≥ 4 years) |

| Surging clinical nutrition R&D partnerships | +0.7% | Regional, concentrated in Brazil | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerating premiumization and humanization of pets

Pet humanization drives the adoption of therapeutic diets as owners increasingly view their pets as family members requiring specialized nutrition. Argentina and Brazil lead South America in premium segment penetration, with Argentina's premium dog food market accounting for 8% of total volume. In the Pet Food Industry, Alican holds approximately a 14% share of the premium segment. Consumer willingness to invest in health-focused formulations creates opportunities for functional benefits, including digestive support, dental care, and weight management. This trend correlates with rising urbanization rates in major markets, such as Colombia, where middle-class households earning above USD 20,000 annually are projected to increase.

Veterinarian-led prescription uptake for chronic diseases

Veterinary prescription patterns increasingly favor therapeutic diets for managing chronic conditions, including renal disease, diabetes, and obesity in aging pet populations. Clinical studies from Brazilian veterinary institutions have demonstrated the efficacy of specialized formulations in managing urinary tract diseases and digestive sensitivities, thereby supporting prescription compliance rates in metropolitan areas. Royal Canin Academy's South American regional expertise, anchored by Argentina-based staff, facilitates knowledge transfer and prescription protocols across the region. Prescriber compliance remains limited outside Tier-1 metropolitan areas, creating geographic disparities in therapeutic diet adoption rates.

Rapid expansion of e-commerce and DTC (Direct-to-Consumer) fulfillment

Digital commerce transformation accelerates therapeutic diet accessibility through enhanced last-mile delivery and subscription models. Brazil's e-commerce infrastructure supports direct-to-consumer fulfillment, with online channels demonstrating a 12.1% CAGR through 2030. Mercado Libre's dominance in South American e-commerce provides established platforms for distributing pet food, while social media channels enable targeted marketing for specialized therapeutic formulations. Colombian market dynamics illustrate this trend, with formal retailers accounting for more than half of food distribution and expanding e-commerce capabilities.

Tax-reform talks lowering effective pet-food VAT (Value Added Tax)

Brazil's tax reform discussions aim to address the pet food industry's substantial tax burden, which currently stands at approximately 50%, compared to 7-20% for basic foods. Industry advocates seek reclassification of pet food to reduce effective VAT rates, potentially improving affordability and market access for therapeutic diets[1]Source: Nicole Kerwin, “USDA: Colombian market bodes well for US pet food exports,” Pet Food Processing, petfoodprocessing.net. The reform timeline remains uncertain, but successful implementation could significantly impact pricing structures and consumer adoption rates. USDA analysis indicates Brazil's pet food sector is among the most heavily taxed nationally, creating competitive disadvantages versus conventional pet food categories.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High retail price versus conventional pet food | -1.4% | Global, acute in price-sensitive segments | Medium term (2-4 years) |

| Stringent MAPA (Ministry of Agriculture, Livestock and Food Supply) product-registration process | -1.1% | Brazil, affecting regional exports | Long term (≥ 4 years) |

| Low prescriber compliance outside Tier-1 metro areas | -0.8% | Rural areas across South America | Long term (≥ 4 years) |

| Fragmented cold-chain for wet therapeutic diets | -0.6% | Regional, especially interior markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Retail Price Versus Conventional Pet Food

Therapeutic diets command premium pricing that can be two to three times higher than conventional pet food, creating affordability barriers for price-sensitive consumers across South America. Brazil's pet food sector faces additional cost pressures from tax burdens approaching 50%, compared to 7-20% for basic foods, making therapeutic diets particularly expensive relative to standard options. Economic volatility and currency devaluation in regional markets further exacerbate affordability constraints, particularly affecting middle-income pet owners who represent the primary growth opportunity for the adoption of therapeutic diets.

Stringent MAPA (Ministry of Agriculture, Livestock and Food Supply) Product Registration Process

Brazil's Ministry of Agriculture, Livestock and Supply (MAPA) maintains rigorous product registration requirements through the system, creating lengthy approval timelines and compliance costs for therapeutic diet manufacturers. The registration process requires extensive documentation, including nutritional analysis, manufacturing protocols, labeling compliance, and facility certifications, with approval cycles often extending 12-18 months. International manufacturers face additional complexity navigating Brazilian regulatory requirements, while smaller regional producers struggle with compliance costs and technical documentation requirements. These barriers limit the speed of product innovation and market entry for specialized therapeutic formulations, particularly affecting novel ingredients and advanced nutritional technologies that require extensive safety validation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sub Product: Digestive Sensitivity Dominance with Urinary Tract Up-Swing

Digestive sensitivity formulas accounted for 18.12% of 2025 revenue, the largest share of the South America pet diet market size. Clinical proof points and owner recognition of gastrointestinal symptoms underpin elevated reorder rates. Urinary tract solutions exhibit a 9.15% CAGR, propelled by feline urolithiasis awareness campaigns and growing cat ownership clusters across Brazilian and Chilean metros. R&D pipelines also prioritize renal and diabetes care, anchoring multi-brand portfolios while extending therapeutic reach. Obesity-management and oral-care diets ride preventive-health currents, offering cross-category growth avenues that augment overall South America pet diet market potential.

Second-generation products utilize hydrolyzed proteins, fiber blends, and functional botanicals to enhance palatability without compromising the integrity of the prescription. Local ingredient biorefineries lessen import exposure for taurine, omega-3s, and specialized fibers, strategically positioning regional manufacturers to shave costs and accelerate time-to-market. Collectively, these innovations solidify sub-product diversity and augment value capture within the South America pet diet market.

By Pets: Dogs Lead, Cats Accelerate

Dogs maintain market leadership with a 56.63% share in 2025, supported by South America's substantial canine population and established veterinary prescription practices for therapeutic diets. Brazil's dog population represents the primary market opportunity, with therapeutic diet adoption concentrated in metropolitan areas, where veterinary compliance rates exceed those in rural regions. Argentine market dynamics illustrate this pattern, with Alican targeting premium dog food segments representing 8% of the national market.

Cats demonstrate superior growth momentum at 9.95% CAGR through 2031, reflecting evolving pet ownership patterns and increasing recognition of feline-specific nutritional requirements. Brazil's cats represent a significant untapped potential, particularly for urinary tract and renal management diets that address breed-specific health challenges. Other pets, including exotic and small animals, constitute emerging segments supported by the expansion of veterinary specialization and diversification trends in urban pet ownership.

By Distribution Channel: Specialty Reigns, Online Surges

Specialty stores maintain market leadership with a 34.12% share in 2025, leveraging their veterinary relationships and specialized product knowledge, which is essential for making therapeutic diet recommendations. These channels offer critical consultation services and prescription validation, particularly important for complex therapeutic formulations that require professional guidance. Independent pet shops and veterinary clinics dominate this segment, though consolidation trends favor larger specialty chains with enhanced inventory management capabilities.

Online channels are projected to demonstrate the fastest growth at a 11.35% CAGR through 2031, driven by enhanced last-mile delivery capabilities and direct-to-consumer subscription models. Brazil's e-commerce infrastructure supports this expansion, with digital platforms enabling targeted marketing for specialized therapeutic diets and automated reorder systems improving customer retention. Supermarkets and hypermarkets maintain a significant presence through convenience and accessibility, while other channels, including convenience stores, serve price-sensitive segments with basic therapeutic diet options.

Geography Analysis

Brazil dominated the South America pet diet market with 59.02% in 2025, driven by a strong pet population and an annual production capacity exceeding 4.2 million metric tons. High urbanization, robust veterinary networks, and anticipated VAT relief are anticipated to propel the market toward a 9.55% CAGR through 2031. Key manufacturers, including BRF Pet, Special Dog, and Premier Pet, are aggressively adding extrusion lines, wet-food retorts, and cold-chain hubs to defend their share and upgrade their therapeutic portfolios.

Argentina trails as the second-largest territory, where premium dog food already accounts for a good share of the volume. Vitalcan’s Tierra del Fuego plant and Alican’s expansion project, aimed at high export penetration, testify to ongoing capacity scale-up. Wet therapeutic penetration remains thin, underscoring a sizable runway for canned and pouch formulations across the South America pet diet market.

Chile, Colombia, Peru, and their contiguous countries jointly account for the remaining share, yet still achieve brisk adoption rates. Colombia’s dog and cat food market, valued at a good rate in 2024, benefits from duty-free access under the U.S.-Colombia Trade Promotion Agreement. As pet ownership rises from 25% to 30% of households, formal retail chains and e-commerce incumbents are collaborating to increase the penetration of premium and therapeutic offerings throughout the South American pet diet market.

Competitive Landscape

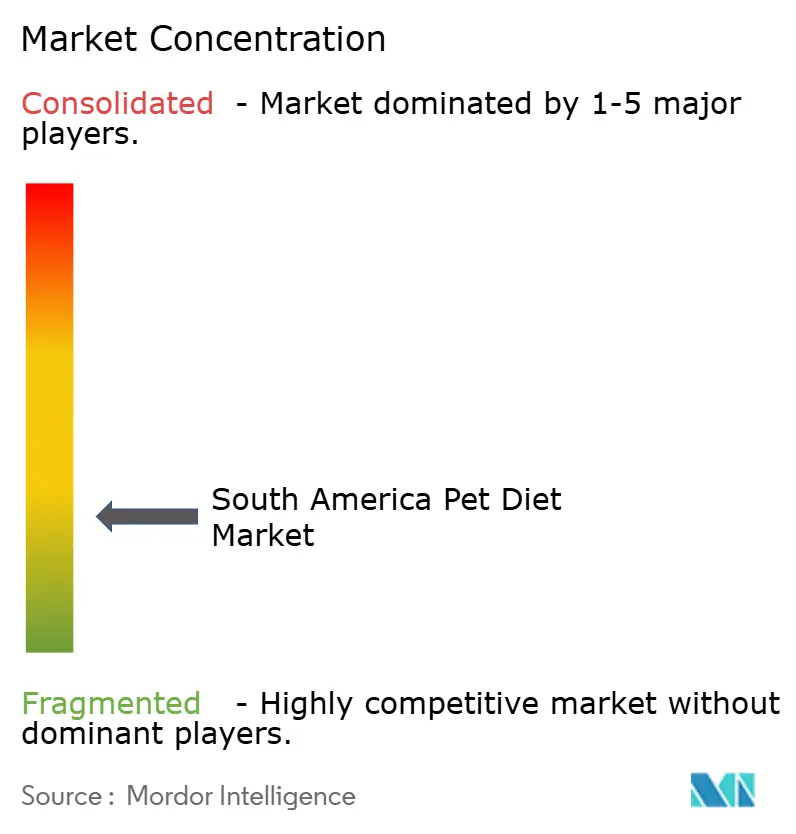

The South America Pet Diet Market is shaping a low-concentration arena. BRF’s 2021 purchase of Hercosul and Mogiana vaulted the company. Top brands collectively captured a minor share of the revenue in 2024, reflecting a low level of concentration in the South America pet diet market. Strategic M&A continues as players pursue scale, negotiate ingredient contracts, and expand distribution capabilities across multi-country networks.

Technology adoption is equally pivotal. Kemin’s laboratory investment enhances on-site chromatographic testing, enabling the creation of custom micro-ingredient blends. Corbion’s algae expansion in Brazil anchors the local supply of long-chain omega-3s for renal and cardiac diets[3]Source: Corbion nv, “Corbion Annual Report 2024,” corbion.com. Formulation science increasingly incorporates novel proteins such as those from black soldier fly, pea, and fava to achieve amino-acid targets while trimming carbon footprints, marking a differentiator in premium therapeutic SKUs within the South America pet diet market.

Marketing and channel strategies tilt toward omnichannel engagement. Premier Pet and Special Dog harness influencer partnerships, as well as tele-consultation platforms, to reinforce prescription adherence. Newcomers leverage D2C models to capture subscription revenue, while legacy brands pilot click-and-collect programs. Competitive dynamics therefore hinge on innovation cadence, supply-chain agility, and the capacity to satisfy both veterinarian and consumer expectations in the South America pet diet market.

South America Pet Diet Industry Leaders

BRF Global

Colgate-Palmolive Company (Hill's Pet Nutrition Inc.)

Mars Incorporated

Nestle (Purina)

Alltech

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Alimentos Prosalud opened a USD 10 million pet food production facility in Costa Rica with 500,000 daily canned unit capacity, targeting premium wet pet food exports to over 20 countries including the United States, Canada, Spain, and Germany.

- March 2023: Colgate-Palmolive Company's pet care subsidiary Hill’s Pet Nutrition launched its new line of prescription diets to support pets diagnosed with cancer. This prescription line, Diet ONC Care, offers complete and balanced formulas in both dry and wet forms for cats and dogs.

- January 2023: Mars Incorporated partnered with the Broad Institute to create an open-access database of dog and cat genomes to advance preventive pet care. It is aimed at developing more effective precision medicines and diets that lead to scientific breakthroughs for the future of pet health.

South America Pet Diet Market Report Scope

Diabetes, Digestive Sensitivity, Oral Care Diets, Renal, Urinary tract disease are covered as segments by Sub Product. Cats, Dogs are covered as segments by Pets. Convenience Stores, Online Channel, Specialty Stores, Supermarkets/Hypermarkets are covered as segments by Distribution Channel. Argentina, Brazil are covered as segments by Country.| Derma Diets |

| Diabetes |

| Digestive Sensitivity |

| Obesity Diets |

| Oral Care Diets |

| Renal |

| Urinary tract disease |

| Other Veterinary Diets |

| Cats |

| Dogs |

| Other Pets |

| Convenience Stores |

| Online Channel |

| Specialty Stores |

| Supermarkets/Hypermarkets |

| Other Channels |

| Brazil |

| Argentina |

| Rest of South America |

| By Sub Product | Derma Diets |

| Diabetes | |

| Digestive Sensitivity | |

| Obesity Diets | |

| Oral Care Diets | |

| Renal | |

| Urinary tract disease | |

| Other Veterinary Diets | |

| By Pets | Cats |

| Dogs | |

| Other Pets | |

| By Distribution Channel | Convenience Stores |

| Online Channel | |

| Specialty Stores | |

| Supermarkets/Hypermarkets | |

| Other Channels | |

| By Geography | Brazil |

| Argentina | |

| Rest of South America |

Market Definition

- FUNCTIONS - Pet foods are usually intended to provide complete and balanced nutrition to the pet but are primarily used as functional products. The scope includes the food and supplements consumed by pets including veterinary diets. Supplements/nutraceuticals that are directly supplied to pets are considered within the scope.

- RESELLERS - Companies engaged in reselling of pet food without value addition have been excluded from the market scope, in order to avoid double counting.

- END CONSUMERS - Pet owners are considered to be the end-consumers in the market studied.

- DISTRIBUTION CHANNELS - Supermarkets/hypermarkets, specialty stores, convenience stores, online channels and other channels are considered within the scope. The stores which are exclusively providing pet related basic and custom products are considered within the scope of specialty stores.

| Keyword | Definition |

|---|---|

| Pet Food | The scope of pet food includes the food that is eatable by pets including food, treats, veterinary diets, and nutraceuticals/supplements. |

| Food | Food is animal feed intended for consumption by pets. It is formulated to provide essential nutrients and meet the dietary needs of various types of pets, including dogs, cats, and other animals. These are generally segmented into dry and wet pet foods. |

| Dry Pet Food | Dry pet foods may be extruded/baked (kibbles) or flaked. They have a lower moisture content, typically around 12-20%. |

| Wet Pet Food | Wet pet food, also known as canned pet food or moist pet food, generally has a higher moisture content compared to dry pet food, often ranging from 70-80%. |

| Kibbles | Kibbles are dry, processed pet food in small, bite-sized pieces or pellets. They are specifically formulated to provide balanced nutrition for various domestic animals, such as dogs, cats, and other animals. |

| Treats | Pet Treats are special food items or rewards given to pets, to show affection, and encourage good behavior. They are especially used during training. Pet treats are made from various combinations of meat or meat-derived materials with other ingredients. |

| Dental Treats | Pet dental treats are specialized treats that are formulated to promote good oral hygiene in pets. |

| Crunchy Treats | It is a type of pet treat that has a firm and crispy texture which can be a good source of nutrition for pets. |

| Soft and chewy treats | Soft and Chewy pet treats are a type of pet food product that is formulated to be easy to chewy and digest. They are usually made from soft and pliable ingredients, such as meat, poultry, or vegetables, that have been blended and formed into bite-sized pieces or strips. |

| Freeze-dried & Jerky Treats | Freeze-dried and jerky treats are snacks given to pets, that are prepared through a special preservation process, without damaging the nutritional content, resulting in long-lasting, nutrient-rich treats. |

| Urinary Tract Disease Diets | These are commercial diets that are specifically formulated to promote urinary health and reduce the risk of urinary tract infections and other urinary problems. |

| Renal Diets | These are specialized pet foods formulated to support the health of pets with kidney disease or renal insufficiency. |

| Digestive Sensitivity Diets | Digestive-sensitive diets are specially formulated to meet the nutritional needs of pets with digestive issues such as food intolerances, allergies, and sensitivities. These diets are designed to be easily digestible and to reduce the symptoms of digestive problems in pets. |

| Oral Care Diets | Oral care diets for pets are specially formulated diets produced to promote oral health and hygiene in pets. |

| Grain-Free Pet Food | Pet food that does not contain common grains like wheat, corn, or soy. Grain-free diets are often preferred by pet owners seeking alternative options or if their pets have specific dietary sensitivities. |

| Premium Pet Food | High-quality pet food formulated with superior ingredients often offers additional nutritional benefits compared to standard pet food. |

| Natural Pet Food | Pet food made from natural ingredients, with minimal processing and without artificial preservatives. |

| Organic Pet Food | Pet food is produced using organic ingredients, free from synthetic pesticides, hormones, and genetically modified organisms (GMOs). |

| Extrusion | A manufacturing process used to produce dry pet food, where ingredients are cooked, mixed, and shaped under high pressure and temperature. |

| Other Pets | Other pets include birds, fish, rabbits, hamsters, ferrets, and reptiles. |

| Palatability | The taste, texture, and aroma of pet food influence its appeal and acceptance by pets. |

| Complete and Balanced Pet Food | Pet food that provides all essential nutrients in appropriate proportions to meet the nutritional needs of pets without additional supplementation. |

| Preservatives | These are the substances that are added to pet food to extend its shelf life and prevent spoilage. |

| Nutraceuticals | Food products that offer health benefits beyond basic nutrition, often contain bioactive compounds with potential therapeutic effects. |

| Probiotics | Live beneficial bacteria that promote a healthy balance of gut flora, supporting digestive health and immune function in pets. |

| Antioxidants | Compounds that help neutralize harmful free radicals in the body, promoting cellular health and supporting the immune system in pets. |

| Shelf-Life | The duration of which pet food remains safe and nutritionally viable for consumption after its production date. |

| Prescription diet | Specialized pet food formulated to address specific medical conditions under veterinary supervision. |

| Allergen | A substance that can cause allergic reactions in some pets, leading to food allergies or sensitivities. |

| Canned food | Wet pet food that is packed in cans and contains higher moisture content than dry food. |

| Limited ingredient diet (LID) | Pet food formulated with a reduced number of ingredients to minimize potential allergens. |

| Guaranteed Analysis | The minimum or maximum levels of certain nutrients present in pet food. |

| Weight management | Pet food designed to help pets maintain a healthy weight or support weight loss efforts. |

| Other Nutraceuticals | It includes prebiotics, antioxidants, digestive fiber, enzymes, essential oils and herbs. |

| Other Veterinary Diets | It includes weight management diets, skin and coat health, cardiac care, and joint care. |

| Other Treats | It includes rawhides, mineral blocks, lickables, and catnips. |

| Other Dry Foods | It includes cereal flakes, mixers, meal toppers, freeze-dried foods, and air-dried foods. |

| Other Animals | It includes birds, fish, reptiles, and small animals (rabbits, ferrets, hamsters). |

| Other Distribution Channels | It includes veterinary clinics, local unregulated stores, and feed and farm stores. |

| Proteins and Peptides | Proteins are large molecules composed of basic units called amino acids which help in the growth and development of pets. Peptides are the short string of 2 to 50 amino acids. |

| Omega-3 fatty acids | Omega-3 fatty acids are essential polyunsaturated fats that play a crucial role in the overall health and well-being of Pets |

| Vitamins | Vitamins are the essential organic compounds that are essential for vital physiological functioning. |

| Minerals | Minerals are naturally occurring inorganic substances that are essential for various physiological functions in pets. |

| CKD | Chronic Kidney Disease |

| DHA | Docosahexaenoic Acid |

| EPA | Eicosapentaenoic Acid |

| ALA | Alpha-linolenic Acid |

| BHA | Butylated Hydroxyanisol |

| BHT | Butylated Hydroxytoluene |

| FLUTD | Feline Lower Urinary Tract Disease |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: IDENTIFY KEY VARIABLES: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms