Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 2.78 Billion |

| Market Size (2026) | USD 2.9 Billion |

| Market Size (2031) | USD 3.55 Billion |

| Growth Rate (2026 - 2031) | 4.15% CAGR |

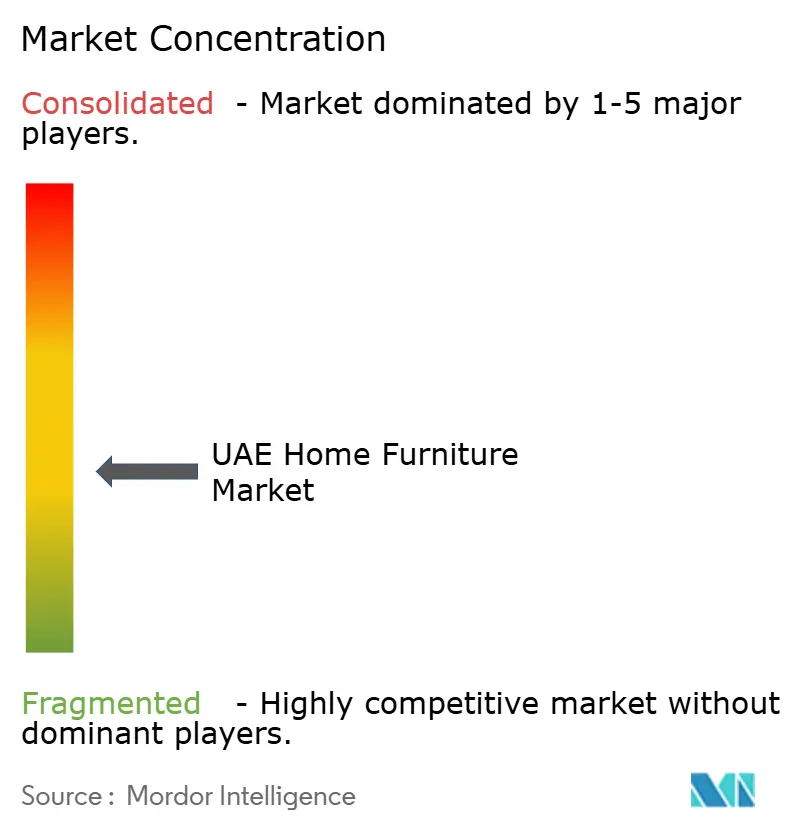

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

UAE Home Furniture Market Analysis by Mordor Intelligence

The UAE home furniture market size was valued at USD 2.78 billion in 2025 and estimated to grow from USD 2.9 billion in 2026 to reach USD 3.55 billion by 2031, at a CAGR of 4.15% during the forecast period (2026-2031). This growth is propelled by a surge in residential handovers across Dubai and Abu Dhabi, the ongoing hospitality boom, and government-led industrial policies that encourage local manufacturing and supply-chain localization. Rising demand for flexible living solutions, such as rent-to-furnish packages and subscription services, accelerates purchase cycles and deepens market penetration among transient residents. Luxury villa completions on Palm Jumeirah and Emirates Hills fuel premium furniture sales, while mid-range offerings retain mass-market appeal due to competitive pricing and financing options. At the same time, sustainability mandates from Dubai Municipality spur interest in circular design and recycled materials that reshape product innovation across the value chain[1]Source: Dubai Municipality, “Circular Design Guidelines,” dubai.gov.ae..

Key Report Takeaways

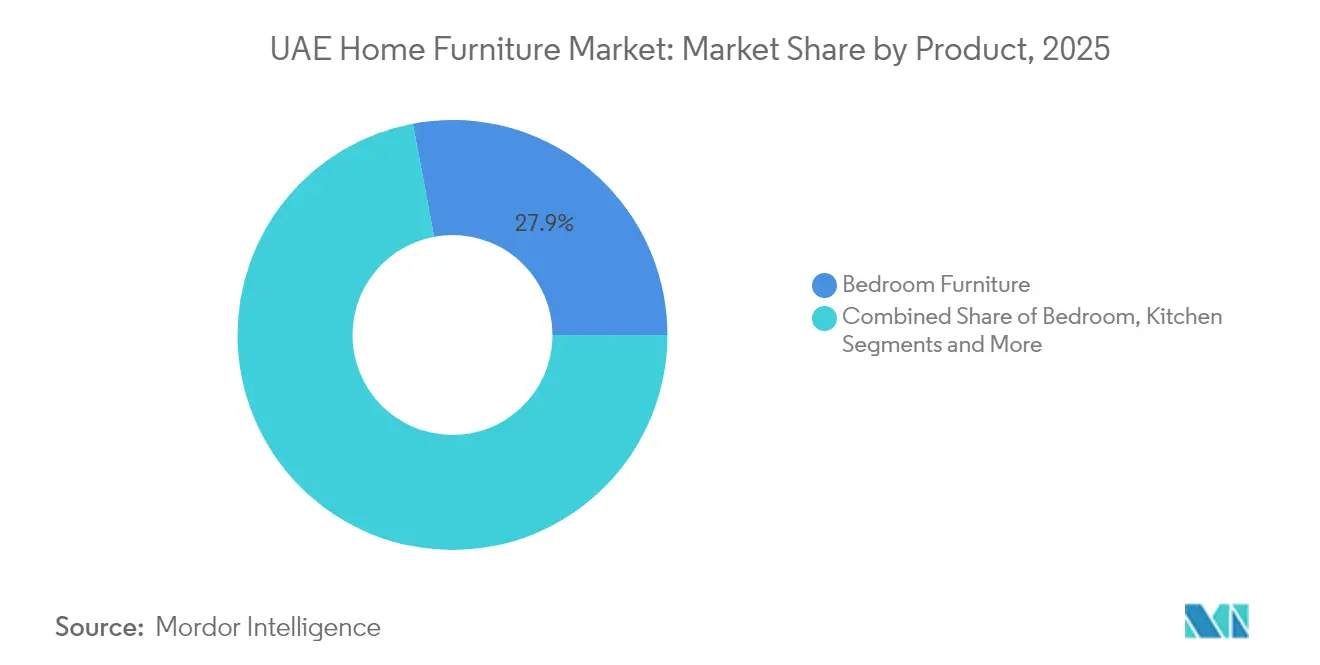

- By product, bedroom furniture held 27.95% of the UAE home furniture market share in 2025, while kitchen furniture is forecast to register a 5.46% CAGR through 2031.

- By material, wood dominated with 69.98% of the UAE home furniture market size in 2025, but metal furniture is set to expand at a 5.21% CAGR to 2031 .

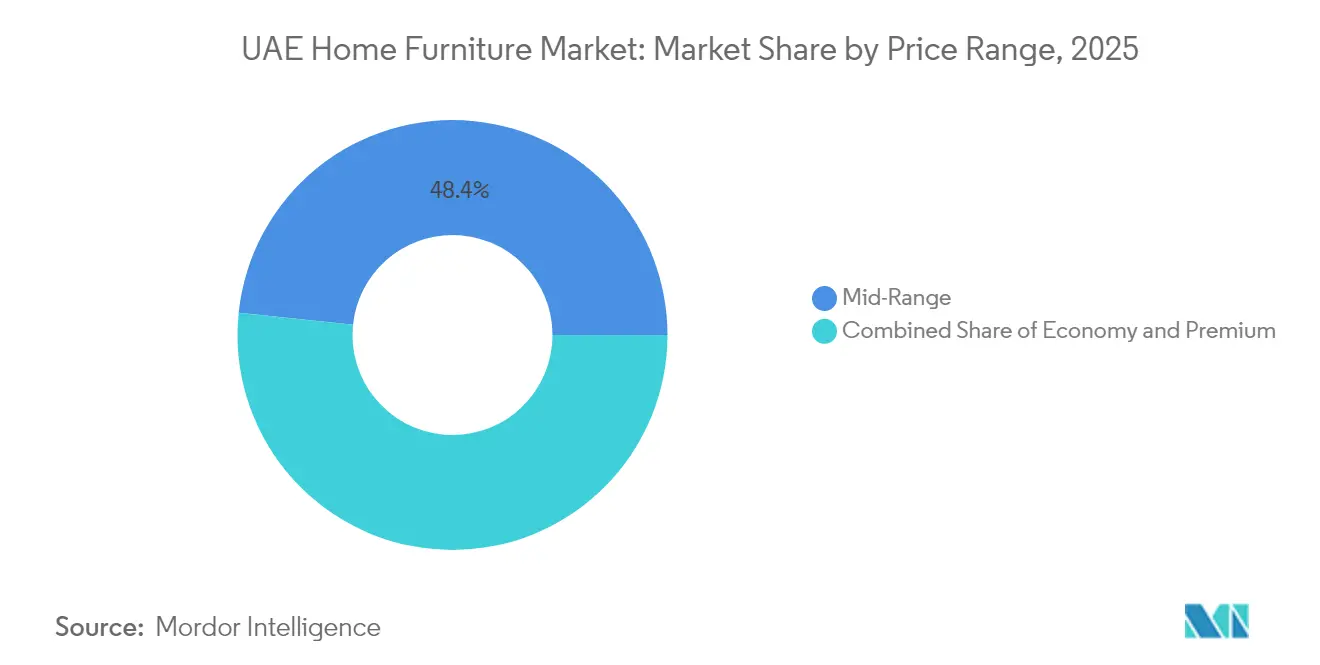

- By price range, mid-range offerings accounted for 48.35% of the UAE home furniture market size in 2025, whereas premium furniture is projected to advance at a 5.78% CAGR through 2031.

- By distribution channel, specialty stores retained 43.92% revenue share in 2025; the online channel is poised for the fastest expansion at 6.83% CAGR to 2031.

- By geography, Dubai led with 40.88% revenue share in 2025, while the Northern Emirates are on track to post the quickest 5.49% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

UAE Home Furniture Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Post-pandemic residential refurbishments | +0.8% | Dubai, Abu Dhabi, Sharjah | Short term (≤ 2 years) |

| Growing hospitality & vacation-home pipeline | +1.2% | Dubai, Abu Dhabi luxury corridors | Medium term (2-4 years) |

| Operation 300bn and related manufacturing incentives | +0.6% | Nationwide, with hubs in Dubai Industrial City | Long term (≥ 4 years) |

| Rent-to-furnish and subscription models | +0.9% | Dubai Marina, JBR, Downtown; expanding to Abu Dhabi | Medium term (2-4 years) |

| Ultra-luxury villa handovers on Palm Jumeirah | +0.4% | Palm Jumeirah, Emirates Hills | Short term (≤ 2 years) |

| Circular-design mandates from Dubai Municipality | +0.3% | Dubai, potential federal rollout | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Boom in Post-Pandemic Residential Refurbishments

A 34% jump in Dubai real-estate sales value to AED 151 billion in 2024 signaled robust housing turnover that translated into fresh furniture demand[2]Source: DAMAC Properties, “Dubai Property Sales 2024,” damacproperties.com. Many buyers now prioritize home-office setups and multifunctional pieces to support hybrid work lifestyles, increasing average ticket sizes across bedroom and living-room categories. Rising rents—18% for short-term and 13% for long-term leases—nudge residents toward ownership, triggering complete refurnishing cycles for newly acquired units. Population growth above 12% adds incremental households that purchase full suites rather than piecemeal items. This momentum favors the UAE home furniture market by stabilizing baseline demand even amid global macroeconomic uncertainty.

Growing Hospitality & Vacation-Home Pipeline

More than 40 hotels slated through 2025 will inject over 10,100 rooms into Dubai’s inventory, while Abu Dhabi’s cultural tourism projects deepen commercial furniture requirements[3]Source: Elite Properties, “Dubai Hospitality Pipeline,” eliteproperties.ae. Luxury and upper-upscale properties already constitute 67% of Dubai’s stock, so procurement budgets lean toward premium fixtures that elevate guest experience. Hotel occupancy reaching 78% in H1 2024 confirms revenue recovery and justifies continued capital expenditure on bespoke furnishings. Vacation-home investors in waterfront communities furnish repeatedly to secure higher nightly rates, creating repeat business for manufacturers. Together, hospitality and vacation homes lift wholesale order volumes and diversify revenue streams beyond straightforward residential sales.

Government Incentives for Local Manufacturing

The UAE’s plan to lift manufacturing’s GDP share from AED 133 billion to AED 300 billion by 2031 allocates financing, land leases, and R&D grants that directly lower entry barriers for domestic furniture producers[4]Source: Emirates News Agency, “Operation 300bn Progress Update,” wam.ae. Dubai Industrial City’s roadmap envisions 500 factories by 2026, offering plug-and-play infrastructure that reduces capex for new joinery and metal-work plants. Preferential public procurement rules under the “Make it in the Emirates” banner grant local goods favored status, bolstering sales pipelines. Increased R&D funding accelerates the development of eco-friendly laminates and smart furniture that integrate charging ports and IoT sensors. Over time, these interventions elevated regional self-sufficiency and shielded the UAE home furniture market from external supply shocks.

Rise of Rent-to-Furnish & Furniture-Subscription Models

Companies such as TUKA Dubai report double-digit monthly growth by leasing curated room packages that suit quick-turn expat rentals. Blueground’s USD 20 million allocation toward its Dubai expansion underscores institutional faith in furniture-as-a-service profitability. With 60% of Dubai residents relocating within three years, flexibility ranks high, and subscription solutions mitigate upfront costs while satisfying design aspirations. Corporate demand from multinationals setting up regional headquarters assures stable utilization rates, improving unit economics. These models also advance sustainability goals by prolonging product life cycles via refurbishment and rotation, a factor increasingly valued by regulators and consumers alike.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising hardwood import tariffs & logistics costs | -0.7% | Nationwide, heavier in Dubai & Abu Dhabi luxury | Short term (≤ 2 years) |

| Fragmented unorganized carpentry sector | -0.5% | Northern Emirates, Sharjah | Medium term (2-4 years) |

| Volatile expatriate churn affecting demand predictability | -0.4% | Dubai, Abu Dhabi, all Emirates | Long term (≥ 4 years) |

| Price-sensitive mass segment shifting to second-hand platforms | -0.3% | Dubai Marina, Sharjah, Ajman | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Hardwood Import Tariffs & Logistics Costs

Implementation of a revised Integrated Customs Tariff expanded product codes to 13,400, adding compliance complexity and modestly increasing clearing fees for importers. Standard 5% duties levied on CIF values now interact with elevated container rates that persist well above 2019 baselines, squeezing retailer margins. Wood imports totaling USD 1.17 billion in 2023, with China as the top supplier, expose buyers to currency swings and geopolitical risk. Courier-shipment duty-free thresholds fell from AED 970 to AED 300, raising landed costs on small-parcel e-commerce orders and accessory items. Mid-range and economy segments feel the brunt because price elasticities limit their ability to pass on cost increases.

Fragmented Unorganized Carpentry Sector Limiting Scalability

Thousands of small workshops deliver customized joinery yet often lack standardized processes, driving inconsistent product quality and longer lead times. Informal labor arrangements restrict access to bank financing and industrial-zone leases that would permit mechanization. Regulatory compliance costs tied to Dubai Municipality’s handling and safety codes challenge micro-operators with limited capital reserves. Skill-development programs remain sporadic, leaving persistent gaps in advanced finishing techniques essential for premium and export-grade furniture. Fragmentation therefore caps sector-wide productivity and slows the transition toward internationally competitive manufacturing clusters.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Bedroom Dominance Drives Market Foundation

Bedroom furniture captured 27.95% of the UAE home furniture market size in 2025, underscoring consumers’ emphasis on private living spaces and cultural norms prioritizing restful environments. Luxury villa completions deliver turnkey master-suite packages, while apartment developments target modular wardrobes and multifunctional beds that maximize space. Kitchen furniture leads to growth with a 5.46% CAGR due to rising culinary enthusiasm and smart-appliance integration that necessitates custom cabinetry. Living-room and dining-room sets ride the hospitality boom, supplying serviced apartments and vacation rentals with cohesive aesthetics. Home-office lines maintain post-pandemic momentum as flexible working policies become entrenched.

Sustained bedroom demand stems from robust housing turnover and high rental yields that encourage owners to furnish attractively for tenants. Kitchen innovation features antimicrobial surfaces and space-saving units, aligning with health and wellness priorities in the UAE home furniture market. Outdoor sets employ weather-resistant alloys and UV-stable fabrics to suit villa terraces and hotel pool decks, factors that justify premium pricing. Bathroom furniture remains niche but benefits from upscale hotel standards that influence residential aspirational buying. Multifunctional “other” pieces such as sofa-beds and expandable tables cater to expatriates who prefer adaptable layouts during short leases.

By Material: Wood Heritage Meets Metal Innovation

Wood retained 69.98% share of the UAE home furniture market size in 2025, reflecting established customer familiarity and versatile design appeal. Supply-chain pressures and eco-label requirements foster experimentation with engineered panels and reclaimed hardwood varieties that satisfy circular directives. Metal furniture is forecast to record a 5.21% CAGR as contemporary styles emphasize sleek profiles, durability, and lighter shipping weights that curb freight costs. Plastic and composite blends fill outdoor and institutional niches where moisture resistance is critical. Engineered materials incorporating bamboo fibers and recycled aluminum gain traction as ESG metrics influence procurement decisions.

Local aluminum smelting capacity positions the UAE favorably for metal furniture exports within the GCC, reducing reliance on imported raw materials. Hybrid constructions marry wood veneers with steel framing, creating products that appeal to both traditional and minimalist tastes. FSC-certified timber sourcing commands a growing price premium yet appeals to government buyers complying with green-building codes. Metal’s maintenance advantages resonate with hotel operators seeking long service intervals and quick refurbishment cycles. Over time, material mix adjustments will mirror the balance between cost containment, design trends, and regulatory compliance in the UAE home furniture market.

By Price Range: Premium Acceleration Signals Market Evolution

Mid-range merchandise held 48.35% share of the UAE home furniture market size in 2025, buoyed by competitive price-quality ratios that resonate with middle-income expatriates. Installment plans and festive-season promotions further sustain turnover within this tier. Premium furniture is projected to expand at a 5.78% CAGR through 2031 as the influx of high-net-worth individuals fuels demand for exclusive brands and bespoke craftsmanship. Economy lines face mounting competition from refurbished goods and rental packages that undercut upfront pricing. Nonetheless, stable job creation maintains baseline consumption even in the lower tiers.

Consumers often trade up over successive housing moves, migrating from economy starter kits to mid-range or premium collections as income rises. Luxury shoppers seek provenance and limited editions, prompting collaborations between UAE retailers and European maisons that deepen the premium assortment. Financing products such as pay-later platforms democratize mid-range access without sacrificing cash-flow flexibility. Inflationary pressures encourage cost-conscious shoppers to extend replacement cycles, nudging retailers toward loyalty benefits and service warranties. Cross-tier mobility keeps retailers agile in assortment planning across the UAE home furniture market.

By Distribution Channel: Digital Transformation Reshapes Retail Landscape

Specialty furniture stores retained 43.92% revenue share in 2025, leveraging in-store visualization tools and complimentary design consultations that ease high-involvement purchasing decisions. These outlets increasingly incorporate AR kiosks and online booking systems to bridge physical-digital touchpoints. Online channels are anticipated to post a 6.83% CAGR as high internet penetration, secure payment gateways, and same-day delivery options normalize e-commerce transactions for bulky items. Home-center chains provide one-stop convenience, bundling décor accessories that raise average basket sizes. Hypermarkets target impulse buys and entry-level furniture suited for studio apartments.

Omnichannel strategies now dominate boardroom agendas, with click-and-collect and white-glove assembly services improving customer satisfaction. Proprietary last-mile fleets optimize costs and ensure damage-free deliveries, a critical factor for heavy goods. Marketplace algorithms personalize recommendations, driving conversion rates in the UAE home furniture market. Virtual showrooms reduce the need for large footprints, freeing capital for logistics infrastructure. Finally, data analytics aids inventory optimization, mitigating the demand volatility tied to expatriate churn.

Geography Analysis

Dubai accounted for 40.88% revenue share in 2025, anchored by strong tourism, luxury real estate, and a cosmopolitan consumer base that spans all price levels. Real-estate transactions worth AED 306.3 billion in Q3 2024 translated into substantial first-time furniture purchases and renovation projects. The emirate’s positioning as a design hub attracts international exhibitions that showcase new trends and foster B2B linkages. Smart-city initiatives spur demand for connected furniture that integrates with home-automation ecosystems. Green-building mandates reinforce interest in certified materials and circular design across the UAE home furniture market.

Abu Dhabi leverages oil-revenue stability and cultural tourism to support furniture spending in both residential and commercial projects. Saadiyat Island’s Museum district requires custom furnishings that merge regional aesthetics with modern functionality. Manufacturing value addition of AED 197 billion in 2023 strengthens local supply chains, reducing reliance on imported case-goods. Government housing programs sustain mid-range demand by offering subsidized mortgages to Emirati nationals. Meanwhile, premium hotel developments such as the Louvre-adjacent resort elevate procurement standards.

Sharjah and the Northern Emirates record the fastest 5.49% CAGR as affordable housing developments attract young families and industrial-zone staff. Competitive land prices permit larger living spaces, translating into higher per-unit furniture volumes despite lower ticket averages. Retailers expand smaller format stores in Ajman and Ras Al Khaimah to capture untapped communities while leveraging centralized e-commerce fulfillment. Cross-border shoppers from Oman and Saudi Arabia further diversify regional sales. Infrastructure improvements like the Etihad Rail corridor promise smoother inter-emirate logistics, reinforcing the integrated nature of the UAE home furniture market.

Value Chain Analysis

The UAE home furniture value chain relies on imported raw materials and finished goods, with wood-based products playing a major role. Local joinery, upholstery, and metal fabrication support residential and hospitality fit-outs, while product localization (finishes, sizes, and compliance labeling) is handled by importers, distributors, and retailers. Developers and hospitality operators increasingly buy through turnkey fit-out contractors that bundle design, manufacturing, installation, and after-sales service.

Logistics largely follows the UAE port system. Jebel Ali Port (DP World) and Khalifa Port (AD Ports Group) function as the main gateways, with East Coast routing via Khorfakkan Port (Gulftainer) used to diversify supply chains. Downstream, distribution spans specialty stores and home centers, and omnichannel fulfillment needs (assembly, returns, and white-glove delivery) shape warehousing and last-mile requirements for bulky goods. Gulftainer’s Al Dhaid Multi-Modal Trade Corridor (June 2026) links an inland hub to Khorfakkan Port, and Gulftainer’s announced Khorfakkan expansion plan (July 2026) targets higher container throughput with additional inland capacity through dry ports. Key constraints remain lead times and cost volatility for imported inputs, alongside uneven quality and scalability across the fragmented workshop segment, which tends to push larger players toward industrial-zone manufacturing, standardized processes, and tighter coordination with retail and project schedules.

Competitive Landscape

The UAE home furniture market exhibits moderate fragmentation, with global giants, regional chains, and niche boutiques competing vigorously for share. IKEA ranks high in brand health by offering modular designs and transparent pricing that appeal to value-oriented customers. Home Centre and Pan Emirates draw on localized merchandising and installment plans to fortify mid-range leadership. Digital natives like TUKA Dubai disrupt traditional ownership patterns with subscription services that capture transient clientele. Concurrently, luxury entrants such as Ethan Allen, Bentley Home, and Bugatti Home enrich the premium spectrum and elevate design standards across the board.

Technology investment separates front-runners from laggards such as AR visualization, AI-driven recommendations, and CRM platforms enhance consumer journeys. Vertical integration emerges among regional manufacturers that acquire carpentry workshops to control quality and shorten lead times. Sustainability credentials—ranging from FSC-certified wood to take-back programs, differentiating brands in tendering processes for government and hospitality contracts. Strategic partnerships with developer’s secure turnkey supply agreements that stabilize revenue flow in the UAE home furniture market. Competitive dynamics thus hinge on balancing cost efficiency, digital proficiency, and ESG compliance.

M&A activity rises as retailers seek scale to offset logistics costs and strengthen bargaining power with suppliers. E-commerce marketplaces court private-label opportunities that extend margins and foster customer loyalty. International players use Dubai’s free-trade zones as distribution hubs to reach wider GCC and African markets, intensifying regional rivalry. Manufacturers deploy robotics and lean practices to raise productivity in anticipation of Operation 300bn incentives. Ultimately, firms that harmonize omnichannel reach, curated assortments, and sustainable practices will command outsized influence over market direction.

UAE Home Furniture Industry Leaders

IKEA

Home Centre

PAN Emirates Home Furnishings

Danube Home

The One

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Localization and faster project fulfillment are creating a practical opportunity across the UAE home furniture ecosystem for manufacturers and fit-out partners that can meet developer and hospitality timelines while aligning with national industrial priorities. In April 2026, the UAE Cabinet approved an AED 1 billion National Industrial Resilience Fund to support localization, supply-chain resilience, and AI adoption in production. This reinforces the rationale for automating joinery, upholstery, and panel processing in domestic facilities, and procurement frameworks that favor in-country value approaches create an advantage for suppliers that can evidence local content and compliant sourcing in large, repeatable tenders linked to residential handovers and hospitality pipelines.

A second opportunity centers on integrated, service-led offerings that combine design, customization, delivery, and refurbishment. This includes service models aimed at both premium personalization and the operational needs of multi-site operators. Evidence of this shift is RAKEZ signing an agreement in May 2026 with MAGRABi Retail Group to establish a Store Manufacturing Centre in Ras Al Khaimah, designed to service store fit-outs and refurbishments at scale (capacity referenced at 140 stores annually). This model extends to furniture and interior packages for residential and hospitality clients. On specifications, demand for smart and multi-functional furniture, alongside more sustainable product choices (certified materials, low-VOC finishes, and circular design practices referenced in Dubai), creates room for suppliers to industrialize customization without long lead times, while also supporting take-back, refurbishment, or subscription-compatible product designs.

Recent Industry Developments

- June 2026: IKEA UAE introduced a revamped 6,100 sqm New Market Hall at Dubai Festival City with interactive, AI-enabled tools such as Ask IKEA and expanded immersive room settings. The upgrade strengthens in-store conversion for high-consideration categories and supports omnichannel journeys by improving discovery, planning, and attachment sales.

- May 2026: Danube Home opened a new 35,000 sq ft phygital showroom at Festival Plaza, Jebel Ali, integrating AI-powered retail assistance branded as Yara. The format raises competitive pressure on specialty retail by blending guided selling with digital navigation, while also acting as a fulfillment and service touchpoint for larger-ticket purchases.

- November 2024: Bentley Home opened its first store in Dubai, expanding access to its luxury furniture collections in a key premium retail corridor. The entry adds depth to the high-end assortment in the emirate and increases competitive intensity for premium players targeting luxury villas and branded residence customers.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the value of home furniture sold in the UAE for household use, including items for living, dining, sleeping, storage, and home working, across offline and online channels.

Scope exclusions: We exclude non-furniture home furnishings such as home textiles, decor accessories, and major appliances.

Segmentation Overview

- By Product

- Living Room & Dining Room Furniture

- Bedroom Furniture

- Kitchen Furniture

- Home Office Furniture

- Bathroom Furniture

- Outdoor Furniture

- Other Furniture

- By Material

- Wood

- Metal

- Plastic & Polymer

- Others

- By Price Range

- Economy

- Mid-Range

- Premium

- By Distribution Channel

- Home Centers

- Specialty Furniture Stores (including exclusive brand outlets and local stores from the unorganized sector)

- Online

- Other Distribution Channels (includes hypermarkets, supermarkets, teleshopping, departmental stores, etc.)

- By Geography

- Dubai

- Abu Dhabi

- Sharjah

- Northern Emirates (Ajman, UAQ, RAK, Fujairah)

Data Sources, Market Sizing, and Validation

Desk Research

Desk work was used to set the base structure of the model and to anchor demand signals that are visible in public data. Sources we relied on for assumptions include releases from the UAE Federal Competitiveness and Statistics Centre, Dubai Statistics Center indicators, UN Comtrade trade statistics for furniture-related HS codes, and World Bank population and macro series. We also reviewed customs and port updates, relevant municipality building and housing indicators where available, and public tariff and standards notes for imported furniture.

To cross-check the supplier landscape and revenue direction, we reviewed annual reports and investor presentations of large retailers and brands with UAE operations, plus reputable press coverage and trade publications. A paid subscription for company financials and intelligence and a shipment-level import and export database were used selectively to validate directionally where volumes and pricing were moving. These examples are not exhaustive, and many other public and paid references were used during data collection, validation, and clarification.

Primary Interviews and Surveys

Primary conversations were run with furniture retailers, distributors, local manufacturers, and sourcing teams, and then complemented with feedback from mall-based store managers and online channel operators. Since this is a country market, the respondent checks were focused on UAE demand patterns, pricing behavior by range, channel mix shifts, and how housing handovers and refurbishment cycles are translating into furniture purchases.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 13% | |

| Mid tier: 43% | Functional/Unit leaders: 39% | |

| Smaller Players: 21% | Managers: 48% |

Market-Sizing & Forecasting

Market sizing was built using a top-down approach where household demand is reconstructed from UAE population and household formation signals, housing completions and handovers, and typical furniture replacement and refurbishment cycles. We then adjusted for channel mix and price range movement to align the model with retail reality.

To keep the totals realistic, we corroborated with selective bottom-up checks such as sampled average selling prices by category multiplied by estimated unit volumes, plus channel-side roll-ups from major retailers and specialty store clusters.

Inputs in the model included indicators such as residential unit handovers and new supply, household consumption trends, import value and volume movement for furniture categories, the online share shift within home furniture, and range-level pricing changes between economy, mid-range, and premium. When some categories had limited visibility in public series, gaps were handled through proxying with the closest import group, then validating the implied pricing and sell-through with primary feedback.

Forecasting used scenario analysis supported by time series smoothing on the core drivers, and was refined using expert views on housing activity, consumer spending, and promotional intensity. Where a driver showed a one-off shock, assumptions were normalized before the forward run so the forecast did not overreact to a single period.

Data Validation & Update Cycle

Validation was handled through multiple checks so the final totals matched real market signals. We compared modeled values against independent indicators such as furniture import trends, retailer revenue direction, and visible channel shifts, then reviewed any large variances before sign-off. If a mismatch remained after the first pass, we revisited the assumptions and re-contacted respondents to confirm whether the change was structural or temporary.

A multi-step analyst review was applied, where category and channel outputs were checked for logical share movement and for pricing consistency across years. Reports are refreshed annually, and interim updates are triggered when material events occur, such as major housing cycle changes, sharp currency or freight shifts that affect imported furniture pricing, or large policy moves. Before delivery, the latest data is rechecked so clients receive the most current view available.

Mordor Intelligence's UAE Home Furniture Market Size Compared Against Other Published Estimates

It is normal to see different market values for UAE home furniture, because publishers do not always count the same items even when the title looks similar. Differences typically come from what gets included as furniture versus furnishings, the base year used, and how price and channel shifts are carried into forecasts.

The benchmark table shows a clear spread for the 2025 value, and in Mordor Intelligence's model the scope is kept to home furniture only (by product, material, price range, channel, and UAE geography), without rolling in adjacent home furnishings or wider contract furniture demand.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.78 B (2025) | |

| Trade Journal B | USD 2.90 B (2026) | Uses a different year and appears to reference a broader UAE furniture narrative, where home furniture is mentioned alongside overall furniture context, which can shift comparability when totals are discussed without a consistent base-year build. |

| Global Consultancy A | USD 2.28 B (2025) | Applies a narrower value capture and a longer forecast horizon, and the public summary provides fewer checks on channel mix and price range progression, which can pull the base-year value down when retail pricing and premiumization are treated conservatively. |

Reading the three figures together, most of the gap can be traced back to base year choice and what is counted inside the home furniture wallet. By keeping the inputs tied to housing activity, trade movement, and channel and pricing shifts that can be explained and rechecked, we arrive at a practical number that can be reproduced and updated in a consistent way year over year.

Key Questions Answered in the Report

How large is the UAE home furniture market in 2026?

The sector is valued at USD 2.9 billion in 2026 and is forecast to hit USD 3.55 billion by 2031.

Which product category leads furniture sales in the UAE?

Bedroom furniture is dominant, accounting for 27.95% of 2025 revenue thanks to sustained housing turnover and cultural preferences for comfortable private spaces.

What is driving premium furniture demand?

Ultra-luxury villa handovers in Dubai and a growing high-net-worth resident base are boosting premium furniture, which is set to grow at a 5.78% CAGR through 2031.

How important is e-commerce to UAE furniture sales?

Online channels are the fastest growing distribution avenue, projected to expand at a 6.83% CAGR as platforms enhance delivery logistics and virtual visualization tools.

Which emirate registers the highest furniture market growth?

Northern Emirates collectively post the quickest 5.49% CAGR between 2026 and 2031, propelled by affordable housing and industrial expansion.

Page last updated on: