Market Overview

| Study Period | 2021 - 2031 |

|---|---|

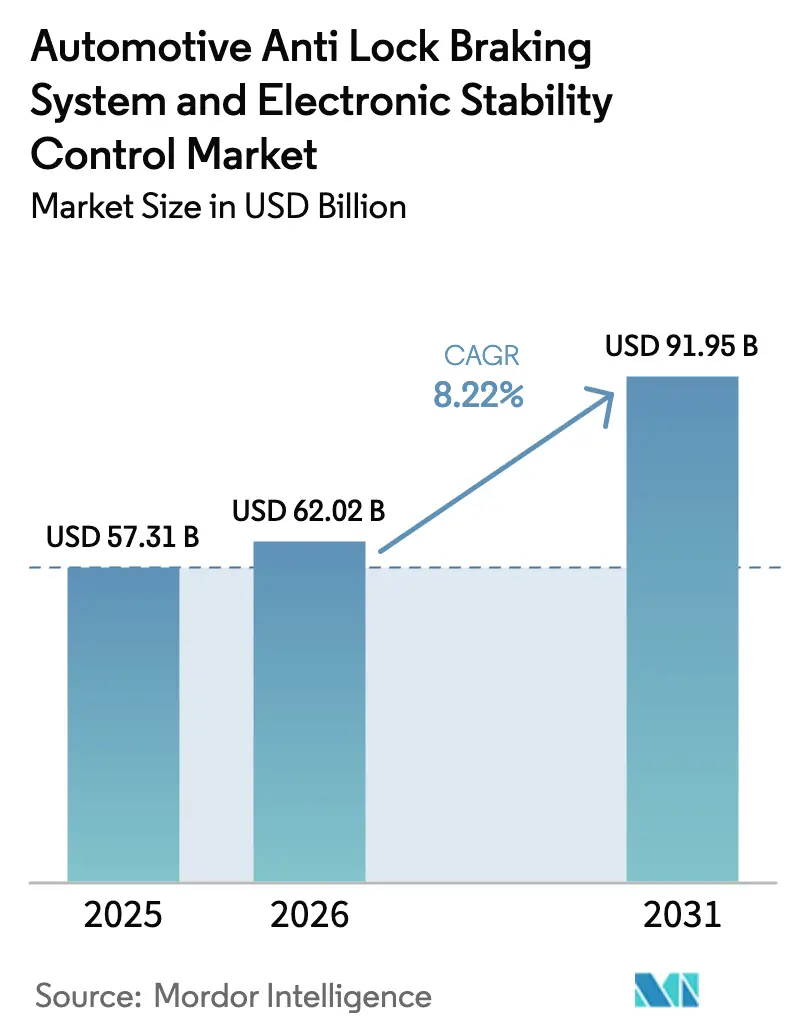

| Market Size (2026) | USD 62.02 Billion |

| Market Size (2031) | USD 91.95 Billion |

| Growth Rate (2026 - 2031) | 8.22% CAGR |

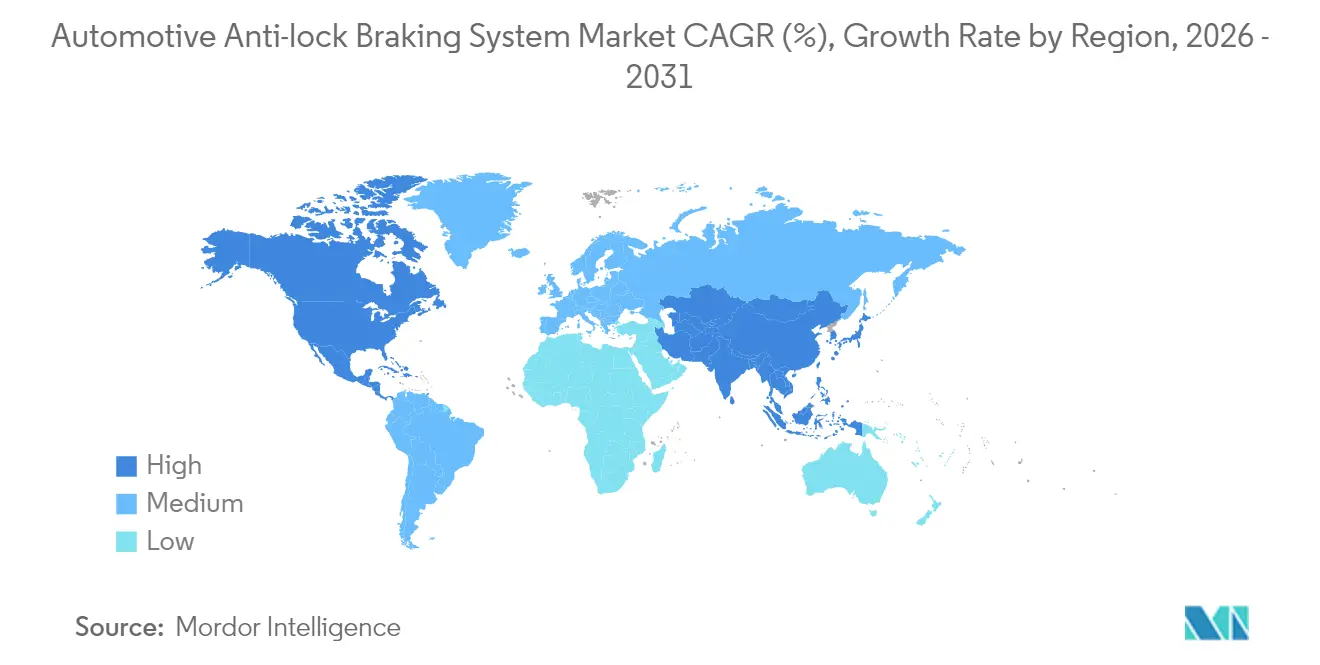

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

| Market Concentration | High |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Anti-Lock Braking System and Electronic Stability Control Market Analysis by Mordor Intelligence

The Automotive Anti-Lock Braking System and Electronic Stability Control Market size was valued at USD 57.31 billion in 2025 and estimated to grow from USD 62.02 billion in 2026 to reach USD 91.95 billion by 2031, at a CAGR of 8.22% during the forecast period (2026-2031). Growth is anchored in mandatory safety regulations, electrified platforms that favor brake-by-wire designs, and the steady rebound of global vehicle production. Regulators in the European Union, the United States, India, and China now regard ABS as foundational to wider active-safety suites, prompting OEMs to embed ABS into virtually every new vehicle segment. Suppliers are capitalizing on these mandates by bundling ABS with advanced driver assistance controllers, while insurers reward fleets and consumers that opt for active-safety packages. Alongside rising production volumes, electric two-wheelers and battery electric cars are creating the fastest incremental demand as single-channel and electric ABS architectures gain popularity.[1]National Highway Traffic Safety Administration, “Automatic Emergency Braking Final Rule,” nhtsa.gov

Key Report Takeaways

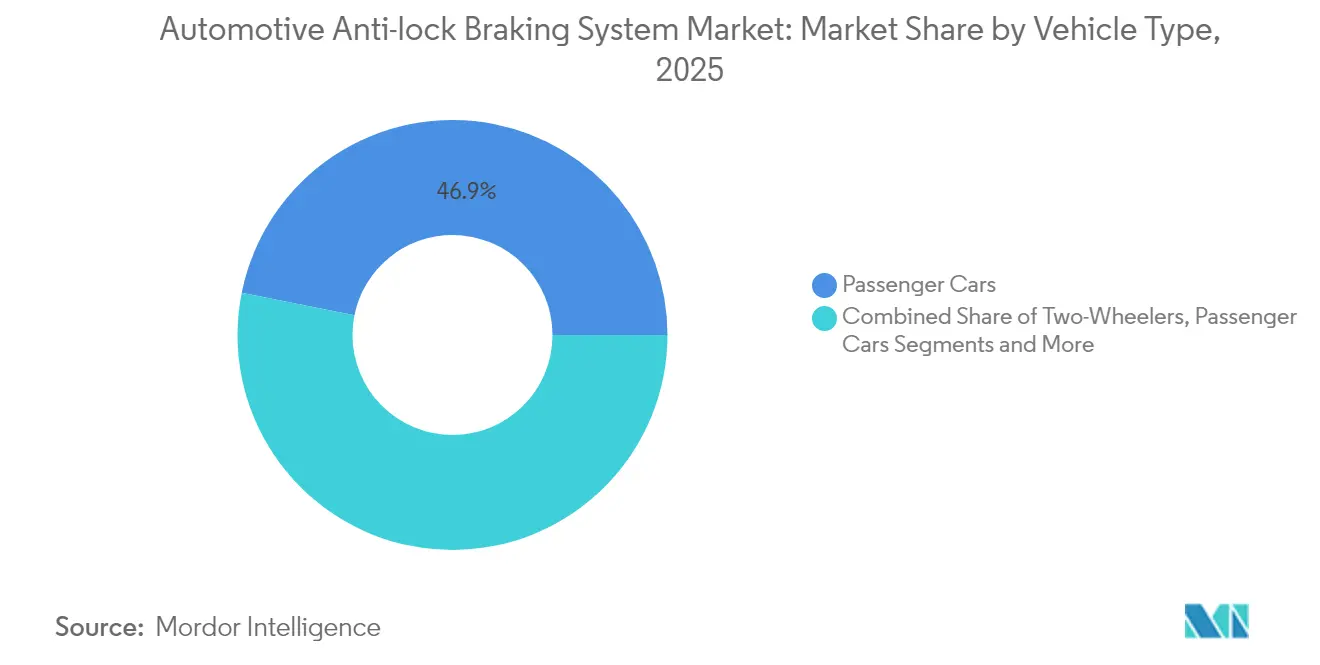

- By vehicle type, passenger cars held 46.85% of the automotive anti-lock braking system market share in 2025, whereas two-wheelers are set to expand at a 15.05% CAGR through 2031.

- By component, electronic control units accounted for 33.20% of 2025 revenue and are growing fastest at 11.95% CAGR to 2031.

- By ABS type, 4-channel configurations captured 60.70% share of the automotive anti-lock braking system market size in 2025; single-channel units will grow at 14.42% CAGR between 2026-2031.

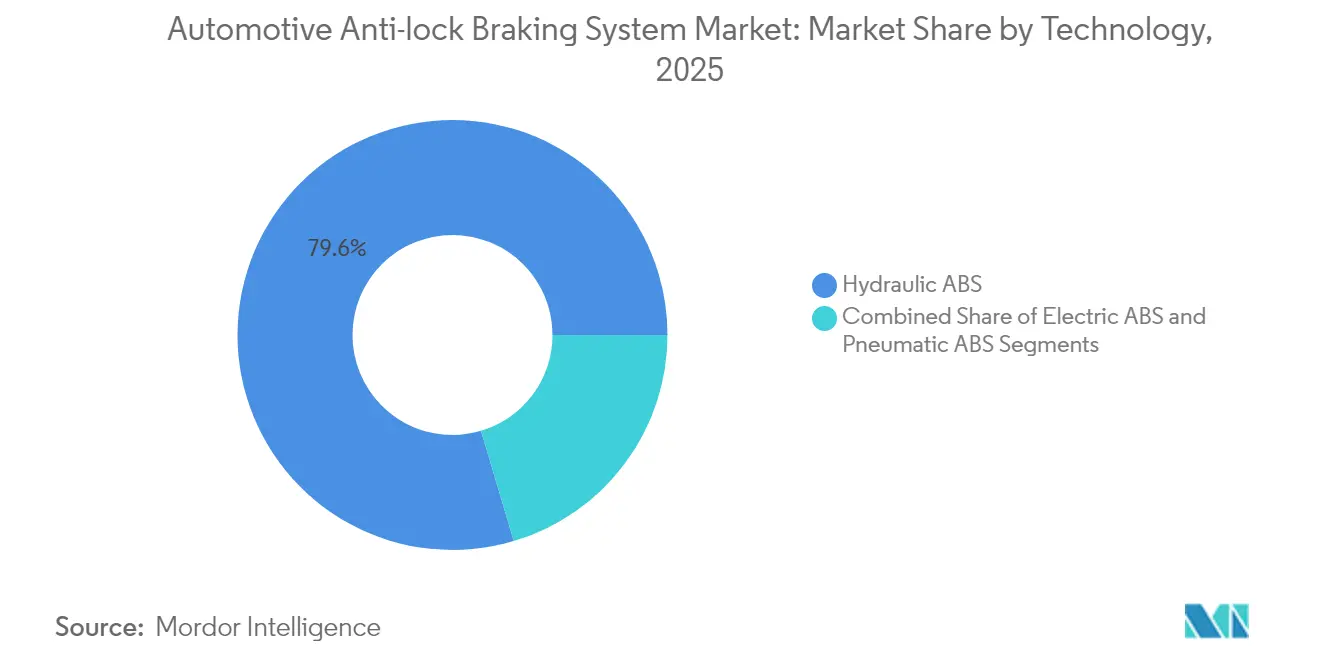

- By technology, hydraulic solutions dominated with 79.60% of 2025 revenue, while electric ABS technology is forecast to rise at a 12.95% CAGR to 2031.

- By end user, OEM installations represented 91.05% of 2025 revenue, whereas the aftermarket retrofit segment will climb at 12.18% CAGR through 2031.

- By geography, Asia Pacific accounts for 36.10% market share, whereas North America is expected to grow at 13.28% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Automotive Anti-Lock Braking System and Electronic Stability Control Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Point Impact on Market CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mandatory Safety Regulations | +2.2% | Global, with emphasis on EU, North America, and India | Short term (≤ 2 years) |

| Rising Global Passenger‐Car & 2-Wheeler Production | +1.6% | Global, with highest impact in APAC | Medium term (2-4 years) |

| Electrification Platforms | +1.3% | Global, with emphasis on China, Europe, and North America | Long term (≥ 4 years) |

| Growing Insurance Incentives | +1.1% | North America, Europe, and developed APAC markets | Medium term (2-4 years) |

| Rapid Retrofit Demand | +0.4% | North America and Europe | Medium term (2-4 years) |

| Bundeled Offering by Tier-1 Suppliers | +0.2% | Global, with emphasis on premium vehicle segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Mandatory Safety Regulations Driving Global ABS Adoption

Stringent policies such as UN R78 for motorcycles, FMVSS-122 in the United States, and AIS-150 in India are pushing ABS fitment toward 100% in new vehicles. The U.S. National Highway Traffic Safety Administration’s rule requiring automatic emergency braking by 2029 makes ABS core to achieving compliance. Europe already enforces motorcycle ABS on scooters above 125 cc, influencing ASEAN nations that rely heavily on two-wheelers. India mirrored this trend, compelling suppliers to release cost-optimized single-channel solutions. UN ESCAP estimates that motorcycle ABS can cut fatalities by 31% unescap.org, reinforcing regulators’ confidence.

Rising Global Vehicle Production Expanding ABS Market Footprint

Post-pandemic manufacturing recovery is most pronounced in Asia Pacific, where China returned to full-scale capacity and India’s two-wheeler output set new highs in 2024. Increased unit volumes translate directly into greater ABS demand, especially as ABS migrates from optional to standard equipment. Bosch notes that advanced ABS can prevent 40% of two-wheeler crashes, a statistic resonating with consumers and policymakers.

Growing Insurance Incentives for Active-Safety Equipped Vehicles

North American and European insurers now use telematics to gauge accident risk, granting lower premiums to fleets that deploy ABS and similar systems. Verizon Connect reports that commercial operators see both safety and financial gains from equipping trucks with ABS-based packages. This economic nudge accelerates mid-range vehicle penetration and pushes retrofits into used fleets.

Electrification Platforms Transforming ABS Architecture

Electric powertrains necessitate brake-by-wire integration, blending mechanical braking with regenerative energy capture. An MDPI review finds that brake-by-wire enables quicker actuation than traditional hydraulics, aligning with autonomous driving requirements. Suppliers that master electronic control hardware and software secure a first-mover advantage as BEV volumes rise.

Restraints Impact Analysis*

| Restraint | (~) % Point Impact on Market CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High BOM Cost | -1.2% | APAC, South America, and Africa | Medium term (2-4 years) |

| Integration Complexity | -0.8% | Global, with emphasis on commercial vehicles | Medium term (2-4 years) |

| Semiconductor Supply-Chain | -0.6% | Global | Short term (≤ 2 years) |

| Cyber-Security Certification | -0.3% | Europe and North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cost Barriers Limiting Penetration in Price-Sensitive Markets

ABS price premiums remain challenging for low-cost motorcycles and entry-level cars in India, Indonesia, and Brazil, where a few USD can sway purchase decisions. OEM margins average 7.2%, while suppliers hover near 5.5%, limiting room to absorb ABS costs. Tier-1 vendors therefore re-engineer hydraulic units to remove valving complexity, adopt shared ECUs, and localize production to achieve viable price points.

Semiconductor Supply Constraints Impacting Production Capacity

Lingering chip shortages since 2023 continue to disrupt ABS supply chains, extending lead times. Some OEMs have revised module layouts to trim chip counts, while vertically integrated players secure allocation from in-house semiconductor divisions. The U.S. Federal Register notes that new NCAP updates from 2026 will intensify semiconductor demand because additional ADAS validation is required.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Electric Two-Wheelers Driving Innovation

Passenger cars anchored the automotive anti-lock braking system market in 2025, delivering 46.85% revenue thanks to mandatory fitment in Europe, China, and North America. Stable car demand, paired with increasingly sophisticated driver assistance packages, ensures a consistent revenue base. The segment will grow in tandem with ADAS penetration, though at a slower pace than two-wheelers. The automotive anti-lock braking system market size for passenger cars is projected to expand at 7.98% CAGR, supported by OEM integration of brake control with lane-keeping and adaptive cruise functions.

Electric two-wheelers inject faster momentum at 15.05% CAGR. Mandates in India and Europe require ABS on motorcycles above 125 cc, propelling single-channel architectures that weigh and cost less than four-wheel solutions. Electric scooters popular in China and Southeast Asia favor regenerative braking, forcing suppliers to fuse ABS algorithms with energy-recovery logic. Bosch forecasts mass-market rider assistance deployment by 2026, underscoring regional appetite for active safety on two-wheelers.

By Component: ECUs Evolving with AI Integration

Electronic control units remained the largest component segment in 2025 at 33.20% revenue, a share lifted by rising computational needs. AI firmware now interprets wheel-speed data, road friction coefficients, and vehicle load in real time, enabling predictive braking. This functionality drives a 11.95% CAGR outlook for ECUs, well ahead of other components. Wheel-speed sensors follow in value, benefiting from solid-state designs that withstand vibration on two-wheelers and heavy trucks.

Hydraulic control units face weight and efficiency redesigns for battery electric vehicles, where every kilogram impacts range. Valves and actuators exploit lightweight aluminum housings and advances in mechatronics to cut response times. As AI moves onto central domain controllers, ECU suppliers adapt by offering over-the-air update capabilities to maintain cyber compliance, mitigating one of the key restraints on software-defined braking.

By ABS Type: Single-Channel Systems Expanding in Two-Wheelers

Four-channel architectures dominated at 60.70% revenue in 2025. They remain standard in passenger cars and light trucks because they modulate each wheel independently, maximizing control on slippery surfaces. Single-channel units, in contrast, apply one hydraulic circuit to the front wheel of a motorcycle and can reduce costs by 35%. They therefore headline growth with a 14.42% CAGR and will equip the vast majority of sub-250 cc two-wheelers by 2030.

Three-channel systems hold a specialist niche in light commercial vans where dual rear wheels share one channel, balancing performance and price. Continental’s modular product line shows OEMs can scale from one to four channels without altering sensor sets, providing a migration path for entry-level models that later upgrade to full coverage.

By Technology: Electric ABS Gaining Momentum

Hydraulic solutions represented 79.60% of 2025 sales because they are entrenched, proven, and supported by global servicing networks. However, the automotive anti-lock braking system market is now tilting toward electric control. Electric ABS, with a 12.95% CAGR outlook, integrates pressure control via electro-mechanical boosters and facilitates seamless blending with regenerative braking. An MDPI study confirms brake-by-wire enhances pedal feel consistency, critical for autonomous taxi fleets where multiple riders alternate during a single day.

Pneumatic ABS retains a place in heavy-duty trucks and buses that rely on air brakes. Suppliers are migrating to electronic air-processing units that consolidate ABS, traction control, and stability functions, reflecting convergence across braking disciplines.

By End User: Aftermarket Retrofit Demand Accelerating

OEM fitment secured 91.05% revenue in 2025. Automakers treat ABS as a baseline safety pillar, integrating it at design inception to satisfy crash-avoidance protocols. Nonetheless, the aftermarket unlocks new territory. Fleet operators, insurers, and ride-hail platforms retrofit ABS into vans and older buses, chasing lower premiums and regulatory compliance in low-emission zones.

Diagnostic specialists like Noregon Systems supply software that interfaces with mixed-age fleets, streamlining maintenance and reducing downtime. As governments tighten inspection regimes, aftermarket ABS calibration will become mandatory, pushing further demand for certified retrofit modules and expected to foresee a growth at 12.18% CAGR by 2031.

Geography Analysis

Asia Pacific leads the automotive anti-lock braking system market with 36.10% market share, propelled by China’s production scale and India’s regulatory surge. India’s ABS mandate on motorcycles is growing significantly, with suppliers establishing local ECU plants to avoid import tariffs. China pairs ABS with compulsory electronic stability control on passenger cars, keeping domestic tier-1 suppliers in lockstep with multinational competitors. Japanese and South Korean OEMs integrate ABS with proprietary hybrid systems, sharpening regional technology leadership.

North America expands at highest CAGR at 13.28% by 2031, with U.S. demand buoyed by upcoming AEB rules and Canada aligning with FMVSS standards. Commercial fleet retrofits gain traction where insurers offer multiline discounts. Mexico’s assembly plants, serving export markets, pre-install ABS to satisfy both U.S. and EU homologation. Smaller yet growing markets in the Middle East, Africa, and South America witness Brazil mandating ABS on all new motorcycles, and Saudi Arabia incentivizing fleets that adopt advanced safety packages.

Europe follows, underpinned by the EU General Safety Regulation that obliges ABS on all new vehicles and positions it within broader AEB validation. Germany remains the region’s innovation hub, with suppliers piloting ABS-based harsh-brake data to improve road-friction mapping. Gapwaves notes that extra radar sensors required for AEB complement ABS signals for redundancy. Eastern European assembly plants extend adoption to entry-level cars, ensuring uniform safety standards.

Competitive Landscape

The automotive anti-lock braking system market is moderately consolidated. Each allocates significant annual revenue to R&D, advancing electric booster designs and software stacks that extend ABS into predictive brake control. Continental’s February 2025 upgrade to its driver-assistance suite exemplifies the pivot toward integrated sensing and actuation.

Mid-tier challengers exploit regional niches. Mando and Hyundai Mobis leverage cost advantages in South Korea to provide budget ABS for emerging ASEAN makers. WABCO (now part of ZF) pushes pneumatic ABS for heavy trucks, while Hitachi Astemo targets high-performance motorcycles with dual-channel units. Suppliers without substantial electronics capabilities face pressure as automakers center brake software inside domain controllers, shifting value from hardware to code.

Innovation focus now extends to AI-based friction estimation and over-the-air firmware, creating a bridge from conventional ABS toward fully autonomous brake management. ZF’s R&D outlay underscores the capital intensity required to stay relevant. Start-ups specializing in software-defined braking partner with established hydraulics firms, filling gaps in cyber-security certification and system safety analysis.[3]ZF Friedrichshafen AG, “Annual Report 2024,” zf.com

Automotive Anti-Lock Braking System and Electronic Stability Control Industry Leaders

Autoliv Inc.

Robert Bosch GmbH

DENSO Corporation

ZF Friedrichshafen AG

Continental AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Continental Engineering showcased new driver-assistance functions that refine brake intervention timing, enhancing ABS synergy with lane-keeping and adaptive cruise.

- January 2025: Continental launched Conti EfficientPro 5 commercial-vehicle tires and partnered with TNO to link tire wear data with automatic emergency braking, elevating system accuracy under varying grip levels.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global automotive anti-lock braking system (ABS) and electronic stability control (ESC) market as every hydraulic, electric, or pneumatic assembly comprising ECU, sensors, modulator, and valves, whose core function is to prevent wheel lock-up and correct yaw on passenger cars, commercial vehicles, and two-wheelers. According to Mordor Intelligence, values reflect ex-factory prices for OEM fitments and verified aftermarket retrofits.

Scope excludes standalone brake hardware (pads, discs, calipers) and brake-by-wire units sold without embedded ABS/ESC logic.

Segmentation Overview

- By Vehicle Type

- Two-Wheelers

- Passenger Cars

- Light Commercial Vehicles

- Medium and Heavy Commercial Vehicles

- By Component

- Electronic Control Unit (ECU)

- Hydraulic Control Unit

- Wheel Speed Sensors

- Valves & Actuators

- By ABS Type

- 4-Channel

- 3-Channel

- Single-Channel (Motorcycle)

- By Technology

- Hydraulic ABS

- Electric ABS

- Pneumatic ABS

- By End User

- OEM-Fitment

- Aftermarket Retrofit

- By Geography

- North America

- United States

- Canada

- Rest of North America

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia Pacific

- Middle East and Africa

- Turkey

- Saudi Arabia

- United Arab Emirates

- South Africa

- Rest of Middle East and Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Structured interviews with braking engineers, OEM purchasing leads, and safety regulation officials in Asia, Europe, and the Americas supply real-time fitment ratios, price dispersion, and upcoming mandate timelines. Their insights close data gaps and allow us to triangulate our preliminary desk findings.

Desk Research

Mordor analysts begin with public tier-1 datasets such as OICA production tallies, UNECE R13H/R140 mandate files, NHTSA FMVSS 126 defect recalls, Indian MoRTH gazette notifications, and UN Comtrade part-level trade codes, building the addressable vehicle pool and baseline pricing. We reinforce this with peer-reviewed crash avoidance studies and recent 10-K filings and investor decks that reveal system cost trends. Paid resources, including Marklines vehicle launch trackers and D&B Hoovers company financials, let us benchmark average bills of material across regions, while Dow Jones Factiva flags regulatory or supply chain disruptions that may skew forecasts. The sources noted here are illustrative; many additional references supported data gathering and validation.

Market-Sizing & Forecasting

A top-down and bottom-up blend is used. Global vehicle output is paired with mandate-driven penetration curves, then cross-checked against sampled supplier roll-ups before totals are frozen. Key variables like average system ASP, two-wheeler electrification share, semiconductor capacity indices, regional income elasticity, and recall incidence feed our multivariate regression, while ARIMA tests catch cyclical swings. When component data are sparse, we apply primary sourced ratios and flag them for sensitivity reviews.

Data Validation & Update Cycle

Outputs pass multi-layer anomaly checks, peer review, and a senior analyst sign-off. We refresh models each year and issue interim updates when major regulatory or supply shocks occur, ensuring clients always receive the latest view.

Why Mordor Intelligence's Automotive Anti Lock Braking System And Electronic Stability Control Baseline Remains Reliable

Published figures often diverge because study scopes, update cadences, and currency bases differ. Some publishers omit two-wheelers, others fold broader brake electronics into totals, and a few project aggressive uptake without re-pricing semiconductor shocks. Our disciplined scope selection, annual refresh, and transparent variable mapping limit such drift.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 57.31 B | Mordor Intelligence | |

| USD 60.13 B | Global Consultancy A | Excludes retrofit two-wheeler ABS, biennial updates |

| USD 38.83 B | Industry Association B | Counts only OEM passenger car fitments, ignores ESC retrofits |

| USD 136.65 B | Research Publisher C | Bundles full brake electronics suite and service revenues |

These contrasts show that our balanced, transparent path, anchored to measurable vehicle output and clearly dated mandates, gives decision-makers a dependable baseline they can readily trace and reproduce.

Key Questions Answered in the Report

What is driving the rapid growth of electric two-wheeler ABS adoption?

Mandates in India and Europe, coupled with rising electric scooter sales, lead to a 15.05% CAGR for single-channel systems that integrate regenerative braking.

How large is the automotive anti-lock braking system market in 2026?

The automotive anti-lock braking system market totals USD 62.02 billion in 2026.

Why are insurers offering discounts for ABS-equipped fleets?

Telematics data show reduced collision risk when ABS and related active-safety features are present, providing measurable underwriting benefits that lower premiums.

Which technology segment is outpacing the traditional hydraulic ABS?

Electric ABS linked to brake-by-wire controls is the fastest segment, expanding at a 12.95% CAGR as electric vehicles become mainstream.

How do semiconductor shortages affect ABS supply?

Chip scarcity lengthens delivery times and pushes suppliers to redesign modules with fewer integrated circuits, temporarily restraining production growth.

Which region currently leads the automotive anti-lock braking system market?

Asia Pacific holds the largest regional revenue, led by China’s passenger-car output and India’s motorcycle ABS mandates.

Page last updated on: