South America Fixed Wireless Access Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

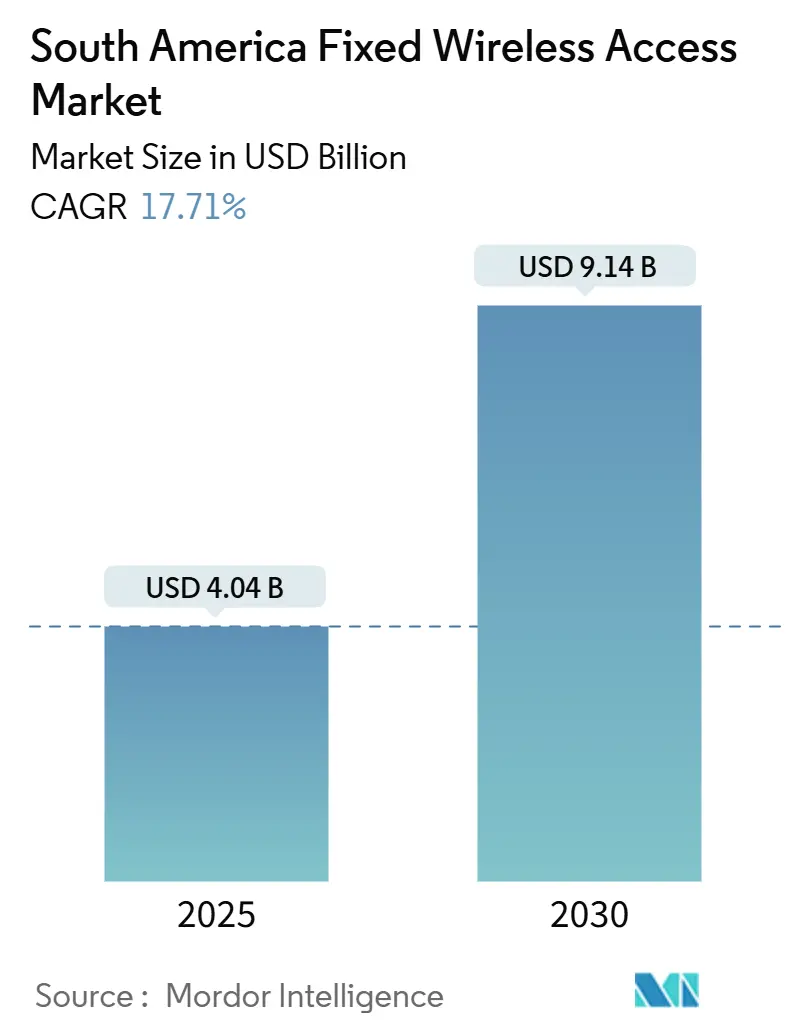

| Market Size (2025) | USD 4.04 Billion |

| Market Size (2030) | USD 9.14 Billion |

| Growth Rate (2025 - 2030) | 17.71% CAGR |

| Fastest Growing Market | South America |

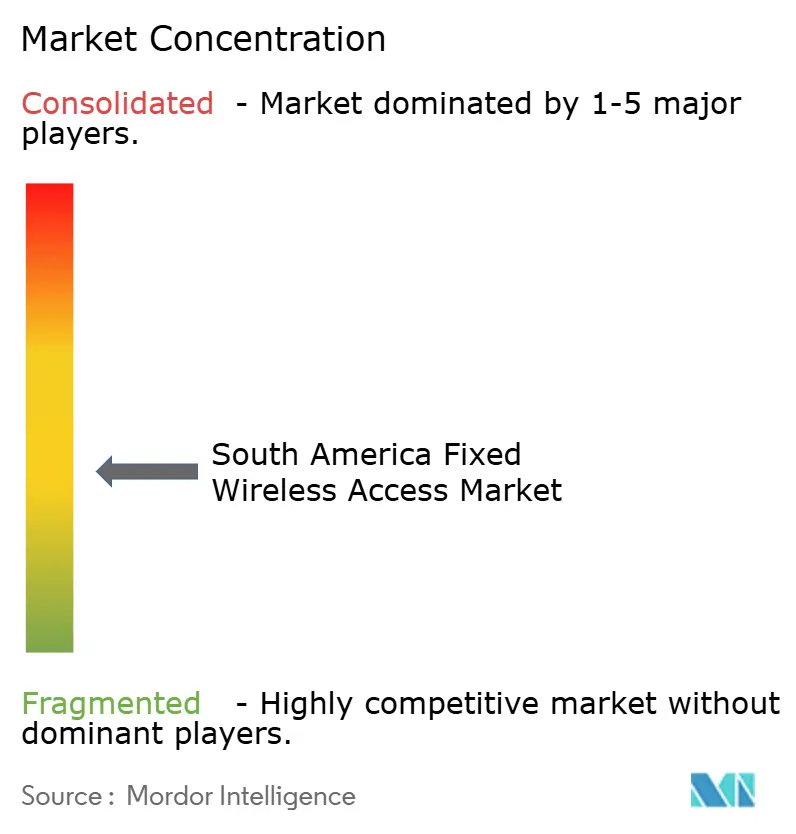

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Fixed Wireless Access Market Analysis by Mordor Intelligence

The South America Fixed Wireless Access Market size is estimated at USD 4.04 billion in 2025, and is expected to reach USD 9.14 billion by 2030, at a CAGR of 17.71% during the forecast period (2025-2030).

Accelerated government-funded rural connectivity, operator reuse of 5G backhaul, and spectrum refarming position the Fixed Wireless Access market as a cost-effective alternative to fiber across varied terrains. Services lead growth as operators favor predictable recurring revenue. Enterprise demand for rapid deployment and mining sector connectivity strengthens commercial uptake, while mmWave adoption gains speed in dense urban and industrial zones. Neutral-host pilots and open-RAN architectures further lower entry barriers, yet rapid urban fiber rollouts and economic volatility temper the overall growth outlook.

Key Report Takeaways

- By type, services held 65.64% of the Fixed Wireless Access market share in 2024 and are advancing at a 20.01% CAGR through 2030.

- By application, residential accounted for 59.29% of the Fixed Wireless Access market size in 2024; commercial usage is expanding at a 24.73% CAGR to 2030.

- By frequency band, sub-6 GHz commanded 81.80% share of the Fixed Wireless Access market size in 2024 while mmWave use is growing at a 30.04% CAGR to 2030.

- By deployment mode, indoor CPE led with 71.75% share of the Fixed Wireless Access market size in 2024; outdoor CPE is growing at a 26.53% CAGR through 2030.

- By geography, Brazil contributed 42.02% of the Fixed Wireless Access market share in 2024, and Chile is projected to grow at a 23.19% CAGR through 2030

Proportional positioning is established by comparing regional contributions against the global total, including that of South america. The fixed wireless access market share in our global report expresses these relative weights.

South America Fixed Wireless Access Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government-subsidized rural broadband programs | +3.2% | Brazil, Colombia, Peru, Chile, Argentina | Medium term (2-4 years) |

| Commercial 5G rollouts accelerating FWA backhaul reuse | +4.1% | Brazil, Chile, Colombia, Argentina, Mexico | Short term (≤ 2 years) |

| Cost-effective spectrum refarming in sub-6 GHz bands | +2.8% | Region-wide | Long term (≥ 4 years) |

| Precision agriculture and mining IoT demand in remote areas | +2.3% | Chile, Peru, Brazil, Argentina | Medium term (2-4 years) |

| Neutral-host open-RAN pilots lowering entry barriers | +1.9% | Brazil, Colombia | Long term (≥ 4 years) |

| Battery-backed CPE design solving power outages | +1.4% | Rural and semi-urban areas | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Government-subsidized Rural Broadband Programs

Government funding sharply improves FWA business cases across underserved zones. Brazil’s National Broadband Plan set aside USD 1.2 billion in 2024 with 40% targeted at wireless builds. Colombia’s Ministry of ICT launched a USD 800 million program reaching 1,200 municipalities.[1]Brazil Ministry of Communications, “National Broadband Plan 2024 Funding Allocation,” mcom.gov.br Peru announced a USD 600 million digital inclusion budget prioritizing Andean wireless deployments. [2]Ministry of ICT Colombia, “Connectivity in Rural Municipalities,” mintic.gov.coThese allocations reduce operator risk by co-financing infrastructure and guaranteeing take-up, cutting cost-per-passing to USD 200-400 compared with more than USD 1,500 for fiber in remote highlands.

Commercial 5G Rollouts Accelerating FWA Backhaul Reuse

Operators leverage live 5G backhaul to serve both mobile and fixed customers, trimming FWA deployment costs by up to 40%. TIM Brasil’s 5G footprint in 607 towns during 2024 unlocked wider FWA coverage without parallel transport builds. [3]TIM Brasil, “2024 Integrated Report,” tim.com.brClaro Colombia bundled 5G and FWA broadband at USD 25-35 monthly, undercutting fiber. The model is most effective where fiber coverage sits below 20% but 5G already reaches 60-70% of residents.

Cost-effective Spectrum Refarming in Sub-6 GHz Bands

Chile freed 200 MHz of 3.5 GHz spectrum in 2024 by reallocating satellite bands without fresh auction fees, letting operators extend FWA quickly. Colombia shifted 2.5 GHz WiMAX licenses to LTE/5G uses under relaxed coverage rules. Refarming bypasses high reserve prices—often more than USD 0.15 per MHz-pop—freeing capital for network rollout rather than license outlays.

Precision Agriculture & Mining IoT Demand in Remote Areas

High-value industrial IoT cases fuel premium FWA lines priced between USD 500-1,500 a month. Chile’s USD 35 billion copper sector relies on low-latency links for automated trucks and sensors. Brazil’s farms, making up 27% of GDP, deploy drone analytics and soil monitoring that require always-on bandwidth. Demand for ruggedized CPE and dedicated spectrum raises average revenue well above residential levels.

Restraints Impact Analysis*

| Restraint | (-) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High spectrum-auction reserve prices | -2.1% | Argentina, Mexico | Short term (≤ 2 years) |

| Rapid fiber deployment along key urban corridors | -1.8% | Brazil, Chile urban zones | Medium term (2-4 years) |

| Tropical rainfall degrading mmWave link availability | -1.3% | Northern Brazil, Colombia | Long term (≥ 4 years) |

| Political-economic volatility curbing telco CAPEX | -2.4% | Argentina, Peru | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Spectrum-auction Reserve Prices

Argentina priced 3.5 GHz lots at USD 0.18 per MHz-pop in 2024, nearly double the regional mean, shifting operator capital from networks to license fees. Mexico saw unsold blocks as bidders balked at similar valuations. Such mispricing slows service launches, hinders new entrants, and perpetuates incumbent dominance.

Political-economic Volatility Curbing Telco CAPEX

Argentina’s 2024 currency slide exceeded 50%, prompting Telecom Argentina to trim capex plans by 25%. Peru’s leadership turnover has delayed spectrum and infrastructure-sharing decisions, lengthening payback periods. Suppliers raise prices or delay deliveries, compounding network rollout risk across neighboring nations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Services Lead Recurring Growth

Services accounted for 65.64% of the Fixed Wireless Access market share in 2024, with a forecast 20.01% CAGR that outpaces hardware. Operators bundle installation, support, and cloud connectors, locking in steady cash flows. TIM Brasil generated more than BRL 3 billion from managed services in 2024, proving the economics of a service-centric approach. Hardware’s 34.36% slice faces margin compression as CPE commoditizes, though advanced Wi-Fi 7 gateways such as Nokia’s FastMile 4 spur premium niches.

The Fixed Wireless Access market size tied to hardware still grows where battery-backed and solar-powered CPE address unreliable grids. Vendors like Baicells and Tycon Systems broaden rural reach with stand-alone power. Access units grow slower because early market stages favor wide macro coverage over dense small-cell layers.

By Application: Enterprise Momentum Intensifies

Residential lines kept 59.29% of the Fixed Wireless Access market size in 2024, boosted by subsidy programs and competition with cable. Commercial demand is the sharper growth engine, scaling at 24.73% CAGR through 2030 as businesses value rapid provisioning. SMEs accept modest premiums for same-month activation that fiber cannot match.

Industrial deals, though fewer, yield highest ARPU. Dedicated mining circuits cost up to USD 1,500 monthly, justified by safety and automation rules. Intelsat’s smart-farming pact with CNH Industrial illustrates how specialized service levels capture outsized returns. Because satellite latency hinders real-time control, FWA becomes preferred for autonomous tractors and drones.

By Frequency Band: mmWave Picks Up Speed

Sub-6 GHz bands dominated 81.80% of the Fixed Wireless Access market share in 2024 due to broad coverage and affordable gear. Harmonized 3.5 GHz allocations support multi-vendor ecosystems that press equipment prices downward. mmWave, however, records a 30.04% CAGR on the back of urban capacity needs. Chile’s 26 GHz auction raised USD 100 million in 2024, underscoring operator intent to deploy high-bandwidth links.

Rain fade remains an obstacle in equatorial belts, steering mmWave rollouts to drier southern metros. Huawei’s CPE Pro 3 with advanced beamforming mitigates humidity losses, widening potential footprints. Unlicensed 60 GHz options gain favor for campus environments where zero-license cost offsets limited range.

By Deployment Mode: Outdoor CPE Gains Ground

Indoor units still capture 71.75% share due to ease of self-install for households. Concrete walls common in Latin architecture dampen signals, pushing operators toward outdoor CPE in fringe and industrial sites. Outdoor gear grows at 26.53% CAGR through 2030 and frequently includes solar modules, as with Zyxel’s NR7103 targeting off-grid farms.

Industrial users specify pole-mounted gear for ruggedness and line-of-sight. Weather-proof designs with high-gain antennas lengthen reach, cutting tower density and capex. The shift enlarges the Fixed Wireless Access market size tied to professional installation and maintenance contracts, creating fresh service revenue layers.

Geography Analysis

Brazil generated 42.02% of regional revenue in 2024 owing to a large subscriber base, a supportive National Broadband Plan, and operator capital outlays topping USD 2 billion yearly. Vivo extended FWA offers to more than 200 cities by 2024, demonstrating a scalable reuse of existing 5G sites. TIM Brasil posted BRL 25,448 million revenue in 2024 with strong margins backed by integrated fixed-mobile bundles.

Chile, while smaller, is projected to post the quickest rise at 23.19% CAGR to 2030. A USD 450 million spectrum auction in 2024 fostered healthy rivalry among participants. Entel aims to add 500,000 FWA lines by 2026 under clear deployment norms from Subtel.

Colombia’s USD 800 million rural program covers 1,200 towns, pairing funding with coverage obligations. Shared-network deals between Tigo and Movistar shave costs by 35%, accelerating coverage. Argentina’s currency risk curbs short-term spending, yet operators maintain strategic FWA builds that hedge against fiber delays. Peru, Mexico, and smaller Central American nations benefit from falling gear prices and policy alignment, gradually increasing the Fixed Wireless Access market size as local pilots mature.

Mordor Intelligence examines the fixed wireless access market across diverse other regional markets as well, including Asia, Middle East, and Africa, while also offering granular country-level perspectives for France and Germany and more.

Competitive Landscape

Market concentration is moderate. Claro Brasil, Vivo, and TIM Brasil leverage spectrum depth and large footprints to cross-sell mobile and FWA. Telecom Argentina and Entel Chile round out the leading tier. Open-RAN and neutral-host models encourage niche competitors that rent shared infrastructure rather than build standalone networks, nudging fragmentation.

Equipment suppliers such as Huawei, ZTE, Nokia, and Ubiquiti pursue direct sales to mines and farms, bypassing telcos in some cases. The Telecom Infra Project lists South America among early targets for neutral-host trials, signaling likely shifts in traditional wholesale relationships. The ultimate structure depends on regulator willingness to allow spectrum leasing and infrastructure sharing at scale.

Incumbents react with differentiated vertical solutions. Vivo bundles cloud storage, security, and FWA under a single invoice for SMEs. Claro partners with Starlink for satellite backhaul in deep rural pockets, extending reach where fiber or microwave is impractical. Such hybrid strategies protect share but widen the service menu for end users.

South America Fixed Wireless Access Industry Leaders

Claro Brasil

Telecom Argentina

Entel Chile

Movistar

Vivo (Telefonica)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: América Móvil acquired ClaroVTR in Chile for USD 2.1 billion, unlocking converged FWA and pay-TV plays.

- September 2024: TIM Brasil earmarked USD 1.5 billion for 2025-2027 to expand 5G and FWA across 1,000 towns.

- August 2024: Claro Colombia partnered with Starlink to supply satellite backhaul for remote FWA sites.

- July 2024: Huawei launched CPE Pro 3 with extended temperature tolerance for industrial users.

South America Fixed Wireless Access Market Report Scope

| Hardware | Consumer-Premise Equipment (CPE) |

| Access Units (Femto and Picocells) | |

| Services |

| Residential |

| Commercial (SME, Enterprise and Retail) |

| Industrial (Mining, Oil and Gas, Utilities, Agriculture) |

| Sub-6 GHz (3.5 GHz, 4.9 GHz, 5 GHz) |

| mmWave (24-29 GHz, 37-40 GHz, 60 GHz) |

| Indoor CPE |

| Outdoor CPE |

| Brazil |

| Chile |

| Colombia |

| Peru |

| Argentina |

| Mexico |

| Rest of South America (Panama, Costa Rica, Uruguay, Guatemala, and Others) |

| By Type | Hardware | Consumer-Premise Equipment (CPE) |

| Access Units (Femto and Picocells) | ||

| Services | ||

| By Application | Residential | |

| Commercial (SME, Enterprise and Retail) | ||

| Industrial (Mining, Oil and Gas, Utilities, Agriculture) | ||

| By Frequency Band | Sub-6 GHz (3.5 GHz, 4.9 GHz, 5 GHz) | |

| mmWave (24-29 GHz, 37-40 GHz, 60 GHz) | ||

| By Deployment Mode | Indoor CPE | |

| Outdoor CPE | ||

| By Country | Brazil | |

| Chile | ||

| Colombia | ||

| Peru | ||

| Argentina | ||

| Mexico | ||

| Rest of South America (Panama, Costa Rica, Uruguay, Guatemala, and Others) |

Key Questions Answered in the Report

What is the projected value of South America’s Fixed Wireless Access market in 2030?

The market is forecast to reach USD 9,140.42 million by 2030.

Which segment grows fastest within Fixed Wireless Access services?

Commercial applications grow at a 24.73% CAGR through 2030.

Why are services outpacing hardware in revenue growth?

Operators bundle installation, maintenance, and cloud add-ons, creating stable recurring income.

How does spectrum refarming aid Fixed Wireless Access expansion?

It releases mid-band frequencies without fresh auction costs, freeing capital for network builds.

Which country records the quickest Fixed Wireless Access growth?

Chile is expected to expand at a 23.19% CAGR through 2030.

What limits mmWave deployment in tropical zones?

Heavy rainfall in northern regions degrades high-frequency link reliability, restricting coverage.

Page last updated on: