Fixed Wireless Access Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 43.47 Billion |

| Market Size (2031) | USD 84.37 Billion |

| Growth Rate (2026 - 2031) | 14.18% CAGR |

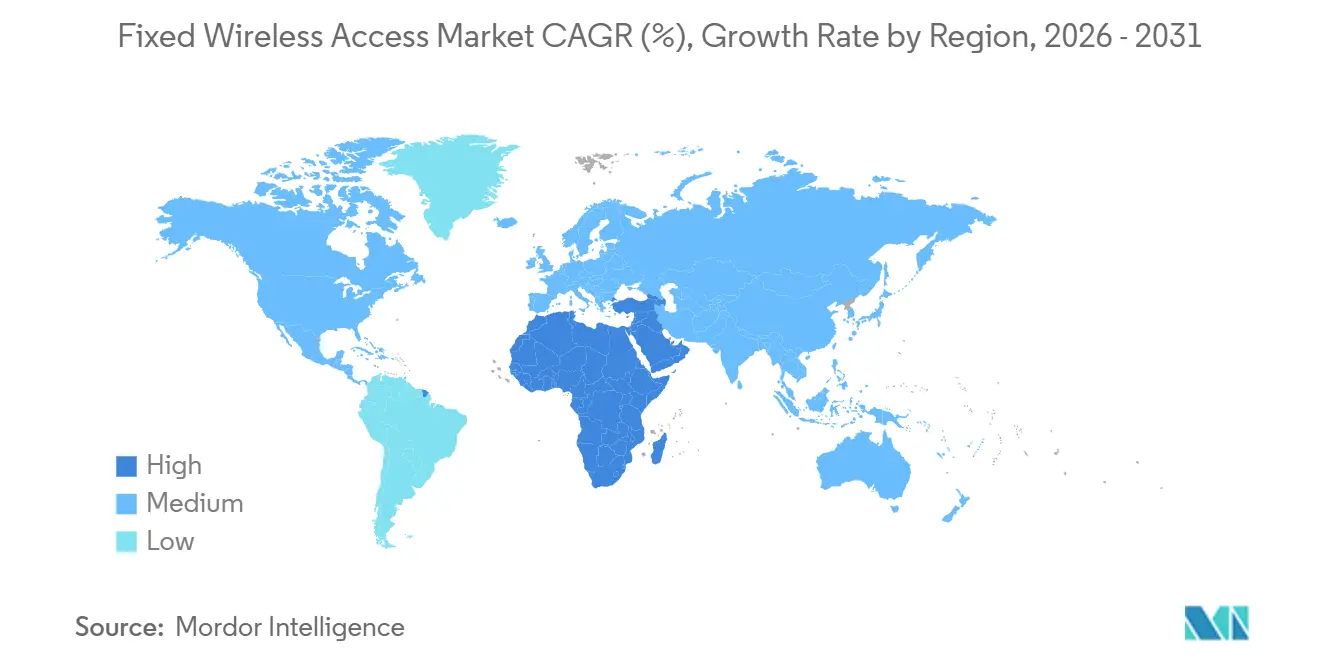

| Fastest Growing Market | Africa |

| Largest Market | North America |

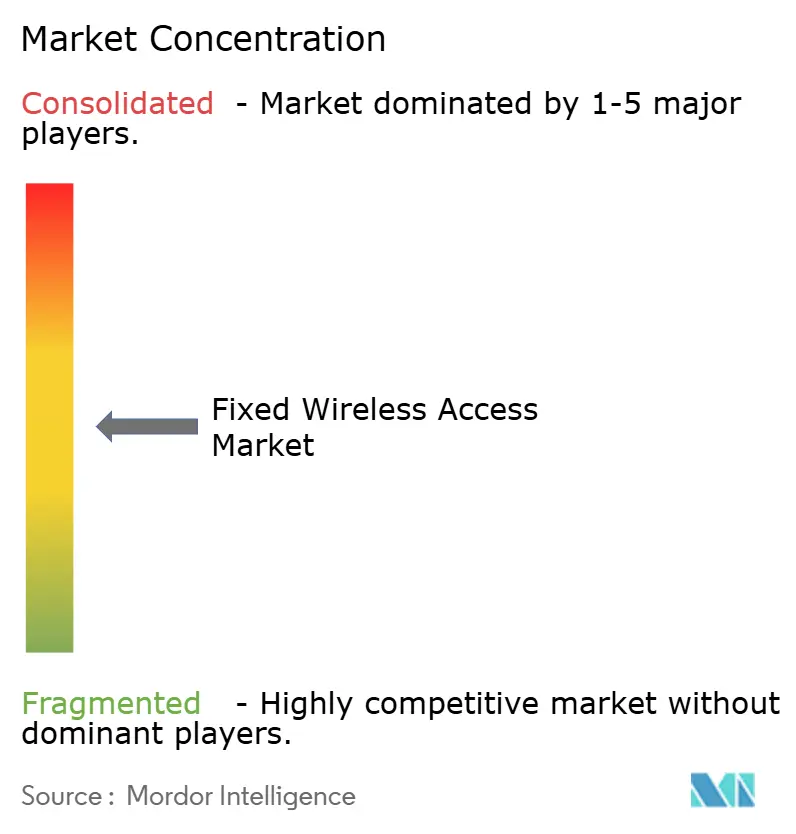

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Fixed Wireless Access Market Analysis by Mordor Intelligence

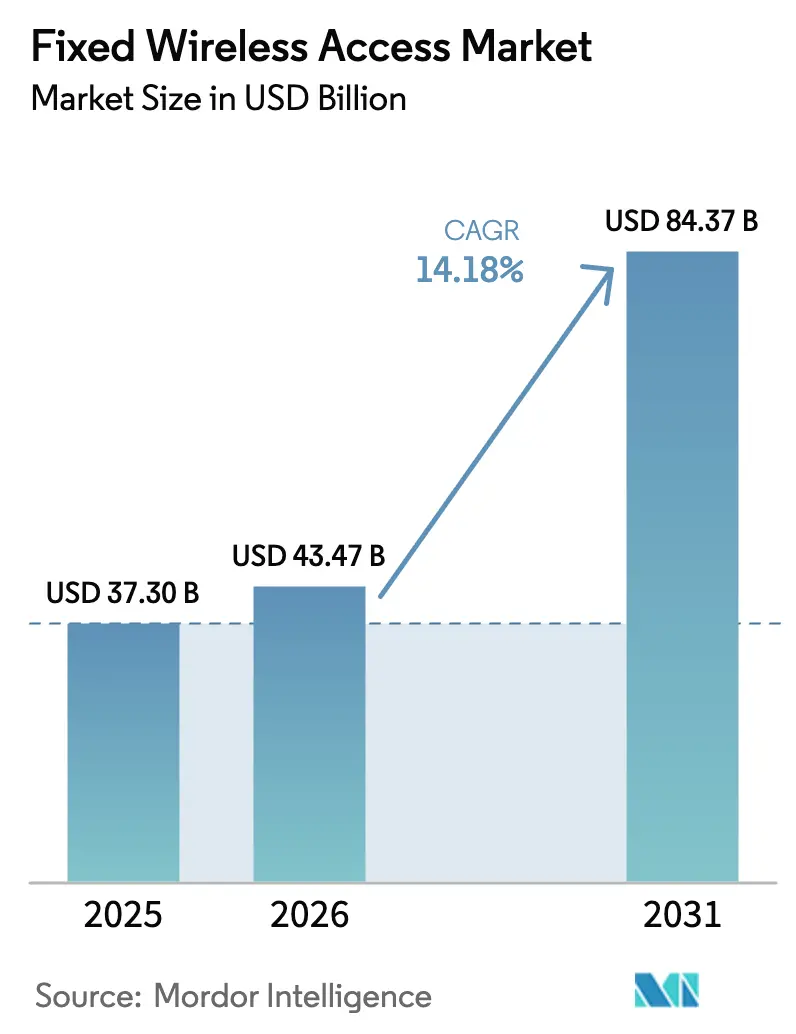

The Fixed Wireless Access Market size is expected to increase from USD 37.30 billion in 2025 to USD 43.47 billion in 2026 and reach USD 84.37 billion by 2031, growing at a CAGR of 14.18% over 2026-2031.

Ongoing 5G mid-band rollouts, nationwide spectrum allocations, and AI-enabled customer-premise equipment are tipping the economics of last-mile connectivity in favor of wireless, especially in suburban and rural zones. Operators are leaning on fixed wireless because trench-and-conduit fiber builds remain expensive, while policy makers have declared FWA an eligible technology under multiple broadband stimulus programs. Hardware still generates most revenue, yet services are expanding faster as carriers pivot toward recurring subscriptions, managed security, and SD-WAN backup packages. Residential demand dominated in 2025, but government, public-safety, and enterprise users are now adopting FWA for rapid disaster recovery and branch resilience. Across bands, sub-6 GHz spectrum supplies the core coverage footprint, whereas mmWave supports multi-gigabit speeds in high-rise districts where population density justifies dense small-cell grids.

Key Report Takeaways

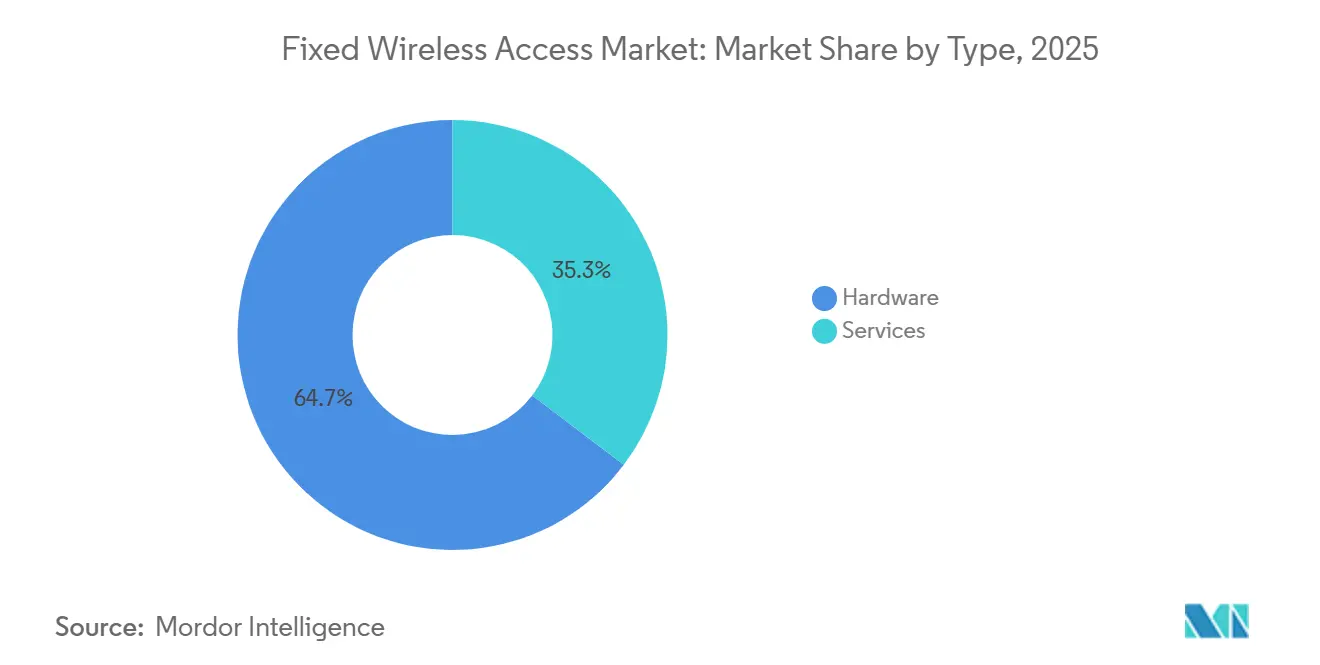

- By type, hardware led with 64.68% revenue share in 2025, while services are forecast to advance at a 15.36% CAGR through 2031.

- By application, residential connections captured 71.91% share in 2025, whereas government and public safety usage is predicted to grow at 14.77% CAGR to 2031.

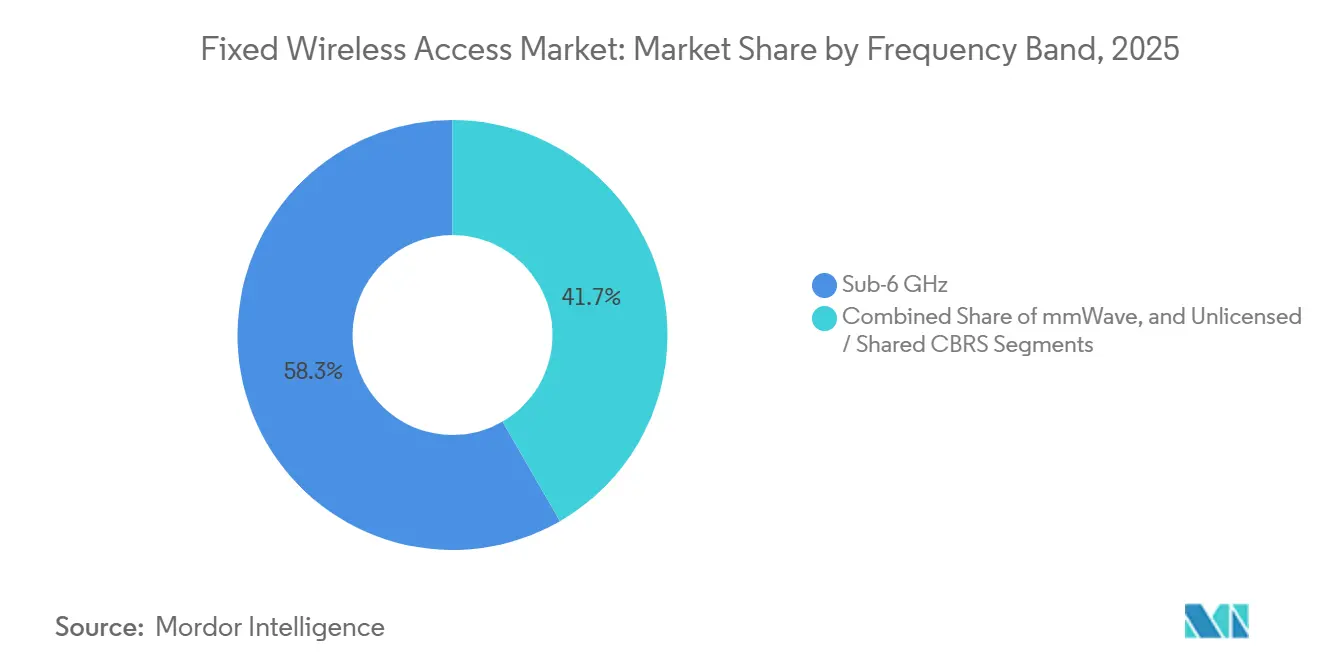

- By frequency band, sub-6 GHz held 58.33% of the Fixed Wireless Access market share in 2025, while mmWave deployments are set to expand at 14.47% CAGR over the outlook.

- By deployment mode, indoor CPE commanded a 67.47% share of the Fixed Wireless Access market size in 2025, yet self-install window-mount units are on track to rise at 14.53% CAGR to 2031.

- By geography, North America generated 33.56% of 2025 revenue, whereas Africa is expected to post the fastest regional CAGR at 15.06% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Fixed Wireless Access Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 5G roll-out accelerating gigabit-class FWA | +3.2% | North America and Asia-Pacific first movers | Medium term (2-4 years) |

| Rural broadband stimulus programmes | +2.8% | North America, Europe, select Asia-Pacific markets | Medium term (2-4 years) |

| FWA as cost-effective last-mile alternative to fiber | +2.5% | Global suburban and rural zones | Long term (≥ 4 years) |

| Enterprise SD-WAN backup connectivity demand | +1.9% | Enterprise hubs worldwide | Short term (≤ 2 years) |

| Spectrum auction design favoring mid-band sharing | +1.6% | North America, Europe, Middle East | Medium term (2-4 years) |

| AI-optimized CPE self-install reducing truck rolls | +1.4% | Highest uptake in North America | Short term (≤ 2 years) |

| Rise of corporate net-zero targets driving wireless power-efficient access | +1.2% | North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

5G Rollout Accelerating Gigabit-Class FWA

Mid-band 5G between 3.3 GHz and 4.2 GHz combines coverage and capacity, making gigabit-class FWA commercially viable. U.S. operators launched 5G home internet in more than 70 metropolitan areas during 2024, delivering median download speeds above 300 Mbps and peaks above 1 Gbps. Carriers in Japan, South Korea, and India mirrored this push, using existing mobile sites to avoid long fiber build-outs. Per-bit delivery cost falls by roughly 40% when operators shift from LTE to 5G New Radio, allowing competitive pricing against cable incumbents. Industry forecasts show global FWA connections exceeding 330 million by 2029, with 5G accounting for nearly all net additions after 2026.

Rural Broadband Stimulus Programmes

The United States BEAD initiative earmarked USD 42.45 billion in 2024 for unserved locations and explicitly labeled FWA as an acceptable solution.[1]National Telecommunications and Information Administration, “Broadband Equity, Access, and Deployment Program,” ntia.gov States such as Texas and Montana are directing funds toward wireless builds where fiber costs exceed USD 10,000 per passing. Europe’s Digital Decade policy takes a similar stance, permitting FWA in areas where fiber economics are unfavorable, provided symmetrical 100 Mbps is guaranteed. India’s BharatNet Phase III and Australia’s Regional Broadband Scheme also include FWA eligibility, anchoring multi-year demand pipelines.

FWA as Cost-Effective Last-Mile Alternative to Fiber

Fiber-to-the-home construction averages USD 2,500-USD 5,000 per passing in U.S. suburbs, whereas FWA capex runs USD 300-USD 800 per subscriber, including radio and CPE.[2]Nokia, “Nokia FastMile 5G Gateway,” nokia.com This 5-to-10x cost edge shortens payback to less than two years when neighborhood penetration tops 20%. Operators bypass trenching, permitting, and right-of-way delays, reducing time to market from more than a year for fiber to fewer than six months for FWA. South African, Mexican, and Brazilian carriers apply the same model to leapfrog copper loops and reach underserved households.

Enterprise SD-WAN Backup Connectivity Demand

Businesses adopt FWA as a secondary link that kicks in instantly when terrestrial fiber goes down. SD-WAN orchestration from leading router vendors automates failover, ensuring video meetings and cloud workflows stay live. Carriers bundle gigabit-class FWA with managed security and monitoring, creating high-margin service tiers. Financial, healthcare, and retail chains cite resilience mandates and hybrid work as purchase drivers. Enterprises also subsidize FWA for remote employees who face unreliable cable connections.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Spectrum scarcity and regulatory uncertainty | -1.8% | Asia-Pacific and Europe hot spots | Medium term (2-4 years) |

| High mmWave densification capex | -1.5% | Urban cores worldwide | Long term (≥ 4 years) |

| Fiber price erosion compressing FWA ARPU | -1.3% | Americas, Europe, parts of Asia-Pacific | Medium term (2-4 years) |

| Weather-induced signal degradation in mmWave bands | -0.9% | Tropical and monsoon climates | Short term (≤ 2 years) |

| State-aid rules limiting subsidised FWA deployments | -0.3% | European Union (EU) Member States | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fiber Price Erosion Compressing FWA ARPU

Cable and fiber incumbents lowered gigabit tariffs by up to 20% during 2024-2025, squeezing average revenue per user for wireless competitors. Some carriers now bundle FWA with mobile unlimited plans, discounting combined service by USD 10-USD 25 to sustain subscriber growth. The strategic pivot shifts competition from pure price to experiential factors such as rapid self-installation, month-to-month contracts, and responsive customer support.

Weather-Induced Signal Degradation in mmWave Bands

Millimeter-wave signals above 24 GHz attenuate sharply in heavy rain, losing more than 10 dB per kilometer at precipitation rates above 25 mm per hour.[3]IEEE, “Rain Attenuation Studies for 5G mmWave Communications,” ieeexplore.ieee.org Operators counter by adopting dual-band CPE that falls back to sub-6 GHz during storms, yet this design raises device costs. In tropical zones, carriers limit mmWave to short-range links or indoor mesh deployments, restricting its market footprint.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type Hardware and Services

Hardware accounted for 64.68% of 2025 revenue, mirroring the installed base of indoor gateways, outdoor units, and small-cell radios. Despite this lead, services revenue is set to outpace hardware at 15.36% CAGR through 2031, as operators lean on subscription models for stable cash flow. The Fixed Wireless Access market size for services is projected to rise from USD 15.4 billion in 2026 to nearly USD 32 billion by 2031. Subsidized or zero-cost CPE tactics accelerate subscriber onboarding, letting carriers recoup device spend over 24- or 36-month plans.

Managed-service offerings span network monitoring, cloud-hosted security, and real-time quality analytics. Deutsche Telekom’s machine-learning engine predicts device failure and dispatches replacements before outages occur, cutting churn and service calls. Access-unit shipments are also shifting toward multi-role devices that double as mesh nodes, reducing backhaul costs and expanding indoor reach.

By Application Residential and Government Leadership

Residential demand captured 71.91% of 2025 connections, underpinning FWA’s original value proposition as a cable and DSL substitute. Yet government and public-safety users now represent the fastest-growing slice, advancing at 14.77% CAGR on resilience mandates. First responder agencies in the United States gained 5G-certified FWA gear for mobile command posts in 2024, while Japan’s prefectural governments must equip backup wireless links by 2026.

Commercial chains favor FWA for rapid store openings when leased lines are unavailable on short notice. Coffee shops, logistics warehouses, and hospitality venues report lower total connectivity cost and faster provisioning than legacy DSL. Industrial campuses see value in private 5G slices that support robotics and low-latency automation, expanding the Fixed Wireless Access market beyond pure broadband.

By Frequency Band Sub-6 GHz and mmWave

Sub-6 GHz frequencies delivered 58.33% of 2025 revenue due to their wide coverage radius and better building penetration. The Fixed Wireless Access market size tied to these bands remains dominant, yet mmWave is rising at 14.47% CAGR, unlocking 2-4 Gbps speeds in skyscraper clusters. U.S. carriers demonstrated peaks above 4 Gbps in dense cores, while Korean operators achieved 2 Gbps service in Seoul’s Gangnam district.

Concurrent growth is visible in shared CBRS bands, which allow enterprises and regional ISPs to deploy wireless broadband without buying spectrum licenses. Neutral-host campus networks running in 3.55-3.7 GHz slots serve stadiums and airports, widening the addressable customer base.

By Deployment Mode Indoor, Outdoor, and Self-Install

Indoor gateways made up 67.47% of deployment share in 2025, but self-install window-mount devices will rise at 14.53% CAGR as AI-driven beam-forming cuts set-up time from hours to minutes. One national carrier reports 90% self-install success, eliminating costly truck rolls that historically consumed up to 30% of first-year revenue.

Outdoor CPE remains vital in low-density areas where stronger signal is mandatory. Hybrid designs featuring detachable antennas are gaining traction, combining the simplicity of indoor units with the reach of rooftop gear. Vendors are converging toward integrated Wi-Fi 7 and 6 GHz support, preparing for bandwidth-intensive applications such as cloud gaming and VR streaming.

Geography Analysis

North America generated 33.56% of 2025 revenue, buoyed by aggressive U.S. and Canadian rollouts that leverage mid-band spectrum cleared in recent auctions. The Fixed Wireless Access market share in the region is stabilizing as household penetration tops 15%, prompting carriers to chase incremental growth in rural clusters. Federal programs continue to reimburse capital spend, although competition from discounted fiber is intensifying.

Africa is set to deliver the fastest growth at 15.06% CAGR through 2031. Operators in South Africa, Kenya, Nigeria, and Egypt build on existing LTE towers, vaulting over copper and limited fiber grids.[4]Safaricom, “5G Home Internet Launch in Kenya,” safaricom.co.ke Price points often undercut wired alternatives by 30%-40%, prompting rapid subscriber adoption among mobile-first households.

Asia-Pacific remains a scale engine where India, China, and Japan deploy FWA to close digital gaps in remote regions. India’s flagship 5G FWA service targets 100 million households at pricing roughly 40% below cable. In the Middle East, sovereign spectrum allocations allow carriers in Saudi Arabia and the United Arab Emirates to ship multi-gigabit residential and enterprise packages, while Europe’s growth trails due to state-aid rules that still prioritize fiber builds.

Mordor Intelligence provides coverage of the fixed wireless access market across other key regional markets, including Middle East, South America, Africa, North America, and Asia, each with their regulatory frameworks and demand patterns. Detailed country-level analysis extends to France and Germany incorporating local coverage and market participation, as required.

Competitive Landscape

The vendor ecosystem shows moderate concentration. Five radio access suppliers account for roughly 60% of equipment shipments, yet more than a dozen CPE makers serve operators, preventing one-sided pricing power. Carriers diversify their supply chains by awarding parallel contracts to at least two radio vendors, balancing risk and bargaining leverage. Mobile operators are the chief disruptors, taking broadband market share from cable and fiber incumbents by bundling mobile plans with home internet.

Start-ups such as Tarana Wireless and Cambium Networks fill performance gaps where legacy LTE falters, offering proprietary waveforms or ruggedized outdoor units for industrial and rural deployments. Chipset competition remains intense, with Qualcomm, MediaTek, and Samsung vying to embed AI accelerators that predict network congestion and steer traffic accordingly. Release 18 specifications promise lower-cost devices and flexible network slicing, raising the stakes for all suppliers.

Price competition is moving beyond consumer tiers. Enterprises and public agencies issue tenders for managed FWA links that guarantee throughput under congestion, often packaged with SD-WAN and security services. The emerging field of private 5G over shared bands creates white-space opportunity for integrators and cloud providers eager to tack edge-compute workloads onto wireless backbones.

Fixed Wireless Access Industry Leaders

Huawei Technologies Co. Ltd.

Nokia Corporation

Ericsson AB

Qualcomm Technologies Inc.

Samsung Electronics Co. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: T-Mobile expanded 5G Home Internet to an additional 10 million rural U.S. households, leveraging fresh 2.5 GHz spectrum and AI network planning tools.

- November 2025: Verizon and Ericsson began rolling out 5G Standalone FWA across 25 U.S. metro areas, adding network slices for public safety.

- October 2025: Reliance Jio announced JioAirFiber surpassed 10 million subscribers, the fastest adoption curve globally.

- September 2025: Qualcomm introduced the Snapdragon X80 modem with AI-based predictive optimization and 6 GHz unlicensed support.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study considers the fixed wireless access (FWA) market as all revenue earned from devices and services that deliver last-mile broadband using licensed or lightly licensed cellular spectrum, primarily 4G LTE and 5G, to a static customer premises equipment (CPE) that then distributes Wi-Fi or Ethernet within homes and businesses. The model tracks hardware shipments, managed service fees, and related subscription revenues in every major region.

Scope exclusion: Satellite or unlicensed Wi-Fi backhaul solutions are not included.

Segmentation Overview

- By Type

- Hardware

- Consumer Premise Equipment (CPE)

- Access Units (Femto and Picocells)

- Services

- Hardware

- By Application

- Residential

- Commercial

- Industrial

- Government and Public Safety

- By Frequency Band

- Sub-6 GHz

- mmWave (Above 24 GHz)

- Unlicensed / Shared CBRS

- By Deployment Mode

- Indoor CPE

- Outdoor CPE

- Self-Install Window-Mount CPE

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia

- Middle East and Africa

- Middle East

- Israel

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

To ground the numbers, our team held structured calls with network planners at top mobile operators, senior engineers at CPE vendors, and regulators overseeing universal-service programs across North America, Europe, Asia Pacific, the Gulf states, and Latin America. Insights on 5G deployment timelines, subsidy uptake, and outdoor CPE pricing fed directly into the model and reconciled any mismatches spotted during desk analysis.

Desk Research

We first mined open-source benchmarks from respected bodies such as the International Telecommunication Union, the FCC, the European 5G Observatory, GSMA Intelligence, Ericsson Mobility Report, and national statistics portals, which supply subscriber counts, spectrum allocations, and rural broadband targets. Company filings, investor decks, and large-carrier tariff sheets added typical average revenue per user. Paid intelligence sets that Mordor analysts access, including D&B Hoovers for operator financials and Dow Jones Factiva for deal flow, helped cross-check growth hotspots. The sources named illustrate our desk research foundation; many additional references were reviewed for data points, context, and gap confirmation.

Market-Sizing & Forecasting

Mordor Intelligence applied a top-down build that aligns national household and business counts with broadband penetration targets, spectrum roll-outs, and government funding pools, which are then translated into potential FWA subscriptions. Selected bottom-up checks, carrier reported subscriber adds, sampled CPE average selling prices, and tower lease data validated totals and flagged over-inflated pockets. Key variables include 5G base-station growth, CPE shipment forecasts, spectrum auction schedules, rural broadband subsidies, typical ARPU shifts, and fiber passings per capita. An error-corrected multivariate regression, informed by primary expert consensus, projects each driver through the forecast period and produces the growth rate that underpins our baseline.

Data Validation & Update Cycle

Outputs undergo variance scans versus independent traffic, device, and capex trackers before a senior reviewer sign-off. Reports refresh every twelve months, with interim updates triggered by spectrum policy changes, major subsidy awards, or step-shifts in carrier guidance. Just before delivery, an analyst re-runs the checks so clients receive the latest view.

Why Mordor's Fixed Wireless Access Market Baseline Earns Trust

Published estimates rarely match because firms diverge on what revenue streams, CPE classes, and forecast windows they include.

Key gap drivers are scope creep into satellite broadband, reliance on aggressive CPE price deflation curves, conversion of connection counts to revenue without validating ARPU, and infrequent refresh cycles that ignore fast-moving 5G deployments.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 39.06 B (2025) | Mordor Intelligence | - |

| USD 161.27 B (2024) | Global Consultancy A | Combines FWA with all cellular backhaul and includes satellite links |

| USD 36.54 B (2024) | Industry Publisher B | Uses limited operator sample and flat ARPU, undercounts emerging Asia volumes |

| USD 145.34 B (2024) | Trade Journal C | Applies single global ASP and projects revenue directly from device shipments |

The comparison shows that once inconsistent scopes and unchecked assumptions are stripped away, Mordor's disciplined mix of verified variables, frequent updates, and dual-layer validation yields a balanced baseline practitioners can reproduce and trust for strategic planning.

Key Questions Answered in the Report

What is the expected revenue for the global Fixed Wireless Access market in 2031?

The market is projected to reach USD 84.37 billion by 2031, up from USD 43.47 billion in 2026.

How fast is the Fixed Wireless Access market expected to grow?

The market is forecast to post a 14.18% CAGR between 2026 and 2031.

Which region is projected to grow fastest in Fixed Wireless Access?

Africa is set to record the highest regional CAGR at 15.06% through 2031, driven by mobile-first economies.

Why are operators choosing FWA over fiber in rural areas?

FWA capital expenditure per subscriber ranges from USD 300-USD 800, far below the USD 2,500-USD 5,000 per-passing costs typical for fiber-to-the-home builds.

What technology shift is enabling gigabit-class Fixed Wireless service?

Mid-band 5G spectrum between 3.3 GHz and 4.2 GHz delivers better capacity-coverage balance, reducing per-bit cost by roughly 40% compared with LTE.

How are enterprises using Fixed Wireless Access?

Firms deploy FWA as an SD-WAN backup link, ensuring immediate failover during fiber outages and supporting hybrid work connectivity.

Page last updated on: