Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

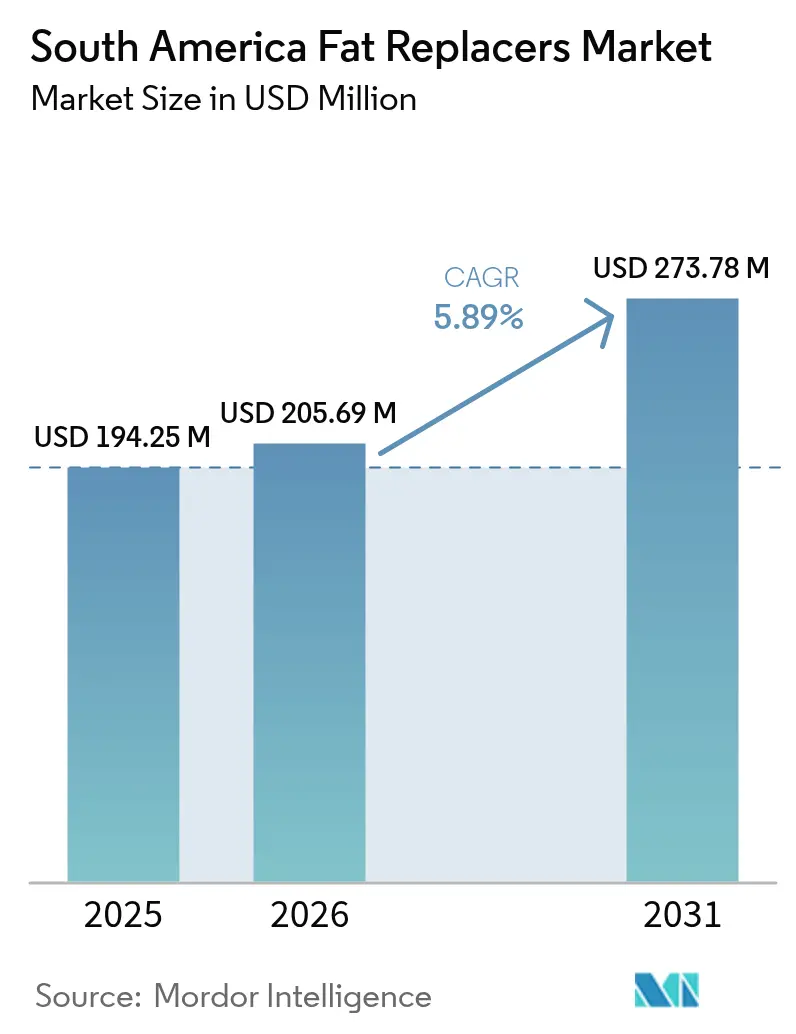

| Base Year Market Size (2025) | USD 194.25 Million |

| Market Size (2026) | USD 205.69 Million |

| Market Size (2031) | USD 273.78 Million |

| Growth Rate (2026 - 2031) | 5.89% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Fat Replacers Market Analysis by Mordor Intelligence

South America fat replacers market size in 2026 is estimated at USD 205.69 million, growing from 2025 value of USD 194.25 million with 2031 projections showing USD 273.78 million, growing at 5.89% CAGR over 2026-2031. The fat replacers market growth is driven by regulatory changes, increasing consumer demand for healthier processed foods, and advancements in plant-based product development. The implementation of clean-label requirements and front-of-package (FOP) labeling regulations has increased the adoption of carbohydrate, protein, and lipid-based technologies. These technologies enable manufacturers to reduce saturated fat content while maintaining product texture, taste, and shelf stability. Companies are expanding their local research and development capabilities, utilizing agricultural by-products for functional ingredients, and establishing strategic partnerships to secure raw materials and enhance technical expertise. The market development in South America is particularly influenced by Brazil's established functional food regulations and Argentina's updated labeling requirements, creating opportunities for companies that can validate fat reduction claims and efficiently navigate regulatory processes.

Key Report Takeaways

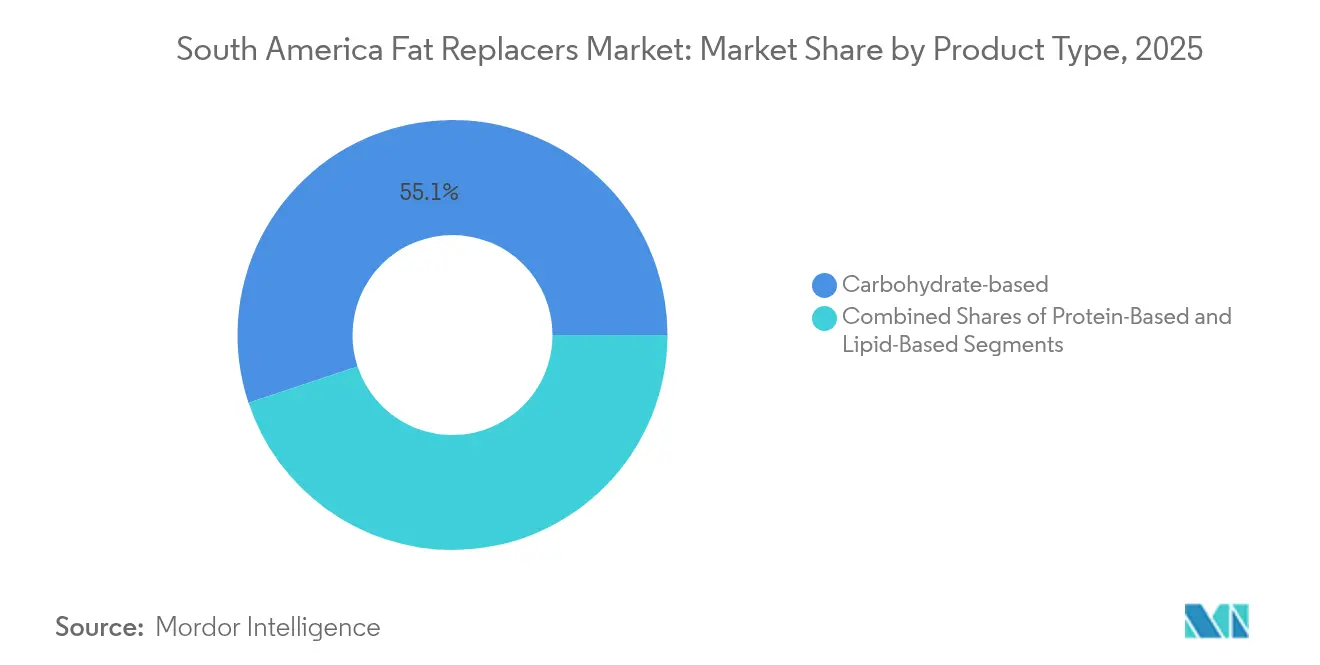

- By type, carbohydrate-based solutions led with 55.10% of South America's fat replacers market share in 2025, while protein-based alternatives posted the fastest 7.18% CAGR through 2031.

- By source, plant-based offerings accounted for 63.05% share of the South America fat replacers market size in 2025 and are projected to expand at 7.46% CAGR between 2026-2031.

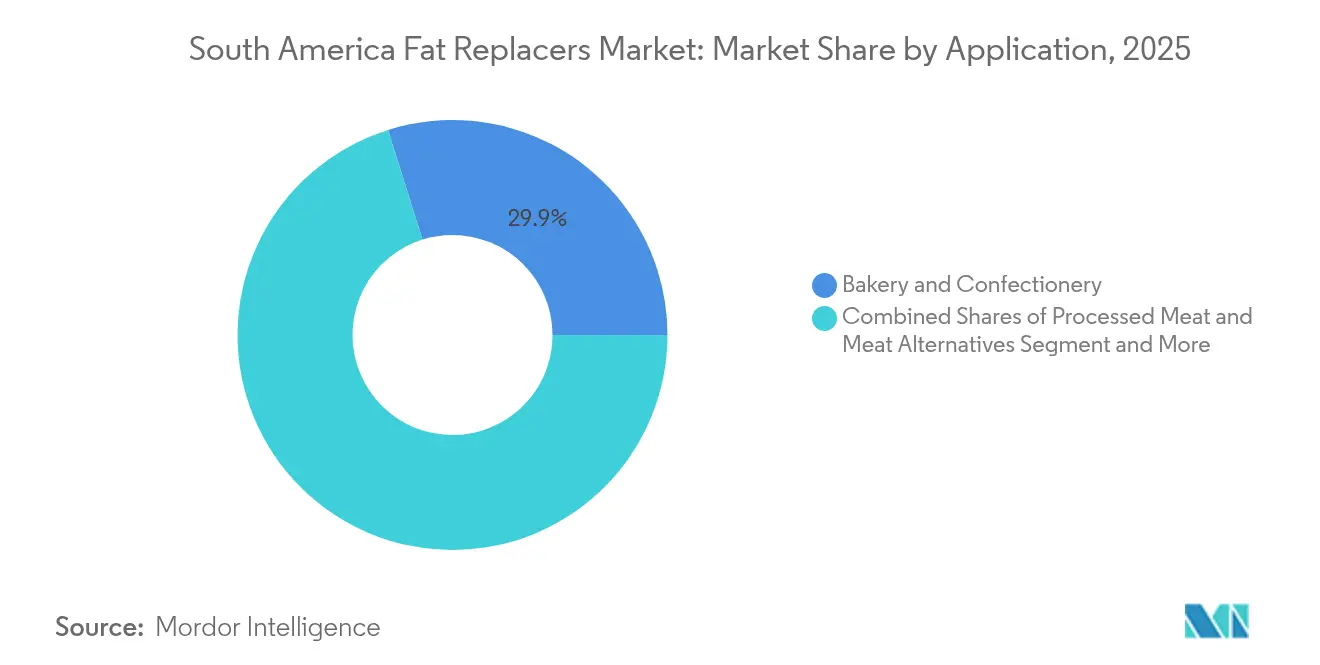

- By application, bakery and confectionery captured 29.85% revenue share in 2025; processed meat and meat alternatives are expected to grow at a 7.05% CAGR to 2031.

- By geography, Brazil held 46.55% of the South America fat replacers market in 2025, whereas Argentina records the highest 6.42% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South America Fat Replacers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing consumer demand for healthier processed foods | +1.8% | Brazil, Argentina, Colombia | Medium term (2-4 years) |

| Growth in functional food and beverage segment | +1.5% | Brazil, Argentina | Long term (≥ 4 years) |

| Regulatory push for nutritional labeling | +1.2% | Brazil, Argentina, Colombia | Short term (≤ 2 years) |

| Rising demand for vegan and plant-based products | +1.0% | Brazil, Argentina | Medium term (2-4 years) |

| Increased adoption of low-calorie traditional and regional foods | +0.8% | Colombia, Rest of South America | Long term (≥ 4 years) |

| Expansion of low-fat dairy product lines | +0.7% | Brazil, Argentina | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Consumer Demand for Healthier Processed Foods

McKinsey's regional survey shows that 46% of South American millennials to pay premiums for healthier packaged foods after the pandemic[1]Source: McKinsey & Company, “Latin American Consumer Health Survey,” mckinsey.com. Retail scans confirm declining sales of high-saturated-fat SKUs, motivating Brazilian and Argentinian manufacturers to retrofit flagship lines with carbohydrate-based bulking agents or protein emulsifiers. Reformulation preserves brand equity, avoids re-registration costs, and secures shelf space, especially in supermarkets that now rank products on nutrition scores. Mass-market bakeries have reduced average fat content per serving, illustrating how incremental tweaks, rather than entirely new launches, can defend market share. Similar dynamics appear in Colombia's ready-meal aisles, where low-fat arepas gained prominence despite historically fat-rich recipes. The increasing consumer awareness of health risks associated with high-fat diets has prompted manufacturers to invest in fat replacement technologies. Government initiatives promoting healthier food choices have further accelerated the adoption of fat replacers across the South American food industry.

Growth in Functional Food and Beverage Segment

The market for fat replacers is experiencing growth due to several key factors. Functional beverages containing plant-derived emulsifiers show higher growth rates compared to carbonated soft drinks in urban markets. Baru almond protein isolates serve dual purposes by providing protein content and enabling viscosity control, which facilitates sugar reduction and fat replacement. The streamlined MERCOSUR mutual-recognition procedures enable efficient cross-border shipments, reducing delivery times for Argentine co-packers targeting the functional dairy market. The consistent increase in disposable incomes supports the growth of premium-priced functional snacks, ensuring sustained market expansion. Apart from that, ANVISA's 1999 recognition of "alimentos funcionais" normalized health claims within Brazil's regulatory lexicon, enabling straightforward label statements linking fat reduction to cardiovascular benefits[2]Source: ANVISA, “Legislação de Alimentos Funcionais e Novos Alimentos,” anvisa.gov.br. Consumer awareness of health benefits associated with fat replacers encourages manufacturers to diversify their product offerings. Regional food processors continue to invest in research and development to develop effective fat-replacement solutions that maintain product quality while reducing calories.

Regulatory Push for Nutritional Labeling

Argentina's ANMAT Resolution 267/2024 replaced black octagon warnings with a mandatory FOP disclosure grid that lists total fat, saturated fat, and calories per 100 g according to the Ministry of Health, Argentina[3]Source: ANMAT, “Resolución 267/2024 Etiquetado Frontal,” argentina.gob.ar. The 2026 compliance deadline for new labeling regulations is accelerating the adoption of fat replacer ingredients as manufacturers seek to improve their products' nutrient profiles. Brazil's ANVISA reinforced this trend by implementing enhanced labeling requirements in March 2024. The existing MERCOSUR additive regulations already include approved carbohydrate- and protein-based replacers, allowing manufacturers to focus on reformulation rather than ingredient approval processes. Limited implementation timeframes are pushing manufacturers toward established global suppliers who offer ready-to-use solutions and local technical support. These regulatory developments across South America have generated immediate market demand for fat replacers, particularly in high-fat processed food segments. Food manufacturers are directing resources toward product reformulation efforts to maintain organoleptic properties while meeting new requirements.

Rising Demand for Vegan and Plant-Based Products

Trend in plant-based adoption has influenced other South American markets, with expanding vegan and flexitarian communities in São Paulo, Buenos Aires, and Bogotá driving purchase decisions. Plant-based formulations naturally reduce saturated fat content, leading to increased use of soy, chickpea, and mycoprotein emulsifiers for texture enhancement. NotCo's AI technology reduces prototype development time to 3 months, enabling manufacturers to introduce dairy-free spreads and pâtés tailored to regional preferences. Green-banana biomass combined with teff flour reduces recipe fat while maintaining texture quality. While cost remains a challenge, manufacturers address this through vertical integration and utilization of agricultural waste streams. Consumer awareness of health benefits and sustainability drives continuous innovation in fat replacement technologies. Regional food manufacturers invest in research and development to develop cost-effective, locally sourced fat replacement solutions that satisfy both nutritional requirements and sensory expectations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Low consumer awareness of fat replacers | -0.9% | Colombia, Rest of South America | Short term (≤ 2 years) |

| Technical challenges in replicating taste and texture | -0.7% | Brazil, Argentina, Colombia | Medium term (2-4 years) |

| Consumer perception of inferiority in low-fat products | -0.5% | Brazil, Argentina | Medium term (2-4 years) |

| Shelf-life and storage challenges with certain fat replacers | -0.4% | Colombia, Rest of South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Low Consumer Awareness of Fat Replacers

The fat replacers market faces significant challenges in consumer adoption and market penetration. Despite the growing health consciousness among consumers, the lack of awareness about fat replacers remains a major obstacle. Without dedicated educational campaigns, consumers tend to choose traditional full-fat products, particularly in rural areas. Retailers avoid emphasizing "fat-reduced via fiber" claims on product packaging to prevent alienating traditional customers. While major dairy companies develop QR-code educational microsites, small and medium enterprises lack resources for such initiatives, limiting market penetration in smaller cities. Government-funded nutrition programs may reduce the knowledge gap over the next two years, but immediate purchasing barriers persist. Unclear labeling regulations for fat replacer ingredients and insufficient industry-wide consumer education about product safety and benefits further restrict market growth.

Technical Challenges in Replicating Taste and Texture

The fat replacers market faces several technical constraints. Protein isolates undergo denaturation at temperatures exceeding 190°C in cassava-based snacks, resulting in inconsistent mouthfeel. Carbohydrate bulking agents introduce unwanted sweetness, conflicting with sugar reduction objectives. Manufacturing scale-up encounters difficulties when viscosity increases surpass pump capacities, particularly affecting contract manufacturers with diverse equipment lines. Regional small and medium enterprises experience extended product launch timelines due to repeated formulation adjustments. High-temperature processing stability remains a technical challenge, especially in extruded snack production. The interaction between fat replacers and native food components creates texture and flavor issues requiring extensive reformulation. Some fat replacer compounds demonstrate limited shelf-life stability, requiring additional preservation systems. Temperature-sensitive fat replacers demand specific handling and storage conditions, increasing operational expenses for manufacturers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Protein Innovation Accelerates Despite Carbohydrate Dominance

Carbohydrate-based variants hold 55.10% of the South America fat replacers market share in 2025, primarily due to their lower cost and established performance in high-volume bakery applications. The well-established distribution networks for cassava and corn starches provide stable cost structures for manufacturers serving price-sensitive markets. However, the South America fat replacers market shows a clear shift toward protein-based alternatives, which are growing at a 7.18% CAGR through 2031. These protein-based ingredients meet consumer demands for reduced fat content while providing higher protein content, making them suitable for clean-label products in dairy beverages and sports nutrition bars.

Green-banana biomass combined with chickpea protein achieves a viscosity of 1.4 Pa·s at 25 °C, comparable to palm fat standards in confectionery fillings. This performance reduces the traditional advantages of lipid-based alternatives. The partnership between Enifer and ethanol manufacturer FS demonstrates this shift, as they transform corn-ethanol byproducts into mycoprotein at costs competitive with imported whey. Their pilot facility's planned capacity of 500 t in 2025 may accelerate widespread adoption beyond specialty products. In response, carbohydrate-based manufacturers are combining native starch with soluble fiber to improve moisture retention and product longevity, maintaining their market position in regions where protein ingredients remain expensive. The South American fat replacers market demonstrates a dynamic balance between established carbohydrate-based solutions and emerging protein alternatives, each serving distinct market segments and price points. The ongoing innovation in both categories, coupled with regional manufacturing capabilities, indicates sustained growth potential across multiple food applications.

By Source: Plant-Based Dominance Reflects Sustainability Priorities

Plant-derived ingredients captured 63.05% of the market in 2025 and are on track for a 7.46% CAGR, cementing their leadership through 2031. South America's fat replacers market size for plant-based variants is buoyed by abundant soybean, corn, and emerging crop supply chains. Broad consumer perception of plant sources as “natural” and environmentally friendly offsets taste prejudices that once plagued early formulations. Microbial solutions—led by mycoprotein butter prototypes—collect momentum, yet their combined revenue remains minor compared to botanical inputs.

Brazilian R and D institutes illustrate how agribusiness waste valorization cuts ingredient costs while boosting rural incomes. Microbial-based alternatives, exemplified by Mycorena, report 55% saturated-fat reduction versus dairy butter but must scale fermentation infrastructure and satisfy nascent regulatory pathways. Animal-based replacers persist in specialty charcuterie, yet regulatory scrutiny on cholesterol keeps their outlook stagnant. The success of alternative fat sources depends heavily on technological advancements in production methods and regulatory approvals. Market adoption will likely accelerate as manufacturers overcome these challenges while maintaining cost competitiveness.

By Application: Processed Meat Innovation Drives Growth Despite Bakery Leadership

The bakery and confectionery segment accounted for 29.85% of the South American fat replacers market in 2025, as carbohydrate fibers effectively provide bulk to dough and frostings without affecting baking times. The processed meat and meat alternatives segment is projected to grow at a CAGR of 7.05%, driven by health-focused product reformulations. The South American fat replacers market is witnessing robust expansion as manufacturers develop innovative solutions to meet consumer demands for healthier food options. Rising obesity rates and increasing consumer awareness of the health risks associated with high-fat diets are accelerating the adoption of fat replacers across the region. Fat replacers are gaining prominence in South America as consumers seek healthier food alternatives. The market is experiencing significant growth due to increasing health consciousness and regulatory pressure to reduce fat content in processed foods.

The South American food industry is experiencing significant transformations in fat reduction technologies across multiple segments. Brazil's expanding chilled-meat sector integrates lipid-mimicking hydrocolloids that permit sodium and nitrite reduction, satisfying multilayer health policies. Plant-forward burgers gain mainstream traction through improved juiciness delivered by structured vegetable fats, further lifting demand. Dairy receives tailored innovations like Cargill's Lévia+c, which maintains overrun and melt resistance in ice cream even after a 35% saturated-fat reduction. Beverage use cases remain exploratory, primarily focusing on mouthfeel enhancement in oat or rice milks served in café chains across Buenos Aires and Rio.

Geography Analysis

Brazil stacked up 46.55% of the South American fat replacers market in 2025, thanks to its USD 209 billion food-processing complex and long-standing functional-food regulations that simplify new ingredient clearance, according to the Food Export Association. Brazil's food manufacturing sector demonstrates significant technological advancement in alternative protein production. The country's robust infrastructure supports efficient product development and distribution processes. Companies utilize established cold-chain logistics networks and numerous co-packing facilities to enable nationwide product distribution at competitive costs. Research partnerships between universities and industries in Minas Gerais and São Paulo regions facilitate the integration of international fat replacement technologies into traditional Brazilian foods like pão de queijo.

Argentina follows as the fastest grower at a 6.42% CAGR. ANMAT’s late-2024 decree obliges stricter disclosure of saturated fat and calories, effectively compelling reformulation across bakery, dairy, and ready-meal segments, according to the Government of Argentina. Ingredient vendors focusing on turnkey carbohydrate-fiber blends gain quick traction because large FMCGs prioritize speed-to-compliance. Additionally, Buenos Aires’ incubation hubs host startups engineering algal lipids designed to match charcuterie mouthfeel, widening local supplier choice.

Colombia and the rest of South America offer emerging prospects as public-health authorities inch toward stricter nutrient limits. Economic Commission for Latin America and the Caribbean (ECLAC) projects 11% growth in South American agricultural exports in 2024, enlarging raw-material pools for plant-based fats. Bogotá’s processed-meat plants already experiment with cassava-derived hydrocolloids to satisfy budding urban health awareness. Smaller markets such as Chile and Peru demonstrate consumer uptake of FOP “Nutri-Score”-style labeling pilots, signaling future legislative convergence. Nonetheless, fragmented retail landscapes and lower purchasing power delay ubiquitous adoption.

Competitive Landscape

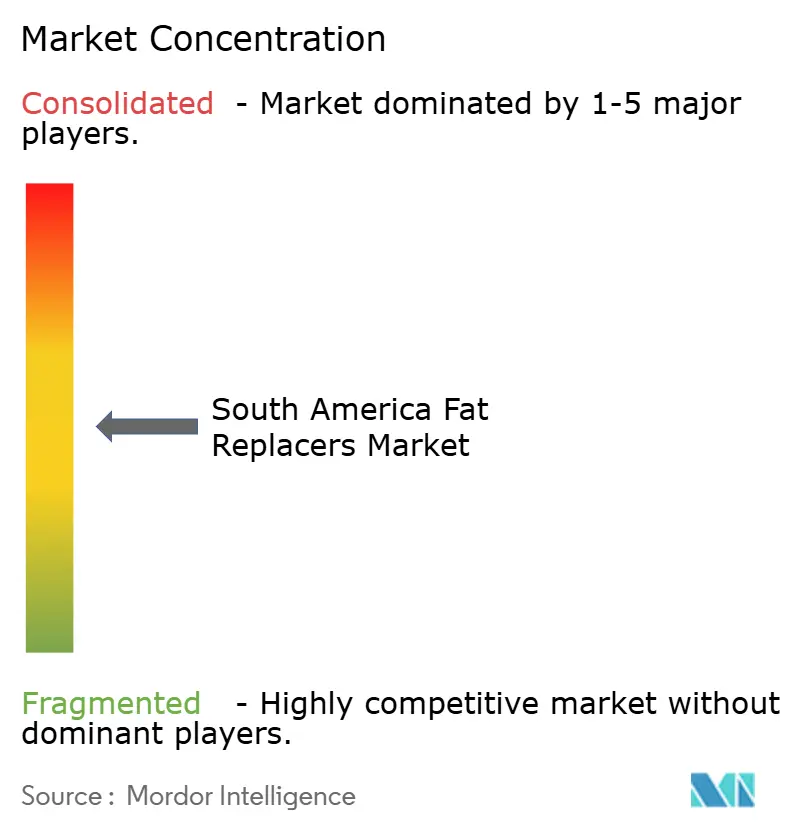

The South American fat replacers market shows moderate concentration, with the top five firms controlling major revenue. Some of the major companies include Cargill, Incorporated, Archer Daniels Midland Co., Ingredion Inc., Tate and Lyle PLC, Kerry Group plc, etc. Global ingredient majors maintain scale advantages, but regional specialists exploit deep knowledge of indigenous crops and localized taste preferences. Tate and Lyle’s intended USD 1.8 billion acquisition of CP Kelco aims to fuse hydrocolloid and sweetening technologies, broadening solutions that deliver simultaneous fat, sugar, and texture optimization. Also, Cargill, Incorporated invests USD 8.5 million in South American facility upgrades to meet WHO iTFA guidelines, positioning its edible oils arm for stricter policy eras.

Localization remains decisive. Cargill’s Lévia+c for Brazilian dairy underscores how bespoke formulation wins over generic global offerings. Enifer’s waste-to-mycoprotein partnership with FS illustrates circular-economy narratives that resonate with regulators and sustainability-minded brands. Start-ups leverage AI and precision fermentation to slash pilot times, placing competitive pressure on incumbents to accelerate their own digitalization roadmaps. Meanwhile, distributors such as IMCD and Brenntag expand value-added application labs that help tier-two clients navigate technical hurdles without heavy R and D spend, ensuring a pipeline of mid-market customers.

Consolidation momentum coexists with vibrant start-up scenes. Venture funding gravitates toward microbial and precision-lipid platforms that address outstanding sensory gaps. Yet, given regulatory lead times and capital intensity, collaborative models—licensing, joint ventures, or toll manufacturing—dominate commercialization strategies. Intellectual-property depth, regional regulatory fluency, and robust technical-service teams collectively decide competitive staying power.

South America Fat Replacers Industry Leaders

Ingredion Inc.

Archer Daniels Midland Co.

Cargill, Incorporated

Kerry Group plc

Tate and Lyle PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Enifer partnered with Brazilian ethanol giant FS to establish a 500-ton pilot facility for mycoprotein production from corn ethanol byproducts, supported by BRL 9.8 million from FINEP. The initiative targets animal nutrition markets in Brazil, Ecuador, and Chile, with potential expansion to human food applications, demonstrating waste stream valorization in fat replacer production.

- May 2025: ADM unveiled a new nutrient factory in Apucarana, Paraná, designed to increase production capacity by 40%. The facility produces customized formulations for poultry, swine, and aquaculture applications, supporting Brazil's growing animal nutrition market expected to grow 2.6% annually.

- September 2024: WEGO launched a sustainable cocoa substitute made from roasted carob pods to address supply challenges and price volatility. The product is low in fat, high in dietary fiber, and free from allergens, positioning it as a healthier alternative for food developers.

- June 2024: Tate and Lyle announced the proposed USD 1.8 billion acquisition of CP Kelco to create a leading global specialty food and beverage solutions business. The transaction enhances capabilities in sweetening, mouthfeel, and fortification technologies critical for fat replacer applications, with completion expected in Q4 2024.

South America Fat Replacers Market Report Scope

The South America Fat Replacers Market is segmented by the source that includes plants and animals. Based on type, the market is divided into carbohydrate-based, protein-based, and lipid-based. The market is also bifurcated on the basis of application which includes bakery and confectionery, beverages, processed meat, convenience food, and others. The study also involves the analysis of regions such as Brazil, Argentina, and the Rest of South America.

By Product Type

| Carbohydrate-Based |

| Protein-Based |

| Lipid-Based |

By Source

| Plant-based |

| Animal-based |

| Microbial-based |

By Application

| Bakery and Confectionery |

| Dairy and Frozen Desserts |

| Beverages |

| Processed Meat and Meat Alternatives |

| Convenience Food/Ready Meals |

| Others |

By Geography

| Brazil |

| Argentina |

| Rest of South America |

| By Product Type | Carbohydrate-Based |

| Protein-Based | |

| Lipid-Based | |

| By Source | Plant-based |

| Animal-based | |

| Microbial-based | |

| By Application | Bakery and Confectionery |

| Dairy and Frozen Desserts | |

| Beverages | |

| Processed Meat and Meat Alternatives | |

| Convenience Food/Ready Meals | |

| Others | |

| By Geography | Brazil |

| Argentina | |

| Rest of South America |

Key Questions Answered in the Report

What is the current size of the South America fat replacers market?

The market is valued at USD 205.69 million in 2026 and is projected to hit USD 273.78 million by 2031.

Which segment grows fastest in the South America fat replacers market?

Protein-based replacers expand at a 7.18% CAGR through 2031, driven by dual fat-reduction and protein-fortification benefits.

How do recent regulations influence market demand?

Argentina’s stricter front-of-package labeling and Brazil’s updated ANVISA framework compel rapid product reformulation, spurring near-term ingredient uptake.

Why are plant-based fat replacers so dominant?

They hold 63.05% share thanks to abundant regional crops, favorable sustainability perceptions, and clean-label positioning.

Which application area offers the highest growth?

Processed meat and meat alternatives show a 7.05% CAGR as oleogel and structured-lipid technologies enable low-fat formulas without sensory compromise.

Page last updated on: