Building Integrated Photovoltaic (BIPV) Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 16.66 Billion |

| Market Size (2031) | USD 47.02 Billion |

| Growth Rate (2026 - 2031) | 23.06% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Building Integrated Photovoltaic (BIPV) Market Analysis by Mordor Intelligence

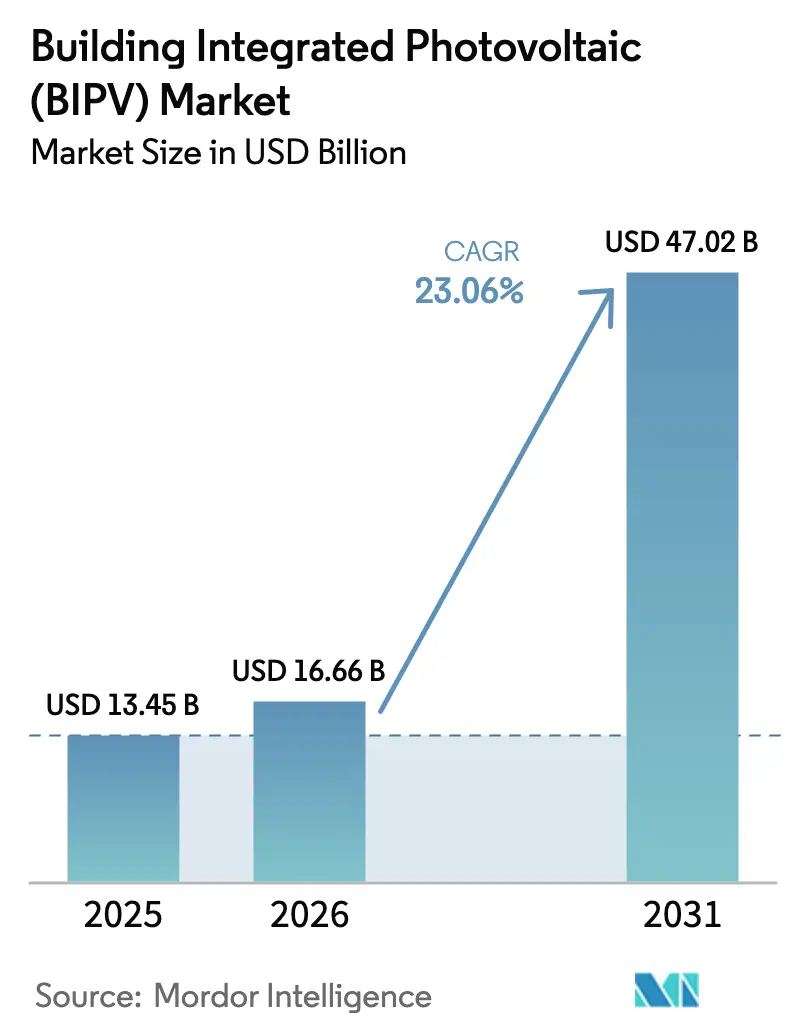

The Building Integrated Photovoltaic Market size is projected to be USD 13.45 billion in 2025, USD 16.66 billion in 2026, and reach USD 47.02 billion by 2031, growing at a CAGR of 23.06% from 2026 to 2031.

The growth trajectory is anchored in zero-carbon building codes, corporate net-zero pledges, and rapid progress in perovskite-silicon tandem cells that raise output without enlarging roof or façade footprints. Lower balance-of-system costs, faster permitting cycles in China and the EU, and insurer acceptance of UL 1703-compliant mounting kits are compressing payback periods to 7-9 years in high-irradiance markets. Developers now specify solar-ready curtain walls at the concept stage, viewing photovoltaic skins as load-bearing components rather than rooftop accessories. Competitive intensity remains moderate, giving architects latitude to choose between crystalline panels, thin-film laminates, or transparent glazing while securing multi-supplier bids that keep module prices on a downward slope.

Key Report Takeaways

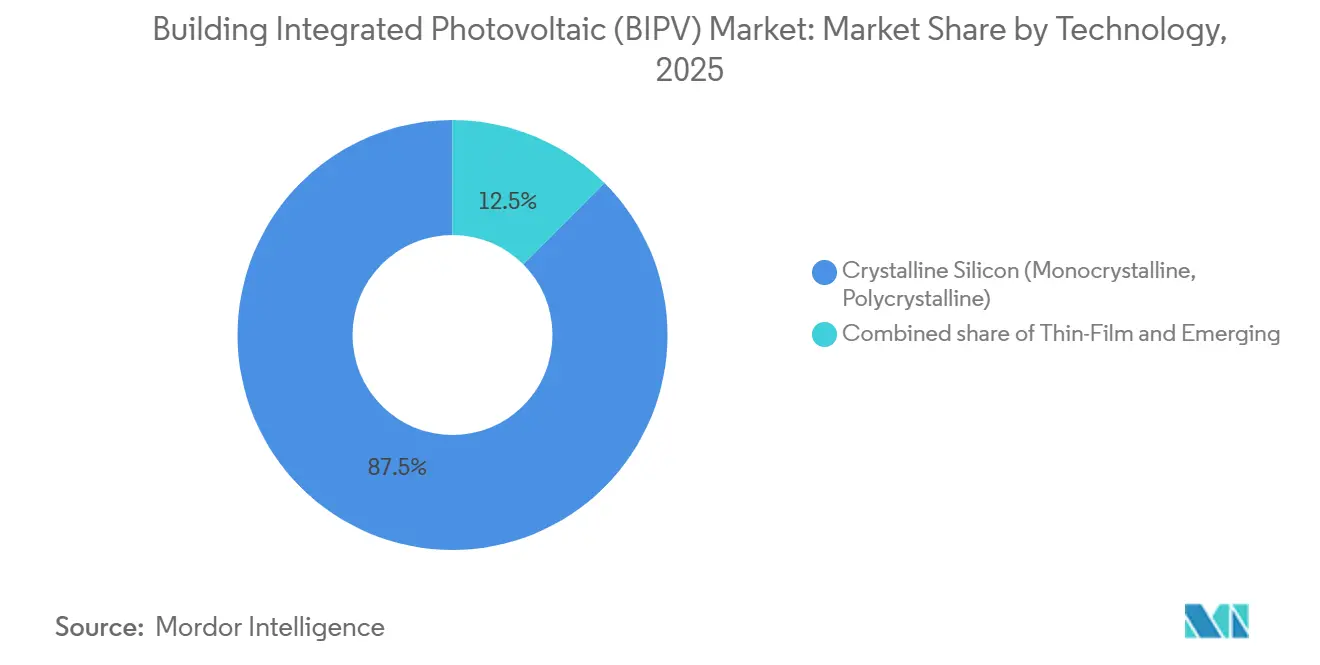

- By technology, crystalline silicon retained 87.5% of 2025 installations, while perovskite and tandem architectures are forecast to post a 27.5% CAGR to 2031, making them the fastest advancing segment.

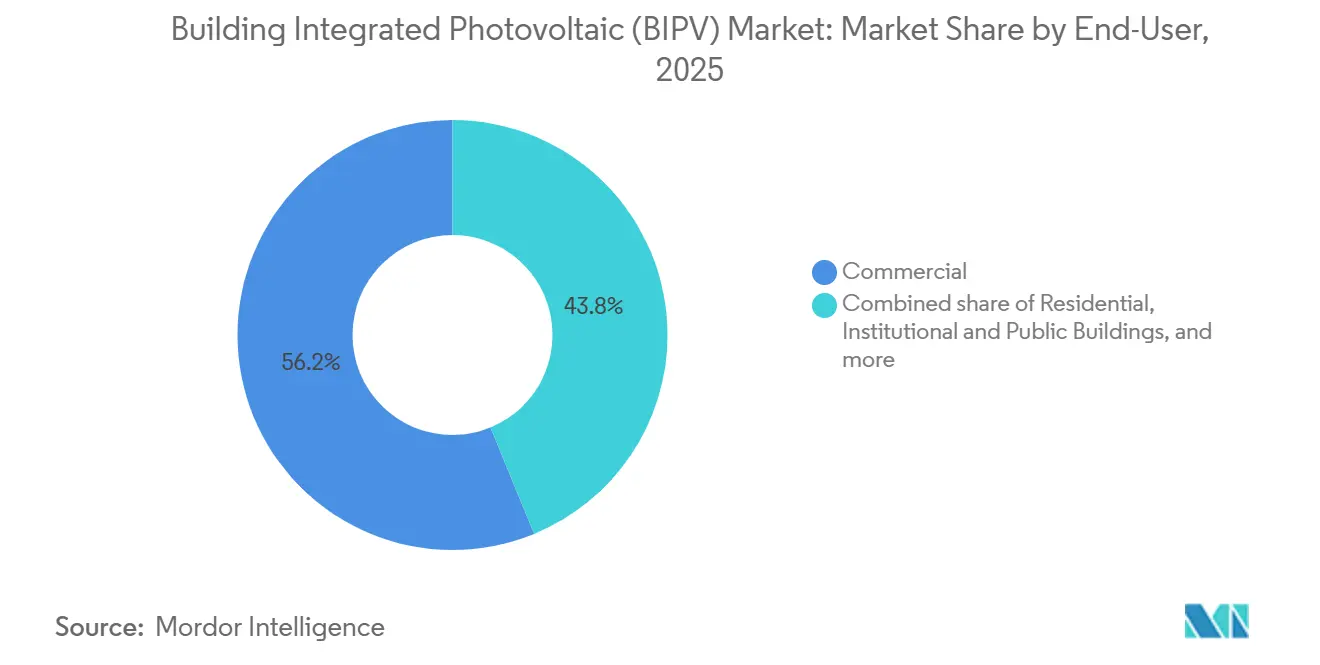

- By end-user, commercial buildings captured 56.2% revenue in 2025 and are poised to expand at a 24.6% CAGR through 2031, leading demand across all application groups.

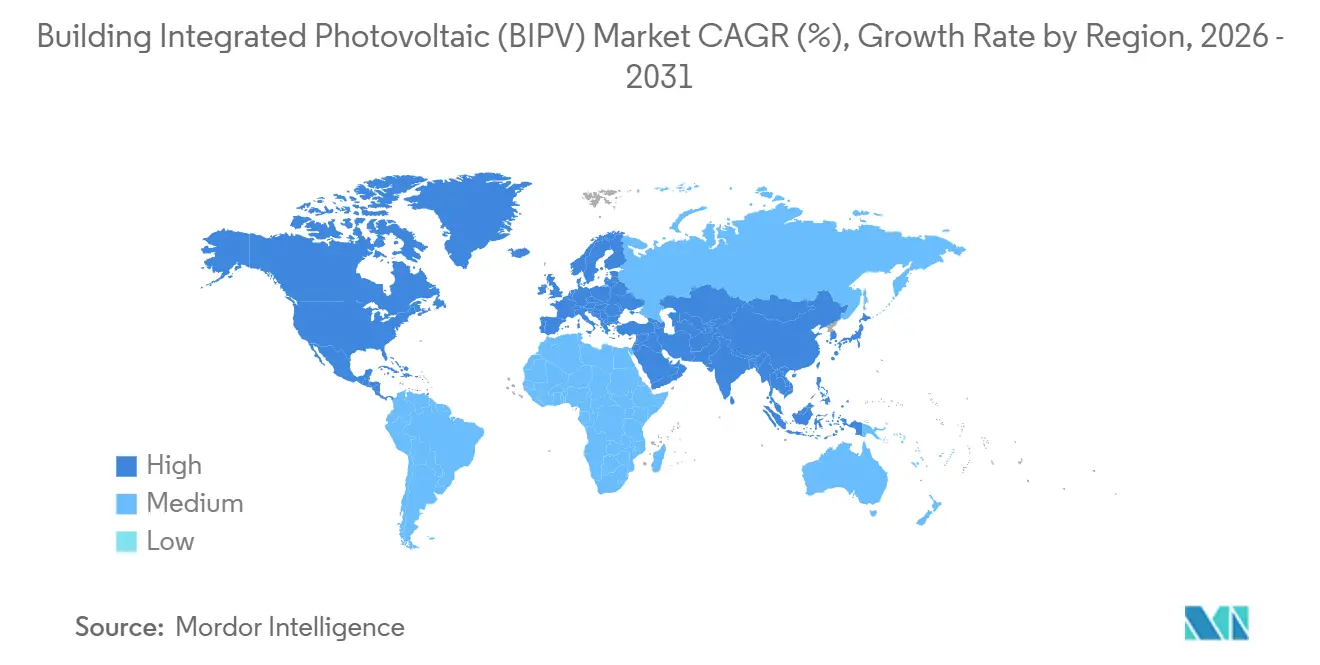

- By geography, Asia-Pacific captured 40.7% of the building-integrated photovoltaic (BIPV) market in 2025 and is set to grow at 23.8% annually up to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Building Integrated Photovoltaic (BIPV) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supportive policy incentives and zero-carbon building mandates | +6.2% | Europe, North America, China | Medium term (2-4 years) |

| Declining PV and balance-of-system costs | +5.8% | Global, early gains in Asia-Pacific and Middle East | Short term (≤ 2 years) |

| Rising demand for net-zero and smart-city developments | +4.5% | Urban centers across APAC, EU, North America | Medium term (2-4 years) |

| Growth of façade-integrated transparent PV glass | +3.1% | Europe, North America, premium commercial segments in APAC | Long term (≥ 4 years) |

| Corporate ESG and green-building certification pressures | +2.9% | Global, led by multinational headquarters in North America and Europe | Short term (≤ 2 years) |

| 5G-ready rooftop infrastructure synergy | +1.1% | Urban APAC, North America, select Middle-East smart cities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Supportive Policy Incentives & Zero-Carbon Building Mandates

Europe’s Energy Performance of Buildings Directive 2024/1275 requires solar-ready roofs on all new structures by 2030, and phased retrofits for public buildings above 250 square meters now begin in 2027.[1]European Commission, “Energy Performance of Buildings Directive 2024/1275,” ec.europa.eu Germany’s KfW 442 program earmarked EUR 500 million in 2025 to subsidize 10-30% of installed costs, while France extended MaPrimeRénov grants up to EUR 11,000 for integrated façades. China’s whole-county solar mandate, covering 676 counties by late 2025, obliges new industrial rooftops to host on-site generation or purchase renewable certificates, effectively guaranteeing a pipeline for the Building Integrated Photovoltaic (BIPV) market.[2]National Development and Reform Commission of China, “Whole-County Distributed Solar Initiative,” ndrc.gov.cn These rules shorten permitting cycles, train specialist installers, and shift BIPV from a discretionary upgrade to a code requirement. As more jurisdictions transpose similar directives, developers front-load solar envelopes into schematic designs to avoid costly redesigns later in the approval process.

Declining PV & Balance-of-System Costs

Monocrystalline PERC modules dropped to USD 0.12 per watt in mid-2025, and competitive pressure among inverter suppliers trimmed electronics pricing by 18% year-on-year. Standardized curtain-wall kits released by AGC and NSG/Pilkington cut on-site labor by 25% by integrating junction boxes and weather seals at the factory. Transparent PV glass still costs 20-40% more than low-E glazing, but high-rent developers recoup premiums by monetizing electricity and reducing mechanical-penthouse congestion. In the Gulf, the levelized cost of BIPV electricity fell below retail tariffs in 2025, enabling subsidy-free adoption where irradiance tops 2,200 kWh/m²/yr. As BOS manufacturers scale, the Building Integrated Photovoltaic (BIPV) market enjoys price elasticity that opens mid-tier commercial projects previously priced out of integrated solar façades.

Rising Demand for Net-Zero / Smart-City Developments

Multinational tenants now embed net-zero clauses in leasing contracts, pressuring landlords to integrate on-site renewables or lose premium occupants. Amazon targets 5 GW of self-generation by 2030, while Google pursues 24/7 carbon-free electricity across its campuses.[3]Amazon.com Inc., “Sustainability Report 2025,” sustainability.amazon.com Smart-city masterplans in NEOM, Masdar City, and Singapore’s Tengah district specify 100% renewable energy, with BIPV the de facto option when land for ground arrays is scarce. Rooftops hosting 5G micro-cells now generate rental income that lifts project IRRs 1.5-2.5 percentage points in dense cores. These converging forces create reliable demand signals that underpin long-term supply agreements between module makers and real-estate developers.

Growth of Façade-Integrated Transparent PV Glass

Semi-transparent perovskite cells reached 17.7% efficiency at 12% visible transmittance in 2025 laboratory tests. Onyx Solar delivered 300 façade projects across Europe by end-2025, showing that amorphous-silicon and CdTe laminates can meet thermal-insulation codes without external shading. Transparent BIPV blocks infrared radiation, cutting HVAC demand 15-20% in glass-heavy towers and offsetting its premium within 10-12 years. Heritage buildings embrace the solution to comply with renewable mandates without altering skylines, and tenant surveys report 8-10% higher comfort scores after installations. As tandem perovskite-silicon variants near 25-year warranty certification, the Building Integrated Photovoltaic (BIPV) market gains a technology that blends daylighting with megawatt-scale generation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High initial installation and design complexity | -3.7% | Global, acute in retrofit markets across North America and Europe | Short term (≤ 2 years) |

| Structural and fire-safety code barriers | -2.4% | North America, Europe, select APAC jurisdictions with stringent building codes | Medium term (2-4 years) |

| Limited skilled installers and façade-engineering know-how | -2.1% | Global, most severe in North America, emerging APAC markets, and South America | Medium term (2-4 years) |

| Supply-chain constraints for specialty BIPV glass | -1.8% | Global, with bottlenecks concentrated in Europe and North America for low-iron tempered glass | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Initial Installation & Design Complexity

BIPV requires tight coordination among structural, electrical, and façade teams, yet few general contractors offer that integrated workflow. New York and California demand separate approvals for structural load, interconnection, and fire egress, pushing soft costs 12-18% above rooftop arrays and stretching timelines by up to six months.[4]New York City Department of Buildings, “Solar Permitting Guide 2025,” nyc.gov Custom curtain-wall integration can add EUR 550-850/m² to budgets, nudging cost-conscious developers toward cheaper carports. Insurers levy 5-15% premiums until inspectors confirm UL 1703 and IEC 61730 compliance, reflecting caution over water ingress and rapid-shutdown reliability. A talent bottleneck compounds risks: fewer than 2,000 certified installers operate in North America, leading developers to import European crews at USD 800/day, which erodes project margins until local training accelerates.

Structural / Fire-Safety Code Barriers

Retrofitting curtain walls with crystalline panels adds 15-25 kg/m², obliging costly structural assessments and occasional tenant relocations. German and French fire authorities stipulate 1.2-m clearance from egress windows and rapid-shutdown inverters de-energizing within 10 seconds, cutting usable façade area 10-15% and raising BOS spend. Japan’s seismic code demands wind-tunnel testing for façade loads above 20 kg/m², prolonging approval by 8-12 weeks. These localized requirements fragment the global product mix, preventing module makers from enjoying economy-of-scale production runs. Until standards bodies harmonize protocols, the Building Integrated Photovoltaic (BIPV) market must budget region-specific engineering, delaying the ultimate cost convergence with conventional glass façades.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Crystalline Dominance Faces Emerging Disruption

Crystalline silicon commanded 87.5% of 2025 volume, equating to the largest Building Integrated Photovoltaic (BIPV) market share, yet perovskite-silicon tandems are set to erode that lead with a 27.5% CAGR to 2031. LONGi’s Hi-MO 9 hit 24.92% efficiency, reinforcing silicon’s high-wattage advantage, while First Solar’s Series 7 CdTe maintained output in high-temperature warehouses. Still, laboratory tandem cells at 29.1% efficiency have spurred pilot façades across Europe, indicating looming parity. Early field data from Heliatek’s organic films suggest 25-year durability is attainable, undermining the perception that flexible modules are short-life novelties. The Building Integrated Photovoltaic (BIPV) market now offers architects a spectrum from rigid, high-density panels to light organic rolls, allowing project teams to match substrate, weight, and aesthetics. Supply-chain nuances matter: low-iron glass shortages can stall crystalline projects, whereas polymer-substrate tandems bypass that constraint. Once IEC 61215 certification reaches perovskite modules in 2027, financing barriers will fall, and crystalline players may confront accelerated share loss.

Second-generation thin films occupy a middle ground. CdTe, CIGS, and amorphous silicon demonstrate lower temperature coefficients, which protects yield in desert climates, yet their energy density still trails top-tier mono-PERC. As module prices slide, thin films pivot to niche value, curved skylights, heritage façades, and ultra-light tensile roofs, rather than head-to-head wattage battles. OEMs are investing in hybrid lines that laminate perovskite coatings onto crystalline wafers, chasing efficiency gains without radical factory retools. The outcome will decide whether silicon defends incumbency or concedes premium architectural projects to newer chemistries within the Building Integrated Photovoltaic (BIPV) market.

By End-User: Commercial Leadership Driven by ESG Mandates

Commercial real-estate owners generated 56.2% of 2025 demand and will grow at 24.6% through 2031, a pace that keeps them the Building Integrated Photovoltaic (BIPV) market size front-runner among user groups. LEED v5 now deducts points for high-carbon façades unless offset by on-site renewables, effectively making integrated solar a ticket to Platinum ratings. Developers tap sustainability-linked loans that trim interest rates 25-75 basis points when carbon thresholds are met, turning BIPV from a cost center to a financing lever. Class-A offices also monetize prestige; tenants pay 3-5% rent premiums for verified net-zero space, a margin that funds façade upgrades without extending payback.

Residential uptake lags despite strong French and German incentives, mainly due to fragmented ownership structures, longer municipal permitting, and homeowner unfamiliarity with maintenance. Tesla’s Solar Roof V3.5 tackles aesthetics but still targets affluent households. Industrial facilities occupy a pragmatic middle tier, locking in electricity costs for cold-storage depots and desert-based warehouses where peak-day tariffs bite margins. Public buildings trail but will accelerate as the EU and several U.S. states enforce net-zero procurement rules from 2027. Singapore’s SolarNova airport project showcased how anchor public contracts de-risk supply chains, encouraging private follow-on deals and expanding the overall Building Integrated Photovoltaic (BIPV) market.

By Building Element: Rooftop Dominance with Façade Innovation

Rooftop systems continue to dominate because pitch and orientation deliver the highest energy-to-cost ratios, especially when integrated as weatherproof membranes. Façade solutions are the fastest riser, fuelled by transparent and coloured glass that meets aesthetic review boards while monetising otherwise passive surfaces. The AUE Basel project installed 167 kW across 1,141 m² of façades, meeting 45,000 kWh yearly demand without infringing heritage guidelines. Window and skylight products now secure low-U-value glazing while producing power, reducing HVAC loads, and lighting glare simultaneously. Dynamic shading devices like Solskin track the sun, cutting HVAC consumption up to 80% and adding generation capacity on balconies and louvres. Frankfurt Airport’s 17.4 MW vertical array shows that even non-optimal orientations are viable at scale when land is scarce.

Geography Analysis

Asia-Pacific controlled 40.7% of global volume in 2025 and is forecast to grow 23.8% annually through 2031, protecting its leadership in the Building Integrated Photovoltaic (BIPV) market. China’s 676-county solar mandate guarantees continuous demand, while Japan’s feed-in tariff revision rewards self-consumption, lifting rooftop economics. Shenzhen obliges commercial buildings above 5,000 m² to install BIPV skins, funneling orders to domestic giants LONGi, Trina, and Risen. India sets 300 GW solar by 2030 with a carved-out BIPV target for government facilities, but heterogeneous state codes and a shortage of façade engineers slow roll-out. ASEAN pilots, led by Singapore’s Tengah district, mandate solar-ready roofs on 42,000 homes, showing scalability once policy clarity arrives.

Europe ranks second, propelled by the Energy Performance of Buildings Directive. Germany, France, and Spain underwrite 30-50% of project costs, while Sweden’s carbon tax above EUR 100/tCO₂ steers lifecycle economics toward integrated solar. The United Kingdom’s Future Homes Standard pushes residential developers to adopt BIPV from 2025, though post-Brexit labor shortages inflated installer wages 12-15% after 2024. Nordic daylight fluctuations complicate annual yield but spur interest in high-efficiency tandem panels that offset seasonal lows. Altogether, supportive incentives anchor a predictable pipeline that multinationals use to trial cross-border procurement strategies within the Building Integrated Photovoltaic (BIPV) market.

North America’s expansion clusters in California, New York, and parts of Canada, where updated net-metering and 30% federal ITC compress payback to 8-10 years. California’s Title 24 extends solar mandates to commercial buildings over 10,000 ft², triggering façade retrofits on older stock. New York’s Climate Act compels municipal property managers to offset 70% of electricity with renewables by 2030, driving state contracts toward BIPV façades. The Middle East and Africa remain nascent yet promising, with NEOM and Masdar City embedding solar skins in master plans that target 100% renewable supply. High irradiance above 2,200 kWh/m²/yr offers sub-6-year payback even without subsidies, positioning the region as the next growth pole for the Building Integrated Photovoltaic (BIPV) market.

Competitive Landscape

Top-five suppliers captured around 35% of 2025 revenue, leaving a long tail of regional specialists, glazing innovators, and façade engineering firms. Tier-one crystalline producers, Hanwha Q-Cells, Canadian Solar, LONGi, and Trina, adapt bifacial and half-cut cells for vertical orientation, but still sell mainly through EPCs rather than architects who influence early design. Onyx Solar and Ertex Solartechnik thrive in heritage retrofits where aesthetic clearance outweighs pure wattage, commanding premiums insulated from commodity price swings. Heliatek’s organic films, weighing under 500 g/m², unlock tensile roofs that crystalline modules cannot mount safely, broadening the Building Integrated Photovoltaic (BIPV) market to stadiums and membrane structures.

Strategic moves in 2025 underline an innovation race. Hanwha’s Q.ANTUM NEO platform at 22.8% efficiency pairs with pre-certified façade kits that cut labor by 20%. LONGi scaled Hi-MO 9 after Fraunhofer certification at 24.92% efficiency, aligning with China’s distributed solar program. Tesla bundled Solar Roof V3.5 with 71.67 kWh Powerwall 3 storage, enabling three-day off-grid autonomy for upscale residences. Canadian Solar’s TOPBiHiku7 achieved 740-W output, targeting low-light northern markets. Patent filings reveal AGC and Pilkington prototyping switchable-tint BIPV glazing that could command 40-50% premiums in WELL-certified offices, hinting at functional convergence of daylight control and power generation.

Barriers to entry persist. IEC 61730 and UL 1703 certification runs 12-18 months and costs millions, deterring start-ups. Supply-chain bottlenecks for low-iron glass constrain capacity expansions, while perovskite encapsulation technology remains proprietary and closely guarded. Yet ample whitespace remains in rapid-shutdown electronics, lightweight substrates, and modular plug-and-play façades. Overall, the Building Integrated Photovoltaic (BIPV) market balances incumbent scale with niche differentiation, creating a competitive equilibrium that rewards both volume efficiency and architectural customization.

Building Integrated Photovoltaic (BIPV) Industry Leaders

Onyx Solar Energy SL

AGC Inc.

Nippon Sheet Glass (Pilkington)

Solaria Corporation

Ertex Solartechnik GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: The Eindhoven University of Technology (TU/e) has secured a funding boost of EUR 1.5 million for its UPSCALE project. This funding comes courtesy of the esteemed Clean Energy Transition Partnership (CETPartnership). The UPSCALE initiative is set to transform how perovskite-based photovoltaics (PV) are incorporated into our buildings.

- June 2025: Huasun and TÜV Rheinland launched the first lifecycle evaluation protocol for vertical BIPV modules, filling a standards gap for façade systems.

- February 2025: Microquanta launched the world's largest building-integrated photovoltaic (BIPV) project, harnessing perovskite panels, at the University Student Entrepreneurship Center in Shanxi. The installation, perched atop the translucent roof of the center in Shenchi County, Shanxi Province, boasts a capacity of 17.92 kWp. The double-glass perovskite modules, each measuring 1,200 mm x 1,000 mm, are engineered for a light transmittance of approximately 40%.

- February 2025: Avancis unveiled its newest module series for building-integrated photovoltaics (BIPV), signaling a shift from traditional thin-film technology. The newly launched Skala Matrix range harnesses crystalline solar technology, boasting superior output compared to the Skala Prime panels, which utilize CIGS technology. However, the Skala Prime panels continue to be offered in the lineup.

Global Building Integrated Photovoltaic (BIPV) Market Report Scope

Building-integrated photovoltaics (BIPVs) are solar power-producing products or systems that are effortlessly integrated into the building envelope and parts of building apparatuses such as façades, roofs, or windows. A BIPV system serves a dual purpose and is an integral component of the building skin that concurrently converts solar energy into electrical energy.

The building-integrated photovoltaic (BIPV) market is segmented by type, end-user, and geography. By type, the market is segmented into crystalline silicone, thin-film (CdTe, CIGS, a-Si), and emerging (Perovskite, Organic PV, Tandem). By end-user, the market is segmented into residential, commercial, industrial, and institutional and public buildings. The report also covers the market size and forecasts for the building-integrated photovoltaic (BIPV) market across major regions, such as Asia-Pacific, North America, Europe, South America, and Middle East and Africa. For each segment, the market sizing and forecasts have been done based on revenue (USD).

| Crystalline Silicon (Monocrystalline, Polycrystalline) |

| Thin-Film (CdTe, CIGS, a-Si) |

| Emerging (Perovskite, Organic PV, Tandem) |

| Residential |

| Commercial |

| Industrial |

| Institutional and Public Buildings |

| Roofs |

| Facades/Curtain Walls |

| Windows and Transparent Glazing |

| Skylights and Atriums |

| Shading Devices (Louvers, Balconies) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Spain | |

| Italy | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Nigeria | |

| Egypt | |

| Rest of Middle East and Africa |

| By Technology | Crystalline Silicon (Monocrystalline, Polycrystalline) | |

| Thin-Film (CdTe, CIGS, a-Si) | ||

| Emerging (Perovskite, Organic PV, Tandem) | ||

| By End-User | Residential | |

| Commercial | ||

| Industrial | ||

| Institutional and Public Buildings | ||

| By Building Element (Qualitative Analysis) | Roofs | |

| Facades/Curtain Walls | ||

| Windows and Transparent Glazing | ||

| Skylights and Atriums | ||

| Shading Devices (Louvers, Balconies) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Spain | ||

| Italy | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Nigeria | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the forecast value of the Building Integrated Photovoltaic (BIPV) market by 2031?

The market is projected to reach USD 47.02 billion by 2031, growing at a 23.06% CAGR over 2026-2031.

Which technology segment is expected to grow the fastest through 2031?

Perovskite and tandem architectures are forecast to post a 27.5% CAGR, outpacing other technologies.

Why are commercial buildings the largest adopters of BIPV?

They have large façade areas and access to sustainability-linked financing, enabling them to prioritize on-site generation and meet ESG targets.

How do policy mandates influence BIPV demand in Europe?

The Energy Performance of Buildings Directive requires solar-ready roofs on new structures by 2030, turning integrated photovoltaics into a compliance obligation.

What are the main barriers to residential deployment?

Fragmented ownership, longer permitting cycles, and higher upfront costs keep many homeowners from choosing building-integrated systems despite subsidies.

Page last updated on: