South America Data Center SSD Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2025 - 2031 |

| Historical Data Period | 2019 - 2023 |

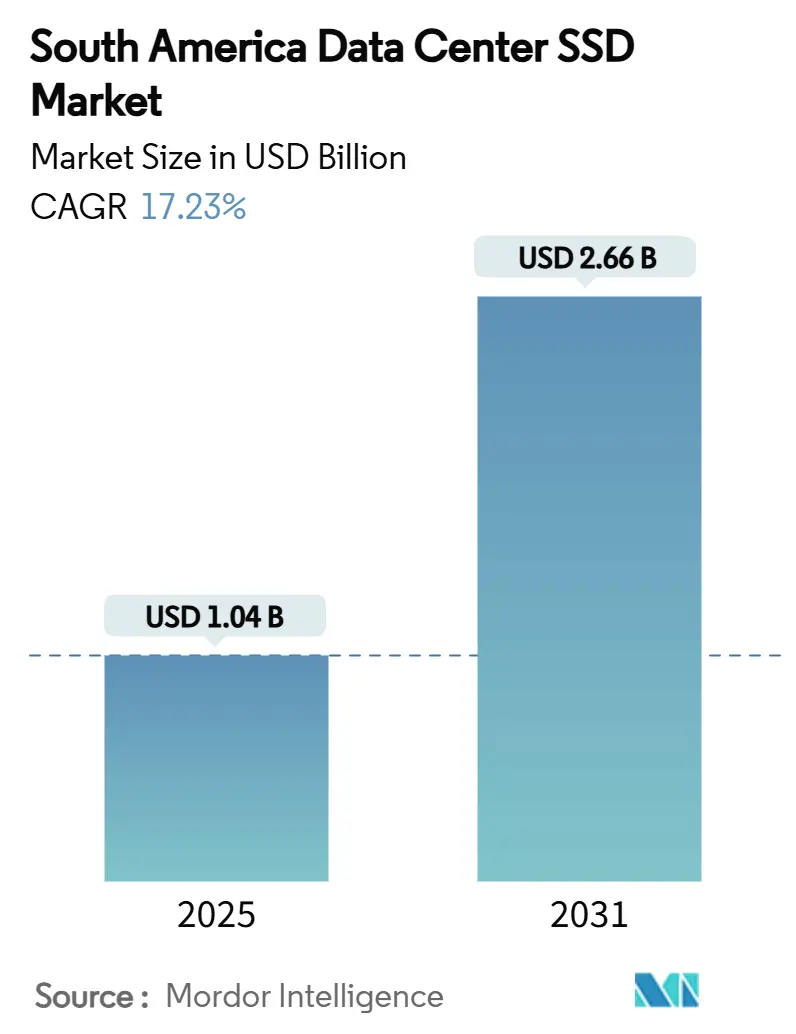

| Market Size (2025) | USD 1.04 Billion |

| Market Size (2031) | USD 2.66 Billion |

| Growth Rate (2025 - 2031) | 17.23% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Data Center SSD Market Analysis by Mordor Intelligence

The South America data center SSD market size is projected to reach USD 1.04 billion in 2025 and is expected to expand to USD 2.66 billion by 2031, posting a 17.23% CAGR. This trajectory reflects hyperscale cloud build-outs, AI workload proliferation, and government policies that position the region as a digital infrastructure hub. Brazil’s national data center blueprint, backed by planned USD 0.37 trillion investments, anchors demand for ultra-low-latency storage, while renewable energy incentives lower operating costs for all-flash facilities. Amazon Web Services, Huawei Cloud, and local champions such as Scala Data Centers lead new capacity announcements that prioritize NVMe and EDSFF drives for density and power efficiency. Interface migration from SATA/SAS to PCIe Gen4 and Gen5 continues unabated, and enterprise appetite for balanced mixed-use SSD architectures underpins steady procurement even amid NAND price compression. Rapid skills development programs for NVMe-oF integration, coupled with circular-economy lithium reclamation initiatives, further strengthen the South America data center SSD market growth outlook.

Key Report Takeaways

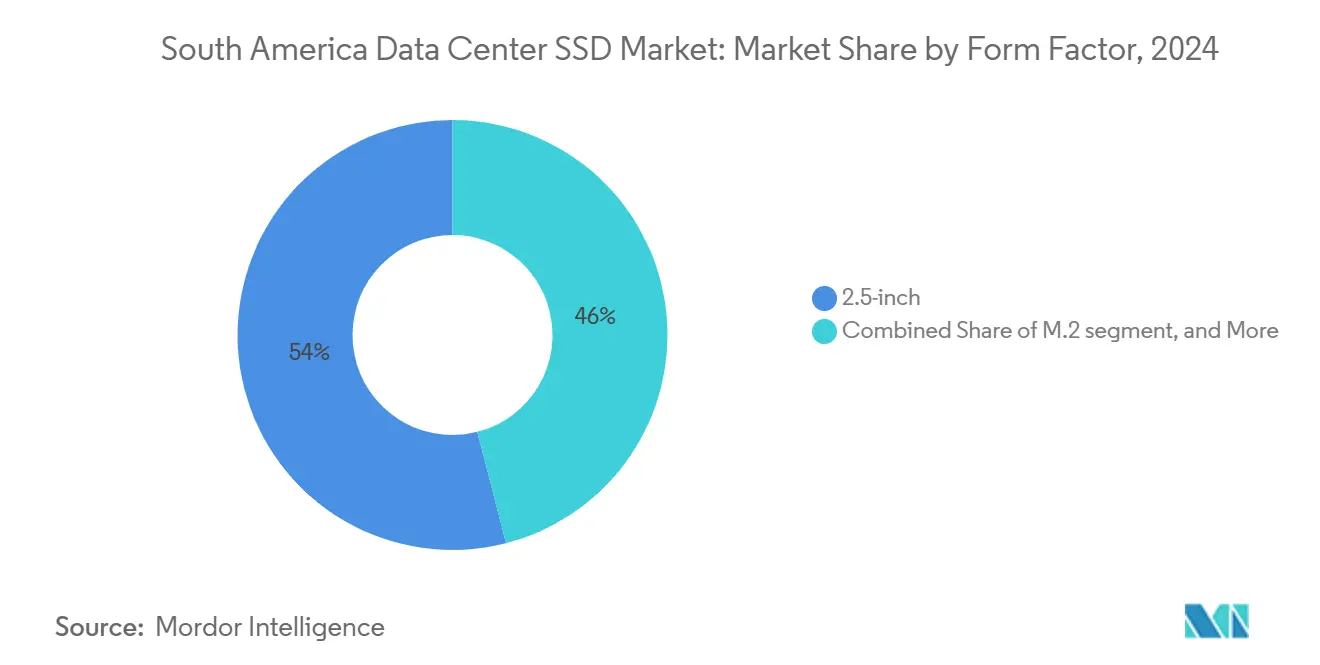

- By form factor, 2.5-inch drives held 54% of the South America data center SSD market share in 2024, while EDSFF is forecast to rise at a 21.40% CAGR to 2031.

- By interface, PCIe commanded 65% share of the South America data center SSD market size in 2024 and is advancing at a 20.60% CAGR.

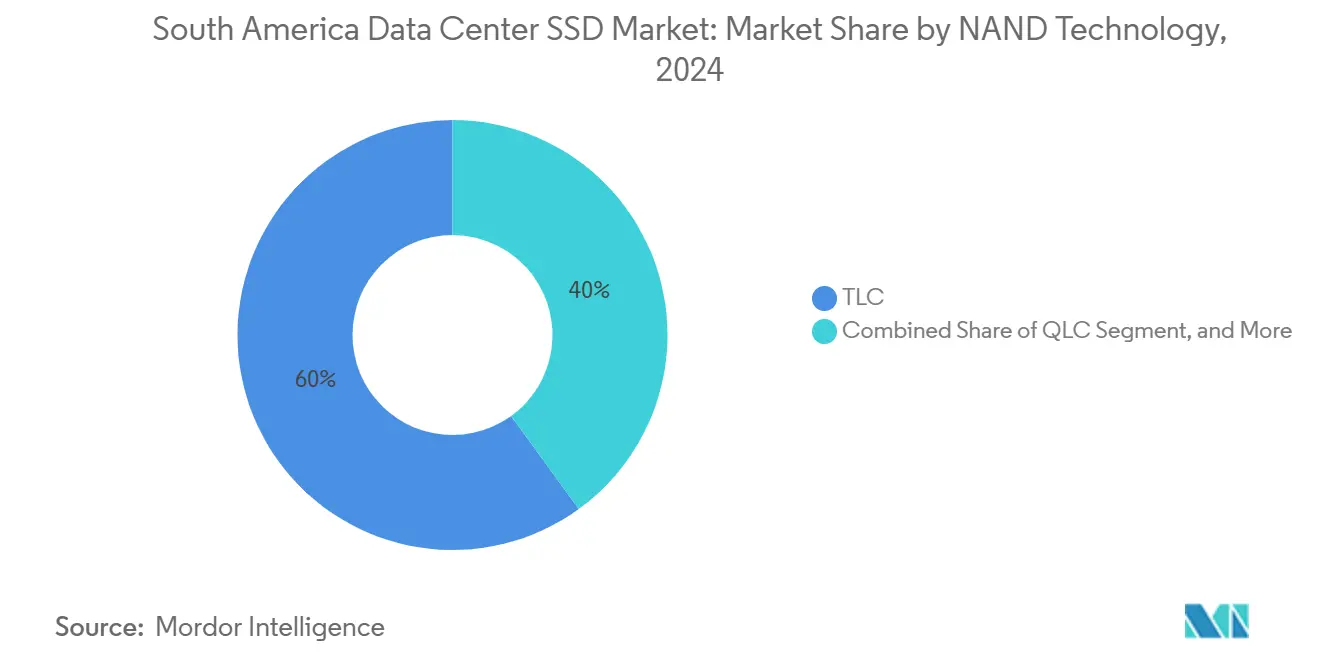

- By NAND technology, TLC led with 60% revenue share in 2024 in the South America data center SSD market ; QLC is projected to expand at a 19.10% CAGR through 2031.

- By drive architecture, mixed-use captured 45.50% share of the South America data center SSD market size in 2024, while write-intensive drives record the highest CAGR at 19.80%.

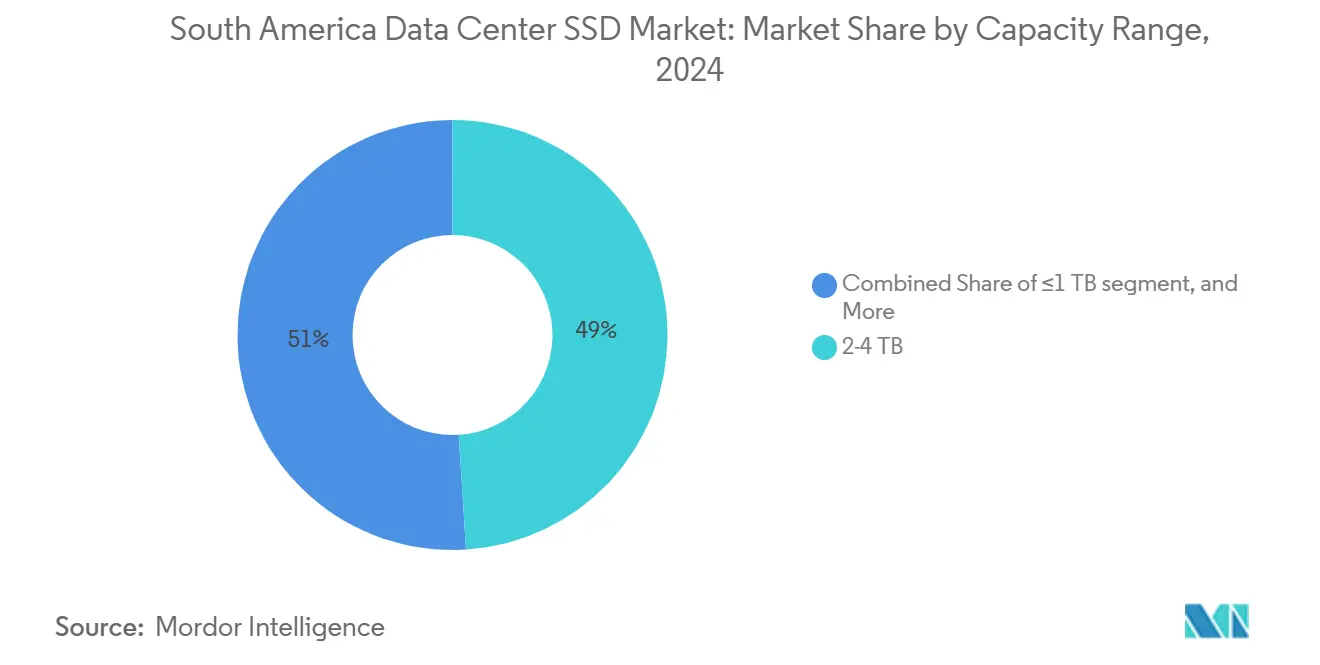

- By capacity, 2-4 TB drives accounted for 49.00% of the South America data center SSD market size in 2024; ≥4 TB drives are set to grow at 21.90% CAGR.

- By end-user, hyperscale cloud providers led with 51.10% share in 2024 in the South America data center SSD market , whereas colocation facilities are forecast to grow at 21.50% CAGR.

- By country, Brazil contributed 60.20% of the South America data center SSD market share in 2024, and Chile is the fastest-growing country at 17.70% CAGR.

Future direction is shaped by developments occurring across multiple regions, with Latin america contributing to the overall trajectory. The outlook on worldwide data center ssd market reflects how these are expected to evolve collectively.

South America Data Center SSD Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid growth of hyperscale and local CSP build-outs | +4.2% | Brazil, Chile, Argentina | Medium term (2-4 years) |

| AI and HPC workloads requiring ultra-low latency SSDs | +3.8% | Brazil, Colombia, Chile | Long term (≥ 4 years) |

| Accelerating NVMe adoption displacing SATA/SAS | +3.1% | Global | Short term (≤ 2 years) |

| Carbon-neutral mandates pushing all-flash retrofits | +2.4% | Brazil, Chile | Medium term (2-4 years) |

| Mercosur tariff relief on NAND components lowering TCO | +1.9% | Brazil, Argentina, Paraguay | Short term (≤ 2 years) |

| Circular-economy lithium reclamation lowering SSD pricing | +1.3% | Chile, Argentina | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid growth of hyperscale and local CSP build-outs

Massive investments from AWS, Huawei Cloud, and Scala Data Centers accelerate expansion plans that depend on predictable low-latency SSD performance. AWS earmarked USD 1.8 billion for new Brazilian capacity, while Amazon announced USD 4 billion for a Chile cloud region, directly stimulating bulk SSD orders [1]Amazon Web Services, “AWS to Launch New Cloud Region in Chile,” aws.amazon.com. Local operator Scala committed USD 50 billion to its AI City campus in São Paulo, which will require high-density EDSFF deployments for 4.7 GW of IT load. Domestic capital participation, exemplified by Patria’s USD 1 billion data center platform, further broadens demand. Hyperscalers favor SSDs that deliver consistent 4KB latency rather than peak throughput, supporting rapid NVMe-oF rollouts and driving the South America data center SSD market.

AI and HPC workloads requiring ultra-low latency SSDs

Regional adoption of large language models and machine learning drives sustained demand for sub-millisecond storage. Huawei Cloud’s Pangu 5.5 framework supports supernodes equipped with more than 160,000 accelerator cards, each node paired with NVMe SSDs for real-time model training [2].Scala Data Centers, “AI City Campus Announcement,” scaladatacenters.com Service providers like Telconet upgraded to OceanStor Dorado all-flash arrays to ensure dependable inference performance, while DapuStor introduced 32 TB QLC drives that cut rack-level storage cost by 60%. The resulting preference for high-endurance write-intensive media underpins the 19.80% CAGR of that segment within the South America data center SSD market

Accelerating NVMe adoption displacing SATA/SAS

Enterprise buyers are abandoning legacy interfaces because PCIe NVMe SSDs deliver an order-of-magnitude bandwidth improvement. KIOXIA projects NVMe to account for 91% of enterprise SSD shipments by 2025 and supports this migration with CM9 Series PCIe 5.0 drives that reach 14 GB/s sequential read speeds [3]Huawei Cloud, “Pangu Model 5.5 Launch,” huawei.com. NVMe-oF solutions enable resource pooling over Ethernet fabrics, reducing stranded capacity and boosting utilization. Marvell and Foxconn-Ingrasys jointly validated Ethernet Bunch of Flash configurations that simplify scale-out architectures. These developments reinforce the PCIe share gains within the South America data center SSD market.

Carbon-neutral mandates pushing all-flash retrofits

Brazil obtains 85% of its electricity from renewable sources, and tax incentives link data center benefits to carbon reduction commitments. Scala Data Centers publicly targets 100% renewable usage, making all-flash arrays attractive because they consume 40-50% less power than mixed HDD fleets. Samsung’s latest QLC V-NAND boosts density while lowering watt-per-terabyte metrics, supporting both sustainability and cost objectives. Circular-economy lithium reclamation initiatives underway in Chile enhance raw-material availability and reduce SSD component costs, providing additional momentum for flash adoption.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aggressive price erosion squeezing vendor margins | -2.80% | Global | Short term (≤ 2 years) |

| Shortage of skilled NVMe-oF integrators in region | -1.90% | Brazil, Argentina, Colombia | Medium term (2-4 years) |

| Municipal e-waste rules constraining NAND disposal | -1.40% | Brazil, Chile, Argentina | Medium term (2-4 years) |

| Grid instability raising SSD data-center OPEX | -1.20% | Peru, Colombia, Argentina | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Aggressive price erosion squeezing vendor margins

Global oversupply compressed NAND pricing during 2024, curbing profitability for drive makers. Western Digital’s Q3 2025 earnings showed modest cloud revenue declines despite rising shipment volumes, underscoring margin pressure. Suppliers trimmed output to stabilize pricing; nevertheless, enterprise SSD average selling prices remain subdued, challenging investment in localized South American support infrastructure. Smaller regional resellers struggle to sustain services as large vendors prioritize higher-volume geographies, tempering immediate upside for the South America data center SSD market.

Shortage of skilled NVMe-oF integrators in region

Disaggregated storage architectures require competencies in RoCE, Priority Flow Control, and congestion management that are scarce outside primary metros. Cisco’s RoCE over VXLAN deployment guides illustrate the complexity of tuning lossless Ethernet fabrics [4].KIOXIA America, “CM9 Series PCIe 5.0 NVMe SSDs,” kioxia.com Secondary markets such as Bogotá and Lima depend on a limited pool of certified engineers, forcing enterprises to hire costly consultants from São Paulo or abroad. Longer project timelines and higher professional-services bills delay NVMe-oF rollouts, hindering near-term growth of the South America data center SSD industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form Factor: EDSFF Drives Next-Generation Density

The 2.5-inch category retained 54% share of the South America data center SSD market in 2024, rooted in the extensive installed base of existing servers. EDSFF, however, is scaling fastest at a 21.40% CAGR, encouraged by hyperscalers that value its superior airflow management and hot-swap ergonomics. The South America data center SSD market size linked to EDSFF shipments is projected to pass USD 920 million by 2031.

EDSFF’s appeal includes higher power budgets and standardized thermals. KIOXIA’s XD7P E1.S delivers up to 7.68 TB in a slim envelope designed for dense 1U platforms, while ATP Electronics’ N651Si Series operates reliably from -40 °C to 85 °C, suiting edge deployments. Meta’s and Microsoft’s public advocacy of open E1.S designs accelerates ecosystem maturity, signaling a structural pivot away from legacy 2.5-inch trays across the South America data center SSD market.

By Interface: PCIe Dominance Accelerates Legacy Displacement

PCIe already accounts for 65% of the South America data center SSD market and will maintain more than 80% penetration by 2031 as SATA inventories decline. The South America data center SSD market size for PCIe units is forecast to post a USD 2 billion value by the end of the period.

Micron promotes EDSFF E3.S modules paired with PCIe 5.0 links that solve signal-integrity challenges. Seagate’s Nytro 4350 NVMe series illustrates real-world bandwidth, achieving 10× SATA throughput thanks to four-lane PCIe 4.0 connectivity. NVMe-oF technologies extend PCIe benefits across Ethernet or InfiniBand fabrics, enabling pooled flash architectures that further entrench PCIe’s leadership in the South America data center SSD market.

By NAND Technology: QLC Emerges as Cost-Efficiency Leader

TLC remains the workhorse with 60% share, but QLC is on a 19.10% CAGR path as users prioritize cost per terabyte. Samsung’s advanced QLC V-NAND improves endurance while lowering energy draw. DapuStor’s 32 TB Gen4 QLC models claim a 60% total cost-of-ownership advantage over HDD arrays. SK hynix commenced volume output of 321-layer devices that lift capacity ceilings and write-cycle durability. These innovations reassure buyers about reliability and cement QLC’s ascent in capacity-centric AI data pipelines within the South America data center SSD market.

By Drive Architecture: Mixed-Use Balances Performance Requirements

Mixed-use media captured 45.50% share in 2024 because enterprises need steady read and write behavior for diverse workloads. The South America data center SSD market share for mixed-use is supported by widespread virtualization and database adoption.

Write-intensive drives show the top CAGR at 19.80% as AI training bursts grow. SK hynix’s PS1012 U.2 targets high-write environments, while Solidigm’s D7-PS1030 offers up to 15.36 TB at mid-endurance ratings. Sophisticated wear-leveling and over-provisioning keep latency predictable, lowering risk for adopters across the South America data center SSD market.

By Capacity Range: High-Capacity Drives Lead Growth

Drives in the 2-4 TB bracket hold 49.00% share today, a sweet spot for most virtualized workloads. Yet units ≥4 TB will log 21.90% CAGR as AI training sets and vector databases swell. This cohort will account for the next USD 900 million of South America data center SSD market size gains.

KIOXIA’s LC9 122.88 TB dual-port NVMe SSD and Micron’s 6550 ION 60 TB E3.S module illustrate the density leap. By fitting 2.5 PB into a 2U chassis, operators cut rack count and power draw, aligning with green mandates across Brazil and Chile. Such density economics reinforce the high-capacity pivot in the South America data center SSD market.

By End-User: Hyperscale Drives Market Transformation

Hyperscale cloud providers controlled 51.10% of spending in 2024 owing to standardized rollouts and massive procurement volumes. The South America data center SSD market size attached to hyperscalers should exceed USD 1.4 billion by 2031.

Colocation facilities will expand fastest at 21.50% CAGR because enterprises embrace hybrid IT. Digital Realty designs low-latency zones for algorithmic trading requiring NVMe arrays, and Equinix relies on high-performance SSD clusters to process 90 million traffic records daily. Enterprise data centers still demand compliance-oriented storage such as Hitachi VSP 5600 with 10 PB of NVMe flash, yet the capital intensity of private builds pushes many workloads toward colocation, broadening South America data center SSD market participation.

Geography Analysis

Brazil accounts for 60.20% of the South America data center SSD market share, fueled by its 85% renewable power mix and a pro-investment regulatory stance. Government incentives waive import duties on qualified IT equipment and link tax breaks to green-energy procurement, accelerating all-flash adoption across São Paulo, Rio, and the emerging Northeast hub. AWS, Huawei, and Scala collectively announced multibillion‐dollar campuses, each specifying PCIe Gen4 or Gen5 NVMe storage, thereby anchoring volume demand.

Chile is the fastest-growing geography at a 17.70% CAGR through 2031. Amazon’s USD 4 billion cloud region and Equinix’s USD 130 million Santiago facility strengthen the national ambition to become a Pacific connectivity node. Submarine cable concentration lowers latency to US West Coast peering points, making local edge caches vital. The South America data center SSD market size accruing to Chilean deployments is projected to triple by 2031, with EDSFF adoption mirroring hyperscale blueprints.

Argentina, Colombia, Peru, and the rest of South America present mixed yet improving fundamentals. Colombia benefits from KIO Networks’ 6 MW Bogotá campus and tax incentives under ProColombia. Argentina’s Mercosur tariff relief opens cost advantages for NAND imports although macroeconomic volatility weighs on new builds. Peru’s grid reliability issues drive uptake of energy-efficient SSDs combined with redundant UPS investment. Collectively, these secondary clusters will contribute an incremental USD 400 million to the South America data center SSD market by 2031.

Analysis of the data center ssd market by Mordor Intelligence spans multiple other regional evaluations across North America, Asia, and Europe, supported by country-level insights for United States and China, wherein local market conditions keep varying from one country to another.

Competitive Landscape

Global tier-one suppliers dominate shipments, yet regional challengers narrow gaps through localized support and aggressive pricing. Samsung, KIOXIA, and Western Digital leverage vertical integration to secure large hyperscale orders. Huawei and YMTC pursue share via FusionSSD and Xtacking-based products that bundle competitive endurance with value pricing, appealing to cost-sensitive customers.

Strategic differentiation centers on ecosystem partnerships. Samsung’s USD 1.69 billion purchase of FläktGroup adds precision cooling to its portfolio, allowing bundled infrastructure solutions that lower total cost of ownership for all-flash halls. KIOXIA collaborates with Marvell and Foxconn-Ingrasys on Ethernet Bunch of Flash platforms that reduce fabric complexity, an attractive proposition in skills-constrained markets. Solidigm, backed by SK hynix, explores a US IPO to fund capacity expansion and firmware R and D targeting AI write patterns.

Skill shortages create white-space opportunities. Vendors offering on-site NVMe-oF training or managed storage-as-a-service gain traction among enterprises lacking deep engineering benches. Local system integrators partnering with component makers to package turnkey flash pods can unlock underserved mid-market demand, potentially reshaping competitive dynamics within the South America data center SSD market.

South America Data Center SSD Industry Leaders

Samsung Electronics Co., Ltd.

Kioxia Corporation

Huawei Technologies Co., Ltd. (FusionSSD)

Micron Technology, Inc.

Western Digital Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Samsung Electronics acquired FläktGroup for EUR 1.5 billion (USD 1.69 billion) to enhance data center cooling offerings.

- May 2025: KIOXIA America introduced CM9 Series PCIe 5.0 NVMe SSDs up to 61.44 TB capacity.

- May 2025: Patria invested USD 1 billion in a new regional data center platform.

- April 2025: Seagate announced Exos M HAMR drives reaching 36 TB while cutting energy per terabyte by 60%.

- March 2025: KIOXIA America unveiled LC9 Series 122.88 TB dual-port NVMe SSDs for AI clusters

- December 2024: SK hynix developed PS1012 U.2 SSDs optimized for AI data centers.

South America Data Center SSD Market Report Scope

| 2.5-inch (U.2/U.3) |

| M.2 |

| PCIe Add-in Card |

| EDSFF (E1.S / E1.L / E3) |

| SATA | |

| SAS | |

| PCIe | PCIe/NVMe Gen3 |

| PCIe/NVMe Gen4 | |

| PCIe/NVMe Gen5 | |

| PCIe/NVMe Gen6 |

| SLC |

| MLC |

| TLC |

| QLC |

| Read-Intensive (1 DWPD) |

| Mixed-Use (3 DWPD) |

| Write-Intensive (10 DWPD) |

| less than 1 TB |

| 1-2 TB |

| 2-4 TB |

| above 4 TB |

| Hyperscale Cloud Providers |

| Colocation / Carrier-Neutral Facilities |

| Enterprise and Financial Services Data Centers |

| Brazil |

| Argentina |

| Chile |

| Colombia |

| Peru |

| Rest of South America |

| By Form Factor | 2.5-inch (U.2/U.3) | |

| M.2 | ||

| PCIe Add-in Card | ||

| EDSFF (E1.S / E1.L / E3) | ||

| By Interface | SATA | |

| SAS | ||

| PCIe | PCIe/NVMe Gen3 | |

| PCIe/NVMe Gen4 | ||

| PCIe/NVMe Gen5 | ||

| PCIe/NVMe Gen6 | ||

| By NAND Technology | SLC | |

| MLC | ||

| TLC | ||

| QLC | ||

| By Drive Architecture | Read-Intensive (1 DWPD) | |

| Mixed-Use (3 DWPD) | ||

| Write-Intensive (10 DWPD) | ||

| By Capacity Range | less than 1 TB | |

| 1-2 TB | ||

| 2-4 TB | ||

| above 4 TB | ||

| By End-User | Hyperscale Cloud Providers | |

| Colocation / Carrier-Neutral Facilities | ||

| Enterprise and Financial Services Data Centers | ||

| By Geography | Brazil | |

| Argentina | ||

| Chile | ||

| Colombia | ||

| Peru | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the South America data center SSD market?

The market stands at USD 1,044.76 million in 2025 and is projected to reach USD 2,660.47 million by 2031, reflecting a 17.23% CAGR.

Which SSD form factor is most widely deployed in the region?

The 2.5-inch form factor leads with 54% share in 2024, although EDSFF is accelerating fastest at a 21.40% CAGR.

Why has PCIe become the dominant interface in South American data centers?

PCIe, coupled with NVMe, delivers far greater bandwidth than legacy SATA/SAS and now captures 65% share as operators adopt NVMe-oF fabrics for scale-out architectures.

Which country accounts for the largest share of regional SSD demand?

Brazil contributes 60.20% of spending, driven by hyperscale investments and its 85% renewable-energy power mix that favors all-flash facilities.

How are AI workloads influencing SSD purchasing decisions?

Large language models and real-time analytics need sub-millisecond latency and high write endurance, propelling a 19.80% CAGR for write-intensive SSDs.

What key restraint could slow market expansion?

Continued NAND price erosion squeezes vendor margins, trimming as much as 2.8% from the market’s forecast CAGR and delaying some regional rollouts.

Page last updated on: