Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

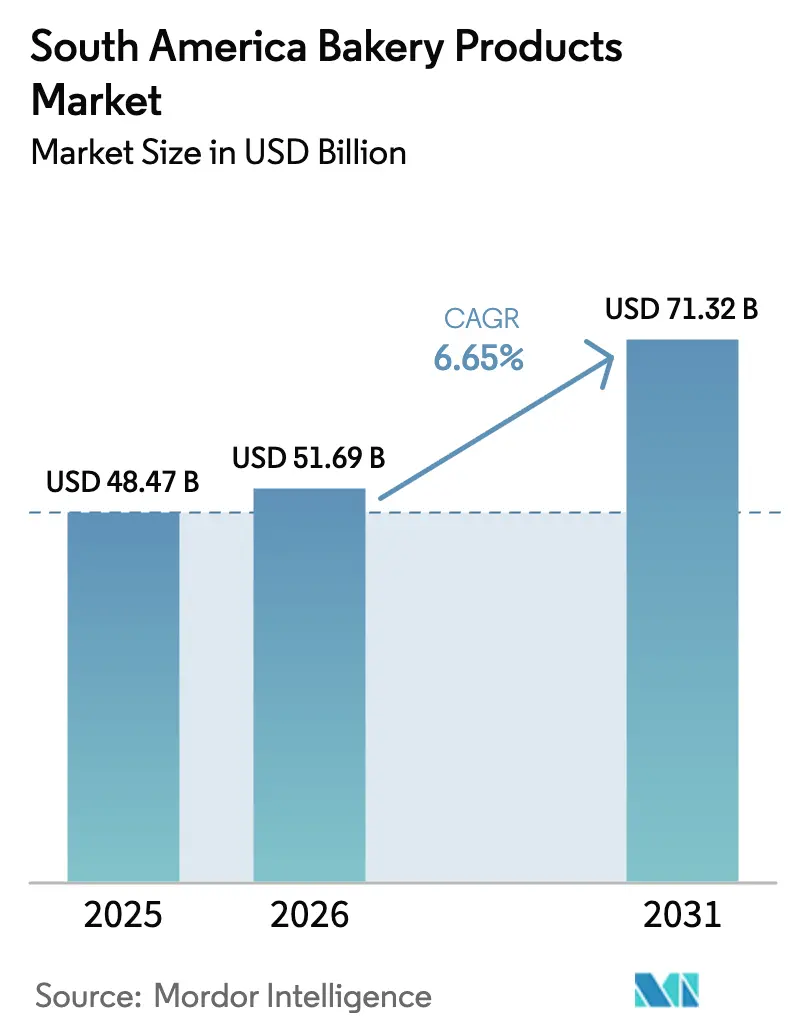

| Base Year Market Size (2025) | USD 48.47 Billion |

| Market Size (2026) | USD 51.69 Billion |

| Market Size (2031) | USD 71.32 Billion |

| Growth Rate (2026 - 2031) | 6.65% CAGR |

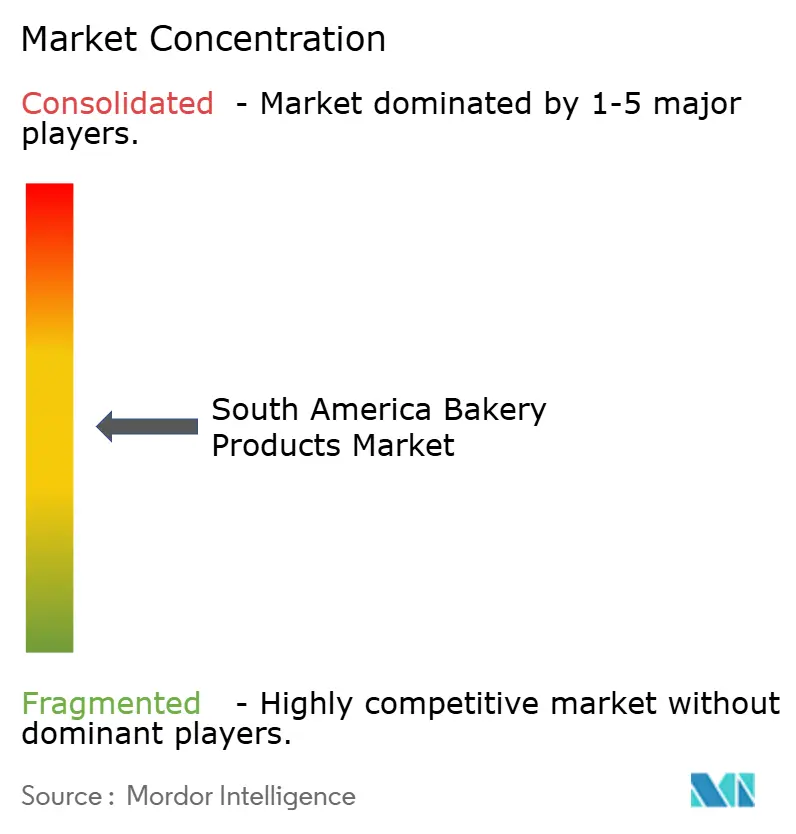

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Bakery Products Market Analysis by Mordor Intelligence

The South America bakery products market size was valued at USD 48.47 billion in 2025 and estimated to grow from USD 51.69 billion in 2026 to reach USD 71.32 billion by 2031, at a CAGR of 6.65% during the forecast period (2026-2031). The South American bakery products market is growing steadily, driven by established regional companies. In Brazil, Grupo Bimbo maintains market presence through its Pullman and Plusvita brands, addressing local consumer preferences. Wickbold, another Brazilian company, contributes to market growth with its bread and snack offerings. Argentina's Bagley Argentina SA has established itself in the biscuits and cookies segment. In Colombia, Productos Ramo SA has gained recognition with products like Chocoramo chocolate-covered cake and Gala pastries. These companies influence market dynamics by responding to consumer demand for health-conscious and convenient bakery options. Advancements in packaging and production technology have improved product shelf life and quality. The companies have expanded their reach through partnerships with local retailers and e-commerce platforms. Their success stems from understanding and adapting to regional preferences, which supports the market's development. The market is also driven by increasing urbanization and changing consumer lifestyles, which drive demand for packaged bakery products. Furthermore, the integration of traditional recipes with modern production methods has enabled companies to maintain authenticity while achieving scale in their operations.

Key Report Takeaways

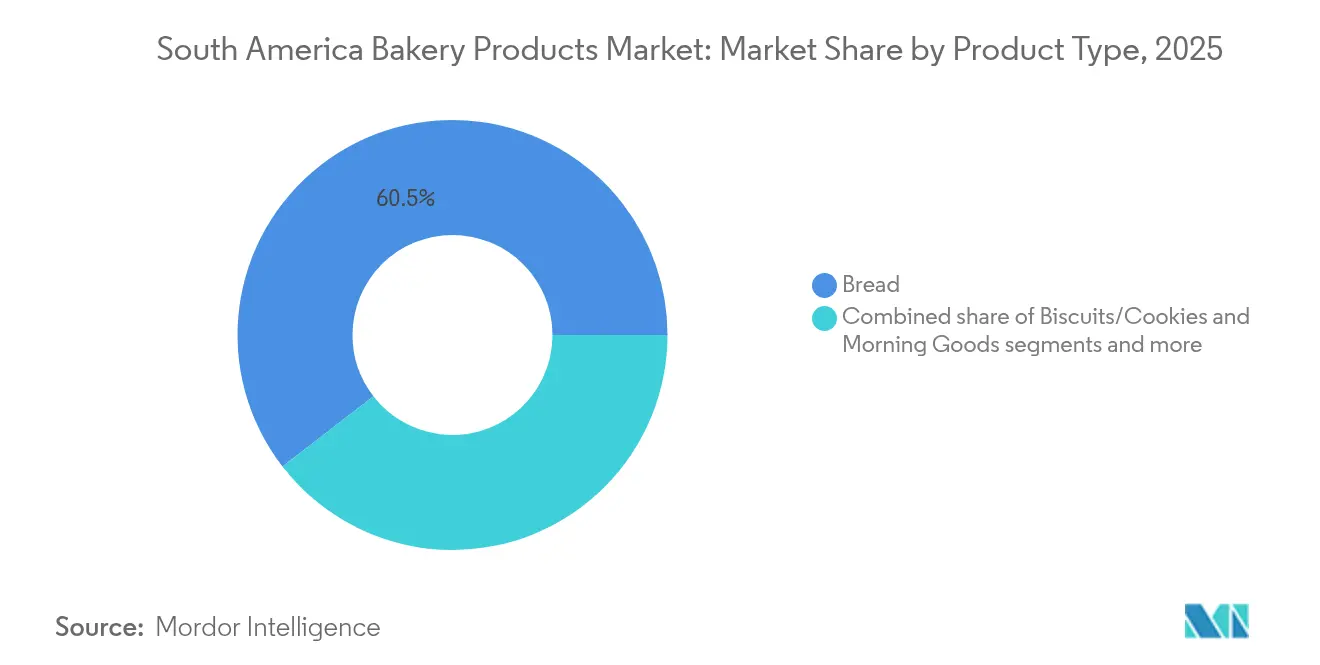

- By product type, bread held 60.48% of the South America bakery products market share in 2025.

- Morning goods are projected to post a 9.12% CAGR through 2031, the fastest among product segments.

- By form, fresh products accounted for 81.85% of the South America bakery products market size in 2025; frozen products are set to expand at a 7.6% CAGR to 2031.

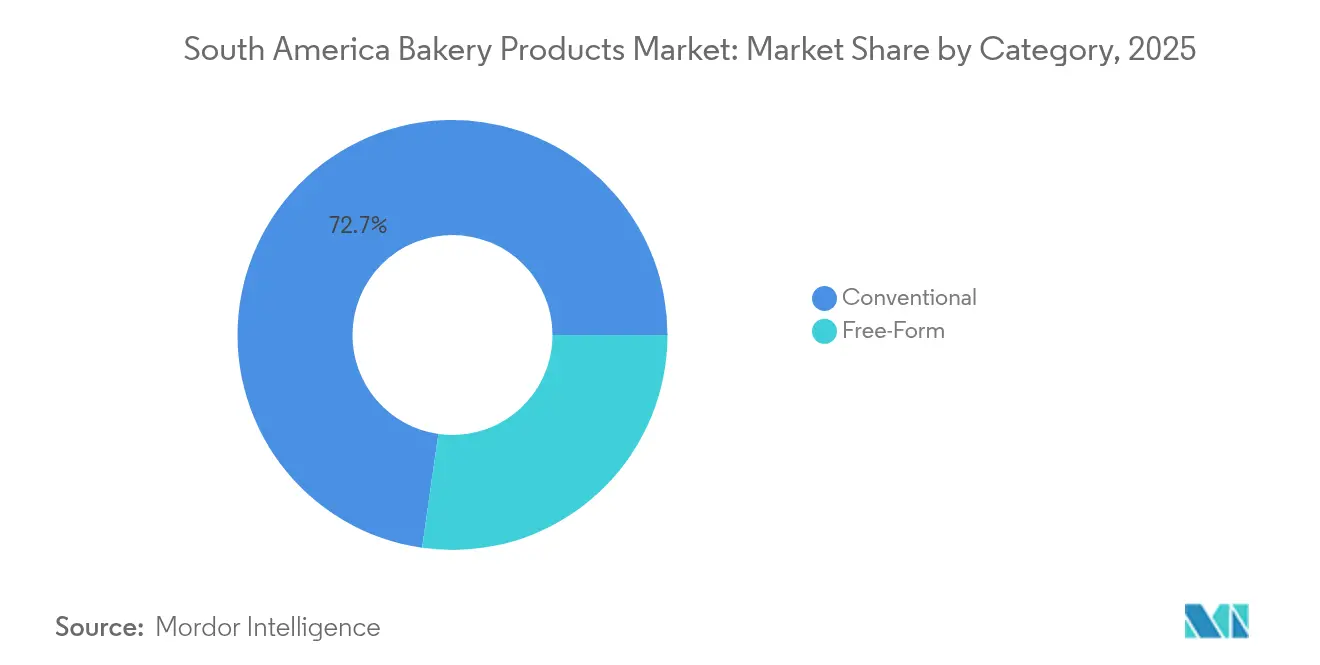

- By category, conventional offerings commanded 72.74% share of the South America bakery products market size in 2025, while free-form products are advancing at 8.21% CAGR.

- By distribution channel, off-trade led with 57.21% revenue share in 2025; on-trade is forecast to grow at 9.35% CAGR through 2031.

- By Geography, Brazil contributed 46.05% of regional revenue in 2025; Colombia is expected to record the highest national CAGR at 8.72% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South America Bakery Products Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Urbanization and rising disposable income | +1.8% | Brazil, Colombia, Argentina | Medium term (2-4 years) |

| Demand for artisanal and premium products | +1.2% | Urban centers region-wide | Long term (≥ 4 years) |

| Health and wellness: clean label, free-from | +1.0% | Brazil, Chile, Argentina | Medium term (2-4 years) |

| Expansion of cafés and quick-service outlets | +0.8% | Regional premium segments | Short term (≤ 2 years) |

| Strategic marketing campaigns | +0.6% | Major metropolitan areas | Short term (≤ 2 years) |

| Innovations in packaging and flavors | +0.7% | Export-oriented, urban retail | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Urbanization and Rising Disposable Income

Urbanization and rising disposable incomes are driving the growth of South America's bakery products market. In 2024, the region had approximately 186.6 million urban dwellers, with an overall urbanization rate of 87%, and Argentina reached 93%. This urban concentration has increased the demand for convenient, ready-to-eat bakery products [1]Source: World Bank, “Urban Population (% of Total) – Latin America & Caribbean,” data.worldbank.org. In Brazil, Grupo Bimbo offers products such as Pullman sliced bread and Plusvita cakes to serve consumers seeking quick meals and snacks. In Colombia, Productos Ramo provides Chocoramo and Gala pastries, while in Argentina, Bagley's Chocolinas and Criollitas cookies and crackers meet consumer snacking needs. The increase in disposable income has strengthened the demand for premium and artisanal baked goods in major metropolitan areas like São Paulo, Buenos Aires, and Bogotá. Local establishments, such as Padaria Bella Paulista in São Paulo, offer specialized breads and pastries. Consumer preferences are shifting toward bakery products that combine health benefits with convenience, as demonstrated by Wickbold's whole-grain breads in Brazil and Ramo's portion-controlled snack cakes in Colombia. Companies are adapting their packaging and formats to facilitate consumption at home, work, or during commutes. The bakery products market continues to expand as it adapts to the changing preferences of South American urban consumers.

Demand for Artisanal and Premium Bakery Products

In South America, particularly in Brazil and Argentina, urbanization and rising disposable incomes are fueling a growing appetite for artisanal and premium bakery products. In Brazil, Grupo Bimbo's acquisition of Wickbold, a bakery in São Paulo known for its whole-grain and specialty breads, highlights the nation's shift towards high-quality, artisanal offerings. In 2024, Brazilian households averaged nearly BRL 1,180 in spending on grocery and bakery items, underscoring their increased disposable income and a readiness to invest in quality [2]Source: Associação Brasileira de Supermercados (ABRAS) / SuperHiper, “SuperHiper – Agosto de 2024 Report,” superhiper.abras.com.br. This acquisition not only bolsters Grupo Bimbo's portfolio with brands like Wickbold and Seven Boys but also resonates with the evolving preferences of Brazilian consumers, who are gravitating towards sophisticated and health-oriented bakery choices. Meanwhile, Argentina's urban centers are witnessing a surge in gourmet bakeries, signaling a broader trend towards premium products. "La Panadería de Pablo" in Buenos Aires, for instance, is carving a niche by providing artisanal breads and pastries crafted with traditional methods and natural ingredients, appealing to a consumer base that values authenticity and quality. These trends underscore a significant shift in consumer behavior, with artisanal and premium bakery products taking center stage in South America's market evolution.

Health and Wellness: Clean Label and Free-From Trends

In South America, the bakery products market is witnessing a surge, largely driven by a rising demand for clean-label and health-conscious options. These include gluten-free, zero-sugar, and additive-free products. According to projections from the International Congress on Obesity (ICO 2024, São Paulo), by 2044, nearly half of adult Brazilians (48%) will grapple with obesity, and an additional 27% will be classified as overweight [3]Source: World Obesity Federation, “Almost Half of Brazilian Adults Will Be Living with Obesity Within 20 Years,” worldobesity.org. This alarming statistic indicates that a staggering three-quarters of Brazilian adults will face weight-related challenges. Responding to this growing health consciousness, brands across South America are pivoting their offerings. For instance, Brazilian firm Jasmine Alimentos has rolled out gluten-free breads, cookies, and cakes, while Wickbold is promoting whole-grain and additive-free products. In Colombia, Boronas and Latido are catering to health-savvy consumers with their gluten-free and naturally sweetened breads and snack cakes. Meanwhile, in Argentina, brands like Celipan are introducing clean-label biscuits and breads, emphasizing transparency and natural ingredients. These trends underscore a significant shift in consumer behavior, with health and wellness taking center stage, driving innovation, and propelling the South American bakery market forward.

Strategic Marketing and Promotional Campaigns

In South America's bakery products market, strategic marketing and promotional campaigns are pivotal in shaping consumer behavior and driving growth. Brands are increasingly aligning their initiatives with the preferences of health-conscious and socially aware consumers, mirroring the rising demand for clean-label and free-from products. For instance, in Brazil, Grupo Bimbo's "Bimbo Global Race" stands out as a successful campaign. In 2024, the initiative not only aimed to donate 3 million slices of bread to food banks but also promoted active lifestyles, thereby enhancing brand loyalty. On a similar note, Jasmine Alimentos is tapping into health trends, promoting its gluten-free and organic packaged bakery products. Their targeted campaigns emphasize natural ingredients and health benefits, resonating with urban consumers in search of healthier food choices. These marketing strategies underscore how South American bakery brands are adeptly navigating changing consumer preferences, leveraging campaigns to boost product awareness, solidify brand trust, and broaden their market reach in tune with health and wellness trends.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply chain disruptions | -1.1% | Regional agricultural zones | Short term (≤ 2 years) |

| Regulatory challenges for clean labeling | -0.8% | Brazil, Argentina | Medium term (2-4 years) |

| Competition from freshly baked products | -0.6% | Urban artisanal hubs | Long term (≥ 4 years) |

| Shift to healthier snack alternatives | -0.4% | Health-focused demographics | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory Challenges for Clean Labeling

Regulatory hurdles surrounding clean labeling are stifling the growth of South America's bakery products market, introducing uncertainty and escalating compliance costs for producers. In Brazil, newly instituted front-of-pack warning labels for sugar, sodium, and saturated fats have compelled major brands, like Wickbold and Bauducco, to reformulate their popular sliced breads and cookies. However, inconsistent enforcement and disputes over deadlines have deterred smaller bakeries from venturing into clean-label innovations. These challenges have also slowed the adoption of healthier product lines, impacting the overall market growth. Furthermore, Brazil's 2023 regulation concerning "whole grain" claims faced backlash. It allowed certain packaged breads and biscuits, containing only a hint of wholemeal flour, to be marketed as whole grain. This not only muddied the waters for discerning consumers but also jeopardized trust in genuinely healthier options, such as Jasmine Alimentos' gluten-free breads. Meanwhile, in Argentina, stringent front-of-pack labeling mandates, including black octagon warnings, have impacted products like Havanna's alfajores and Fargo's cakes. These regulations limit marketing to children and prohibit sales in schools. Although these measures aim to promote healthier consumer choices, industry lobbying and postponed enforcement have led to uncertainty, inflating costs associated with reformulation and packaging.

Competition from Freshly Baked Products

In South America, the growth of the packaged bakery segment is being stunted by competition from freshly baked products. These warm, on-premise alternatives are drawing both impulse and routine purchases. In Brazil, neighborhood padarias and supermarket bake-off counters, such as Pão de Açúcar and Carrefour, are refreshing items like pão francês, cakes, and pão de queijo multiple times a day. This strategy is successfully diverting shoppers from pre-sliced and wrapped loaves. Delivery platforms, including iFood and Rappi, see padarias bundling fresh rolls and pastries with coffee, offering rapid, low-fee fulfillment. This service directly competes with packaged breads and snack cakes, catering to both home and workplace needs. In Argentina, panaderías and chains like Las Medialunas del Abuelo entice commuters with freshly baked medialunas and customizable fillings. This approach is diminishing the demand for packaged sweet biscuits during breakfast and merienda. Colombia’s Pan Pa’ Ya! and Tostao Café & Pan highlight the aroma, warmth, and freshness of their products, effectively undercutting the market for packaged cookies and mini-cakes. In Chile, Castaño is making similar waves with city-center ovens, while sourdough micro-bakeries in capital markets are emphasizing shorter ingredient lists, outpacing the “clean-label” claims of packaged goods. The outcome is clear: a decline in visits to ambient bakery aisles, quicker replacement cycles, and intensified promotional efforts from packaged brands to secure their shelf space.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Bread Dominance Faces Morning Goods Disruption

In 2025, bread commands a dominant 60.48% market share, underscoring its status as a household staple throughout South America. Brands such as Brazil's Wickbold and Grupo Bimbo's diverse offerings play a pivotal role in this supremacy, presenting everything from traditional loaves to specialty whole-grain options. Bread's ubiquitous presence, found in both urban supermarkets and local neighborhood stores, solidifies its status as the cornerstone of the bakery market.

Morning goods are set to be the fastest-growing segment, with projections indicating a 9.12% CAGR through 2031. This surge is largely attributed to urbanization and evolving breakfast preferences leaning towards convenience. Grupo Bimbo is at the forefront, promoting packaged croissants and their “Little Bites” muffin-style snacks for those on the move. In Colombia, Productos Ramo taps into this trend with their snack cakes, Gala and Chocoramo, which double as popular breakfast alternatives. While cakes and pastries thrive on a culture of premiumization and celebration, biscuits and cookies from Argentina's Bagley capitalize on snacking moments, benefiting from their extended shelf life in warmer climates.

By Form: Fresh Products Lead While Frozen Gains Infrastructure Support

In 2025, fresh products command a dominant 81.85% market share, buoyed by consumer preferences for softness, freshness, and local sourcing. In Brazil, top brands such as Bauducco, Wickbold, and Pullman cultivate robust consumer loyalty, offering a diverse range of packaged breads that span from classic white loaves to unique specialty varieties. Grupo Bimbo fortifies its market stance with its Ana Maria brand, which caters to health-conscious consumers with its reduced-sugar breads. Meanwhile, Crocantissimo and Panco diversify the market with their innovative formats and flavor extensions. Collectively, these brands anchor fresh packaged bakery items as staples in South American households.

On the other hand, frozen products are on an upswing, charting a 7.6% CAGR through 2031. This growth is largely attributed to advancements in cold chain logistics and a burgeoning demand from the foodservice sector. In Brazil, Pão & Arte has broadened its horizons, introducing artisanal-style breads to its frozen bakery lineup. Concurrently, Brico Bread has rolled out ready-to-bake frozen offerings, merging convenience with unwavering quality. These developments underscore the transition of frozen bakery items from a niche market to a mainstream staple. They not only present operational advantages for eateries but also deliver traditional flavors to consumers, albeit with an extended shelf life. The interplay of fresh and frozen segments underscores the delicate balance of tradition and innovation that defines South America's bakery landscape.

By Category: Conventional Holds Ground as Free-Form Accelerates

In 2025, the conventional category commands a 72.74% market share, bolstered by consumer familiarity, affordability, and robust retail availability. In Brazil, household staples like Pullman and Wickbold dominate supermarket shelves, offering classic packaged breads and rolls tailored for daily consumption. Brands such as Panco and Bauducco further fortify this segment with product lines that resonate with cultural eating habits, achieving broad household penetration and solidifying the conventional category’s dominance across South America.

Free-form products are on an upward trajectory, boasting an 8.21% CAGR through 2031, driven by heightened health awareness and meticulous ingredient scrutiny. In Brazil, Braven Foods has rolled out gluten-free and lactose-free powdered bakery mixes, while Wickbold has diversified its offerings with additive-free and wholegrain packaged breads. Meanwhile, in Argentina, Celipan has launched gluten-free biscuits and breads, catering to the clean-label-conscious shopper. These innovations underscore the transformative influence of free-form products on consumer behavior, prompting traditional manufacturers to reformulate existing ranges to align with clean-label standards. While conventional products still reign supreme, the swift ascent of free-form offerings signals a generational pivot towards health-centric choices in South America’s bakery landscape.

By Distribution Channel: Off-Trade Dominance Challenged by On-Trade Revival

In 2025, off-trade channels, spearheaded by supermarkets, hypermarkets, and convenience stores, command a 57.21% market share, owing to their diverse product offerings and competitive pricing. In Brazil, retailers like Pão de Açúcar and Carrefour lead the packaged bakery market, showcasing a vast array of breads, biscuits, and pastries. Meanwhile, in Colombia, private labels from chains such as Grupo Éxito are winning over households with budget-friendly alternatives. These contemporary retailers are not just relying on product range but are also amplifying consumer loyalty through strategic promotions and heightened in-store visibility.

On-trade channels are on an upswing, boasting a 9.35% CAGR projected through 2031, fueled by a revival in cafés, restaurants, and institutional dining. Brands such as Havanna in Argentina and Casa Bauducco in Brazil are not only running cafés but are also retailing their packaged cakes, alfajores, and biscuits in supermarkets and specialty stores, broadening their market reach. In a similar vein, Juan Valdez cafés in Colombia are retailing their popular cookies and brownies, making them accessible through both modern retail and online avenues. This trend underscores how on-trade entities are seamlessly merging with retail, establishing a formidable presence in both arenas.

Geography Analysis

In 2025, Brazil commands a dominant 46.05% share of South America's bakery products market, buoyed by its vast population, sophisticated retail infrastructure, and robust manufacturing capabilities. Established brands, including Bauducco and Pullman, lead the charge in packaged bread and morning goods, capitalizing on their extensive distribution networks and the trust they've cultivated with consumers. The trend of premiumization is evident, with companies rolling out cleaner-label and fortified bakery items, catering to the health-conscious urbanites of São Paulo and Rio de Janeiro.

Colombia emerges as the region's fastest-growing market, with projections indicating a 8.72% CAGR surge through 2031. This growth is anchored in the nation's economic stability, a burgeoning middle class with increased purchasing power, and a vibrant café culture that fuels the demand for packaged delights like muffins and croissants. Local powerhouse Grupo Nutresa is at the forefront, broadening its bakery offerings with a keen focus on healthier formulations and an expansive retail presence, underscoring the role of strategic investments and product innovation in this rapid ascent.

Across South America, diverse growth patterns emerge. Argentina, despite facing economic headwinds, boasts a resilient bakery culture, with consumers steadfastly supporting traditional products and local brands. Chile's progressive regulatory landscape champions the adoption of clean-label and premium bakery goods, a trend underscored by Puratos’ recent investment in a UHT production plant in Santiago. Urbanization drives growth in Peru, especially in Lima, though challenges in rural infrastructure slow penetration. Meanwhile, smaller markets like Ecuador, Uruguay, and Paraguay, though currently underpenetrated, present promising long-term prospects as consumer sophistication rises and retail formats evolve.

Competitive Landscape

South America's packaged bakery products market is fragmented, and brands are increasingly emphasizing premiumization and health-driven differentiation in their marketing strategies. Major players, such as Wickbold and Bauducco, are positioning their packaged breads and cakes as cleaner-label, whole-grain, or reduced-sugar options. This strategy aims to attract health-conscious urban consumers, and the use of premium packaging further reinforces their value proposition. Meanwhile, local brands in Argentina and Colombia are highlighting their artisanal heritage and cultural authenticity in their messaging. This approach appeals to traditional preferences while also adapting to modern convenience trends.

As competition intensifies, technology adoption emerges as a pivotal differentiator. Manufacturers are increasingly leveraging digital platforms and supply chain innovations. For instance, companies like Grupo Bimbo and M. Dias Branco are broadening their e-commerce footprint. They've forged partnerships with prominent delivery platforms and established direct-to-consumer online stores, ensuring their products reach consumers beyond conventional retail avenues. On the production front, advancements like automation in baking lines and the incorporation of quality monitoring systems are not only curbing waste but also ensuring product consistency. Furthermore, the introduction of sustainable packaging solutions aligns with both consumer expectations and regulatory demands. Such tech-driven initiatives bolster efficiency and deepen consumer engagement.

Market strategies underscore the significance of expansion, acquisitions, and local manufacturing investments. Grupo Bimbo is fortifying its presence in South America, acquiring regional entities and seamlessly integrating their offerings. In a bid to bolster the bakery and patisserie segments, Puratos inaugurated a new UHT production facility in Chile. Collaborations with retail chains and foodservice operators amplify distribution, especially for morning goods and free-form products. Concurrently, emerging disruptors are establishing footholds in clean-label and specialty segments, indicating a vibrant competitive landscape. This evolution underscores the necessity for established players to adapt continually to uphold their market leadership.

South America Bakery Products Industry Leaders

Europastry, S.A.

Grupo Bimbo SAB de CV

M Dias Branco S.A.

Alicorp S.A.A.

Grupo Arcor S.A.I.C.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Nestlé announced an expanded USD 1.3 billion investment plan in Brazil through 2028, covering new production lines and digital distribution enhancements

- March 2025: Flowers Foods introduced Wonder brand snack cakes in South America, adding eleven SKUs such as crème-filled cupcakes and mini donuts to diversify beyond core bread.

- September 2024: Grupo Bimbo launched “Bimbo Cero Cero” bread, free from added sugar, salt, and preservatives, responding to health-conscious consumer trends.

South America Bakery Products Market Report Scope

Bakery products are prepared from flour or meal derived from grains and are available in a wide range. The South American bakery products market is segmented based on product type, distribution channel, and geography. Based on product type, the market has been segmented into cakes and pastries, biscuits & cookies, bread, and pizza crust. Based on the distribution channel, the market is segmented into hypermarkets/supermarkets, convenience stores, specialty stores, and online retailing. Also, the study provides an analysis of the bakery products market in the emerging and established markets across the South America region, including Brazil, Argentina, and the Rest of South America. For each segment, the market sizing and forecasts have been done on the basis of value in USD million.

By Product Type

| Bread |

| Cakes and Pastries |

| Biscuits/Cookies |

| Morning Goods |

| Other Product Types |

By Form

| Fresh |

| Frozen |

By Category

| Conventional |

| Free-Form |

By Distribution Channel

| On- Trade Channel | |

| Off- Trade Channel | Supermarkets/Hypermarkets |

| Convenience/Grocery Stores | |

| Specialist Bakery Shops | |

| Online Retail Stores | |

| Other Distribution Channel |

By Country

| Brazil |

| Argentina |

| Colombia |

| Chile |

| Peru |

| Rest of South America |

| By Product Type | Bread | |

| Cakes and Pastries | ||

| Biscuits/Cookies | ||

| Morning Goods | ||

| Other Product Types | ||

| By Form | Fresh | |

| Frozen | ||

| By Category | Conventional | |

| Free-Form | ||

| By Distribution Channel | On- Trade Channel | |

| Off- Trade Channel | Supermarkets/Hypermarkets | |

| Convenience/Grocery Stores | ||

| Specialist Bakery Shops | ||

| Online Retail Stores | ||

| Other Distribution Channel | ||

| By Country | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the 2026 value of the South America packaged bakery products market?

The market is valued at USD 51.69 billion in 2026 and is projected to reach USD 71.32 billion by 2031.

Which product segment is growing the fastest across South America?

Morning goods, comprising croissants, muffins, and Danish pastries, are forecast to register a 9.12% CAGR through 2031.

How large is Brazil’s share of packaged bakery sales in the region?

Brazil generated 46.05% of total regional revenue in 2025, maintaining its position as the leading national market.

Which health trends influence new bakery launches?

Clean-label, free-from, and reduced-sugar formulations dominate innovation pipelines as consumers seek transparency and wellness.

Page last updated on: