Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 10.17 Billion |

| Market Size (2026) | USD 10.65 Billion |

| Market Size (2031) | USD 13.39 Billion |

| Growth Rate (2026 - 2031) | 4.68% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

South America Ice Cream Market Analysis by Mordor Intelligence

The South American ice cream market size is expected to grow from USD 10.17 billion in 2025 to USD 10.65 billion in 2026 and is forecast to reach USD 13.39 billion by 2031 at 4.68% CAGR over 2026-2031. The market is driven by increasing urbanization that concentrates consumers in cities, fostering demand for impulse snacking and convenient formats. Regulatory requirements for front-of-pack sugar warnings are influencing product innovation, prompting manufacturers to prioritize reduced-sugar, functional, and health-focused variants. Leading multinational corporations such as Unilever and Nestlé maintain a strong market presence, while regional players leverage local flavor innovation and robust distribution networks to remain competitive. Strategic initiatives, including portfolio rationalization and spin-offs, indicate a shift toward faster, localized innovation. Premiumization trends are evident in the rising demand for artisanal formats, tropical fruit flavors, and non-dairy alternatives. Additionally, evolving consumption patterns are being shaped by experiential on-trade channels and the rapid expansion of e-commerce platforms. Investments in cold-chain infrastructure are enhancing distribution efficiency; however, the market faces challenges such as raw material price volatility and climate-related supply chain disruptions. These pressures are driving consolidation, acquisitions, and a focus on technology-driven product development across the region.

Key Report Takeaways

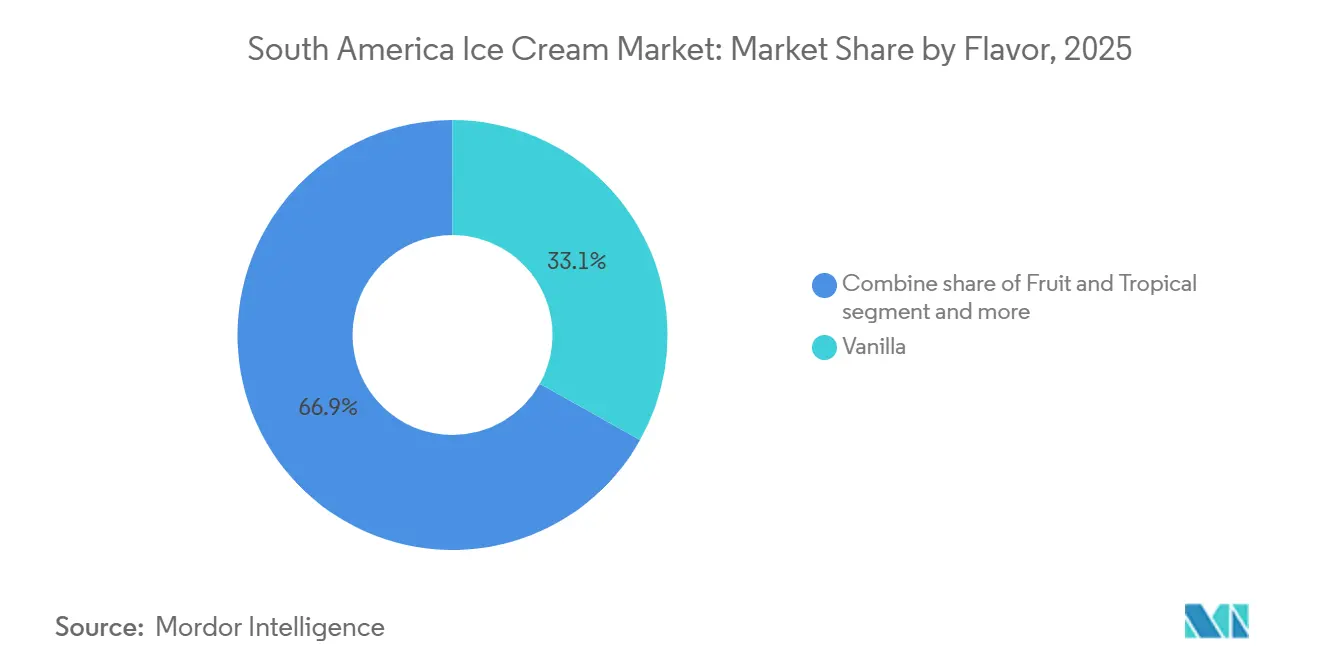

- By flavor, vanilla led with 33.12% of the South American ice cream market share in 2025, while fruit and tropical variants are forecast to expand at a 5.72% CAGR through 2031.

- By product type, take-home formats accounted for 45.78% of the South American ice cream market size in 2025, and artisanal offerings are poised to grow at a 5.71% CAGR.

- By category, dairy products dominated with 79.86% of share in 2025; non-dairy alternatives are projected to rise at a 5.83% CAGR through 2031.

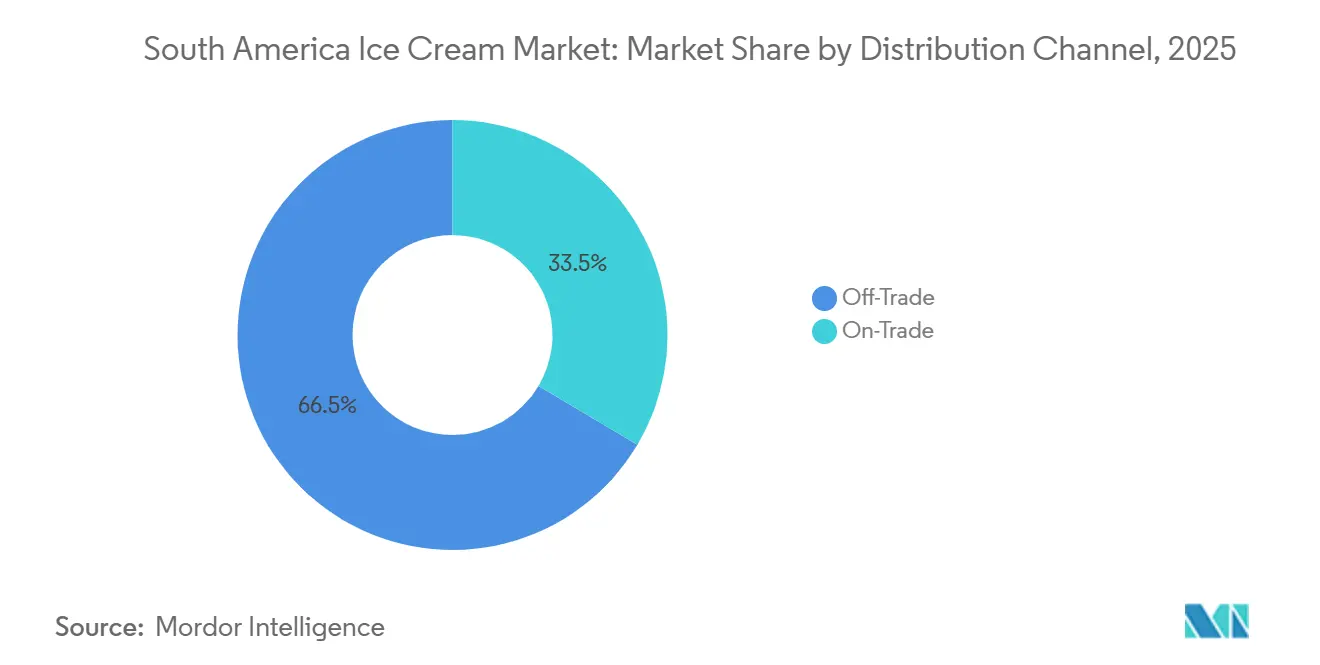

- By distribution channel, off-trade outlets held 66.48% of sales in 2025 and are advancing at a 5.92% CAGR, eclipsing on-trade growth.

- By geography, Brazil captured 52.02% of regional revenue in 2025; Chile represents the fastest-growing market with a 6.01% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South America Ice Cream Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising urbanization shifts lifestyles toward convenience snacking | +0.9% | Brazil, Argentina, Chile, Colombia - urban centers São Paulo, Buenos Aires, Santiago, Bogotá | Medium term (2-4 years) |

| Demand for premium artisanal flavors like tropical fruits | +0.7% | Brazil (North and Southeast regions), Chile (Santiago, Valparaíso), Argentina (Buenos Aires) | Long term (≥ 4 years) |

| Growth in e-commerce and food delivery platforms | +0.8% | Brazil, Argentina, Chile, Colombia - metropolitan areas with iFood, Rappi, Pedidos Ya penetration | Short term (≤ 2 years) |

| Health trends boost low-sugar and functional ice creams | +0.6% | Chile, Brazil, Argentina - markets with front-of-pack labeling mandates | Medium term (2-4 years) |

| Popularity of plant-based dairy-free alternatives | +0.5% | Brazil, Chile, Argentina - urban millennials and Gen Z consumers | Long term (≥ 4 years) |

| Lactose intolerance awareness drives non-dairy options | +0.4% | Brazil, Argentina, Colombia - overlaps with plant-based demand | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising urbanization shifts lifestyles toward convenience snacking

Urbanization across South America is driving a shift in consumer behavior toward convenience-focused snacking, creating high-demand consumption corridors where modern retail formats integrate with delivery platforms. According to the World Bank, urban populations in 2024 reached 88% in Brazil and 92% in Argentina[3]Source: World Bank "Urban Population Data", worldbank.org. This trend significantly benefits the ice cream market, as urban centers see heightened impulse purchases, particularly during peak summer months when rising temperatures boost demand. Discounters and e-commerce platforms are enhancing accessibility for cost-conscious consumers, while rapid delivery services such as iFood and Rappi strengthen the convenience proposition by offering near-instant delivery. These factors collectively position ice cream as a key indulgence in metropolitan markets, driven by urban migration, multi-channel retail strategies, and the growth of digital food ecosystems.

Demand for premium artisanal flavors like tropical fruits

The South American market for premium artisanal ice cream is undergoing significant growth, driven by affluent urban consumers seeking unique flavors and superior taste experiences. This trend is reflected in the increasing demand for tropical and regionally sourced fruits such as açaí, cupuaçu, and camu-camu, highlighting both a commitment to local biodiversity and a shift away from synthetic or conventional flavor profiles. Companies, including startups and established brands, are leveraging this opportunity by introducing small-batch, sustainability-focused products. These offerings often feature upcycled ingredients and single-origin inputs, enhancing their premium positioning. The proliferation of artisanal parlors and branded ice cream shops across major cities demonstrates strong confidence in high-margin, experience-oriented foodservice formats.

Growth in e-commerce and food delivery platforms

The South American ice cream market is undergoing a significant transformation driven by the rapid expansion of e-commerce and food delivery platforms, which are effectively bridging the gap between suppliers and consumers. Leading players such as iFood in Brazil and Rappi across multiple countries are capitalizing on quick-commerce models, offering 30-minute delivery guarantees. These efforts are supported by advancements in cold-chain logistics, which minimize product spoilage and extend market reach. Companies adopting digital-first strategies, particularly those focusing on direct-to-consumer subscription models, are achieving notable growth. Conversely, traditional wholesalers and convenience stores face increasing challenges, particularly due to the absence of real-time inventory management systems. This shift is redefining the boundaries between retail and foodservice, positioning digital channels as a critical enabler of accessibility, convenience, and long-term growth in the region's ice cream market. Additionally, the integration of data analytics and AI-driven insights is helping brands optimize supply chains and enhance customer engagement. As consumer preferences evolve, companies that invest in digital transformation and innovative delivery models are expected to gain a competitive edge in the market.

Health trends boost low-sugar and functional ice creams

In South America, health trends are reshaping the ice cream market. Regulatory mandates on front-of-pack labeling are pushing manufacturers to reformulate products, opting for lower sugar content and incorporating functional ingredients. In 2024, Brazil's National Health Surveillance Agency (ANVISA) updated its front-of-pack labeling regulations, mandating warning symbols for high sugar content [1]Source: Agência Nacional de Vigilância Sanitária, “Labeling Standards,” ANVISA, gov.br. Similarly, countries like Chile, Brazil, and Argentina have enacted stringent labeling rules. These regulations discourage high-sugar offerings, leading to the introduction of reduced-fat, lactose-free, and plant-protein ice cream variants. Consumers are showing a growing preference for functional additions in their ice creams, such as protein, fiber, and probiotics. Moreover, natural sweeteners like stevia and xylitol are becoming increasingly popular in plant-based formulations. This evolution in the market underscores the dual influence of regulatory pressures and shifting consumer preferences, with low-sugar and functional ice creams emerging as pivotal drivers of innovation and growth in the region.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health concerns over high sugar and calories | -0.8% | Chile, Brazil, Argentina - markets with front-of-pack labeling and sugar taxes | Medium term (2-4 years) |

| Supply chain disruptions in cold chain logistics | -0.6% | Brazil, Peru, Paraguay - rural and peri-urban areas with infrastructure gaps | Short term (≤ 2 years) |

| Raw material price volatility for dairy and sugar | -0.7% | Brazil, Argentina, Colombia - dairy and sugar-producing regions | Short term (≤ 2 years) |

| Intense competition from multinationals and locals | -0.5% | Brazil, Argentina, Chile - urban markets with high retail density | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Health concerns over high sugar and calories

In South America, health concerns over high sugar and calorie content are curbing ice cream consumption, especially among urban consumers who now view it more as an indulgent treat than a daily snack. The Chilean Ministry of Health has advised in its 2024 dietary guidelines to limit frozen dessert consumption to just once a week. This poses challenges, especially for impulse buys near schools [2]Source: Chilean Ministry of Health, “Dietary Guidelines 2024,” MINSAL, minsal.cl. Many countries are expanding front-of-pack labeling and implementing sugar-related fiscal measures, further discouraging these impulse purchases and intensifying regulatory scrutiny on manufacturers. While companies are rolling out reduced-sugar and reformulated variants in response, these changes often come with higher ingredient costs or compromises on taste. This not only compresses profit margins but also raises competitive barriers. Larger multinational corporations can better absorb these reformulation costs thanks to their global research and development scale. In contrast, regional players find themselves at a crossroads, having to choose between premium pricing and potential profit erosion. Additionally, the growing emphasis on health and wellness trends is reshaping consumer preferences, compelling manufacturers to innovate while navigating regulatory complexities. Companies that fail to adapt to these evolving dynamics risk losing market share in an increasingly competitive landscape. rejection if sensory profiles deviate significantly from established expectations.

Supply chain disruptions in cold chain logistics

The South America ice cream market faces significant challenges due to cold-chain logistics constraints. Infrastructure deficiencies escalate operational costs and restrict market penetration in rural areas. While substantial investments are enhancing cold-chain capacity in urban regions, peri-urban and rural areas continue to rely heavily on outdated diesel-powered refrigerated trucks. This dependency increases vulnerability to fuel price volatility and climate-related disruptions. Temperature fluctuations during last-mile delivery frequently result in product spoilage and wastage, further straining supply chains. Additionally, power outages caused by extreme weather events compromise product quality and integrity. These issues disproportionately impact smaller market players, particularly those lacking robust backup systems or diversified distribution networks, thereby limiting their ability to expand beyond major urban centers. Addressing these logistical inefficiencies is critical for fostering sustainable growth and unlocking the market's full potential in underserved regions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Flavor: Tropical Variants Reshape Taste Hierarchies

In 2025, traditional flavors such as vanilla, commanding a 33.12% market share, remained a cornerstone of the South American ice cream market due to their broad consumer appeal and cost-efficient formulation. Chocolate, underpinned by the region's cocoa heritage, continued to experience strong demand. However, fluctuations in cocoa prices have compelled manufacturers to optimize formulations and explore alternative ingredients to maintain profitability. Conversely, fruit and tropical flavors represent the fastest-growing segment, with a projected CAGR of 5.72% through 2031. This growth is driven by the region's strong preference for ingredients like açaí, cupuaçu, guava, and passion fruit. These flavors resonate particularly well in Brazil, where biodiversity-inspired formulations and locally sourced ingredients are gaining consumer acceptance and visibility.

Beyond traditional offerings, flavors such as dulce de leche, cookies-and-cream, and salted caramel are serving as platforms for premium and limited-edition product innovations. To comply with stricter labeling regulations and address the increasing demand for vegan options, manufacturers are introducing reduced-sugar and plant-based tropical variants. Flavor development is increasingly aligned with sustainability initiatives, incorporating upcycled fruit ingredients, single-origin cocoa, and traceable vanilla to enhance premium positioning. As a result, flavor innovation is evolving beyond basic taste differentiation to deliver a comprehensive value proposition centered on health, authenticity, and environmental sustainability.

By Product Type: Artisanal Formats Gain Momentum

In 2025, take-home ice cream led the South American market, capturing a 45.78% share, primarily driven by the popularity of family-size tubs and multi-packs distributed through supermarkets and hypermarkets. Impulse products, such as single-serve bars and cones, benefit from extensive distribution networks; however, profitability is constrained by aggressive promotional activities and fluctuations in raw material costs. Conversely, the artisanal ice cream segment is experiencing robust growth, with a CAGR of 5.71% projected through 2031. This expansion is supported by the proliferation of parlors in major urban centers and the entry of foodservice chains into the category, capitalizing on higher-margin opportunities and the increasing demand for premium, experience-oriented offerings.

Premiumization is driving innovation across all product categories. High-value offerings, including single-origin cocoa, exotic fruit sorbets, and alcohol-infused variants, are commanding price premiums and appealing to affluent millennial consumers. In response, take-home ice cream products are introducing smaller premium tubs designed for urban singles and couples, while investments in cold-chain infrastructure are enhancing accessibility in rural areas. Although weather variability continues to influence overall sales, premium brands and artisanal collaborations are achieving significant growth, reflecting a regional shift toward quality, innovation, and differentiated consumer experiences in the ice cream market.

By Category: Non-Dairy Alternatives Accelerate

In 2025, dairy ice cream is set to maintain its stronghold in the South American market, boasting a commanding 79.86% share. This dominance is bolstered by consumer familiarity, efficient production methods, and established supply chains. The traditional taste and texture of dairy ice cream resonate with mainstream consumers, especially those sensitive to price. Meanwhile, non-dairy alternatives, projected to grow at a CAGR of 5.83% through 2031, are rapidly gaining traction. This surge is largely attributed to increasing awareness of lactose intolerance, the rise of plant-based diets, and a growing emphasis on ethical consumption. As the region becomes more receptive to lactose-free and vegan options, there's a notable surge in innovation. Formulations based on coconut, almond, oat, cashew, and even Brazil nuts are emerging, with premium brands harnessing technology to mimic the mouthfeel of dairy and boost sensory appeal.

While non-dairy products grapple with higher formulation costs and the challenge of replicating dairy's texture, regulatory changes and front-of-pack labeling mandates are leveling the playing field. These shifts are nudging dairy producers to rethink and reformulate their high-sugar products. Non-dairy brands are carving out a niche as cleaner, modern alternatives. In response, traditional dairy players are diversifying, venturing into plant-based, lactose-free, and reduced-fat offerings to mitigate risks. The increasing incorporation of alternative sweeteners and functional ingredients underscores a significant evolution in the category, as both dairy and non-dairy entities align with the shifting demands for health, sustainability, and transparency.

By Distribution Channel: Off-Trade Dominance Solidifies

In South America, off-trade channels, including supermarkets, hypermarkets, convenience stores, and online platforms, dominated ice cream distribution, accounting for 66.48% of sales in 2025. These channels offered a range of products, from family-size tubs and multi-packs to impulse buys, through extensive retail networks. While convenience stores and kiosks primarily drove single-serve purchases, online platforms like iFood and Rappi revolutionized access with their rapid delivery and subscription models. Even with challenges like margin pressures from promotions and fluctuations in raw material costs, off-trade channels maintained their dominance, with digital-first strategies emerging as the fastest-growing segment.

On-trade venues, however, are gaining traction by catering to experiential demands, projected to grow at a CAGR of 5.92% through 2031. In urban centers like São Paulo, Buenos Aires, and Santiago, artisanal parlors and foodservice chains flourish as consumers increasingly seek premium, customizable, and visually appealing experiences. Brands such as Chiquinho Sorvetes, Diletto, and Grupo Nutresa are expanding their parlors and branded shops, underscoring ice cream's significance as a lucrative foodservice adjacency. Specialty stores and gourmet retailers are addressing the needs of health-conscious consumers with functional and plant-based offerings, while the premium pricing of these products is bolstered by narratives of transparency and sustainability. Collectively, both on-trade and digital channels are reshaping the ice cream consumption landscape, merging indulgence with convenience and enriched experiences.

Geography Analysis

In 2025, Brazil is set to command a dominant 52.02% share of the South American ice cream market. This stronghold is bolstered by Brazil's vast population, heightened urbanization, a mature retail framework, and a sophisticated food delivery system. Investments in cold-chain logistics, coupled with evolving labeling regulations, have spurred innovations, particularly in premium and reduced-sugar ice cream segments. While Argentina boasts a rich ice cream consumption tradition and a robust domestic dairy foundation, its growth is hampered by macroeconomic challenges and currency fluctuations.

Chile emerges as the standout performer, projected to grow at a CAGR of 6.01% through 2031. This growth is fueled by rising incomes, a regulatory environment that incentivizes compliant reformulation, and a burgeoning artisanal ice cream parlor scene in urban centers. Meanwhile, Colombia and Peru are on the rise, driven by a burgeoning middle class and deeper retail penetration. However, challenges remain, as rural cold-chain limitations hinder broader distribution. Regional players are making strategic acquisitions, bolstering their positions in the Andean corridor and underscoring their confidence in sustained demand.

While smaller markets like Paraguay, Uruguay, and Bolivia, hold a modest slice of the regional sales pie, they offer enticing prospects for consolidation and expansion. Companies eyeing these markets recognize the potential rewards of investing in infrastructure and localized distribution. In summary, South America's ice cream landscape is a tapestry of Brazil's dominant scale, Chile's rapid ascent, and the gradual modernization of secondary markets, all weaving into a more formal retail and cold-chain narrative.

Competitive Landscape

In the South American ice cream market, a mix of multinational giants like Unilever and Nestlé competes with robust regional players such as Arcor, Grupo Nutresa, and Chiquinho Sorvetes. While global brands harness vast portfolios, marketing prowess, and robust supply chains, regional firms thrive on local tastes, nimble distribution, and deep brand loyalty. Multinationals are streamlining their focus on core ice cream operations, leading to quicker decisions and localized product innovations.

Regional players are making strategic acquisitions to boost procurement efficiencies and retail visibility. Meanwhile, the rise of private labels in budget-conscious segments is intensifying competition. As retailers champion store brands, established players counter with heightened promotions, premium product lines, and accelerated new product launches to safeguard their brand value and shelf presence.

Innovation is at the forefront, with companies venturing into plant-based, functional, and premium indulgent offerings, mirroring evolving consumer tastes. Urban artisanal parlor chains are carving a niche by prioritizing customization and unique experiences. Concurrently, bolstered investments in cold-chain logistics are broadening distribution networks, easing operational challenges, and amplifying competition in both mature and nascent South American markets.

South America Ice Cream Industry Leaders

-

Unilever PLC

-

Nestlé S.A.

-

Arcor S.A.I.C.

-

Helacor S.A.

-

Colombina S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Lactalis invested USD 55.3 million to expand its dairy processing facilities in Paraná, Brazil. This strategic investment increases ultra-high temperature milk production capacity while scaling up operations in yogurt, fermented dairy products, beverages, and desserts, strengthening its presence in the South American dairy market and supporting downstream ice cream and dessert manufacturers.

- June 2025: Nestlé is set to invest USD 1.3 billion in Brazil by 2028 to enhance production capacity, modernize technological infrastructure, and drive innovation and sustainability across core food and beverage categories, thereby strengthening its South American ice cream business.

- April 2024: Hortifruti Natural da Terra, a prominent player in Brazil, introduced its first private-label ice cream line, featuring a range of traditional and gourmet flavors. The company is strategically expanding its private-label portfolio to include over 300 products, aiming to strengthen its market position in the frozen dessert segment.

South America Ice Cream Market Report Scope

Ice cream is a frozen dessert made by blending a base, traditionally dairy, such as milk or cream, or non-dairy alternatives like coconut, almond, oat, or cashew, with sweeteners, flavors, and stabilizers, then freezing while churning to create a smooth texture. The South American ice cream market is segmented by flavor, product type, category, distribution channel, and country. By product type, the market is segmented into artisanal ice cream, impulse ice cream, and take-home ice cream. By flavor, the market is segmented into vanilla, chocolate, fruit and tropical, and others. By category, the market is segmented into conventional and organic. By distribution channel, the market is segmented into on-trade and off-trade. By country, the market is segmented into Brazil, Argentina, Chile, Peru, Colombia, Paraguay, Uruguay, and the rest of South America. The market forecasts are provided in terms of value (USD).

By Flavor

| Vanilla |

| Chocolate |

| Fruit and Tropical |

| Others |

By Product Type

| Artisanal Ice Cream |

| Impulse Ice Cream |

| Take-home Ice Cream |

By Category

| Dairy |

| Non-Dairy |

By Distribution Channel

| On-Trade | |

| Off-Trade | Supermarkets/Hypermarkets |

| Specialist Retailers | |

| Convenience Stores | |

| Online Retail Stores | |

| Other Distribution Channels |

By Geography

| Brazil |

| Argentina |

| Chile |

| Columbia |

| Peru |

| Paraguay |

| Uraguay |

| Rest of South America |

| By Flavor | Vanilla | |

| Chocolate | ||

| Fruit and Tropical | ||

| Others | ||

| By Product Type | Artisanal Ice Cream | |

| Impulse Ice Cream | ||

| Take-home Ice Cream | ||

| By Category | Dairy | |

| Non-Dairy | ||

| By Distribution Channel | On-Trade | |

| Off-Trade | Supermarkets/Hypermarkets | |

| Specialist Retailers | ||

| Convenience Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | Brazil | |

| Argentina | ||

| Chile | ||

| Columbia | ||

| Peru | ||

| Paraguay | ||

| Uraguay | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the South America ice cream market in 2026?

The market is valued at USD 10.65 billion in 2026, with a projected rise to USD 13.39 billion by 2031 at a 4.68% CAGR.

Which flavor generates the most revenue?

Vanilla leads with 33.12% of revenue, maintaining broad appeal across the region.

Which segment is growing fastest?

Artisanal formats post the highest growth, advancing at a 5.71% CAGR through 2031 on the back of experiential retail and premium ingredients.

How important is e-commerce for ice cream sales?

Online channels already capture 11% of off-trade sales in Brazil and are expanding rapidly thanks to insulated delivery logistics.

Page last updated on: