Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

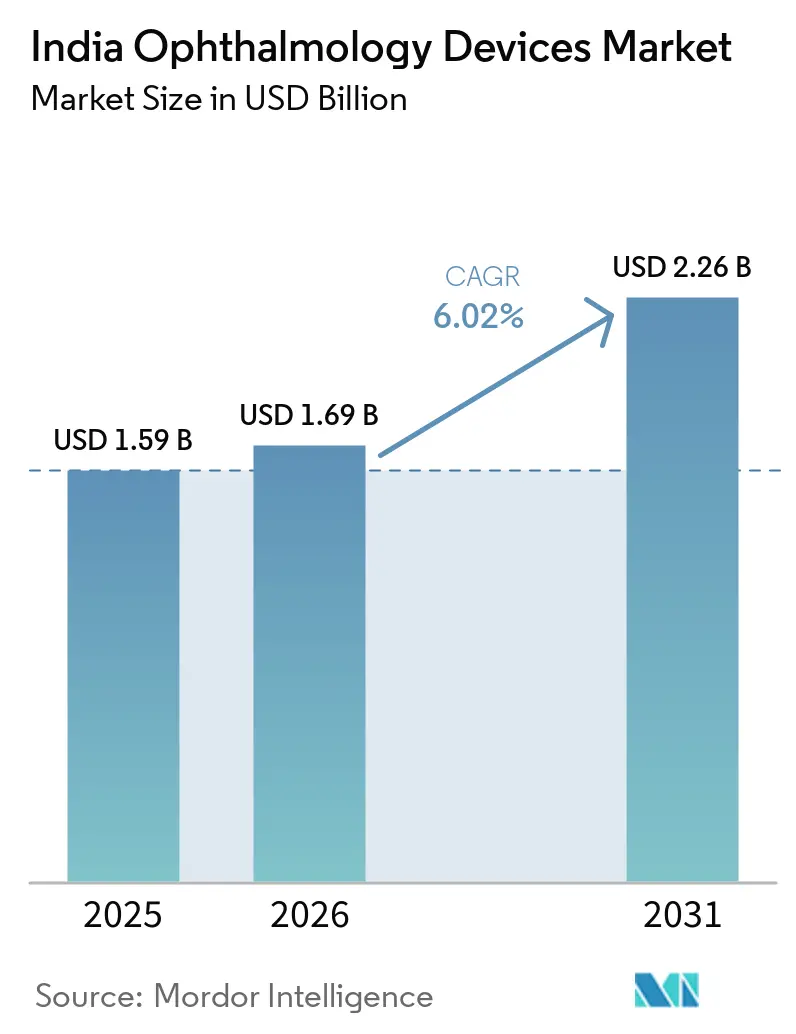

| Base Year Market Size (2025) | USD 1.59 Billion |

| Market Size (2026) | USD 1.69 Billion |

| Market Size (2031) | USD 2.26 Billion |

| Growth Rate (2026 - 2031) | 6.02% CAGR |

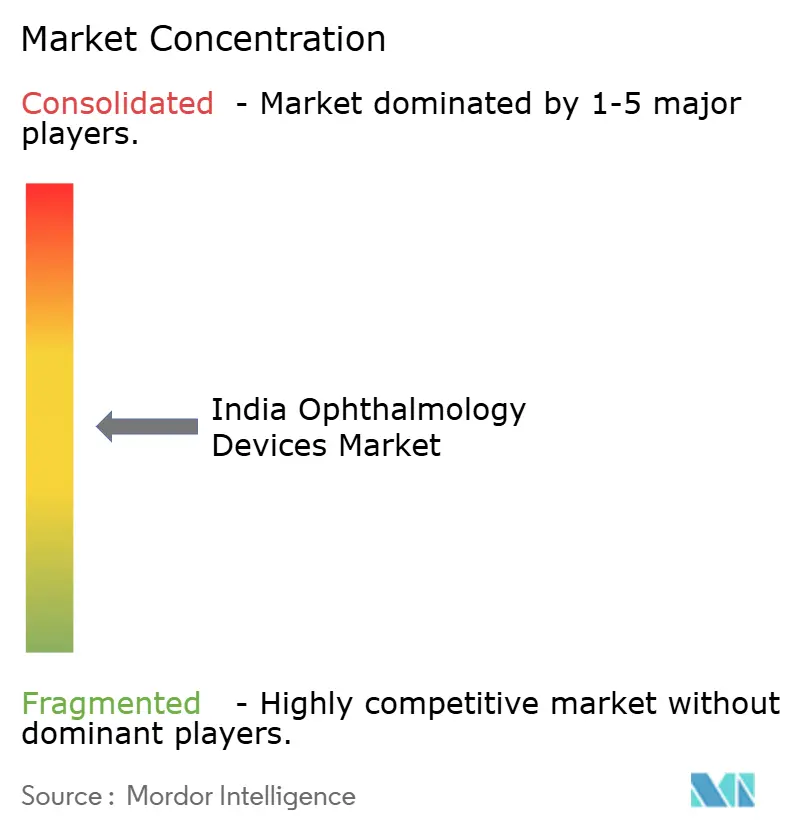

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Ophthalmology Devices Market Analysis by Mordor Intelligence

The India Ophthalmology Devices Market size was valued at USD 1.59 billion in 2025 and is estimated to grow from USD 1.69 billion in 2026 to reach USD 2.26 billion by 2031, at a CAGR of 6.02% during the forecast period (2026-2031).

Robust public‐health funding, rising digital‐screen exposure, and a widening pool of older adults are aligning to create a broad, stable demand base that shields the India ophthalmology devices market from short-term economic swings. The National Programme for Prevention and Control of Blindness (NPCB) and the Ayushman Bharat Health Infrastructure Fund (AB-HIF) together underwrite large‐scale device procurements, while private hospitals and ambulatory surgery centres chase premium technologies to attract urban patients. Indigenous start-ups now introduce frugal innovations that undercut traditional import prices by up to 50%, prompting global brand owners to localise production and re-engineer mid-tier platforms for the India ophthalmology devices market. Competitive intensity is pivoting from pure hardware credentials to service uptime, clinician training, and digital connectivity, signalling a maturity arc that historically took longer to unfold in comparable emerging markets.

Key Report Takeaways

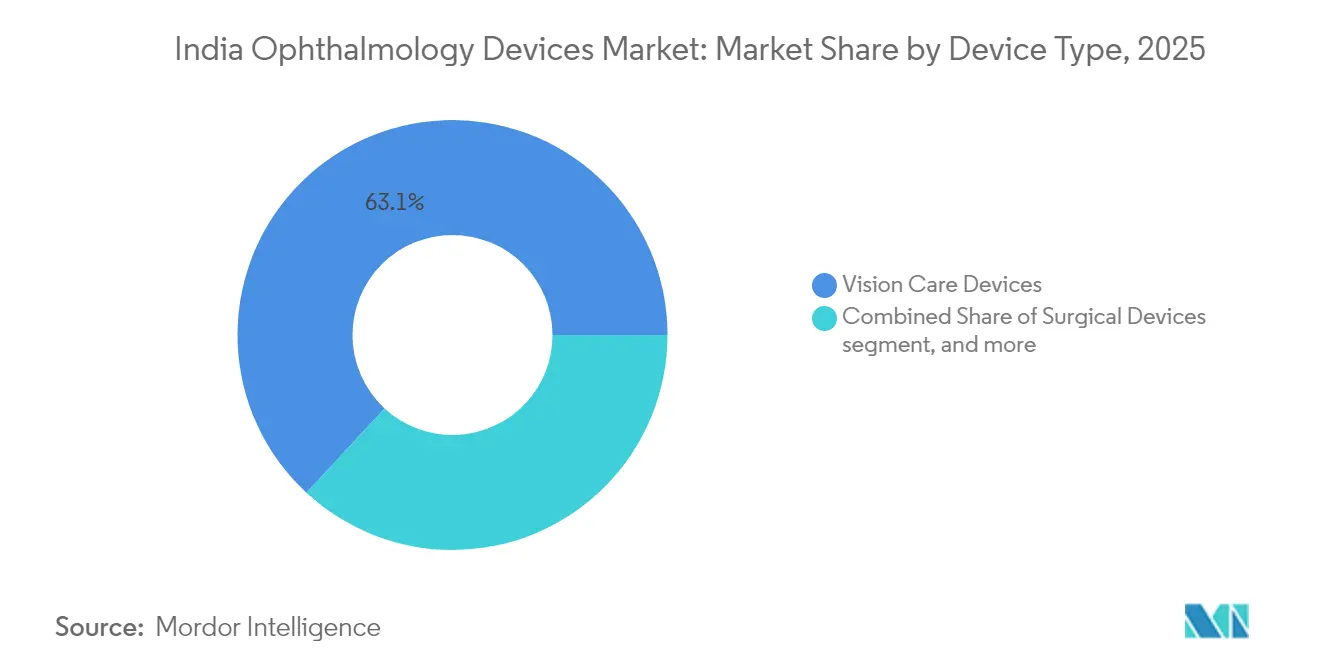

- By device type, vision care devices led with 63.12% India ophthalmology devices market share in 2025, whereas diagnostic & monitoring devices are projected to expand at a 8.87% CAGR through 2031.

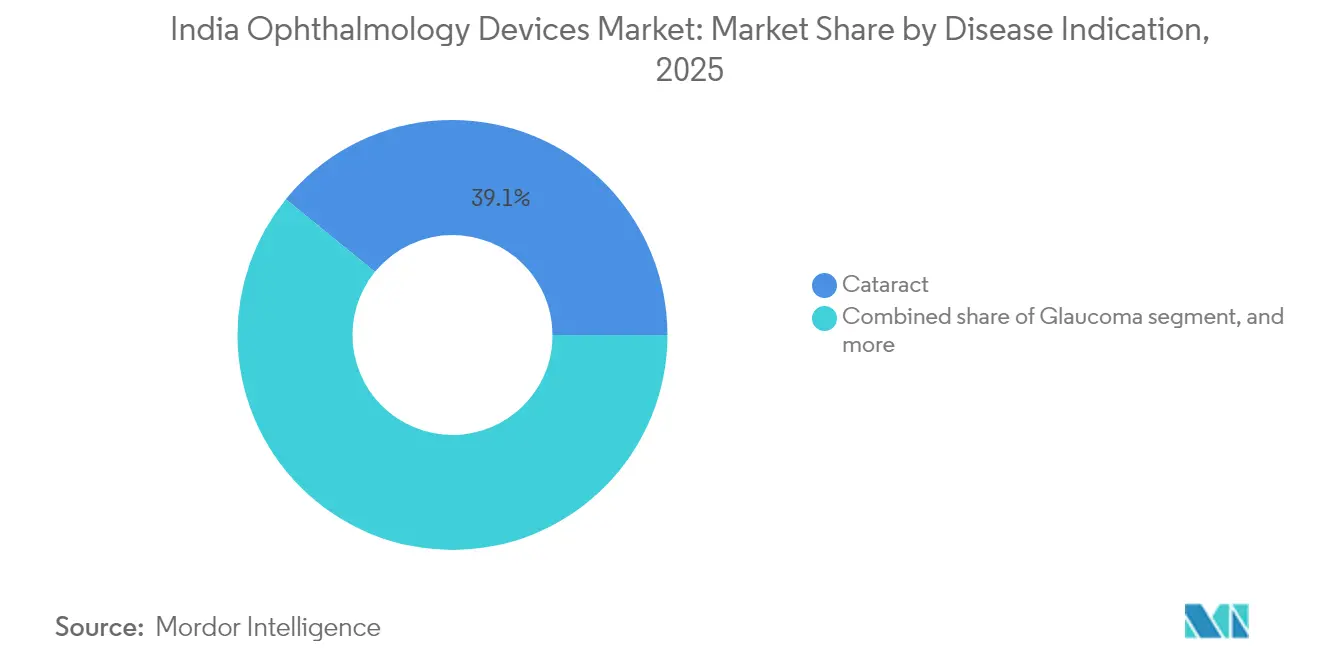

- By disease indication, cataract solutions captured 39.12% share of the India ophthalmology devices market size in 2025, while diabetic-retinopathy products are positioned to grow at an 8.05% CAGR to 2031.

- By end-user, hospitals accounted for 45.25% of the India ophthalmology devices market size in 2025; ambulatory surgery centres are expected to post the fastest 7.78% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Ophthalmology Devices Market Trends and Insights

Driver Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| National Program for Prevention & Control of Blindness (NPCB) catalysing state-level device procurements | +1.2 | National, with emphasis on underserved states | Medium term (2-4 years) |

| Expansion of Ayushman Bharat Health Infrastructure Fund driving ophthalmic OT upgrades | +0.9 | National, strongest in Tier-II/III cities | Medium term (2-4 years) |

| Rapid uptake of femtosecond-laser-assisted cataract surgery (FLACS) in Tier-I cities | +0.7 | Metropolitan and Tier-I cities | Short term (≤ 2 years) |

| Surge in screen-induced myopia among 6–18-year-olds boosting prescription spectacles | +1.1 | Urban centres, especially South & West India | Long term (≥ 4 years) |

| Growing penetration of CSR-funded mobile eye-surgery camps in rural West India | +0.6 | Rural West India, expanding to Central & East | Medium term (2-4 years) |

| Emergence of indigenous low-cost OCT & fundus cameras from start-ups (e.g., Remidio) | +0.8 | National, early adoption in South India | Medium term (2-4 years |

| Source: Mordor Intelligence | |||

National Programme for Prevention and Control of Blindness Catalysing State-level Device Procurements

The NPCB earmarked INR 2 506.9 crore for district eye-care projects in the current plan cycle, and tenders now prioritise portable slit lamps, handheld fundus cameras, and modular phaco machines for secondary facilities[1]Bhopal Memorial Hospital & Research Centre, “NPCB Budget Allocation,” bmhrc.ac.in. States that deploy mobile ophthalmic units report shorter referral times, nudging private vendors to embed battery back-up and rugged casings in product designs. The funding stream also mandates training quotas, so manufacturers that bundle onsite workshops gain a competitive edge. Ultimately, steady NPCB financing shores up baseline demand across the India ophthalmology devices market, creating visibility that helps suppliers justify local assembly lines.

Ayushman Bharat Health Infrastructure Fund Driving Ophthalmic OT Upgrades

The Union budget allocates more than INR 90 000 crore for AB-HIF in 2025, releasing capital to modernise operating theatres in 12 000 public hospitals[2]Ministry of Health & Family Welfare, “Ayushman Bharat Health Infrastructure Fund Brief,” mohfw.gov.in. Ophthalmology departments are utilising these grants to install networked microscopes, sterilisation pods, and environment-control systems that reduce postoperative infection rates. Interoperable software integrates the new hardware with the Ayushman Bharat Digital Mission, providing asset-usage analytics that influence future procurement models. When utilisation rates become transparent, administrators favour platforms with documented uptime histories, pushing global and domestic vendors to deliver verified service metrics to protect India ophthalmology devices market share.

Rapid Uptake of Femtosecond Laser-Assisted Cataract Surgery in Tier-I Cities

Metropolitan eye chains are marketing Femtosecond Laser-Assisted Cataract Surgery (FLACS) as a gentler alternative to conventional phacoemulsification, even though it adds roughly INR 70 000 to a cataract bill. Surgeons highlight sub-2 mm incisions and faster visual recovery to position FLACS as a premium bundle with toric or multifocal intraocular lenses. As patients upgrade, disposable accessory consumption rises, amplifying recurring revenue. Vendors that provide integrated laser, imaging, and IOL suites find stronger bargaining power with top chains, contributing to the demand slope that lifts the India ophthalmology devices market.

Surge in Screen-Induced Myopia Among 6–18 Year-olds Boosting Prescription Spectacles

Screen time among urban students often exceeds 6 hours a day, and researchers project paediatric myopia prevalence could reach 48.1% by 2050[3]Times of India, “Urban Screen Time and Myopia,” timesofindia.indiatimes.com. Parents now seek earlier eye exams, swelling footfall at optical outlets and driving adoption of handheld autorefractors for on-site refraction. Blue-light filtering and anti-fatigue lenses become standard upsell features, reinforcing Vision Care Devices as the economic anchor of the India ophthalmology devices market.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of trained vitreo-retinal surgeons in Tier-II/III cities | –0.8 | Tier-II/III cities, Central & East India | Medium term (2-4 years) |

| High 12% GST on ophthalmic capital equipment raising cap-ex barriers for small clinics | –0.6 | National, felt most in smaller cities | Short term (≤ 2 years) |

| Price-sensitive consumer base limiting adoption of daily-disposable contact lenses | –0.4 | National, stronger in rural areas | Long term (≥ 4 years) |

| Fragmented after-sales service network outside metro clusters | –0.5 | Semi-urban & rural regions nationwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shortage of Trained Vitreo-Retinal Surgeons in Tier-II/III Cities

India has about 1 400 registered retinal specialists for more than 1.4 billion citizens, leaving many districts without adequate surgical coverage. Hospitals hesitate to invest in advanced vitrectomy consoles when qualified staff remain scarce, muting high-end device demand outside metros. Equipment makers respond with intuitive graphical interfaces and remote-support modules, yet real expansion awaits residency pipeline reforms. Until then, the talent deficit slows penetration of complex systems in large pockets of the India ophthalmology devices market.

High GST on Ophthalmic Capital Equipment Raising Cap-ex Barriers for Small Clinics

Ophthalmic capital goods still attract a 12% Goods and Services Tax, unlike ostomy appliances that were lowered to 5% in 2024. For single-chair clinics, the tax adds meaningful strain to cash flows because input-credit eligibility is unclear, pushing many owners to defer purchases. Larger hospital chains leverage volume discounts and financing deals to blunt the impact, widening the competitive gulf. Unless future GST Council rulings reduce the rate, small practices will struggle to refresh fleets, affecting overall velocity in the India ophthalmology devices market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Vision Care Dominance and Diagnostic Acceleration

Vision Care Devices, ranging from frames to automated lens edging systems, held 63.12% India ophthalmology devices market share in 2025. The rise of organised retail chains and corporate wellness programmes drives demand for quick refraction tools and lens-coating units that allow same-visit dispensing. Parallel e-commerce platforms funnel online shoppers into stores for final fittings, boosting traffic for objective refraction kiosks. AI-enabled lens-measurement apps further compress consultation times, increasing throughput without large capital spend.

Diagnostic & Monitoring Devices are on track for a 8.87% CAGR because portable OCT scanners, smartphone-linked fundus cameras, and home tonometry kits blend affordability with clinical precision. Regulatory acceptance of offline AI, illustrated by the CDSCO nod to Remidio’s Medios DR AI in 2024, enhances clinician confidence. Investment flows into cloud platforms that analyse imaging data, trading upfront hardware margins for subscription revenues. Surgical Devices remain smaller but capture high-value spend as FLACS and microincision vitrectomy units replace legacy phaco systems in referral hospitals. Suppliers leverage service contracts that guarantee 95% uptime, embedding loyalty and recurring part sales into the India ophthalmology devices market size calculus.

By Disease Indication: Cataract Volume and Diabetic Retinopathy Velocity

Cataract equipment retains the largest slice of India ophthalmology devices market size at 39.12% because public hospitals must meet surgery targets set under NPCB. High-volume district centres prefer dual-phaco workstations that permit parallel cases, lifting daily throughput. Disposable injector systems and foldable intraocular lenses account for the bulk of consumable spend, sustaining manufacturer service footprints in semi-urban belts.

Diabetic retinopathy solutions promise an 8.05% CAGR as India hosts more than 101 million diabetics. Early-stage screening now migrates into primary clinics and mobile vans, empowering non-ophthalmologists to capture retinal images. AI algorithms triage cases by severity, freeing scarce specialists for complex interventions. Glaucoma and age-related macular degeneration segments follow behind yet harvest incremental demand through minimally invasive implants and sustained-release drug dispensers, nudging cross-selling opportunities across the India ophthalmology devices market.

By End-user: Hospital Scale Meets ASC Agility

Hospitals captured 45.25% of the India ophthalmology devices market size in 2025, driven by their capacity to host complex multi-specialty clinics and obtain AB-HIF grants for operating-theatre upgrades. Digital imaging suites link operating rooms to teaching auditoriums, reinforcing hospitals’ role as talent hubs and service referral nodes. Specialty ophthalmic clinics place second; their nimble governance lets them trial AI triage tools sooner, expanding patient rosters without proportionate staff additions.

Ambulatory surgery centres log an expected 7.78% CAGR because insurers push for procedures that qualify for same-day discharge, cutting cost per case by up to 40%. Vendors respond with compact phaco machines and integrated sterilisation modules that fit space-constrained venues. Mobile eye units, often CSR funded, operate hub-and-spoke circuits that serve migration corridors, embedding rugged devices into rural delivery models across the India ophthalmology devices market.

Competitive Landscape

Global manufacturers such as Alcon, Johnson & Johnson Vision Care, and Carl Zeiss Meditec secure enduring visibility through surgeon-training academies, broad distribution, and multi-modal portfolios. Alcon’s worldwide sales rose 8% in 2023 to USD 9.37 billion, and part of that growth came from customising mid-price phaco platforms for Indian procurement contracts. These incumbents enter value-sensitive tiers by launching compact workstations that share core optics with flagship lines but exclude premium automation, thereby protecting margin while defending their India ophthalmology devices market share.

Indigenous contenders, led by Remidio, Sankara Health Innovation, and Forus Health, deliver smartphone-integrated retinal cameras, low-cost OCT units, and AI screening engines that operate offline. Remidio’s Medios DR AI received CDSCO approval in 2024 and the company closed USD 25 million in venture funding, elevating its valuation to USD 67.5 million. Domestic innovation unlocks price points that Tier-III clinics can afford without sacrificing diagnostic accuracy, pulling latent demand into the formal channel. International brands react by exploring licensing or co-manufacturing deals to maintain relevance across the India ophthalmology devices market.

Service differentiation gains prominence. Hospital groups demand uptime guarantees above 95% and expect remote diagnostics to resolve minor glitches within 45 minutes. Vendors now house spare-part depots in eight logistics hubs instead of three, slashing turnaround times. Subscription-based maintenance contracts, once optional, become prerequisite for tender eligibility. As refurbishment quality improves, a price band emerges where certified pre-owned systems compete against new low-cost devices, adding complexity to market positioning decisions. By 2030, the combined share of the top five manufacturers is projected to hover near 55%, keeping the India ophthalmology devices market in the moderately fragmented zone where both global and local players can thrive.

India Ophthalmology Devices Industry Leaders

Johnson & Johnson Vision Care

Carl Zeiss Meditec AG

Bausch + Lomb Corp.

Alcon Inc.

EssilorLuxottica SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Remidio received CDSCO approval for AI modules targeting glaucoma and age-related macular degeneration, expanding its regulatory-cleared portfolio.

- April 2025: Dr Mohan’s Diabetes Specialities Center deployed an in-house AI algorithm that flags early retinal lesions during routine diabetes check-ups, raising screening coverage for its 350 000 patient base.

- February 2025: Kerala launched Nayanamritham 2.0, India’s first state-wide AI eye-disease screening network, in partnership with Remidio and state health authorities.

- October 2024: Remidio’s Medios DR AI, an offline diabetic-retinopathy solution, secured CDSCO clearance, permitting nationwide commercial rollout.

India Ophthalmology Devices Market Report Scope

As per the scope of the report, ophthalmology devices are medical devices used in the identification and treatment of ocular defects or deficiencies and eye disorders. The ophthalmology devices are designed for diagnostics, surgical, and vision correction purposes. These devices are continuously gaining increased importance and adoption due to the high prevalence of various ophthalmic diseases, such as glaucoma, cataract, and other vision-related issues.

The segmentation of the India ophthalmology devices market is categorized by device type, disease indication, and end-user. By device type, the market includes diagnostic and monitoring devices such as OCT scanners, fundus and retinal cameras, autorefractors and keratometers, corneal topography systems, ultrasound imaging systems, perimeters and tonometers, and other diagnostic and monitoring devices. Surgical devices are further segmented into cataract surgical devices, vitreoretinal surgical devices, refractive surgical devices, glaucoma surgical devices, and other surgical devices. Vision care devices include spectacle frames and lenses, as well as contact lenses. By disease indication, the market is segmented into cataracts, glaucoma, diabetic retinopathy, and other conditions. By end-user, the market is divided into hospitals, specialty ophthalmic clinics, ambulatory surgery centers (ASCs), and other users. The report offers the value (in USD) for the above segments.

By Device Type

| Diagnostic & Monitoring Devices | OCT Scanners |

| Fundus & Retinal Cameras | |

| Autorefractors & Keratometers | |

| Corneal Topography Systems | |

| Ultrasound Imaging Systems | |

| Perimeters & Tonometers | |

| Other Diagnostic & Monitoring Devices | |

| Surgical Devices | Cataract Surgical Devices |

| Vitreoretinal Surgical Devices | |

| Refreactive Surgical Devices | |

| Glaucoma Surgical Devices | |

| Other Surgical Devices | |

| Vision Care Devices | Spectacles Frames & Lenses |

| Contact Lenses |

By Disease Indication

| Cataract |

| Glaucoma |

| Diabetic Retinopathy |

| Other Disease Indications |

By End-user

| Hospitals |

| Specialty Ophthalmic Clinics |

| Ambulatory Surgery Centers (ASCs) |

| Other End-users |

| By Device Type | Diagnostic & Monitoring Devices | OCT Scanners |

| Fundus & Retinal Cameras | ||

| Autorefractors & Keratometers | ||

| Corneal Topography Systems | ||

| Ultrasound Imaging Systems | ||

| Perimeters & Tonometers | ||

| Other Diagnostic & Monitoring Devices | ||

| Surgical Devices | Cataract Surgical Devices | |

| Vitreoretinal Surgical Devices | ||

| Refreactive Surgical Devices | ||

| Glaucoma Surgical Devices | ||

| Other Surgical Devices | ||

| Vision Care Devices | Spectacles Frames & Lenses | |

| Contact Lenses | ||

| By Disease Indication | Cataract | |

| Glaucoma | ||

| Diabetic Retinopathy | ||

| Other Disease Indications | ||

| By End-user | Hospitals | |

| Specialty Ophthalmic Clinics | ||

| Ambulatory Surgery Centers (ASCs) | ||

| Other End-users | ||

Key Questions Answered in the Report

What is the current India ophthalmology devices market size?

The market is valued at USD 1.69 billion for 2026.

How fast is the India ophthalmology devices industry expected to grow?

A CAGR of 6.02% is forecast for 2026-2031, taking the market to USD 2.26 billion by 2031.

Which device category holds the largest India ophthalmology devices market share?

Vision Care Devices lead with 63.12% share in 2025, driven by strong demand for spectacles and contact lenses.

Why are Diagnostic and Monitoring Devices growing rapidly?

AI integration and portable designs enable earlier disease detection, supporting a projected 8.87% CAGR through 2031.

What regional markets show the highest growth potential?

Northern, Central, and Northeastern states demonstrate high upside due to expanding health infrastructure and tele-ophthalmology programmes.

How are indigenous manufacturers affecting competition?

Local start-ups offer cost-effective, AI-enabled equipment that forces multinational brands to recalibrate pricing and after-sales strategies, reshaping competitive dynamics.

Page last updated on: