Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

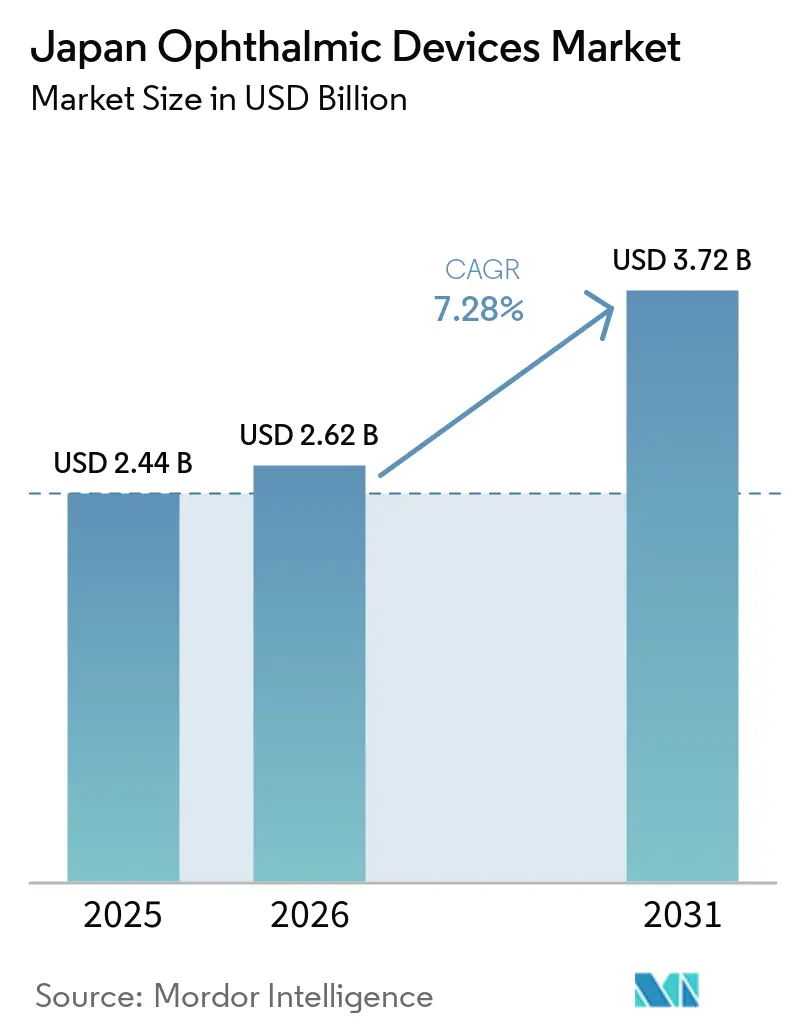

| Base Year Market Size (2025) | USD 2.44 Billion |

| Market Size (2026) | USD 2.62 Billion |

| Market Size (2031) | USD 3.72 Billion |

| Growth Rate (2026 - 2031) | 7.28% CAGR |

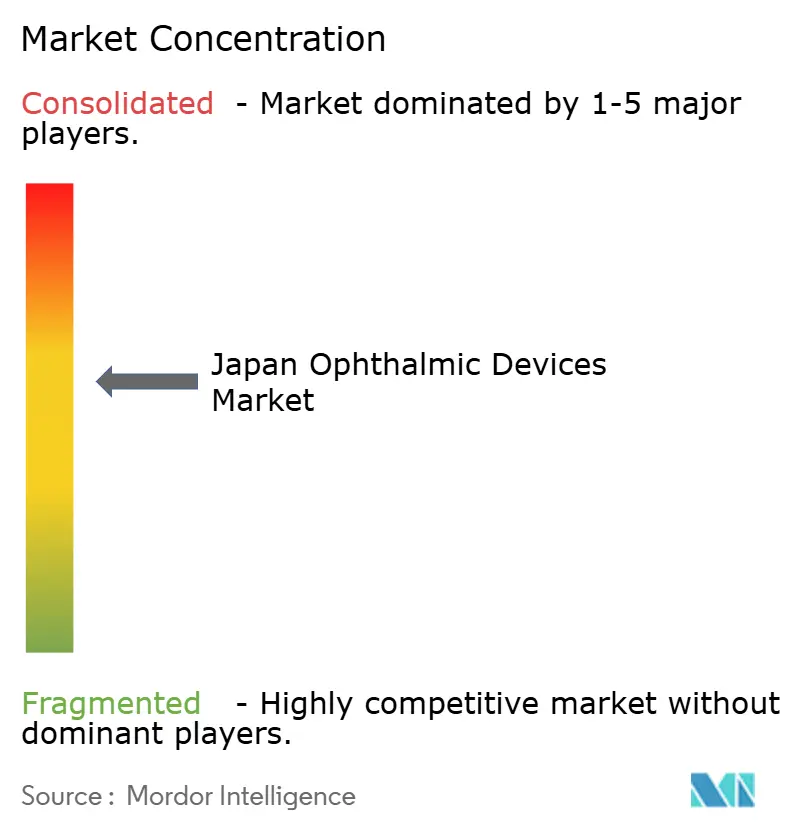

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan Ophthalmic Devices Market Analysis by Mordor Intelligence

The Japan ophthalmic devices market size is expected to grow from USD 2.44 billion in 2025 to USD 2.62 billion in 2026 and is forecast to reach USD 3.72 billion by 2031 at 7.28% CAGR over 2026-2031. A super-aged population, fast-advancing imaging technologies, and reforms that reward outpatient care are reinforcing demand. Vision care products continue to dominate unit volumes, but diagnostic platforms anchored in optical coherence tomography (OCT) are expanding the addressable base of high-value capital equipment. Surgical volumes are migrating to ambulatory settings as fee parity closes the cost gap with hospitals, prompting rapid adoption of compact workstations and single-use disposables. At the same time, rigorous PMDA approval rules and new human-factors mandates are lengthening launch timelines, pushing firms to strengthen local clinical collaborations to maintain speed. The widening urban-rural ophthalmologist divide further amplifies interest in AI-assisted screening tools that can relieve physician workload and extend reach into underserved prefectures.

Key Report Takeaways

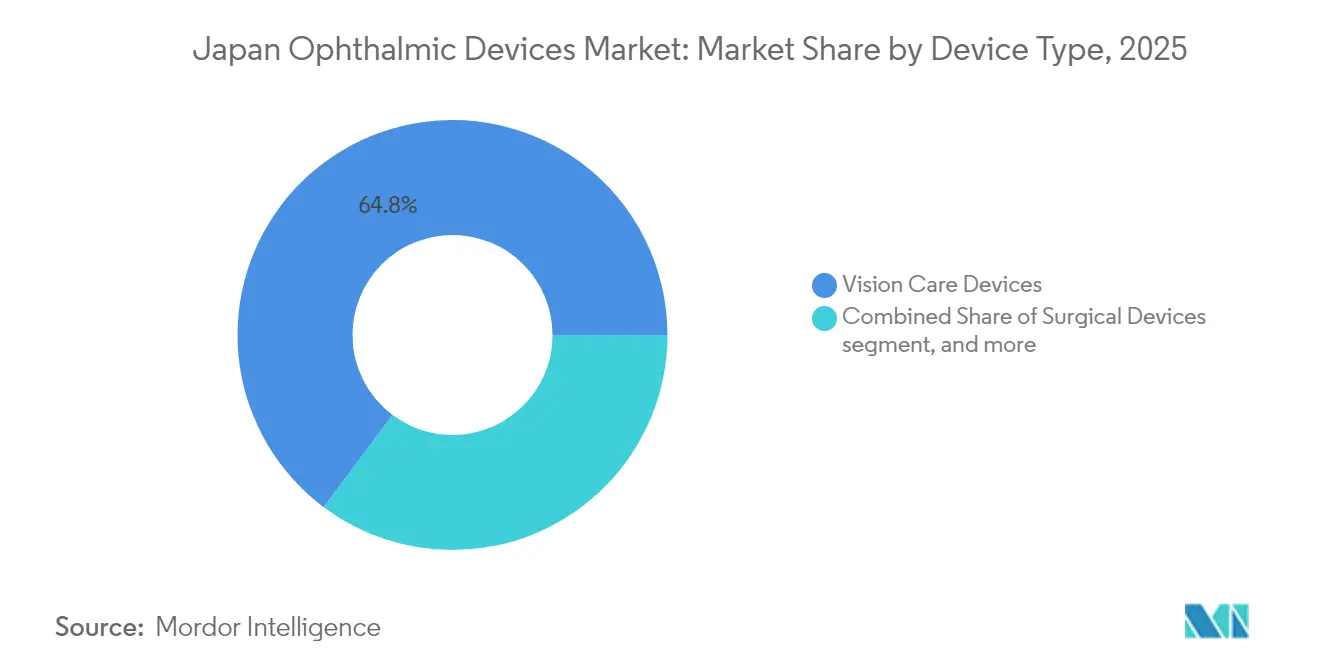

- By device type, vision care products led with 64.78% of Japan ophthalmic devices market share in 2025, while diagnostic and monitoring platforms are projected to expand at a 9.58% CAGR through 2031.

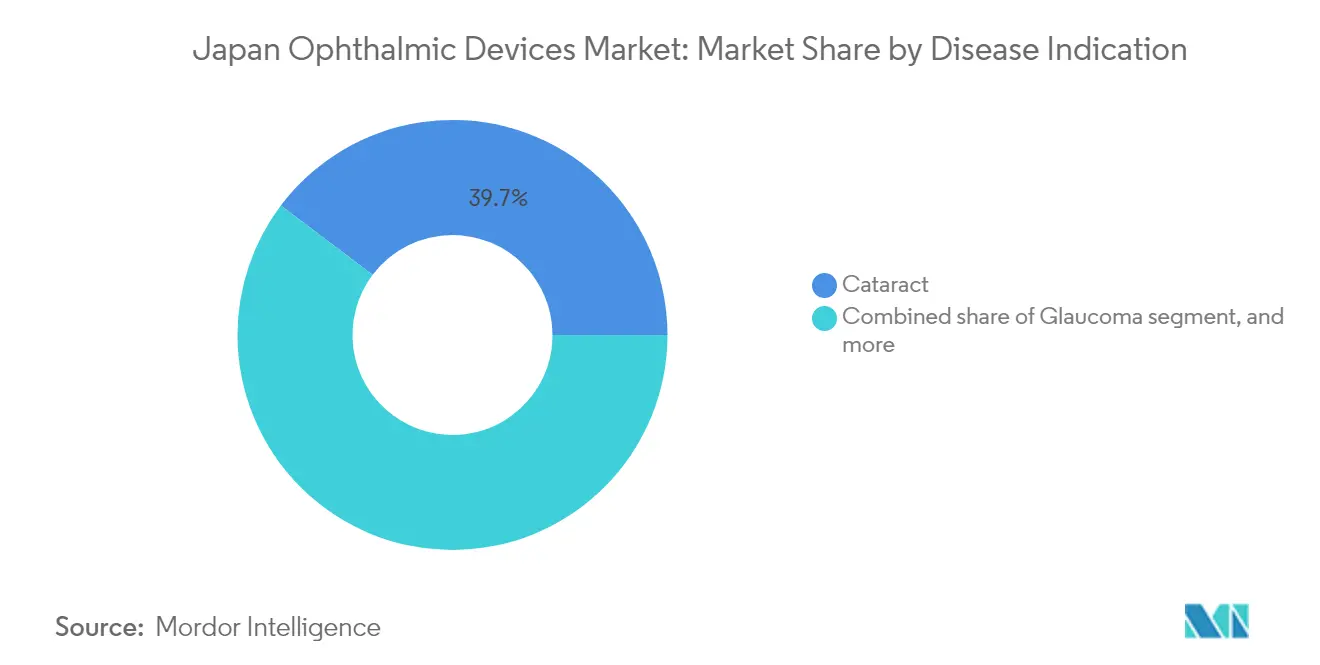

- By disease indication, cataract accounted for 39.72% share of the Japan ophthalmic devices market size in 2025; diabetic retinopathy devices are anticipated to grow at a 8.84% CAGR to 2031.

- By end-user, hospitals commanded 45.10% revenue in 2025 whereas ambulatory surgery centers are forecast to grow at 8.72% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Japan Ophthalmic Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapidly ageing population driving cataract surgery volumes | +2.0% | Nationwide, especially major metro areas | Long term (≥ 4 years) |

| Rising juvenile myopia & early-diagnosis demand | +1.3% | Urban school districts | Long term (≥ 4 years) |

| Reimbursement reforms encouraging out-of-hospital procedures | +1.0% | Tier-2 and Tier-3 cities | Medium term (2-4 years) |

| Adoption of AI-enabled imaging & screening platforms | +0.9% | National referral networks | Medium term (2-4 years) |

| Expansion of ambulatory surgery centers in Tier-2 cities | +0.7% | Regional growth corridors | Medium term (2-4 years) |

| Penetration of premium toric & multifocal IOLs | +0.6% | High-income urban clusters | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapidly-Ageing Population Driving Cataract Surgery Volumes

An unprecedented demographic shift places nearly 30% of Japan’s citizens above 65, triggering consistent cataract surgery demand that reached 1.6 million procedures in 2019 and continues to climb in 2025. Hospital audits show a growing share of patients over 90 benefiting from modern phacoemulsification combined with premium intraocular lenses, with documented cognitive score gains from 25.65 to 27.08 on the MMSE after surgery[1]Shoji Kinoshita, “Cataract Surgery Outcomes in Centenarians,” Medicine, medicinejournal.com. This broader health impact positions cataract care as more than a vision solution and amplifies purchaser willingness to pay for femtosecond laser platforms, toric lens calculators, and digitally assisted microscopes. Manufacturers bundle ergonomic handpieces and workflow software to sustain throughput amid a tightening surgical workforce. Over the long run, this driver is expected to lift the Japan ophthalmic devices market by 2.0 percentage points of cumulative CAGR.

Rising Prevalence of Juvenile Myopia & Demand for Early Diagnosis

Japanese myopia rates among children aged 6-14 rose from 10% in the late 1970s to 53% by 2010 and remain above 36% in 2025, with COVID-19-related indoor lifestyles worsening the trend. The scale of the issue prompted Santen to launch RYJUSEA Mini (atropine 0.025%) in April 2025, the first locally approved therapy to slow myopia progression. Uptake of axial-length measurement devices, auto-refractors with cycloplegic modes, and school-based screening kiosks is accelerating. Vision-care market leaders promote spectacle lenses such as MiYOSMART and daily disposable contact lenses through omnichannel campaigns targeting concerned parents. These developments collectively could add 1.3 percentage points to the sector’s growth trajectory through 2030.

Government Reimbursement Reforms Encouraging Out-of-Hospital Procedures

Fee-schedule parity between hospitals and office-based suites now encourages vitreoretinal, glaucoma, and cataract procedures to shift into ambulatory surgery centers, especially across tier-2 cities where land and construction costs are lower. A 97.3% single-surgery success rate for retinal detachment in office settings demonstrates quality parity with inpatient facilities. Device makers respond with portable phaco machines, compact vitrectomy consoles, and disposable trocar kits that reduce sterilization needs. The forthcoming conditional approval pathway under the revised PMD Act is expected to shorten SaMD review times, enhancing innovation flow to ASCs. Analysts attribute roughly a 1.0 percentage-point uplift to the Japan ophthalmic devices market CAGR from this policy environment.

Adoption of AI-Enabled Imaging & Screening Platforms

Machine-learning algorithms integrated into tabletop or handheld fundus cameras deliver reliable diabetic-retinopathy triage—achieving an incremental cost-effectiveness ratio of JPY 1.6 million per QALY, far beneath Japan’s willingness-to-pay threshold[2]Etsuko Nishida et al., “AI Cost-Effectiveness in Diabetic Retinopathy,” ScienceDirect, sciencedirect.com. Hospitals already employing AI-powered checklists report a threefold improvement in near-miss detection during cataract surgery. Despite limited open imaging datasets, vendors train models with federated-learning approaches inside domestic university networks to comply with privacy laws. Wider deployment in primary-care settings is expected once the PMDA’s priority review lane for SaMD becomes fully operational in 2026, adding an estimated 0.9 percentage points to forecast CAGR.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital cost of advanced surgical workstations | -1.8% | Smaller Tier-3 cities & rural clinics | Medium term (2-4 years) |

| Stringent PMDA approval & post-market surveillance requirements | -1.5% | All foreign and domestic entrants | Long term (≥ 4 years) |

| Shrinking ophthalmologist workforce in rural prefectures | -1.2% | Rural and remote prefectures | Long term (≥ 4 years) |

| National fee-schedule cuts exerting price pressure | -1.0% | Nationwide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capital Cost of Advanced Surgical Workstations

Femtosecond laser units, multimodal microscopes, and robotic cataract platforms require upfront payments topping USD 350,000, locking out clinics that handle fewer than 18 cases per week[3]Japan International Eye Hospital, “Economic Evaluation of Femtolaser Adoption,” jieh.jp. While leading chains in Tokyo and Osaka easily secure financing, smaller providers face thin margins because reimbursement rates have not risen in line with device precision upgrades. Leasing and pay-per-procedure contracts now appear in tender documents, yet interest rates above 2% add further strain. As a result, the addressable pool of purchasers narrows, trimming 1.8 percentage points from the five-year growth outlook of the Japan ophthalmic devices market.

Stringent PMDA Approval & Post-Market Surveillance Requirements

Class III and IV device filings require Japanese-language dossiers, local clinical files, and adherence to the JIS T 62366-1:2022 usability standard, stretching review timelines to as long as 16 months. Foreign entrants must also appoint a domestic design-ated marketing authorization holder and conduct periodic post-market performance studies. Although the agency opened an English-language guidance portal in March 2025 to clarify expectations, compliance costs still shave 1.5 percentage points from overall CAGR potential, tempering the optimism surrounding fast-growing subsegments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Vision Care Dominates While Diagnostics Accelerate

Vision-care platforms accounted for 64.78% of 2025 revenue, reflecting the nation’s long-standing reliance on corrective eyewear. HOYA’s channel audits show contact-lens penetration expanding at 2% per year, with bifocal and myopia-control options fueling basket size gains. Diagnostic and monitoring equipment is the fastest riser, set to log a 9.58% CAGR through 2031 as self-imaging OCT, swept-source devices, and AI-ready fundus scanners move from tertiary centers into primary clinics. Adoption of Canon’s OCT-R1, which earned a Red Dot award for its compact footprint, exemplifies this pivot toward earlier detection. Across both tiers, value-added software subscriptions help offset fee-schedule pressure by bundling analytics dashboards and remote consultation features into hardware sales. These multi-modal strategies underpin sustained leadership for platform vendors while widening access to proactive eye-health management.

Growth momentum in surgical devices remains steady, underpinned by minimally invasive glaucoma stents, single-use vitrectomy cutters, and compact phaco consoles designed for ASC workflows. Femtosecond laser cataract systems deliver added precision, yet their high capital requirement restricts uptake to high-volume metropolitan centers. To narrow this affordability gap, manufacturers trial pay-per-click models that align unit economics with procedure counts in tier-2 clinics. As a result, the Japan ophthalmic devices market size attributed to surgical technology is expected to expand but at a more measured pace than diagnostics.

By Disease Indication: Cataract Leads While Diabetic Retinopathy Accelerates

Cataract surgery devices generated 39.72% of sales in 2025 as surgical demand surged among patients over 80. Outcomes remain favorable, even for centenarians, which reinforces patient and insurer confidence in advanced intraocular lenses. Surgeons blending manual small-incision cataract surgery with toric lens alignment software report lower residual refractive error, encouraging further investment in precision guidance modules. Meanwhile, the public discourse links cataract interventions with reductions in fall risk and cognitive decline, helping justify funding for high-performance consumables despite fee-schedule cuts.

Diabetic-retinopathy management tools represent the fastest-growing niche with a projected 8.84% CAGR. Government data show diabetes prevalence at 12% among adults, creating large screening backlogs in primary care. AI-triage systems packaged with non-mydriatic cameras compress evaluation times, while early vitrectomy protocols improve visual acuity in patients with macular edema. Post-operative intravitreal bevacizumab reduces neovascular glaucoma by 80% in high-risk eyes, encouraging retina specialists to package anti-VEGF injectables with micro-incision surgery kits. This integrated care model anchors robust demand for diagnostic and therapeutic consumables in endocrinology clinics that now embed ophthalmology pods.

By End-User: Hospitals Lead While ASCs Gain Momentum

Tertiary hospitals maintained 45.10% revenue share in 2025, buoyed by their role in treating complex retina and neuro-ophthalmology cases. University networks employ upward of 1,500 academic ophthalmologists who champion early access to investigational platforms under clinical-trial exemptions. Despite this dominance, capacity constraints and physician-hour caps are prompting redistributions of routine cataract and glaucoma surgeries to satellite ASCs. These centers, often located within 15 km of rail stations in tier-2 cities, record patient stays under four hours while adhering to operating-room air-quality standards.

Ambulatory surgery centers will post a 8.72% CAGR through 2031 on the back of fee-parity policies, streamlined PMD Act approvals for office-based suites, and an aging cohort seeking same-day discharge. Equipment makers respond with mobile phaco units, pre-packed vitreoretinal procedure kits, and AI-guided sterile-field monitors tailored to tight footprints. Specialty clinics, though smaller, remain essential for chronic disease follow-up. They increasingly leverage teleophthalmology to monitor intraocular pressure remotely, aligning with national goals to curb urban-rural service gaps.

Geography Analysis

Competitive Landscape

The Japan ophthalmic devices market features a moderately consolidated structure with entrenched multinationals competing alongside technology-focused domestic specialists. Alcon maintains leadership in intraocular lenses and phaco systems through continuous firmware updates that integrate astigmatism-alignment aids. Johnson & Johnson Vision extends reach via myopia-control contact lenses launched in joint promotions with pediatric clinics. HOYA’s 50% share in specialty contact-lens retailers anchors its dominance in vision care; the firm augments this position with MiYOSMART spectacle lenses that slow axial-length progression.

Nidek leverages decades-long relationships with local distributors to stay top-of-mind among ophthalmologists for refractive diagnostics and surgical lasers. Canon’s imaging division gains momentum after the OCT-R1’s Red Dot accolade, positioning the device as a premium yet space-efficient option for multisite chains. Strategic alliances accelerate innovation: Kubota Vision collaborates with IQVIA Services Japan and AUROLAB to scale its pocket-sized OCT, targeting monitoring of diabetic macular edema in handheld formats. BVI Medical focuses on glaucoma solutions, eyeing SaMD-enabled workflow analytics to differentiate its Leos system when widely commercialized in 2025.

White-space opportunities persist in rural prefectures plagued by workforce shortages. Companies bundling AI algorithms with cloud-based interpretation services stand to capture these under-served pockets. Meanwhile, manufacturers navigate downward price pressure from biennial fee-schedule revisions by expanding aftermarket service contracts and offering predictive-maintenance subscriptions that reduce downtime. Moderately concentrated competition and differentiated localization strategies together shape sustainable, innovation-driven growth prospects through the decade.

Japan Ophthalmic Devices Industry Leaders

Alcon Inc.

Johnson & Johnson Vision Care

HOYA Corporation

Nidek Co. Ltd

Topcon Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: PMDA launched an English-language portal to guide overseas firms through device approval steps.

- December 2024: PMDA issued new labeling rules to prevent medication errors, including specific packaging for eye-drop-like formulations .

- October 2024: MHLW proposed PMD Act amendments introducing a conditional approval pathway for high-needs devices.

- August 2024: Compliance with JIS T 62366-1:2022 usability standard became mandatory for all new device submissions.

- April 2024: BVI Medical gained PMDA clearance for its PODEYE hydrophobic monofocal IOL.

Japan Ophthalmic Devices Market Report Scope

As per the scope of the report, ophthalmology devices are the equipment that is used for the diagnosis and treatment of various ophthalmic diseases, such as cataracts, glaucoma, and refractive errors. Ophthalmic drugs are used to treat eye infections and some of the above-mentioned diseases. The drugs covered in the report are glaucoma drugs, retinal disorder drugs, dry eye disease drugs, drugs for infections, and other drugs. The Japan Ophthalmic Devices & Drugs Market is Segmented By Product (Devices (Surgical Devices (Intraocular Lenses, Ophthalmic Lasers, and Other Surgical Devices), and Diagnostic Devices), and Drugs (Glaucoma Drugs, Retinal Disorder Drugs, Dry Eye Drugs, Allergic Conjunctivitis and Inflammation Drugs, and Other Drugs), and Disease (Glaucoma, Cataract, Age-Related Macular Degeneration, Inflammatory Diseases, Refractive Disorders, and Other Diseases). The report offers the value (in USD million) for the above segments.

By Device Type

| Diagnostic & Monitoring Devices | OCT Scanners |

| Fundus & Retinal Cameras | |

| Autorefractors & Keratometers | |

| Corneal Topography Systems | |

| Ultrasound Imaging Systems | |

| Perimeters & Tonometers | |

| Other Diagnostic & Monitoring Devices | |

| Surgical Devices | Cataract Surgical Devices |

| Vitreoretinal Surgical Devices | |

| Refreactive Surgical Devices | |

| Glaucoma Surgical Devices | |

| Other Surgical Devices | |

| Vision Care Devices | Spectacles Frames & Lenses |

| Contact Lenses |

By Disease Indication

| Cataract |

| Glaucoma |

| Diabetic Retinopathy |

| Other Disease Indications |

By End-user

| Hospitals |

| Specialty Ophthalmic Clinics |

| Ambulatory Surgery Centers (ASCs) |

| Other End-users |

| By Device Type | Diagnostic & Monitoring Devices | OCT Scanners |

| Fundus & Retinal Cameras | ||

| Autorefractors & Keratometers | ||

| Corneal Topography Systems | ||

| Ultrasound Imaging Systems | ||

| Perimeters & Tonometers | ||

| Other Diagnostic & Monitoring Devices | ||

| Surgical Devices | Cataract Surgical Devices | |

| Vitreoretinal Surgical Devices | ||

| Refreactive Surgical Devices | ||

| Glaucoma Surgical Devices | ||

| Other Surgical Devices | ||

| Vision Care Devices | Spectacles Frames & Lenses | |

| Contact Lenses | ||

| By Disease Indication | Cataract | |

| Glaucoma | ||

| Diabetic Retinopathy | ||

| Other Disease Indications | ||

| By End-user | Hospitals | |

| Specialty Ophthalmic Clinics | ||

| Ambulatory Surgery Centers (ASCs) | ||

| Other End-users | ||

Key Questions Answered in the Report

What is the current size and growth outlook of the Japan ophthalmic devices market?

The market is valued at USD 2.62 billion in 2026 and is projected to reach USD 3.72 billion by 2031, reflecting a 7.28% CAGR over the forecast period.

Which device category holds the largest share today?

Vision care products—including eyeglass and contact-lens solutions—command 64.78% of total 2025 revenue, driven by high myopia prevalence and rising demand for premium corrective lenses.

What are the main factors propelling market expansion?

A super-aged population fueling cataract surgeries, fast adoption of AI-enabled diagnostics, and fee-schedule reforms that encourage outpatient procedures are the foremost growth engines.

How do reimbursement policies influence purchasing trends?

Fee parity between hospitals and ambulatory surgery centers (ASCs) is shifting routine cataract, glaucoma, and vitreoretinal cases into office-based suites, spurring demand for compact surgical consoles and single-use kits.

What hurdles must new entrants overcome?

Stringent PMDA approval processes—requiring Japanese-language dossiers, local clinical data, and compliance with the JIS T 62366-1:2022 usability standard—extend time-to-market and elevate compliance costs.

Which end-user segment is growing the fastest?

Ambulatory surgery centers lead in growth with a forecast 8.72% CAGR to 2031, benefiting from streamlined regulatory pathways and patient preference for same-day discharge.

Page last updated on: