China Mining Logistics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

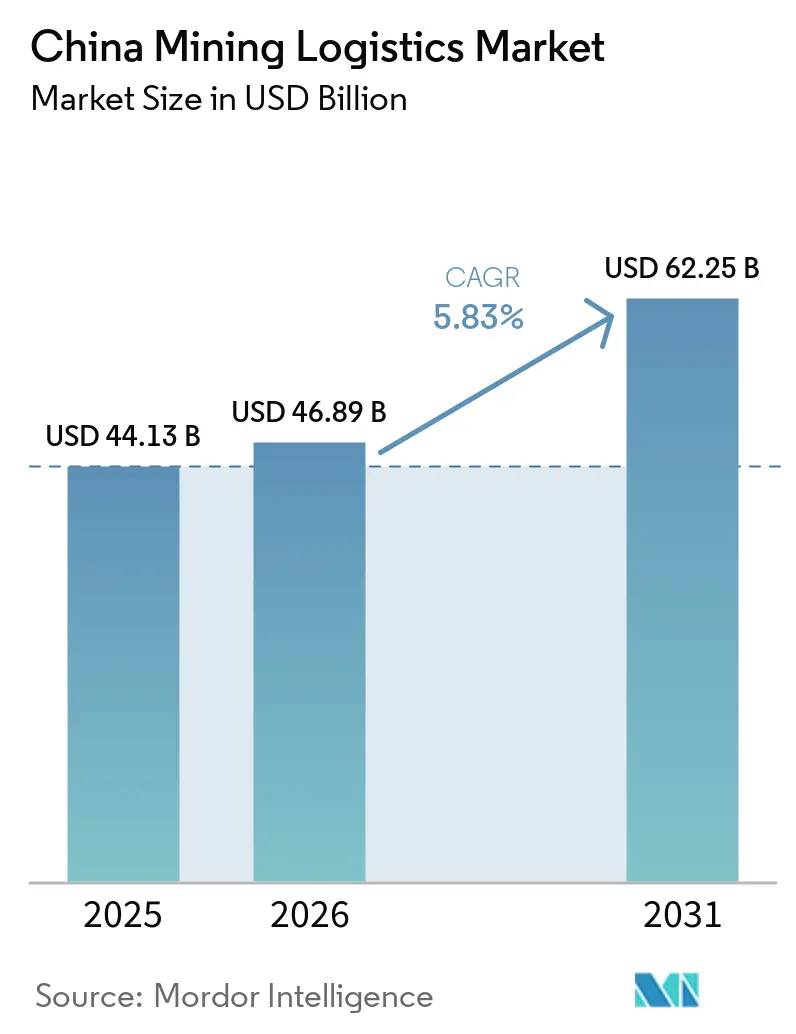

| Base Year Market Size (2025) | USD 44.13 Billion |

| Market Size (2026) | USD 46.89 Billion |

| Market Size (2031) | USD 62.25 Billion |

| Growth Rate (2026 - 2031) | 5.83% CAGR |

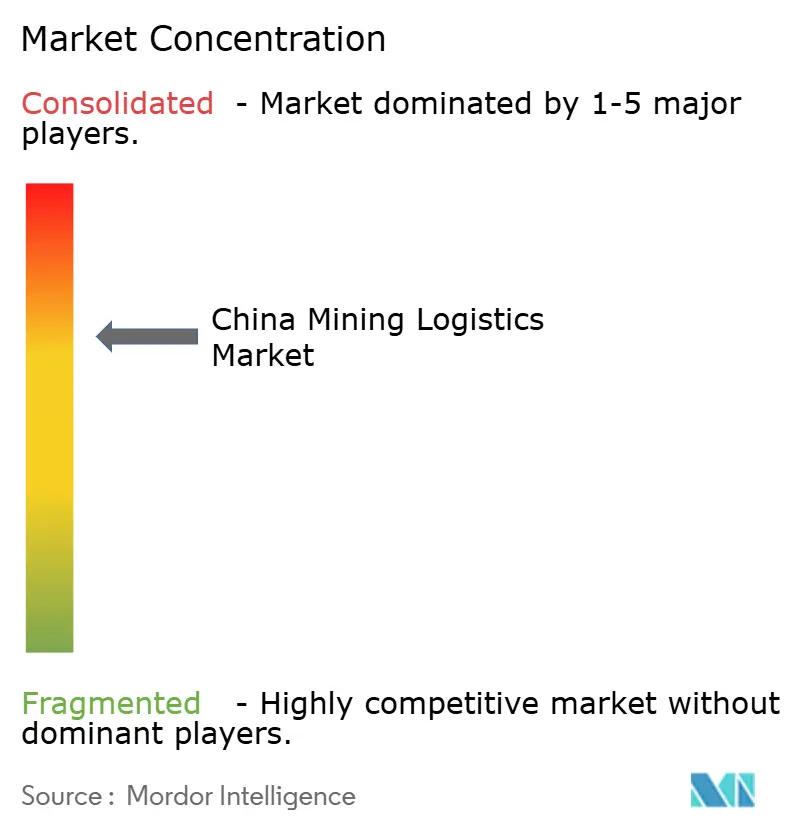

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Mining Logistics Market Analysis by Mordor Intelligence

The China mining logistics market size was estimated at USD 44.13 billion in 2025 and is expected to increase from USD 46.89 billion in 2026 to USD 62.85 billion by 2031, growing at a CAGR of 5.83% from 2026 to 2031.

The China mining logistics market is supported by steady-state investment in heavy-haul rail, bulk port capacity, and mine automation, which together reduce cycle times and improve transport efficiency for coal, iron ore, and base metals. The current expansion of the China mining logistics market depends less on pure output growth and more on tighter integration between mine sites, rail corridors, ports, and downstream processing clusters, which supports revenue durability even when commodity pricing is less favorable. China’s 2025 refining dominance across critical minerals keeps inbound ore and concentrate flows concentrated around a limited number of smelters and processing hubs, and that concentration keeps logistics corridors strategically important for public investment planning. The China mining logistics market also benefits from policy support aimed at lowering national logistics costs through modal shift, hub consolidation, and standardized multimodal billing, which is already changing how shippers contract for bulk cargo movement. At the same time, the China mining logistics market still faces pressure from steel-cycle volatility, environmental compliance spending, and weak first-mile connectivity in inland mining belts, which means the strongest opportunities remain with operators that control integrated rail, port, warehousing, and value-added service networks[1]“With New Export Controls on Critical Minerals, Supply Concentration Risks Become Reality,” International Energy Agency, iea.org.

Key Report Takeaways

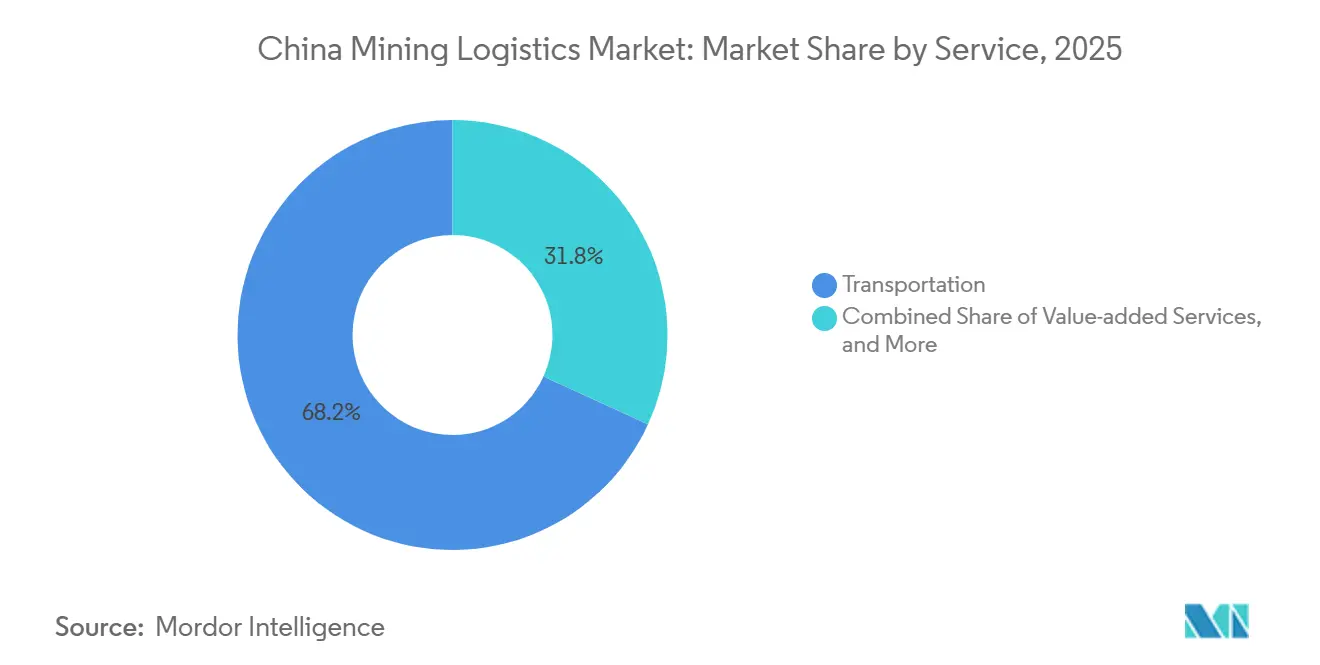

- By service, transportation held 68.18% of the China mining logistics market share in 2025, while value-added services are forecast to expand at a 6.49% CAGR through 2031.

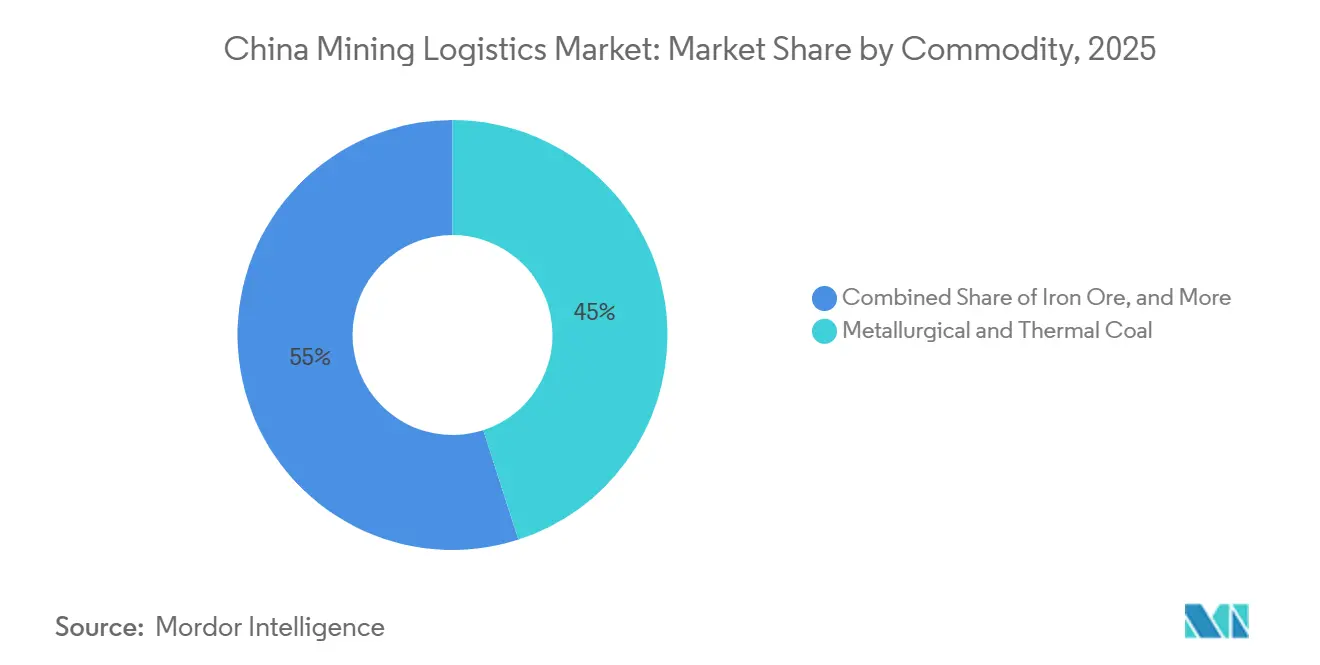

- By commodity, metallurgical and thermal coal held 45.03% share of the China mining logistics market size in 2025, while base metals are projected to grow at a 6.3% CAGR through 2031.

- By geography, North China held 35.58% of the China mining logistics market share in 2025, while Northwest China is expected to record the highest CAGR of 6.74% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

China Mining Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rail-water corridor expansion for coal and ore | +1.4% | North China, Southwest China, Northwest China | Medium term (2-4 years) |

| Strategic mineral and energy security investment | +1.2% | Global with domestic concentration in Northwest and Northeast China | Long term (≥ 4 years) |

| Deepwater ore-terminal capacity expansion | +0.9% | North China, Bohai Rim, East China | Medium term (2-4 years) |

| Lower logistics cost and modal-shift policy push | +0.8% | Global, priority urban freight hubs in East and Central China | Short term (≤ 2 years) |

| Port-side ore blending and processing | +0.5% | East China, Rizhao, Ningbo, North China | Medium term (2-4 years) |

| Autonomous haulage and smart dispatch deployment | +0.7% | Northwest China, North China open-pit coal and ore belts | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rail-Water Corridor Expansion for Coal and Ore

The China mining logistics market is being reshaped by rail-water corridor development that is redirecting bulk flows across coal and ore routes. China’s railways carried 1.6 billion tons of freight in the first 5 months of 2025, up 3.1% year on year, while rail-water intermodal container volumes rose 18.4% as standardized multimodal products gained traction. That operating shift matters because it strengthens the economics of integrated movement instead of isolated port or rail transactions. Corridor expansion in Southwest China is also widening access between inland production centers and export gateways, thereby improving the commercial case for mining output from interior provinces. As more cargo moves under single-contract logistics structures, the China mining logistics market should continue to reward operators that can combine inland pickup, mainline rail, port handling, and downstream delivery into one service chain.

Strategic Mineral and Energy Security Investment

The China mining logistics market is also supported by state-backed investment tied to energy security and critical mineral processing. The Shuohuang Railway has passed 5 billion cumulative tons of coal moved by April 2025, which shows the scale of dedicated infrastructure already supporting west-to-east energy flows. China’s refining position remains central to this logic, with the IEA stating in 2025 that China held an average 70% refining share across 19 of 20 strategically important minerals IEA. That level of concentration keeps inbound logistics corridors to smelter and processing clusters strategically important even when short-term commodity markets soften. In the China mining logistics market, this creates a durable floor for corridor investment because logistics infrastructure is serving national supply security as much as commercial freight demand.

Deepwater Ore-Terminal Capacity Expansion

Deepwater berth expansion is lowering structural cost across imported ore logistics in the China mining logistics market. Beibu Gulf Port is investing USD 2.24 billion in two 300,000-ton ore berths and 6 transshipment berths at Fangchenggang, with a designed annual throughput capacity of 67.5 million tons. At Caofeidian, the next expansion phase extends the quay to 910 meters and supports simultaneous berthing for two 400,000-ton vessels after the deep-water route entered the national coastal public navigation framework in 2026. Qingdao’s second 400,000-ton ore terminal entered service in October 2025 and lifted capacity at Dongjiakou’s ore cluster materially. For the China mining logistics market, wider use of ultra-large ore carriers improves per-ton freight economics and strengthens the advantage of ports that can process very large bulk arrivals with limited dwell time.

Lower Logistics Cost and Modal-Shift Policy Push

The China mining logistics market is benefiting from direct policy pressure to reduce national logistics costs and move more bulk cargo off roads. The State Council’s target for China’s logistics cost-to-GDP ratio is 13.5% by 2027, down from 14.4% in 2023, through multimodal restructuring and stronger hub systems. In April 2026, 5 government departments issued guidance to focus freight hub investment across 30 cities over 3 years, with rail as the backbone and rail-water projects receiving subsidy support of 40% to 60%, depending on the region. The share of coal moved by rail had already risen under national coal logistics planning, confirming that this shift was underway before the latest funding round. In the China mining logistics market, that policy direction favors integrated operators that can provide rail access, multimodal billing, and lower first-leg road dependence, while smaller mine-gate trucking firms face sustained displacement pressure.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Environmental compliance capex for bulk nodes | -0.6% | Global, priority in Bohai Rim and Pearl River Delta ports | Short term (≤ 2 years) |

| Steel-cycle and ore-price volatility | -0.7% | Global, with amplified effect in North and East China steel corridors | Short term (≤ 2 years) |

| First-mile mine-to-mainline bottlenecks | -0.5% | Northwest China, North China, Shanxi, Inner Mongolia | Medium term (2-4 years) |

| Coastal hub disruption sensitivity | -0.3% | East China, South China coastal clusters | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Environmental Compliance Capex for Bulk Nodes

Environmental compliance is raising capital intensity for the China mining logistics market, especially at bulk terminals and inland handling nodes. Operators are being pushed toward dust suppression systems, sealed conveyors, wastewater controls, and higher use of electrified equipment at ports and transfer stations. CHN Energy’s Huanghua Port Phase V project was presented in 2025 as a near-zero carbon terminal with 16 categories of green technology, showing the scale of investment now needed in new-generation bulk infrastructure. Large state-backed operators can more easily absorb these costs because port development is tied to broader public and energy priorities. In the China mining logistics market, smaller private bulk operators remain more exposed because compliance spending directly competes with working capital during weaker throughput periods[2]“Logistics Costs and Multimodal Transport, International Comparisons,” Ministry of Ports, Shipping and Waterways and DPIIT, Government of India, digifootprint.gov.in.

Steel-Cycle and Ore-Price Volatility

Steel-cycle weakness remains one of the clearest demand-side limits on the China mining logistics market. China’s crude steel output fell to a 7-year low of 960.8 million tons in 2025, and output in the first 2 months of 2026 dropped another 3.6% year on year to 160.3 million tons. The OECD Steel Committee said in 2025 that global steel excess capacity reached 640 million metric tons, while China’s steel exports rose to a record 131 million metric tons. China’s 2026 steel plan also calls for orderly capacity reduction and closure of outdated mills, which keeps pressure on some ore and coal routes. For the China mining logistics market, this does not remove the need for bulk movement, but it does reduce route pricing power and makes premium contract capture harder during weaker steel production cycles[3]“Qingdao Port Dongjiakou Monthly Iron Ore Import Throughput Exceeds 7 Million Tons,” Shandong Department of Transport, jtt.shandong.gov.cn.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: Value-Added Services Gaining Share In An Increasingly Integrated Supply Chain

Transportation held 68.18% of the China mining logistics market share in 2025, which reflects the sheer weight of coal, iron ore, and mineral concentrate movement across the country. Rail and sea and inland waterways remain the dominant transport sub-modes because public policy, freight corridor funding, and port investment all favor bulk movement at scale. Road transport still plays an essential first-mile role in mountain and interior mining areas where rail connectivity is incomplete. Air logistics remains a very small part of the service mix because mining cargo is usually heavy and low value per unit of weight, though refined metals and critical spare parts still use faster modes when timing matters.

The fastest growth is in value-added services, which are projected to expand at a 6.49% CAGR through 2031 as mills outsource blending, grade optimization, and moisture management to logistics operators at ports. Warehousing and inventory management remain important because steel mills and power plants need buffer stocks to smooth procurement cycles and protect operations during transport disruptions. Baowu’s 10-million-ton intelligent ore blending center at Rizhao Port shows how the China mining logistics industry is shifting from pure cargo movement toward service layers that improve furnace input quality and lower on-site handling needs. As that model spreads, the China mining logistics market should see a larger share of revenue come from customized processing contracts rather than only transport and handling fees[4]“CHN Energy Successfully Clears Customs Clearance for Inaugural Mongolian Coal Shipment,” SASAC, sasac.gov.cn.

By Commodity: Coal Dominates Volume, Base Metals Drive Future Growth

Metallurgical and thermal coal accounted for 45.03% share of the China mining logistics market size in 2025, driven by China’s continued dependence on coal across power generation and steelmaking. Coal logistics is the most mature commodity chain in the China mining logistics market because it already relies on dedicated heavy-haul railways, specialized coastal carriers, enclosed terminals, and established north-to-south coastal dispatch patterns. Thermal coal mainly moves from northern mining regions to southern power markets, while metallurgical coal serves inland steelmaking centers through a mix of domestic rail and seaborne imports. Cross-border flows are also widening, as CHN Energy cleared its first commercial shipment of Mongolian coal in July 2025 through a new rail logistics channel.

Base metals are the fastest-growing commodity group at a 6.3% CAGR through 2031, supported by demand from electric vehicles, battery manufacturing, and renewable energy systems. Iron ore remains the second-largest commodity segment because China still depends heavily on imported high-grade ore for steel production. Seaborne iron ore imports reached 210 million tons in the first 2 months of 2026, up 10% year on year, even while steel output weakened, which points to continued stock building at ports. The Springer analysis on China’s metal-sector foreign investment showed that overseas mining projects are increasingly paired with logistics corridor control, which links future copper, nickel, and lithium supply more tightly to Chinese processing hubs. Gold remains small in tonnage but high in value intensity, while other minerals such as bauxite, phosphate, and lithium form a growing tail that benefits from the same supply security programs shaping the broader China mining logistics industry.

Geography Analysis

North China accounted for 35.58% of the China mining logistics market share in 2025, and that lead rests on the concentration of bulk assets around the Bohai Rim. The deep-water route to Caofeidian is now part of China’s national coastal public navigation system, which allows routine full-load berthing for 400,000-ton ore carriers and lowers per-vessel logistics costs for mills in the Beijing-Tianjin-Hebei cluster. Qingdao Dongjiakou’s second 400,000-ton ore terminal became operational in October 2025, and monthly iron ore throughput exceeded 7 million tons in its first full month of operation. Tianjin and Hebei ports complement Qingdao by serving different parts of the steel and chemical supply chain. This gives North China a stronger degree of redundancy than most other regions in the China mining logistics market.

Northwest China is the fastest-growing regional block, with the China mining logistics market size there set to expand at a 6.74% CAGR through 2031 as coal and critical mineral output rise. EACON’s 120 battery-electric autonomous trucks at the Zhundong open-pit coal mine show how producers are improving mine-site movement even while external rail links remain constrained. The April 2026 freight hub guidance gives western projects the highest subsidy ratios, which confirms that policy makers see Northwest China as the region with the biggest infrastructure gap against production potential. Until more mine-to-rail links are completed, road collection and intermediate handling will keep weighing on cost and timing in this part of the China mining logistics market.

East China and Southwest China support growth in different ways, but both are important to the next stage of the China mining logistics market. East China remains the strongest ore import and processing zone because of its large industrial base and its port-linked value-added services. Baowu’s intelligent blending center at Rizhao shows how ports in this region are moving beyond handling fees and adding processing revenue on top of cargo throughput. Southwest China is improving through the New International Land-Sea Trade Corridor and the build-out of new transport and logistics projects around Chongqing. South China gains from Beibu Gulf’s deepwater investment and from stronger inflows of imported raw materials for southern industrial users. Central China and Northeast China remain incremental contributors, with the former tied to Yangtze intermodal stability and the latter linked to Mongolia-facing rail trade and the pace of industrial recovery.

Competitive Landscape

The China mining logistics market is moderately concentrated at the top level. A small group of large state-backed organizations controls the most valuable rail slots, port berths, and access to public projects, while many regional trucking, warehousing, and agency firms still compete for local and first-mile work. CHN Energy remains one of the strongest positions in the China mining logistics market because it combines coal mining, dedicated rail assets, and port operations into a single system. That structure gives it a cost and scheduling advantage on major energy corridors that smaller standalone operators cannot easily match. The China mining logistics market also includes diversified integrators such as Sinotrans, Xiamen Xiangyu, and COSCO Shipping Logistics, which compete through end-to-end service contracts that combine inland movement, ocean freight, customs handling, and trade support.

Several strategic moves show how competition is shifting across the China mining logistics market. In June 2025, Xiamen Xiangyu and Shunda Mining launched Shunyu Shipping to operate capesize bulk carriers on the West Africa-to-China mineral corridor, demonstrating how logistics providers are moving upstream into vessel ownership to capture a larger share of freight margins. In April 2026, Nantong Xiangyu Shipbuilding signed contracts for 3 new bulk carriers, extending fleet support for Xiangyu’s bulk commodity logistics business. COSCO SHIPPING Specialized Carriers also announced 3 deck-extendable heavy-lift vessels and a new China-Middle East-Europe multimodal route in January 2026, strengthening transport capacity for mining and energy equipment movement. These moves show that scale players are not only defending cargo volumes but also widening control over vessel, corridor, and specialized project logistics.

Technology vendors are becoming more influential at the mine and port interface within the China mining logistics market. CiDi went public in Hong Kong in December 2025 after reporting delivery of 630 autonomous mining truck solution units in 2025, which highlighted how fast the domestic automation ecosystem is expanding. EACON said it had deployed more than 2,500 autonomous trucks across more than 30 projects, and the company claimed a 51.6% revenue share in China’s autonomous mining haulage solutions segment in 2024. This shift transfers part of the competitive leverage away from labor-intensive open-pit trucking contractors and toward software and systems providers. The remaining white space in the China mining logistics market sits in rail slot management, inland river logistics modernization, and digital coordination tools that can connect multiple shippers to constrained bulk transport assets more efficiently.

China Mining Logistics Industry Leaders

China Energy Investment Corporation

Sinotrans Limited

COSCO SHIPPING Logistics & Supply Chain Management Co., Ltd.

China State Railway Group (CR)

Xiamen Xiangyu Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Nantong Xiangyu Shipbuilding (an Xiamen Xiangyu affiliate) signed construction contracts for three new bulk carriers (one 63,800 DWT and two 82,000 DWT), continuing fleet expansion to support Xiangyu's bulk commodity logistics business.

- March 2026: EACON Mining achieved a significant deployment milestone with 120 battery-electric wide-body trucks operating under its ORCASTRA autonomous haulage system at the CHN Energy-operated Zhundong Open-Pit Coal Mine in Northwest China, forming one of the world's largest BEV haulage fleets at a single site. The deployment supports continuous autonomous charging and intelligent fleet dispatching at scale.

- March 2026: CHN Energy commissioned a 2 GW solar installation at its Lingwu coal-mining subsidence area in Ningxia, completing the full 4 GW Lingwu renewable base. The project repurposes mine-impacted land for power generation and strengthens west-to-east clean energy logistics integration.

- January 2026: COSCO SHIPPING Specialized Carriers announced 3 deck-extendable heavy-lift vessels and a new China-Middle East-Europe multimodal route dedicated to wind, hydrogen, and nuclear energy equipment transport, at its Global Partners Conference in Guangzhou. The expansion targets EPC contractors and renewable energy developers and adds specialized logistics capacity relevant to mining equipment exports.

China Mining Logistics Market Report Scope

| Transportation | Road |

| Rail | |

| Sea and Inland Waterways | |

| Air | |

| Warehousing and Inventory Management | |

| Value-Added Services |

| Iron Ore |

| Metallurgical and Thermal Coal |

| Base Metals (Cu, Zn, Ni) |

| Gold |

| Other Minerals/Metals |

| North China |

| Northeast China |

| East China |

| Central China |

| South China |

| Southwest China |

| Northwest China |

| By Service | Transportation | Road |

| Rail | ||

| Sea and Inland Waterways | ||

| Air | ||

| Warehousing and Inventory Management | ||

| Value-Added Services | ||

| By Commodity | Iron Ore | |

| Metallurgical and Thermal Coal | ||

| Base Metals (Cu, Zn, Ni) | ||

| Gold | ||

| Other Minerals/Metals | ||

| By Geography | North China | |

| Northeast China | ||

| East China | ||

| Central China | ||

| South China | ||

| Southwest China | ||

| Northwest China |

Key Questions Answered in the Report

What is driving growth in China’s mining logistics space through 2031?

Growth is being supported by rail and port capacity expansion, policy-backed modal shift, and more value-added services at ports, with the sector projected to reach USD 62.25 billion by 2031 at a 5.83% CAGR.

Which service category contributes the most revenue?

Transportation remains the largest service category with 68.18% share in 2025 because bulk mining cargo still depends mainly on rail, coastal shipping, inland waterways, and supporting road links.

Which commodity group is growing the fastest?

Base metals is the fastest-growing commodity segment, with a forecast CAGR of 6.3% through 2031, supported by demand from electric vehicles, batteries, and renewable energy systems.

Why does North China remain the leading regional hub?

North China led with 35.58% share in 2025 because the Bohai Rim combines deepwater ore terminals, strong rail-port integration, and proximity to major steel and coal corridors.

What is the biggest operational risk for bulk cargo operators?

Steel-cycle weakness and concentration at a small number of coastal ore hubs remain the biggest risks because weaker steel output and port disruption can quickly affect route utilization and contract pricing.

How is automation changing mine logistics in China?

Autonomous haulage is reducing in-pit transport friction, with more than 4,000 autonomous vehicles already operating in open-pit coal mines in 2025 and further scaling in 2026.

Page last updated on: